Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.72 Billion |

| Market Size (2026) | USD 3.85 Billion |

| Market Size (2031) | USD 4.57 Billion |

| Growth Rate (2026 - 2031) | 3.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Fertilizers Market Analysis by Mordor Intelligence

The Vietnam fertilizers market size was valued at USD 3.72 billion in 2025 and estimated to grow from USD 3.85 billion in 2026 to reach USD 4.57 billion by 2031, at a CAGR of 3.50% during the forecast period (2026-2031). Vietnam benefits from a domestic urea surplus, strong government modernization programs, and growing exports to Cambodia, South Korea, and the Philippines. Competitive pressure comes from logistics inflation and a new 5% VAT that changes cost dynamics, yet the tax credit mechanism ultimately favors local producers[1]Source: Ministry of Finance, “Tax Policy and VAT Implementation Guidelines 2025,” MOF.GOV.VN . Precision-fertigation systems and specialty fertilizer demand for high-value export crops are driving technology investment, while counterfeit imports and dependence on potash and DAP continue to weigh on margins. Meanwhile, aggressive capacity additions by domestic leaders and alliances with global distributors strengthen Vietnam’s role as a regional fertilizer hub.

Key Report Takeaways

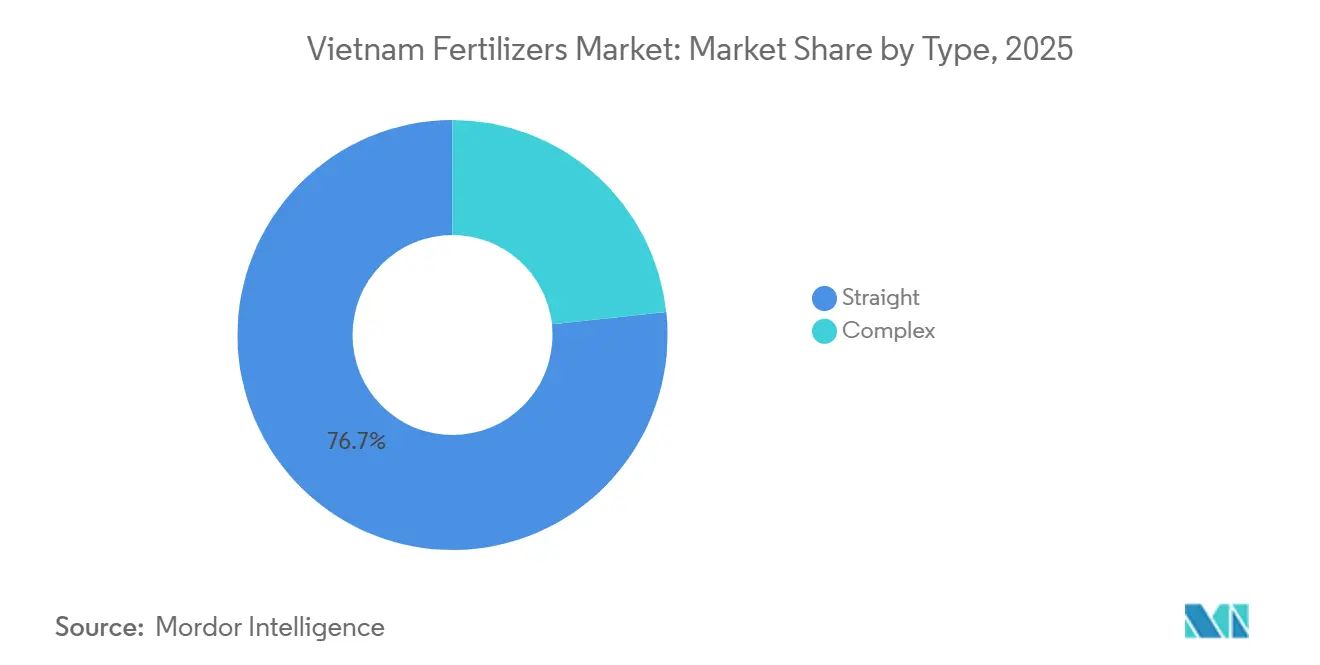

- By type, straight fertilizers held 76.7% of the Vietnam fertilizers market share in 2025 and are projected to expand at a 3.4% CAGR to 2031.

- By form, conventional products accounted for 68.2% of the Vietnam fertilizers market size in 2025, while specialty formulations recorded the fastest growth at a 3.6% CAGR through 2026-2031.

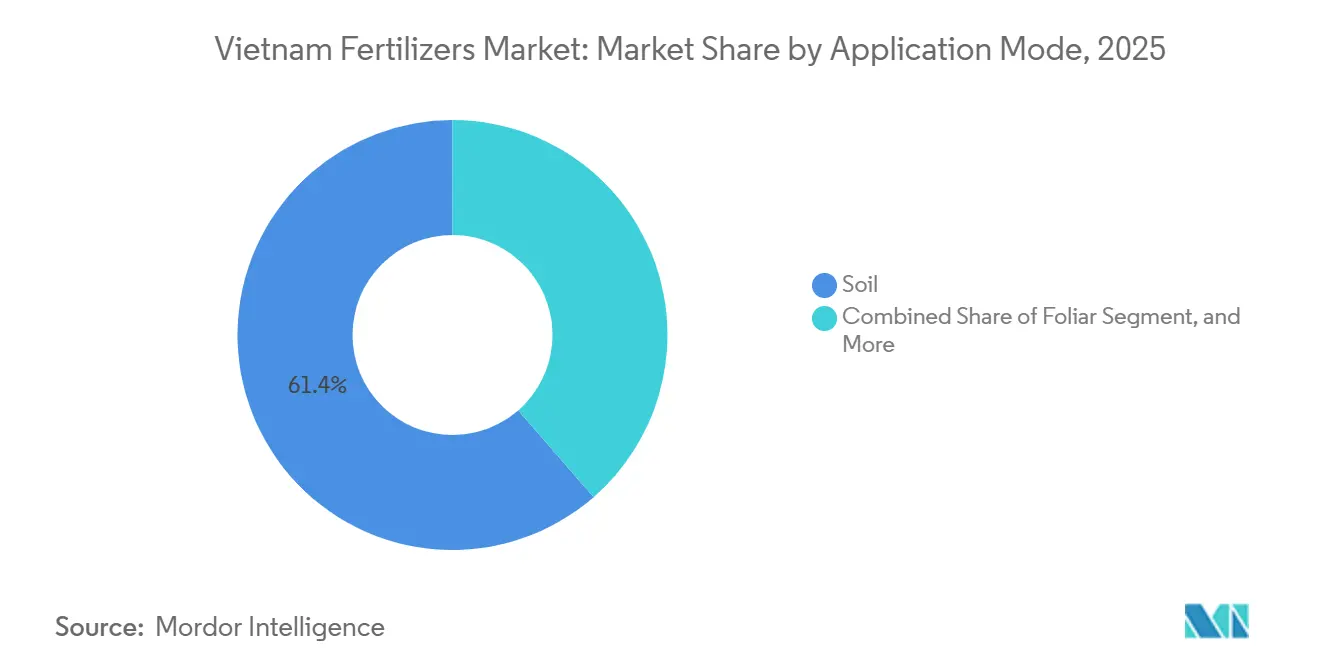

- By application, soil application accounted for 61.4% of the market share in 2025, yet fertigation is growing at a 3.6% CAGR through 2026-2031.

- By crop type, field crops captured 44.6% of the market revenue in 2025, whereas turf and ornamental applications are forecast to rise at a 5.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surplus domestic urea driving export push | +0.6% | National export corridors to Cambodia, South Korea, Philippines | Medium term (2-4 years) |

| Pending 5% VAT credit lowers local production cost | +0.4% | Nationwide | Short term (≤ 2 years) |

| Shift to specialty grades for high-value export crops | +0.5% | Mekong Delta, Red River Delta | Long term (≥ 4 years) |

| Precision fertigation adoption in Mekong and Red River deltas | +0.3% | Mekong Delta 883,000 ha; Red River Delta 231,000 ha | Medium term (2-4 years) |

| Government organic fertilizer targets (50% area by 2050) | +0.4% | National, early uptake in northern provinces | Long term (≥ 4 years) |

| E-commerce platforms reaching smallholders | +0.2% | Rural areas nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surplus Domestic Urea Driving Export Push

Vietnam produces a urea surplus of about 1.2 million metric tons annually, enabling 2024 exports of 1.73 million metric tons valued at USD 709.91 million, a 11.7% volume jump over 2023. Cambodia absorbed 34.3% of shipments, followed by South Korea at 12.7% and the Philippines at 6.3%. Cost advantages stem from integrated gas-based complexes in Phu My and Ca Mau that secure competitive feedstock pricing. The export momentum spreads freight risk and lifts plant utilization, thus buoying domestic earnings even when local demand moderates.

Pending 5% VAT Credit Lowers Local Production Cost

The implementation of 5% VAT credits in Vietnam's fertilizer market reduces production costs for domestic manufacturers, enhancing their competitiveness against imports. The transition from VAT exemption to a 5% VAT regime, effective July 1, 2025, enables producers to reclaim input VAT on natural gas and equipment. This tax adjustment decreases net production costs compared to imported fertilizers subject to full taxation. While the measure increases working capital requirements, it strengthens profit margins for domestic companies, particularly during peak seasons when diammonium phosphate (DAP) and potash import prices increase.

Precision-Fertigation Adoption in Mekong and Red River Deltas

Government targets for 1 million ha of low-emission rice by 2030 accelerate fertigation. Enfarm Agritech installed 500 IoT soil-nutrient sensors that lowered fertilizer use 30% and lifted coffee yields 30%, generating revenue of VND 1.5 billion (USD 62,500) as of 2025 [2]Source: Enfarm Agritech, “IoT Agriculture Technology Deployment 2024–2025,” ENFARM.VN. VNPT’s (Vietnam Post and Telecommunications Group) digital agriculture platform scales recommendations nationwide, linking sensor data to tailored dosage alerts. Reduced wastage improves profit and mitigates runoff, aligning with emerging environmental rules.

Government Organic Fertilizer Targets

The Vietnamese government implemented the National Strategy for Sustainable Agricultural Development to 2030, with a vision to 2050. The policy aims to convert 50% of agricultural land to organic practices by 2050, which is projected to increase the demand for microbial, composted, and bio-fertilizers. Early adoption is visible in northern provinces where vegetable exports must meet stringent residue norms. Local manufacturers diversify into bio-based lines, leveraging domestic cassava starch and molasses feedstocks. Long-term quotas provide visibility for investors planning capacity additions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics cost for liquids and CRF to remote provinces | -0.4% | Remote provinces, mountainous and island regions | Medium term (2-4 years) |

| Counterfeit and sub-standard imports eroding farmer trust | -0.3% | Border provinces, rural networks | Short term (≤ 2 years) |

| Potash and DAP import dependence exposed to price shocks | -0.5% | Nationwide | Short term (≤ 2 years) |

| Seasonal inventory glut depressing producer margins | -0.2% | National, especially domestic plants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Logistics Cost for Liquids and CRF to Remote Provinces

The high logistics costs associated with transporting liquid fertilizers and Controlled-Release Fertilizers (CRFs) to Vietnam's remote provinces constrain market growth. These costs increase final prices, reduce adoption rates, and restrict market penetration. Vietnam's logistics expenses constitute a significant portion of agricultural business revenue due to infrastructure limitations, supply chain inefficiencies, and dependence on international shipping. Transportation represents 60% of fertilizer logistics costs in Vietnam, compared to the global average of 30%. Ocean freight costs increased from USD 3,000 per container before the pandemic to USD 14,000 in 2024 [3]Source: Vietnam Logistics Business Association, “Supply Chain Cost Analysis 2024,” VLBA.ORG.VN. Additionally, road accessibility to the mountainous Northwest region remains restricted. The temperature-controlled shipping requirements for liquid and controlled-release fertilizers further increase delivery costs, limiting specialty fertilizer adoption beyond the delta regions.

Potash and DAP Import Dependence – Exposed to Price Shocks

Vietnam imports all its potash requirements and depends significantly on imported Diammonium Phosphate (DAP). This reliance on foreign sources of potash and DAP exposes Vietnam's agricultural sector to global market volatility, supply chain disruptions, and cost fluctuations. The Vietnamese market is particularly influenced by the policies and supply chain dynamics of major fertilizer producers, notably China and Russia. In 2024, supply disruptions led to a 48% increase in landed costs, affecting farmers' operational budgets. While Vietnam continues research into domestic phosphate rock processing, commercial production remains a future prospect, leaving the country's fertilizer market susceptible to international price movements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Straight Fertilizers Dominate Traditional Agriculture

Straight fertilizers accounted for the largest Vietnam fertilizers market share of 76.7% in 2025 and are also projected to be the fastest-growing segment, advancing at a CAGR of 3.4% through 2031, driven by cost-sensitive smallholder practices in rice, corn, and sugarcane production. Within this group, urea benefits from strong domestic production economics, whereas DAP and MAP remain import-dependent, adding price volatility. Complex fertilizers account for a smaller slice yet expand faster as plantation operators seek balanced NPK blends with sulfur and micronutrients.

Urea’s accessibility underpins traditional broadcast application, but nitrogen losses through volatilization spur interest in inhibitors and coating technologies. Complex blends are gaining traction among coffee and fruit growers targeting export-grade yields. Micronutrient formulations, though nascent, address zinc and boron deficiencies common in lateritic soils, lifting fruit quality premiums. Continued government education on nutrient stewardship is anticipated to shift volumes toward balanced formulas by decade-end.

By Form: Conventional Products Maintain Market Leadership

Conventional products are the largest segment, accounting for 68.2% of the Vietnam fertilizers market size in 2025, reflecting entrenched distribution networks and familiarity with broadcast tools. Specialty forms posted a 3.6% CAGR through 2031, driven by fertigation and greenhouse growth. Water-soluble crystals and liquid suspensions result in rapid uptake in drip-irrigated tropical fruit orchards, improving nutrient efficiency compared with granular top-dressing.

Controlled-release fertilizers command premium pricing and face steep freight costs to remote provinces, but large coffee estates are willing to pay higher outlays to cut labor costs. Microbial inoculants and humic-enriched liquids address soil health concerns and meet organic certification criteria. As digital platforms expand, specialty suppliers can efficiently serve niche demand, encouraging portfolio diversification among major producers.

By Application Mode: Soil Application Dominates Despite Fertigation Growth

Soil application methods accounted for 61.4% of usage in 2025, consistent with broad-acre rice cultivation and widespread broadcast equipment. Fertigation, which accounts for a small share of total tonnage, is the fastest-growing channel, with a 3.6% CAGR through 2031. Government subsidies for low-emission rice encourage drip and sprinkler retrofits, while high-value fruit orchards adopt venturi injectors for precise dosing.

The cost of installing on-farm water infrastructure remains the primary barrier, especially for fragmented holdings of less than 2 hectares. Demonstrated savings in nutrient use and improved uniformity persuade progressive cooperatives and contract farmers supplying export chains. Foliar feeding remains a niche practice, reserved for micronutrient corrections and stress mitigation during the flowering stages in coffee and pepper.

By Crop Type: Field Crops Lead While Ornamentals Show Rapid Expansion

Field crops are the largest segment and consumed 44.6% of the market share in 2025, with 7.7 million ha of rice as the anchor demand. Corn and sugarcane output also contribute to steady nitrogen and potash requirements. Vietnam's position as a major global rice exporter drives substantial consumption of conventional fertilizers to maintain high agricultural productivity. The Mekong and Red River Deltas, which serve as the country's primary agricultural regions, generate the majority of fertilizer demand. The government provides subsidies and sets yield targets for field crops to promote fertilizer usage, aiming to ensure food security and maintain its status as a significant food exporter.

Turf and ornamental segments are growing fastest at a 5.1% CAGR through 2031, driven by urban landscaping and resort development along Vietnam’s coastline. Golf course expansions in Da Nang and Phu Quoc adopt slow-release turf blends and chelated micronutrients to satisfy aesthetic standards. Horticulture captures premium pricing overseas, incentivizing precise nutrition regimes to meet residue thresholds. Coffee plantations in the Central Highlands integrate micronutrient and organic amendments to elevate cup score, securing higher contracts from specialty buyers. High-value crop cultivation requires advanced fertilization methods, including liquid, water-soluble, and controlled-release fertilizers, which improve efficiency and reduce environmental impact.

Geography Analysis

The Mekong Delta represented a significant share of national nutrient use in 2025, leveraging 2.5 million ha of fertile alluvial plains and year-round canal logistics. Barges ferry bulk urea from Ca Mau downstream to farm-gate retailers at a cost-effective price. Precision-fertigation plots are piloted on 120,000 ha of export rice paddies, aligning with government emission targets.

The Red River Delta covers a smaller area yet registers the fastest rate of technology adoption, with 231,000 ha under water-saving irrigation. Urban proximity to Hanoi creates a niche for organic and premium specialty fertilizers that suit high-margin vegetable and floriculture clusters. Logistics hubs at Hai Phong port ease the flow of potash and specialty raw materials.

The central coastal and highland provinces maintain a stable demand for cassava, coffee, and rubber. Mountainous terrain raises domestic trucking costs, constraining specialty uptake despite coffee’s export orientation. Border districts with Cambodia and Laos serve dual roles as consumption zones and export corridors, with Vietnamese producers capturing more than 30% of Cambodian fertilizer demand in 2024. Government incentives for integrated crop-livestock systems in the Central Highlands encourage the adoption of compost and bio-fertilizers, complementing chemical inputs to improve soil organic matter.

Competitive Landscape

The Vietnamese fertilizer market is moderately fragmented. The top five companies controlled a significant combined share in 2025, led by PetroVietnam Fertilizer and Chemicals Corporation JSC and Binh Dien Fertilizer JSC. State-affiliated firms leverage integrated feedstock links and access to capital, while private players carve niches in specialty and regional markets.

Strategic alliances reshape positioning. Samsung C&T Corporation partnered with PVCFC in September 2024 to expand global distribution and procure raw materials efficiently. PVFCCo’s April 2025 tie-up with TGS aims to develop the green value chain, while a parallel pact with PTSC optimizes coastal logistics. TTC AgriS commissioned two microbial plants in January 2025 to tap the organic premium segment.

Technology is a growing differentiator. VNPT’s national digital platform connects sensor data to nutrient advisories and embeds branded fertilizer recommendations in its dashboard. E-commerce portals reduce channel layers and deliver sealed packs to remote farmers, limiting counterfeits and boosting brand recognition. Compliance with MARD (Ministry of Agriculture and Rural Development) Circular 01/2024 on quality controls favors certified domestic producers, accelerating consolidation through the acquisition of smaller blenders lacking testing resources.

Vietnam Fertilizers Industry Leaders

Agricultural Products and Materials Joint Stock Company

Baconco Company Limited

Binh Dien Fertilizer Joint Stock Company

PetroVietnam Fertilizer and Chemical Corporation

Southern Fertilizer Joint Stock Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Petro Vietnam Fertilizer and Chemicals Corporation (PVFCCo) launched NPK PHU MY 15-15-15+5S+TE SOP fertilizer in Vietnam. This nutritional product aims to support sustainable agricultural practices in the country.

- June 2025: Bulgarian fertilizer manufacturer Agropolychim has initiated construction of a calcium nitrate plant at its Devnya facility near Varna port, with the EUR 40 million (USD 43.2 million) plant having an annual production capacity of 50,000 metric tons. The facility will manufacture various liquid fertilizers enhanced with calcium, sulfur, magnesium, potassium, and micronutrients.

- April 2025: Behn Meyer AgriCare Vietnam initiated its Phase 2 factory expansion in Ba Ria-Vung Tau, Vietnam, with a groundbreaking ceremony that also marked the introduction of new organic fertilizer products Growel M+ for rice cultivation, Minotec Super and Minotec Pro for fruit and vegetable farming, and Gowin for coffee plantations. The expansion aims to meet the growing market demand in Vietnam.

Vietnam Fertilizers Market Report Scope

Complex, Straight are covered as segments by Type. Conventional, Speciality are covered as segments by Form. Fertigation, Foliar, Soil are covered as segments by Application Mode. Field Crops, Horticultural Crops, Turf & Ornamental are covered as segments by Crop Type.Type

| Complex | ||

| Straight | Micronutrients | Boron |

| Copper | ||

| Iron | ||

| Manganese | ||

| Molybdenum | ||

| Zinc | ||

| Others | ||

| Nitrogenous | Urea | |

| Others | ||

| Phosphatic | DAP | |

| MAP | ||

| TSP | ||

| Others | ||

| Potassic | MoP | |

| SoP | ||

| Others | ||

| Secondary Macronutrients | Calcium | |

| Magnesium | ||

| Sulfur | ||

Form

| Conventional | |

| Speciality | CRF |

| Liquid Fertilizer | |

| SRF | |

| Water Soluble |

Application Mode

| Fertigation |

| Foliar |

| Soil |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf & Ornamental |

| Type | Complex | ||

| Straight | Micronutrients | Boron | |

| Copper | |||

| Iron | |||

| Manganese | |||

| Molybdenum | |||

| Zinc | |||

| Others | |||

| Nitrogenous | Urea | ||

| Others | |||

| Phosphatic | DAP | ||

| MAP | |||

| TSP | |||

| Others | |||

| Potassic | MoP | ||

| SoP | |||

| Others | |||

| Secondary Macronutrients | Calcium | ||

| Magnesium | |||

| Sulfur | |||

| Form | Conventional | ||

| Speciality | CRF | ||

| Liquid Fertilizer | |||

| SRF | |||

| Water Soluble | |||

| Application Mode | Fertigation | ||

| Foliar | |||

| Soil | |||

| Crop Type | Field Crops | ||

| Horticultural Crops | |||

| Turf & Ornamental | |||

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Primary Nutrients: N, P and K, Secondary Macronutrients: Ca, Mg and S, Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms