Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

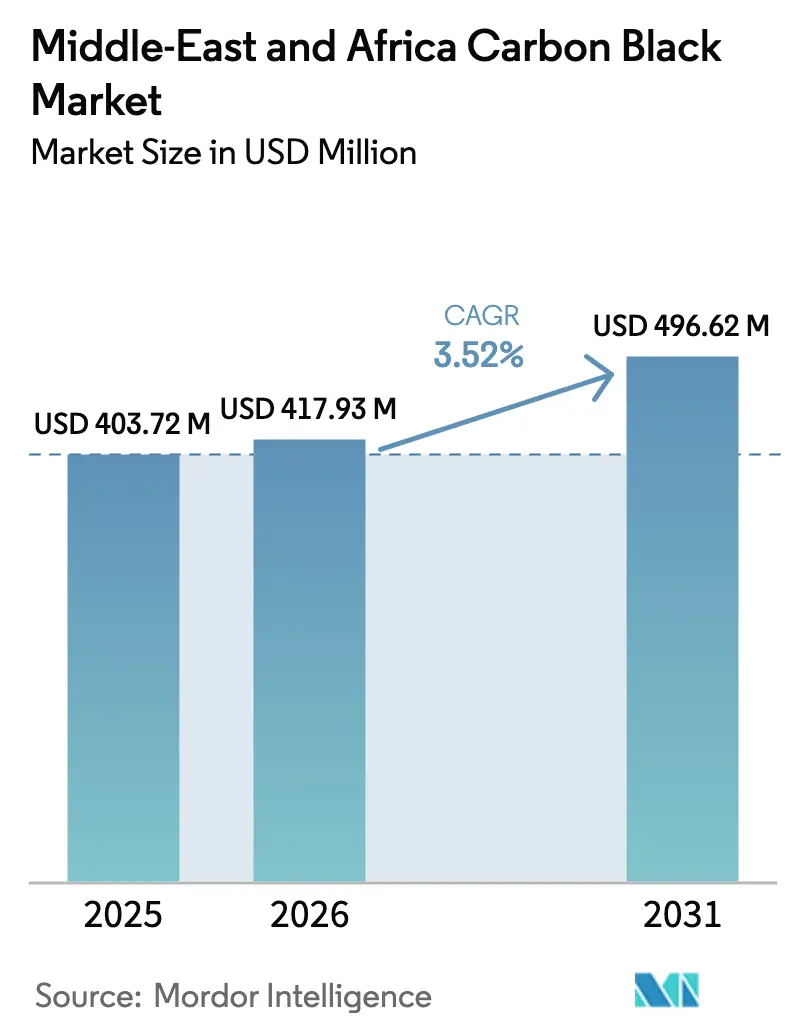

| Base Year Market Size (2025) | USD 403.72 Million |

| Market Size (2026) | USD 417.93 Million |

| Market Size (2031) | USD 496.62 Million |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

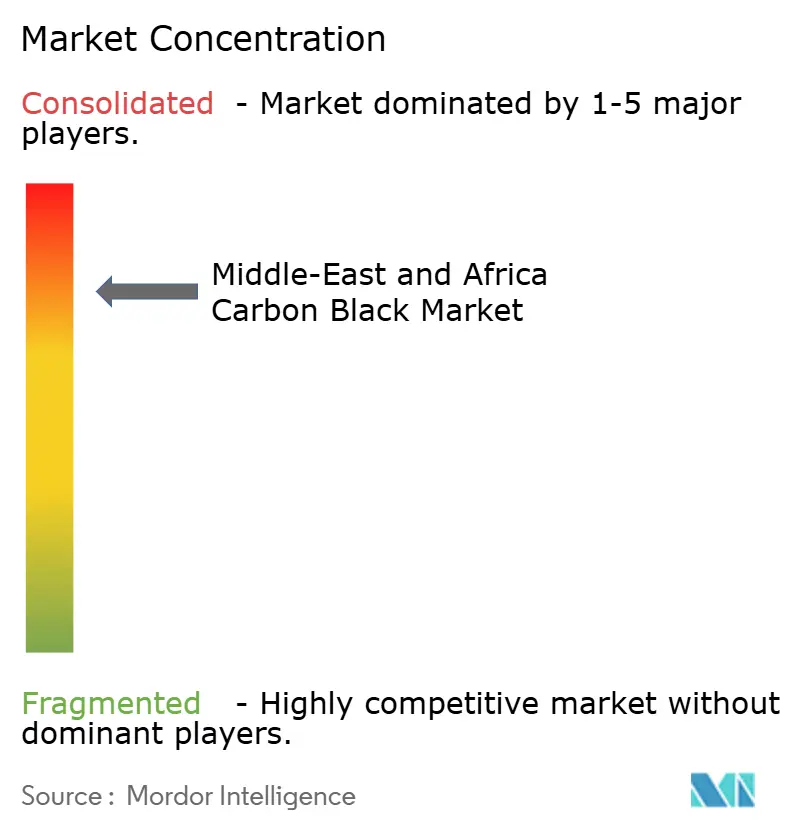

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle-East And Africa Carbon Black Market Analysis by Mordor Intelligence

The Middle-East and Africa Carbon Black Market size is expected to grow from USD 403.72 million in 2025 to USD 417.93 million in 2026 and is forecast to reach USD 496.62 million by 2031 at 3.52% CAGR over 2026-2031. Firm feedstock availability in oil-rich economies underpins cost competitiveness, while sovereign wealth funds channel capital into petrochemical clusters that anchor tire, plastics, and energy-storage supply chains. Automotive localization programs in Saudi Arabia and the United Arab Emirates elevate in-region procurement of reinforcement and conductive grades, and public-private ventures accelerate recovered carbon black adoption in circular economy roads. At the same time, specialty grades for batteries, textiles, and coatings command higher margins, partially cushioning the impact of the gradual switch to silica-rich “green” tires. Competitive focus rests on process efficiency, emissions abatement, and strategic partnerships that secure customer offtake in diversified downstream industries.

Key Report Takeaways

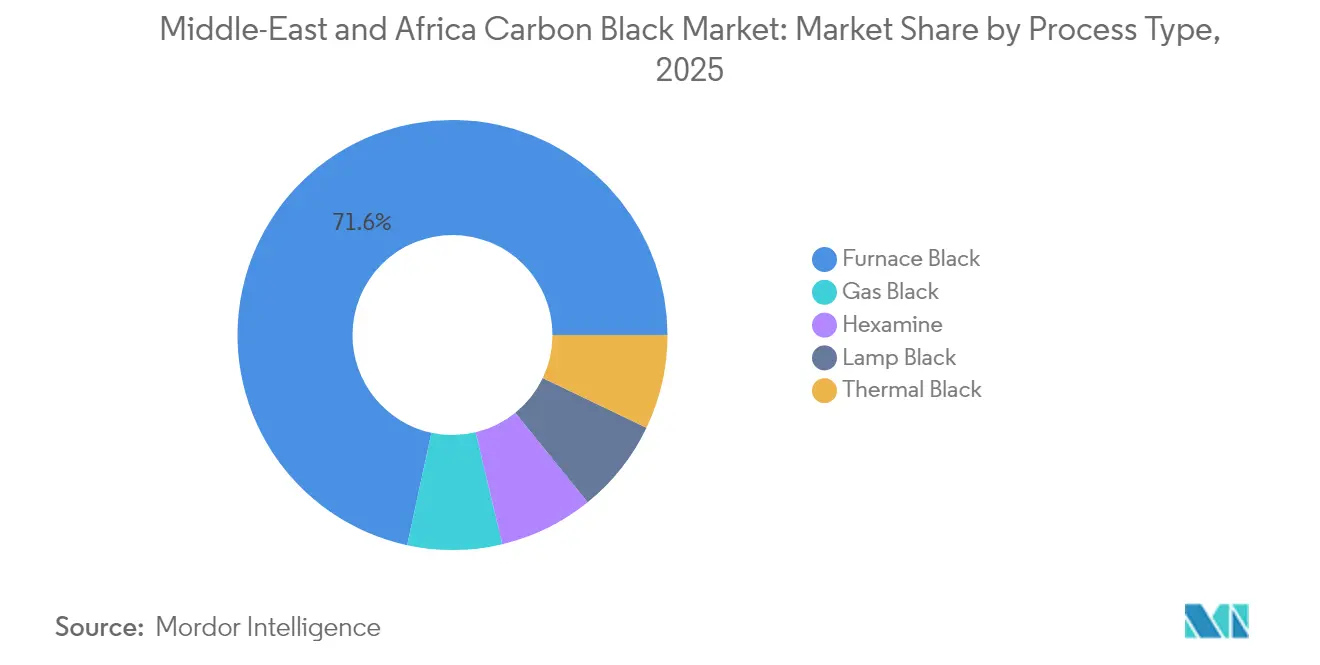

- By process type, Furnace Black captured 71.62% of the Middle-East and Africa carbon black market share in 2025; it is also the fastest-growing process segment at a 4.31% CAGR through 2031.

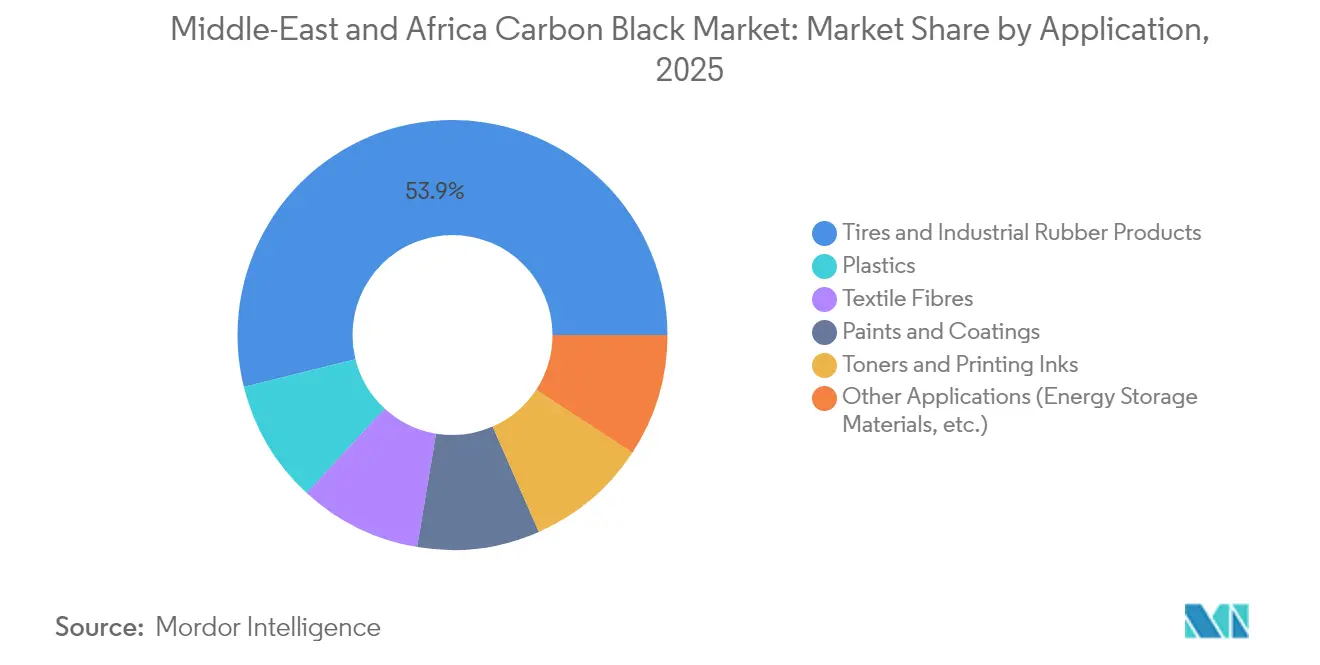

- By application, Tires and Industrial Rubber Products led with a 53.88% revenue share in 2025, while Other Applications are projected to expand at a 4.66% CAGR to 2031.

- By geography, Saudi Arabia held 29.86% of regional revenue in 2025, whereas the United Arab Emirates is forecast to post the fastest growth at a 4.52% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle-East And Africa Carbon Black Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing application in the fiber and textile industries | +0.8% | Turkey, Egypt, Morocco | Medium term (2-4 years) |

| Expansion of the automotive and tire sector | +1.2% | Saudi Arabia, UAE, Turkey | Long term (≥ 4 years) |

| Surge in conductive carbon black for Li-ion battery gigafactories | +0.9% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Recovered carbon black uptake in circular-economy road projects | +0.6% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| Increasing market penetration of specialty black | +0.7% | UAE, Saudi Arabia, Turkey | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Application in Fiber and Textile Industries

Advanced fiber-modification techniques now embed carbon black pigments that deliver antimicrobial protection against Staphylococcus aureus and Escherichia coli, helping regional mills supply healthcare and hygiene fabrics. Turkey benefits by aligning these technologies with its Twelfth Development Plan green mandates, while Egypt’s petrochemical complex secures upstream feedstock. The integration of carbon black in nylon, polyester, and acrylic fibers spreads demand beyond commodity apparel into higher-value technical textiles. As brands pursue traceable and sustainable inputs, specialty black grades gain pricing power and longer contracts.

Expansion of Automotive and Tire Sector

Saudi Arabia’s USD 550 million Pirelli plant in King Abdullah Economic City will roll out 3.5 million passenger tires annually from 2026, locking in furnace-grade volumes for two decades. Localization extends into electric-vehicle housings, battery components, and sealing systems, all of which employ tailored carbon black dispersions. Turkey leverages EU proximity to supply emission-compliant tire lines, while the United Arab Emirates channels petrochemical intermediates into synthetic rubber. Construction and mining projects across the Gulf and Africa further enlarge off-highway tire demand, reinforcing steady shipments of abrasion-resistant reinforcement blacks. Collectively, these dynamics anchor long-term baseline consumption even as vehicle electrification reshapes materials mixes.

Surge in Conductive Carbon Black for Li-ion Battery Gigafactories

Regional power-storage ambitions call for high-conductivity additives that lower cell impedance and extend cycle life. Orion’s PRINTEX kappa series reports premium uptake in pouch-cell electrodes destined for the United Arab Emirates’s solar-plus-storage farms. Saudi Arabia’s NEOM project lists more than 20 GWh of stationary storage, translating to incremental carbon black offtake in both anode and cathode slurries. Nanoparticle morphologies optimized for electronic pathways also enhance dynamic charge acceptance in advanced lead-acid batteries used for grid balancing. Government incentives that waive import duties on battery inputs shorten payback periods for local gigafactory investors, locking in multi-year supply contracts for conductive blacks.

Recovered Carbon Black Uptake in Circular-Economy Road Projects

Pyrolysis systems deliver recovered carbon black (rCB) with 40 to 50% cost savings against virgin equivalents while emitting less than 0.5 tons of CO2 per tonne produced[1]European Commission, “Advanced Pyrolysis for Low-Emission Carbon Black,” cordis.europa.eu. United Arab Emirates highway tenders now mandate rCB asphalt modifiers, cutting virgin binder use and diverting waste tires from landfills. Nigeria’s extended-producer-responsibility laws funnel scrap tires into organized recycling streams, ensuring feedstock flow for new rCB plants. As infrastructure outlays accelerate across East and West Africa, contractors specify rCB-modified asphalt that improves fatigue life and skid resistance. The material’s lower carbon footprint aids governments in meeting Paris Agreement targets without compromising pavement durability.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating switch to silica-based “green” tires | -1.1% | Turkey, UAE | Medium term (2-4 years) |

| Volatile feedstock pricing and supply risk | -0.9% | Saudi Arabia, UAE, Nigeria | Short term (≤ 2 years) |

| Competition from low-cost Asian imports | -0.7% | Import-dependent economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Switch to Silica-Based “Green” Tires

OEM mandates for lower rolling resistance drive the replacement of carbon black with precipitated silica and silane coupling agents that cut fuel consumption by as much as 7%[2]J. Wang et al., “Carbon–Silica Dual Phase Fillers in Green Tires,” Nature, nature.com . While silica improves wet grip, it complicates tire recycling and raises compounding costs, forcing Turkish plants to retrofit mixers and sourcing logistics. The transition threatens baseline demand for furnace blacks used in passenger car treads across the GCC. Producers respond by co-developing hybrid filler systems and expanding into specialty blacks for sidewalls and inner liners that retain reinforcement roles.

Volatile Feedstock Pricing and Supply Risk

Crude-linked feedstock swings squeeze margins, prompting Cabot to raise global contract prices in December 2024 to recover higher energy and maintenance costs. Currency depreciation in Nigeria and spot shortages tied to refinery turnarounds further destabilize procurement budgets for small compounding firms. South Africa’s coal-based stream faces rising carbon taxes, eroding cost advantages, and hastening potential capacity rationalization. Integrated producers in the Gulf partially hedge risk through long-term naphtha contracts, yet they remain exposed to geopolitical disruptions that constrain shipping lanes in the Red Sea and Strait of Hormuz.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Process Type: Furnace Black Drives Technical Innovation

Furnace Black contributed 71.62% of regional revenue in 2025 and is projected to expand at 4.31% CAGR through 2031, supported by retrofits that recover waste heat and lower SOx emissions. Producers in Saudi Arabia and the United Arab Emirates leverage captive feedstock from steam crackers to maintain continuous operations and tight particle-size control. Gas Black retains niche status for high-jetness inks and Li-ion electrodes, yet supply remains constrained by reactor complexity. Lamp Black grows steadily in inks and coatings for metal packaging, benefiting from e-commerce-driven canning volumes. Thermal Black and Acetylene Black provide specialty conductivity in wire and cable insulation. The process landscape favors integrated refiners able to monetize by-product streams while meeting tightening emission caps.

By Application: Specialty Segments Outpace Traditional Demand

Tires and Industrial Rubber Products still accounted for 53.88% of 2025 revenue, anchored by OEM expansions and aftermarket growth. The Middle East and Africa carbon black market share that this application holds is projected to ease slightly as specialty grades accelerate. Other Applications, covering batteries, plastics, coatings, and fibers, are forecast to grow at a 4.66% CAGR.

Energy-storage demand rises as gigawatt-scale PV projects integrate lithium-iron-phosphate batteries requiring highly conductive carbon additives. Textile mills in Turkey and Morocco embed antimicrobial blacks in athletic and medical fabrics to command export premiums. Inkjet and laser printing segments use fine-particle blacks that enable high optical density at reduced tint strength, lowering overall pigment cost per square meter. This diversification shields producers from cyclical swings in tire output and supports balanced plant loadings.

Geography Analysis

Saudi Arabia anchored the Middle-East and Africa carbon black market in 2025 with a 29.86% revenue share, thanks to embedded feedstock advantages and multi-year offtake agreements with global tire majors. The United Arab Emirates is set to outpace the region with a 4.52% CAGR to 2031.

Free-zone incentives in Abu Dhabi streamline equipment imports for new masterbatch and energy-storage ventures, creating a virtuous feedback loop that lifts carbon black offtake. Turkey combines EU-aligned regulations with strong automotive and textile bases, tapping its Twelfth Development Plan to modernize green logistics and enhance materials circularity. Strategic rail links shorten lead times to European customers, boosting exports of value-added compound and battery components. In Africa south of the Sahara, Nigeria’s end-of-life tire rules trigger investment in pyrolysis hubs that supply recovered carbon black and fuel. South Africa wrestles with high carbon taxes on its coal-based stream, pushing Sasol to evaluate gasification retrofits or capacity cuts. Morocco sees rising demand for automotive wiring harnesses and textile fibers, reinforcing imports of conductive and pigment grades. Collectively, these geographies illustrate how policy, feedstock, and industrial strategy converge to shape growth trajectories across the Middle East and Africa carbon black market.

Competitive Landscape

The Middle-East and Africa carbon black market features consolidation with vertically integrated majors such as Birla Carbon, SABIC, and ADNOC holding the advantage of captive feedstock and regional logistics. Mid-tier independents fill supply gaps in specialty grades, while new entrants pursue recovered carbon black technology to undercut virgin costs and meet sustainability quotas. Price leadership remains fluid because each quarterly contract now includes feedstock escalation clauses tied to Brent and propylene benchmarks.

Middle-East And Africa Carbon Black Industry Leaders

Cabot Corporation

Birla Carbon

Continental Carbon Company

Orion S.A

SABIC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Orion confirmed plans to idle three to five carbon black lines across the Americas and EMEA by end-2025 to focus capital on higher-performing units.

- March 2024: Cabot Corporation launched PROPEL E8 engineered reinforcing black for low-rolling-resistance, high-durability tire treads.

Middle-East And Africa Carbon Black Market Report Scope

Carbon black (also known as acetylene black, channel black, furnace black, lamp black, and thermal black) is a substance made from the incomplete combustion of coal and coal tar, vegetable matter, or petroleum products such as fuel oil, fluid catalytic cracking tar, and ethylene cracking. Carbon black is used in tires and other rubber goods as a colorant and reinforcing filler, as a pigment, and wear protection ingredient in plastics, paints, and ink pigment. The carbon black market is segmented by process type, application, and geography. By process type, the market is segmented into furnace black, gas black, lamp black, and thermal black. By application, the market is segmented into tires and industrial rubber products, plastics, toners and printing inks, paints and coatings, textile fibers, and other applications. The report covers the market size and forecast for the anchors and grouts market in 3 countries across the Middle East and Africa. For each segment, the market sizing and forecasts have been based on revenue (USD million) and volume (kilotons) for all the above details.

By Process Type

| Furnace Black |

| Gas Black |

| Lamp Black |

| Thermal Black |

| Hexamine |

By Application

| Tires and Industrial Rubber Products | |

| Plastics | Films and Sheets |

| Pressure Pipes | |

| Molded Parts | |

| Toners and Printing Inks | |

| Paints and Coatings | |

| Textile Fibres | Nylon |

| Polyester | |

| Acrylic | |

| Other Applications (Energy Storage Materials, etc.) |

By Geography

| Saudi Arabia | United Arab Emirates |

| Qatar | |

| Kuwait | |

| Turkey | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Morocco | |

| Rest of Middle-East and Africa |

| By Process Type | Furnace Black | |

| Gas Black | ||

| Lamp Black | ||

| Thermal Black | ||

| Hexamine | ||

| By Application | Tires and Industrial Rubber Products | |

| Plastics | Films and Sheets | |

| Pressure Pipes | ||

| Molded Parts | ||

| Toners and Printing Inks | ||

| Paints and Coatings | ||

| Textile Fibres | Nylon | |

| Polyester | ||

| Acrylic | ||

| Other Applications (Energy Storage Materials, etc.) | ||

| By Geography | Saudi Arabia | United Arab Emirates |

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Morocco | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the Middle East and Africa carbon black market in 2026?

The market is valued at USD 417.93 million in 2026 and is projected to grow at a 3.52% CAGR to USD 496.62 million by 2031.

Which process segment leads the regional market?

Furnace Black leads with 71.62% revenue share in 2025 and is also the fastest-growing process at a 4.31% CAGR through 2031.

What is driving specialty carbon black demand in the region?

Rapid growth in battery gigafactories, technical textiles, and UV-resistant plastics is shifting demand toward conductive and pigment-grade blacks that offer higher margins and performance benefits.

How is recovered carbon black influencing supply dynamics?

Recovered carbon black provides 40-50% cost savings and lower emissions compared with virgin grades, and government mandates for circular economy roads in the UAE and Nigeria are accelerating its uptake.

Which country is expected to grow fastest between 2026 and 2031?

The United Arab Emirates is forecast to record the highest growth, expanding at a 4.52% CAGR as low-carbon investments spur specialty-grade consumption.

Page last updated on: