Vietnam Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

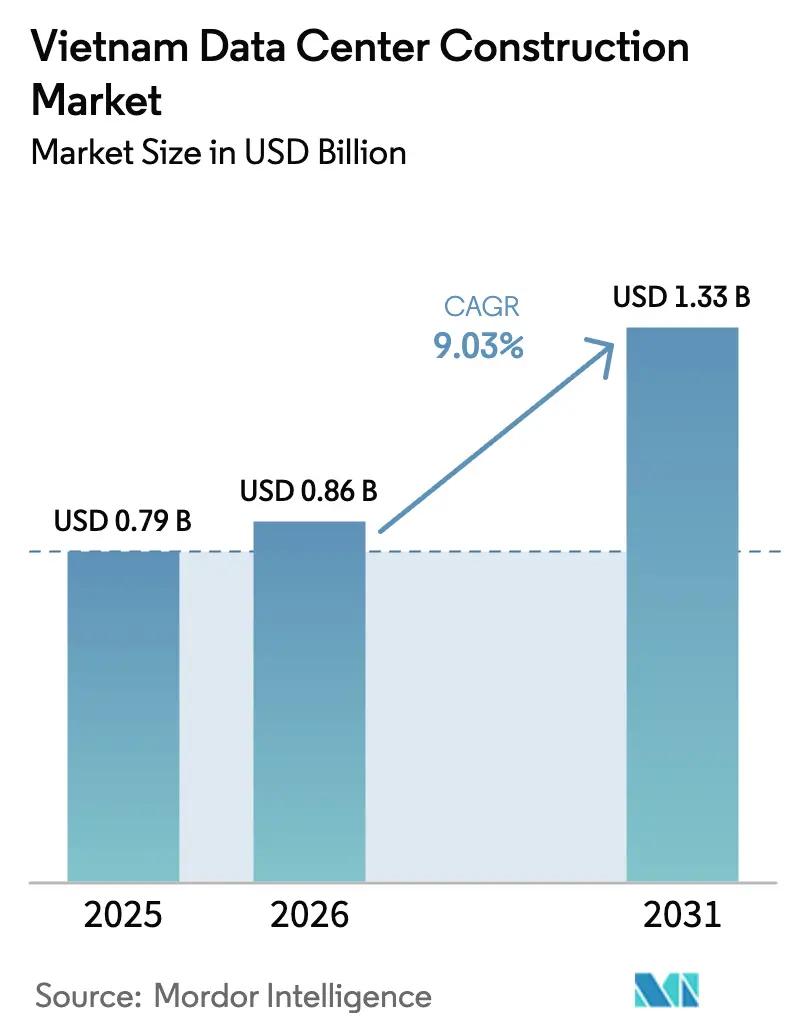

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

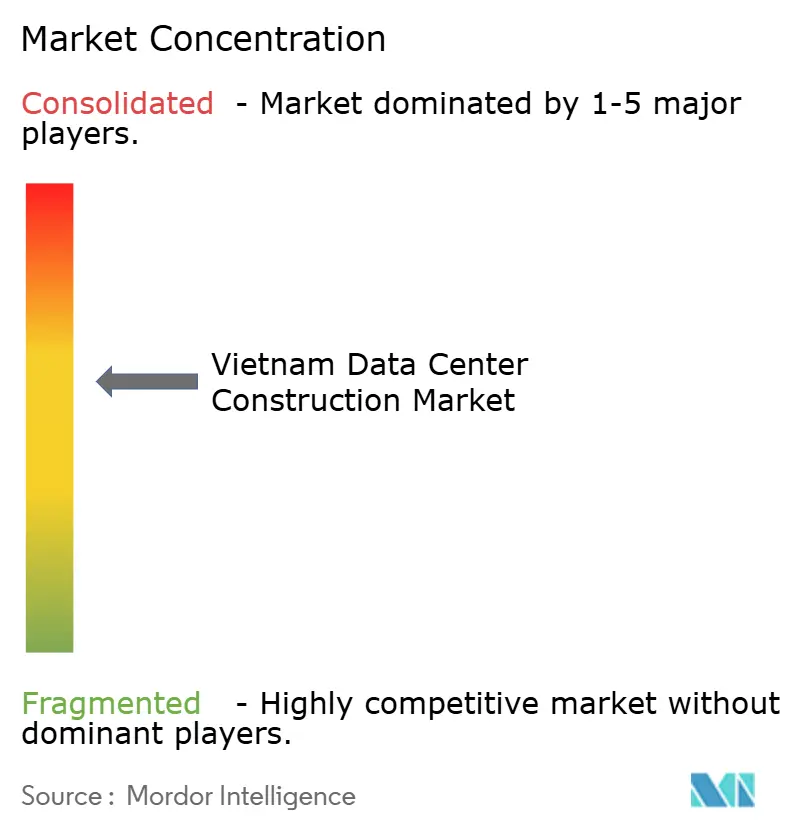

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Data Center Construction Market Analysis by Mordor Intelligence

The Vietnam data center construction market size was valued at USD 0.79 billion in 2025 and estimated to grow from USD 0.86 billion in 2026 to reach USD 1.33 billion by 2031, at a CAGR of 9.03% during the forecast period (2026-2031). Rapid digital-sovereignty regulations, the rollout of renewable power-purchase agreements, and record submarine-cable expansions have combined to position Vietnam as Southeast Asia’s next large-scale hosting hub. A national data center scheduled for completion in late-2025, full foreign-ownership liberalization, and a 50 Tbps Asia Direct Cable now in service collectively lower market-entry barriers while lifting demand visibility. Domestic telcos leverage legacy fiber assets and early‐mover colocation campuses to retain dominant share, yet hyperscalers now deploy self-build facilities to meet localization mandates faster. Investor appetite remains buoyant despite grid-stability concerns because long-term PPAs cut energy-cost risk, while 5G densification pushes compute closer to users and unlocks edge-center opportunities.

Key Report Takeaways

- By tier rating, Tier 3 sites led with 60.75% of the Vietnam data center construction market share in 2025, whereas Tier 4 sites are projected to grow at 11.7% CAGR through 2031.

- By data-center type, the colocation segment held 56.70% revenue share of the Vietnam data center construction market size in 2025, while the self-build hyperscaler segment records the fastest 12.9% CAGR to 2031.

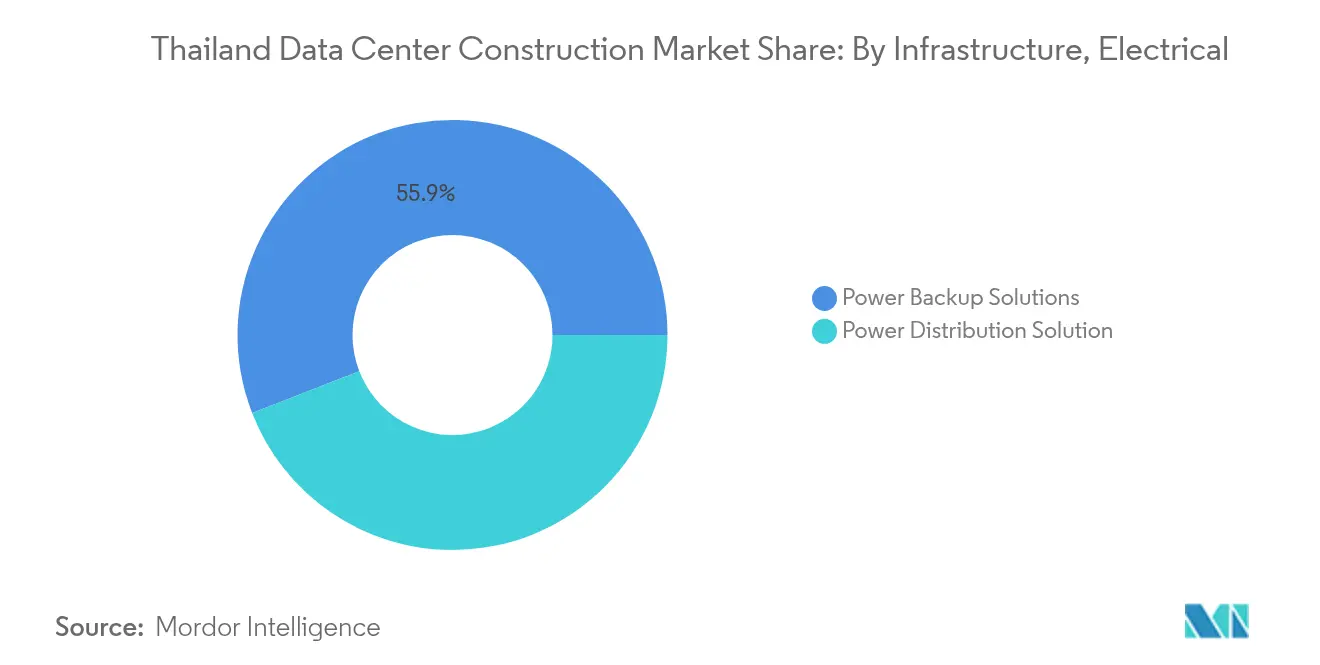

- By electrical infrastructure, power-backup solutions captured 55.90% of the Vietnam data center construction market share in 2025; power-distribution systems expand at 13.6% CAGR during 2026-2031.

- By mechanical infrastructure, cooling systems accounted for 44.85% of the Vietnam data center construction market size in 2025, yet server & storage hardware advances at a 13.9% CAGR to 2031.

- Viettel, VNPT, FPT, and CMC Telecom collectively commanded roughly 96.60% market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-localization mandate (Decree 53) | +2.1% | National, with concentration in Ho Chi Minh City and Hanoi | Short term (≤ 2 years) |

| Cloud and OTT traffic boom | +1.8% | National, with spillover to secondary cities | Medium term (2-4 years) |

| Low power tariffs and renewable PPAs | +1.4% | National, with advantages in renewable-rich provinces | Long term (≥ 4 years) |

| Nationwide 5G + fiber backhaul rollout | +1.2% | National, with early gains in major urban centers | Medium term (2-4 years) |

| Sub-sea cable expansion (ADC2, SJC2) | +0.9% | National, with primary impact on coastal landing points | Short term (≤ 2 years) |

| Green-finance access for "net-zero" DCs | +0.7% | National, with focus on industrial parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Localization Mandate Drives Demand

Vietnam’s Decree 53 and the comprehensive Data Law effective July 2025 oblige global platforms to store designated “important” and “core” data onshore.[1]Hogan Lovells — “Vietnam’s New Data Law Enters Into Force July 2025,” hoganlovells.com Compliance timelines accelerate facility sourcing, evidenced by Alibaba shifting from state-rented racks to dedicated builds. The government-funded National Data Center, due late-2025, sets common security and redundancy baselines that raise enterprise expectations. Google’s plan for its first domestic hyperscale site underlines how sovereignty statutes now dictate footprint strategies. Together these policies create a predictable, captive pipeline for local construction contractors.

Cloud and OTT Traffic Surge Amplifies Infrastructure Needs

Commercial 5G went live nationwide in October 2024 and averaged 247.78 Mbps download by March 2025, enabling UHD streaming and cloud gaming that swell back-end compute demand. Government targets guarantee 200 Mbps fixed speeds for 90% of households by 2025,[2]Developing Telecoms — “Vietnam Targets 200 Mbps Universal Fixed Broadband,” developingtelecoms.com while enterprises gain symmetric 1 Gbps pipes. Viettel’s ongoing 140 MW campus with 60 kW racks epitomizes how service-provider traffic forecasts translate directly into high-density design. Each incremental rise in last-mile capacity multiplies local processing workloads, sustaining utilization rates well above regional averages.

Renewable-Energy Access Transforms Economics

Direct Power Purchase Agreements effective March 2025 permit data-center buyers to source electricity straight from wind and solar producers. Power Plan VIII targets up to 36% renewables by 2030, channeling USD 136.3 billion into grid expansion. Viettel’s Hoa Lac campus secured the nation’s first green credit loan from HSBC, signalling capital-market preference for low-carbon builds nld.com.vn. Regional solar tariffs ranging 1,012–1,383 VND/kWh let operators arbitrage geography for cheaper and greener electrons.[3]Ministry of Industry and Trade — “Solar Tariff Framework 2025,” moit.gov.vnLong-dated PPAs therefore curb OPEX volatility and advance ESG credentials simultaneously.

Nationwide 5G Rollout Creates Edge-Compute Demand

Decree 88/2025 subsidizes carriers installing 20,000+ 5G sites by end-2025, front-loading latency-sensitive use cases. The Science & Technology ministry’s digital infrastructure plan allocates 788 MW total designed capacity by 2030, stipulating green builds that support AI at the edge. As spectrum utilization climbs, content providers shift workloads to micro-edge modules co-located within aggregation nodes, expanding addressable construction beyond primary metros.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High imported CAPEX / OPEX | -1.6% | Stronger effect on foreign builders | Short term (≤ 2 years) |

| Skilled MEP commissioning talent gap | -1.2% | Ho Chi Minh City & Hanoi | Medium term (2-4 years) |

| Grid instability in hydropower-lean seasons | -0.9% | Northern provinces | Short term (≤ 2 years) |

| Speculative AI-DC overbuild bubble risk | -0.8% | Major urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Import Dependency Raises Costs

Vietnam’s semiconductor base still emphasizes design, forcing imports of precision switchgear, chillers, and GPUs, exposing builders to freight surcharges and currency swings. Construction-cost benchmarks issued under Decision 409/QĐ-BXD cannot offset equipment price escalation when global supply tightens. Schneider Electric’s pivot to expand manufacturing in the United States underscores how suppliers are regionalizing, leaving Southeast Asian buyers vulnerable to lead-time gaps

MEP-Skills Shortage Delays Projects

The domestic ICT workforce will be 200,000 specialists short by 2025, with acute deficits in high-density cooling, UPS commissioning, and AI-optimized rack integration. Government program 1002/QĐ-TTg targets skills uplift through 2035, but near-term gaps inflate labor premiums and extend ramp-up schedules. Binh Dinh’s plan to train 7,500 semicon and AI engineers is promising yet insufficient at national scale, magnifying execution risk for concurrent hyperscale builds

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Reliability Push Elevates Tier 4 Growth

Tier 3 sites retained 60.75% market share in 2025 as most enterprises still balance redundancy and capex prudence. The Vietnam data center construction market size for Tier 3 therefore remained largest, while Tier 4 operations set the fastest 11.7% CAGR trajectory into 2031. Investors interpret frequent power-quality incidents as justification for moving workloads to fully concurrent systems, even when capital costs rise. Viettel’s 140 MW Tan Phu Trung campus targets Tier III certification yet benches Tier IV-ready modules for AI clusters, signalling a transitional design mindset.

Higher-tier momentum also mirrors hyperscaler tolerance thresholds; GPU training clusters cannot risk downtime without jeopardizing multi-day job runs. NVIDIA’s memorandum with the Vietnamese government to open an AI R&D center imposes Tier 4 baselines on supply-chain partners. As the Vietnam data center construction market broadens, Tier 4 build-to-suit contracts drive premium service revenues, while Tier 1/2 footprints contract toward dev-test and local-edge use cases.

By Data Center Type: Hyperscaler Self-Build Era

Colocation retained 56.70% share in 2025, anchoring the Vietnam data center construction market. Nonetheless, self-build hyperscale programs clock a 12.9% CAGR as Google, Alibaba, and regional OTT players prioritize full-stack control. Deregulation in 2024 allowing 100% foreign ownership eliminates equity constraints that once steered entrants toward colocation leases.

Joint-venture blueprints remain relevant; STT GDC’s alliance with VNG combines local permits and land banks with international best-practice construction. Yet most hyperscalers favor outright greenfield builds to integrate proprietary network fabrics, specialized security, and custom-AI chip clusters. The trend forces colocation incumbents to chase differentiation via edge-site density, sovereign-cloud tiers, or sector-specific compliance wrappers.

By Electrical Infrastructure: Distribution Overhauls Outpace Backup

Power-backup equipment still comprised 55.90% of Vietnam data center construction market share in 2025 because diesel gensets and UPS strings remain foundational amid grid curtailments. However, Vietnam data center construction market size for power-distribution gear expands at a stronger 13.6% CAGR through 2031, propelled by AI rack densities hitting 60 kW. Schneider Electric and NVIDIA jointly launched reference designs that embed busway-level telemetry and software-defined power quality, redefining distribution architectures.

Hydropower-shortfall episodes saw 11 dams shut units in 2024, cutting 50.8 million kWh supply in single days, underscoring that redundant power paths alone are insufficient without intelligent distribution. Consequently, developers deploy adaptive switchboards, battery-energy-storage systems, and grid-interactive controllers that shave peak and harvest tariff arbitrage. Power-usage-effectiveness targets below 1.4 now hinge more on smart distribution than on backup runtime alone.

By Mechanical Infrastructure: AI-Optimized Servers Gain Ground

Cooling held 44.85% share in 2025; Vietnam’s tropical humidity makes advanced chillers and CRAH arrays unavoidable base cost. Yet servers and storage post the highest 13.9% CAGR as generative-AI pipelines proliferate. Here, the Vietnam data center construction market size rise stems from 8-GPU baseboards and NVMe over-fabric arrays that push per-rack draw sixfold.

Viettel’s upcoming facility integrates back-door liquid exchangers to sustain 60 kW racks without raising white-space temperatures above 27 °C. Off-site examples such as Digital Edge’s PUE 1.193 Manila plant prove tropical AI halls can hit efficiency benchmarks through aisle containment and heat-recovery loops. Vietnamese operators now embed AI-based building-management systems that tune fan curves, thereby shrinking chiller energy by up to 12%, reinforcing the link between mechanical innovation and OPEX competitiveness.

Geography Analysis

Ho Chi Minh City anchors capacity deployment, hosting Viettel’s 140 MW flagship—Vietnam’s first triple-digit-megawatt campus and a top-10 Southeast-Asian facility. Its pull factors include clustered submarine-cable landings, industrial-park land reserves, and a dense digital-economy customer base. Hanoi ranks second; CMC’s USD 300 million CCS complex widens the capital region’s footprint and caters to ministries seeking compliant sovereign-cloud hosting.

Da Nang is maturing as the third node; six active sites now offer 500 racks, and a 1,000-rack expansion broke ground in March 2025, leveraging the city’s ambitions as an international financial center. National cable policy adds up to four new 60 Tbps systems by 2025, dispersing connectivity resilience and enabling secondary-city feasibility. The Asia Direct Cable, live since April 2025, multiplies available international bandwidth, letting operators optimize latency and disaster-recovery topologies across the coastal axis.

Regional differentials in solar PPA tariffs (South 1,012 VND/kWh versus North 1,383 VND/kWh) guide hyperscalers to southern provinces for mega-campuses while encouraging northern builds to over-spec backup and establish renewable microgrids. Consequently, the Vietnam data center construction market exhibits a hub-and-spoke layout in which primary metros host multi-story flagships, and edge clusters fan out along 5G aggregation rings.

Competitive Landscape

Domestic telcos Viettel, VNPT, FPT, and CMC collectively held 97% market share in 2024, supported by legacy fiber backbones and preferential access to government workloads. Foreign-ownership liberalization in 2024 shifts the competitive field; NTT inaugurated Ho Chi Minh City 1 with 6 MW at Tier III and is scouting a second 20 MW. STT GDC partnered VNG to acquire land and start a 120 MW campus, introducing Singapore-grade design standards.

Strategy now pivots on AI readiness and sustainability. Schneider Electric-NVIDIA ecosystems embed liquid cooling and DCIM-with-GPU telemetry, giving early adopters a performance edge. Domestic incumbents retaliate by pre-leasing entire data halls to cloud players on long tenures, locking in revenue while funding efficiency retrofits. Edge-compute specialists emerge to service the 20,000-base-station 5G grid; micro-DC operators pursue <500 kW pods inside industrial parks, meeting ultra-low-latency use cases.

Barriers to entry remain non-trivial: land conversion approvals can stretch 12 months, and talent scarcity inflates commissioning overhead. Yet capital inflows persist as sovereign-cloud certainty offsets execution risk, setting Vietnam’s investment narrative apart from peers facing political volatility.

Vietnam Data Center Construction Industry Leaders

-

Viettel IDC

-

VNPT (VNPT NET + VNPT IDC)

-

FPT Telecom Data Center

-

CMC Telecom

-

NTT GDC Vietnam

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Schneider Electric and NVIDIA launched a global AI-factory partnership with Vietnam earmarked for pilot energy-efficient campuses

- June 2025: CMC began building the USD 300 million CCS Hanoi AI hub spanning 23 floors and 90,000 m²

- May 2025: Ministry of Science & Technology approved a 2025-2030 plan targeting 788 MW designed capacity and 11 new green data centers

- April 2025: Viettel broke ground on a 140 MW Ho Chi Minh City campus, Vietnam’s first >100 MW site, designed for PUE < 1.4

- April 2025: Asia Direct Cable entered service, adding 50 Tbps and eclipsing cumulative existing overseas bandwidth.

- March 2025: Decree 57/2025 enabled direct renewable PPAs, unlocking long-term price stability for data-center operators.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Vietnam data center construction market as all capital expenditure outlays needed to erect greenfield or brownfield data center buildings, covering electrical fit-outs, mechanical systems, racks, and core civil works that bring a facility to "powered shell" readiness.

Scope Exclusions: Land acquisition costs and the purchase of IT equipment such as servers or network gear fall outside this boundary.

Segmentation Overview

-

By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

-

By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

-

By Infrastructure

-

By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

-

By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

-

By Electrical Infrastructure

Detailed Research Methodology and Data Validation

Primary Research

Interviews were held with project managers at local engineering, procurement and construction firms, design consultants, facility operators, and regional colocation buyers across Ho Chi Minh City, Hanoi, and Da Nang. Their insights on current price per megawatt, tier-upgrade premiums, and lead times enabled us to confirm secondary numbers and refine forecast assumptions.

Desk Research

We gathered baseline figures from open government portals such as the General Statistics Office of Vietnam, the Ministry of Information and Communications, customs shipment records, and power-grid data published by Electricity of Vietnam. Trade associations, including the Vietnam Internet Association and the Asia Cloud Computing Association, helped us size typical megawatt additions and average build costs. Our analysts also mined company filings, investor decks, and reputable press releases describing announced hyperscale campuses. To enrich construction benchmarks, we leveraged D&B Hoovers for contractor revenues, Dow Jones Factiva for project news, and Questel for cooling and modular-build patents. This list is illustrative; many additional sources supported data collection and validation.

Market-Sizing & Forecasting

Mordor analysts first reconstructed Vietnam's total spend using a top-down "build cost × commissioned MW" model fed by power-capacity statistics, planning approvals, and average benchmarks. Select bottom-up checks, such as sampling EPC invoices and rack counts, validated the total. Key variables tracked include new megawatts announced, renewable-energy share, tier-mix migration, imported equipment duties, and construction-labor indices. Forecasts for the future are produced through multivariate regression with scenario overlays that test power-price swings and foreign-investment rules, then aligned with sentiment collected in our expert calls. Gaps in individual bottom-up inputs are bridged by applying weighted regional averages from similar Southeast Asian builds.

Data Validation & Update Cycle

Every model run passes variance checks against historical capex bands and independent signals like transformer imports. Outliers trigger peer reviews before sign-off. The dataset refreshes annually and is reread mid-cycle if a material event, such as a hyperscale groundbreaking above 50 MW, occurs.

Why Our Vietnam Data Center Construction Baseline Commands Reliability

Published market estimates vary because firms choose different build-cost assumptions, tier coverage, and refresh cadences.

Typical gap drivers include whether self-built hyperscaler projects are counted, if electrical redundancy premiums are included, and whether land or IT hardware sneaks into "construction" totals. Mordor's scope mirrors actual EPC spend only, applies uniform FX and inflation factors, and updates the model each year, which keeps our baseline balanced and traceable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.72 B | Mordor Intelligence | - |

| USD 0.24 B | Regional Consultancy A | Excludes Tier 4 builds and counts projects <2 MW only. |

| USD 0.65 B | Global Research Firm B | Uses announced investment, not annualized spend, and rolls land cost into totals. |

These comparisons show that once scope and cost definitions are normalized, Mordor's disciplined bottom-up checks anchored to verifiable MW commissions deliver the most dependable starting point for strategic planning.

Key Questions Answered in the Report

How big is the Vietnam Data Center Construction Market?

The Vietnam Data Center Construction Market size is expected to reach USD 0.86 billion in 2026 and grow at a CAGR of 9.03% to reach USD 1.33 billion by 2031.

What is the current Vietnam Data Center Construction Market size?

In 2026, the Vietnam Data Center Construction Market size is expected to reach USD 0.86 billion.

Who are the key players in Vietnam Data Center Construction Market?

Turner Construction Company, Artelia Group, AECOM, Coteccons Construction Joint Stock Company and Rider Levett Bucknall are the major companies operating in the Vietnam Data Center Construction Market.

What years does this Vietnam Data Center Construction Market cover, and what was the market size in 2025?

In 2025, the Vietnam Data Center Construction Market size was estimated at USD 0.86 billion. The report covers the Vietnam Data Center Construction Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Vietnam Data Center Construction Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: