Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.55 Billion |

| Market Size (2026) | USD 5.99 Billion |

| Market Size (2031) | USD 23.58 Billion |

| Growth Rate (2026 - 2031) | 31.55% CAGR |

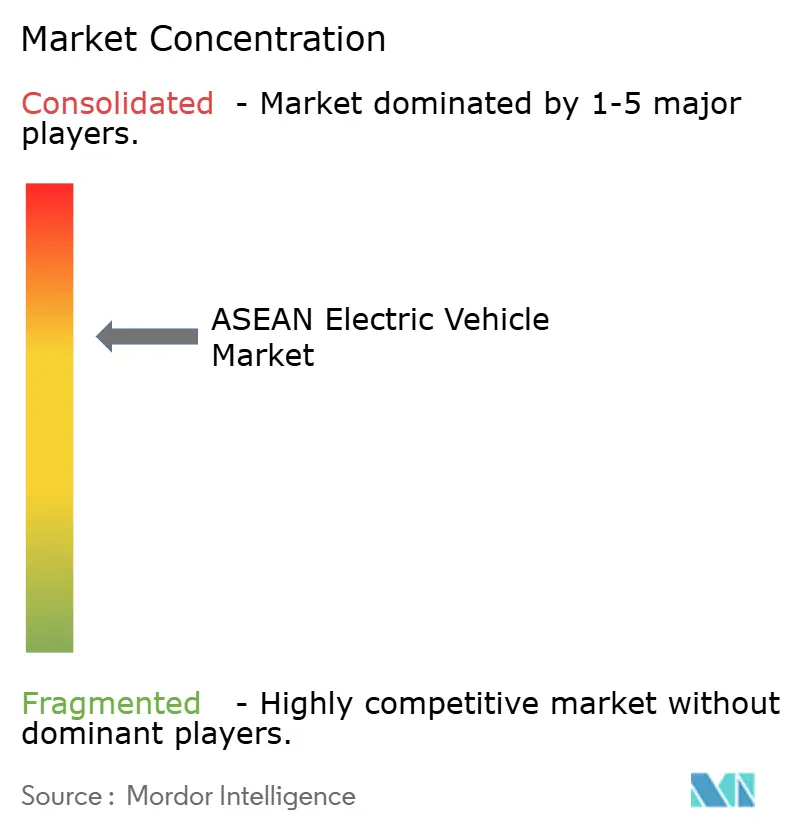

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Electric Vehicle Market Analysis by Mordor Intelligence

The ASEAN electric vehicle market size is expected to grow from USD 4.55 billion in 2025 to USD 5.99 billion in 2026 and is forecast to reach USD 23.58 billion by 2031 at 31.55% CAGR over 2026-2031. Spirited government incentives, abundant nickel reserves that underpin local battery supply chains, and the rapid build-out of public and private charging infrastructure anchor this trajectory. Thailand’s EV3.5 subsidy program, Indonesia’s luxury-tax exemptions, and Vietnam’s multi-year registration-fee waivers widen consumer access while compelling original-equipment manufacturers (OEMs) to localize production. Chinese automakers leverage aggressive pricing and early-mover manufacturing investments to dominate early market share positions while Japanese, Korean, and regional brands accelerate catch-up strategies. Grid integration initiatives under the ASEAN PowerGrid and maturing battery-swap ecosystems for two-wheelers open fresh revenue pools across services, software, and second-life battery streams.

Key Report Takeaways

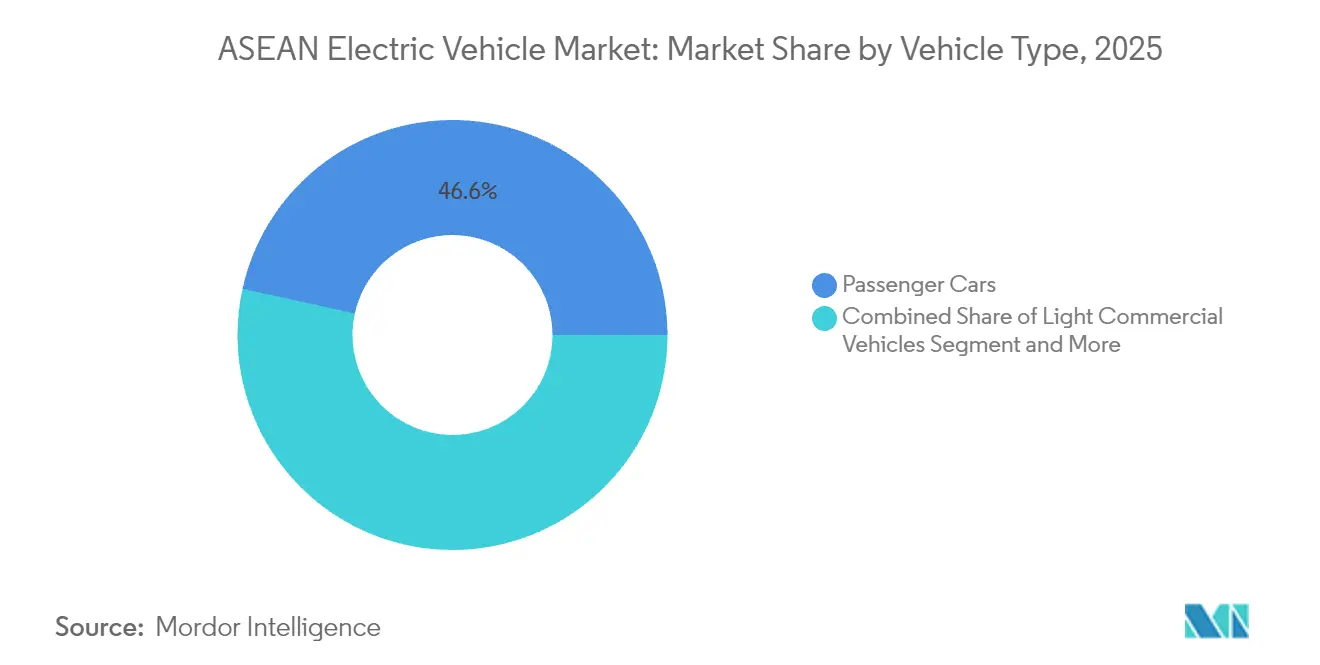

- By vehicle type, passenger cars led with 46.55% share of the ASEAN electric vehicle market size in 2025, whereas two- and three-wheelers are poised to grow at a 32.40% CAGR to 2031.

- By drive-train, battery electric vehicles captured 85.70% share of the ASEAN electric vehicle market size in 2025, while fuel-cell electric vehicles are advancing at a 38.90% CAGR during 2026-2031.

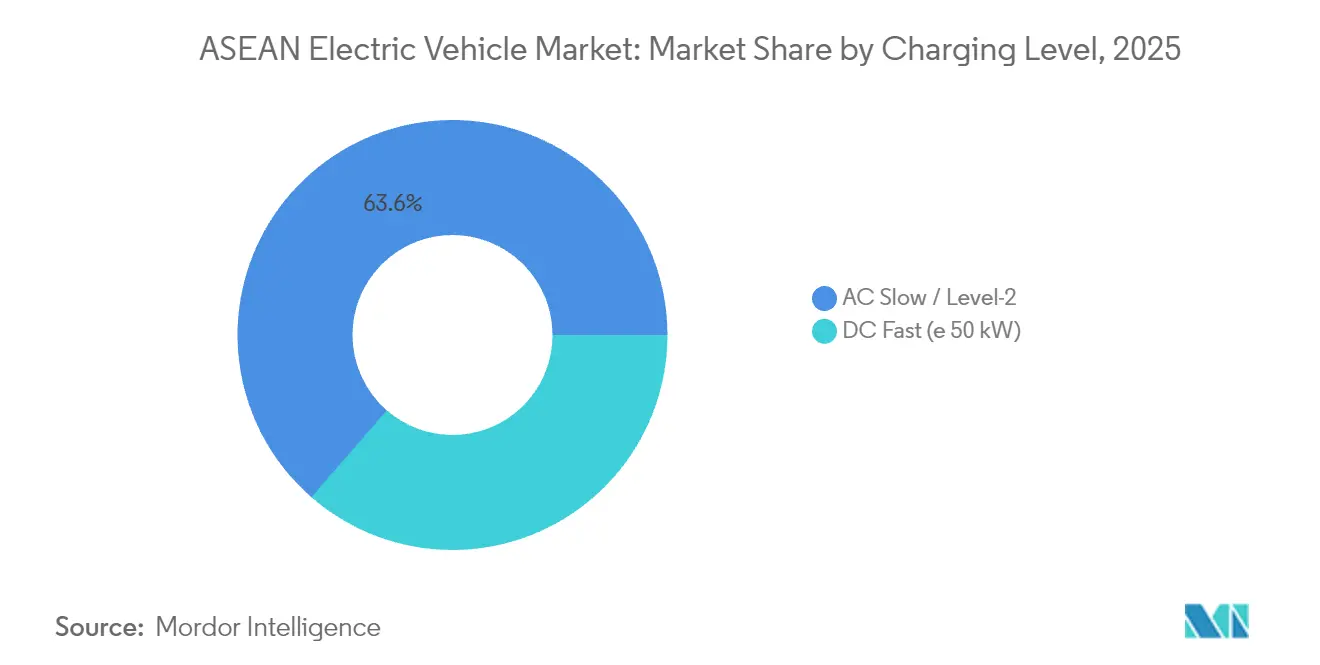

- By charging level, AC slow/Level-2 installations held 63.60% of the ASEAN electric vehicle market size in 2025; DC fast-charging points are forecast to rise at a 32.85% CAGR through 2031.

- By end-user, personal and household customers accounted for 75.10% of the ASEAN electric vehicle market size in 2025, yet commercial fleets are on track for a 33.60% CAGR to 2031.

- By country, Thailand commanded 38.95% of the ASEAN electric vehicle market share in 2025; Indonesia is projected to expand at a 33.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government EV Purchase Incentives | +8.5% | Thailand, Indonesia, Vietnam, Philippines | Short term (≤ 2 years) |

| OEM Localization Commitment | +7.1% | Thailand, Indonesia, Malaysia | Medium term (2-4 years) |

| Rapid DC Charging Rollout | +6.2% | Thailand, Indonesia, Malaysia, Singapore | Medium term (2-4 years) |

| Nickel Battery Supply Advantage | +5.8% | Indonesia, Philippines | Long term (≥ 4 years) |

| Zero-Tariff EV Trade | +4.3% | ASEAN-wide | Short term (≤ 2 years) |

| Two-Wheeler Battery Swap | +3.9% | Vietnam, Indonesia, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Purchase and Excise-Tax Incentives

Aggressive fiscal programs underpin early adoption across the ASEAN electric vehicle market. Thailand channels 34 billion baht in subsidies that require local assembly for eligibility, a policy mirrored by Indonesia’s 0% luxury tax and 1% VAT on battery electric vehicles through 2025. Vietnam has extended registration-fee exemptions until 2027, while Malaysia targets a 20% EV sales mix by 2030 via purchase-tax relief and import-duty waivers. The Philippines mandates a 5% EV share in government and corporate fleets under the Electric Vehicle Industry Development Act, further reducing landed costs through zero-tariff imports. These coordinated instruments have lifted Thailand’s EV sales and turbocharged Vietnam’s electric-motorcycle sales volumes[1]“Vietnam motorbike boom goes electric,” Thanh Niên, thanhnien.vn.

OEM Localization Commitments

The ASEAN electric vehicle market is shifting from import-led to locally manufactured supply. BYD’s USD 1 billion Indonesian hub coming online in late 2025 will produce 150,000 vehicles annually, while Hyundai’s USD 1.55 billion complex near Jakarta adds 250,000-unit capacity. Thailand has secured over USD 3 billion in Chinese OEM pledges, anchored by Great Wall Motor and Chery. VinFast’s outward expansion includes new lines in Indonesia and India, and Geely enters via a joint venture with PT Handal Indonesia Motor to scale 100 retail outlets in three years. These factories meet rising local-content thresholds, compress logistics costs, and seed component ecosystems across batteries, power electronics, and software.

Rapid Roll-Out of DC Fast-Charging Corridors

Charging density moves from bottleneck to catalyst as policymakers and utilities co-invest in public networks. Thailand operates 3,720 public stations as of March 2025 and targets 12,000 by 2030, complemented by 1,450 battery-swap kiosks. Indonesia counts 1,582 public chargers across 1,131 sites after a 157% annual build-out, while home-charger installations climbed 334% to 14,524 units in 2024. Singapore maintains one charger for every three EVs and plans for 60,000 points by 2030, the region’s highest per-capita ratio. Malaysia’s February 2025 guidelines codify technical and safety norms to support 10,000 stations. Vietnam’s VinFast leads with 150,000 ports yet still faces a shortfall estimated by the International Energy Agency at up to 350,000 additional units by 2040 [2]“Global EV Outlook 2024,” International Energy Agency, iea.org.

Nickel-Rich Battery Supply Advantage

Indonesia’s ban on unprocessed ore exports diverts global battery investment toward its domestic refining parks. The country controls about 52% of worldwide nickel reserves and seeks 140 GWh of cell capacity by 2030, aiming for a top-three global ranking by 2027. POSCO’s USD 441 million refinery will launch in North Maluku in 2025, while Zhejiang Huayou Cobalt will replace LG Energy in the USD 7.7 billion Project Titan. Downstream integration shortens lead times, lowers cathode costs, and anchors battery exports to Thailand, Vietnam, and the Philippines. Manila explores similar pathways but weighs the environmental trade-offs of intensified mining against the economic upside.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High EV Price Gap | -4.8% | ASEAN-wide; notably Indonesia, Philippines | Short term (≤ 2 years) |

| Patchy Tier-2 Charging | -3.2% | Indonesia, Philippines, Myanmar, Cambodia, Laos | Medium term (2-4 years) |

| Grid Instability, Peak Loads | -2.7% | Indonesia, Philippines, Vietnam | Long term (≥ 4 years) |

| Diesel Pickup Cultural Preference | -1.9% | Thailand, Malaysia, Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Retail Price Gap Vs. ICE

Entry-level EVs across ASEAN are often priced at twice that of comparable internal-combustion models, curbing mass-market uptake. Indonesia’s penetration reached 9.1% in 1H 2025 despite a 267% sales spike, as the remaining sticker premium deters cost-sensitive buyers. Thailand’s premium-car sub-segment experienced softening demand once incentives tapered, revealing elasticity to subsidy removal. Freight operators highlight elevated upfront costs for medium-duty trucks, even though battery-swap pilots hint at 30-40% lifetime savings. Continual price compression depends on localized battery packs and scale economics from new regional plants [3]“Price gap slows EV adoption in ASEAN,” South China Morning Post, scmp.com.

Patchy Charging Outside Tier-1 Cities

Metropolitan clusters capture most infrastructure investment, whereas rural corridors trail in charger density. Indonesia’s 1,582 public units mainly serve Java and Bali, leaving archipelago provinces underserved. Vietnam’s network remains concentrated in Ho Chi Minh City and Hanoi despite soaring electric-motorcycle adoption, intensifying range anxiety in provincial areas. The Philippines operates 912 chargers for more than 110 million residents and targets 7,300 by 2028, yet execution risks persist around land-use and permitting. Reliability audits show higher fault rates at public-sector stations, underscoring the maintenance burden on cash-strapped local agencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Two-Wheelers Drive Electrification

Passenger cars delivered 46.55% of the ASEAN electric vehicle market in 2025, yet electric motorcycles posted a sales jump in Vietnam in 1H 2025, powered by VinFast’s 488% domestic surge. Two- and three-wheelers are rewriting the growth script, projecting a growth of 32.40% CAGR by 2031. Indonesia and Thailand replicate this momentum through ride-hail incentives that waive parking fees and license-plate charges. The light-commercial segment gains traction as e-commerce fulfillment fleets log 20-30% fuel savings, nudging logistics operators toward electrification mandates. Medium and heavy trucks lag while waiting for higher-density batteries and fiscal levers that neutralize upfront differentials.

Urban delivery riders cite the convenience of battery-swap networks that compress refueling to under two minutes. Vietnam targets 1 million zero-emission motorcycles by 2030, an ambition linked to congestion-charge exemptions in Hanoi. Singapore pilots electric ride-hail permits that prioritize emissions-free vehicles at high-density airport ranks, enhancing driver economics. Buses and coaches benefit from municipal procurement targets, with Singapore aiming for 50% electric buses by 2030 and Vietnam’s Nghe An province mandating fully electric additions from 2025. Collectively, these policies accelerate modal diversification within the ASEAN electric vehicle market.

By Drive-Train Technology: BEV Dominance with FCEV Emergence

Battery electric vehicles maintained 85.70% ASEAN electric vehicle market share in 2025 and anchor most OEM roadmaps through 2031. Lower battery prices, rising energy density, and expanded charging corridors reinforce consumer confidence. Plug-in hybrids carve out a transition niche in Thailand where public skepticism over highway charger availability lingers. Toyota leverages brand equity by bundling home-charger installation and extended warranties, insulating hybrid residual values.

Fuel-cell electric vehicles register the highest 2026-2031 CAGR at 38.90% from a small base. Indonesia’s PLN opened the sub-region’s first hydrogen station in Jakarta in 2024 and plans 22 green-hydrogen plants producing 203 tons yearly. Singapore tests hydrogen buses on dedicated lanes near port zones, and Malaysia’s Petronas evaluates blue-hydrogen blending for commercial fleets. A pan-ASEAN working group is drafting fuel-cell safety codes to align with UN Regulation 134, a prerequisite for scaled imports. This technology pluralism cushions the ASEAN electric vehicle market against raw-material volatility.

By Charging Level: DC Fast-Charging Acceleration

AC slow chargers dominate household and workplace settings but face saturation limits. Their installed base represented 63.60% of 2025 infrastructure, supported by packaged incentives from utilities that discount off-peak energy. Demand for 150-kW and above DC nodes grows as ride-hail, taxi, and intercity bus operators compress turnaround times, propelling a 32.85% CAGR. Thailand prioritizes highway rest-stop rollouts, using grant-matching schemes to attract private capital.

Indonesia’s PLN app integrates charger reservation, payment, and diagnostic alerts, galvanizing user trust. Singapore enforces interoperability through a national backend that pools data from all charge-point operators to optimize future grid upgrades. Malaysia stipulates that new high-rise developments allocate 15% of parking bays to EV charging to avert retrofit challenges. Dynamic-pricing pilots in Thailand’s Provincial Electricity Authority show that time-of-use spreads of 40% between peak and valley can shift 22% of overnight charging load, easing distribution strain.

By End-User Type: Commercial Fleet Transformation

Household buyers captured 75.10% of the ASEAN electric vehicle market size in 2025, thanks to rising model availability and generous incentives. Corporations now accelerate fleet overhauls to hit ESG targets and secure fuel-expense savings, delivering a 33.60% CAGR outlook for commercial segments. Grab and Lazada pilot electric two-wheelers with battery-swap subscriptions that halve operating costs per mile compared with gasoline scooters.

Municipal transit agencies lock in bulk orders for electric buses under sovereign-bond-backed procurement, ensuring vendor financing at favorable rates. The Philippines’ Electric Vehicle Industry Development Act aims a 5% electric share for all government and corporate fleets, creating predictable demand for mid-range sedans and vans. Indonesia showcased 395 electric cars and 90 motorcycles during the 2025 ASEAN Summit, signaling official endorsement. Extended-warranty packages and telematics-based insurance discounts further strengthen the commercial value proposition.

Geography Analysis

Thailand sustains leadership in the ASEAN electric vehicle market, holding 38.95% share in 2025 on the back of its “Detroit of Asia” manufacturing cluster and the EV3.5 incentive that blends subsidies with local-content rules. Domestic sales climbed 40% in 2025, supported by 3,720 public chargers and the goal for 30% of all vehicle production to be electric by 2030. The revised 2025 subsidy now awards 1.5 credits for each exported EV, incentivizing OEMs to leverage Thailand as a regional export hub.

Indonesia shows the steepest trajectory, tracking a 33.10% CAGR through 2031, fuelled by its 52% share of global nickel reserves and a USD 1.3 billion BYD plant coming online in 2025. Policy relief like 0% luxury tax, 1% VAT, and duty-free parts imports persists until the end of 2025. The Indonesia Battery Corporation orchestrates joint ventures that target 140 GWh cell capacity by 2030, elevating the country to a pivotal supply-chain node.

Vietnam leads two-wheeler electrification, with electric-motorcycle volumes up 99.2% in H1 2025. Hanoi and Ho Chi Minh City roll out congestion-zone exemptions and low-interest loans for small-format EVs. Malaysia’s sales jumped from 850 units in 2021 to 14,800 in 2024 due to import-duty waivers and a 10,000-charger roadmap. Singapore posts the highest adoption rate at 19% of new cars in 2023, anchored by dense charging and carbon taxes on high-emission vehicles. The Philippines capitalizes on zero-tariff imports under EVIDA, while Brunei, Cambodia, Laos, and Myanmar craft foundational policies around fiscal stimuli and grid readiness, completing the mosaic of the ASEAN electric vehicle market.

Competitive Landscape

Chinese brands hold a commanding early lead in Thailand’s 2025 battery-electric segment and Indonesia’s first-half registrations. BYD scales rapidly with the Atto 3 and Dolphin models, complemented by Denza for premium buyers. Great Wall Motor introduces the Ora Good Cat, leveraging Thailand’s free-trade zone advantages. Japanese incumbents answer with hybrid-dominated portfolios while fast-tracking dedicated EV lines; Toyota will commence Indonesian production in 2026, and Isuzu readies an electric pickup tailored to Southeast Asian duty cycles.

Strategic alliances shape market positioning. SAIC partners with Huawei on smart-cockpit software to capture digital-native consumers, whereas Hyundai collaborates with LG Energy Solution on integrated battery packs for Indonesian models. Grab’s fleet-electrification accord with BYD secures preferential pricing and embedded telematics, creating a platform lock-in. Battery recycling emerges as a white-space play, with Singapore’s TES partnering with local utilities to pilot closed-loop programs by 2026.

Price competition narrows margins, prompting OEMs to layer subscription-based services such as autonomous-driving over-the-air updates and energy-management apps. Regulatory convergence across ASEAN on safety and emissions standards lowers certification costs but raises compliance thresholds, favoring capital-rich players. Scale efficiencies, localized chemistries, and digital ecosystems thus converge to redefine winners in the ASEAN electric vehicle market.

ASEAN Electric Vehicle Industry Leaders

BYD Co. Ltd.

SAIC Motor / MG Motor

Hyundai Motor Company

Wuling Motors

VinFast Auto Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Proton completes a USD 19.5 million EV line in Tanjung Malim, Malaysia, with 20,000-unit annual capacity expandable to 45,000.

- August 2025: NIO debuts in Singapore and schedules its Firefly right-hand-drive hatchback for early 2026 rollout.

- July 2025: Toyota confirms first Southeast Asian EV production at its Indonesian facility and will begin producing electric vehicles with the bZ4X model in Indonesia by the end of this year.

- August 2024: Hyundai commits 1 billion baht (USD 28 million) to a Thailand plant slated for 2026 production under the EV3.5 scheme.

ASEAN Electric Vehicle Market Report Scope

An electric vehicle is powered by an electric motor instead of an internal combustion engine. An electric vehicle uses a large traction battery pack to power the electric motor and must be plugged into charging equipment. Electric vehicles use batteries such as lead acid, nickel metal hydride, and lithium-ion batteries. Lithium-ion batteries are commonly found in electric vehicles due to their excellent energy retention.

The ASEAN electric vehicle market is segmented by vehicle type, drive train technology type, and country. Based on vehicle type, the market is segmented into passenger and commercial vehicles. Based on drive train technology, the market is segmented into a battery, plug-in hybrid, and fuel-cell electric vehicles. Based on the country, the market is segmented into Thailand, Malaysia, Indonesia, Singapore, and the Rest of ASEAN. For each segment, market size and forecast have been calculated based on value (USD million).

By Vehicle Type

| Two and Three Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Buses and Coaches |

By Drive-train Technology

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Hybrid Electric Vehicles (HEV) |

By Charging Level

| AC Slow / Level-2 |

| DC Fast (≥ 50 kW) |

By End-User Type

| Personal / Household |

| Commercial Fleet and Logistics |

| Government and Public Transport |

By Country

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Philippines |

| Singapore |

| Myanmar |

| Cambodia |

| Laos |

| Brunei |

| By Vehicle Type | Two and Three Wheelers |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| Buses and Coaches | |

| By Drive-train Technology | Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) | |

| Fuel-Cell Electric Vehicles (FCEV) | |

| Hybrid Electric Vehicles (HEV) | |

| By Charging Level | AC Slow / Level-2 |

| DC Fast (≥ 50 kW) | |

| By End-User Type | Personal / Household |

| Commercial Fleet and Logistics | |

| Government and Public Transport | |

| By Country | Indonesia |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Philippines | |

| Singapore | |

| Myanmar | |

| Cambodia | |

| Laos | |

| Brunei |

Key Questions Answered in the Report

How large is the ASEAN electric vehicle market in 2026?

The ASEAN electric vehicle market size stands at USD 5.99 billion in 2026, with a forecast 31.55% CAGR to 2031.

What is driving two-wheeler electrification in Southeast Asia?

Battery-swapping networks, supportive fiscal incentives, and high urban motorcycle density push two-wheelers toward a 32.40% CAGR through 2031.

How fast are DC fast-chargers being deployed?

DC fast-charging points are slated to grow at a 32.85% CAGR, underpinned by Thailand’s 12,000-station target and Indonesia’s rapid public-network expansion.

What hurdles still impede mass adoption?

A lingering retail-price premium over ICE models, patchy rural infrastructure, grid-stability concerns, and cultural loyalty to diesel pickups remain key challenges.

Page last updated on: