Video Encoder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 3.33 Billion |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

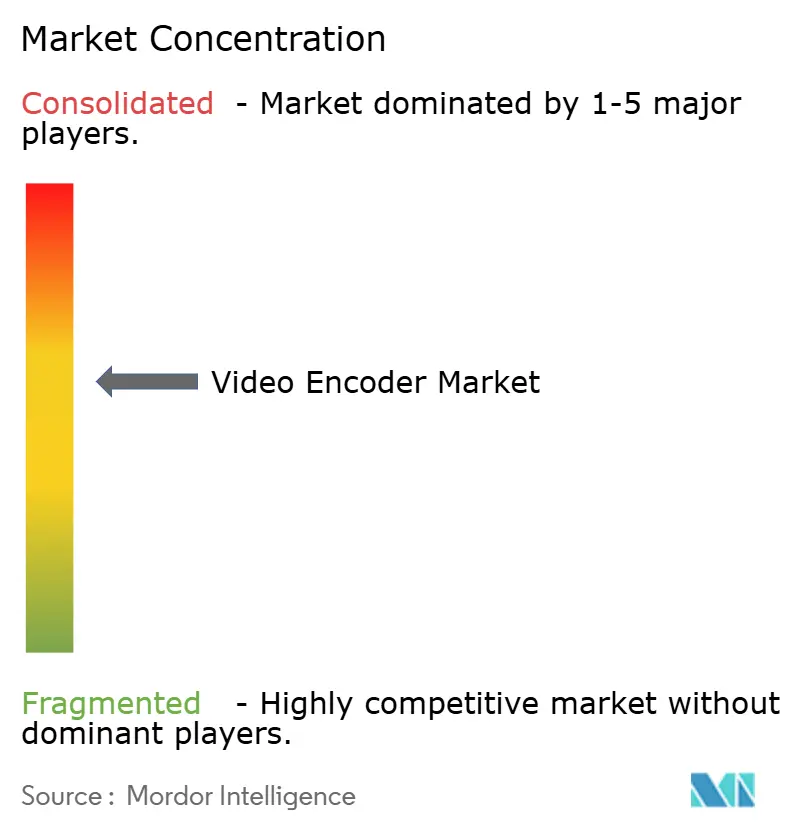

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Encoder Market Analysis by Mordor Intelligence

The video encoder market size is expected to grow from USD 2.55 billion in 2025 to USD 2.67 billion in 2026 and is forecast to reach USD 3.33 billion by 2031 at 4.54% CAGR over 2026-2031. This steady trajectory mirrors the sector’s ongoing transition from legacy H.264/AVC toward more efficient standards such as AV1 and VVC/H.266 while workflows migrate from fixed-function appliances to cloud-native infrastructure. Demand accelerates as multiscreen OTT viewing, 5G-enabled live streaming, and the proliferation of ultra-high-definition (UHD) formats place bandwidth optimization at the core of investment decisions. Hardware encoders currently anchor mission-critical broadcast operations, yet SaaS offerings gain momentum because elastic scaling lowers total cost of ownership for variable workloads. Supply-chain pressures on ASIC and FPGA components, coupled with codec royalty uncertainties, temper near-term spending but simultaneously widen opportunities for royalty-free alternatives.

Key Report Takeaways

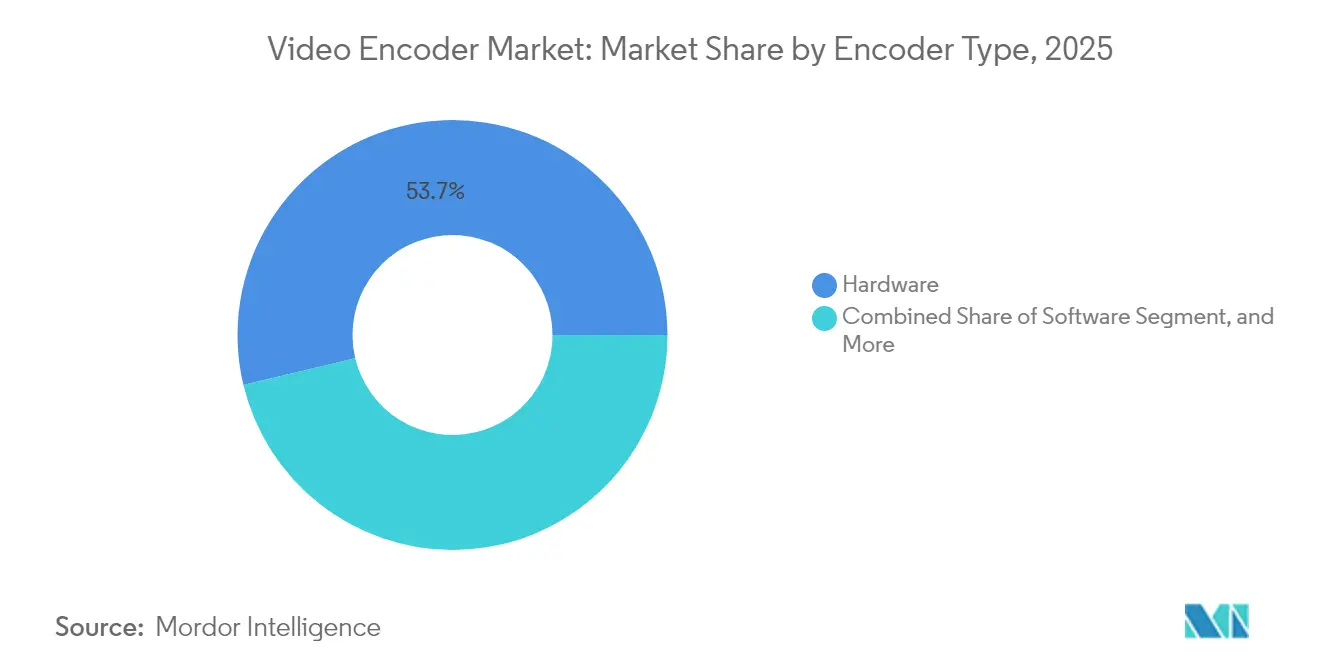

- By encoder type, hardware encoders led with 53.74% of the video encoder market share in 2025; cloud/SaaS solutions are projected to post the fastest 5.88% CAGR through 2031.

- By encoding standard, H.264/AVC captured 44.20% of the video encoder market size in 2025, while VVC/H.266 is expected to grow at a 5.29% CAGR to 2031.

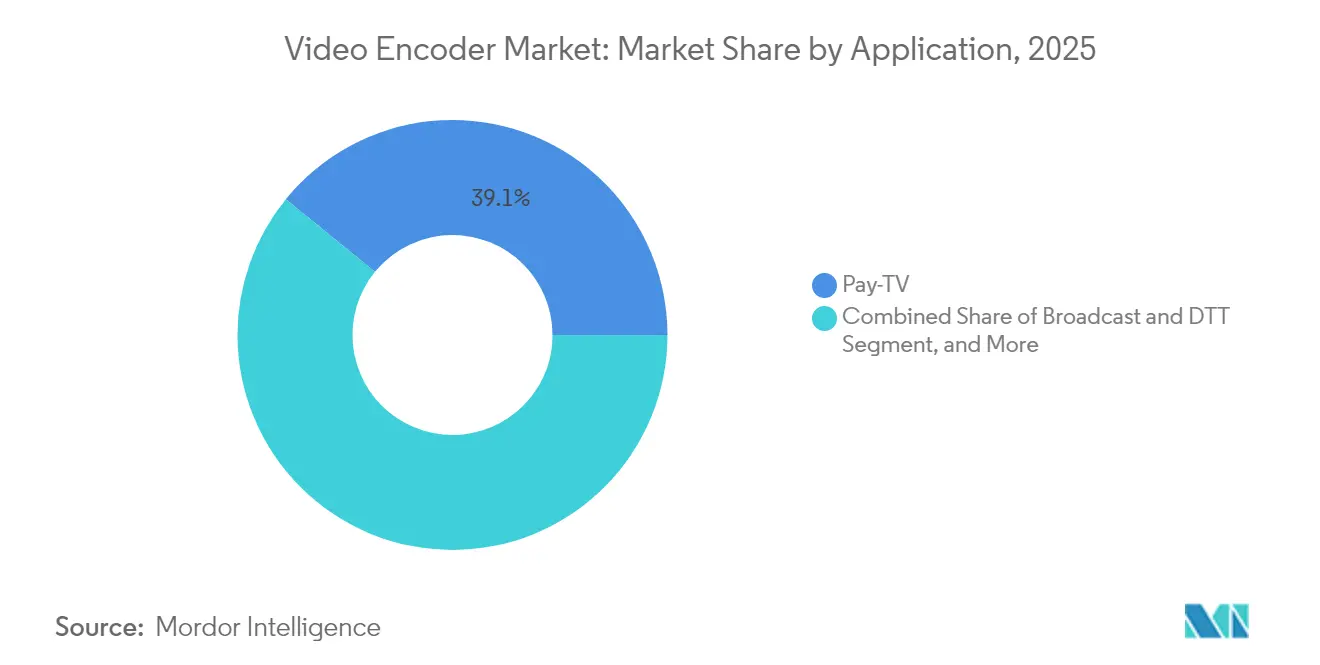

- By application, pay-TV held 39.12% revenue share in 2025; OTT and live streaming are advancing at a 5.52% CAGR through 2031.

- By end-user, media and entertainment represented 44.91% demand in 2025, whereas enterprise/corporate usage is rising at a 5.41% CAGR to 2031.

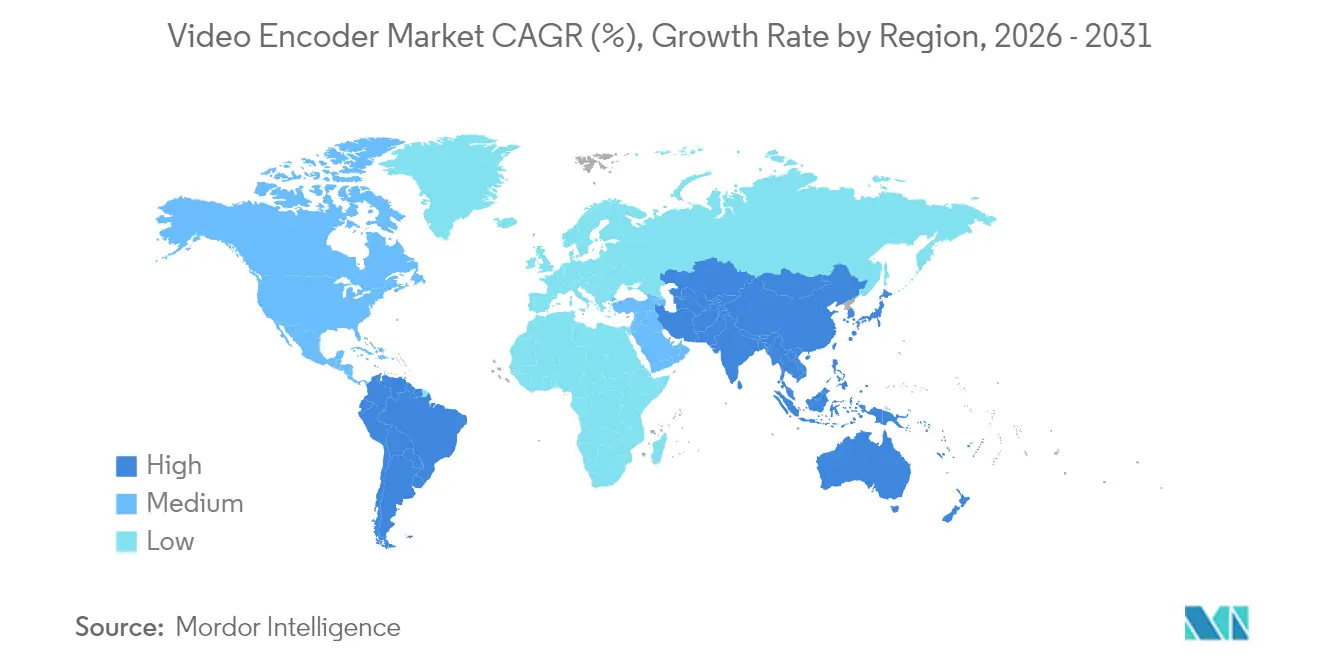

- By geography, North America accounted for 33.25% of 2025 revenue, yet Asia-Pacific is on track for the highest 5.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Video Encoder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of multiscreen and OTT video consumption | +1.2% | Global; strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Proliferation of 5G networks enabling UHD live streaming | +0.9% | Asia-Pacific core; spill-over to North America and Europe | Long term (≥ 4 years) |

| Migration from AVC to royalty-free AV1 | +0.8% | Global; led by North America and Europe | Medium term (2-4 years) |

| Cloud-native encoding workflows lowering TCO for broadcasters | +0.7% | North America and Europe; expanding in Asia-Pacific | Short term (≤ 2 years) |

| Edge encoding demand for low-latency interactive video | +0.5% | Global; early adoption in developed markets | Medium term (2-4 years) |

| Government funding for emergency surveillance networks | +0.4% | Asia-Pacific and Middle East; selective North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising popularity of multiscreen and OTT video consumption

OTT platforms optimize delivery across smartphones, tablets, and connected TVs, often producing 15 adaptive-bitrate profiles per asset to guarantee uninterrupted playback. Netflix’s shift to AV1 brought 30% bandwidth savings and lower CDN costs, proving the economic value of advanced compression. [1]Netflix Technology Blog, “AV1 Codec Implementation and Performance Analysis,” NETFLIXTECHBLOG.COM Manufacturers such as Samsung embed HDR10+ support that pushes content owners to preserve wider color gamut, raising demand for high-performance encoders able to process HDR and SDR simultaneously. As more smart-TV operating systems integrate voice-controlled search, frame-accurate trick-play features require additional metadata, further enlarging encoding workloads. These factors collectively sustain premium encoder adoption for multiscreen environments.

Proliferation of 5G networks enabling UHD live streaming

Commercial 5G deployments in Japan and South Korea have already enabled field tests of 8K and 4K60 live feeds, delivering uplink speeds of 100 Mbps from moving vehicles.[2]NTT Docomo, “5G Network 8K Live Streaming Trial Results,” DOCOMO.NE.JP Broadcasters can now bypass satellite links for remote production, trimming contribution costs and setup times. Low-latency edge nodes bring end-to-end delays below 50 ms, critical for interactive sports betting and fan engagement applications. China Mobile’s rollout of 5G-based surveillance across 200 cities further underscores how cellular backhaul can substitute fixed fiber in massive video networks. Encoder vendors capable of integrating 5G modems and network slicing APIs gain first-mover advantage as mobile operators commercialize premium video tiers.

Migration from AVC to high-efficiency, royalty-free codecs (AV1)

YouTube’s migration of all ≥480p assets to AV1 eliminated roughly USD 100 million in annual H.264 royalties and delivered 20% bitrate savings, illustrating powerful incentives to adopt open codecs. Alliance for Open Media’s expansion to include Intel, AMD, and ARM ensures silicon-level decoding becomes ubiquitous, mitigating device compatibility risks that stalled earlier transitions. Meta’s adoption across Facebook and Instagram strengthens AV1’s network effect by improving mobile user experience in bandwidth-constrained markets. For broadcasters, royalty-free licensing simplifies long-term budgeting as content libraries grow into petabyte scale. As cloud GPU instances add AV1 hardware acceleration, encoding throughput rises, lowering per-minute costs and unblocking at-scale adoption.

Cloud-native encoding workflows lowering TCO for broadcasters

AWS Elemental MediaConvert processed over 1 billion minutes of video monthly in 2024, showcasing elasticity that cuts 40–60% off lifetime ownership cost compared with fixed appliances.[3]Amazon Web Services, “Elemental MediaConvert Usage Statistics and Performance Metrics,” AWS.AMAZON.COM Serverless pipelines let broadcasters spin up thousands of transcodes during prime time and wind them down minutes later. Microsoft Azure’s FPGA-based instances match appliance-grade performance while preserving cloud flexibility, satisfying latency-sensitive users. Hybrid deployments-on-premises appliances bursting to the cloud-gain favor among tier-1 sports networks that require deterministic performance for marquee events yet want to avoid over-provisioning idle hardware. Consequently, vendors blending appliance reliability with SaaS orchestration capture an expanding share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex for ultra-low-latency hardware encoders | -0.8% | Global; acute for small broadcasters | Short term (≤ 2 years) |

| Fragmented patent pools and codec royalty uncertainties | -0.6% | Global; highest in cost-sensitive markets | Medium term (2-4 years) |

| Supply-chain risks for ASIC/FPGA components | -0.5% | Global; concentration in Asia-Pacific fabrication | Short term (≤ 2 years) |

| Power-consumption limits in edge/portable use-cases | -0.4% | Global; critical for mobile and IoT | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capex for ultra-low-latency hardware encoders

Encoders delivering sub-20 ms glass-to-glass latency cost USD 50,000–200,000 per unit, pricing smaller broadcasters out of interactive or VR offerings. ASIC-based designs demand bespoke silicon, and volumes remain niche, limiting economies of scale. E-sports tournament organizers frequently allocate six-figure budgets merely for encoding rigs across multi-camera broadcasts, squeezing margins for mid-tier events. With semiconductor talent diverted toward AI inference and crypto, advances in purpose-built video silicon slow, prolonging premium pricing.

Fragmented patent pools and codec royalty uncertainties

VVC/H.266’s multiple pools require separate negotiations, pushing combined royalties above HEVC and delaying broad deployment. Firms lacking deep legal resources hesitate to incorporate VVC, instead extending AVC lifetimes despite efficiency penalties. HEVC’s lingering disputes illustrate how opaque royalties can suppress market momentum for years. The contrast with AV1’s zero-royalty model intensifies pressure on patent holders but leaves current adopters in limbo, forcing multi-codec strategies that inflate operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Encoder Type: Cloud solutions accelerate infrastructure reinvention

Hardware appliances represented 53.74% of 2025 revenue, underscoring their legacy foothold in mission-critical contribution and distribution. Yet the video encoder market size for cloud/SaaS offerings is projected to expand at a 5.88% CAGR, the fastest among all types, as broadcasters prioritize opex flexibility over capex lock-in. Cloud adoption surges among digital-first studios needing instantaneous scale for episodic releases, while software encoders on COTS servers continue serving corporate campuses where IT staff can manage workloads internally.

In live sports, appliances retain primacy owing to deterministic performance and SDI integration, but hybrid architectures emerge wherein on-site gear sends mezzanine feeds to cloud clusters for ABR packaging at scale. Disaster recovery strategies increasingly mirror this approach, allowing rapid failover to the cloud without duplicating entire appliance fleets. Vendors able to orchestrate transcodes across heterogeneous infrastructures widen competitive moats as customers avoid single-point dependencies.

By Encoding Standard: Next-gen codecs redefine efficiency frontier.

H.264/AVC still commands 44.20% of the video encoder market share because of near-universal device support, yet bandwidth pressures and royalty costs push operators toward alternatives. VVC/H.266 leads growth at a 5.29% CAGR thanks to 50% bitrate savings over HEVC, pivotal for 8K streaming. Meanwhile, AV1’s royalty-free proposition lures OTT services seeking predictable costs, even if computational complexity remains higher today.

The video encoder market size tied to AV1 receives a tailwind from Intel’s Arc Pro GPUs and Apple’s iPhone 15, both offering native decode. As such, silicon populates consumer devices, and distributors accelerate AV1 adoption to reduce CDN bills. In the professional realm, GPU-accelerated VVC encoding within AWS MediaConvert removes prior performance bottlenecks, convincing early adopters to test live trials for 4K HDR channels. Multi-codec ladders will persist through 2031 as content owners hedge against licensing risks and device heterogeneity.

By Application: OTT’s rapid ascent reshapes revenue mix.

Pay-TV still generated 39.12% of 2025 demand as cable and satellite operators refresh headends, but growth pivots to OTT and live streaming, which will post a 5.52% CAGR. The expansion reflects cord-cutting coupled with sports rights migrating online. Security and surveillance maintain a stable trajectory, aided by smart-city programs specifying centralized video analytics that depend on efficient encoding for petabyte-scale archives. Remote education and corporate webcasting enjoy structural tailwinds from hybrid work, spurring enterprises to embed broadcast-grade quality into town-halls and training sessions.

OTT workflows place a premium on adaptive bitrate efficiency and DRM integration, steering buyers toward software-definable products. Conversely, surveillance deployments emphasize continuous 24/7 operation, favoring ruggedized hardware encoders dissipating minimal heat. The resulting application diversity prevents consolidation around a single architecture, necessitating modular portfolios that address disparate latency, reliability, and cost requirements.

By End-user Industry: Enterprise adoption broadens customer base

Media and entertainment accounted for 44.91% of 2025 revenue, reflecting studios, broadcasters, and streaming giants that ingest massive libraries. Enterprises, however, will show the fastest 5.41% CAGR as video becomes embedded in daily operations-from earnings webcasts to immersive product demos. Healthcare providers deploy encoders inside telemedicine carts for real-time diagnostics, while schools capture lectures for asynchronous learning.

Corporate IT teams favor cloud-native services to avoid specialty hardware, yet financial-services firms often stipulate on-premises solutions to satisfy data residency mandates. Government agencies mandate FIPS-certified modules, opening niches for vendors with compliance pedigrees. Thus, suppliers must tailor products to vertical-specific security and integration needs while maintaining common codec roadmaps.

Geography Analysis

North America generated 33.25% of revenue in 2025, underpinned by entrenched broadcast networks and the headquarters of major streaming services that demand premium UHD workflows. Replacement investment outweighs greenfield builds, yet software-defined transformations continue as cloud economics improve.

Asia-Pacific’s video encoder market size is on a 5.26% CAGR path to 2031, buoyed by massive smart-city surveillance projects, rapid 5G densification, and growing appetite for multilingual OTT catalogs. Local manufacturing ecosystems for electronics and semiconductors shorten supply chains and accelerate pilot deployments.

Europe pursues sustainability by mandating lower power envelopes and enforcing privacy protections, prompting adoption of efficient codecs and on-premises processing for sensitive footage. Regional public broadcasters modernize in step with DVB and HbbTV updates, forming steady demand for hybrid workflows.

Competitive Landscape

Innovation and Adaptability Drive Market Success

The market remains moderately fragmented. Hardware stalwarts such as Harmonic, Cisco, and MediaKind anchor broadcast workflows, whereas AWS Elemental and Google Cloud target elastic, usage-based encoding in the cloud arena. Hybrid orchestration is becoming the competitive battleground as customers demand appliance-like reliability paired with on-demand scale.

Strategic moves illustrate convergence. Harmonic’s acquisition of Ateme’s broadcast unit broadens software talent while preserving appliance lineage. Intel’s Arc Pro silicon underpins a hardware ecosystem optimized for AV1, supplying cloud providers and workstation OEMs alike. Cisco’s USD 120 million capacity build reinforces North American self-reliance amid supply-chain vulnerabilities.

Emerging vendors emphasize AI-assisted quality optimization and ultra-low-latency edge devices. Bitmovin’s ISO 27001 certification removes compliance roadblocks for regulated industries, while VITEC’s sub-50 ms appliances unlock new interactive use cases.

Video Encoder Industry Leaders

Harmonic Inc.

CommScope Holding Company, Inc.

MediaKind Global, Inc.

Cisco Systems, Inc.

Imagine Communications Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Harmonic committed USD 85 million to advance VVC/H.266 hardware acceleration for 8K live streams in sports and entertainment venues, positioning itself to meet rising demand for ultra-high-definition workflows as premium 8K displays gain traction.

- July 2025: AWS Elemental enlarged its global encoding footprint with new facilities in Mumbai and São Paulo, cutting latency for Asia-Pacific and South American customers by up to 40%. The sites feature specialized AV1 hardware to serve growing interest in royalty-free compression across emerging markets.

- May 2025: Cisco Systems completed the USD 120 million purchase of edge-computing firm Z3 Technology, enhancing Cisco’s portfolio of power-efficient, low-latency encoders tailored for 5G and Internet-of-Things deployments.

- March 2025: Intel introduced new Xeon processors that embed VVC/H.266 acceleration, allowing data centers to handle next-generation codecs without add-on cards and lowering cloud-encoding costs by as much as 60% compared with software-only approaches.

Global Video Encoder Market Report Scope

The video encoder market encompasses the industry involved in producing, selling, and developing video encoding hardware and software. The Video Encoder Market Report is Segmented by Encoder Type (Hardware, Software, Cloud/SaaS), Encoding Standard (H.264/AVC, H.265/HEVC, AV1, VVC/H.266, Other), Application (Pay-TV, Broadcast and DTT, OTT and Live Streaming, Remote Education and Corporate Webcasting, and More), End-user Industry (Media and Entertainment, Enterprise/Corporate, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Cloud / SaaS |

| H.264 / AVC |

| H.265 / HEVC |

| AV1 |

| VVC / H.266 |

| Other Encoding Standard |

| Pay-TV |

| Broadcast and DTT |

| OTT and Live Streaming |

| Security and Surveillance |

| Remote Education and Corporate Webcasting |

| Media and Entertainment |

| Enterprise / Corporate |

| Government and Defence |

| Education |

| Healthcare |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Encoder Type | Hardware | ||

| Software | |||

| Cloud / SaaS | |||

| By Encoding Standard | H.264 / AVC | ||

| H.265 / HEVC | |||

| AV1 | |||

| VVC / H.266 | |||

| Other Encoding Standard | |||

| By Application | Pay-TV | ||

| Broadcast and DTT | |||

| OTT and Live Streaming | |||

| Security and Surveillance | |||

| Remote Education and Corporate Webcasting | |||

| By End-user Industry | Media and Entertainment | ||

| Enterprise / Corporate | |||

| Government and Defence | |||

| Education | |||

| Healthcare | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the video encoder market?

The market is valued at USD 2.67 billion in 2026 and is projected to reach USD 3.33 billion by 2031.

Which encoder type is growing the fastest?

Cloud/SaaS solutions are expected to post the highest 5.88% CAGR through 2031.

How dominant is H.264/AVC today?

H.264/AVC retains 44.20% share, remaining the most widely deployed codec despite efficiency limits.

Why are AV1 and VVC gaining traction?

AV1 offers royalty-free licensing and about 20% bitrate savings, while VVC/H.266 provides 50% better compression over HEVC, critical for 8K workflows.

Which region will lead future growth?

Asia-Pacific is forecast to expand at a 5.26% CAGR, propelled by 5G rollouts and large-scale surveillance projects.

How are 5G networks influencing encoder demand?

5G enables high-bandwidth, low-latency UHD streaming, encouraging broadcasters to adopt encoders that can deliver 4K and 8K live content economically.

Page last updated on: