Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 60.16 Billion |

| Market Size (2031) | USD 77.62 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

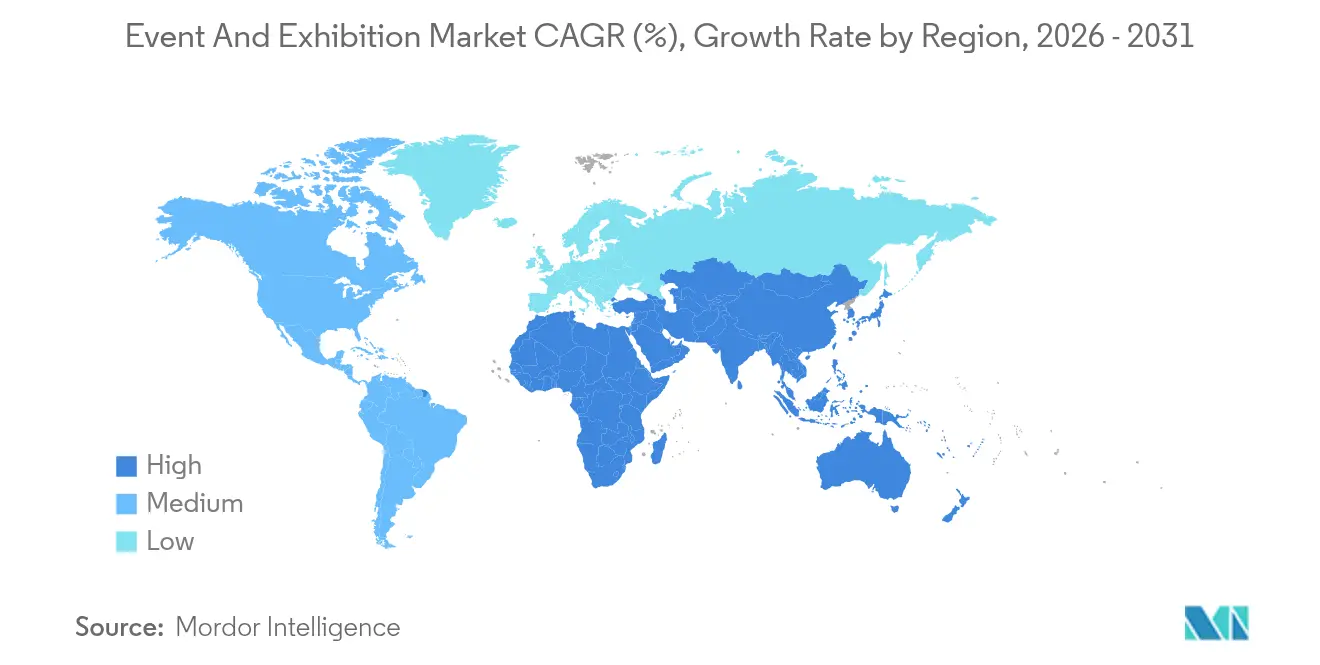

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Event And Exhibition Market Analysis by Mordor Intelligence

The Event And Exhibition Market size was valued at USD 57.17 billion in 2025 and estimated to grow from USD 60.16 billion in 2026 to reach USD 77.62 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031).

Corporate budgets, hybrid-format adoption, and sustainability mandates jointly sustain demand while reshaping business-event design. Live attendance rebounded in 2024 and early-2025, supported by rising travel spend and venue investments. Technology platforms, especially those embedding AI, now underpin nearly every stage of event planning. Infrastructural build-outs in the Gulf and ASEAN nations increase venue supply, pressuring established Western destinations to innovate. Consolidation among organizers and venue operators accelerates, signaling a shift toward scale-driven efficiencies and tighter supplier ecosystems.

Key Report Takeaways

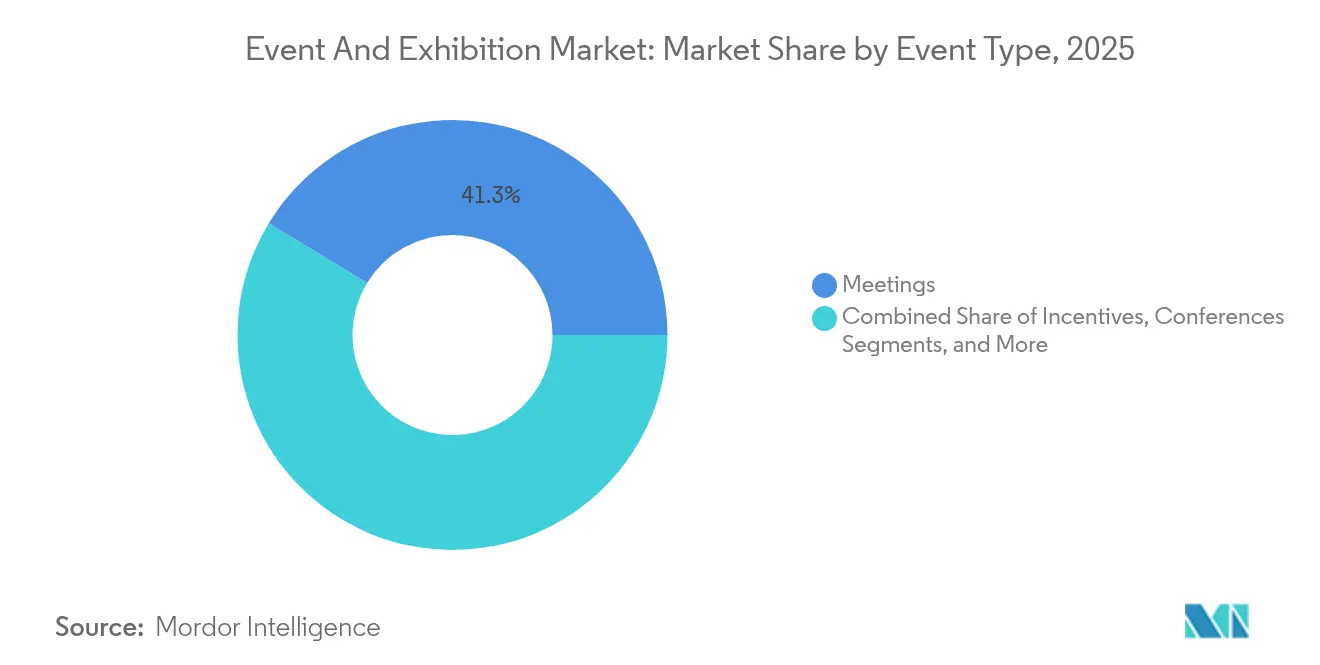

- By event type, Meetings led with a 41.30% MICE market share in 2025; Hybrid/Virtual Events are advancing at a 6.55% CAGR through 2031.

- By service type, Event Planning and Management accounted for 25.55% of the MICE market size in 2025, while Audio-Visual and Technology Services are forecast to grow at 6.78% CAGR to 2031.

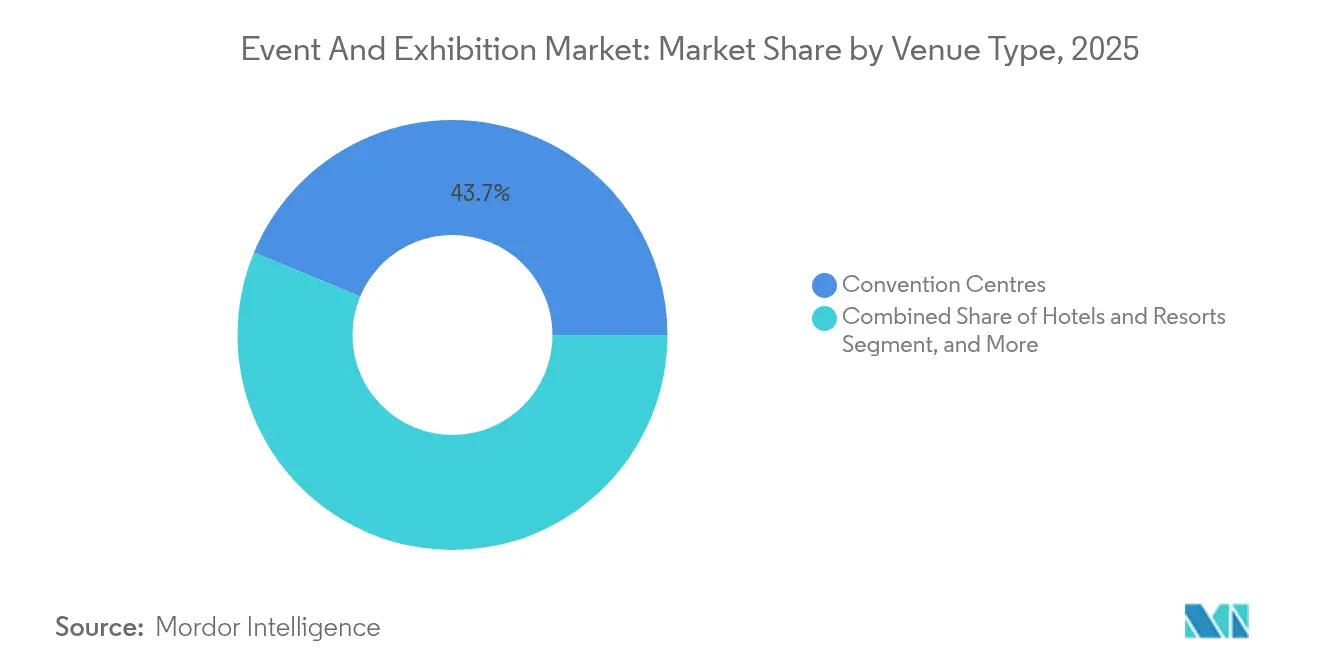

- By venue type, Convention Centers held 43.73% of the MICE market size in 2025; Outdoor/Unconventional Venues are projected to expand at a 6.95% CAGR to 2031.

- By industry vertical, IT and Telecom captured 17.44% of MICE market share in 2025 and is projected to post a 6.22% CAGR to 2031.

- By Geography, North America held 37.60% of global revenue in 2025, whereas the Middle East and Africa region is expected to record a 6.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Event And Exhibition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rebound of in-person business travel budgets | +1.2% | North America and Europe | Short term (≤ 2 years) |

| Corporate sustainability mandates toward carbon-neutral events | +0.8% | Europe and North America | Medium term (2-4 years) |

| Technology-enabled hybrid formats expanding attendee reach | +1.1% | Global | Short term (≤ 2 years) |

| Destination marketing incentives in emerging economies | +0.7% | Middle East and Africa, ASEAN | Medium term (2-4 years) |

| Experiential design demand from Gen-Z/Millennial workforces | +0.6% | Global urban centers | Long term (≥ 4 years) |

| Large-scale infrastructure build-outs in Gulf and ASEAN markets | +0.9% | Middle East and Africa, Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rebound of In-Person Business Travel Budgets

Corporate travel outlays rose sharply during 2024, and 42% of companies budgeted higher spending for 2025 compared with 2024. Conference attendance intentions also improved; 60% of business travelers planned at least one trade-show visit in 2024, reflecting renewed emphasis on face-to-face networking. Longer booking lead times-averaging 53 days for international trips-show planners locking in rates early to manage cost uncertainty. The revived spend broadened demand beyond primary hubs, lifting secondary cities where venue costs remain lower. Resulting volume uplift has already flowed into premium meeting spaces, AV services, and specialized logistics suppliers.

Technology-Enabled Hybrid Formats Expanding Attendee Reach

Organizers have shifted from emergency virtual solutions to implementing mature hybrid strategies. Virtual platforms are increasingly being adopted, driven by advancements in AI-powered matchmaking and content personalization, which significantly enhance attendee satisfaction. Features like real-time translation and AR/VR integrations are breaking down geographic and linguistic barriers, enabling broader audience engagement without substantial cost increases. Sponsors are showing greater interest in premium virtual booths due to their ability to generate valuable, data-driven leads. Hybrid event structures are proving effective in generating additional revenue while aligning with ESG goals and addressing travel budget constraints.

Corporate Sustainability Mandates Shifting Toward Carbon-Neutral Events

ESG compliance evolved from voluntary marketing to formal board-level metric between 2024 and mid-2025. The European Corporate Sustainability Reporting Directive requires Scope 3 emission disclosure, compelling companies to quantify event footprints. ISO 20121 adoption accelerated as planners sought proven frameworks for waste, energy, and community impact management. Venues with on-site renewable energy and zero-waste certifications gained preference, and carbon-offset packages became standard feature sets.[1]MeetGreen, “Carbon Offsets In Event Planning,” meetgreen.com This shift differentiates suppliers that can furnish audit-ready data, turning sustainability into a competitive filter rather than a peripheral add-on.

Large-Scale Infrastructure Build-Outs in Gulf and ASEAN Markets

Dubai committed USD 2.7 billion to enlarge Expo City’s exhibition complex, scheduled for phased completion by 2031.[2]Northstar Meetings Group, “Dubai Exhibition Centre Expo City Expansion,” northstarmeetingsgroup.com Marina Bay Sands’ expansion, entering final design in 2024, will add a 15,000-seat arena and high-end events and exhibition or Meetings, Incentives, Conferences and Exhibitions (MICE) facilities by July 2029. Parallel projects in Beijing and Riyadh multiply available gross floor area, reducing per-square-foot rental costs and inviting global organizers to rotate events away from congested Western centers. Government incentives, such as visa-on-arrival schemes and tax holidays, layer additional attraction for corporate planners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile air-travel and accommodation pricing | -0.9% | Global long-haul corridors | Short term (≤ 2 years) |

| Geopolitical uncertainty and visa restrictions | -0.7% | Europe-Asia routes, United States-China flows | Medium term (2-4 years) |

| Data-privacy and cybersecurity compliance costs | -0.4% | Europe, North America, global roll-out | Medium term (2-4 years) |

| Rising ESG scrutiny on carbon footprints | -0.3% | Europe, North America, Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Air-Travel and Accommodation Pricing

Hotel room rates increased 4.5% per attendee for 2025, while trans-Atlantic business-class airfares rose 4% over 2024 levels.[3]Prevue Meetings, “Per-Attendee Costs to Rise 4.5% in 2025,” prevuemeetings.com Regional disparities complicate planning: Indian metros posted 8.5-9% room-rate growth, whereas some Nordic cities rose 5.6%. Mega-events like Expo Osaka inflate local inventory costs by double-digit percentages, forcing planners to book earlier or compress program durations. These swings prompt higher contingency budgets and encourage hybrid participation models to offset travel spending unpredictability.

Geopolitical Uncertainty and Visa Restrictions

The 2025 launch of Europe’s ETIAS authorization adds time and compliance steps for 30 million annual visa-exempt travelers. Strained United States-China relations sustain trade-policy volatility, discouraging large delegations and complicating sponsorship flows. Rising nationalist rhetoric in several markets heightens last-minute visa rejections, eroding confidence in international attendance. Organizers respond by routing events to politically neutral destinations, or layering virtual tracks to secure participation continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Event Type: Meetings Dominance Challenged by Hybrid Innovation

Meetings delivered 41.30% of 2025 revenue within the MICE market, affirming their central role in decision-making and relationship building. This segment’s stability supports baseline venue occupancy and predictable service demand. Hybrid/Virtual Events, however, are forecast at a 6.55% CAGR through 2031, the fastest among formats. The incremental reach offered by hybrid structures attracts sponsors seeking global impressions without proportional travel costs. Organizers incorporate AI-assisted matchmaking and digital exhibit halls, blending physical engagement with robust data capture. Conferences continue to appeal for content-focused gatherings, while Incentives regain traction as employers emphasize retention. Exhibitions, once volume drivers for large venues, now integrate immersive tech and data-rich lead-gen to remain relevant. The MICE market size for meetings is poised to grow steadily even as hybrid models broaden the ecosystem.

Corporate buyers deploy outcome-based metrics that weigh engagement depth, sustainability performance, and ROI. Hybrid platforms mitigate carbon footprints and budget variability, positioning them as essential complements rather than substitutes. Suppliers that master synchronous physical and digital delivery stand to capture a larger probability-weighted share of upcoming program spend.

By Service Type: Technology Services Accelerate Amid Planning Consolidation

Event Planning and Management providers held 25.55% of 2025 MICE market size, reflecting planners’ need for integrated expertise across venue logistics, compliance, and attendee engagement. Audio-Visual and Technology Services exhibit a 6.78% CAGR outlook to 2031, fueled by demand for high-fidelity streaming, XR experiences, and on-site bandwidth. Venue Rental remains indispensable but faces margin compression as new capacity comes online in emerging regions. Transportation and Logistics suppliers navigate rate volatility, requiring dynamic pricing tools.

Accommodation partners reposition through loyalty integrations and extended-stay packages that dovetail with “bleisure” trends. Food and Catering operators shift menus toward locally sourced and plant-forward offerings to satisfy ESG metrics. Technology overlays, including AI venue-sourcing and predictive analytics, now differentiate full-service agencies. Consequently, service portfolios evolve from siloed line items toward bundled, data-driven platforms optimized for end-to-end event life cycles.

By Venue Type: Convention Centers Lead While Unconventional Spaces Surge

Convention Centers accounted for 43.73% of 2025 MICE market size, reflecting their scale economies and embedded service ecosystems. However, Outdoor/Unconventional Venues are projected to rise 6.95% CAGR through 2031, mirroring corporate appetite for experiential, social-media-friendly settings. Hotels and Resorts leverage embedded lodging to secure multi-day programs, while Corporate Owned Facilities gain renewed investment as cost-control instruments. The MICE market share enjoyed by convention centers could dilute over time as younger audiences favor authenticity and unique aesthetics. Venues therefore upgrade 5G connectivity, modular designs, and backstage infrastructure to compete on flexibility. Environmental credentials have become a key selection filter; rooftops, repurposed warehouses, and nature-integrated properties stand out when they demonstrate renewable energy sourcing and smart-waste systems.

Technological readiness is no longer optional. Organizers demand symmetrical 1 Gbps connectivity and native integration with virtual-event software. Properties that cannot deliver tech parity cede demand to adaptable spaces. Consequently, capital expenditure priorities in 2025 focus on fiber backbones, interactive LED installations, and AI-driven crowd-flow analytics.

By Industry Vertical: IT and Telecom’s Dual Leadership Drives Innovation

IT and Telecom secured 17.44% MICE market share in 2025 and is on a 6.22% CAGR track through 2031. Continuous product-cycle launches, developer conferences, and partner ecosystems underpin volume. Healthcare and Pharmaceuticals follow closely, buoyed by continuing-education mandates and R&D showcases. BFSI sponsors programs around fintech and regulatory compliance, though macro-economic uncertainty tempers short-term growth. Automotive and Manufacturing shift content toward electrification and supply-chain resilience. Government and Public Sector gatherings, including the COP 30 Summit, prioritize climate-action deliberations. Cross-industry events emerge around sustainability and digital transformation, highlighting convergence themes. The MICE market size linked to IT and Telecom is primed for further expansion as 5G, AI, and cybersecurity remain headline drivers of enterprise agendas.

Technology firms also act as early adopters of carbon accounting and hybrid architecture. Their requirements cascade through supplier contracts, accelerating the broader market’s adoption of emission-tracking tools and immersive tech layers. Providers that deliver verifiable green practices and robust digital infrastructure stand out when courting tech-sector budgets.

Geography Analysis

North America commanded 37.60% of global MICE market revenue in 2025, supported by mature infrastructure, headquarters concentration, and advanced hybrid adoption. U.S. business-travel spending reached USD 265.5 billion in 2024, or 87% of 2019 volume. Canada’s hotel-construction pipeline expanded 54% year-over-year in 2024, enlarging event capacity. Mexico leveraged proximity and competitive cost structures to draw corporate meetings aimed at Latin-American audiences. Though growth rates are modest, the region retains scale and innovation leadership, offering high-bandwidth venues and seasoned service ecosystems.

Europe remained a pivotal destination derived from historical convention assets and rigorous regulatory frameworks. Sustainability criteria influenced 50% of 2024 planner venue decisions, and Germany topped European meeting-destination rankings. The pending ETIAS requirement adds complexity for non-EU attendees yet promises more secure movement flows. “Bleisure” behavior accelerated, with 60% of visitors extending trips for leisure. The MICE market will likely see stabilized demand across Tier 1 cities, with incremental programs shifting toward carbon-efficient secondary hubs.

The Middle East and Africa region showcased the fastest CAGR outlook at 6.42% to 2031. Dubai’s USD 2.7 billion Expo City expansion and Saudi Arabia’s Vision 2030 venue pipeline expand supply and stimulate competitive pricing. Regional hotel pipelines counted 607 projects and 147,088 rooms as of mid-2025. Incentives and meetings dominated 2024 program mix, yet Retail and Online-Retailer segments posted 145% growth, revealing diversification. Government-backed visa facilitation and destination-marketing funds further propel inbound program volume.

Asia-Pacific’s ASEAN bloc demonstrated robust FDI inflows of USD 230 billion in 2024, reinforcing demand for cross-border corporate events. Marina Bay Sands’ arena expansion promises new large-format capacity by 2029, reaffirming Singapore’s status as a regional hub. China continued to build mega-centers such as Beijing’s International Exhibition Centre Phase 2, yet geopolitical headwinds tempered outbound delegate flows. Overall, the region’s long-term trajectory remains positive, driven by demographic growth and supply-chain diversification.

Regulatory Landscape

Regulation affecting event and exhibition operations increasingly sits at the intersection of cross-border mobility, trade facilitation, and digital compliance for hybrid delivery. In the United States, industry advocacy through the Exhibitions and Conferences Alliance (ECA) points to frictions related to trade and tariff measures, international visa processing, and sustainability goals tied to Net Zero expectations that corporate buyers are embedding into supplier contracts.

In Europe, the European Exhibition Industry Alliance (EEIA) has flagged administrative barriers, including delayed visa approvals and complex A1 form procedures, as a competitiveness constraint for business events. The 2025 rollout of ETIAS adds another authorization step for visa-exempt travelers. On the digital side, the United Kingdom is tightening obligations that directly influence hybrid-event platforms and venue connectivity, including the UK Telecommunications Security Code of Practice (2026, Version 11) and Ofcom activity under the Online Safety Act 2023, including a July 2026 phase focused on transparency and user choice for large online services. These changes raise compliance and cybersecurity requirements for organizers and technology vendors operating across regions.

Value Chain Analysis

The value chain spans event owners (corporates, associations, governments) and organizers, through venue operators (convention centers, arenas, hotels), and a layered services stack that includes planning and management, stand build and production, AV and streaming, event apps and registration, security and access control, catering, freight forwarding and on-site logistics, accommodation blocks, and post-event analytics. Technology platforms increasingly orchestrate workflows end-to-end, tying venue inventory, exhibitor sales, attendee engagement, and ROI measurement into a single operating layer. This structure supports consolidation among agencies, venue managers, and event-tech providers.

Key bottlenecks sit upstream in technology and infrastructure inputs that hybrid formats depend on. Semiconductor and related component constraints flagged by Broadcom in March 2026, including capacity bottlenecks at TSMC and longer lead times for items such as PCBs, can tighten availability and pricing for networking, compute, and on-site production gear used by venues and AV suppliers. On the demand and monetization side, large B2B convenings act as transaction nodes that pull through multiple tiers of the chain, including the 3rd China International Supply Chain Expo (CISCE) hosted by CCPIT in July 2025 with over 6,000 cooperation agreements, and the inaugural WAVES summit in India (May 2025) that facilitated over USD 1.1 billion in media and entertainment deals. Both underscore how exhibitions and summits function as marketplaces for partnerships, procurement, and distribution agreements.

Competitive Landscape

Competitive Landscape

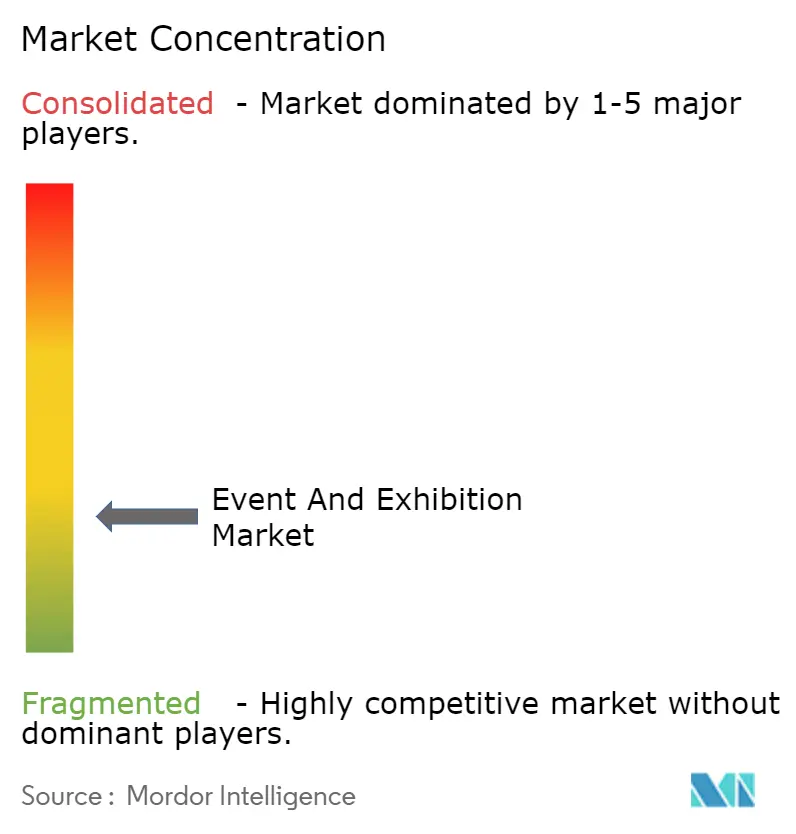

The event and exhibition or the MICE market displayed moderate fragmentation in 2024, yet consolidation advanced briskly. Legends finalized its acquisition of ASM Global in August 2024, creating a venue-management portfolio exceeding 350 venues across five continents. Informa purchased Ascential for USD 1.5 billion, assimilating marquee events such as Money 20/20 and Cannes Lions. Technology providers pursued capability adjacency: Cvent added Prismm’s spatial-design software in April 2025 and QuickMobile’s mobile-app suite in July 2025. Private-equity interest rose, evidenced by Clarion Capital Partners’ August 2025 takeover of Marketplace Events, North America’s largest B2C show organizer.

Competition now tilts toward platform depth and global footprint. Suppliers wielding integrated venue networks, AI planning tools, and audited sustainability credentials secure preferred-partner status among corporate buyers. Regional firms leverage local language fluency, regulatory familiarity, and governmental ties to protect share in emerging markets. White-space opportunities persist in carbon-consulting services and turnkey hybrid-production studios. The interplay between consolidation and tech adoption is likely to reshape bargaining power, nudging the MICE market toward an ecosystem where fewer, larger entities orchestrate increasingly complex event portfolios.

Event And Exhibition Industry Leaders

Informa PLC

ASM Global Holdings Inc.

Messe Frankfurt GmbH

GL Events SA

Reed Exhibitions (RX Global)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity area is deepening the technology layer around hybrid participation, personalization, and measurable outcomes, as adoption has shifted from pilots to broad operational use. In its 37th Global Exhibition Barometer (findings concluded June 2026, released July 2026), UFI reported that 91% of exhibition-industry companies are using AI, indicating a fast-moving baseline where differentiation depends more on integrated data, content, and operations than on standalone tools. That creates room for organizers and venues to standardize AI-enabled matchmaking, translation, content personalization, and automated sales and service workflows across portfolios.

Another visible whitespace is building event formats that sit closer to strategic procurement and infrastructure investment cycles, particularly in telecom and digital infrastructure, where deal-making and ecosystem coordination are central objectives. OFC 2026 in Los Angeles (March 2026) convened about 16,000 attendees and 700+ exhibitors, including NVIDIA, Cisco, and Ciena, around optical networking for AI-era data centers, illustrating how exhibitions are functioning as convergence points for high-value supply-chain alignment. At the same time, the market continues to open capacity and destination options through large venue pipelines in the Gulf and ASEAN (for example, Dubai’s USD 2.7 billion Expo City exhibition expansion plan). This gives organizers more flexibility in redesigning global event calendars and gives service providers a basis to scale operating models across new venues with more consistent digital and sustainability standards.

Recent Industry Developments

- July 2026: Legends ASM Global entered a 15-year venue management agreement (with a 10-year renewal option) covering the Acrisure Amphitheater and Amway Stadium in Grand Rapids, Michigan. The mandate combines venue operations with hospitality delivery under a single operator. This supports the shift toward bundled, multi-venue service contracts that can standardize technology, food and beverage, and commercial programs across assets.

- March 2026: ASM Global partnered with Simpleview to roll out a unified network of websites and related technology across its venue portfolio. The move strengthens digital discovery, booking, and customer experience consistency across venues. It also raises the importance of owned digital channels and data capture for venue operators competing for planners and exhibitors.

- August 2025: Clarion Capital Partners acquired Marketplace Events, expanding its exposure to the consumer-show segment at scale. The transaction adds to consolidation among organizers and owners seeking portfolio efficiencies in marketing, exhibitor sales, and operational procurement. It also increases the ability to invest in shared technology stacks and standardized event formats across multiple shows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the event and exhibition market is defined as the revenues generated from planning, organizing, marketing, and delivering in-person and hybrid events and exhibitions, including exhibitor related and organizer led revenue streams, reported in USD.

Scope exclusions: We exclude pure virtual-only event software subscriptions and general tourism spend that cannot be linked back to a specific event or exhibition.

Segmentation Overview

- By Event Type

- Meetings

- Incentives

- Conferences

- Exhibitions

- Hybrid/Virtual Events

- By Service Type

- Event Planning and Management

- Venue Rental

- Transportation and Logistics

- Accommodation

- Food and Catering

- Audio-Visual and Technology Services

- Other Service Types

- By Venue Type

- Convention Centers

- Hotels and Resorts

- Outdoor / Unconventional Venues

- Corporate Owned Facilities

- By Industry Vertical

- IT and Telecom

- Healthcare and Pharmaceuticals

- Banking, Financial Services and Insurance (BFSI)

- Automotive and Manufacturing

- Hospitality and Tourism

- Government and Public Sector

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To set the boundaries and build the first demand view, we start with public sources that describe exhibition activity and event spending patterns over time. Useful anchors include global exhibition metrics (space sold, exhibitors, visitors) published by associations such as UFI, and US business-to-business trade show tracking (net square feet sold, attendance, exhibitor count, gross revenue) released through IAEE and CEIR. We also review national statistics programs such as the US Bureau of Labor Statistics for employment and wage signals in event-related services, and the US Census Bureau for services and business pattern indicators that help us sanity check the scale.

Next, we layer in operator signals and market context from annual reports, investor presentations, venue operator releases, and reputable press coverage on major show calendars and cancellations. For pricing and company-level revenue indicators, we use paid subscriptions for company financials and news screening, and patent databases when technology enablement trends (ticketing, registration, crowd management) need directional confirmation. The desk inputs are used to shape assumptions and create checkpoints, and this list is not exhaustive because many other sources were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk view and to fill gaps that are hard to observe in public data, especially around organizer revenue mix and how pricing moves with show scale. We speak with organizers, venue operators, service partners, and large exhibitor-side decision makers across Americas, EMEA, and APAC, so regional recovery patterns and event format shifts are reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | APAC: 40% |

| Mid tier: 43% | Functional/Unit leaders: 41% | EMEA: 36% |

| Smaller Players: 19% | Managers: 42% | Americas: 24% |

Market-Sizing & Forecasting

We size the market using a top-down build that reconstructs event and exhibition revenue pools from observable activity signals, which are then converted into value using realistic pricing and revenue-share assumptions. In practice, this means we align the model to indicators such as exhibition space rented, number of events held, exhibitor participation, visitor attendance, and recovery of venue utilization, and then translate them into revenues through inputs like exhibitor fees, sponsorship fees, entrance fees, and organizer services. Because pricing varies by format and region, we also track average booth pricing directionally, sponsorship intensity for large shows, and the share of hybrid events that still monetizes on-site components.

After the top-down totals are formed, we run selective bottom-up checks to confirm the order of magnitude, such as sampling organizer revenues, reviewing venue calendars, and applying sampled average revenue per event across a validated count of major events in key markets. Where smaller local events are not consistently disclosed, we handle the gap by using informed ranges from interviews and adjusting the long tail contribution to fit independent activity signals. For forecasting, scenario analysis is used so the model can reflect different paths for corporate marketing budgets, travel normalization, venue capacity additions, and pricing reset cycles, and then the final path is selected based on what experts see as the most probable near-term operating environment.

Data Validation & Update Cycle

Outputs are checked against multiple independent signals before sign-off, so large swings must be explainable through a clear driver like event count, attendance, or pricing. We run variance checks across regions and revenue streams, followed by an analyst review that looks for abnormal jumps, currency timing mismatches, or double counting between organizer services and exhibitor payments. If a material inconsistency is found, respondents are re-contacted and assumptions are refined, and then the model is re-run so the impact is visible.

Reports are refreshed annually, and interim updates are made when major events occur, such as sharp changes in venue utilization, regulation shifts affecting gatherings, or sudden demand shocks. Before delivery, an analyst completes a fresh pass on key inputs so clients receive an updated view that matches the latest available indicators.

Mordor Intelligence's Event and Exhibition Market Size Measured Against Other Published Estimates

Published market sizes for events and exhibitions often do not match because the boundary around what counts as event revenue is not consistent, and because recovery assumptions after disruption can be treated very differently. In this space, even small choices around what to include as organizer services, or how to treat hybrid formats, can move the total by several billions.

The table shows a spread that mainly comes from scope and conversion choices, including whether adjacent categories like pure virtual platforms and generalized travel spending are folded in, and whether pricing is assumed to rebound quickly or gradually. In Mordor Intelligence's model, revenues are counted only when they are directly tied to event execution and monetization (exhibitor fees, sponsorship, entry fees, and event services), which keeps the total aligned to measurable activity signals like event counts and space sold.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 57.17 B (2025) | |

| Industry Association A | USD 162.00 B (2024) | Uses a broader economic impact style lens that can include exhibitor and visitor spending spillovers beyond organizer revenues, and may combine direct and indirect effects, which inflates comparability with revenue-only models. |

| Trade Journal B | USD 48.90 B (2025) | Leans on a narrower paid-registration and organizer income view, and often applies conservative recovery and sponsorship assumptions, which can understate long-tail and services revenue tied to exhibitions. |

Looking across the three numbers, the key takeaway is that inclusion rules matter more here than any single growth rate assumption. When the scope is kept tied to event-linked revenue streams and validated with activity indicators, the estimate stays traceable and easier to update as calendars, attendance, and pricing shift.

Key Questions Answered in the Report

How large is the event and exhibition market in 2026?

The sector equals USD 60.16 billion in 2026 and is forecast to reach USD 77.62 billion by 2031.

Which region is growing fastest for business events?

The Middle East and Africa is projected to post a 6.42% CAGR through 2031, buoyed by heavy venue investment and destination marketing incentives.

Which event format is expanding quickest?

Hybrid/Virtual Events are set for a 6.55% CAGR, reflecting sustained demand for technology-enabled global reach.

What service category is seeing the highest growth?

Audio-Visual and Technology Services lead at a 6.78% CAGR as immersive and AI-driven experiences become standard.

Which industry vertical spends the most on events?

IT and Telecom holds the largest and fastest-growing share, accounting for 17.44% of 2025 revenue and a 6.22% CAGR outlook.

What key risk should planners watch in 2026?

Persistently volatile air-travel and lodging prices remain the most immediate budgeting challenge, with a projected negative 0.9% drag on global CAGR.

Page last updated on: