Vietnam Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

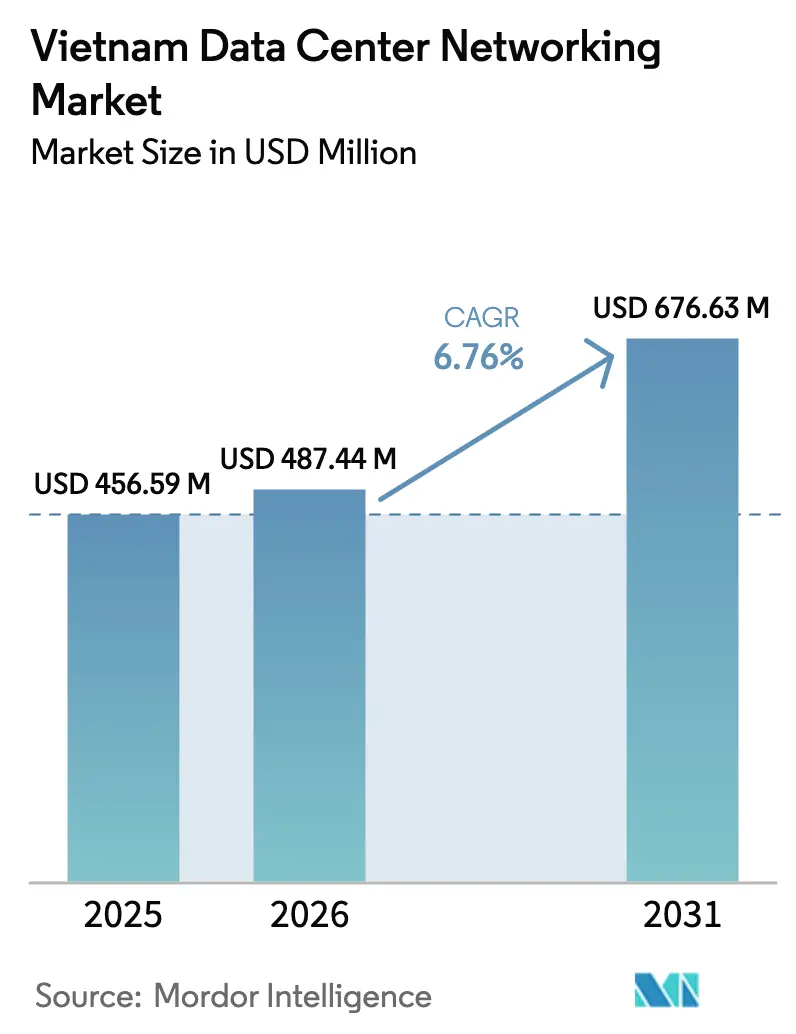

| Base Year Market Size (2025) | USD 456.59 Million |

| Market Size (2026) | USD 487.44 Million |

| Market Size (2031) | USD 676.63 Million |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Data Center Networking Market Analysis by Mordor Intelligence

The Vietnam data center networking market size was valued at USD 456.59 million in 2025 and estimated to grow from USD 487.44 million in 2026 to reach USD 676.63 million by 2031, at a CAGR of 6.76% during the forecast period (2026-2031). Mandatory data-localization rules, continuous rollout of 5G, and heavy cloud capital expenditure give the market a firm growth foundation. Public-sector digital programs—most notably the National Digital Transformation Programme through 2025—anchor near-term demand, while record-scale private investments such as Viettel’s 140 MW facility signal durable long-term momentum. Hyperscalers, financial services institutions, and manufacturers are simultaneously upgrading to 25 GbE and 100 GbE architectures, which lifts switching, routing, and optical-interconnect revenue. Supply-chain tightness in advanced silicon and rising power tariffs remain headwinds, yet broad-based domestic and foreign investment keeps the overall outlook positive.

Key Report Takeaways

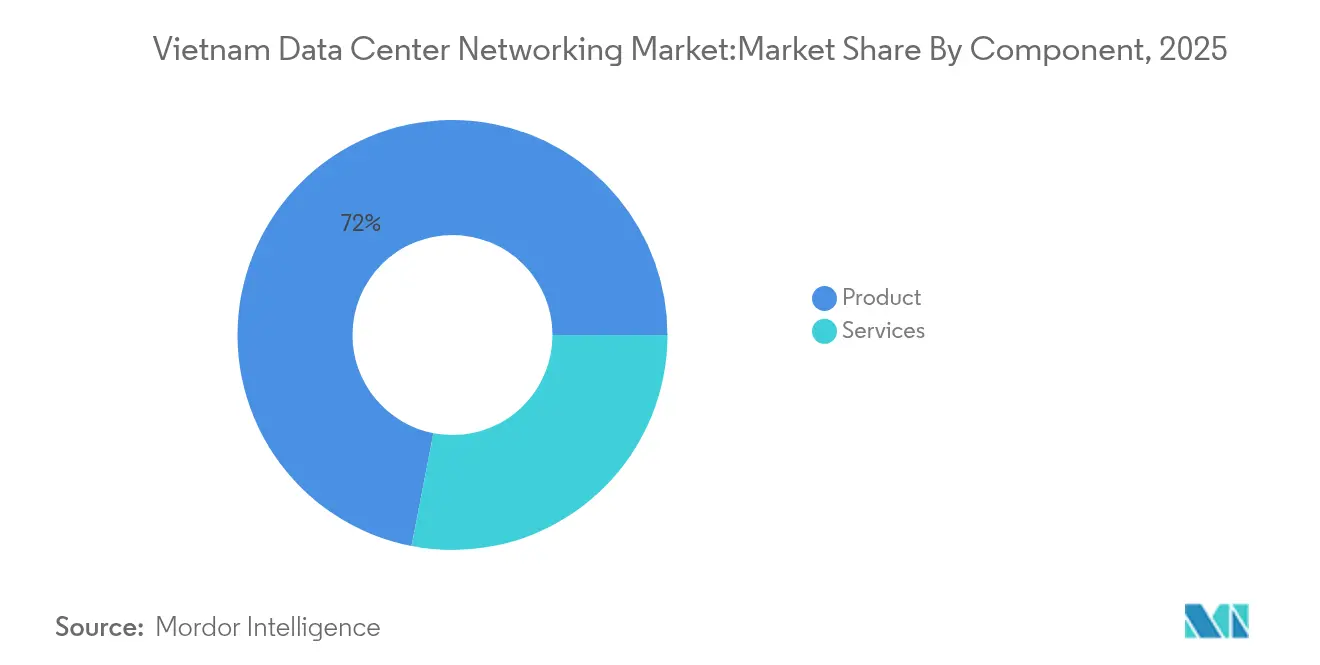

- By component, products held 71.95% of the Vietnam data center networking market share in 2025; Services are projected to log the fastest 6.88% CAGR to 2031.

- By end-user, IT and Telecommunications led with 35.30% revenue share in 2025, while Manufacturing and Industrial is poised for the highest 7.05% CAGR through 2031.

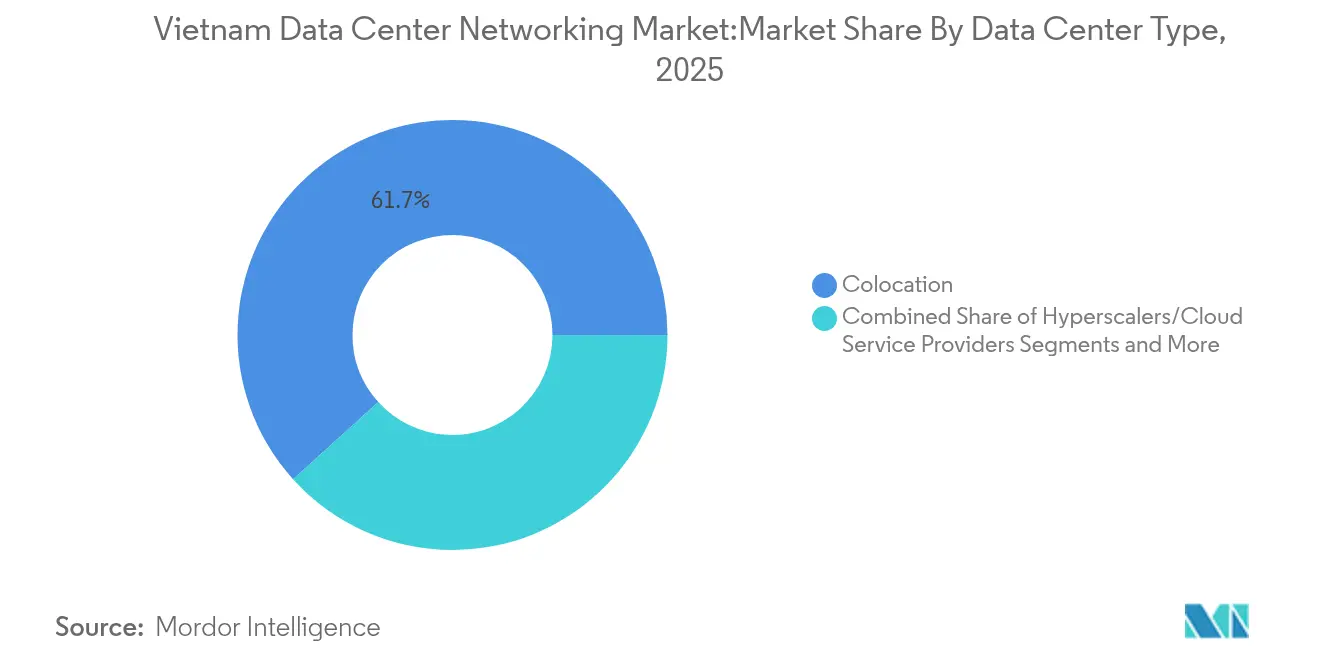

- By data-center type, colocation facilities captured 61.70% share of the Vietnam data center networking market size in 2025; Hyperscalers and Cloud Service Providers are forecast to grow at 7.95% CAGR toward 2031.

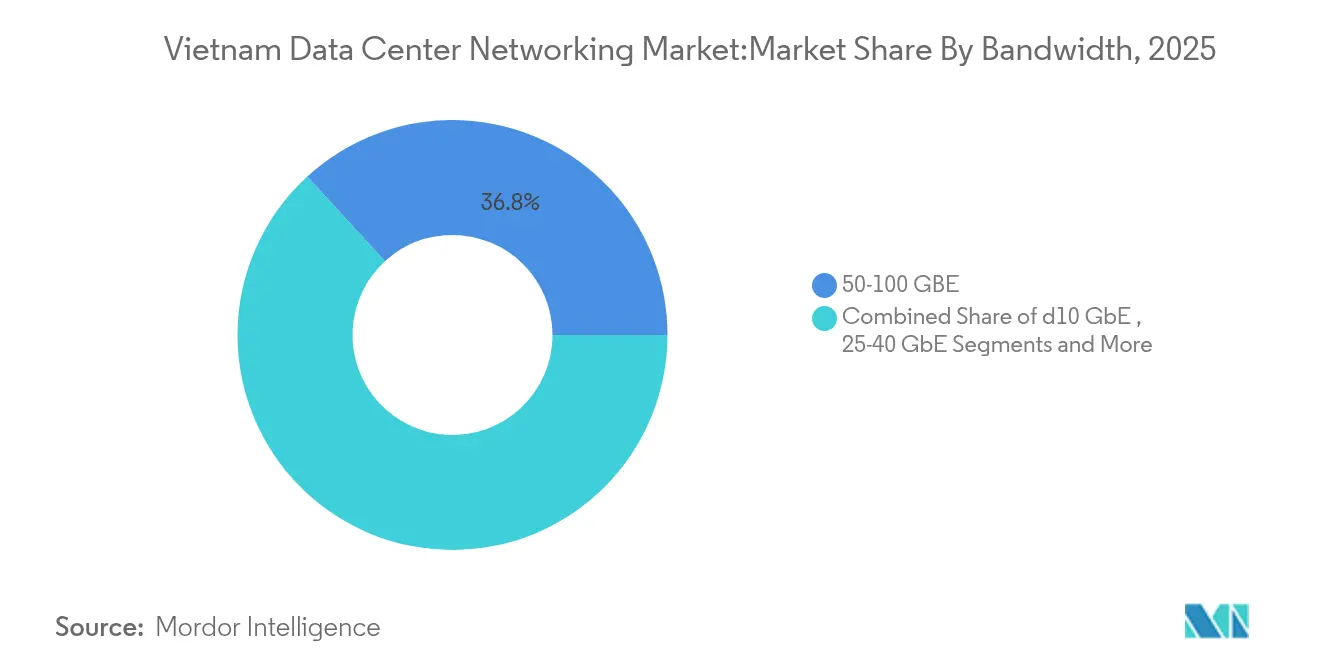

- By bandwidth, the 50-100 GbE class commanded 36.80% of the Vietnam data center networking market size in 2025, whereas greater than 100 GbE deployments should advance at an 8.35% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam represents one dimension of a structure that spans multiple countries, continents and economic zones. Our global data center networking market report covers details on that full structure.

Vietnam Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing hyperscale and cloud CAPEX in Vietnam | +1.8% | National, concentrated in Ho Chi Minh City and Hanoi | Medium term (2-4 years) |

| Surge in edge-computing needs for smart-city and manufacturing projects | +1.2% | National, with early gains in Ho Chi Minh City, Da Nang, Binh Duong | Long term (≥ 4 years) |

| Government incentives (National DC Strategy 2025) | +1.5% | National | Short term (≤ 2 years) |

| Shift toward SDN and intent-based networking | +0.9% | National, enterprise-focused | Medium term (2-4 years) |

| 5G rollout driving DC router refresh | +1.1% | National, telecom operator-led | Short term (≤ 2 years) |

| Corporate ESG mandates favoring energy-efficient silicon | +0.7% | National, multinational enterprise-focused | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing hyperscale and cloud CAPEX in Vietnam

Hyperscale builds now dominate large-ticket ICT spending as operators race to satisfy data-localization rules and regional hub ambitions. Viettel’s USD 261 million, 140 MW campus sets a new domestic benchmark, offering 10 kW racks that are optimised for AI workloads. [1]Viettel Group, “Viettel launches 140 MW data center,” viettel.com.vn VNPT’s 23,000 m² Hanoi facility with 2,000 racks supports 2 Gbps per rack, underscoring the rapid transition from 1 GbE to 25 GbE and 100 GbE switching backbones. Government targets calling for 870 MW of national capacity by 2030 underpin multi-year demand for high-bandwidth routing, optical-transport, and software-defined fabrics. Foreign cloud providers such as Alibaba Cloud have announced local zones to comply with storage rules, bringing new procurement volume to the Vietnam data center networking market.

Surge in edge-computing needs for smart-city and manufacturing projects

Samsung’s USD 20 billion cluster—producing 925 million handsets—operates thousands of real-time quality-control sensors that require local compute nodes and low-latency Ethernet fabrics. Foxconn’s deployment of 2,500 VDIs across six plants demonstrates the shift toward micro data centers and SDN controllers at factory floors. Binh Duong and Da Nang city programs add public-sector edge demand, driving incremental switch and firewall shipments. As operators densify 5G radios, tower-based micro data centers further enlarge the Vietnam data center networking market footprint.

Government incentives (National DC Strategy 2025)

Mandatory in-country processing for critical citizen and enterprise data forces cloud migrations onto domestic sites. The National Digital Transformation Programme stipulates 100% cloud adoption for state agencies by 2030, while Project 06’s biometric identity roll-out already serves 50 million citizens. Tax holidays and land-lease discounts for semiconductor and AI projects lighten capex burdens and catalyse facility build-outs. Two new green data centers totalling 241.5 MW are slated for completion by 2025, further enlarging addressable switch and router pools.

Shift toward SDN and intent-based networking

Vietnam International Bank cut transaction latency 85% after migrating 400 apps to Cisco Application Centric Infrastructure, enabling near-monthly mobile-banking feature releases. [2]Cisco Systems, “VIB accelerates with Cisco ACI,” cisco.com Banking digitisation—93% of institutions pursue tech upgrades—creates a sustained appetite for controller-based fabrics that automate policy, security, and QoS. Huawei’s intent-based portfolio resonates with enterprises wary of single-vendor lock-in. Manufacturing fabs also need rapid, policy-driven network re-configurations when production lines switch SKUs, lifting SDN penetration across the Vietnam data center networking market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export-control-driven ASIC lead-time risk | -1.4% | Global supply chain affecting Vietnam | Short term (≤ 2 years) |

| Shortage of advanced network-architecture talent | -0.8% | National, concentrated in major cities | Medium term (2-4 years) |

| Rising electricity tariffs eroding TCO | -0.6% | National | Long term (≥ 4 years) |

| Persistent cybersecurity gaps in enterprises | -0.5% | National, SME-focused | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export-control-driven ASIC lead-time risk

Advanced switching silicon now requires 40-60 week lead times because of expanded U.S. dual-use controls, doubling historical norms and inflating capex.[3]Bureau of Industry and Security, “Commerce Control List updates,” commerce.govVietnam still imports USD 50 billion in electronic parts annually, exposing local data-center builds to shipment slips and price spikes. Global surveys show 44% of operators suffered outages tied to parts shortages, underscoring operational risk within the Vietnam data center networking market.

Shortage of advanced network-architecture talent

Vietnam counts only 6,000 semiconductor engineers yet targets 1 million technology workers by 2030. Even with Cisco’s Networking Academy certifying 100,000 professionals, demand for AI-ready, high-density data-center designers outstrips supply. The skills gap raises labor costs, elongates deployment schedules, and compels many operators to outsource network operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Products Retain Revenue Dominance

Products generated 71.95% of Vietnam data center networking market revenue in 2025, reflecting the hardware-intensive stage of the country’s digital build-out. Core-to-edge switch refreshes from 1 GbE to 25 GbE and 100 GbE contribute the bulk, while router upgrades align with 5G backhaul expansion. Storage-area networking, application delivery controllers, and next-generation firewalls add incremental volume as data-localization laws amplify in-country storage and security needs. The Vietnam data center networking market size for Products is expected to widen in absolute terms even as growth decelerates relative to Services.Services, though only 28.05% of the 2025 spend, will advance at a 6.88% CAGR through 2031. Skill shortages make professional services indispensable for design, migration, and lifecycle support. Managed network services are especially attractive to mid-sized manufacturers and banks seeking outcome-based contracts that trim capex and de-risk operations. As SDN and intent-based platforms proliferate, vendors earn recurring revenue from controller licensing, network-analytics subscriptions, and security-policy automation, reinforcing the services uptrend across the Vietnam data center networking industry.

By End-User: Telecom Leads, Manufacturing Rises Fast

Telecom and IT operators commanded 35.30% of 2025 revenue, mirroring Viettel, VNPT, and FPT’s aggressive 5G and cloud rollouts. Techcombank’s LinuxONE stack that quadrupled transaction throughput demonstrates how financial institutions also drive enterprise-grade routing and switching demand. Government projects tied to national digital identity broaden the user base, while media, healthcare, and education add new workloads such as UHD streaming and telehealth services.Manufacturing and Industrial verticals, buoyed by China-plus-one relocations, are poised for a 7.05% CAGR. Samsung’s factories in Thai Nguyen and Bac Ninh require AI-enabled defect inspection and IoT telemetry, prompting micro data center and high-bandwidth switch installations. Industrial parks replicate this template, ensuring that the Vietnam data center networking market expands beyond the traditional metro hubs.

By Data-Center Type: Colocation Dominates Today

Colocation facilities accounted for 61.70% of the Vietnam data center networking market share in 2025. Viettel IDC, CMC Telecom, and VNPT secure enterprise and public-sector workloads that want Tier III uptime without heavy upfront capex. High-density colocation suites already offer 10 kW racks, setting the stage for AI hardware adoption.Hyperscalers and Cloud Service Providers will post an 7.95% CAGR, the fastest segment growth. Alibaba Cloud’s planned local zone and Viettel’s 140 MW campus illustrate the hyperscale pivot. These facilities need leaf-spine fabrics, 400 GbE aggregation, and automated optics, lifting the Vietnam data center networking market size substantially over the forecast period.

By Bandwidth: Migration to greater than 100 GbE Accelerates

The 50-100 GbE tier held 36.80% share in 2025, balancing cost and performance for most enterprises. VNPT’s engineering rule of 2 Gbps per rack reflects typical design in current builds. Legacy ≤10 GbE links persist in branch and edge sites, while 25-40 GbE serves as the mainstream migration path. 100 GbE is the fastest-growing tier at 8.35% CAGR. Viettel’s new data center supports average rack power of 10 kW and up to 60 kW, necessitating 400 GbE spine connectivity. Cisco and NVIDIA’s Spectrum-X roadmap provides integrated 400/800 GbE AI fabrics, widening availability of ultra-high-speed options. The Asia Direct Cable’s 50 Tbps link supplies the long-haul capacity to knit these data centers together.

Geography Analysis

Ho Chi Minh City and Hanoi anchor the Vietnam data center networking market thanks to robust telecom backbones, data-ready power grids, and proximity to corporate headquarters. Ho Chi Minh City hosts Viettel’s 140 MW super facility and NTT’s Saigon Hi-Tech Park build, solidifying its role as the primary hyperscale cluster. Municipal authorities’ smart-city roadmap mandates pervasive IoT, necessitating edge nodes in district offices and public transport corridors. Hanoi, the administrative and R&D center, benefits from Samsung’s USD 220 million research hub and VNPT’s latest 2,000-rack data center. National digital-government workloads bring low-latency requirements that boost premium routing and cybersecurity spend. Da Nang emerges as a third pole with six operational facilities and submarine-cable landing stations offering 90 Tbps of bandwidth. Provincial zones such as Binh Duong, Thai Nguyen, and Bac Ninh leverage manufacturing clusters to justify micro data centers and 5G edge nodes. Federal infrastructure plans allocating USD 36 billion in 2025 for roads and fiber backbones tighten latency between these growth corridors, deepening penetration of the Vietnam data center networking market nationwide.

Mordor Intelligence tracks the data center networking market across other major regions such as Europe, Africa, and North America, with additional country-level coverage spanning Taiwan, China, Poland, Nigeria, United States, and France, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The Vietnam data center networking market combines state-owned telecom incumbents with multinational vendors that localise production. Viettel IDC’s 40% service share and VNPT’s cloud expansion give domestic firms purchasing scale, but they depend on Cisco, HPE, Juniper, and Huawei for switching, routing, and SDN controllers. Cisco’s relocation of 30% of its global hardware assembly to Vietnam strengthens supply resiliency and lowers import duties, enabling competitive pricing.

Strategic differentiation now hinges on AI optimisation and sustainability. Cisco’s Silicon One plus NVIDIA Spectrum-X stack targets energy-efficient 400 GbE neural-network training clusters, addressing ESG mandates. FPT’s AI Factory, built with NVIDIA and HPE, illustrates a Vietnamese integrator moving up the value chain. Specialist players such as Broadcom and Intel supply merchant silicon, while domestic firms like CMC Telecom develop SD-WAN overlays tailored to local compliance rules.

Market entry barriers remain moderate. Colocation operators procure off-the-shelf leaf-spine fabrics, letting new entrants like NTT and ST Telemedia establish footprints through greenfield builds. Conversely, edge-computing and SME cloud remain fragmented, creating white-space for startups focused on software-defined security or intent-based network analytics. Overall, competition is vigorous but not prohibitive, which sustains innovation for end-users of the Vietnam data center networking industry.

Vietnam Data Center Networking Industry Leaders

Cisco Systems Inc.

Arista Networks Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise

Huawei Technologies Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cisco expanded its partnership with NVIDIA to integrate Silicon One with Spectrum-X, delivering unified AI-ready data-center networking architectures.

- June 2025: Prime Minister Phạm Minh Chính met Cisco Asia-Pacific leaders; Cisco pledged to help certify 100,000 Vietnamese professionals and explore a semiconductor-training hub.

- June 2025: Redis Ltd. and BNH Technology Consulting partnered to broaden Redis Enterprise adoption for real-time data workloads in Vietnam.

- May 2025: Vietnam approved a 2025-2035 STEM workforce program aimed at scaling high-tech talent pipelines for AI and biotech.

Vietnam Data Center Networking Market Report Scope

Data center networking refers to the set of technologies, protocols, and hardware used to connect physical and network-based devices and manage the network infrastructure, storage, and processing of applications and data. Data center networking is very critical for 100% uptime of data centers. In the current web-connected world, business workloads are executed on single computers, hence leading to the need for data center networking. Networks provide servers, clients, applications, and middleware with a standard plan to stage the execution of workloads and also to manage access to the data produced.

The Vietnam data center networking market is segmented by component type (product (Ethernet switches, routers, storage area network (SAN), application delivery controller (ADC), and other networking equipment), services (installation & integration, training & consulting, and support & maintenance)), by end-user (IT & telecommunication, BFSI, government, media & entertainment, and other end users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Products | Ethernet Switches |

| Routers | |

| Storage Area Network (SAN) | |

| Application Delivery Controllers (ADC) | |

| Network Security Appliances | |

| Software-Defined Networking (SDN) Controllers | |

| Optical Interconnects | |

| Services | Installation and Integration |

| Training and Consulting | |

| Support and Maintenance | |

| Managed Network Services |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Defense |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Other End-Users |

| Colocation |

| Hyperscalers/Cloud Service Providers |

| Edge/Micro Data Centers |

| less than or equal to10 GbE |

| 25-40 GbE |

| 50-100 GbE |

| Greater than 100 GbE |

| By Component | Products | Ethernet Switches |

| Routers | ||

| Storage Area Network (SAN) | ||

| Application Delivery Controllers (ADC) | ||

| Network Security Appliances | ||

| Software-Defined Networking (SDN) Controllers | ||

| Optical Interconnects | ||

| Services | Installation and Integration | |

| Training and Consulting | ||

| Support and Maintenance | ||

| Managed Network Services | ||

| By End-User | IT and Telecommunications | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Defense | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial | ||

| Other End-Users | ||

| By Data-Center Type | Colocation | |

| Hyperscalers/Cloud Service Providers | ||

| Edge/Micro Data Centers | ||

| By Bandwidth | less than or equal to10 GbE | |

| 25-40 GbE | ||

| 50-100 GbE | ||

| Greater than 100 GbE | ||

Key Questions Answered in the Report

How large is the Vietnam data center networking market today?

The Vietnam data center networking market reached USD 487.44 million in 2026 and is projected to hit USD 676.63 million by 2031.

Which component category is expanding the fastest?

Services will grow at 6.88% CAGR to 2031, driven by demand for design, integration, and managed network operations.

Why are greater than 100 GbE deployments accelerating?

AI workloads, hyperscale builds, and new submarine cables require ultra-high throughput, moving many operators directly to 400 GbE classes.

What role do localization laws play in market growth?

Rules mandating domestic storage of Vietnamese user data compel foreign and local firms to build in-country facilities, boosting hardware and services demand.

Page last updated on: