Vietnam Home Improvement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.77 Billion |

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 4.72 Billion |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

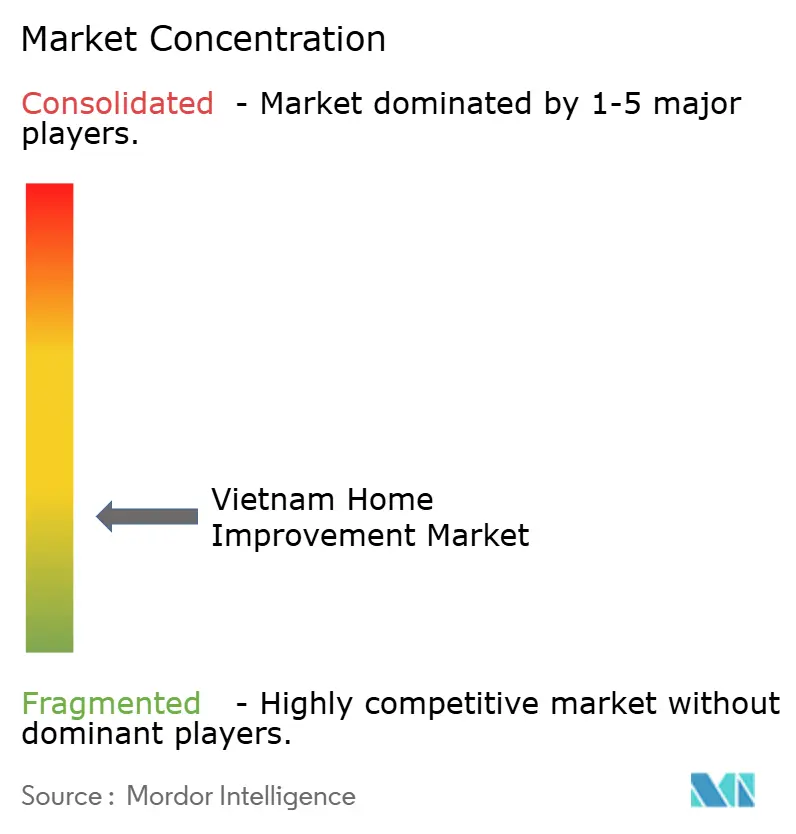

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Home Improvement Market Analysis by Mordor Intelligence

The Vietnam home improvement market size is expected to grow from USD 3.77 billion in 2025 to USD 3.91 billion in 2026 and is forecast to reach USD 4.72 billion by 2031 at a 3.84% CAGR over 2026-2031. The Vietnam home improvement market is experiencing steady growth, supported by rapid urbanization and the expansion of modern residential developments. A rising middle-income population is driving demand for higher-quality and aesthetically pleasing home solutions. Streamlined construction permitting has shortened approval cycles, making it easier for developers and contractors to complete projects efficiently. Financial support through social-housing credit programs and faster public investment disbursement has improved liquidity across the construction and renovation sector. Digital channels, including e-commerce platforms and livestream commerce, are making tools, fixtures, and décor more accessible, accelerating consumer adoption. The market is shifting toward premium offerings, with developers integrating biophilic design, smart lighting, and innovative materials into new communities. Renovation and remodelling activities continue to grow as homeowners seek modern, multifunctional living spaces. Regional hubs, particularly in southern and central Vietnam, are driving overall demand due to urban expansion and new economic zones. Fragmented competition allows local companies to leverage regional expertise, faster delivery, and flexible payment terms. Large-scale infrastructure projects, administrative reforms, and social-housing initiatives are creating long-term, predictable demand, benefiting both domestic and international home improvement suppliers.

Key Report Takeaways

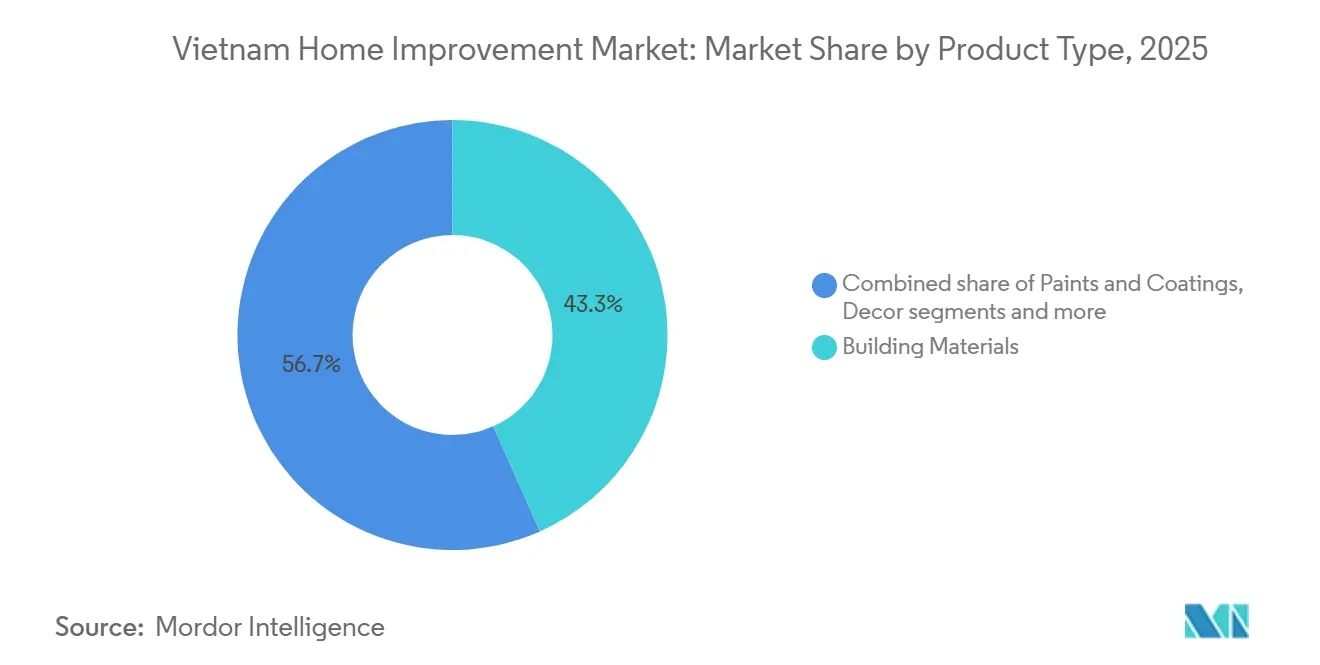

- By product type, building materials led with 43.33% of the Vietnam home improvement market share in 2025, while décor and lighting are projected to expand at a 9.33% CAGR to 2031.

- By distribution channel, home improvement stores held 51.36% of the Vietnam home improvement market share in 2025, and online retail is projected to record a 7.33% CAGR through 2031.

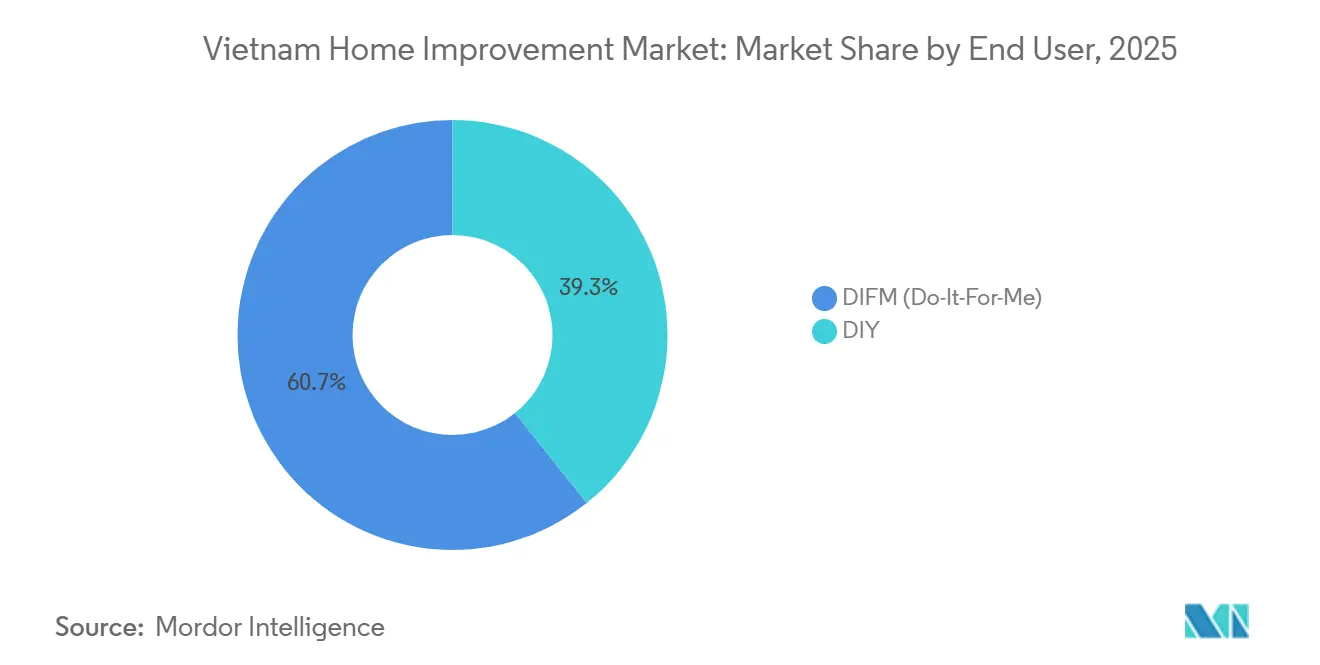

- By end user, the DIFM segment commanded 60.73% of the Vietnam home improvement market share in 2025, whereas DIY is forecast to grow at an 8.73% CAGR to 2031.

- By project type, renovation accounted for 45.37% of the Vietnam home improvement market share in 2025, and remodelling is projected to expand at a 7.40% CAGR to 2031.

- By geography, Southern Vietnam captured 47.74% of the Vietnam home improvement market size in 2025, while Central Vietnam is projected to record the fastest growth at an 8.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Home Improvement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban migration surge and rising disposable earnings | +1.6% | Urban centers and growth corridors | Long term (≥ 4 years) |

| Government-led renovation subsidies | +1.1% | National and provincial renewal clusters | Medium term (2–4 years) |

| Online home-improvement sales boom | +0.9% | Metro and tier-2 city catchments | Short term (≤ 2 years) |

| Compact-space DIY upgrades | +0.7% | Dense urban housing and rental markets | Short term (≤ 2 years) |

| High-spending repatriate consumers | +0.6% | Metro suburbs and high NRI inflow states | Medium term (2–4 years) |

| Eco-friendly building material uptake | +0.5% | Eco-focused urban districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban migration surge and rising disposable earnings

Vietnam exceeded 45% urbanization in 2025, with policymakers targeting 50% by 2030, expanding the potential market for renovation and remodelling in dense urban clusters[1]Open Development Mekong, “Urbanization in Vietnam,” Open Development Vietnam, vietnan.opendevelopmentmekong.net. Household incomes are also rising, with official surveys showing higher monthly earnings in 2025, enabling discretionary spending on upgrades beyond basic repairs. The IMF highlights that investment levels remain elevated at around 31% of GDP through 2026, supporting private construction activity and home-related expenditures as credit channels normalize[2]IMF Staff, “Vietnam: 2025 Article IV Consultation,” IMF, elibrary.imf.org. As per capita GDP surpassed USD 5,000 in 2025, urban households are increasingly investing in smart fixtures, premium flooring, and upgraded bathrooms that enhance comfort and efficiency. Suppliers with regional manufacturing and Vietnam-tailored product lines, such as LIXIL, are well-positioned to benefit from this trend. The World Bank further notes that domestic demand is bolstered by a faster real estate recovery and clearer project clearance procedures, sustaining home improvement purchasing momentum in key cities.

Government-led renovation subsidies

Policy support for housing renewal scaled up significantly in 2024 and 2025, with a nationwide campaign rebuilding over 330,000 substandard dwellings ahead of schedule (vietcetera.com). The program boosted demand for construction materials, benefiting steel and cement producers, while leading domestic suppliers reported strong sales during the 2025 construction season (hoaphat.com.vn). A VND145 trillion (USD 6 billion) social-housing credit package, complemented by city-level interest support, unlocked financing for both new units and refurbishment projects in priority districts (vietnamnews.vn; vietnamplus.vn). Ho Chi Minh City plans to deliver 28,500 social housing units in 2026, with prepared land for multiple projects, sustaining demand for interior finishes and fixtures[3]Vietnam News Agency, “Việt Nam sees strong e-commerce growth in 2025,” Vietnam News, vietnamnews.vn. Hanoi is advancing a pipeline of 69 projects, including major developments in Dong Anh District, creating large procurement opportunities for home improvement products (vietnamplus.vn). As project delivery accelerates, large contractors with established client relationships and strong backlogs, such as Coteccons, are positioned to benefit from more predictable project sequencing.

Online home-improvement sales boom

E-commerce is rapidly reshaping home-improvement retail in Vietnam, with home-related categories consistently performing among the top online sellers. Livestream commerce and platform innovations, such as TikTok Shop, are transforming product discovery and purchase behavior, favoring official brand stores that ensure quality and warranties. Recent regulatory updates, including a new E-commerce Law, have strengthened platform responsibilities and consumer protections, formalizing the ecosystem and building trust. Consumers are increasingly prioritizing authenticated storefronts, reflecting a quality-first mindset even as these stores represent a smaller share of sellers. Major brands are enhancing omnichannel strategies by linking online orders to nearby store inventory, enabling faster delivery and more convenient services. These developments are broadening market access to younger homeowners and first-time buyers, who are more willing to purchase home improvement products online and utilize bundled installation or after-sales services.

Compact-space DIY upgrades

Urban households in Vietnam are increasingly embracing DIY projects to reconfigure small living spaces for work, study, and leisure. Consumers are showing a clear preference to undertake upgrades themselves when feasible, supported by domestic smart-home players and official brand storefronts offering self-install kits and app-based tutorials. These resources reduce barriers for basic improvements, such as lighting, switches, and storage solutions. Recent amendments to construction regulations provide clarity on exemptions for internal repairs, creating a predictable framework for small-scale DIY activities. While DIY adoption grows, complex tasks like electrical or plumbing work remain within contractor-led “Do-It-For-Me” services. Hybrid service models that combine remote guidance with local installer support are emerging, helping expand DIY adoption beyond major urban centers. This trend reflects a broader shift toward multifunctional, self-customized living environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented supply chain leading to inconsistent quality standards | −0.6% | Unorganized nodes and peri-urban markets | Medium term (2–4 years) |

| Escalating property costs limiting remodel spend | −0.4% | Major urban centers | Short term (≤ 2 years) |

| Fluctuating global input prices | −0.3% | Globally exposed input-linked categories | Short term (≤ 2 years) |

| Limited skilled installers in Tier-2 and Tier-3 cities | −0.2% | Tier-2 and tier-3 city clusters | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fragmented supply chain leading to inconsistent quality standards

Raw-material volatility affects project budgets and retail pricing, creating uncertainty for both consumers and trade buyers in 2026. Iron ore and energy inputs moved through sharp cycles in 2025, which influenced steel mill spreads and stocking decisions in the distribution channel[4]ASEMCONNECT (VITIC, MOIT), “Vietnam’s steel market in October 2025,” ASEMCONNECT, asemconnectvietnam.gov.vn. Domestic construction materials, including cement, are also subject to seasonal and weather-driven volume variations, which can compress margins when combined with cost swings. While rising selling prices can partially offset these pressures, the pass-through varies by product category and brand strength. Integrated producers with expanded capacity have greater flexibility to manage throughput and product mix during periods of price volatility. Investments in low-carbon cement lines and logistics efficiency further help certain manufacturers mitigate the impact of material cost fluctuations on final pricing.

Limited skilled installers in Tier-2 And Tier-3 cities

The installer pipeline outside major metropolitan areas remains limited, increasing execution risks for time-sensitive renovation and remodelling projects. Manufacturers and retailers face service coverage gaps that can slow the adoption of advanced fixtures and smart home systems requiring trained technicians. Industrial growth in secondary cities has tightened local labor pools, prompting contractors to rotate crews from urban centers at higher cost. This shortage can lead to delayed project completion and inconsistent service quality, impacting customer satisfaction. Over time, standardized installation kits and modular product designs are helping to reduce installation time and bridge skill gaps. Expanded vocational training programs and consistent enforcement of safety standards are critical to stabilizing installation quality. As demand for home improvement and remodelling grows in emerging urban corridors, addressing installer shortages will be key to sustaining market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Material Innovation Outpacing Volume Growth

Building Materials accounted for a 43.33% share in 2025, anchoring the category mix with structural steel, cement, and ceramic tiles that form the backbone of residential and small-commercial projects. Price volatility in steel, energy inputs, and logistics influenced working capital cycles for mills and distributors, as rebar and ore spreads shifted during the year. Cement sales experienced seasonal and weather-related dips, although infrastructure spending sustained baseline demand. Analysts project firmer selling prices and improved mill throughput, which could enhance gross margins for integrated producers. Specialty capacity expansions, including railway-grade rails and specialized steels at Dung Quat, are broadening product offerings to support transport infrastructure and diversified project pipelines. Low-carbon production and energy-efficient processes are increasingly being adopted to meet environmental standards and export compliance requirements.

Paints, coatings, décor, and lighting categories are driving growth through plant upgrades, premium product lines, and developer-focused specifications. New color systems, interior finishes, and exclusive supply agreements have strengthened brand performance in retail and project pipelines. Tools and equipment are benefiting from e-commerce adoption and omnichannel strategies that integrate point-of-sale experience centers with online content and services. The Vietnam home improvement market size for décor and lighting is projected to expand at a 9.33% CAGR between 2026 and 2031 as developers and homeowners invest in premium surfaces and connected ambient systems. Plumbing and electrical categories are advancing as brands refresh premium lines and introduce antibacterial and surface-protection technologies to meet hygiene expectations. Regulatory modernization, including a national construction information system and digitized approvals, further supports category momentum by clarifying compliance benchmarks for materials and systems.

By Project Type: Renovation Dominates, Remodeling Surges

Renovation represented 45.37% of activity in 2025 as aging stock and deferred maintenance met better financing access and stronger contractor mobilization. Nationwide housing repair initiatives completed large-scale rebuilds ahead of schedule, generating significant demand for core materials and finishing products. Social-housing credit programs and city-level interest support have sustained repair and upgrade cycles, encouraging more households to engage with formal procurement channels. Infrastructure beautification and utility upgrades in high-traffic urban corridors provide additional opportunities for renovation spending. The digitization of project approval processes and the expansion of construction data systems are improving phase sequencing and project efficiency. Together, these factors are maintaining a strong baseline of renovation activity across core cities and surrounding areas.

Remodelling is projected to grow at a 7.40% CAGR through 2031 as buyers reconfigure living spaces with premium finishes and smart functions suited to evolving urban lifestyles. New residential projects are increasingly equipped with wiring and infrastructure that facilitate post-handover upgrades, including smart lighting, advanced kitchens, and high-spec bathrooms. Premium materials such as sintered stone, high-performance laminates, and antibacterial sanitaryware are helping brands protect margins in the remodelling segment. Product updates and category roadmaps emphasize simplified installation and long-term durability, aligning with urban apartment and villa upgrade cycles. Maintenance and minor repair work continue to generate recurring demand for paints, sealants, fixtures, and service calls. Overall, remodelling complements renovation activity, expanding the market’s scope and supporting steady growth across residential segments.

By End User: Professional Contractors Retain Control, DIY Gaining Ground

Do-It-For-Me (DIFM) or professional installation captured a 60.73% share in 2025, reflecting Vietnam’s long-standing reliance on skilled trades for structural and systems work in both old and new housing stock. The national housing repair campaigns were executed primarily by professional installers, reinforcing the central role of DIFM in meeting tight deadlines and technical standards. Contractor backlogs indicate strong confidence in delivering large-scale residential and public infrastructure projects, with teams capable of mobilizing across multiple sites. Leading firms emphasize repeat-client relationships and enhanced technical capabilities, enabling them to handle more complex project scopes as developments scale. Clearer permitting pathways for well-defined projects further support contractor efficiency and reliability. Together, these factors anchor DIFM as a key driver of market activity and professional service demand in 2026 and beyond.

DIY outpaced the market in 2025 and continues to gain traction at an 8.73% CAGR through 2031, as digital channels reduce knowledge gaps for simple upgrades. DIY activity is also gaining traction as homeowners increasingly pursue manageable projects themselves, supported by digital tools and online knowledge resources. Self-install smart kits, app-based tutorials, and in-store experience zones make it easier for consumers to explore products and complete simpler upgrades. Legal clarity on internal repairs that do not affect structural or fire safety reduces perceived regulatory hurdles and encourages time-bound DIY initiatives. Surveys indicate that a significant share of homeowners plan to undertake projects independently when design and installation are straightforward. Over time, hybrid models combining remote guidance with local installer support are expected to expand DIY adoption into Tier-2 and Tier-3 cities, where certified installer availability remains limited. This combination of DIFM reliability and growing DIY engagement is shaping a more versatile and accessible home improvement market in Vietnam.

By Distribution Channel: Omnichannel Convergence Accelerating

Store-based formats held the lead with 51.36% share in 2025 as customers continued to test finishes, verify colors, and evaluate fixture mechanics in person before purchase, especially for high-ticket items. Large retail chains are expanding their footprints and investing in logistics to improve fulfillment speed and last-mile reliability in major urban centers. Developers with integrated retail ecosystems link post-handover upgrades to curated assortments that align with project specifications, simplifying decision-making and installation scheduling for homeowners. Specialty showrooms are driving category education and premiumization, particularly in sanitaryware, smart toilets, and designer surfaces, through new galleries and updated product offerings. Consumers continue to balance in-store evaluation with digital tools for product discovery and service bookings, supporting the growth of omnichannel platforms. This combination of tactile experience and online support positions retailers to capture greater market share in the coming years.

The Vietnam home improvement market size for online retail is projected to expand at a 7.33% CAGR as livestreams, authenticated brand storefronts, and improved delivery windows draw more planned purchases to digital channels. National e-commerce continues to consolidate among leading platforms, with household and home-related goods consistently ranking among the top-selling categories. The government’s new E-commerce Law enhances platform accountability and tax compliance, creating a more formal and trusted environment for high-value transactions. Mall-style storefronts that emphasize authenticity and warranty support are capturing disproportionately high sales relative to their seller base, reflecting consumer demand for quality assurance online. Project procurement and direct manufacturer sales continue to complement traditional retail, particularly for large-scale contracts where cost optimization and specification compliance are priorities. Together, these trends are strengthening both digital and physical channels, creating a more integrated and efficient home improvement market in Vietnam.

Geography Analysis

Southern Vietnam accounted for 47.74% of the Vietnam home improvement market share in 2025, supported by Ho Chi Minh City’s scale, developer pipelines, and logistics advantages that reduce delivery times and widen assortment depth. The region’s growth is further supported by strategic transport infrastructure, including ports, airports, and expressways, which enhance connectivity to coastal development zones and emerging suburban projects. Developers’ expansion into coastal and suburban areas has stimulated both consumer interest and downstream demand for fixtures, finishes, and interior upgrades. The housing pipeline in HCMC and neighboring provinces has expanded significantly, providing a large base of buyers ready to invest in post-handover improvements. Apartment pricing trends in core urban areas, complemented by more affordable options in surrounding provinces, increase the addressable market for renovation and remodelling activity. Manufacturing hubs, industrial parks, and export logistics reinforce long-term demand, while commercial and infrastructure projects drive additional need for construction chemicals, coatings, and premium finishes.

Northern Vietnam benefits from high urban density, concentrated high-tech manufacturing, and planned transport corridors that support multi-year investment and remodelling cycles. Hanoi’s social housing pipeline and active residential projects provide clear visibility for finishing and interior upgrade demand. Industrial park occupancy remains high, supported by continued foreign direct investment, which maintains construction activity and drives remodelling in districts serving electronics and support industries. Efficient logistics through Hai Phong and planned ring roads and expressways are expected to enhance intra-regional connectivity, expanding the reach of urban home improvement offerings. Cold-weather requirements and specialized facilities shape material selection, influencing demand for fast-curing admixtures and antistatic coatings.

Central Vietnam is the smallest market in volume terms but is projected to grow the fastest at an 8.85% CAGR through 2031 due to Da Nang’s policy incentives, free-trade zone benefits, and rising investor attention. Corporate tax holidays and long-term land leases in free-trade zones encourage high-value industrial development, which drives residential demand for new construction and upgrades. Investments in urban infrastructure and port improvements extend the region’s capacity for manufacturing and logistics, supporting housing growth and home improvement activity. Stricter planning and compliance requirements in urban areas promote synchronized investments in utilities, drainage, and transportation, improving project execution. Smaller regions, including the Mekong Delta and Northern Midlands and Mountainous areas, are experiencing pockets of growth tied to industrial corridors and connectivity improvements. As labor pools expand and supply chains develop, these emerging areas create incremental opportunities for home improvement suppliers and contractors across the country.

Competitive Landscape

The Vietnam home improvement market remains fragmented, with leading suppliers holding a relatively small share, leaving ample room for regional and local specialists to compete on speed, service, and flexible payment terms. Distributors and retailers in Tier-2 and Tier-3 cities maintain strong relationships with contractors and homeowners, enabling fast fulfillment and on-site support. Branded players continue to dominate categories such as plumbing, sanitaryware, and lighting due to certification requirements, warranty offerings, and consumer perceptions of quality. As omnichannel models evolve, companies that effectively integrate digital discovery with physical service are better positioned to convert interest into installation-ready purchases. Sustainability credentials and compliance readiness are emerging as important differentiators, particularly for corporate and developer clients aligning with green building standards.

Strategic moves across the market focus on vertical integration, capacity expansion, and technology upgrades to strengthen competitiveness. Leading players are acquiring specialized firms and expanding manufacturing capabilities to support residential and infrastructure projects, while also enhancing engineering and civil execution capacity. Product-level differentiation remains key, with brands introducing high-durability, antibacterial, and premium features to meet evolving consumer preferences. Innovations in installation efficiency, such as faster-fit systems for constrained urban spaces, help address skill bottlenecks and improve service delivery. These moves, taken together, allow suppliers to capture both large-scale project demand and smaller residential upgrade opportunities.

Digital commerce and technology adoption are reshaping how products are discovered and purchased, especially for higher-value SKUs like paints, lighting, tools, and storage solutions. Livestream platforms and authenticated online storefronts are enhancing trust and compressing the path from awareness to purchase. On the supply side, manufacturers are investing in low-carbon production, energy-efficient systems, and sustainable materials to reduce environmental impact and operational costs. Contractors are leveraging project management and BIM tools to improve delivery quality and maintain schedules on complex assignments. As omnichannel ecosystems, compliance upgrades, and expanded capacities converge, the Vietnam home improvement market is poised for a step-change in service reliability and overall efficiency.

Vietnam Home Improvement Industry Leaders

Eurowindow

Hoa Phat Group

SCG

LIXIL

AkzoNobel (Dulux)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Hoa Phat Group begun building a major new rail and special steel manufacturing facility in the Dung Quat Economic Zone, representing a multi‑billion VND strategic investment to strengthen Vietnam’s industrial capacity. The plant is designed for high‑quality rail and steel production with 700,000 tons of annual capacity, aiming to support domestic infrastructure and reduce reliance on imports while boosting local supply chains for key projects.

- December 2025: Da Nang launched an unprecedented incentive package for its newly established Free Trade Zone, offering tax exemptions, reduced corporate and personal income tax rates, long‑term land leases, and streamlined licensing to attract foreign and domestic investment. These measures aim to position Da Nang as a competitive economic and logistics hub, boosting manufacturing, services, and innovation activity in central Vietnam.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Vietnam's home improvement market as the annual spending on materials, fixtures, tools, and allied installation services used to renovate, repair, or upgrade occupied residential units across the country, regardless of project scale.

Scope exclusion: new-build housing, purely commercial premises, and industrial facility upgrades fall outside this assessment.

Segmentation Overview

- By Product Type

- Building Materials

- Paints and Coatings

- Tools and Equipment

- Decore and Lighting

- Flooring and Tiles

- Plumbing and Electrical

- Others

- By Project Type

- Renovation

- Remodelling

- Maintenance & Repair

- By End User (Value)

- DIY

- DIFM / Professional Installation

- By Distribution Channel

- Home Improvement Stores

- Specialty Stores

- Online

- Others

- By Geography

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured questionnaires with building-material suppliers, DIY chain managers, licensed contractors, and regional planners helped us test average ticket sizes, labor availability, and VAT policy impacts across Hanoi, Ho Chi Minh City, and emerging Tier-2 towns. Follow-up calls ensured regional nuances, especially rising DIFM demand among time-pressed middle-income households, were accurately captured before modeling.

Desk Research

We began with statutory data sets from the General Statistics Office, Ministry of Construction housing surveys, and Vietnam E-commerce Association sales audits, which outline dwelling stock changes, renovation permit counts, and online basket trends. Trade associations such as the Vietnam Association of Building Materials and the Vietnam Retailers Association supplied quarterly price and channel splits, while peer-reviewed articles on urban "tube-house" retrofits enriched our understanding of project archetypes. To validate corporate footprints, our analysts tapped paid databases like D&B Hoovers for revenue cuts and Dow Jones Factiva for press coverage on store roll-outs. The sources cited are illustrative rather than exhaustive; many additional documents were reviewed during data gathering.

Market-Sizing & Forecasting

A top-down build began with residential stock, urban household formation, and average renovation spend. These were multiplied through project-type penetration rates, reconstructed from permit data and supplier sales splits, and then adjusted with building-material price indices. Bottom-up cross-checks sampled ASP × volume from five leading home-center chains and served as guardrails, narrowing variance to ±5 percent. Key drivers modeled include disposable income per capita, VAT incentives on construction inputs, e-commerce share of DIY sales, smart-home device uptake, and cement-steel price correlation. Forecasts to 2030 employ multivariate regression blended with scenario analysis for material-cost shocks, with inputs and elasticities vetted during expert calls.

Data Validation & Update Cycle

Every dataset flows through variance and outlier flags before senior analyst sign-off. Mordor refreshes each model annually, revisiting key assumptions on macro data releases; interim events such as subsidy changes trigger targeted revisions. A final pre-publication sweep guarantees clients receive the latest calibrated view.

Why Our Vietnam Home Improvement Baseline Commands Reliability

Published market values often diverge because firms pick differing scopes, price-index bases, and refresh cadences.

Key gap drivers include whether do-it-for-me labor is fully costed, if small hardware purchases are captured, and how currency swings are handled when imports dominate fittings. Mordor's model anchors on a consistent 2024 dong baseline and rolls forward unit costs quarterly, whereas several publishers freeze prices for the whole forecast or exclude cash DIY purchases captured by Vietnam's VAT portal.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.21 B (2025) | Mordor Intelligence | - |

| USD 3.12 B (2024) | Global Consultancy A | Excludes informal cash DIY sales and updates biennially |

| USD 3.20 B (2024) | Industry Association B | Uses supplier shipment value, not installed value, and omits small-ticket décor |

| USD 5.00 B (2023) | Trade Journal C | Aggregates furniture retail with renovation spend and assumes 8 percent annual growth flat across segments |

In summary, by grounding every figure in auditable residential-stock math, validating with channel checks, and refreshing variables quarterly, Mordor Intelligence delivers a balanced, transparent baseline trusted by decision-makers planning Vietnam renovation investments.

Key Questions Answered in the Report

What is the current valuation of the Vietnam home improvement market?

The Vietnam home improvement market size stood at USD 3.91 billion in 2026 and is projected to reach USD 4.72 billion by 2031.

Which product category leads spending?

Building materials dominate with 43.33% of 2025 revenue, reflecting ongoing social-housing and infrastructure projects.

How fast is online retail growing in this sector?

Online retail sales are increasing at a 7.33% CAGR to 2031 as platforms like Shopee and TikTok Shop expand reach.

Which region in Vietnam offers the highest growth potential for home-improvement vendors?

Central Vietnam shows the fastest growth with an 8.85% CAGR through 2031, driven by new industrial investments and infrastructure upgrades.

What is the outlook for DIY activity?

DIY projects are expected to rise at an 8.73% CAGR through 2031, propelled by e-commerce accessibility, instructional content, and cost-saving motivations.

Page last updated on: