Bitumen Membranes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

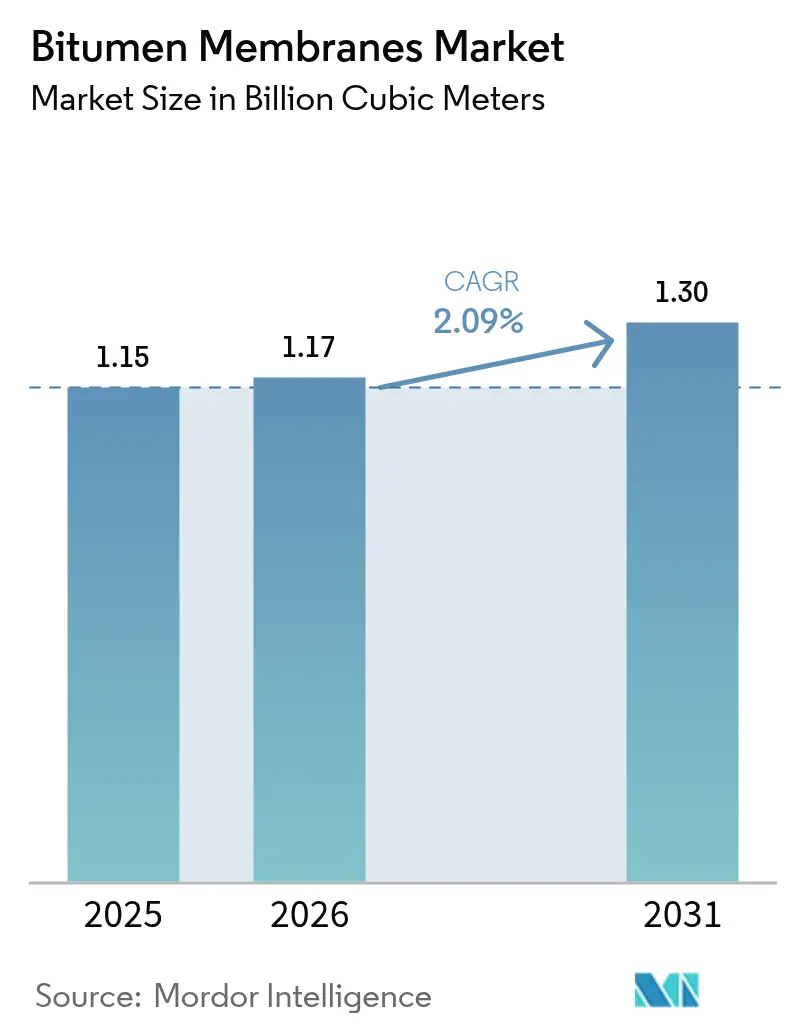

| Market Volume (2026) | 1.17 Billion cubic meters |

| Market Volume (2031) | 1.3 Billion cubic meters |

| Growth Rate (2026 - 2031) | 2.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bitumen Membranes Market Analysis by Mordor Intelligence

The Bitumen Membranes Market size is expected to grow from 1.15 billion cubic meters in 2025 to 1.17 billion cubic meters in 2026 and is forecast to reach 1.3 billion cubic meters by 2031 at 2.09% CAGR over 2026-2031. Stable public-sector capital spending, stricter waterproofing codes, and a shift toward flame-free installation collectively anchor this measured expansion. Contractors weigh lifetime performance and labor savings more heavily than upfront cost, favoring polymer-modified grades that withstand temperature swings and intense rainfall events. Producers leverage regional plants to minimize freight, hedge feedstock swings, and shorten lead times, while crude-linked bitumen price volatility remains the principal cost variable. As self-adhesive solutions displace torch-on systems in fire-restricted zones, manufacturers with proprietary adhesives and cool-roof coatings gain a competitive edge in energy-code-driven retrofit demand.

Key Report Takeaways

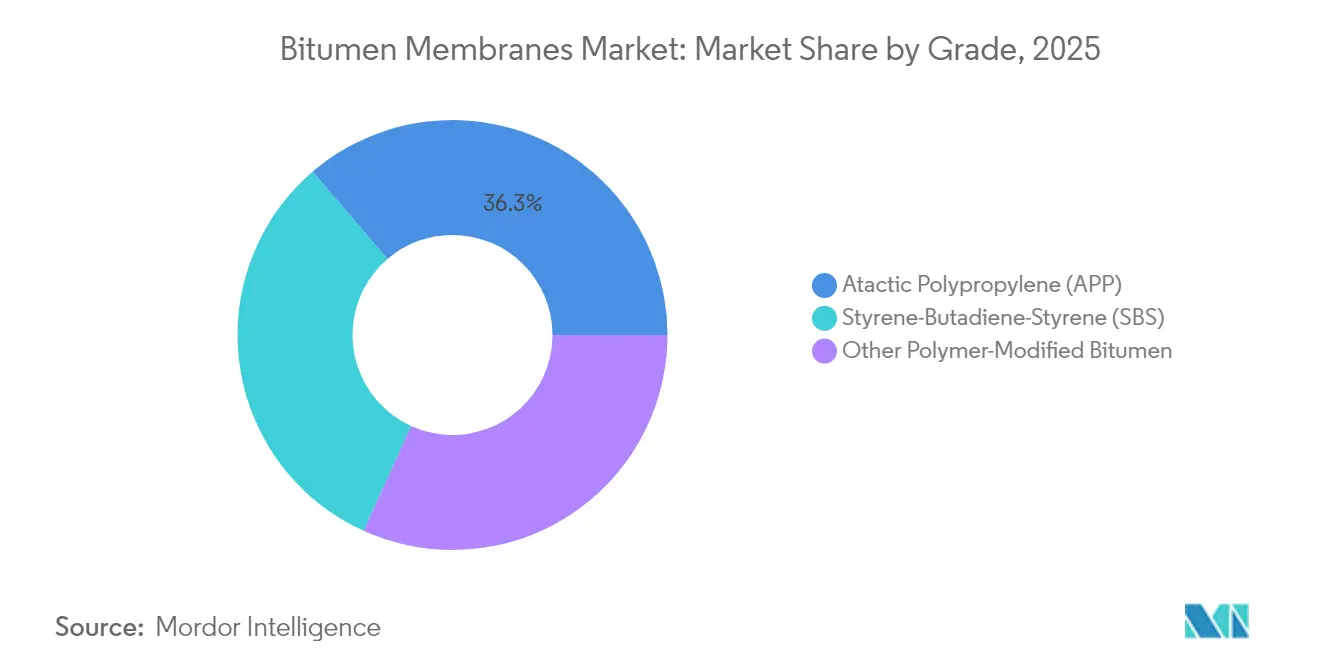

- By grade, APP led with 36.28% volume share in 2025, whereas SBS is advancing at a 2.22% CAGR through 2031.

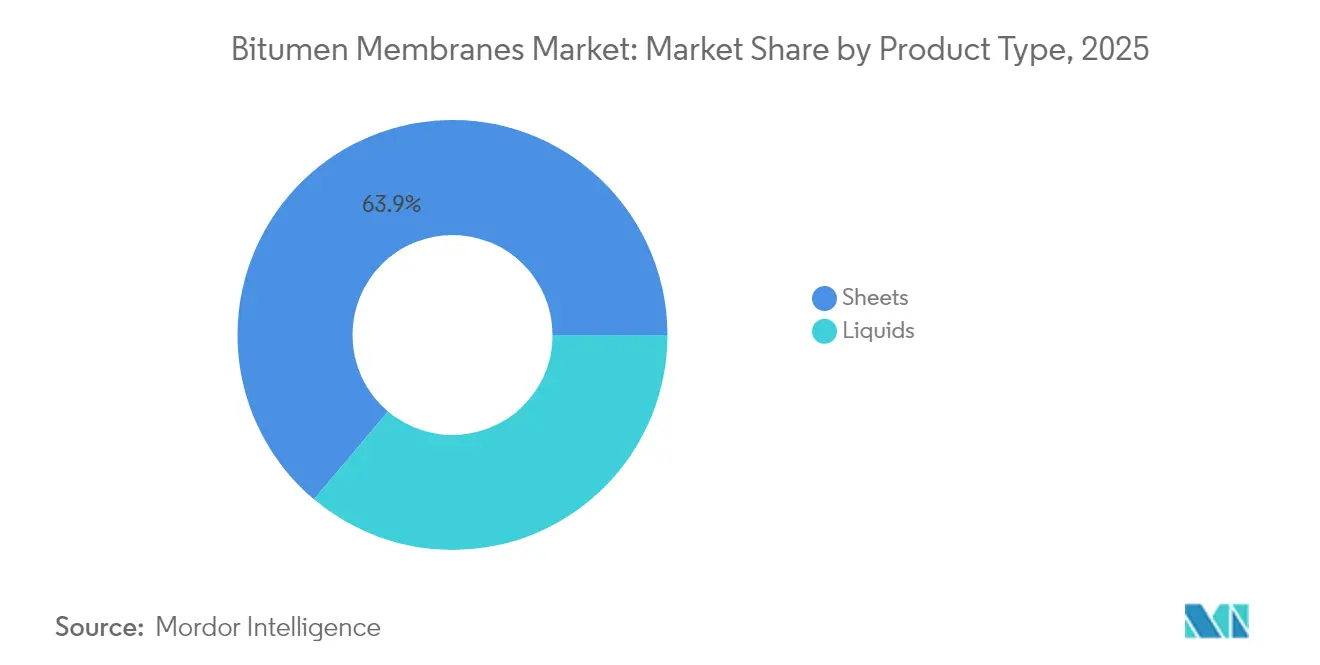

- By product type, sheets accounted for 63.85% of the bitumen membrane market share in 2025, while liquids are projected to log a 2.31% CAGR.

- By application, roofing captured 47.66% of the bitumen membrane market size in 2025; below-grade waterproofing is set to expand at a 2.23% CAGR by 2031.

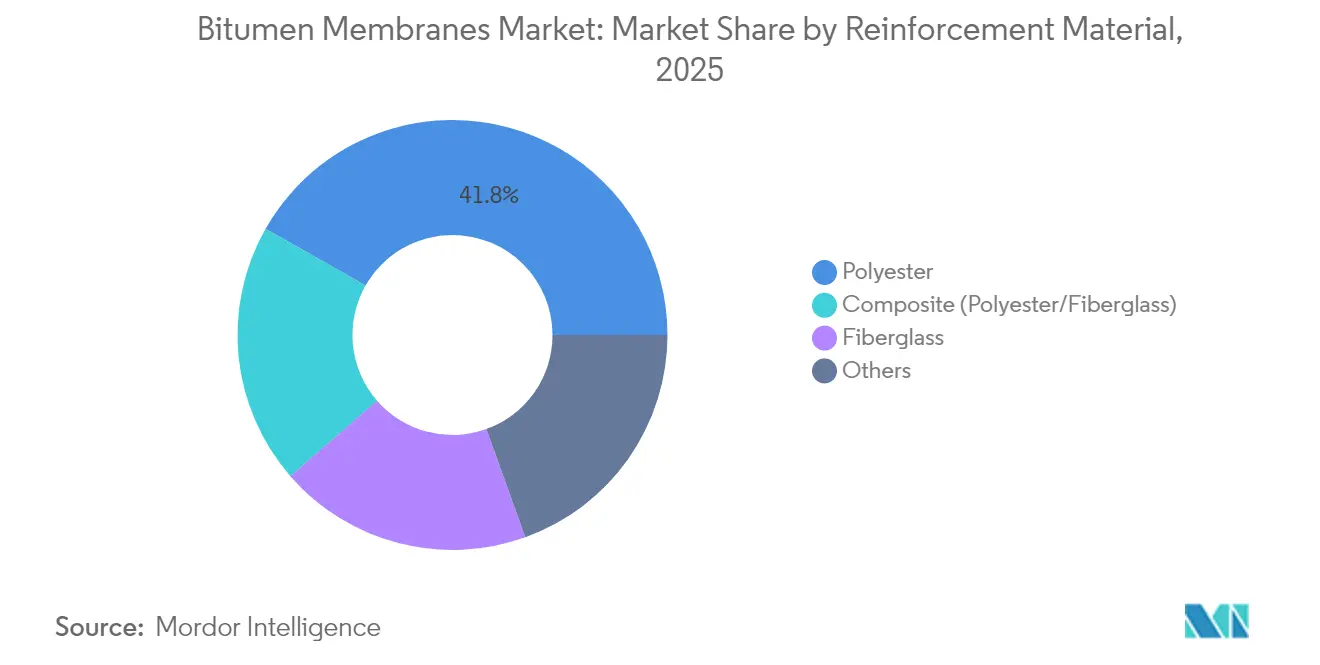

- By reinforcement, polyester dominated with a 41.78% share in 2025, and composite reinforcement is the fastest-growing at a 2.21% CAGR.

- By installation technology, torch-applied held a 35.64% share in 2025, but self-adhesive systems are expected to grow 3.18% CAGR.

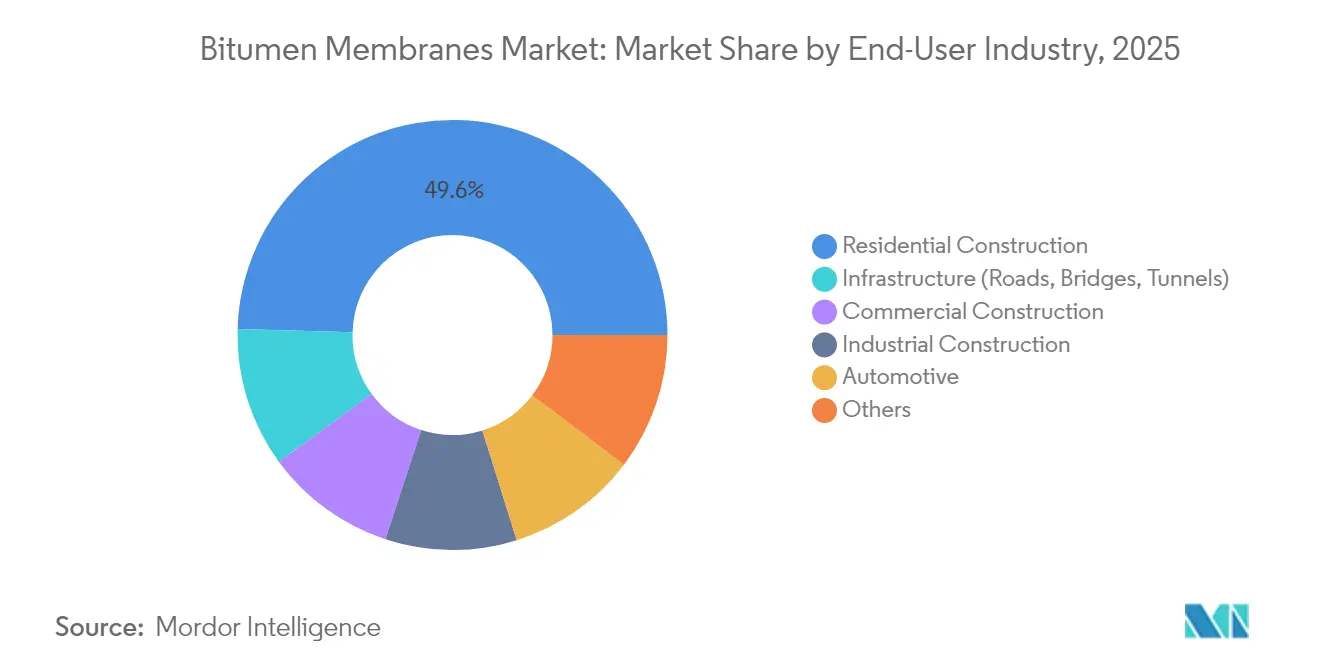

- By end-user, residential construction commanded a 49.55% share in 2025, whereas infrastructure projects posted the highest 2.43% CAGR to 2031.

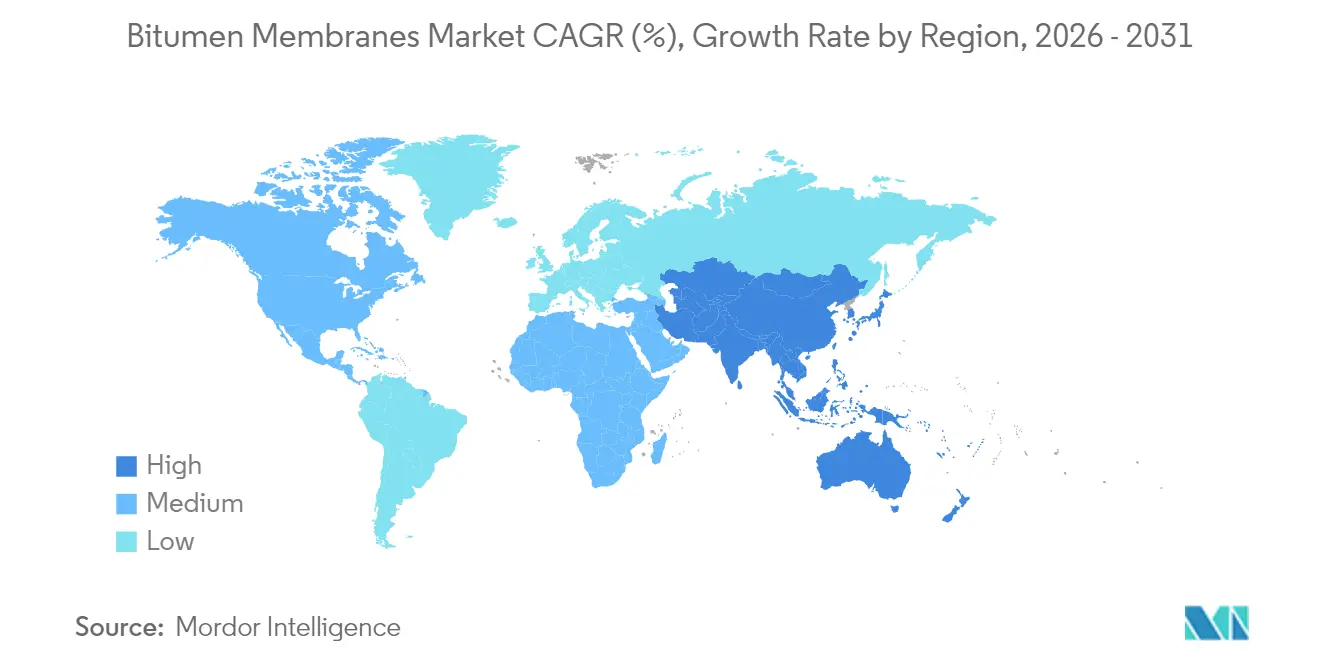

- By geography, Asia-Pacific led with 39.85% share in 2025 and shows the quickest regional pace at 2.21% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bitumen Membranes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in APAC megacity infrastructure spending | +0.60% | Asia-Pacific core, spillover to MEA | Medium term (2-4 years) |

| Extreme-rainfall resilience retrofits | +0.50% | North America & Europe | Long term (≥ 4 years) |

| Energy-code compliance via cool-roof membranes | +0.40% | Global, led by California and EU | Medium term (2-4 years) |

| Growth of torch-free self-adhesive systems | +0.30% | Global, fire-restricted zones | Short term (≤ 2 years) |

| Predictive-maintenance contracts using digital leak detection | +0.20% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Infrastructure Spending Across APAC Megacities

Large-scale capital programs exceeding USD 9 trillion keep the bitumen membrane market firmly oriented toward Asia-Pacific growth. India’s FY 2025 budget earmarks Rs 11.11 lakh crore for transport corridors, industrial parks, and metro lines, each requiring extensive waterproofing. China’s USD 741.5 billion road outlays similarly sustain bridge-deck and tunnel membrane demand. Continual urban rail, airport, and logistics hub construction across ASEAN widens the specification base. The pipeline creates steady volume visibility for manufacturers investing in regional capacity, buffering them against cyclical housing dips.

Extreme-Rainfall Resilience Retrofits in Mature Economies

North American and European building codes increasingly reference hydrostatic head performance and seam integrity in response to intensifying rainfall patterns. Retrofit programs targeting roofs, foundations, and podium decks treat high-grade membranes as risk-mitigation assets. Insurers correlate water ingress claims with envelope failures, incentivizing owners to upgrade before loss events. Municipal resilience mandates widen the addressable retrofit pool, while extended warranties become critical differentiators among suppliers.

Energy-Code Compliance via Cool-Roof Bitumen Membranes

California’s Title 24 (2025) and EU Green Deal objectives raise minimum Solar Reflectance Index thresholds, spurring demand for reflective granule or coating technologies. Projects pairing rooftop photovoltaics with low-VOC, fire-rated membranes see specification pull from both energy and safety codes. Manufacturers that embed light-colored ceramic granules directly into SBS or APP blends report higher compliance pass rates and reduced on-site coating labor[1]California Energy Commission, “2025 Building Energy Efficiency Standards for Residential and Nonresidential Buildings,” ENERGY.CA.GOV .

Growth of Torch-Free Self-Adhesive Membrane Systems

Regulators, insurers, and general contractors converge on open-flame restrictions, propelling self-adhesive uptake in dense urban and mass-timber projects. Peel-and-stick sheets cut installation time, eliminate propane handling, and reduce skilled-labor dependency. Early adopter data indicate 15% labor-cost savings and lower punch-list rework. Suppliers racing to refine adhesive tack life and cold-weather bond strength gain market share as legacy torch fleets age out.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Occupational HSE concerns during torch-on installation | -0.40% | Global, acute in fire-restricted zones | Short term (≤ 2 years) |

| Crude-oil price volatility impacting bitumen costs | -0.30% | Global supply chain impact | Medium term (2-4 years) |

| Substitution threat from bio-based & TPO/EPDM membranes | -0.30% | North America & Europe early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Occupational HSE Concerns During Torch-On Installation

National fire codes and insurer guidelines now regard torch application as a high-hazard activity. UK HSE advisories underscore flash-over and fume exposure risks that escalate when untrained labor uses open flame on combustible substrates. Contractors absorb higher insurance premiums, fire-watch staffing, and ventilation costs, eroding the historical cost advantage of torch-on membranes. Training gaps intensify as skilled installers retire, leading builders to specify self-adhesive alternatives.

Crude-Oil Price Volatility Impacting Bitumen Costs

Bitumen feedstock tracks Brent crude, which cycled between USD 178 and USD 620 per ton from 2020-2024. Refinery utilization bottlenecks and logistical chokepoints add regional price spreads that squeeze non-integrated producers. Fixed-bid construction contracts expose contractors to cost overruns when the asphalt index surges outpace escalation clauses. Some manufacturers hedge with recycled shingle asphalt or bio-modified binders, though current supply volumes cannot offset mainstream demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: SBS Flexibility Gains on APP Dominance

APP held 36.28% of the 2025 volume, underpinned by established sourcing and installer familiarity. The bitumen membrane market size for SBS grades is forecast to advance at a 2.22% CAGR, reflecting superior elasticity in freeze-thaw climates and better flow resistance in hot zones. Manufacturers incorporating bio-circular styrenic block copolymers address sustainability goals without diluting performance. Specification engineers increasingly trade modest upfront premiums for reduced crack-propagation risk over 20-year life cycles, reinforcing SBS momentum.

APP retains primacy in cost-sensitive public bids and regions with milder thermal cycling. Blends integrating recycled polymers help mitigate asphalt cost swings and respond to circular-economy procurement clauses. Specialty polymer variants serve bridge decks and chemical-exposure sites where mechanical and chemical endurance outweigh price. The grade split illustrates how performance-driven segments carve incremental gains while commodity volumes anchor plant utilization.

By Product Type: Sheet Reliability Versus Liquid Versatility

Factory-produced sheets delivered a 63.85% share in 2025, thanks to tight thickness tolerances that underpin long warranty terms. Liquids, expanding at a 2.31% CAGR, suit irregular geometries, podium landscaping, and roof refurbishments requiring seamless detailing. Cold-applied liquids avoid kettle heating and carry lower smell footprints, a growing advantage in urban retrofits.

Hybrid assemblies pairing sheet field coverage with liquid flashings achieve both speed and detail robustness. Sheets remain preferred for high-traffic roofs due to puncture-resistant reinforcements, whereas liquids dominate planter boxes and vertical wall transitions. Producers marketing integrated primer-membrane-topcoat systems lock in chemical compatibility and widen aftermarket revenue streams.

By Application: Roofing Core While Sub-Surface Accelerates

Roofing accounted for 47.66% of 2025 demand, a foundational driver for the bitumen membrane market. Below-grade waterproofing edges ahead at 2.23% CAGR as city basements, podium slabs, and utility tunnels expand. Bridge and parking decks add cyclical boosts tied to public-works outlays; specifications here emphasize tensile recovery under vehicular load.

Cool-roof mandates push roofing formulations toward high-albedo granules, drawing premium margins. Sub-surface membranes adopt double-bond or sandwich assemblies to counter hydrostatic pressure. Structural engineers scrutinize compatibility with crystalline waterproofing admixtures, leading to dual-system designs that combine positive-side bitumen sheets with negative-side integral treatments.

By Reinforcement Material: Polyester Stability Meets Composite Strength

Polyester retained 41.78% share in 2025, balancing elongation, stiffness, and cost. Composites that stitch polyester and fiberglass are pacing at a 2.21% CAGR by spreading load paths across multiple fiber orientations. These hybrids resist puncture and shrinkage, enabling longer expansion-joint spans.

Fiberglass remains indispensable for fire-classified assemblies and chemically aggressive sites like wastewater tanks. Research into recycled PET-based polyester knits aligns reinforcement selection with corporate ESG targets. Advances in binder chemistry improve fiber-bitumen adhesion, boosting fatigue life under cyclical wind uplift on exposed roofs.

By Installation Technology: Self-Adhesive Surges Past Torch Legacy

Torch-applied maintained a 35.64% share in 2025 on entrenched contractor skill sets. Self-adhesive sheets, growing 3.18% CAGR, leverage peel-and-stick simplicity to curtail labor and insurance overhead. SeamShield-style protective films protect adhesive lanes, cutting weld failures by 10% during hoisting. Cold liquids serve niche refurbishments where roof access limits sheet maneuvering.

Heat-welded hot-mop methods persist in petrochemical sites demanding thick bitumen flood coats. Regulatory heat now centers on open flame, accelerating fleet retirement of torches and cylinders. Equipment makers counter with induction-welded lap tools, but adhesive chemistries progress faster, tilting adoption curves toward flame-free lines.

By End-User Industry: Housing Base Underpinned by Infrastructure Upside

Residential construction composed 49.55% of 2025 consumption, anchored in code-mandated foundation and roof waterproofing. Infrastructure spending drives the leading 2.43% CAGR segment through bridges, metros, and water treatment plants specifying high-durability membranes. Commercial skylines add steady growth via energy-efficient roof retrofits in aging office stock.

Industrial and automotive niches prioritize chemical resistance and static-cut protection. Data centers—lifetime cost-conscious owners—deploy monitored membranes, integrating sensors specified at the design stage. Public-private-partnership projects often bundle preventive maintenance, advantaging brands offering full-life services.

Geography Analysis

Asia-Pacific captured 39.85% 2025 volume and leads with a 2.21% CAGR as India and China push megaproject pipelines. India’s Rs 11.11 lakh crore allocation spans highways, dedicated freight corridors, and 14 metro systems, each funneling roofing and sub-surface membrane orders. China’s USD 741.5 billion road modernization sustains bridge-deck volumes, while ASEAN manufacturing zones lift warehouse roofing needs.

North America’s cyclical replacement cycles and stringent cool-roof codes deliver predictable volume and margin. Plant investments—IKO’s USD 390 million dual builds, Atlas Roofing’s USD 200 million Iowa line, and Owens Corning’s southeastern plant—shorten lead times and localize asphalt sourcing. California’s Title 24 shapes formulations nationwide as other states mirror its reflectance and VOC thresholds.

Europe maintains balanced demand through renovation incentives and the pending 2026 Circular Economy Act. High-performance SBS sheets dominate flat-roof refurbishments in Germany and the Nordics, while Mediterranean rebuilds weigh cool-roof liquids to combat urban heat islands. Middle East and Africa gain traction via airport and desalination projects, yet political risk caps mega-project momentum. South America’s commodity-driven booms lift demand sporadically, with exchange-rate swings challenging import economics.

Competitive Landscape

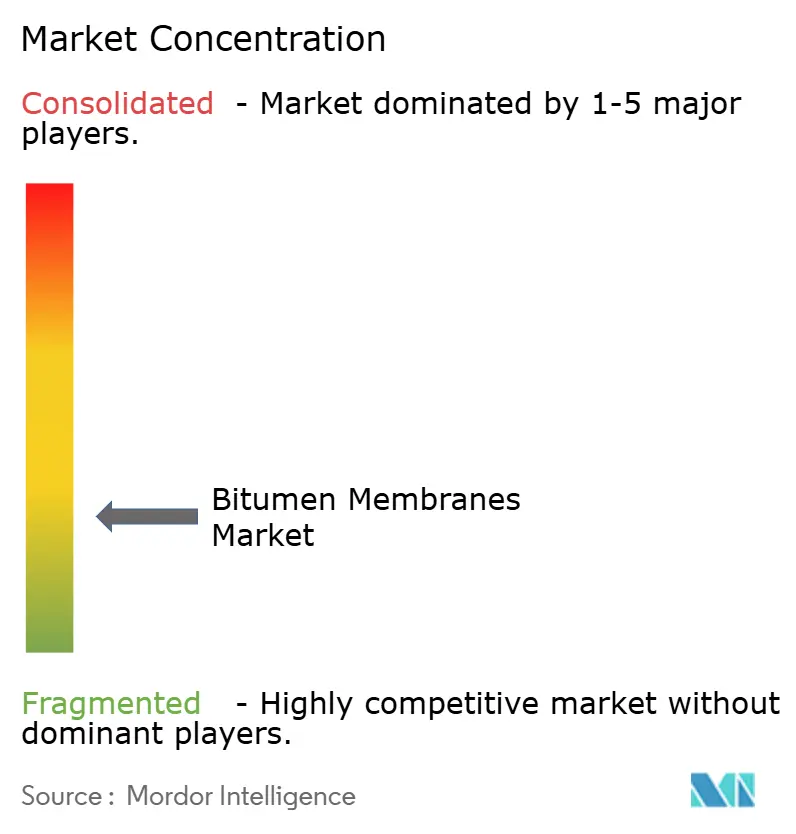

The bitumen membrane market remains highly fragmented; the top five players control roughly 30% combined share, creating room for regional specialists. Vertical integration into asphalt processing insulates leaders from crude swings. IKO’s USD 120 million Missouri plant and USD 270 million Florida complex enhance U.S. Gulf Coast logistics, while Atlas Roofing’s Iowa build targets Midwest supply gaps. GAF expands capacity in Kansas and Georgia to anchor its national distribution grid.

Product innovation centers on self-adhesive adhesives, reflective granulate chemistry, and recycled asphalt integration. Owens Corning’s pilot shingles using reclaimed asphalt hit commercial scale in 2025, signaling circular economy traction. TAMKO’s investment in Northstar Clean Technologies positions it for recycled-content feedstock, diversifying bitumen sources. Digital add-ons, such as cloud-linked leak-detection platforms, differentiate premium lines and underpin service contracts.

Partnerships with membrane-compatible PV mounting firms and cool-roof coating specialists broaden application ecosystems. Firms emphasize training academies to accelerate contractor conversion from torch to peel-and-stick, shrinking warranty claims. Regional challengers leverage government incentives to set up new lines closer to growth corridors, but capital barriers and warranty bankability limit their leap to global scale.

Bitumen Membranes Industry Leaders

BMI Group

GAF Materials LLC

IKO PLC

SOPREMA Group

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sika AG launched the SikaShield HB79, a new product under its SikaShield brand of hybrid Modified Bitumen membrane roofing solutions. This introduction is anticipated to drive innovation and enhance competition in the bitumen membrane market, further solidifying Sika AG's market presence.

- February 2025: Owens Corning has announced plans to invest in a new shingle manufacturing facility in the southeastern United States, with an annual production capacity of 6 million squares. Operations are expected to commence in 2027. This development is likely to strengthen the bitumen membrane market by enhancing supply capabilities and meeting growing demand in the region.

Global Bitumen Membranes Market Report Scope

Bitumen membrane is a viscous substance derived from petroleum and is a dark and adhesive liquid or semi-solid. Extensively applied in construction for waterproofing purposes, these membranes were explicitly created to provide coverage for both industrial and residential structures. Their versatile applications encompass humidification, waterproofing, binding, rustproofing, joint filling, and crack formation. The growing demand within the building and construction industry has driven increased production.

The bitumen membrane market is segmented by grade, product type, end-user industry, and geography. By grade, the market is segmented into atactic polypropylene, styrene-butadiene-styrene. and others (self-adhered, polymer-modified, mineral-surfaced, and others). By product type, the market is segmented into sheets, and liquids, By end-user industry, the market is segmented into construction, automotive, and others (infrastructure development, oil and gas, and others). The report also covers the market size and forecasts for the bitumen membrane market in 27 countries across the globe. The report offers market size and forecasts for the bitumen membrane market in volume (sqm) for all the above segments.

| Atactic Polypropylene (APP) |

| Styrene-Butadiene-Styrene (SBS) |

| Other Polymer-Modified Bitumen |

| Sheets |

| Liquids |

| Roofing |

| Below-Grade Waterproofing |

| Bridge and Parking Decks |

| Other Structural Waterproofing |

| Polyester |

| Fiberglass |

| Composite (Polyester/Fiberglass) |

| Others |

| Torch-Applied |

| Self-Adhesive (Peel and Stick) |

| Cold-Applied (Liquid) |

| Heat-Welded / Hot-Mop |

| Residential Construction |

| Commercial Construction |

| Industrial Construction |

| Infrastructure (Roads, Bridges, Tunnels) |

| Automotive |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Turkey | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Grade | Atactic Polypropylene (APP) | |

| Styrene-Butadiene-Styrene (SBS) | ||

| Other Polymer-Modified Bitumen | ||

| By Product Type | Sheets | |

| Liquids | ||

| By Application | Roofing | |

| Below-Grade Waterproofing | ||

| Bridge and Parking Decks | ||

| Other Structural Waterproofing | ||

| By Reinforcement Material | Polyester | |

| Fiberglass | ||

| Composite (Polyester/Fiberglass) | ||

| Others | ||

| By Installation Technology | Torch-Applied | |

| Self-Adhesive (Peel and Stick) | ||

| Cold-Applied (Liquid) | ||

| Heat-Welded / Hot-Mop | ||

| By End-User Industry | Residential Construction | |

| Commercial Construction | ||

| Industrial Construction | ||

| Infrastructure (Roads, Bridges, Tunnels) | ||

| Automotive | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Turkey | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the bitumen membrane market in 2026?

It stood at 1.17 billion cubic meters in 2026 and is forecast to reach 1.3 billion cubic meters by 2031, representing a 2.09% CAGR.

Which region leads demand for bitumen membranes through 2031?

Asia-Pacific holds 39.85% 2025 share and posts the fastest 2.21% CAGR as India, China, and ASEAN maintain heavy infrastructure pipelines.

Why are self-adhesive membranes growing faster than torch-on systems?

Fire-code restrictions, labor-savings, and insurance incentives make flame-free peel-and-stick sheets attractive, resulting in a 3.18% CAGR for self-adhesive installations.

Which grade of bitumen membrane is gaining traction?

SBS-modified membranes are rising at 2.22% CAGR thanks to superior flexibility and temperature resistance, even though APP still owns the largest share.

How does crude-oil volatility affect membrane manufacturers?

Asphalt feedstock price swings squeeze margins for non-integrated producers; some mitigate risk through recycled asphalt and long-term supply contracts.

What role do cool-roof regulations play in product demand?

Energy codes such as California’s Title 24 accelerate adoption of reflective bitumen membranes, boosting premium product volumes, especially in roof retrofits.

Page last updated on: