Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

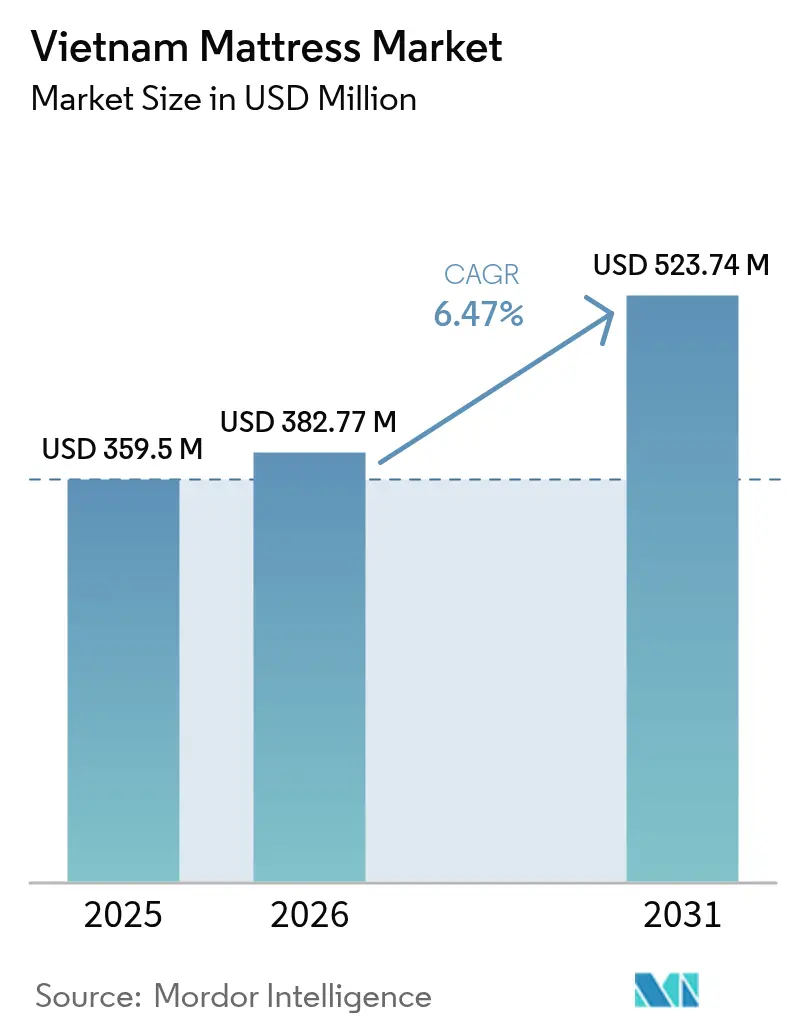

| Base Year Market Size (2025) | USD 359.5 Million |

| Market Size (2026) | USD 382.77 Million |

| Market Size (2031) | USD 523.74 Million |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Mattress Market Analysis by Mordor Intelligence

The Vietnam mattress market size is expected to grow from USD 359.5 million in 2025 to USD 382.77 million in 2026 and is forecast to reach USD 523.74 million by 2031 at 6.47% CAGR over 2026-2031. Expanding middle-class incomes, a deepening focus on sleep health, and accelerating hospitality construction together underpin the growth outlook of the Vietnam mattress market. E-commerce’s rapid infiltration of Tier-2 and Tier-3 cities widens consumer reach, while tourism-led hotel openings amplify commercial demand. Supply-chain localization and natural-latex sourcing from within ASEAN help manufacturers ease import exposure and comply with new environmental rules. Firms that combine omnichannel retail, certified sustainable materials, and flexible production are positioned to capture the next leg of expansion within the Vietnam mattress market.

Key Report Takeaways

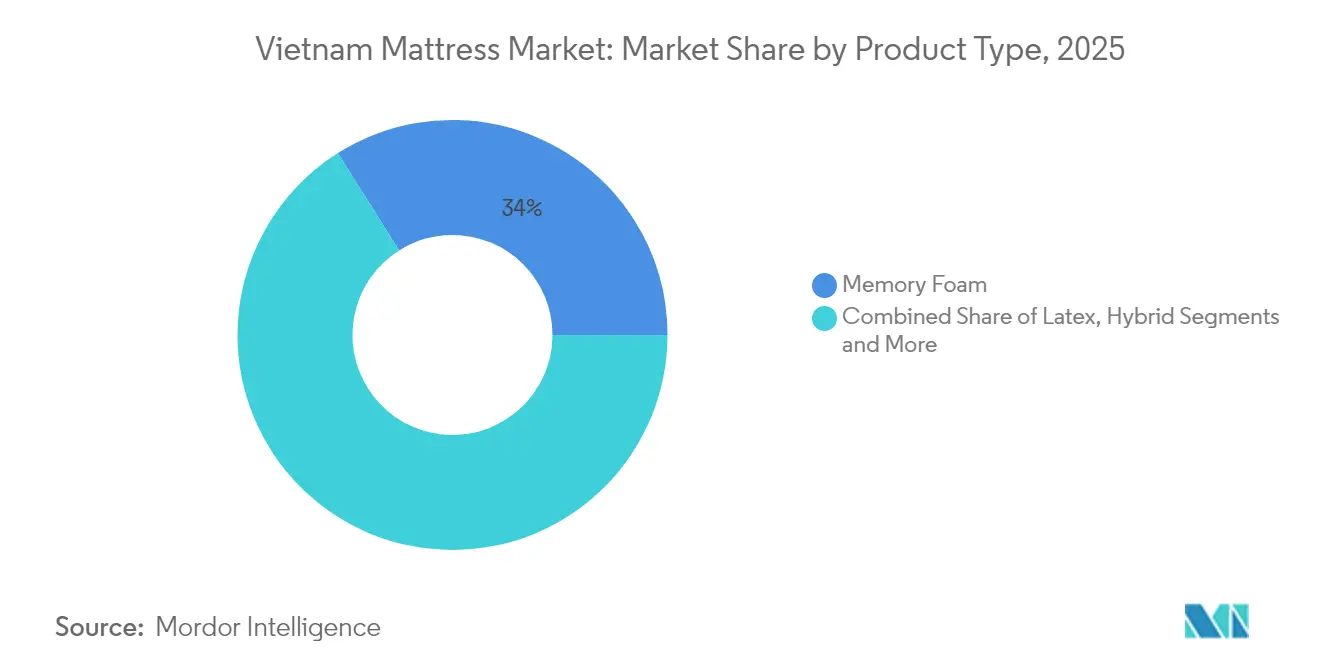

- By product type, memory foam led with 33.95% of Vietnam mattress market share in 2025; hybrid mattresses are forecast to expand at a 6.76% CAGR through 2031.

- By mattress size, queen-size units commanded 34.20% of the Vietnam mattress market size in 2025, while king-size models are expected to grow fastest at a 7.31% CAGR between 2026-2031.

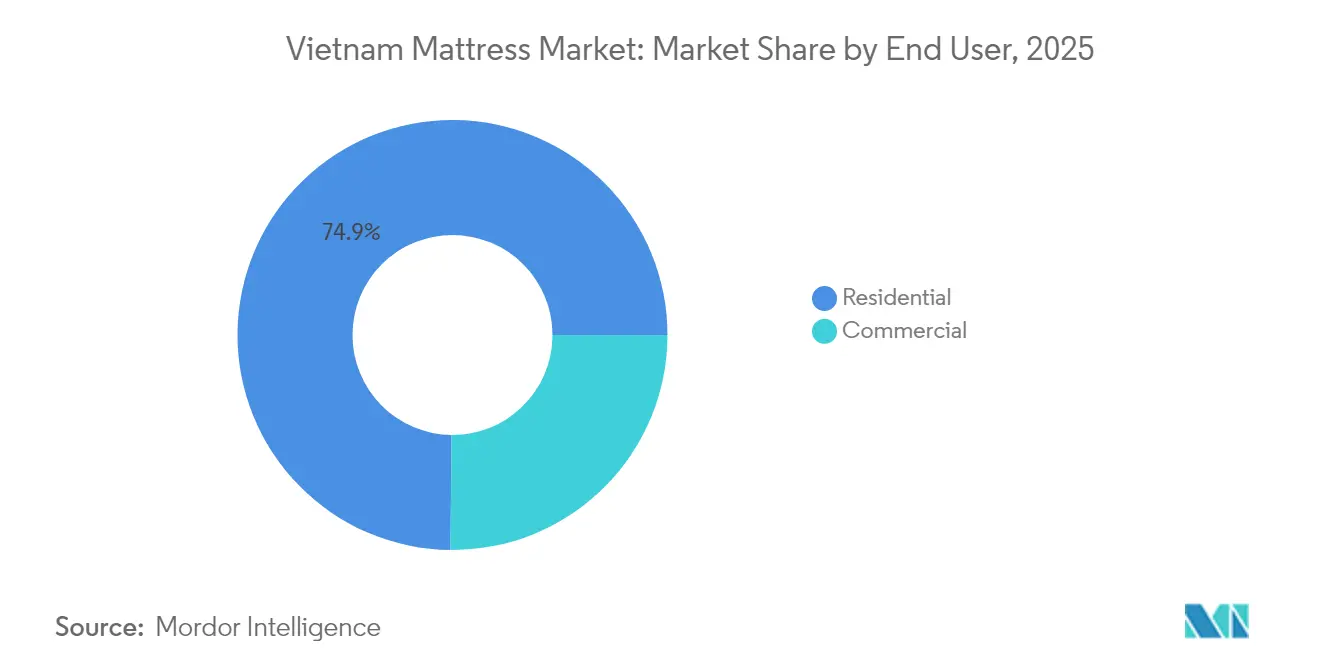

- By end user, the residential segment accounted for 74.85% of the Vietnam mattress market size in 2025; the commercial segment is advancing at a 7.10% CAGR through 2031.

- By distribution channel, B2C retail controlled 70.85% of Vietnam mattress market share in 2025 and is projected to post an 8.03% CAGR over the forecast period.

- By geography, Northern Vietnam held 41.20% of the Vietnam mattress market share in 2025, whereas Central Vietnam is expected to log the fastest 7.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Mattress Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & sleep-health awareness | +1.8% | National, urban centers | Medium term (2-4 years) |

| Booming domestic hospitality pipeline | +1.2% | Central & Northern coastal regions | Short term (≤ 2 years) |

| Rapid e-commerce penetration into Tier-2/3 | +1.0% | Central & Southern provinces | Medium term (2-4 years) |

| Anti-dumping duties redirecting FDI | +0.8% | National manufacturing hubs | Long term (≥ 4 years) |

| ASEAN-sourced latex under new EU rules | +0.6% | Export-oriented factories | Long term (≥ 4 years) |

| Early smart-bed adoption in premium cities | +0.4% | Hanoi & Ho Chi Minh City | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes & Sleep-Health Awareness

Vietnam’s enlarging middle class is directing more of its budget toward wellness categories, and better sleep has turned into a visible lifestyle priority. Consumers now expect an 8-10-year mattress lifespan and willingly pay premiums for certified comfort and durability. Domestic producer Kymdan markets 100% natural-latex models with warranties up to 25 years, validating buyers’ readiness for higher upfront costs[1]Source: Kymdan, “Company Profile & Certifications,” kymdan.com. Government stimulus that lifts household spending further magnifies this trend. Manufacturers responding with ergonomic designs and low-VOC certifications are capturing loyalty inside the Vietnam mattress market. Health consciousness is driving demand for certified products, with consumers increasingly seeking mattresses with Greenguard and UL certifications for environmental safety and spinal support benefits. The shift toward premium segments creates opportunities for manufacturers to differentiate through advanced materials, ergonomic design, and health-focused marketing strategies that resonate with Vietnam's evolving consumer priorities.

Booming Domestic Hospitality Pipeline

Hotel construction is surging, led by projects such as Tru by Hilton’s 14-property rollout and large coastal resorts capable of hosting thousands of guests. Each new room requires multiple mattress sets across its life cycle, directly enlarging commercial-segment volumes. International hotel chains impose rigorous supplier standards, rewarding ISO-certified manufacturers that can meet bulk orders on tight timelines. Developers’ preference for queen- and king-size beds is reinforcing growth in larger mattress formats. Central Vietnam, home to many beachfront projects, is emerging as a hotspot for contract procurement. The geographic concentration of hotel developments along Vietnam's central coast positions this region for accelerated mattress market growth, supported by tourism infrastructure investments and improved accessibility.

Rapid E-commerce Penetration into Tier-2/3 Cities

Vietnam’s online retail value is forecast to top USD 25 billion in 2024, and mattresses are migrating quickly to direct-to-consumer carts. Digital platforms remove geographic barriers, allowing rural households to compare brands previously confined to big-city showrooms. Domestic chain Vua Nệm pairs a 130-store footprint with an intuitive web channel that includes 100-night trials and free return pickup, illustrating best-practice omnichannel execution. Younger buyers rank doorstep delivery and transparent reviews above in-store testing, accelerating online share. Traditional outlets must integrate mobile engagement and next-day fulfillment to protect their presence in the Vietnam mattress market. Free delivery and wide product selection have become top consumer priorities, forcing traditional retailers to adapt their value propositions or risk market share erosion to digitally native competitors.

Anti-dumping Duties on Chinese Mattresses Redirecting FDI

Import tariffs on Chinese mattresses have sparked a supply-chain migration toward Vietnam, giving local plants a larger role in regional sourcing. Several global brands have opened production lines in Dong Nai and Binh Duong to sidestep duties and shorten lead times to ASEAN customers. Foreign direct investors bring process technology and training that raise industry benchmarks for local suppliers. Parallel U.S. duties on Vietnamese exports compel factories to shift toward value-added designs and branded output rather than undifferentiated OEM volume. Manufacturers mastering both compliance and upmarket positioning stand to gain share inside the Vietnam mattress market. Companies that navigate trade compliance requirements while maintaining cost competitiveness will benefit from sustained demand as international buyers continue diversifying their supplier bases away from over-concentrated manufacturing regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented foam supply inflating input cost | −1.4% | National manufacturing corridors | Short term (≤ 2 years) |

| Low replacement cycles in rural areas | −0.9% | Central & Northern rural districts | Long term (≥ 4 years) |

| Intensifying price war from grey-market imports | −0.8% | Urban border trade zones | Medium term (2-4 years) |

| Limited recycling infrastructure | −0.5% | Major municipal regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Foam Supply Inflating Input Costs

Vietnam relies heavily on imported polyurethane feedstock, leaving manufacturers susceptible to currency swings and freight disruptions. Small and mid-sized firms often purchase through multiple distributors, accepting mark-ups that compress margins. In contrast, large players such as Pearl Polyurethane Systems doubled local capacity to 20,000 tons per year in 2025, improving negotiation leverage and costs. Until domestic chemical production scales further, foam-price volatility will challenge stable pricing in the Vietnam mattress market. Long-term contracts with upstream suppliers and recycling initiatives offer partial relief. Raw material price volatility affects different mattress segments disproportionately, with budget-conscious consumers becoming more price-sensitive during inflationary periods, potentially slowing market growth in price-competitive segments. The lack of integrated foam production capabilities within Vietnam necessitates import dependency, exposing manufacturers to currency fluctuations and international supply chain disruptions that can rapidly erode profitability margins.

Low Replacement Cycles in Rural Areas

Households outside tier-one cities typically replace mattresses every 12-15 years, well beyond the 8-10-year cycle common in urban centers. Income constraints, limited product awareness, and difficult logistics curtail new-purchase frequency. Rural consumers remain attached to low-cost innerspring models, slowing adoption of premium memory-foam or latex variants. Manufacturers must introduce entry-level SKUs and installment financing to accelerate turnover. Bridging the urban-rural gap is essential for unlocking the full demand potential of the Vietnam mattress market. The price war dynamics are most pronounced in urban markets where distribution channels are more accessible and consumer awareness of brand authenticity may be lower, requiring manufacturers to invest heavily in brand protection and consumer education initiatives that increase operational costs without directly contributing to revenue growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Memory Foam Leads, Hybrid Accelerates

Memory-foam models secured a 33.95% Vietnam mattress market share in 2025, mirroring growing recognition of pressure-relief and temperature-adaptation benefits in humid climates. Hybrid designs, blending pocketed coils with foam comfort layers, are forecast to register a 6.76% CAGR through 2031, the fastest among all categories. Traditional innerspring units stay prevalent in budget-sensitive and rural segments, while latex variants leverage Vietnam’s abundant rubber supply to cultivate a sustainability narrative. The Vietnam mattress market size for hybrid products is expected to widen as consumers demand balanced support without forgoing contouring comfort. Regulatory pushes toward recyclable components further accelerate interest in latex and modular hybrids.

Continued R&D, including new benchmark testing from Dow and GoodBed, should standardize firmness and durability ratings, informing shopper choices and spurring premium product uptake. Memory-foam manufacturers are adding open-cell structures and gel infusions to enhance airflow within Vietnam’s tropical environment. Hybrid players tout motion isolation and edge support, appealing to couples upgrading from economy models. Latex producers promote hypoallergenic properties supported by certifications such as OEKO-TEX Standard 100. As differentiation sharpens, each sub-segment pursues distinct branding to capture its slice of the Vietnam mattress market.

By Mattress Size: Queen Dominates, King Expands

Queen-size units accounted for 34.20% of Vietnam mattress market share in 2025 thanks to the prevalence of two-bedroom apartments in Hanoi and Ho Chi Minh City. King-size demand is rising fastest with a 7.31% CAGR, fueled by income growth and a preference for spacious sleep surfaces among young families. Double and single sizes retain relevance in student housing, worker dormitories, and smaller urban dwellings. Developers of high-end condos report that mattress dimensions influence buyer perceptions of overall unit luxury. Consequently, larger formats are gaining floor-plan allocation in new projects, expanding the Vietnam mattress market size dedicated to king variants.

E-commerce allows distant consumers to order oversized mattresses without local inventory limits, although last-mile delivery still poses staircase and elevator challenges. Some brands now offer roll-packed king sizes that fit service elevators, mitigating logistics friction. Hotels along Vietnam’s central coast increasingly specify king-size beds in premium rooms, sustaining bulk procurement. Manufacturers must align production schedules with these size shifts to optimize inventory turns. Overall, mattress dimensions are evolving in step with rising living standards and larger dwelling footprints across the Vietnam mattress market.

By End User: Residential Foundation, Commercial Momentum

Residential buyers continued to dominate with 74.85% of Vietnam mattress market size in 2025, yet commercial demand is accelerating at a 7.10% CAGR through 2031. Every new hotel, serviced apartment, or corporate dormitory requires sizable mattress fleets and frequent replacement cycles. Contracts often stipulate flame-retardant fabrics, reinforced perimeter support, and ≥5-year warranty coverage, pushing suppliers toward hospitality-specific lines. On the residential front, consumers increasingly research online, weigh ergonomic claims, and choose installment plans before purchase. The Vietnam mattress market benefits as both household upgrades and tourism infrastructure investments progress in tandem.

Municipal housing programs and private developer launches add tens of thousands of new apartments annually, sustaining baseline residential volume. Meanwhile, corporate relocations and industrial-park expansions create staff-housing projects that fall under the commercial banner. Distinct sales channels, credit terms, and after-sales requirements characterize each end-user group, necessitating segmented go-to-market strategies. Manufacturers adept at juggling both retail branding and institutional tender processes gain resilience. Diversification across end-user categories is emerging as a hedge against cyclicality within the Vietnam mattress market.

By Distribution Channel: B2C Retail Dominance with Digital Integration

B2C outlets captured 70.85% of Vietnam mattress market share in 2025 and are projected to post an 8.03% CAGR, reflecting successful omnichannel models that marry in-store experience with online convenience. Specialty chains deploy sleep consultants and 100-night trials, while mass merchandisers rely on nationwide reach and promotional pricing. Pure-play e-commerce platforms emphasize user reviews, one-day shipping, and free returns, especially appealing to younger, mobile-savvy demographics. B2B project divisions handle bulk orders for hotels, hospitals, and dormitories, structuring deals around technical specifications and extended warranties. Continuous channel innovation remains pivotal to capturing incremental demand inside the Vietnam mattress market.

Augmented-reality apps that visualize mattress fit within a room and AI chatbots providing instant product comparisons are expanding website dwell time and conversion rates. Store footprints are growing selectively in Tier-2 cities where e-commerce awareness rises alongside demand for physical touchpoints. Brands unlock cost efficiencies through centralized fulfillment hubs supporting both digital and brick-and-mortar traffic. Loyalty programs offering mattress protectors, pillows, and recycle-pickup services encourage repeat engagement. Distribution agility will largely dictate competitive outcomes across the Vietnam mattress market.

Geography Analysis

Northern Vietnam’s urban concentration, anchored by Hanoi, drives premium purchases, aided by a sophisticated retail network and rising corporate accommodation needs. Government office expansions and foreign manufacturer headquarters stimulate steady mattress replacement cycles among expatriate and upper-middle-class consumers. Proximity to Chinese component suppliers shortens lead times and moderates costs for plants in Bac Ninh and Hai Phong. However, colder winters prompt a preference for heat-retentive foams, pushing seasonal SKU swaps. Local retailers thus curate assortments around climate cues to keep sell-through rates high in the Vietnam mattress market.

Central Vietnam’s resort pipeline acts as a catalyst for commercial contracts, with properties specifying uniform mattress specifications across hundreds of rooms. Improved airports in Phu Quoc and Cam Ranh funnel international arrivals, raising occupancy and replacement frequency. Retail penetration lags the north, yet as household incomes climb, queen-size adoption is quickening. Latex sourcing from nearby plantations keeps landed costs competitive, enticing newcomers to set up assembly lines in Da Nang. High tourism seasonality nevertheless forces careful cash-flow planning among suppliers courting this sub-market of the Vietnam mattress market.

Southern Vietnam maintains a balanced residential-commercial mix, buoyed by Ho Chi Minh City’s real-estate handovers and industrial-zone dormitory projects. High container-port capacity supports both component imports and finished-mattress exports, reinforcing the region’s manufacturing stature. Consumer preferences skew toward breathable fabrics due to year-round humidity, spurring R&D in moisture-wicking covers. Competitive density is highest here, with international showrooms often opening their first Vietnamese locations on Nguyen Trai Street. Market entrants must therefore differentiate through digital service, ESG transparency, or finance offers to win share in the Vietnam mattress market.

Competitive Landscape

The Vietnam mattress market features moderate fragmentation: global players such as Tempur Sealy, Serta, and Dunlopillo operate alongside domestic names like Vua Nệm, Kymdan, and Everpia. Multinationals capitalize on R&D muscle and supply-chain leverage to launch memory-foam and smart-bed lines locally, while Vietnamese firms exploit cultural proximity and price agility. Pearl Polyurethane Systems’ doubling of foam output underscores the vertical-integration thrust intended to stabilize raw-material costs. Kymdan’s Greenguard certification helps defend premium price points among health-conscious buyers within the Vietnam mattress market.

Vua Nệm carries Tempur and Serta in more than 130 outlets, co-sharing marketing spends and broadening assortment depth. Sustainability is another battleground; firms investing early in take-back logistics and FSC-certified latex earn procurement preference from international hotel chains[3]Source: Tempur Sealy International, “Q1 2025 Investor Presentation,” tempursealy.com. Digital disruptors are experimenting with subscription models that swap mattresses every five years for a fixed monthly fee, appealing to mobile millennials. Grey-market and counterfeit competition remain an overhang, prompting branded players to deploy QR-code verification and extended warranties. Overall, scale economics, ESG compliance, and omnichannel excellence are the three pillars now defining competitive edge in the Vietnam mattress market.

M&A activity is inching upward as mid-tier manufacturers confront cost inflation and EPR compliance burdens. Rumors of Vua Nệm’s 2025 IPO fueling a regional acquisition spree reflect a broader consolidation trajectory. International producers may seek joint ventures to secure latex supply and climb Vietnam’s brand ladder quickly. Smaller firms that lack capital for automation or traceability upgrades could exit, further lifting market concentration. While fragmentation persists today, competitive intensity is set to tighten as players jostle for enduring positions in the Vietnam mattress market.

Vietnam Mattress Industry Leaders

Vua Nệm

Liên Á

Dunlopillo Vietnam

Kim Cương Mattress

KyMDan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Jumiking received the 2025 Strong National Brand award for its natural-rubber mattress line incorporating 25-year warranties.

- February 2025: Dow and GoodBed launched a joint laboratory program to create standardized mattress performance benchmarks for pressure relief and durability.

- January 2025: Pearl Polyurethane Systems doubled annual capacity to 20,000 tons at its Dong Nai plant, citing robust domestic demand and Southeast Asian export prospects.

- October 2024: Pearl Polyurethane Systems inaugurated its Dong Nai manufacturing hub to supply polyurethane systems across Southeast Asia.

Vietnam Mattress Market Report Scope

Mattresses are constructed from a wide range of materials and are available in a range of sizes to suit individual requirements. Mattresses typically feature a quilt-like or similar case constructed from heavy cloth and a range of materials, including foam rubber, hairs, straws, cotton, and metal spring frameworks.

The Vietnam mattress market is segmented by type (innerspring mattress, memory foam mattress, latex mattress, and other mattress types), by application (residential and commercial), and by distribution channel (online and offline). The report offers market size and forecast in value (USD) for all the above segments.

By Product Type

| Innerspring / Coil |

| Foam (including memory foam) |

| Latex |

| Hybrid |

| Other Mattress Types |

By Mattress Size

| Single-size Mattress |

| Double-size Mattress |

| Queen-size Mattress |

| King-size Mattress |

| Custom & Specialty Sizes |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | |

| Online | |

| Other Distribution Channels | |

| B2B/Project |

By Geography

| Northern Vietnam |

| Central Vietnam |

| Southern Vietnam |

| By Product Type | Innerspring / Coil | |

| Foam (including memory foam) | ||

| Latex | ||

| Hybrid | ||

| Other Mattress Types | ||

| By Mattress Size | Single-size Mattress | |

| Double-size Mattress | ||

| Queen-size Mattress | ||

| King-size Mattress | ||

| Custom & Specialty Sizes | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Mass Merchandisers |

| Specialty Mattress Stores (including exclusive brand outlets) | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Project | ||

| By Geography | Northern Vietnam | |

| Central Vietnam | ||

| Southern Vietnam | ||

Key Questions Answered in the Report

What is the projected value of the Vietnam mattress market in 2031?

The market is forecast to reach USD 523.74 million by 2031, expanding at a 6.47% CAGR during 2026-2031.

Which product type currently leads sales in Vietnam?

Memory-foam mattresses hold the top position with a 33.95% share of 2025 revenue.

Which distribution channel is growing the fastest?

B2C retail, including omnichannel showrooms and e-commerce, is advancing at an 8.03% CAGR through 2031.

Why is Central Vietnam viewed as the fastest-growing region?

Large coastal resort projects and better transport links are driving a 7.52% CAGR for the region’s mattress demand.

How is regulation affecting domestic manufacturers?

Extended Producer Responsibility rules require firms to reclaim and recycle used mattresses, prompting investment in circular-economy logistics that raise short-term costs but enhance long-term competitiveness.

Page last updated on: