Vietnam Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

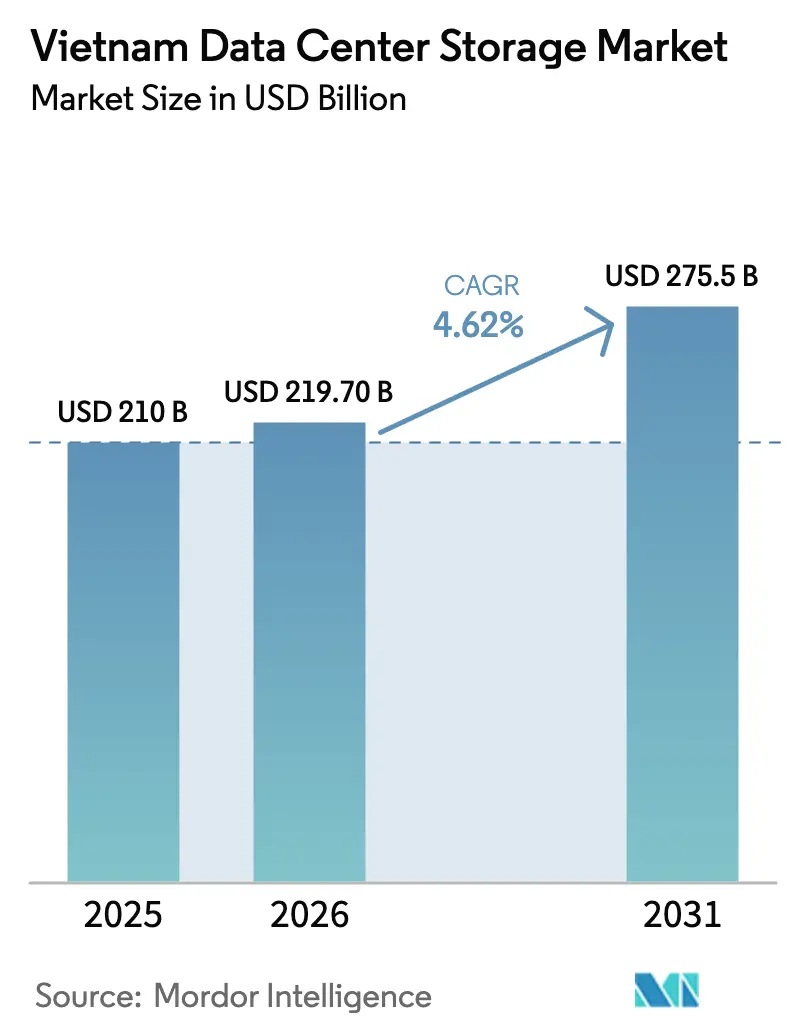

| Base Year Market Size (2025) | USD 210 Billion |

| Market Size (2026) | USD 219.7 Billion |

| Market Size (2031) | USD 275.5 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

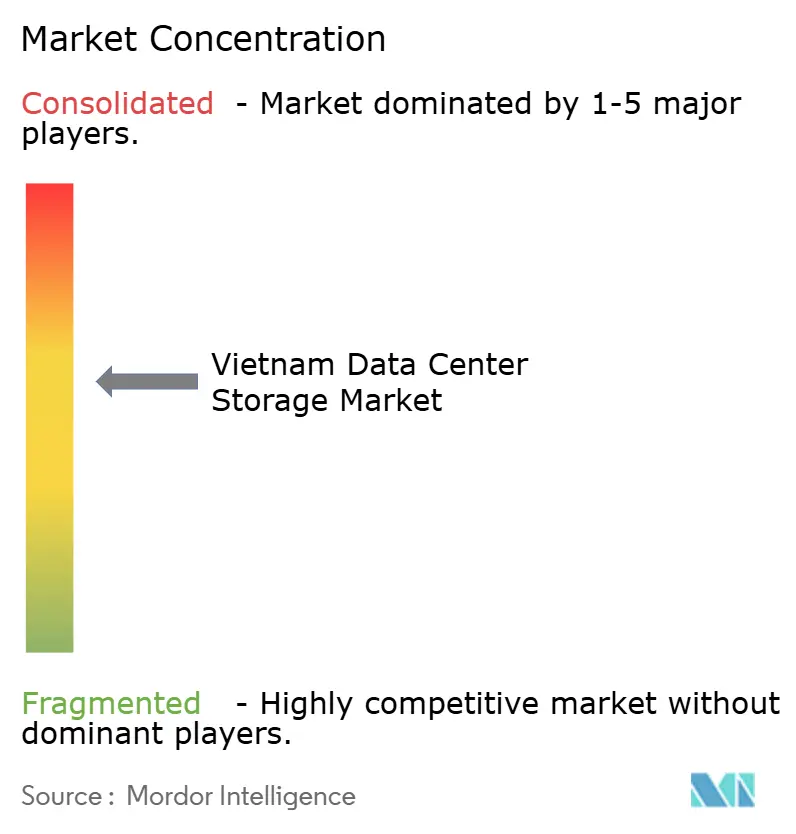

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Data Center Storage Market Analysis by Mordor Intelligence

The Vietnam data center storage market size is expected to grow from USD 210 million in 2025 to USD 219.7 million in 2026 and is forecast to reach USD 275.5 million by 2031 at 4.62% CAGR over 2026-2031. Consistent policy support, 100% foreign‐ownership approval for data centers, and an influx of hyperscale projects position Vietnam as a rising regional hub for enterprise and cloud workloads. National digital‐economy targets, tighter data‐sovereignty rules, and rapid AI/ML adoption lead enterprises to modernize with flash and NVMe platforms. High-density builds such as Viettel’s 140 MW Tan Phu Trung facility illustrate how power-hungry AI clusters are reshaping rack design and storage interface preferences. Liberal regulation accelerates foreign capital inflows, yet grid constraints and a limited talent pool temper near-term capacity execution while opening niches for energy-efficient, managed‐service propositions

Key Report Takeaways

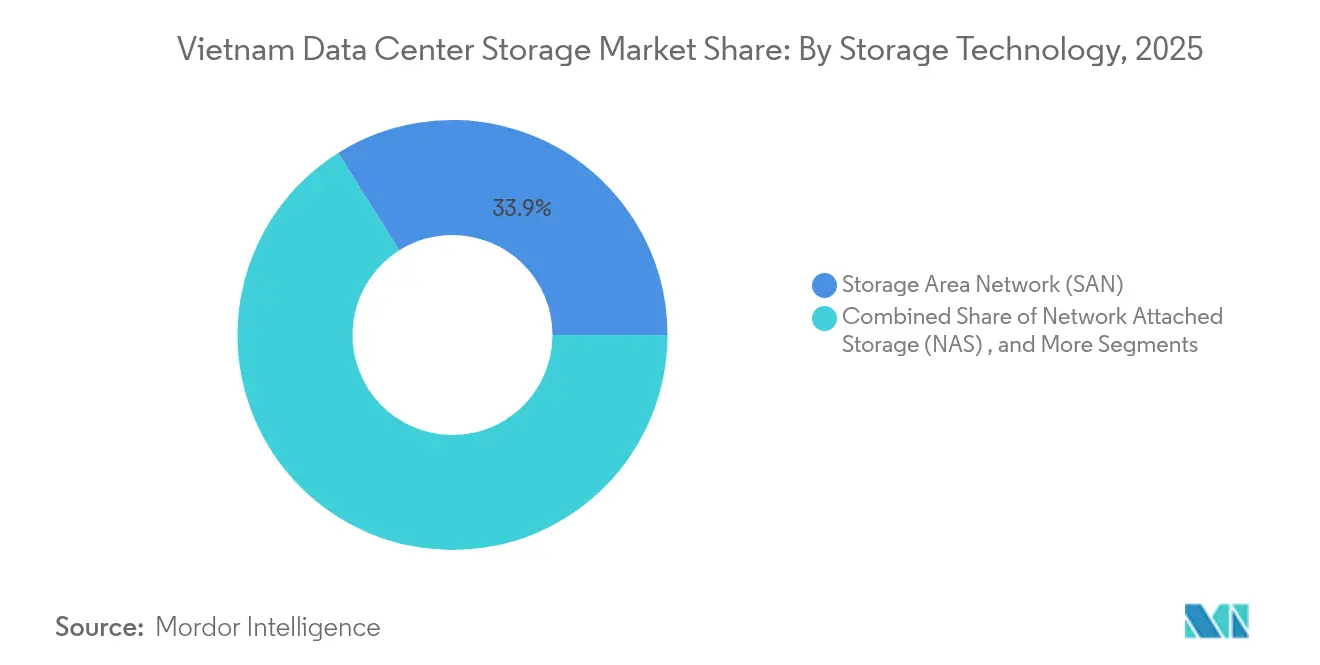

- By storage technology, SAN led with 33.92% revenue share in 2025, while NAS is projected to be the fastest-growing at a 6.58% CAGR to 2031.

- By storage type, HDD arrays accounted for 42.55% of the Vietnam data center storage market size in 2025; all-flash arrays are advancing at a 9.12% CAGR through 2031.

- By data-center type, colocation commanded 49.05% revenue in 2025, while hyperscalers are advancing at an 8.16% CAGR.

- By end user, IT and telecom captured 29.10% of Vietnam data center storage market share in 2025; BFSI is expanding fastest at a 7.21% CAGR.

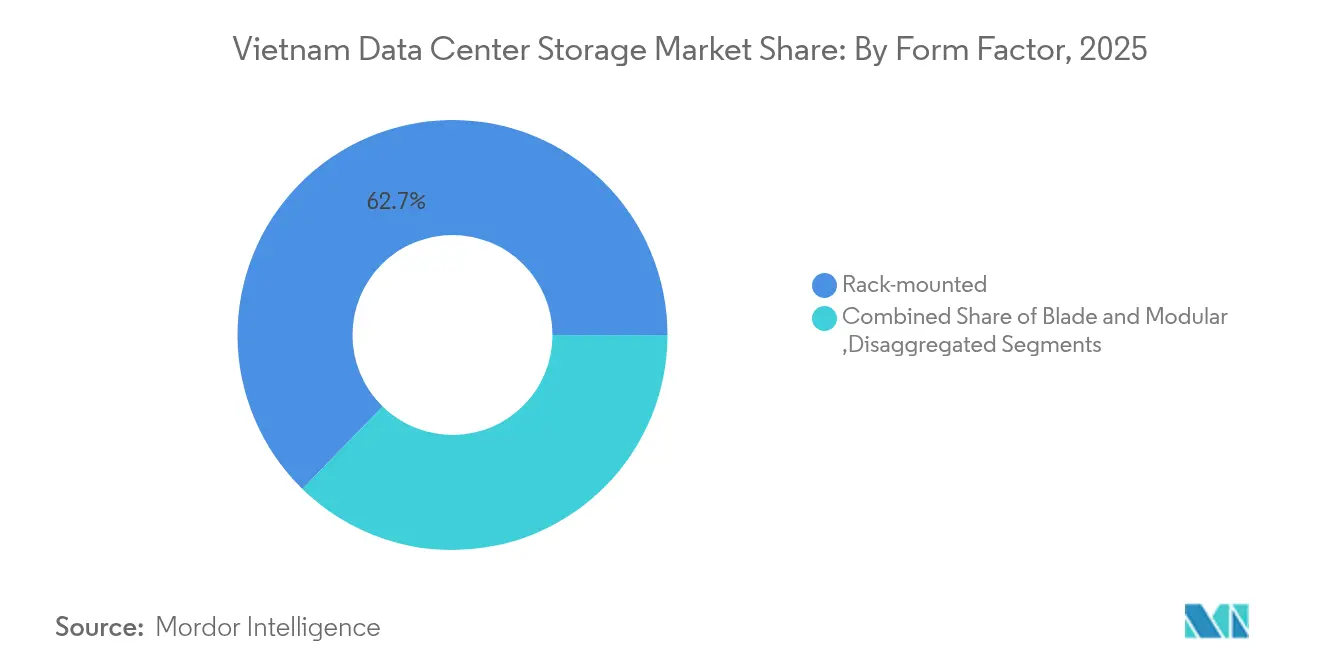

- By form factor, rack-mounted systems held 62.70% share in 2025; composable infrastructure is growing at a 9.28% CAGR.

- By interface, SAS/SATA maintained 53.85% share in 2025; NVMe is increasing at an 8.01% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of IT infrastructure and broadband | +1.2% | Ho Chi Minh City, Hanoi | Medium term (2-4 years) |

| Hyperscale data-center investments | +1.5% | Industrial zones nationwide | Long term (≥4 years) |

| Digital-transformation and data-sovereignty | +1.8% | National | Short term (≤2 years) |

| SME cloud adoption driving NAS | +0.9% | Urban clusters | Medium term (2-4 years) |

| AI/ML workload surge fueling all-flash | +1.1% | Technology hubs | Medium term (2-4 years) |

| 100% foreign-ownership liberalization | +0.7% | National | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expansion of IT Infrastructure and Broadband

Vietnam’s target of 80% household broadband coverage by 2025 under the National Digital Transformation Program is stimulating demand for edge and core storage systems.[1]Ministry of Information & Communications, “Digital Transformation Program 2025,” vietnamnet.vn Ten additional submarine cables planned by 2030 will lift total capacity to 350 Tbps, generating sustained requirements for high-density edge appliances along landing points. Enterprises such as VTI report 70% cost savings after cloud migration, reinforcing hybrid storage uptake for analytics and backup operations vti. Manufacturing and logistics adopters are installing Industry 4.0 workflows that necessitate low-latency, compute-proximate storage for robotics and real-time quality control. Automotive OEMs and electronics exporters are notable early movers, using rack-scale flash to sustain inline analytics on production floors. This infrastructural momentum anchors long-run growth for the Vietnam data center storage market.

Rising Investments in Hyperscale Data Centers

Viettel’s 140 MW Tan Phu Trung build represents Vietnam’s inaugural 100 MW-plus data center, operating at 10 kW per rack—2.5× the national mean—thereby catalyzing demand for NVMe-accelerated, high-density arrays.[2]Anh Minh, “Viettel Starts Vietnam’s First 140 MW Data Center,” vietnamplus.vn Saigon Asset Management’s USD 1.5 billion, 150 MW SAM DigitalHub signals strong capital appetite for hyperscale footprints. Investors target PUE levels below 1.4 through warm-water and rear-door cooling, creating openings for software-defined storage that optimizes workload placement across distributed nodes. Vendors offering horizontally scalable platforms that minimize rack power draw gain a competitive edge as operators standardize on high-performance compute fabrics to serve regional AI demand.

Government Digital-Transformation and Data-Sovereignty Mandates

Vietnam’s Data Law effective July 2025 institutes a three-tier data-classification regime, compelling “core” and “important” datasets to reside domestically kpmg. The National Data Center launches August 2025 with two mirrored facilities housing around 1,000 racks each, establishing proof-of-concept for resilient sovereign architectures cafebiz. Alibaba’s shift from leasing to building its own site exemplifies how cross-border risk assessments trigger greenfield investment vnexpress. Procurement criteria now prioritize at-rest encryption, geo-fencing and audit logging that map directly to legal mandates, bolstering vendors with compliance-ready firmware and in-country service teams. The regulation accelerates near-term storage hardware refresh cycles across state agencies and regulated industries.

Surge in SME Cloud Adoption Driving NAS

The Ministry of Information and Communications’ SME Digital Transformation scheme subsidizes cloud services from 11 domestic providers, lowering entry costs by 20% and accelerating NAS adoption nhandan. Providers such as VNG Cloud tailor pay-as-you-grow models that angle directly at cost-sensitive SMEs. Growth is clear in e-commerce logistics: Ahamove orchestrates 200,000 daily deliveries on MongoDB Atlas, relying on NAS-backed clusters that flex with transaction peaks mongodb. Government workloads further validate NAS: SaoBacDau’s Red Hat OpenStack-based services deliver elastic object storage to ministries requiring domestic hosting redhat. The trend underpins sustained 6.8% CAGR for NAS within the Vietnam data center storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for Tier III/IV sites | -0.8% | Nationwide; acute for small operators | Medium term (2-4 years) |

| Shortage of skilled storage engineers | -1.1% | Urban centers | Long term (≥4 years) |

| Grid-energy constraints for dense racks | -0.6% | Industrial zones | Short term (≤2 years) |

| Rising cooling costs in tropical climate | -0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Tier III/IV Facilities

Tier III certification demands dual-path power, cooling and storage redundancy. Delta Electronics’ EPC contract in Hoa Lac illustrates capital intensity, with developers absorbing long ROI timelines delta. Domestic firms such as CMC Telecom must match global benchmarks to win multinational clients after becoming Vietnam’s first Level 4 Information Security-accredited site cmc. Financing constraints push operators toward vendor-financed, modular blocks and hyper-converged appliances that compress initial outlays. While the restraint suppresses greenfield pace, it stimulates demand for pre-integrated solutions that reduce on-site engineering effort.

Shortage of Skilled Storage Engineers

Vietnam counts roughly 6,000 hardware specialists against a projected need of 20,000 within five years.[3]Channel News Asia, “Vietnam Faces Tech Talent Crunch,” channelnewsasia.com Public programs such as Ho Chi Minh City’s USD 5 million initiative to train 40,000 microchip engineers by 2030 aim to narrow the gap vietnamnet. Meanwhile, vendors embed automation into management stacks, lowering skill thresholds required for day-to-day operations. Hyper-converged platforms and AI-driven telemetry become vital differentiators for operators facing recruitment bottlenecks in the Vietnam data center storage industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Dominance Amid NAS Acceleration

SAN solutions delivered 33.92% of 2025 revenues, reflecting enterprise demand for low-latency, block-level services in mission-critical cores. This share positions SAN as the performance backbone of the Vietnam data center storage market. NAS, climbing at 6.58% CAGR, benefits from SME cloud programs that reward cost-effective, Ethernet-based deployments. The Vietnam data center storage market size for NAS is projected to cross USD 0.1 billion by 2031, aided by government incentives. Direct-attached and object systems supplement specialized edge and archival workloads governed by emerging data-retention rules.

Hybrid adoption patterns intensify as Viettel IDC integrates Cloudian HyperStore to offer object and file services on a unified appliance, combining SAN-grade throughput for transactional workloads with NAS scalability for analytics datacenternews. Software-defined overlays blur protocol boundaries, enabling dynamic selection between block, file and object APIs. Enterprises thus future-proof investments while optimizing TCO, sustaining robust demand across all technology categories.

By Storage Type: HDD Arrays Lead Despite Flash Momentum

HDD arrays accounted for 42.55% of spending in 2025 due to favorable USD per-GB economics. All-flash, the fastest-growing at 9.12% CAGR, captures AI inference, real-time analytics and digital banking peaks. Vietnam data center storage market share for all-flash arrays is slated to climb beyond 31.2% by 2031. Hybrid tiers persist for mid-range workloads that fluctuate between capacity and performance needs.

Flash traction is underscored by Techcombank’s migration to IBM DS8886, quadrupling peak transaction throughput while shrinking rack footprint ibm. Kingston’s DC600M SSD line addresses mixed-use traffic and power efficiency, echoing policy emphasis on sustainable IT kingston. Energy incentives further tilt TCO calculus in favor of flash for operators seeking carbon neutrality certifications.

By Data Center Type: Colocation Leadership with Hyperscaler Growth

Colocation sites held 49.05% of 2025 revenues as enterprises opt for shared infrastructures that offload capital and operational complexity. The Vietnam data center storage market continues to rely on colo for interconnection access and quick deployment. Hyperscalers, bolstered by 8.16% CAGR, drive bulk capacity orders for high-density racks and petascale storage pools. The Vietnam data center storage market size for hyperscalers is estimated to climb from USD 0.07 billion in 2026 to more than USD 0.12 billion by 2031.

Viettel’s 10,000-rack flagship sets a reference design for AI and 5G workloads requiring enhanced power and cooling envelopes genk. Colocation incumbents counter with on-ramp services to AWS, Google Cloud and Azure, adding value-added storage tiers optimized for hybrid migrations. Enterprise and edge micro-data centers remain vital for latency-sensitive manufacturing and public-sector use cases under strict data-localization rules.

By End User: Telecommunications Strength with BFSI Acceleration

IT and telecom captured 29.10% of 2025 revenue, leveraging backbone networks and national backhaul to deliver ISP, CDN and 5G services. BFSI, expanding at 7.21% CAGR, demonstrates outsized appetite for encrypted, low-latency storage to support digital banking, e-payment platforms and regulatory audits. Vietnam data center storage market size for BFSI is forecast to nearly double by 2030.

VPBank’s OpenAPI platform processes 100 million monthly transactions on MongoDB clusters, highlighting new-age workloads that tax storage IO more than capacity mongodb. Government digital offices shift citizen services onto sovereign clouds, prompting expansions in archival and compliance repositories. Healthcare early adopters like Ho Chi Minh City’s eClinica leverage structured storage to consolidate 80,000 electronic patient records, spotlighting sectoral diversification

By Form Factor: Rack-Mounted Dominance with Composable Innovation

Rack-mounted chassis delivered 62.70% of revenue in 2025 thanks to broad ecosystem support and straightforward integration. Composable designs, rising at 9.28% CAGR, disaggregate compute, storage and network to enable dynamic pooling. Vietnam data center storage market size for composable solutions is projected to exceed USD 0.06 billion by 2031.

Dell’s Integrated Rack 7000 bundles liquid cooling and GPU-dense sleds for AI, demonstrating how form-factor innovation keeps pace with power and performance escalation dell. Blade and modular formats serve branch and disaster-recovery nodes, particularly in edge telco shelters requiring compact footprints. Software orchestration engines assign storage volumes on-demand, maximizing utilization and aligning with the skills shortage imperative.

By Interface: SAS/SATA Prevalence with NVMe Emergence

SAS/SATA maintained 53.85% share in 2025 due to mature toolchains and broad application compatibility. NVMe, advancing at 8.01% CAGR, underpins AI training sets and latency-sensitive fintech workloads. Vietnam data center storage market size for NVMe devices is projected to triple between 2025 and 2030.

Kingston’s FURY Renegade G5 PCIe 5.0 SSD posts up to 14,800 MB/s reads, delineating next-gen throughput curves for AI inference. TMBThanachart Bank’s deployment of Huawei end-to-end NVMe cut latency 60% and boosted compute 25%, validating interface migration economics. Fibre Channel persists for mission-critical SAN fabrics, whereas iSCSI and RoCE overlays enable cost-effective Ethernet convergence strategies.

Geography Analysis

Ho Chi Minh City and Hanoi anchor more than two-thirds of storage deployments, reflecting economic clout, fiber density and proximity to submarine cable landings. Viettel’s Tan Phu Trung complex and CMC’s Tan Thuan site position the southern cluster as the primary hyperscale corridor while feeding spillover demand for edge nodes in neighboring provinces soha. In the north, VNPT’s 23,000 sqm Hoa Lac campus with 2,000 racks supports government ministries and state banks, creating a gravitational pull for equipment vendors.

Central provinces increasingly court operators through renewable-power availability. Ninh Thuan hosts 1,500 MW solar and 1,442 MW wind capacity, offering green energy hooks for ESG-driven investors looking to cut Scope 2 emissions energysystemsresearch. Government strategy to designate regional digital hubs by 2050 accelerates fiber rollout and special-economic-zone tax relief, encouraging distributed storage topologies. Coastal locations gain thermodynamic efficiency for free-air and seawater cooling solutions; inland industrial parks offer affordable land to build multi-hectare campuses.

Connectivity remains the decisive factor for site selection across the Vietnam data center storage market. The upcoming submarine cable lines and continued investment in national backbones allow operators to place capacity closer to renewable sources without sacrificing latency to urban demand centers. As metro dark-fiber rates drop, tier-2 cities such as Thai Nguyen emerge as attractive cluster sites, supported by workforce development schemes for semiconductor and AI specializations.

Competitive Landscape

Local telecom groups—Viettel IDC, VNPT VinaData, CMC Telecom and FPT Telecom—leverage long-haul networks, national POPs and government affinity to secure anchor colocation deals and manage 24/7 compliance audits. International hardware majors—Dell Technologies, NetApp, Oracle, Kingston Technology and Huawei—expand through reseller alliances and direct hyperscale engagements, supplying flash arrays, NVMe fabrics and software-defined storage stacks tuned for AI.

Strategic positioning revolves around scalability, energy efficiency and full-stack services. Dell’s AI Factory claims total cost reductions up to 62% versus public-cloud equivalents by integrating compute, cooling and PowerStore arrays under a single rack-scale SKU cafebiz. NetApp’s validation for NVIDIA DGX SuperPOD and Google Cloud partnership underscores hybrid-AI credentials appealing to financial institutions under latency and data-sovereignty pressure. Kingston differentiates with PCIe 5.0 offerings while bundling power-loss protection to ease adoption inside regions facing voltage fluctuation.

The race for talent generates collaborations with universities; Kioxia’s proposed joint program on NVMe curriculum typifies moves to seed long-term channel loyalty. Meanwhile, start-ups in hyper-converged, Kubernetes-native storage nibble at niche segments, banking on simplified ops that resonate with mid-market enterprises lacking deep IT benches. Moderate industry concentration persists as no single vendor surpasses 30% share, fostering healthy price–performance competition across project bids.

Vietnam Data Center Storage Industry Leaders

Viettel IDC Co. Ltd.

VNPT VinaData Co. Ltd.

FPT Telecom International

Dell Technologies Inc.

Seagate Technology Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Qualcomm set up its third-largest global AI R&D center in Vietnam to accelerate local innovation and infrastructure demand

- June 2025: CMC Group launched the USD 300 million CCS Hanoi data center and AI hub spanning 90,000 m², targeting training for 5,000 engineers

- June 2025: Vinatech opened an automated shelving plant in Hoa Binh to scale domestic smart-warehouse solutions

- May 2025: Kingston showcased the FURY Renegade G5 PCIe 5.0 NVMe SSD at COMPUTEX 2025

- April 2025: Viettel broke ground on a 140 MW, 10,000-rack super-large data center in Tan Phu Trung Industrial Park

- March 2025: Saigon Asset Management kicked off the USD 1.5 billion, 150 MW SAM DigitalHub campus

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Vietnam data-center storage market as all on-premise arrays, software layers, and interfaces installed inside domestic colocation, cloud, hyperscale, and enterprise facilities that store, protect, and serve digital content; values are expressed in USD revenue generated within Vietnam for new equipment and active support contracts.

Scope Exclusions: Portable consumer drives, direct public-cloud storage fees billed outside Vietnam, and refurbished second-hand hardware are not counted.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

Interviews were completed with facility engineers in Ho Chi Minh City, storage architects at hyperscalers, and procurement heads across BFSI and telecom clusters. Views on flash penetration, spare-capacity habits, and regulatory budgeting were used to validate volumes and refine adoption curves.

Desk Research

Our analysts gathered supply-side clues from open Vietnamese customs logs, Ministry of Information & Communications rack-import releases, and quarterly operator presentations. We balanced these with industry primers from Statista, the International Trade Administration, and trade associations such as WSTS for semiconductor billings. Company 10-Ks and rack tender notices enriched average selling price (ASP) assumptions, while paid access to D&B Hoovers let us cross-check vendor shipments. The sources listed illustrate, not exhaust, the larger document set consulted for fact finding.

Market-Sizing & Forecasting

A top-down model converts IT-load additions (MW) into installed racks, applies storage spend per rack benchmarks, and then splits totals by technology. Bottom-up spot checks, supplier roll-ups for SAN frames, and sampled ASP × volume from import declarations help tune over or under estimates. Key variables include (i) new rack capacity approved each year, (ii) flash share in fresh arrays, (iii) exchange-rate adjusted ASPs, (iv) data-localization enforcement timing, and (v) average refresh cycles. Multivariate regression projects each driver, letting the forecast reflect scenarios for hyperscale project slippage or faster flash adoption.

Data Validation & Update Cycle

Outputs pass three tiers of analyst review, outlier flags trigger re-contacts, and model variance versus customs data stays below ten percent before sign-off. We refresh numbers yearly, inserting interim updates once major policy or capacity shifts are confirmed.

Why Mordor's Vietnam Data Center Storage Baseline Earns Trust

Published figures often differ because firms adopt wider scopes, import global cloud revenue, or freeze exchange rates months earlier. Our disciplined focus on in-country hardware, paired with an annual refresh cadence, keeps totals aligned with real rack builds and spending sentiment.

Key gap drivers include rival studies folding external cloud fees into hardware revenue, assuming constant ASPs despite the 18% flash price slide in 2024, or extrapolating power-capacity trends without primary checks on storage share.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.21 B (2025) | Mordor Intelligence | |

| USD 0.20 B (2024) | Regional Consultancy A | Includes consumer NAS units; no primary interviews |

| USD 0.51 B (2023) | Industry Portal B | Blends public-cloud storage revenue with hardware sales; uses global rack ASP multipliers |

These comparisons show that Mordor's narrower, hardware-only scope and live primary validation yield a balanced, reproducible baseline that decision-makers can rely on.

Key Questions Answered in the Report

What is the current value of the Vietnam data center storage market?

It is valued at USD 219.7 million in 2026.

How fast is the Vietnam data center storage market expected to grow?

The market is projected to post a 4.62% CAGR and reach USD 275.5 million by 2031.

Which storage technology is growing fastest?

Network attached storage is forecast to expand at a 6.58% CAGR due to SME cloud adoption.

Why are hyperscale projects important for Vietnam?

Projects such as Viettel’s 140 MW campus demand high-density flash arrays and attract foreign capital, fueling long-term infrastructure growth.

What regulatory change influences storage procurement?

Vietnam’s Data Law mandates domestic hosting for “core” and “important” data, driving demand for compliant local facilities.

How severe is the skills shortage?

The country has around 6,000 storage engineers against an expected need of 20,000, increasing interest in managed and automated storage services.

Page last updated on: