Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

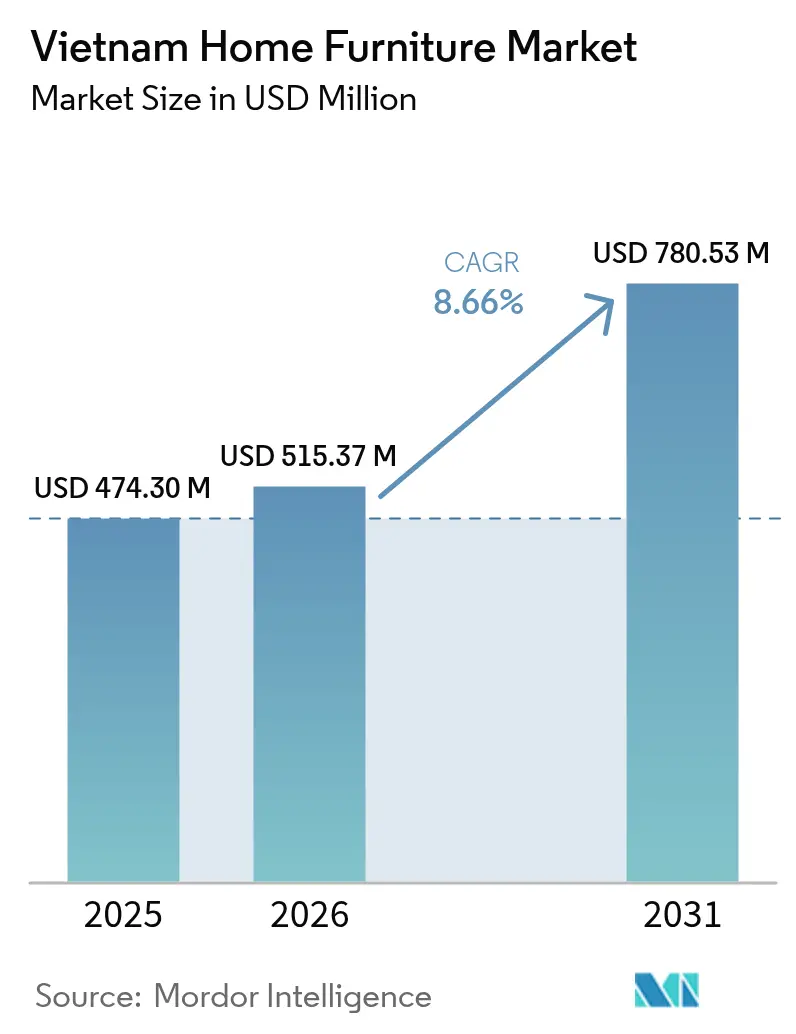

| Base Year Market Size (2025) | USD 474.30 Million |

| Market Size (2026) | USD 515.37 Million |

| Market Size (2031) | USD 780.53 Million |

| Growth Rate (2026 - 2031) | 8.66% CAGR |

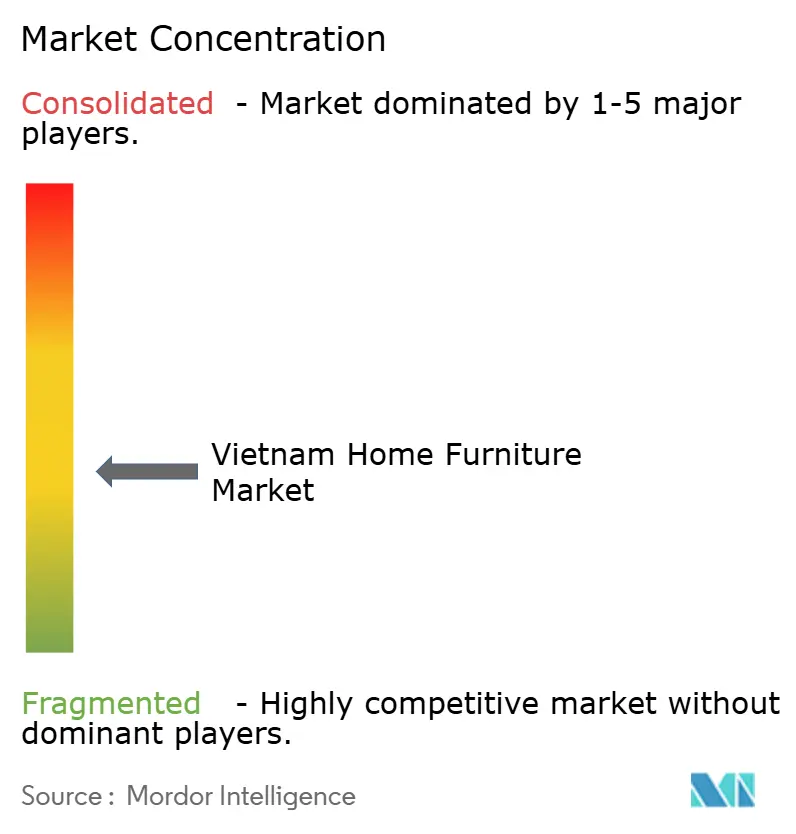

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Home Furniture Market Analysis by Mordor Intelligence

The Vietnam home furniture market size was valued at USD 474.30 million in 2025 and estimated to grow from USD 515.37 million in 2026 to reach USD 780.53 million by 2031, at a CAGR of 8.66% during the forecast period (2026-2031). Robust economic growth, expanding urban middle-class income, and government-backed housing programs are lifting demand across price tiers. Foreign direct investment inflows into processing and manufacturing keep production technology current and costs competitive. Rapid e-commerce adoption widens access to rural and secondary-city buyers, while rising apartment prices create a wealth effect that channels disposable income toward household upgrades. Together these forces reinforce Vietnam’s emergence as Southeast Asia’s most dynamic furniture production and consumption hub.

Key Report Takeaways

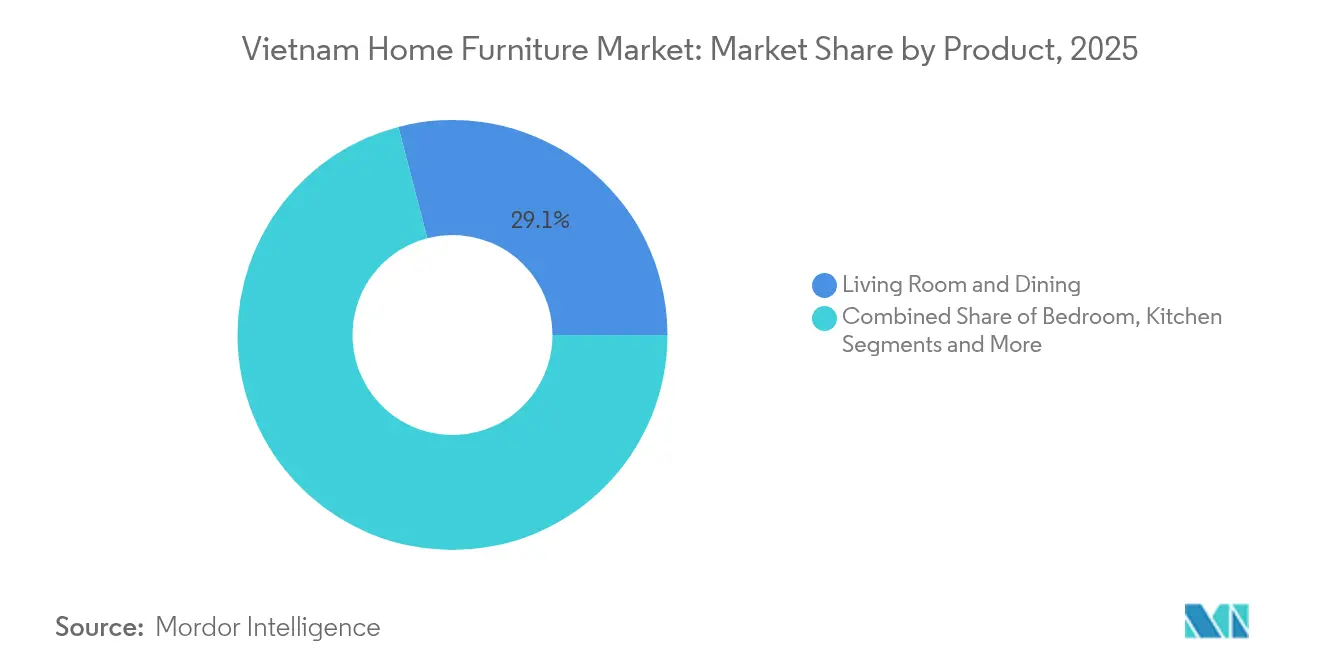

- By product category, Living Room and Dining furniture led with 29.05% revenue share in 2025; Home Office furniture is projected to expand at an 11.25% CAGR through 2031.

- By material, wood captured 58.14% of the Vietnam home furniture market share in 2025, while plastic and polymer materials are forecast to climb at a 12.35% CAGR to 2031.

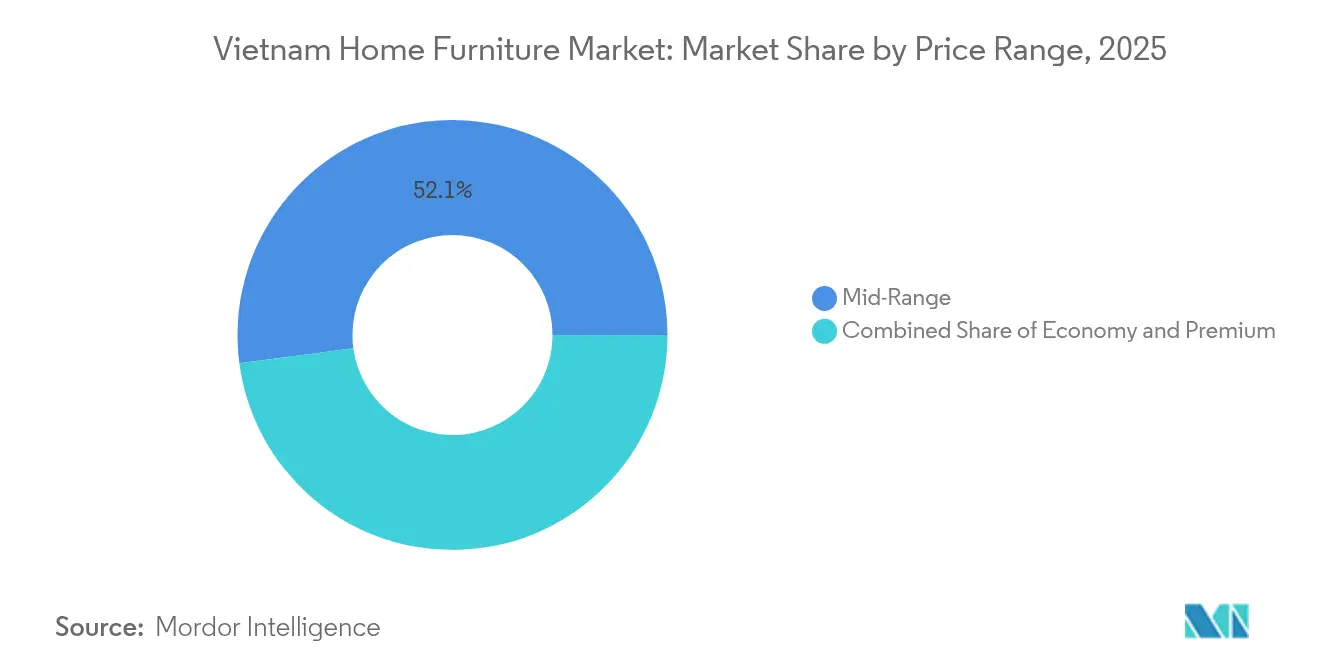

- By price range, mid-range offerings accounted for 52.10% share of the Vietnam home furniture market size in 2025; premium products are set to progress at an 11.05% CAGR over the same period.

- By distribution channel, specialty furniture stores held 45.60% of the Vietnam home furniture market share in 2025; online channels are expected to register a 13.35% CAGR by 2031.

- By geography, southern Vietnam commanded 39.10% share of the Vietnam home furniture market size in 2025, while northern Vietnam is forecast to grow at a 9.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class disposable income | 2.1% | National, with concentration in Ho Chi Minh City and Hanoi | Medium term (2-4 years) |

| Expanding residential construction and urban housing projects | 1.8% | Southern and Northern Vietnam, urban centers | Long term (≥ 4 years) |

| Robust growth of domestic e-commerce platforms | 1.5% | National, with higher penetration in urban areas | Short term (≤ 2 years) |

| Foreign direct investment inflows in furniture manufacturing | 1.3% | Binh Duong, Ho Chi Minh City, and industrial zones | Medium term (2-4 years) |

| Uptake of multi-functional furniture for small apartments | 1.2% | Urban centers, particularly Hanoi and Ho Chi Minh City | Short term (≤ 2 years) |

| Government push for sustainable forestry and certified wood | 0.9% | National, with focus on Central Vietnam forestry regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Disposable Income

Vietnam counts a fast-expanding urban middle class whose purchasing power underpins the Vietnam home furniture market. Retail sales surpassed USD 252 billion in 2024 and are tracking toward USD 350 billion by 2025, with households channeling more earnings into lifestyle goods. More frequent furniture replacement signals a shift from basic utility to design and brand differentiation. Accelerated remote-work adoption raises demand for ergonomic desks and chairs among young professionals. Income gains therefore support both the mid-range core and premium niches of the Vietnam home furniture market. The trend particularly benefits Home Office Furniture and Premium segments, as remote work arrangements and status-conscious consumption patterns reshape buying behaviors.

Expanding Residential Construction and Urban Housing Projects

Government targets for 1 million social housing units by 2030, plus major developer pipelines, add direct volume for furniture suppliers[1]Source: U.S. Department of Commerce, “Vietnam construction sector update 2025,” trade.gov . Vinhomes alone delivered nearly 15,000 residences in 2023, illustrating the scale of downstream demand. Apartment designs emphasize space-saving layouts that favor modular and multi-functional pieces. Public infrastructure outlays sustain a 7% annual construction growth path through 2027. The predictable completion cycle gives manufacturers a clear timeline for inventory planning within the Vietnam home furniture market. Green building initiatives, with approximately 430 certified projects expanding to 582 by 2030, create opportunities for sustainable furniture suppliers meeting environmental standards. The residential construction cycle typically generates furniture purchases within 6-12 months of completion, providing predictable demand patterns for manufacturers and retailers.

Robust Growth of Domestic E-Commerce Platforms

Online spending exceeded VND 1.23 trillion per day in the first half of 2025, 25% above the prior year. Shopee leads with a 55% share while TikTok Shop’s rapid ascent is reshaping digital merchandising costs. Furniture now represents 11% of total online gross merchandise value, proving that bulky items are no longer offline-only categories. Government policy aims for 70% of citizens to shop online by 2030, reinforcing digital momentum. Consequently, nationwide reach and lower last-mile costs are accelerating the Vietnam home furniture market’s penetration into smaller cities. Digital channels reduce inventory costs and showroom requirements, allowing furniture retailers to offer competitive pricing while maintaining profit margins. The e-commerce growth trajectory particularly benefits younger consumers who prefer online research and purchasing, aligning with Vietnam's demographic profile and digital-native behaviors.

Foreign Direct Investment Inflows in Furniture Manufacturing

Processing and manufacturing attracted USD 25.58 billion in FDI during 2024, 66.9% of total capital commitments. Singaporean and Japanese investors are upgrading automation, quality control, and green certification across Vietnamese factories. Modern equipment lifts output available for both export and domestic channels. Planned projects around Long Thanh International Airport promise logistics efficiencies that cut delivery lead times. Foreign investment particularly benefits furniture companies through improved logistics infrastructure, as major projects like Long Thanh International Airport enhance export capabilities and supply chain efficiency. FDI-backed furniture manufacturers often introduce international design standards and quality certifications, elevating the overall market sophistication and consumer expectations.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive consumer base limits premium uptake | -1.4% | National, with higher impact in rural and secondary cities | Medium term (2-4 years) |

| Fragmented and largely unorganized retail landscape | -1.1% | National, particularly affecting distribution efficiency | Long term (≥ 4 years) |

| Rising raw-material (wood and metal) cost volatility | -0.9% | National, with higher impact on manufacturing hubs | Short term (≤ 2 years) |

| Shortage of skilled carpenters amid manufacturing automation | -0.8% | Industrial zones, particularly Binh Duong and Ho Chi Minh City | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Consumer Base Limits Premium Uptake

Mid-range offerings control 52.45% of demand because many households still focus on functional value[2]Source: International Tropical Timber Organization, “Vietnam timber market trends 2024,” itto.int. Income disparities between urban centers and rural provinces dampen willingness to pay for global luxury labels. Sharp housing price increases in Hanoi and Ho Chi Minh City compress discretionary budgets during furnishing periods. Economic uncertainty further encourages consumers to delay non-essential upgrades. Price sensitivity intensifies during economic uncertainty, as consumers defer furniture purchases or opt for lower-cost alternatives when facing financial constraints. The restraint particularly impacts international brands attempting to establish premium positioning, as local manufacturers leverage cost advantages to offer comparable functionality at significantly lower price points.

Fragmented and Largely Unorganized Retail Landscape

Thousands of small family-run furniture shops dominate distribution, often lacking inventory systems or unified service standards[3]Source: Timber Trade Portal, “Vietnam wood-processing sector overview,” timbertradeportal.com. Limited scale raises logistics costs and hinders nationwide warranty coverage. Manufacturers struggle to enforce consistent brand messaging or pricing outside major chains. Rural shoppers sometimes travel to cities to compare models, elongating the purchase cycle. Fragmentation, while preserving entrepreneurial diversity, slows structural efficiency gains across the Vietnam home furniture market. The unorganized landscape creates barriers to implementing sustainable practices, quality certifications, and compliance with emerging regulatory requirements that could enhance Vietnam's furniture market reputation and export competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Office-Work Catalyzes Demand Realignment

Home Office furniture posts an 11.25% CAGR from 2026 to 2031, the fastest among all categories. Living Room and Dining pieces hold 29.05% share as Vietnamese culture values communal space. Bedroom lines enjoy stable replacement demand, while Kitchen upgrades ride modern cooking trends. Bathroom and Outdoor products remain smaller segments yet gain visibility as urban dwellers seek space optimization. Multigenerational households drive interest in convertible sofa-beds and nesting tables that stretch room functionality. The shift toward multi-functional designs becomes evident across all product categories, with Vietnamese consumers increasingly seeking furniture that maximizes utility in smaller urban living spaces. An Cường Wood JSC targets VND 4.05 trillion revenue and VND 450 billion net profit for 2025, reflecting industry confidence in sustained product demand across multiple categories.

The Vietnam home furniture market benefits as remote-work policies formalize hybrid routines across tech and professional services. Compact desks, ergonomic chairs, and integrated storage now headline online sales campaigns. Manufacturers add cable-management features and height-adjustable frames to meet health guidelines. Living Room sets incorporate modular ottomans that double as storage or guest seating. Product innovation therefore links lifestyle shifts to long-run volume growth within the Vietnam home furniture industry. The product segmentation reveals distinct consumer preferences across age groups, income levels, and living situations, enabling manufacturers to develop targeted offerings that address specific market needs and price sensitivities.

By Material: Wood Strength Encounters Sustainability Imperatives

Wood retains a 58.14% share, underpinned by Vietnam’s skilled carpentry tradition and robust supply chains. Plastic and polymer alternatives grow at 12.35% CAGR as young apartment owners value lightweight, easy-clean designs. Metal frames fill office, outdoor, and modernist niches, while engineered composites gain attention for eco-labels and cost savings. Import bills topped USD 316.36 million for U.S. hardwood in 2024, raising traceability scrutiny. VNTLAS certification rollout helps exporters comply with U.S. Lacey Act and EU Timber Regulation. The country imports 4-5 million cubic meters of raw materials annually, with significant portions sourced from higher-risk regions, prompting industry efforts to ensure legal compliance and sustainable sourcing practices. Hòa Phát Group's expansion into high-end flooring production with 70,000 m³/year capacity demonstrates material diversification strategies among major manufacturers.

Sustainability pushes mills to shift toward plantation wood, bamboo, and recycled polymers. Hoa Phat Group’s new 70,000 m³ bamboo flooring line signals mainstream acceptance of alternative fibers. Chemical-free finishes and low-VOC lacquers now feature in premium showrooms. Metal powder-coating innovations lengthen outdoor product life spans under tropical humidity. Material diversification, while easing raw-wood volatility, broadens design possibilities across the Vietnam home furniture market. The material segmentation reflects broader trends toward sustainability, cost optimization, and functional design that address Vietnamese consumers' evolving preferences and living requirements in urban environments.

By Price Range: Premium Upgrades Signal Market Maturation

Premium lines expand at 11.05% CAGR as aspirational buyers invest in statement pieces. Mid-range remains the volume anchor, balancing quality and affordability for mainstream households. Economy offerings still resonate in rural provinces and among first-time apartment dwellers. Cross-tier product strategies help brands retain customers as incomes rise. Financing plans through e-wallets or bank tie-ups soften upfront cost barriers for premium conversions. International partnerships, such as Hoàng Cương Group's collaboration with German brand Junger, introduce premium products with advanced technology and smart features that appeal to affluent Vietnamese consumers.

International collaborations, such as Hoàng Cương with Germany’s Junger, introduce smart-home features like app-controlled lighting. Domestic makers answer with locally styled wood carving and lacquer techniques at mid-range price points. Premium skews higher in Ho Chi Minh City, where expatriate and corporate demand intersect. Rural outlets display entry models yet offer catalog orders for upscale items, narrowing urban-rural choice gaps. Price segmentation enables furniture retailers to implement tiered marketing strategies, showroom layouts, and customer service approaches that address distinct consumer needs and purchase decision factors across different income levels and lifestyle preferences.

By Distribution Channel: Digital Momentum Reshapes Reach

Online platforms grow 13.35% annually, propelled by mobile data affordability and nationwide logistics investments. Specialty furniture stores still manage a 45.60% share through tactile product experiences and on-site customization. Home centers position themselves as renovation one-stops, bundling lighting and décor for convenience shoppers. Hypermarkets and department stores contribute to impulse sales of flat-pack and small-storage items. Omnichannel strategies integrate virtual showrooms and same-day in-store pickup to reduce cart abandonment. Vietnamese consumers increasingly research furniture online before making in-store purchases, creating opportunities for retailers who integrate digital and physical touchpoints effectively.

Shopee and TikTok Shop offer sellers livestream tools that humanize product demos and answer queries in real time. Click-and-collect models cut last-mile costs for bulky shipments. Independent stores digitize catalogs to capture online research traffic while closing sales offline. After-sales installation services build differentiation as pure-play e-tailers intensify price competition. Seamless channel blending defines success across the Vietnam home furniture market. Hybrid distribution models that blend online marketing and ordering with physical showrooms, delivery, and after-sales service enhance customer experience and operational efficiency.

Geography Analysis

Southern Vietnam leads the Vietnam home furniture market with a 39.10% share in 2025, capitalizing on Ho Chi Minh City’s trade corridors and deep manufacturing base. Extensive port capacity streamlines both raw-material imports and finished-goods exports. Residential mega-projects generate predictable furnishing cycles that retailers plan around quarterly. Retail showrooms benefit from dense urban footfall and higher discretionary incomes. Processing clusters shorten order-to-delivery times, reinforcing customer loyalty. The southern region's mature retail infrastructure includes established specialty furniture stores, home centers, and emerging e-commerce fulfillment networks that provide comprehensive market coverage. The southern region's mature retail infrastructure includes established specialty furniture stores, home centers, and emerging e-commerce fulfillment networks that provide comprehensive market coverage

Northern Vietnam is scaling at a 9.15% CAGR due to accelerating infrastructure and robust public investment. Hanoi’s rising apartment values create a wealth effect that channels capital toward home upgrades. Social-housing commitments increase unit completions across satellite towns, spurring volume sales of economy and mid-range lines. Proximity to Chinese component suppliers trims freight costs and broadens style selections. Government incentives for high-tech industry attract young professionals who furnish new apartments with ergonomic designs.

Central Vietnam remains a strategic diversification zone that links north and south corridors. Tourism-driven hospitality demand fuels orders for hotel and resort fit-outs. Provincial governments champion certified forestry projects that feed local joineries with legal wood. Industrial parks around Da Nang improve access to export logistics, enabling smaller workshops to reach global buyers. Balanced growth prevents over-dependency on a single coast, protecting supply chains within the Vietnam home furniture market. The central region's balanced approach to economic development and environmental sustainability aligns with growing consumer preferences for certified wood products and sustainable furniture manufacturing practices.

Value Chain Analysis

Vietnam home furniture value chains run in parallel: an export-oriented chain dominated by larger manufacturers and FDI-backed factories, and a more informal domestic chain that supplies households through fragmented retail. Upstream inputs center on plantation and imported timber, engineered wood, metal components, plastics and polymers, coatings and adhesives, and hardware, while the sector’s exposure to price and lead-time volatility is heightened by imported raw material volumes (4 to 5 million cubic meters annually). Traceability and certification have shifted from optional to operational requirements as firms adopt FSC and PEFC and related documentation practices to maintain access to regulated markets, which tightens supplier qualification and record-keeping across procurement.

Midstream processing includes kiln drying, panel production, CNC-based cutting and edging, finishing, packaging, and assembly. Capability gaps are increasingly tied to design and R&D talent and process digitalization. Downstream routes split between B2B project channels (developers, contractors, and apartment fit-outs) and B2C retail, where specialty furniture stores remain important while e-commerce platforms extend reach beyond major cities. Logistics flows connect manufacturing clusters such as Binh Duong with ports used for both input imports and finished-goods exports, and rising transport costs plus bulky-item last-mile complexity keep warehousing, installation, and after-sales service as key differentiators for branded players.

Competitive Landscape

Vietnam's furniture market exhibits moderate fragmentation with over 4,500 wood processing enterprises, 95% of which are privately owned, creating a competitive environment that balances scale advantages with niche specialization opportunities across different segments and price point. Truong Thanh targets USD 1 billion in revenue by 2030, signaling scale aspirations. An Cường projects VND 4.05 trillion in 2025 sales, supported by showroom expansion and B2B deals. International entrants such as IKEA, Ashley, and Nitori deploy franchising and direct investments to localize assortments. Export-focused clusters in Binh Duong pursue OEM volume, while domestic specialists tune collections to Vietnamese aesthetic codes.

Automation and digital marketing are central competitive levers. Firms integrate CNC routers and edge-banders to standardize quality while cutting labor costs. E-commerce-native brands capture millennial buyers with direct-to-door models and augmented-reality apps. Sustainability credentials gain weight as VNTLAS certificates become table stakes for U.S. and EU buyers. Partnerships like Hoàng Cương–Junger transfer smart-furniture know-how, raising product sophistication. Technology adoption accelerates across the competitive landscape, with companies investing in automation, digital marketing, and e-commerce capabilities to enhance operational efficiency and market reach. The competitive dynamics benefit from Vietnam's skilled workforce, favorable investment climate, and government support for manufacturing sector development.

Market entry barriers stay moderate thanks to abundant subcontractors and localized material supply. Yet customer-service expectations and omnichannel capabilities increasingly separate leaders from laggards. White-space opportunities persist in multi-functional modular sets and certified bamboo collections. Overall, the Vietnam home furniture market balances cost efficiency with rapid design evolution, maintaining healthy but not excessive rivalry. Emerging disruptors include e-commerce-native furniture brands that bypass traditional retail channels, companies specializing in space-saving designs for urban apartments, and manufacturers integrating smart technology and IoT connectivity into furniture products. The fragmented retail landscape creates distribution challenges but also enables multiple go-to-market strategies, from traditional specialty stores to emerging online platforms that reshape customer acquisition and retention approaches.

Vietnam Home Furniture Industry Leaders

AA Corporation

An Cường Wood Working JSC

Minh Dương Furniture

Truong Thành Furniture (TTF)

Phú Tài JSC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-led product and sourcing upgrades create a clear whitespace for certified, documented, and standard-labeled furniture and components sold into Vietnam. Circular No. 12/2026/TT-BCT (effective April 2026) requires imported wood furniture to carry FSC or PEFC sustainability certifications and Vietnamese-language instruction manuals aligned with TCCS 119:2025, which increases the importance of traceable materials, standardized user documentation, and quality systems across importers, retailers, and private-label sellers. Export-market compliance pressure, including the EU Deforestation Regulation becoming mandatory for wood exports to the EU starting in 2026, also drives investments in chain-of-custody, legal wood dossiers, and supplier auditing, and these capabilities can be repackaged into domestic positioning for sustainably sourced wood and engineered panels.

Digital and integrated project-supply models are another active opportunity area, supported by observed shifts in channel behavior and enterprise adoption of integrated planning tools. Online spending intensity in 1H 2025 (over VND 1.23 trillion per day) and the growing role of platforms such as Shopee and TikTok Shop support scale for furniture sellers that can manage bulky delivery, assembly, and returns. At the same time, B2B project demand tied to large housing pipelines encourages bundled solutions spanning panels, surfaces, and installation. Industry leaders are already moving in this direction, including An Cường Wood Working JSC implementing SAP S/4HANA to link production, finance, and supply chain, along with expanded partnerships on developer-oriented material solutions. This suggests room for more ODM/OBM offerings, modular designs for apartments, and service-led differentiation (measurement, customization, and after-sales) in a retail landscape that remains fragmented.

Recent Industry Developments

- May 2026: An Cường Wood Working JSC raised its 2026 business targets, citing a rebound in the domestic property market. The action signaled management confidence in near-term order visibility from housing-related demand and supported continued investment in capacity, channels, and product programs aligned with home furnishing cycles.

- July 2025: An Cường Wood Working JSC approved establishing Green Board Viet Nhat as a subsidiary at Becamex Industrial Park in Binh Phuoc, with an initial investment of VND 234.9 billion for an 87% stake and authorization for potential further investment up to VND 1.044 trillion. This expanded footprint strengthens domestic upstream capability for wood-based panels and supports more stable supply for home-furniture and interior applications.

- December 2024: Oppein inaugurated a B2B franchise showroom in Ho Chi Minh City focused on kitchen, wardrobe, and bathroom solutions for commercial projects. The expansion increased competitive intensity in project-led interior packages and reinforced the role of branded showrooms in capturing developer and contractor specifications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Vietnam home furniture market covers finished furniture bought for household use in Vietnam and sold through offline and online retail, measured in USD value at end-customer prices.

Scope exclusions: We exclude furniture made mainly for offices, hospitality projects, and other non-household settings, along with decor items, appliances, and home improvement materials.

Segmentation Overview

- By Product

- Living Room and Dining Room Furniture

- Bedroom Furniture

- Kitchen Furniture

- Home Office Furniture

- Bathroom Furniture

- Outdoor Furniture

- Other Furniture

- By Material

- Wood

- Metal

- Plastic and Polymer

- Others

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels (includes hypermarkets, supermarkets, teleshopping, departmental stores, etc.)

- By Geography

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the starting structure of the market and to anchor it to official signals that can be checked again each year. We referred to public sources such as the General Statistics Office of Vietnam, Vietnam Customs trade statistics, the World Bank, UN Comtrade, and product and safety guidance from standards bodies that publish furniture-related references. Along with these, we reviewed company annual reports, investor slides, association websites, and reputed business press to track pricing moves, channel shifts, and housing-linked demand.

To make the dataset more practical for sizing, we also used paid subscriptions for company financials and intelligence, and an import and export shipment-level database for cross-checking product flow direction and seasonality. Because public data can be reported with time lags, older series were aligned to the base year using inflation and exchange-rate context from official sources, and then validated against what retailers and distributors described in interviews. The desk sources mentioned here are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with retailers, distributors, furniture brands, and supporting ecosystem participants (such as material and component suppliers) across Vietnam. We used these discussions to confirm what products are treated as home furniture in practice, how offline stores and online selling split demand, and what price movements are realistic by category. Because this is a country market, viewpoints were balanced across key domestic regions, and we re-contacted respondents when desk signals and interview inputs did not match.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 17% | |

| Mid tier: 44% | Functional/Unit leaders: 23% | |

| Smaller Players: 17% | Managers: 60% |

Market-Sizing & Forecasting

Market sizing was built using a top-down and bottom-up blend, but the core model starts from a demand pool view linked to Vietnam household consumption. We first mapped the addressable spend using indicators like new housing completions, urban household formation, renovation and replacement behavior, and the share of furniture purchased through modern retail and e-commerce. Next, category-level price points were set using observed retail price bands and interview-validated mix shifts, and then totals were derived by combining implied volumes with average selling prices.

The totals were then corroborated through selective bottom-up approximations, where it was feasible, by rolling up sampled retailer sales, distributor throughput, and channel checks on how much of demand is imported versus locally made. When gaps appeared, such as limited transparency for small independent stores, we used conservative penetration and turnover assumptions that were stress-tested with managers in the market. For forecasting, scenario analysis was used around housing activity and consumer spending sensitivity, and the final path was selected based on what interviewees viewed as a realistic base case over 2026 to 2031.

Data Validation & Update Cycle

Validation was done by checking whether the modeled market moved in line with independent signals, such as furniture-related import and export trends, housing delivery cycles, and channel expansion patterns reported by retailers. Any large variance was investigated, and assumptions were revised only after a second pass that rechecked the supporting evidence and the interview notes. Before sign-off, the model is reviewed step by step so inputs, formulas, and conversions can be traced back to a clear source or a stated assumption.

Reports are refreshed annually, and interim updates are done when material events occur, such as major policy shifts, sharp currency moves, or sudden demand disruption. If an updated public release or a new interview contradicts the existing view, analysts re-contact relevant respondents and rerun the impacted parts of the model. Right before delivery, a fresh review is completed so clients receive the most current version of the estimates.

Mordor Intelligence's Vietnam Home Furniture Market Size Measured Against Other Published Estimates

Published market sizes for Vietnam home furniture often do not line up because firms make different choices on what counts as home furniture, which selling channels are included, and what base-year currency timing is applied. Our work tries to reduce these differences by keeping the category logic simple, and then checking it against demand and trade signals that can be repeated every year.

Some external numbers combine broader furniture and home-related items, which pushes the total upward even if the growth rate looks reasonable. For Mordor Intelligence, only finished home furniture purchased for household use in Vietnam is counted, and the totals are cross-checked using housing completion signals and furniture import and export flows before finalizing the curve.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 474.30 M (2025) | |

| Industry Report Publisher A | USD 1.10 B (2023) | Uses an earlier base year and a wider product list that can mix household furniture with adjacent items and broader furniture spend, which changes the implied demand pool and raises the total. |

| Market Bulletin B | USD 400.89 M (2024) | Often applies a tighter channel and category capture for the base year and may not fully normalize pricing mix changes across offline and online, which can keep the starting value lower even if growth is similar. |

The spread across sources mainly comes from scope choices and base-year treatment, not from a single math step. When the market is tied to household purchase demand and checked against trade direction, the size becomes easier to reproduce and explain, which helps decision-makers compare plans across years with fewer surprises.

Key Questions Answered in the Report

How large will Vietnam’s home furniture demand be in 2031?

The Vietnam home furniture market size is projected to reach USD 780.53 million by 2031, expanding at an 8.66% CAGR.

Which furniture category is growing fastest in Vietnam?

Home Office furniture is set to grow at an 11.25% CAGR through 2031 as remote work becomes commonplace.

What material holds the biggest share in Vietnamese furniture?

Wood retains 58.14% of demand due to local craftsmanship and mature supply chains.

How important are online channels for Vietnamese furniture sales?

Online platforms are the fastest-rising channel, forecast to post a 13.35% CAGR and broaden rural reach.

Which region buys the most furniture in Vietnam?

Southern Vietnam leads with 39.10% market share owing to Ho Chi Minh City’s economic scale and port access.

Page last updated on: