Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.92 Billion |

| Market Size (2026) | USD 6.3 Billion |

| Market Size (2031) | USD 8.58 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

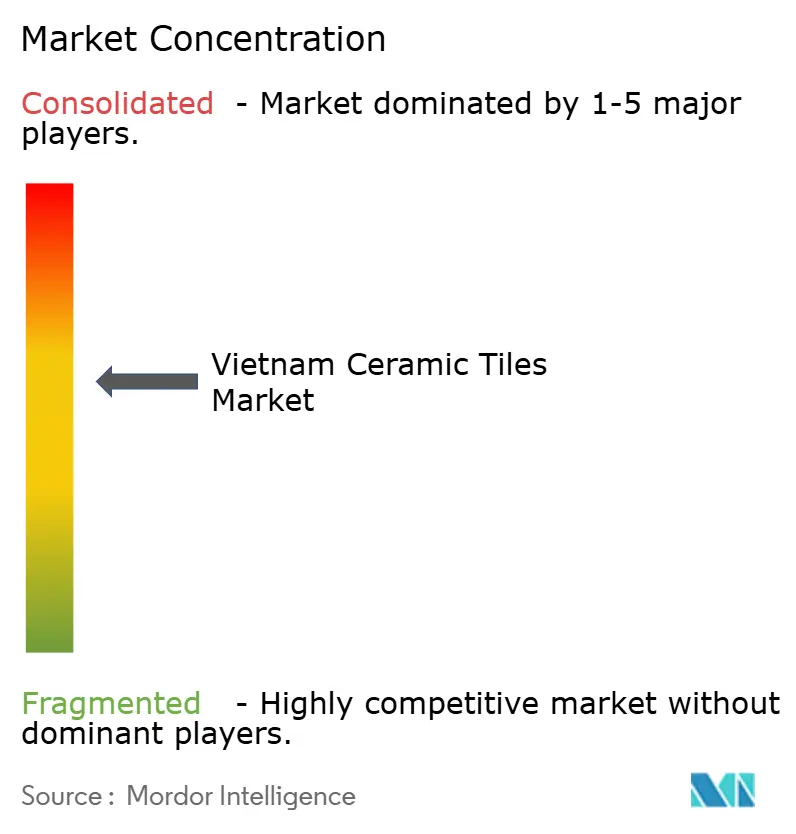

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Ceramic Tiles Market Analysis by Mordor Intelligence

The Vietnam ceramic tiles market size is expected to grow from USD 5.92 billion in 2025 to USD 6.3 billion in 2026 and is forecast to reach USD 8.58 billion by 2031 at 6.39% CAGR over 2026-2031. Construction activity rose 7% annually from 2024 to 2027 as the government earmarked USD 30 billion for public works programs, creating a firm underpinning for fresh tile demand[1]Source: U.S. Department of Commerce, “Vietnam Building Materials Outlook 2025,” commerce.gov. Steady GDP growth of 6-6.5% in 2024 and manufacturing expansion of 8-9% stimulated household incomes, enabling wider adoption of higher-value porcelain and glazed formats. Residential projects remained the single largest consumption base because rapid urban migration lifted housing starts, yet hotel, retail, and transportation hubs emerged as the fastest new outlet for premium slabs. Fragmented competition, expansive export linkages, and rising online sales together foster multiple entry points for investors looking to build scale within the Vietnam ceramic tiles market.

Key Report Takeaways

- By end-user, residential applications held 55.12% of the Vietnam ceramic tiles market share in 2025; commercial applications are advancing at a 7.42% CAGR through 2031.

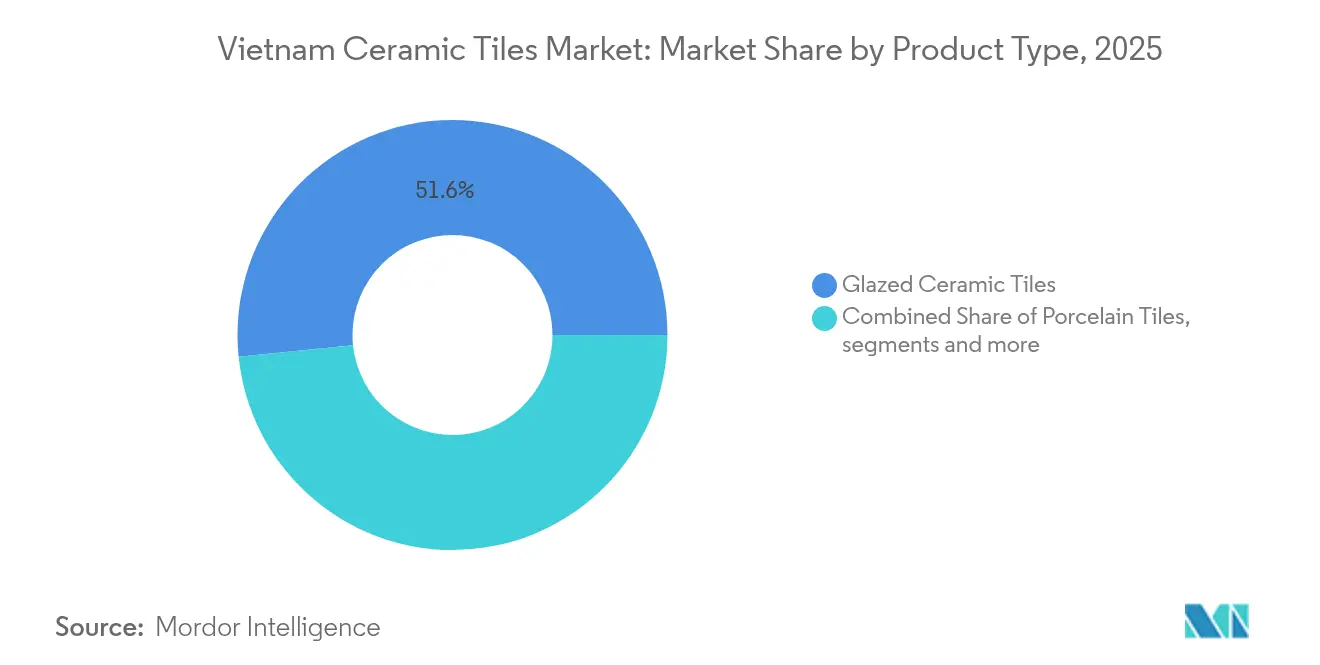

- By product type, glazed ceramic tiles captured 51.62% share of the Vietnam ceramic tiles market size in 2025; porcelain tiles are forecast to grow at an 8.01% CAGR to 2031.

- By application, floor tiles accounted for a 60.35% share of the Vietnam ceramic tiles market size in 2025; roofing tiles are set to record a 6.54% CAGR through 2031.

- By construction type, new construction commanded a 65.25% share of the Vietnam ceramic tiles market size in 2025; renovation is expected to increase at a 6.78% CAGR through 2031.

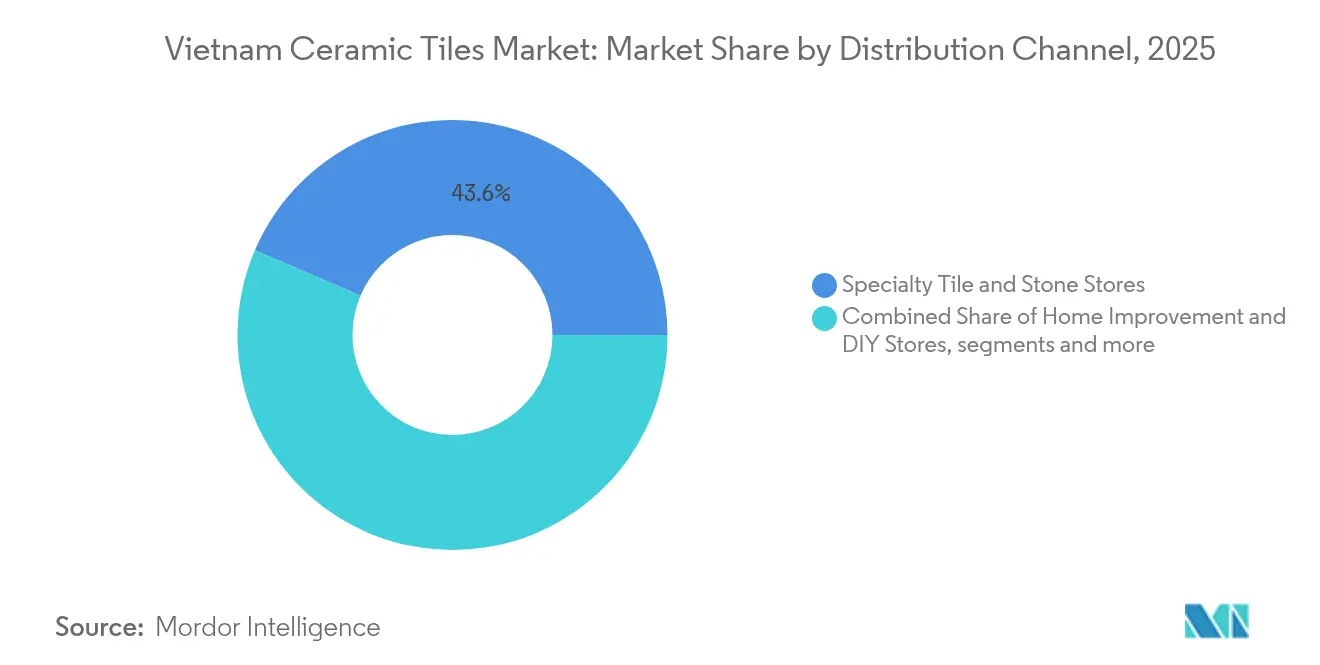

- By distribution channel, specialty tile stores held 43.55% share of the Vietnam ceramic tiles market size in 2025; online retail is poised for an 8.49% CAGR between 2026 and 2031.

- By region, Southern Vietnam led with 39.25% revenue share in 2025; Central Vietnam is projected to expand at a 7.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urbanization & residential housing demand | +1.8% | Ho Chi Minh City & Hanoi | Medium term (2-4 years) |

| Government infrastructure investment & smart-city programs | +1.5% | Central & Northern corridors | Long term (≥4 years) |

| Growing middle-class preference for premium aesthetics | +1.2% | Southern core, expanding Central | Medium term (2-4 years) |

| Expansion of commercial real estate & tourism facilities | +0.9% | Coastal metros & urban centers | Short term (≤2 years) |

| Large-format porcelain slabs for energy-efficient cooling | +0.7% | Nationwide, early in industrial zones | Long term (≥4 years) |

| Localized digital ink-jet printing cuts import dependence | +0.4% | Northern manufacturing clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Urbanization & Residential Housing Demand

National urbanization is moving toward the official 60-65% target by 2030, with provincial master plans spurring high-rise neighborhoods and satellite townships [2]Source: Ministry of Construction, “Digital Transformation in Urban Development,” chinhphu.vn. More than 30,000 new condominium units were delivered in northern cities during 2024, and average selling prices in Hanoi’s primary market jumped 36%, signaling a decisive shift toward branded, higher-value finishes. Social-housing mega-schemes worth 16,000 billion VND in Đông Anh alone will add almost 6,900 units in two phases, anchoring volume for mid-priced tiles. Regulatory clarity from newly enacted Land and Housing Laws is shortening project lead times and bolstering developer confidence. As a result, the Vietnam ceramic tiles market continues to derive its core volume from flooring packages in mass-housing blocks where purchase decisions hinge on durability and ready availability.

Government Infrastructure Investment & Smart-City Programs

A record 230 public works broke ground simultaneously in August 2025, illustrating the government’s commitment to transport, education, and urban resilience. Digital governance reforms have pushed 95% of construction permits online, slashing administrative delays and widening tender opportunities for local tile makers. Flagship mixed-use ventures such as the 2,870-hectare Vinhomes Green Paradise emphasize sustainability and premium building envelopes that heavily specify porcelain slabs. Provincial authorities now steward their smart-city plans, attracting Hong Kong and Shenzhen investors to develop sensor-enabled districts that require long-life, low-maintenance ceramic cladding. Such capital flows ripple across the Vietnam ceramic tiles market and create multi-year order visibility for domestic producers.

Growing Middle-Class Preference for Premium Aesthetics

Vietnam’s rising disposable income base is steering consumers toward larger 60 × 120 cm formats and high-gloss marble looks, reinforcing the 52% share of glazed tiles. Manufacturers have responded by installing Italian ink-jet lines capable of 400 DPI resolution that mimic natural stone and wood with fine tonal gradations. Custom design studios are collaborating with local artisans to launch limited-edition surfaces, tying contemporary interiors to heritage motifs and widening margins. The cultural revival of traditional Cham craft has sparked boutique demand for decorative mosaics that complement mass-produced offerings. This blended premiumization trend positions porcelain as the fastest-expanding product category inside the Vietnam ceramic tiles market.

Large-Format Porcelain Slabs for Energy-Efficient Cooling

Research on humidity-controlling oxides shows that advanced tiles can lower roof surface temperatures by up to 42 °C, translating into 30% cooling-energy savings [3]Source: MDPI, “Humidity-Controlling Ceramic Tiles for Passive Cooling,” mdpi.com. . Pilot installations in industrial parks demonstrate how reflective slabs mitigate heat-island effects and align with the national Net-Zero-by-2050 roadmap. Domestic vendors have started marketing 9 mm-thin “cool roof” panels alongside conventional lines, supported by grants for low-carbon building materials. Corporate occupants value the operational cost reductions, accelerating early adoption in factory retrofits. Over the long term, energy-smart surfaces will reinforce porcelain’s growth trajectory in the Vietnamese ceramic tiles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile energy costs impacting production margins | -0.8% | Northern firing hubs | Short term (≤2 years) |

| Intensifying competition from low-cost imports | -0.6% | Ports & border provinces | Medium term (2-4 years) |

| Production overcapacity driving price pressures | -0.5% | Nationwide clusters | Medium term (2-4 years) |

| Tightening environmental & water-use regulations | -0.4% | Industrial zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Energy Costs Impacting Production Margins

Kilns consume large volumes of natural gas or coal, so spot-price spikes directly erode profitability for Vietnam’s 1,200 tile factories. Many smaller operators still run legacy tunnel kilns with thermal efficiency below 40%, magnifying cost swings. Pilot projects exploring hydrogen-ready burners or rooftop photovoltaics promise relief but demand capital outlays that micro-enterprises cannot shoulder quickly. Resolution 77’s proposed tax relief on imported kiln parts may ease transition, yet short-term margin compression remains likely. Consequently, the Vietnamese ceramic tiles market could experience consolidation as only energy-savvy producers maintain cost competitiveness.

Intensifying Competition from Low-Cost Imports

Regional suppliers, chiefly from China, deliver both raw materials and finished formats at aggressive prices, challenging domestic brands on commodity ranges. Customs data indicate that China retains a 60% share of ceramic inputs shipped into Vietnam, underscoring dependency risks [4]Source: General Department of Vietnam Customs, “Import Structure of Ceramic Inputs 2024,” customs.gov.cn.. Vietnamese firms counter by branding themselves as premium, with top players fetching an 80-90% price premium over low-end imports, but sustaining that gap requires constant design refreshes and process upgrades. The Ministry of Industry and Trade has tightened import-licensing rules to encourage local sourcing, yet loopholes persist through informal border channels. Import pressure, therefore tempers margin expansion in the Vietnamese ceramic tiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Porcelain Shapes Demand Outlook

Porcelain already fuels the premium story within the Vietnam ceramic tiles market, growing at 8.01% CAGR through 2031 as builders pivot to large-format slabs for upscale villas and grade-A offices. Glazed tiles retained a dominant 51.62% Vietnam ceramic tiles market share in 2025 because of their design versatility and competitive price points. Production advances, such as full-body ink-penetration technology, enable porcelain panels to mimic marble veins with 400 DPI precision while delivering superior flexural strength. Domestic brands leverage this performance edge to access export niches in Japan and Australia, where frost resistance and water absorption limits are stringent. In parallel, cultural revival in craft clusters feeds demand for decorative mosaics that enrich boutique hotels and residential accent walls.

Unglazed heavy-duty formats maintain relevance for logistics parks, yet their share gradually declines as porcelain achieves cost parity. Mosaic and patterned subsegments benefit from bespoke orders tied to tourism complexes that narrate regional heritage in lobbies and façades. Research on humidity-responsive ceramics signals future cross-over products that combine aesthetics with passive cooling, potentially refreshing mature categories. As innovation cycles accelerate, producers that integrate design, durability and thermal performance secure pricing power. Overall, product-level diversification is reinforcing value capture inside the Vietnam ceramic tiles market.

By Application: Flooring Anchors Volume While Roofing Emerges

Floor tiles contributed 60.35% of national volume in 2025 because every new apartment and retail outlet prioritizes resilient, easy-clean surfaces underfoot; this anchor segment keeps the Vietnam ceramic tiles market size substantial and predictable. Innovations such as nano-glaze antibacterial finishes help local brands upsell within flooring budgets. In contrast, roofing tiles headline growth at 6.54% CAGR thanks to cool-roof mandates in dense cities where energy codes now reward solar-reflective claddings. Demonstration projects record indoor temperature drops of 3-5 °C, driving municipal procurement for public schools and clinics.

Wall cladding remains a stable mid-volume category, but porcelain façade panels gain investor interest as glass-aluminum systems face cost inflation. Feature walls in cafes and coworking hubs increasingly use digitally printed motifs that replicate terrazzo or terrazul aesthetics without on-site terrazzo waste. Inside bathrooms, slip-rated surfaces and integrated groutless sheets simplify cleaning, supporting tile replacement cycles in hospitality revamps. As developers juggle cost, energy, and maintenance criteria, application choice becomes multidimensional, reinforcing balanced expansion within the Vietnam ceramic tiles market.

By End-User: Commercial Projects Outpace Housing Gains

Residential construction generated 55.12% of 2025 turnover as government stimulus for affordable housing underwrote mass demand for entry-level ranges. Nevertheless, the commercial segment now scales faster, expanding at a 7.42% CAGR as airports, malls, and data centers advance from planning to execution stages. Tourism-linked ventures along the central coast specify designer porcelain to differentiate guest experiences, lifting average selling prices. Hospital and education budgets also allocate more for hygienic, low-VOC materials, prompting tile manufacturers to certify ISO 14001 and cradle-to-grave credentials. As foreign direct investors lease additional warehouse and office space, the commercial slice of the Vietnam ceramic tiles market widens further.

Transport hub development represents a significant commercial opportunity, with projects like the T3 passenger terminal at Tan Son Nhat International Airport demonstrating the scale of infrastructure construction requiring specialized ceramic tile solutions for high-traffic applications. The hospitality subsegment benefits from Vietnam's tourism recovery and expansion, while retail spaces experience strong absorption driven by local and overseas retailers, particularly from China, creating sustained demand for aesthetic and durable ceramic tile solutions.

By Construction Type: Renovation Captures Up-Cycle Investment

New-build contracts still accounted for two-thirds of 2025 sales, bolstered by 230 mega-projects initiated in August 2025 that require long runs of standard floor and wall modules. Even so, the renovation stream is gaining momentum at 6.78% CAGR as a maturing building stock seeks energy upgrades and aesthetic refreshes. Rising resale values incentivize homeowners to re-tile kitchens and bathrooms with premium marble-look planks. Industrial landlords retrofit aged roofs with radiant panels to cut cooling bills and attract green-minded tenants. As environmental rules tighten, non-compliant linings must be replaced, feeding aftermarket demand inside the Vietnam ceramic tiles market.

The construction type segmentation reflects broader economic trends, with government initiatives launching 230 large-scale construction projects in August 2025, spanning transportation, urban development, and educational sectors that primarily involve new construction applications. Renovation activities gain support from improved building regulations and environmental standards, with new regulations like Circular 01/2025/TT-BNNMT establishing environmental quality standards that encourage building upgrades to meet noise, vibration, and environmental compliance requirements.

By Distribution Channel: E-Commerce Accelerates Reach

Specialty tile outlets delivered 43.55% of 2025 revenue because professional contractors still prefer tactile inspection and bulk delivery services. Yet online portals are propelling an 8.49% CAGR by combining augmented-reality visualization and next-day sample dispatch. Leading manufacturers have linked inventory databases to VR showrooms, allowing designers in Da Nang to preview Ho Chi Minh City stock in real time. Home-improvement chains capitalize on DIY trends as middle-class consumers undertake minor upgrades without hiring installers. Meanwhile, direct-to-site logistics platforms streamline procurement for mega-projects, compressing lead times and lowering wastage. This omnichannel evolution broadens market access and price transparency across the Vietnamese ceramic tiles market.

Home improvement and DIY stores benefit from rising middle-class preferences for premium aesthetics and self-directed renovation projects, while direct sales to contractors remain important for large-scale commercial and infrastructure projects. The distribution landscape reflects broader retail trends, with shopping malls in major cities experiencing strong absorption driven by local and overseas retailers, creating opportunities for ceramic tile showrooms and specialty retail concepts. Digital marketing gains prominence through social media platforms, as demonstrated by traditional pottery villages like Bình Đức using Facebook and TikTok for marketing, leading to growing customer bases and increased production demand.

Geography Analysis

Southern Vietnam generated 39.25% of nationwide tile turnover in 2025, anchored by Ho Chi Minh City’s diversified economy and a pipeline of rail, bridge, and smart-district initiatives exceeding 620 trillion VND. Mega-projects like the 2,870-hectare Vinhomes Green Paradise marry green infrastructure with premium interiors, ensuring bulk porcelain orders during 2026-2029 fit-out phases. Office, retail, and hospitality tenants increasingly specify low-maintenance ceramics to mitigate humidity and heavy footfall, reinforcing region-wide demand. Private developers also promote terrace-cool roofing for townhouses to counter tropical heat and comply with new green-building incentives. Consequently, the Vietnamese ceramic tiles market finds its largest single regional customer base in the south.

Central Vietnam is forecast to clock the fastest 7.03% CAGR as Đà Nẵng, Thanh Hóa, and neighboring provinces court industrial and tourism capital. The 44 trillion VND Làng Vân eco-resort sets a template for large-scale resilient construction that favors high-performance tiles. Chinese investor Hoa Liên Hồ Nam’s USD 200 million ASEAN Ceramic Valley underscores the zone’s manufacturing potential and promises localized supply for surrounding coastal projects. Provincial BIM mandates streamline approvals, shortening cash-conversion cycles for contractors. Rising air-connectivity and port upgrades further boost commercial fit-out demand, consolidating the growth narrative for the Vietnam ceramic tiles market in the central corridor.

Northern Vietnam maintains steady expansion through established raw-material quarries and cluster infrastructure around Hưng Yên and Bát Tràng. Urbanization master-plans envisage 60-65% urban share by 2030, elevating apartment construction and associated flooring orders. ESG-labeled industrial parks such as Yên Phong II-C attract multinational tenants whose procurement codes specify certified ceramic finishes. Artisanal pottery villages leverage e-commerce to sell decorative pieces that complement industrial lines, keeping cultural identity alive alongside export ambitions. However, energy-cost sensitivity and stricter water-reuse rules require reinvestment, moderating near-term capacity additions. Overall, geographic diversification helps balance supply-demand dynamics within the Vietnam ceramic tiles market.

Competitive Landscape

The Vietnamese tiles industry exhibits moderate fragmentation with established domestic players competing alongside international entrants, creating dynamic competitive intensity that drives innovation and market expansion. Viglacera led 2024 revenues at 11.906 trillion VND and secured a SACMI technology partnership to install digital presses that lift unit yield and design versatility. Royal Group leverages a 3,000-store national network and export lanes into Northeast Asia and Europe, underscoring the necessity of omnichannel distribution for share defense. Emerging mid-tier players focus on energy-efficient quartz blends that command price premiums in green-building projects, illustrating differentiation avenues beyond volume play.

Foreign entrants add competitive tension: Singapore-backed Lares Pte Ltd obtained a USD 193 million license for ASEAN Vietnam Ceramic Valley, pledging 120 million pieces annually and advanced environmental controls. Chinese equipment vendors offer turnkey kilns with 30% fuel-saving guarantees, lowering barriers for capacity additions yet raising oversupply risks. Producers now emphasize life-cycle cost claims, including 50-year façade durability and recyclability, to answer B2B procurement scorecards. Concurrently, OEMs invest in machine vision for end-of-line QC to cut rejects and maintain export grade ratios above 95%. Innovation, sustainability and network reach therefore delineate success factors inside the Vietnam ceramic tiles market.

Strategic M&A interest is rising as energy and environmental compliance inflate capex thresholds. Domestic conglomerates consider bolt-on acquisitions of niche craft houses to fill design gaps and meet rising bespoke demand from boutique hotels. Technology alliances extend beyond Italy to Spanish ink-set suppliers who license new glaze chemistries that slash firing temperatures by 50 °C. Local banks increasingly evaluate ESG metrics before extending working-capital lines, pressuring laggards to upgrade or exit. The evolving playbook thus rewards agile entities that can align product depth, process efficiency and sustainability credentials within the Vietnam ceramic tiles market.

Vietnam Ceramic Tiles Industry Leaders

Viglacera Corporation

Prime Group

Đồng Tâm Group

Taicera Enterprise Company

Thạch Bàn Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Takao Corporation, ranked in FAST500 for the second year, announced a 13 million m² capacity expansion and a distributor network exceeding 250 partners

- August 2025: Authorities in Thanh Hóa granted Lares Pte Ltd a USD 193 million investment certificate to build ASEAN Vietnam Ceramic Valley, targeting 120 million ceramic products per year.

- April 2025: Viglacera showcased four “Green Ecosystem” lines at Coverings, underscoring its shift toward low-impact materials.

Vietnam Ceramic Tiles Market Report Scope

Ceramic tiles are a mixture of clay and other natural materials, such as sand, quartz, and water. They are primarily used in houses, restaurants, offices, shops, and so on, as bathroom walls and kitchen floor surfaces.

The Vietnam ceramic tile market is segmented by product, which includes glazed, porcelain, scratch-free, and other products; by application, including floor tiles, wall tiles, and other applications; by construction type, including new construction and replacement and renovation; and by end-user, including residential and commercial.

The report offers market size and forecasts for the Vietnam ceramic tiles market in terms of revenue (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Northern Vietnam |

| Central Vietnam |

| Southern Vietnam |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Northern Vietnam | |

| Central Vietnam | ||

| Southern Vietnam | ||

Key Questions Answered in the Report

What is the projected value of the Vietnam ceramic tiles market by 2031?

The Vietnam ceramic tiles market is forecast to reach USD 8.58 billion by 2031, growing at a 6.39% CAGR.

Which product segment is expanding the fastest in Vietnam?

Porcelain tiles lead growth with an 8.01% CAGR because builders value their durability and large-format aesthetics.

How significant is online retail to tile distribution in Vietnam?

Online channels are the fastest-growing distribution route at an 8.49% CAGR thanks to AR visualization tools and nationwide delivery options.

Which Vietnamese region is set to record the highest growth in tile demand?

Central Vietnam is expected to post a 7.03% CAGR through 2031, driven by tourism projects and foreign industrial investment.

What major restraint could slow industry growth?

Volatile energy costs remain the leading constraint, potentially shaving 0.8 percentage points off forecast CAGR until efficiency upgrades take hold.

Page last updated on: