Singapore Data Center Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

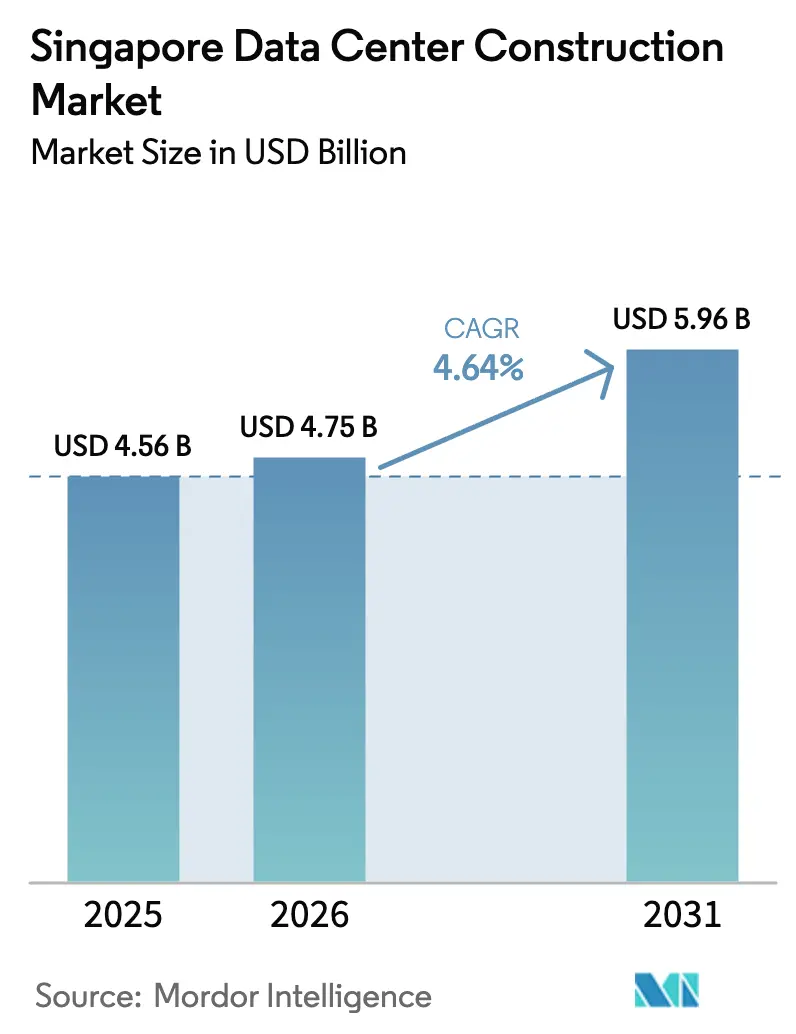

| Base Year Market Size (2025) | USD 4.56 Billion |

| Market Size (2026) | USD 4.75 Billion |

| Market Size (2031) | USD 5.96 Billion |

| Growth Rate (2026 - 2031) | 4.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Data Center Construction Market Analysis by Mordor Intelligence

The Singapore data center construction market size is projected to expand from USD 4.56 billion in 2025 and USD 4.75 billion in 2026 to USD 5.96 billion by 2031, registering a CAGR of 4.64% between 2026 to 2031. A quota-based approach to power allocation, codified in the Green DC Roadmap, is steering developers toward liquid-cooled, high-density campuses that can meet a 1.25 power usage effectiveness ceiling while sourcing 50% of their electricity from renewable sources. At the same time, hyperscalers are doubling down on self-build strategies that integrate proprietary cooling and power fabrics, accelerating the migration of batch processing and model-training workloads to oversized campuses in nearby Johor. Electrical systems remain the single largest cost element, yet mechanical infrastructure is advancing fastest as artificial intelligence workloads push rack densities from 5-8 kW to 40-100 kW. Competitive intensity is rising because the annual 300 MW power cap translates into a zero-sum contest for capacity awards, prompting REIT-led consolidation and modular construction techniques that compress build schedules by 30-40%.

Key Report Takeaways

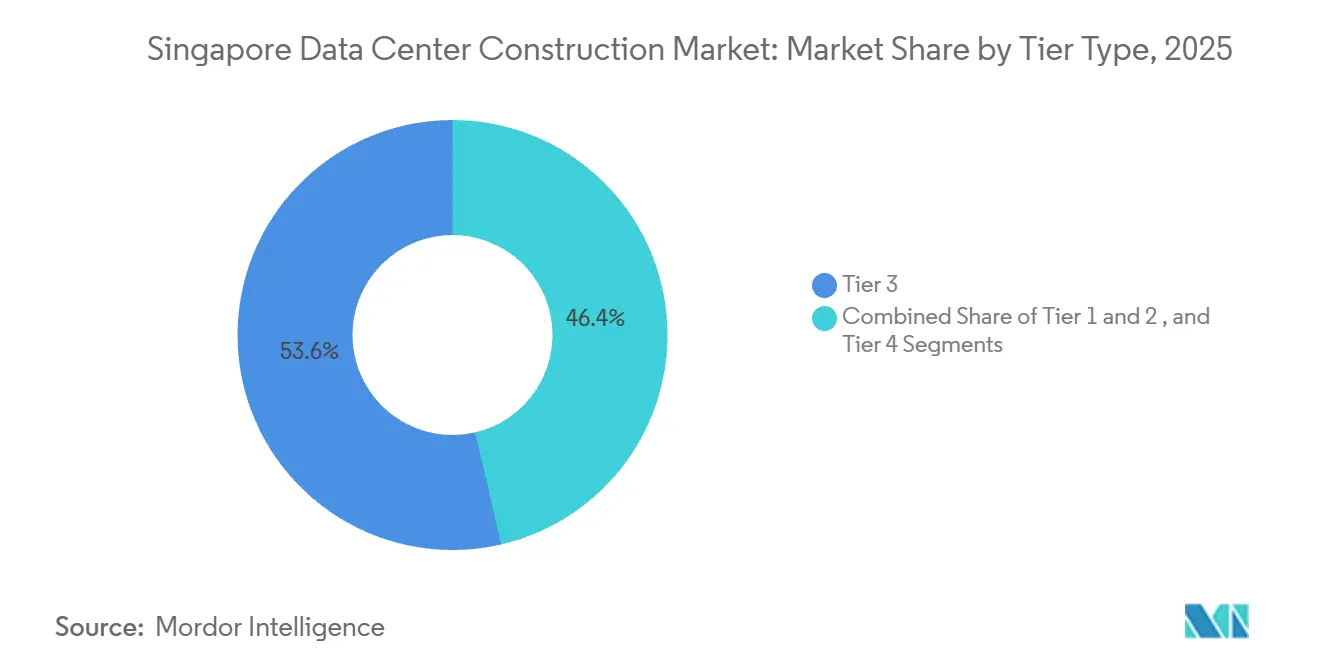

- By tier type, tier 3 facilities led with 53.64% of Singapore data center construction market share in 2025, while tier 4 builds are projected to grow at a 5.43% CAGR through 2031 as fault-tolerant architectures become mandatory for payment and trading platforms.

- By data center type, colocation operators commanded 57.73% market share in 2025, yet hyperscalers and cloud service providers are set to expand at a 5.64% CAGR by 2031 as Amazon Web Services, Google, and Microsoft favor self-build campuses.

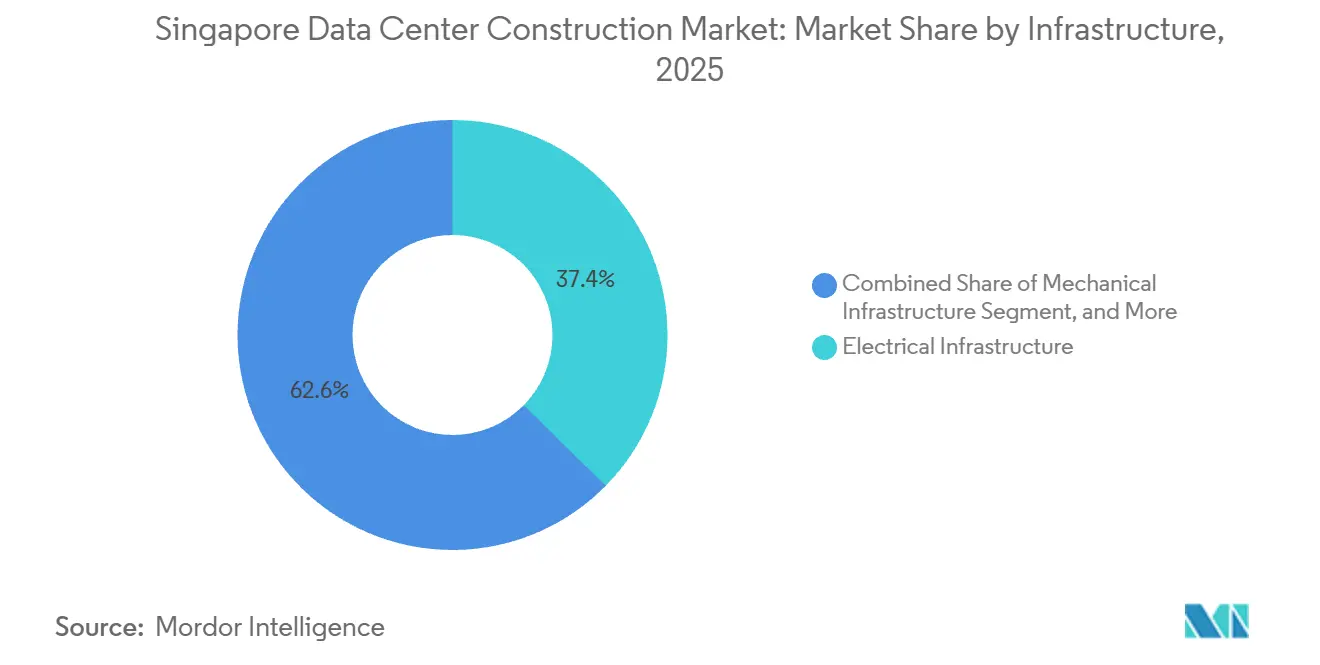

- By infrastructure, electrical systems accounted for 37.38% of the Singapore data center construction market size in 2025, but mechanical systems will rise at a 5.87% CAGR through 2031 on the back of liquid-cooling adoption.

- By data center size, large sites captured 59.49% of the market share in 2025, whereas hyperscale campuses exceeding 30 MW will register a 5.72% CAGR as artificial intelligence clusters demand contiguous floor plates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Power-Allocation Release Under Green DC Roadmap | +1.2% | Jurong Island, Loyang, Tai Seng clusters | Medium term (2-4 years) |

| Surge In AI, GPU-Dense Workloads Requiring New Build Specs | +1.0% | National, spill-over to Johor | Short term (≤ 2 years) |

| Hyperscaler “Singapore-Plus-Johor” Twin-Hub Strategies | +0.8% | Singapore core with Johor satellites | Medium term (2-4 years) |

| Accelerating Sovereign-Cloud and MAS FSI Localization Rules | +0.7% | Financial district, Changi Business Park | Long term (≥ 4 years) |

| Investor Appetite for DC-REIT Conversions | +0.5% | Island-wide | Medium term (2-4 years) |

| Modular Prefabrication to Compress Build Times | +0.4% | Jurong Port Integrated Construction Park | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Power-Allocation Release Under Green DC Roadmap

Singapore ended its three-year capacity moratorium by opening DC-CFA2 on 1 December 2025, conditioning at least 200 MW of new awards on a 1.25 power usage effectiveness ceiling and 50% renewable sourcing. Only operators that can underwrite dedicated solar imports, hydrogen co-generation, or fuel-cell plants are likely to clear the bar, shifting the competitive field toward vertically integrated hyperscalers. The roadmap’s design aligns with the national target of 2 GW-peak solar by 2030 and 1.5 GW of low-carbon imports by 2035, but subsea transmission cables add USD 200-300 million per GW, reinforcing scale economics. Capacity released via the program is therefore concentrated in Jurong Island, Loyang, and Tai Seng industrial zones, where land parcels are bundled with grid interconnections and renewable import links. Successful bidders Equinix, Microsoft, GDS, and an AirTrunk-ByteDance joint venture illustrate that balance-sheet strength plus sustainability credentials now outweigh speed-to-market in quota allocation.[1]Infocomm Media Development Authority, “Data Centre-Call for Application 2,” imda.gov.sg

Surge in AI, GPU-Dense Workloads Requiring New Build Specs

Large language models and real-time inference engines have raised typical rack density an order of magnitude, driving a generational refit cycle. NVIDIA’s Blackwell GPUs demand 40-100 kW per rack, forcing operators to abandon perimeter air cooling in favor of direct-to-chip liquid loops or full immersion, which deliver up to a 0.20 power usage effectiveness gain in tropical climates.[2]NVIDIA Corporation, “Blackwell GPU Architecture Specifications,” nvidia.com Singapore’s SS 715:2025 standard now embeds liquid-cooling best practices, making legacy 5-8 kW environments economically obsolete within five years.[3]Enterprise Singapore, “SS 715:2025 Energy Efficiency Standard,” enterprisesg.gov.sg Vertiv reports that liquid-cooling orders in Singapore doubled in 2025 as operators scramble to future-proof assets, while government-backed artificial intelligence infrastructure funding of USD 27 billion through 2030 ensures sustained demand for high-density campuses.

Hyperscaler “Singapore-Plus-Johor” Twin-Hub Strategies

The Johor-Singapore Special Economic Zone agreement, signed on 7 January 2025, has formalized cross-border campus planning. Developers place power-intensive training clusters in Johor, where tariffs average 13.5 US cents per kWh 43% below Singapore while retaining edge nodes in the city-state to hit sub-2 ms latency budgets. Empyrion Digital’s 200+ MW MY1 campus and Microsoft’s USD 147 million Johor land bank illustrate the scale of this pivot. Fiber redundancy across three subsea and terrestrial paths plus a 2026 rapid-transit link allow shared operations teams to service both hubs. McKinsey forecasts USD 5-7 billion of cross-border data-center outlay by 2030, capturing demand that would otherwise hit Singapore’s 300 MW annual cap.

Accelerating Sovereign-Cloud and MAS FSI Localization Rules

The Monetary Authority of Singapore’s May 2024 Technology Risk Management update now requires financial institutions to ensure 2N+1 redundancy and 4-hour failover for critical workloads, effectively mandating Tier 4 or advanced Tier 3 sites for core banking and payment rails. The January 2025 refresh of Outsourcing Guidelines further locks encryption keys and control planes inside national borders, stimulating sovereign-cloud frameworks across healthcare, education, and government platforms. Tier 4 facilities can command USD 250-300 per kW per month rents roughly a 30% premium over standard Tier 3 space providing strong revenue upside for operators able to certify to Uptime Institute Level IV and BCA Green Mark Platinum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight 300 MW Annual Power Quota and Moratorium Legacy | -0.9% | Central business district, Changi clusters | Long term (≥ 4 years) |

| Highest APAC Construction Cost, USD 11.7 Million/MW and SGD 0.19/Kwh Tariffs | -0.7% | Island-wide, premium versus Malaysia and Indonesia | Medium term (2-4 years) |

| Scarce Brown-Field Plots, Underground or High-Rise Feasibility Unproven | -0.5% | Paya Lebar, Bedok-Tampines land-constrained corridors | Long term (≥ 4 years) |

| Skilled MEP Labor Crunch Inflating Project Timelines | -0.4% | National, spill-over to regional labor pools | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight 300 MW Annual Power Quota and Moratorium Legacy

Singapore’s grid regulator limits new data-center consumption to 300 MW per year, a ceiling intended to keep sectoral load below 12% of national generation. Projects stalled during the 2019-2022 moratorium can only restart once operators prove they can procure 50% low-carbon electricity, creating a circular dependence between hyperscalers and renewable developers. Land parcels that already hold grandfathered allocation rights now command premiums exceeding 40%, especially in Paya Lebar and Loyang. With hydrogen-powered clusters on Jurong Island unlikely to come online before 2028, demand will outstrip supply for at least three years, dampening the Singapore data center construction market growth trajectory.

Highest APAC Construction Cost and Elevated Tariffs

Turner and Townsend ranks Singapore the second most expensive build locale worldwide at USD 14.53 per W in 2025, roughly 35% above Johor or Jakarta benchmarks. Multi-storey designs require reinforced slabs rated beyond 1,500 kg/m², while electrical systems absorb 28 % of capex amid 12-month lead times for switchgear and lithium-ion UPS. Operating expense headwinds are equally stark: SP Group’s industrial tariff of SGD 0.19 per kWh (USD 0.14) adds USD 1.4 million a year in power cost per MW relative to Johor. Combined, these factors remove latency-tolerant workloads from the Singapore data center construction market footprint and push price-sensitive tenants north of the border.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Tier 4 Momentum as Financial Services Tighten Resilience

Tier 3 facilities represented 53.64% of Singapore data center construction market share in 2025, balancing cost with concurrent maintainability for most enterprise clouds. However, the Monetary Authority’s stricter technology risk standards mean the Singapore data center construction market size linked to Tier 4 builds is set to rise steadily; the segment is forecast to post a 5.43% CAGR through 2031. Developers justify the 20-30% higher capex with rental premiums topping USD 300 per kW per month and multi-year take-or-pay contracts from banks, exchanges, and digital-asset custodians.

Operators continue to retrofit Tier 3 halls with additional busways, redundant chillers, and on-site battery energy storage, but only purpose-built Tier 4 campuses can deliver true 2N+1 redundancy. Certification from Uptime Institute now acts as a gating credential for high-margin financial workloads, steering new entrants toward fault-tolerant designs despite longer payback periods. Legacy Tier 1 and Tier 2 stock, concentrated in 2010-era industrial parks, faces a shrinking tenant pool and rising vacancy risk as large enterprises migrate to more resilient footprints.

By Data Center Type: Self-Build Hyperscale Campuses Gain Ground

In 2025, colocation still dominated at 57.73% share, but hyperscalers are driving the next growth leg. The Singapore data center construction market size attributed to hyperscalers and cloud service providers is poised for a 5.64% CAGR as the trio of Amazon Web Services, Google, and Microsoft deploy proprietary cooling and network fabrics inside self-funded campuses. These builds support 100 kW racks, tailored direct-to-chip loops, and custom silicon such as Graviton or TPU accelerators, features difficult to replicate in shared colocation suites.

Multi-tenant landlords defend relevance through dense carrier exchanges and neutral cloud on-ramps, but margin pressure is palpable because hyperscalers now commit to 10-to-15-year leases only when they control base-building design. Enterprise and edge facilities form a residual layer, servicing regulated workloads that must remain on-premises or within 2 km of end users. Nonetheless, the gravitational pull of hyperscale capital means future allocation rounds under the Green DC Roadmap will likely skew toward self-build proposals with embedded renewable power.

By Infrastructure: Mechanical Systems Outpace Electrical Spend

Electrical systems accounted for 37.38% in 2025, yet mechanical infrastructure is the fastest riser, with a CAGR of 5.87%. Liquid-cooling layouts, rear-door heat exchangers, and immersion tanks hold the key to supporting 50-100 kW racks demanded by modern artificial intelligence clusters. Schneider Electric notes that direct-to-chip cold-plate deployments can lift cooling efficiency from 40 % to as high as 90 %, unlocking a potential 0.15 power usage effectiveness benefit.

Power distribution remains vital 11 kV switchgear, bus ducts, and lithium-ion UPS, but modular skids shipped as pre-wired units are flattening the electrical cost curve. Meanwhile, general construction must handle vertical data halls up to nine stories, underpinned by Design for Manufacturing and Assembly prefabrication that slices months from critical paths. Services such as monitoring, predictive maintenance, and performance warranties are being bundled into energy-as-a-service contracts, shifting capex toward opex and deepening vendor lock-ins.

By Data Center Size: Hyperscale Leads New Megawatt Additions

Large sites of 10-30 MW held 59.49% share in 2025, but the hyperscale segment above 30 MW is expanding fastest at 5.72% CAGR. Single-tenant campuses amortize substation, fiber, and renewable-import infrastructure over bigger denominators, lowering all-in cost per kW by up to 20 %. Keppel DC REIT’s USD 1.04 billion purchase of KDC SGP 7 and 8 underscores institutional appetite for 50-100 MW builds pre-leased to cloud majors.

Medium (5-10 MW) and small (< 5 MW) deployments keep niche roles in edge compute, healthcare imaging, and latency-critical trading, yet they lack the economies of scale to compete for artificial intelligence training clusters that can consume 20 MW for weeks. The upcoming 700 MW Jurong Island park is configured specifically for 10-to-15 hyperscale blocks, each wrapped around on-site hydrogen and battery storage, reinforcing a barbell distribution where hyperscale and micro-edge push mid-sized campuses toward consolidation.

Geography Analysis

Singapore’s permissioned footprint centers on Jurong Island, Loyang, Tai Seng, Paya Lebar, and Changi Business Park, where legacy grid feed-ins and subsea-cable proximity converge. The launch of a 700 MW low-carbon precinct on Jurong Island in 2025 cements the zone as the focal point for future capacity, bundling ammonia import terminals, hydrogen electrolyzers, and battery storage to deliver renewable electrons on-tap. Land premiums reflect allocation scarcity; Paya Lebar parcels traded at SGD 2,170 per m² in 2024, 40 % above Loyang, purely due to embedded power rights.

Vertical and even floating concepts are advancing to mitigate land constraints. ST Engineering’s seven-story, 30 MW facility completes in 2026, while Equinix’s nine-story SG6, scheduled for Q1 2027, will stack 20 MW across elevated halls. Efficiency questions linger because tropical humidity challenges heat-rejection systems, yet success would unlock a repeatable template for future builds. Underground designs remain aspirational pending cost and airflow validation.

Just 2 km north, Johor is now an extension of the Singapore data center construction market. Tariffs 43 % lower than the city-state and a 1,770 MW development pipeline at Ibrahim Technopolis and Medini attract hyperscalers seeking unconstrained plots. Cross-border fiber rings coupled with a 2026 rapid-transit shuttle keep round-trip latency under 3 ms for most applications, enabling a twin-hub topology; Singapore hosts the edge nodes for finance and gaming, while Johor shoulders energy-hungry model-training or archival duties. Analysts estimate Johor could capture 30-40 % of incremental capacity that quota rules would otherwise block from Singapore by 2030.

Competitive Landscape

The Singapore data center construction market is moderately concentrated. Keppel DC REIT is the consolidation vanguard, plowing SGD 2.5 billion (USD 1.85 billion) into five acquisitions between September 2024 and December 2025, including full control of KDC SGP 7 and 8 plus a SGD 350 million (USD 259 million) land-lease extension to 2050. REIT structures recycle capital swiftly, giving them an edge when quota windows open.

Hyperscalers are bypassing landlords altogether by self-funding 50-100 MW campuses wrapped with proprietary liquid-cooling, power, and security stacks. Amazon Web Services and Microsoft each signed multi-gigawatt renewable purchase agreements across Southeast Asia that backstop their Singapore allocations, insulating them from tariff swings. Colocation incumbents defend share through dense carrier exchanges, neutral interconnection, and premium Tier 4 offerings for financial clients, yet face margin compression as hyperscalers withdraw anchor loads.

Technology differentiation now hinges on industrialized construction. Global Switch’s Woodlands campus used 350 prefabricated mechanical, electrical, and plumbing modules, trimming build time by 10 % and embodied carbon by 45%. Contractors such as Boustead Projects and Takenaka have invested in digital-twin design and robotic assembly to meet the Building and Construction Authority’s 70 % Design for Manufacturing and Assembly target by 2025. With the next 200 MW of quota tied to sustainability metrics, operators holding BCA Green Mark Platinum and ISO 27001 certificates enjoy a 15-20 % rental premium and expedited permitting pathways.

Singapore Data Center Construction Industry Leaders

Gammon Pte Ltd (Balfour Beatty)

Boustead Projects Ltd.

Dragages Singapore Pte. Ltd.

Takenaka Corporation

Kajima Overseas Asia Pte. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Keppel DC REIT bought the remaining 10 % of Keppel DC Singapore 3 and 1 % of Keppel DC Singapore 4 for SGD 50.5 million (USD 37.4 million), achieving full ownership and bolstering exposure to high-density clusters.

- December 2025: The Infocomm Media Development Authority opened DC-CFA2, releasing at least 200 MW of new quota tied to a 1.25 power usage effectiveness ceiling and 50 % renewable sourcing.

- November 2025: Keppel Infrastructure and JTC Corporation inked an agreement to develop microgrids and artificial intelligence-driven energy optimization at the 700 MW Jurong Island low-carbon park.

- October 2025: Singapore announced the Jurong Island low-carbon data center park, allocating 20 ha for up to 700 MW of capacity alongside hydrogen, ammonia, and battery assets.

Singapore Data Center Construction Market Report Scope

A data center is a physical room, building, or facility that holds IT infrastructure used to construct, run, and provide applications and services, and store and manage the data connected with them. Under data center construction, the capital expenditure incurred while building the existing data center facilities is tracked, and the future capex is estimated based on upcoming data center facilities.

The Singapore Data Center Construction Market Report is Segmented by Tier Type (Tier 1, Tier 2, Tier 3, and Tier 4), Data Center Type (Colocation, Hyperscalers/Cloud Service Providers, and Enterprise and Edge Data Center), Infrastructure (Electrical Infrastructure, Mechanical Infrastructure, General Construction, and Services), and Data Center Size (Small, Medium, Large, and Hyperscale). The Market Forecasts are Provided in Terms of Value (USD).

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small |

| Medium |

| Large |

| Hyperscale |

| Colocation Data Center |

| Hyperscalers/Cloud Service Provider (CSPs) |

| Enterprise and Edge Data Center |

| Electrical Infrastructure | Power Distribution Solution |

| Power Backup Solutions | |

| Mechanical Infrastructure | Cooling Systems |

| Racks and Cabinets | |

| Servers and Storage | |

| Other Mechanical Infrastructure | |

| General Construction | |

| Services - Design and Consulting, Integration, Support and Maintenance |

| By Tier Type | Tier 1 and 2 | |

| Tier 3 | ||

| Tier 4 | ||

| By Data Center Size | Small | |

| Medium | ||

| Large | ||

| Hyperscale | ||

| By Data Center Type | Colocation Data Center | |

| Hyperscalers/Cloud Service Provider (CSPs) | ||

| Enterprise and Edge Data Center | ||

| By Infrastructure | Electrical Infrastructure | Power Distribution Solution |

| Power Backup Solutions | ||

| Mechanical Infrastructure | Cooling Systems | |

| Racks and Cabinets | ||

| Servers and Storage | ||

| Other Mechanical Infrastructure | ||

| General Construction | ||

| Services - Design and Consulting, Integration, Support and Maintenance | ||

Key Questions Answered in the Report

How big is the Singapore data center construction market today?

The market reached USD 4.75 billion in 2026 and is projected to hit USD 5.96 billion by 2031.

What is driving new capacity despite the power quota?

Green DC Roadmap allocations reward operators that couple 1.25 power usage effectiveness with 50% renewable sourcing, unlocking at least 200 MW of fresh supply.

Why are hyperscalers building in Johor as well as Singapore?

Johor offers power tariffs 43% lower than Singapore and unconstrained land, while fiber links keep latency under 3 ms for most workloads.

Which tier type is growing fastest?

Tier 4 sites, offering full 2N+1 redundancy, are forecast to expand at a 5.43% CAGR through 2031 as financial institutions harden resilience.

How are construction costs impacting project timelines?

Costs average USD 14.53 per W, and 12-month lead times for switchgear and chillers require early procurement and modular prefabrication to stay on schedule.

What cooling technologies are becoming standard?

Direct-to-chip liquid cooling and immersion systems are replacing perimeter air handling, allowing rack densities up to 100 kW and delivering power usage effectiveness improvements of roughly 0.15-0.20.

Page last updated on: