Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

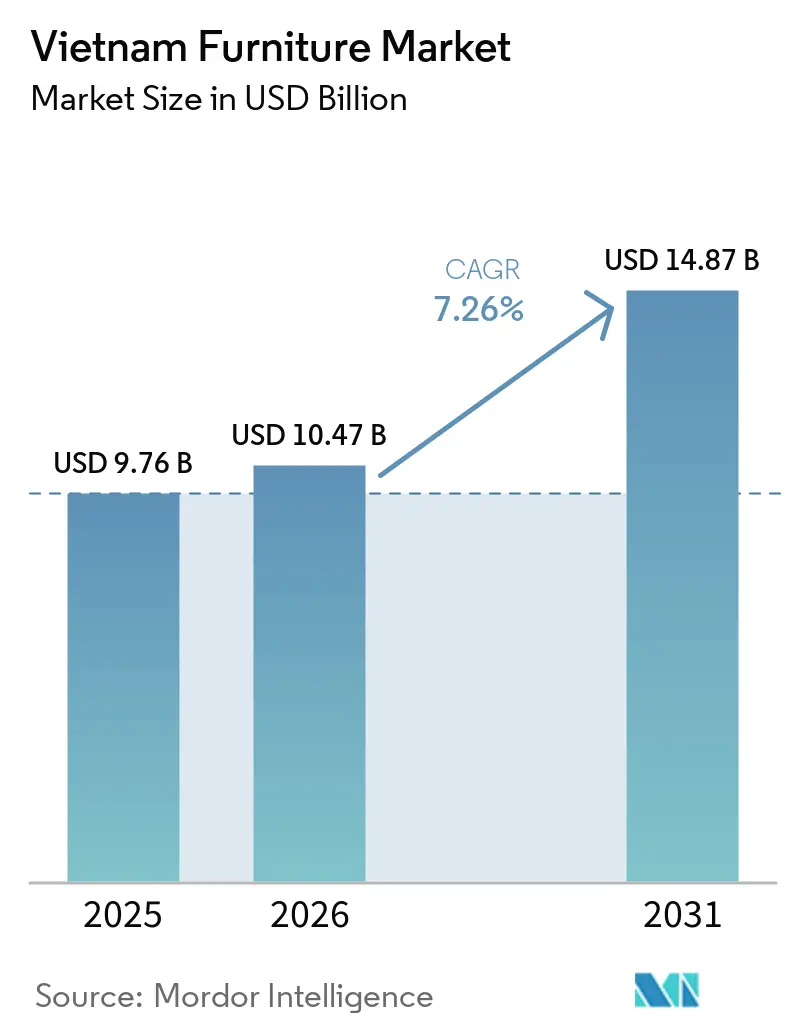

| Base Year Market Size (2025) | USD 9.76 Billion |

| Market Size (2026) | USD 10.47 Billion |

| Market Size (2031) | USD 14.87 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Furniture Market Analysis by Mordor Intelligence

The Vietnam furniture market size is expected to grow from USD 9.76 billion in 2025 to USD 10.47 billion in 2026 and is forecast to reach USD 14.87 billion by 2031 at a 7.26% CAGR over 2026–2031. Vietnam is positioned as a pivotal node in global furniture supply chains, with rankings that now place the country among the top exporters of wood products in Asia-Pacific and worldwide, reflecting strong manufacturing depth and export resilience. Momentum is reinforced by domestic production indicators, with the furniture manufacturing industrial production index up 12.9% in the first quarter of 2025 from a year earlier, which underscores supportive factory utilization and order flows heading into 2026. Export recovery outpaced earlier cycles as 2024 export turnover grew 24.5% year-on-year to USD 13.436 billion, supported by demand normalization in North America and Europe and improved logistical conditions. Structural drivers include preferential trade agreements that eliminate tariffs in the EU and select regional markets, sustained foreign direct investment in processing and manufacturing, and a growing urban middle class that is raising domestic consumption of home furnishings.

Key Report Takeaways

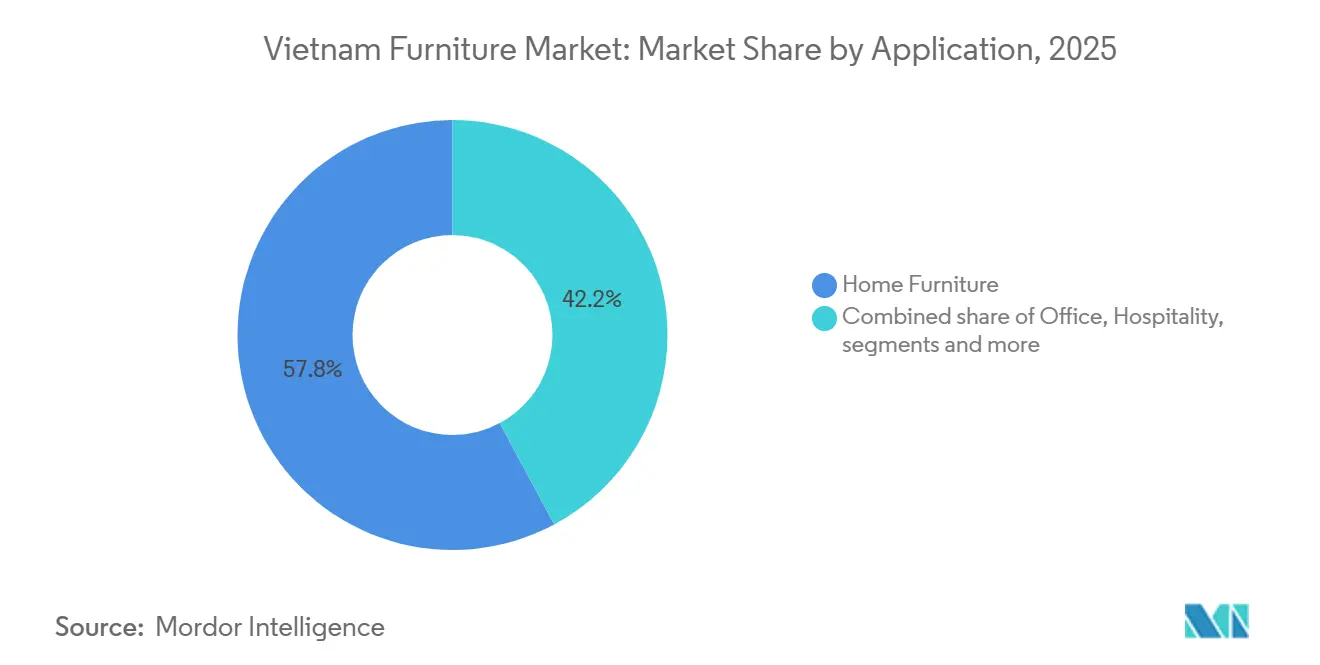

- By application, home furniture led with 57.84% of the Vietnam furniture market share in 2025, and the Vietnam furniture market size for hospitality furniture is projected to grow at 8.76% between 2026 and 2031.

- By material, wood dominated with 68.49% of the Vietnam furniture market share in 2025, and plastic and polymer furniture is projected to expand at 9.48% between 2026 and 2031.

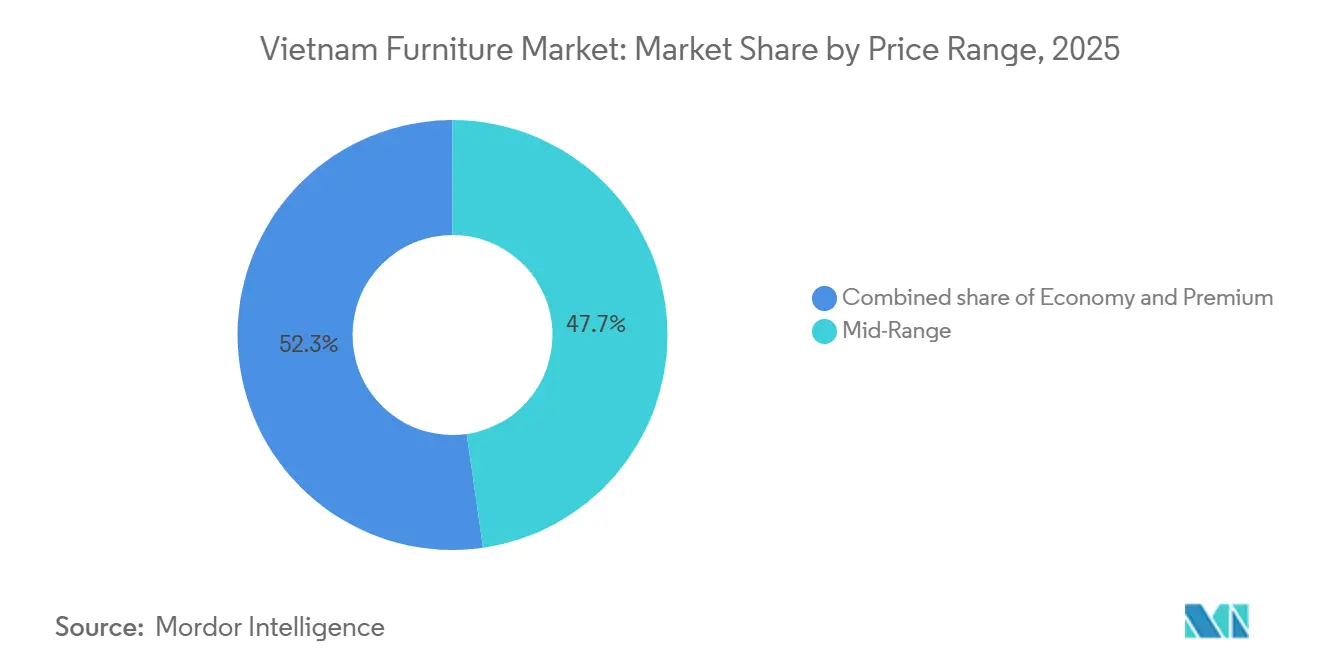

- By price range, the mid-range segment captured 47.74% of the Vietnam furniture market share in 2025, and the Vietnam furniture market size for premium furniture is projected to expand at 8.87% between 2026 and 2031.

- By distribution channel, B2C accounted for 69.84% of the Vietnam furniture market share in 2025. Online retail within B2C is projected to grow at a 10.39% CAGR between 2026 and 2031.

- By geography, Southern Vietnam held 51.76% of the Vietnam furniture market share in 2025, and the Vietnam furniture market size for Southern Vietnam is projected to expand at 9.39% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China+1 Strategy Drives Capacity Additions | +1.7% | National, with concentration in Southern Vietnam (Binh Duong, Dong Nai) and emerging Northern hubs (Hai Phong, Bac Ninh) | Medium term (2-4 years) |

| Urban Consumer Growth, Home Furnishing Upgrades | +1.2% | National, higher in major urban centers (Hanoi, Ho Chi Minh City, Da Nang, Can Tho) | Long term (≥ 4 years) |

| Trade Frameworks Unlock Premium Market Entry | +1.3% | Global export markets (EU, North America, Asia-Pacific), with regulatory influence from EVFTA, CPTPP, and RCEP frameworks | Medium term (2-4 years) |

| Digital Commerce Infrastructure Enables D2C | +1.2% | National, early gains in Hanoi and Ho Chi Minh City, expanding to Tier-2 cities (Da Nang, Can Tho, Hai Phong) | Short term (≤ 2 years) |

| Commercial Real Estate Pipeline Sustains Institutional Demand | +0.8% | National, with concentration in major cities and coastal hospitality destinations, spill-over to secondary urban areas | Medium term (2-4 years) |

| Industry 4.0 Automation Improves Efficiency and Quality | +0.9% | National, led by Southern Vietnam manufacturing clusters (Binh Duong, Dong Nai), expanding to Northern industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

China+1 Strategy Driving Large-Scale Production Capacity Additions

Foreign direct investment is concentrating in processing and manufacturing, with new and additional registered capital of USD 7.97 billion during the first ten months of 2025, representing 56.7% of total FDI, which signals continued capacity additions in wood processing and downstream furniture lines. [1]Source: Ministry of Industry and Trade, “Market Bulletin on Forest Products,” moit.gov.vn A large base of export-ready plants supports this shift, with approximately 1,500 factories exporting and foreign-invested enterprises contributing nearly 40% of export value in 2025, reinforcing the role of multinational capital in scaling productivity and compliance systems. The presence of global operators in Southern and Central Vietnam underscores sustained investment sentiment and links to North American and European retail programs that require stable suppliers and consistent quality standards. Production expansion plans announced in 2025 by leading exporters point to near-term job creation and throughput increases in key clusters such as Binh Duong and Quang Ngai, alongside investments in bonded warehousing and logistics solutions to streamline container flows. Collectively, these initiatives support the Vietnam furniture market by balancing export-led growth with rising domestic demand, while lowering switching risks for international buyers through broader geographic plant footprints and deeper supplier integration.

Growing Urban Consumer Base Driving Home Furnishing and Interior Upgrades

Vietnam’s urbanization rate reached 40% by 2025 and continues to expand at 2.5% to 3% annually, which increases the pool of households purchasing living, dining, and bedroom goods across major cities and emerging urban nodes. [2]Source: General Statistics Office of Vietnam, “Press Release: Socio-Economic Situation in the First Quarter of 2025,” nso.gov.vn The domestic market is benefiting from improved income profiles and a steady flow of new housing, reinforcing retail demand across mid-range and premium price tiers where differentiation is driven by design and materials. E-commerce and digital payments are improving access for consumers outside core urban districts, which helps brands test direct-to-consumer formats while maintaining targeted store footprints in high-traffic locations. The category mix shows stickiness in home furniture staples, while younger cohorts respond to ready-to-assemble options and modular configurations that align with compact urban living spaces and flexible usage requirements. Overall, the urban middle-class dynamic provides a stable backbone of repeat purchases and household upgrades that supports the Vietnam furniture market through cycles, including phases of export volatility.

Multilateral Trade Frameworks Unlocking Premium Market Entry Opportunities

The EU-Vietnam Free Trade Agreement, effective since 2020, removed tariffs on 83% of wood product tariff lines immediately and completed the phase-out of the final 17% by 2025, which allows Vietnamese exporters to ship furniture to the EU at 0% tariffs in 2026. [3]Source: Ministry of Industry and Trade, “Leveraging EVFTA: Vietnam’s Wood Industry Gains Advantage in EU Market,” moit.gov.vn Export momentum into the EU continued in 2025, with year-to-date gains in wooden furniture sales and higher import shares captured by Vietnamese suppliers under preferential access. Regional frameworks complement these advantages, as commitments under RCEP facilitate trade into Japan and Australia for qualified products, reinforcing Vietnam’s role in diversified Asia-Pacific sourcing programs. Preferential access reduces price friction and widens assortments in key import markets that value quality compliance and traceable inputs, thereby supporting steady order allocations to Vietnam across product categories and materials. As a result, trade agreements remain a meaningful tailwind for the Vietnam furniture market, particularly for exporters that combine tariff benefits with strong sustainability credentials and on-time delivery performance.

Digital Commerce Infrastructure Enabling Direct-to-Consumer Distribution Models

Vietnam’s digital economy continued to scale in 2024 and 2025 on the back of expanding e-commerce and logistics infrastructure, which supports online furniture sales across mainstream and premium tiers. Furniture brands are increasing their presence on national platforms and company-owned channels, while optimizing assortment, packaging, and reverse logistics for bulky goods. Cross-border capabilities are also improving, allowing select manufacturers to list directly into regional marketplaces where Vietnamese-made products can compete on price, quality, and lead time. The policy environment supports digital commerce, with national plans encouraging the expansion of the digital economy and the uptake of secure digital payments, which strengthens online conversion rates for durable goods like furniture. This channel shift reinforces the Vietnam furniture market by creating new pathways for consumer reach and by enabling data-led merchandising decisions that support inventory turns and margin control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Raw Material and Logistics Expenses Squeezing Profitability | -1.4% | National, especially Southern export hubs | Short term (≤ 2 years) |

| Stricter US Customs Scrutiny and Anti-Circumvention Measures Elevating Export Costs | -1.8% | Exporters to the US | Medium term (2-4 years) |

| L19: Elevated Real Estate Costs and Disjointed Distribution Networks Limiting Retail Expansion | -0.7% | Urban retail hotspots | Medium term (2-4 years) |

| L20: Evolving Environmental Standards and Trade Regulations Creating Certification Barriers | -0.4% | National, across export compliance frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Raw Material and Logistics Expenses Squeezing Profitability

Vietnam relies on imported timber for higher-grade inputs, with total timber and forest product imports rising in 2024 and reaching USD 1.29 billion in the first half of 2024, which placed upward pressure on material costs for domestic processors. The composition of imports shows a high share of logs and sawn timber, and fluctuations in these categories can influence production schedules and pricing strategies for export contracts. Container shipping volatility compounds cost dynamics, affecting exporters concentrated near Southern ports where throughput is high, and scheduling flexibility is critical. To keep orders, enterprises have absorbed discounts in some export lanes, which narrows margins during tariff and freight spikes and challenges smaller operators with limited working capital buffers. These conditions pressure the Vietnam furniture market’s cost structure, pushing companies to optimize material yields, expand plantation sourcing, and negotiate longer-term contracts with logistics partners to stabilize input and transport costs.

Stricter US Customs Scrutiny and Anti-Circumvention Measures Elevating Export Costs

The US Department of Commerce launched antidumping and countervailing duty investigations on hardwood and decorative plywood from Vietnam in June 2025, citing alleged dumping margins in the range of 138.04% to 152.41% and subsidy rates above de minimis thresholds, which elevate compliance requirements for documentation and verification. The US International Trade Commission issued a preliminary injury determination in July 2025, allowing the investigations to proceed toward scheduled preliminary determinations later in 2025, which sustained risk sentiment among Vietnam-based exporters. Section 232 tariffs imposed in September 2025 include 10% for raw wood and 25% for deep-processed furniture items, with an announced rate increase postponed to January 2027, which affects order pricing and negotiation strategies in 2026. Companies shipping to the United States are reinforcing chain-of-custody systems with self-certification protocols and multi-year records retention to satisfy US Customs and Border Protection verification requirements and to minimize duty exposure. These measures add overhead and process complexity to the Vietnam furniture market, incentivizing investments in traceability, certifications, and compliance training as part of long-term export readiness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Hospitality Leads Growth While Home Furniture Dominates Share

Home furniture accounts for the largest share at 57.84% in 2025, supported by expanding urban households that prioritize living, dining, and bedroom categories, and this share anchors demand stability while the Vietnam furniture market advances into 2026. Office furniture remains the second-largest application by value, with steady demand from corporate users and public sector facilities that favor established casegoods and seating specifications aligned with durability and ergonomic standards. Hospitality furniture is the fastest-growing application with an 8.76% CAGR during 2026 to 2031 as new hotel and resort projects progress across coastal and gateway markets, which increases demand for contract-grade outdoor, lobby, and guestroom furniture. Educational and healthcare furniture respond to public and private capital expenditure cycles, supplying desks, storage, beds, and seating variants for institutional settings where specifications and certification requirements are more stringent. The Vietnam furniture market also scales ready-to-assemble formats for younger urban consumers, which supports value-engineered designs in wood-based panels and mixed materials.

Export composition into the United States shows wood-framed chairs as a leading item by value in 2025, with living and dining room products, bedroom sets, and kitchen furniture also contributing to growing order books, reflecting recovery from the 2023 trough and diversified category momentum in 2024 and 2025. The office category is strengthening after a period of decline earlier in the decade, supported by post-pandemic refurbishment programs and a focus on task seating and modular systems that satisfy hybrid work patterns. Home category upgrades are influenced by urban apartment layouts and storage needs, favoring compact dining, sofa beds, and configurable storage that optimize small spaces without sacrificing aesthetics, which differentiates products in the Vietnam furniture market through practical design. Hospitality’s growth path spans indoor and outdoor applications, with emphasis on resistant finishes, moisture tolerance, and ease of maintenance as tourism continues to normalize across key destinations. Over the forecast period, suppliers that blend compliance, design versatility, and competitive lead times remain well-positioned to capture incremental value in each major application.

By Material: Plastic and Polymer Gain Ground Despite Wood’s Dominance

Wood remains the dominant material with a 68.49% share in 2025, supplied by plantation species such as acacia and rubberwood as well as imported logs and sawn timber, which collectively underpin the Vietnam furniture market’s scale in mass and premium segments. Production data indicate strong activity in early 2025, with industrial forestry indicators rising year-on-year, which supports input availability for manufacturers focusing on export-grade finishing and assembly. Plastic and polymer furniture is the fastest-growing material category at a 9.48% CAGR from 2026 to 2031, reflecting gains in outdoor, hospitality, and value-focused consumer segments where weight, durability, and weather resistance are decisive. Metal-based furniture remains important for commercial and outdoor applications, although price dynamics for steel and aluminum inputs can influence product mix in project channels. Across materials, suppliers are upgrading environmental management and chain-of-custody systems to align with customer and regulatory expectations in export markets, which supports the Vietnam furniture market’s diversification into higher-value products.

Import composition for timber rose during 2024, with logs and sawn timber handling a large share of value, and those shifts required factories to recalibrate unit economics while maintaining on-time deliveries during freight volatility. Companies are investing in environmental certifications, solar power, and biomass consumption to support cleaner operations and cost stability, which strengthens positioning with European and North American buyers that require verified environmental practices. Plastic and polymer advances are supported by new compounds with UV resistance and recyclability features, which broaden outdoor and family-use categories that demand easy cleaning and durability. Material diversification helps the Vietnam furniture market reduce exposure to timber price swings while allowing brands to maintain a price ladder across economy, mid-range, and premium tiers. From 2026 to 2031, suppliers that optimize material sourcing and sustainability credentials are positioned to capture category growth led by wood and accelerated by polymers in targeted segments.

By Price Range: Premium Segment Outpaces Despite Mid-Range Majority

The mid-range segment holds the largest share at 47.74% in 2025, reflecting demand from a growing middle class that values functional designs and reliable materials at accessible prices within the Vietnam furniture market. The premium segment is the fastest-growing price tier with an 8.87% CAGR projected for 2026 to 2031, supported by affluent households, expatriate communities, and commercial buyers specifying higher-end finishes and imported aesthetics. Domestic retail continues to evolve with selective expansion of showrooms and curated assortments that emphasize design, sustainability, and after-sales services that justify higher price points. Participation in global trade fairs and showrooms remains a lever for brand positioning, with Vietnamese exporters showcasing collections to North American and European retailers through national pavilions and category-specific events in 2025. Pricing also reflects certification costs, as sustainably certified wood products typically carry markups that compensate for audit and compliance requirements in developed markets.

E-commerce supports both economy and mid-range growth by allowing direct comparison of specifications and prices, which compresses distribution margins and enables quick testing of new designs at scale. Premium buyers prioritize design houses and curated retail networks that offer customization, modular build-outs, and service packages that include delivery and installation, which raises the value captured in each sale. The Vietnam furniture market is also seeing growth in made-to-order programs for urban apartments and villas, where space optimization and personal style drive higher willingness to pay for bespoke cabinetry and seating. Retail operators are segmenting store footprints by price tier and city zone to balance rent pressure and consumer reach, which stabilizes inventory turnover and working capital needs. Over the forecast horizon, premium outperformance is expected to continue while mid-range remains the volume anchor for the Vietnam furniture market.

By Distribution Channel: Online Retail Surges as B2C Dominates

B2C accounts for 69.84% of value in 2025, reflecting the centrality of home centers, specialty stores, and online platforms in reaching end consumers across major cities and growth corridors, and this share sets the tone for channel strategies in the Vietnam furniture market. Online retail within B2C is the fastest-growing channel at a 10.39% CAGR from 2026 to 2031, driven by wider access to digital payments, logistics improvements, and the scaling of omnichannel capabilities among leading brands. Company networks in Vietnam combine showrooms, supermarkets, and retailer partnerships with e-commerce storefronts, which extend national reach while maintaining service standards that are necessary for large-ticket items. Fragmented domestic retail infrastructure and high urban rents in city cores continue to limit rapid store expansion beyond tier-one locations, which encourages a balanced mix of online-to-offline strategies to protect margins. Project business remains relevant for hospitality, office, and institutional buyers that demand customization, extended payment terms, and compliance documentation, which favors larger integrated manufacturers in the Vietnamese furniture market.

E-commerce expansion is supported by ongoing improvements in regional logistics nodes that enable bulky goods delivery and returns management, which improves customer experience and repeat purchase rates. Brands are rationalizing assortments for online channels, emphasizing SKUs that ship efficiently and survive long-haul handling while still aligning with design trends in key categories. The Vietnam furniture market is also using cross-border e-commerce to reach buyers across ASEAN and Northeast Asia, which reduces reliance on intermediaries and improves speed to market for seasonal collections. Digital marketing and virtual showrooms are now common in the sales cycle for both retail and project buyers, which helps compress discovery timelines and drives higher conversion on curated ranges. Over the next five years, the online channel’s trajectory will remain a defining feature of the Vietnam furniture market as logistics and payments ecosystems continue to mature.

Geography Analysis

Southern Vietnam holds 51.76% of the value in 2025 and is set to grow at a 9.39% CAGR from 2026 to 2031, supported by dense clusters in Ho Chi Minh City, Binh Duong, and Dong Nai that house a large share of wood processing enterprises and integrated exporters in the Vietnam furniture market. Proximity to major ports enables tighter shipping windows and better container availability, which supports export scheduling into the United States and the European Union with lower dwell times. Foreign-invested and domestic manufacturers co-locate with finishing, hardware, and packaging suppliers, which strengthens ecosystem synergies and reduces transport costs within the cluster. Key exporters continue to invest in the south, highlighted by production expansions and logistics improvements announced in 2025, reinforcing the region’s role in export-led growth. The Vietnam furniture market also reflects selective domestic retail expansion in Southern Vietnam, although high rents in core districts temper store count growth and encourage omnichannel strategies.

Northern Vietnam is the second-largest production region, with diversification into bamboo, rattan, and engineered wood, as well as a base of established craft clusters that supply domestic and regional demand. Hanoi provides a consistent market for office, institutional, and premium retail demand, while Hai Phong’s port capabilities support timber imports and exports into Northeast Asia. Competitive labor costs and expanding industrial zones allow new factories to scale operations that serve both the domestic market and nearby export routes. Over 2025 and 2026, enterprises in the north are investing in capacity upgrades and certifications that will improve access to EU and North American buyers under evolving compliance regimes. In the Vietnam furniture market, Northern Vietnam’s mix of raw material access and growing export infrastructure supports a steady contribution to national output despite the south’s scale advantage.

Central Vietnam, including Da Nang, Quang Ngai, and Binh Dinh, is developing as a strategic corridor that links southern and northern supply chains, with Binh Dinh posting USD 1.1 billion in wood export revenue in 2024 and setting a target to double by 2030 under provincial plans. Factories in Central Vietnam benefit from land availability and competitive costs, which attract greenfield investments from Asian manufacturers seeking capacity outside saturated clusters. Investments in the central corridor include new facilities and expansion plans from global exporters, which diversify geographic risk and balance labor availability across regions. Logistics nodes in the central region support regional distribution, which is increasingly important for domestic retail and project deliveries in the Vietnamese furniture market. While distance to major international shipping lanes can present scheduling challenges for time-sensitive export orders, central provinces are closing gaps through continued infrastructure investment and cluster development.

Competitive Landscape

The Vietnam furniture market is moderately fragmented, with an estimated 5,000 enterprises active across the value chain and approximately 1,500 factories dedicated to export, including a significant foreign-invested cohort contributing nearly 40% of export value in 2025. Competition is active across the economy, mid-range, and premium tiers as manufacturers upgrade capabilities in design, finishing, and compliance to match shifting buyer requirements in destination markets. Export-facing firms emphasize vertical integration to gain control over timber sourcing, production, finishing, and logistics, which helps protect margins and quality consistency at scale. Partnerships with major retailers remain a core growth route, and suppliers that meet on-time delivery and sustainability requirements continue to expand allocations in North America and Europe. Digital transformation is progressing, with manufacturers implementing enterprise systems and data tools for production planning, yield optimization, and sales forecasting that enhance competitiveness in the Vietnamese furniture market.

Regulatory developments shape pricing and margin strategies, as Section 232 tariffs on raw and processed goods and ongoing US anti-dumping cases elevate compliance costs and add volatility to negotiated order terms. Exporters are reinforcing traceability and certifications to maintain access to key markets and to align with EU and US requirements, which increases the value of established compliance systems within the Vietnam furniture market. Company strategies in 2025 and 2026 include capacity expansion and product innovation, such as modular seating, motion upholstery, and performance fabrics that serve both residential and contract channels. Select enterprises also deploy capital into environmental upgrades, including solar energy, waste-to-biomass fuel, and ISO-aligned management systems that respond to buyer demands and support long-term operating efficiency.

Notable strategic moves highlight multi-year growth plans and international consolidation. Wanek Furniture, a subsidiary of Ashley Furniture, announced in March 2025 plans to expand Vietnam production capacity by 30% over five years and to build a bonded warehouse in Ba Ria, while targeting a doubling of weekly container exports, which underscores sustained confidence in the Vietnam furniture market. Ashley opened its Wanek Best Private Expo to new partners in February 2025, showcasing modular seating, small spaces collections, and performance fabrics to match retailer demand in North America and beyond. Okamura Corporation moved to acquire Boss Design Limited in April 2025 to strengthen its overseas portfolio, with expected synergies that include broader lounge seating and work booth offerings across Asia and Western markets, where Vietnamese manufacturing can support future sourcing needs. Selected domestic brands expanded retail footprints and strengthened premium positioning through curated showrooms and certified materials, which support brand equity and pricing power in tight urban markets.

Vietnam Furniture Industry Leaders

Duc Thanh Wood Processing JSC

AA Corporation

Kaiser 1 Furniture Industry (Vietnam) Co., Ltd

Tran Duc Furnishings

Cam Ha Furniture JSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: The United States postponed previously announced Section 232 tariff increases on wood items to January 2027, preserving the 10% rate for raw wood and 25% for deep-processed categories in 2026 and providing pricing visibility for exporters.

- April 2025: Okamura Corporation resolved to acquire 100% of Boss Design Limited, enhancing its overseas product lineup with lounge seating, chairs, tables, work booths, and storage, and broadening reach across the UK, EU, US, Japan, and Asia.

- March 2025: Wanek Furniture announced a plan to increase production capacity in Vietnam by 30% over five years and to build a bonded warehouse in Ba Ria, while aiming to double weekly exports from a baseline of 2,400 containers within five years.

- February 2025: Ashley Furniture opened its Wanek Best Private Expo to prospective partners, introducing modular seating, small space solutions, updated sleep lines, and expanded storage and dining options tailored to retailer demand.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Vietnam furniture market as the annual value generated inside the country from design, manufacture, and domestic or export sale of movable household, commercial, institutional, and hospitality furniture made of wood, metal, plastics, and mixed materials.

Scope Exclusion: Built-in kitchens, wardrobes, and fixed joinery that are priced as part of overall construction contracts are excluded.

Segmentation Overview

- By Application

- Home Furniture

- Chairs

- Tables (side tables, coffee tables, dressing tables, etc.)

- Beds

- Wardrobes

- Sofas

- Dining Tables/Dining Sets

- Kitchen Cabinets

- Other Home Furniture (bathroom furniture, outdoor furniture, etc.)

- Office Furniture

- Chairs

- Tables

- Storage Cabinets

- Desks

- Sofas and Other Soft Seating

- Other Office Furniture

- Hospitality Furniture

- Educational Furniture

- Healthcare Furniture

- Other Applications (public places, retail malls, government offices, etc.)

- Home Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B /Project

- B2C/Retail

- By Geography

- Southern Vietnam

- Northern Vietnam

- Central Vietnam

Detailed Research Methodology and Data Validation

Primary Research

To close data gaps, our team conducts semi-structured interviews with furniture manufacturers, export brokers, large home-center buyers, interior designers, and regional e-commerce executives across Ho Chi Minh City, Hanoi, Binh Duong, and Da Nang. The discussions clarify realistic ex-factory prices, production lead times, and penetration of modular and smart designs, allowing us to challenge and refine secondary numbers.

Desk Research

Mordor analysts begin with structured desk work that screens publicly available tier-1 statistics from the General Statistics Office of Vietnam, the Ministry of Industry & Trade trade dashboards, UN-COMTRADE customs flows, and Vietnam Timber & Forest Products Association export briefs. These help us size local production, import substitution, and export momentum. We next mine company filings, prospectuses, and investor presentations to benchmark typical selling prices and channel mixes, while news archives on Dow Jones Factiva and financial snapshots on D&B Hoovers supply timely competitive moves and capacity additions. Finally, peer-reviewed journals and WTO tariff databases let us validate regulatory shock points (for example, EVFTA implementation dates). The sources quoted above are illustrative; many additional references underpin the full evidence set.

Market-Sizing & Forecasting

We initiate a top-down model that rebuilds national furniture output using production indices, export receipts, and import-adjusted consumption, which are then cross-checked with channel sell-through estimates and average selling prices obtained in primary research. Supplier roll-ups on selected wood processors and contract manufacturers provide a bottom-up reasonableness test before final adjustment. Key variables tracked include housing completions, hotel room pipeline, wood-panel price indices, real household disposable income, and container freight rates. A multivariate regression with ARIMA overlays projects each variable to 2030; scenario analysis adjusts for tariff or raw-material shocks. Where respondent-supplied output differs materially from customs data, weighted averages favor the most auditable trail.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, followed by automated variance checks against historical series. Anomalies trigger re-contact of at least one primary respondent. The model is refreshed annually, with intra-year updates when policy or supply-chain events move the market materially.

Why Mordor's Vietnam Furniture Baseline Commands Reliability

Published figures vary because providers choose different boundaries, price bases, and refresh cadences.

Key gap drivers include whether export turnover is blended with local retail sales, the breadth of product classes counted, and the handling of informal cottage production. Mordor reports the full value of furniture manufactured in Vietnam, irrespective of shipment destination, priced at ex-factory level for 2025, whereas some assessments track only domestic retail or capture export FOB values without double-count correction.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 9.62 B (2025) | Mordor Intelligence | - |

| USD 1.49 B (2024) | Regional Consultancy A | Counts domestic retail only; omits export sales and contract manufacturing |

| USD 20.5 B (2025) | Trade Journal B | Uses export turnover and production value, inflating by double-counting intermediate sales |

| USD 0.39 B (2024) | Global Consultancy A | Focuses solely on home-furniture sub-segment, excludes institutional and contract channels |

The comparison shows that when scope and pricing bases diverge, estimates swing widely. Mordor's disciplined variable selection, transparent modeling, and annual refresh give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the Vietnam furniture market size in 2026 and its growth outlook to 2031?

It is USD 10.47 billion in 2026 and is projected to reach USD 14.87 billion by 2031 at a 7.26% CAGR, reflecting continued expansion across export and domestic channels.

Which segments lead the Vietnam furniture market by application and material?

Home furniture leads by application with 57.84% share in 2025, while wood leads by material with 68.49% share in 2025, supported by plantation species and imported inputs.

How are trade agreements influencing the Vietnam furniture market in 2026?

EVFTA provides 0% tariffs into the EU and RCEP commitments support regional access, improving price competitiveness and share capture for compliant exporters.

What risks are Vietnam’s furniture exporters monitoring for the U.S. market in 2026?

Section 232 tariffs and ongoing U.S. anti-dumping and countervailing duty investigations increase compliance costs and require robust traceability and documentation.

Which channel is growing fastest in the Vietnam furniture market?

Online retail within B2C is the fastest, advancing at a 10.39% CAGR through 2031 as brands scale omnichannel capabilities and logistics improve.

Which region holds the largest share within Vietnam and how fast is it growing?

Southern Vietnam holds 51.76% share in 2025 and is projected to grow at 9.39% CAGR through 2031, anchored by industrial clusters and export infrastructure.

Page last updated on: