Veterinary Stereotactic Radiosurgery Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

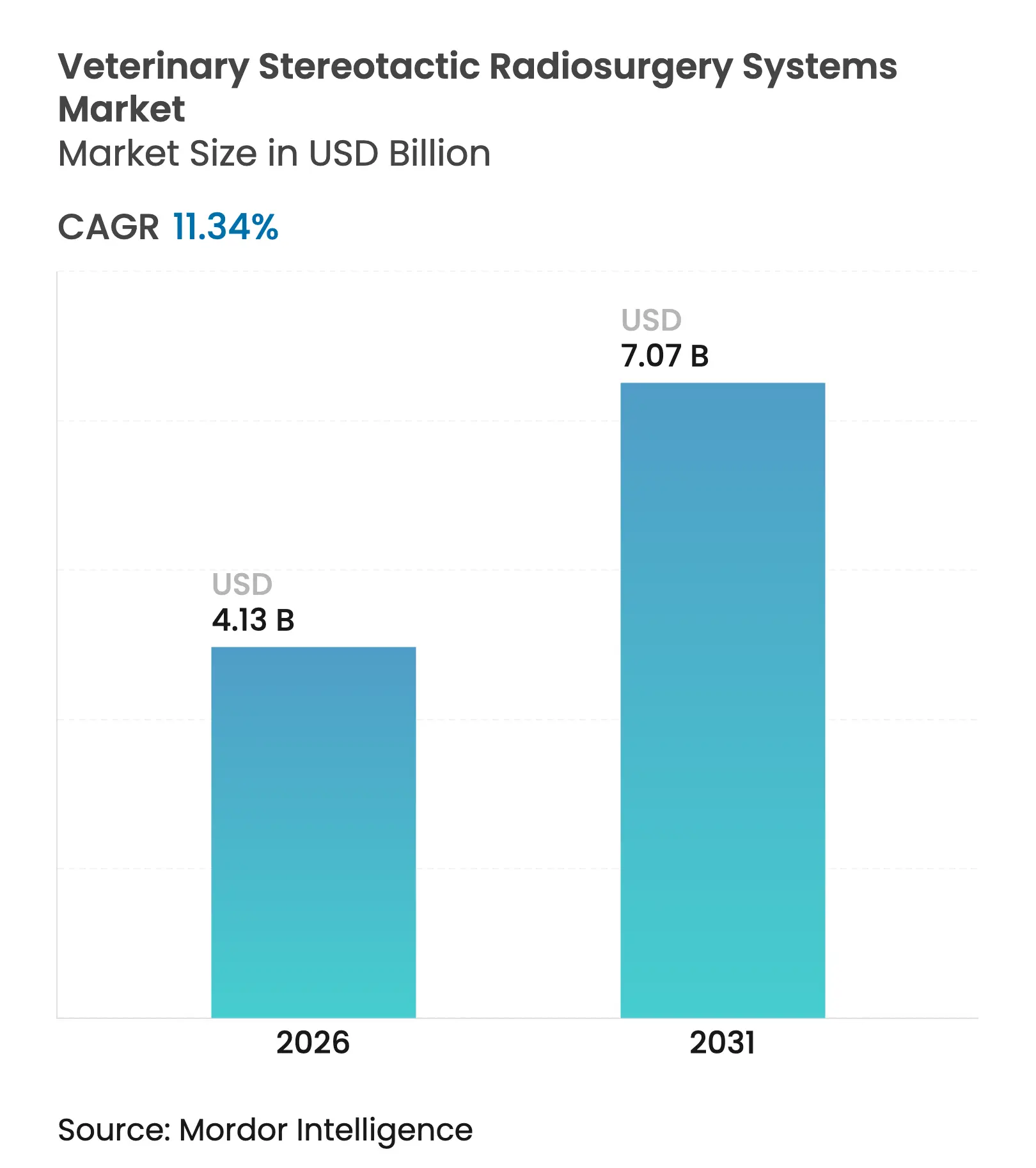

| Market Size (2026) | USD 4.13 Billion |

| Market Size (2031) | USD 7.07 Billion |

| Growth Rate (2026 - 2031) | 11.34 % CAGR |

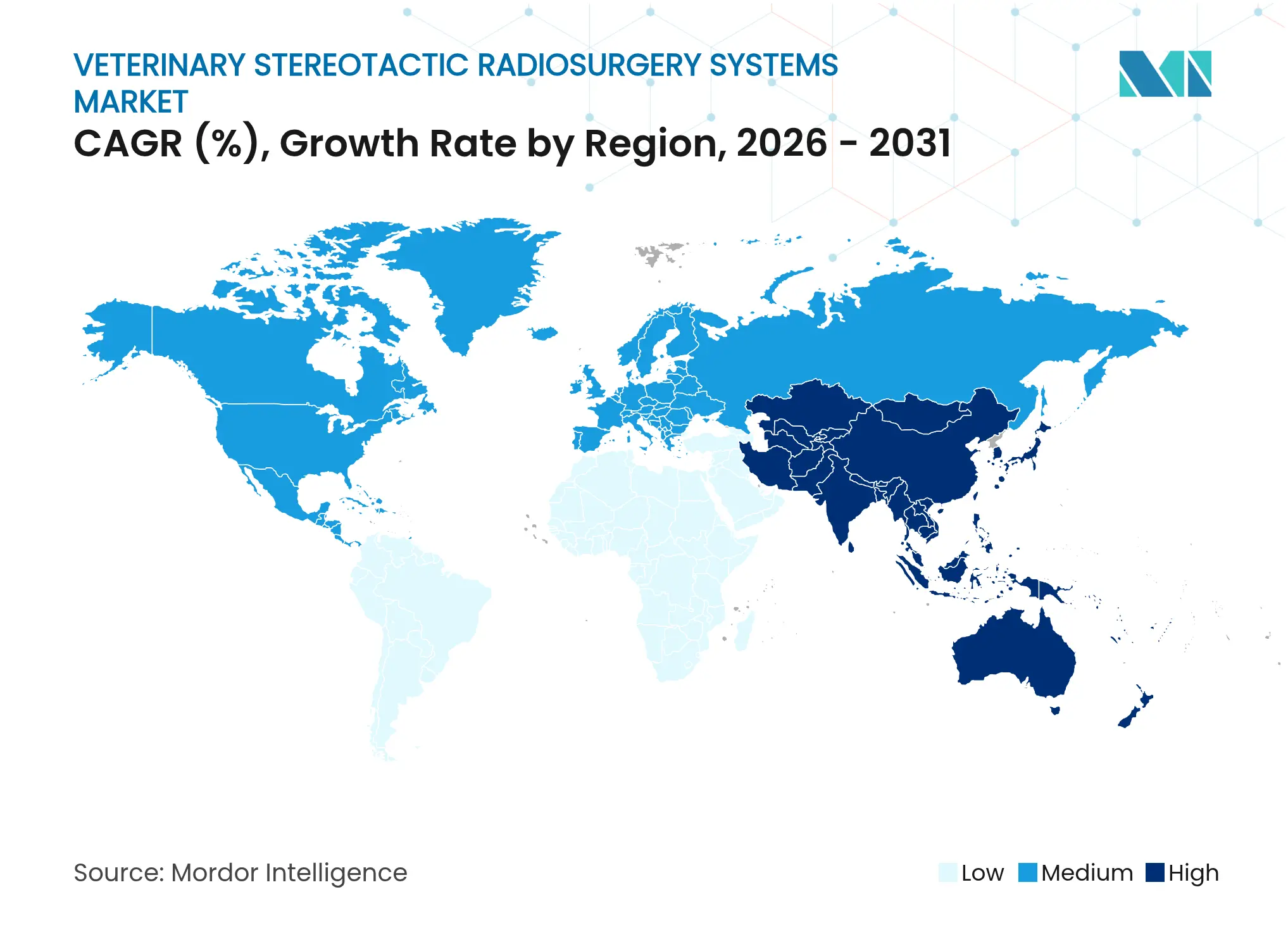

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Veterinary Stereotactic Radiosurgery Systems Market Analysis by Mordor Intelligence

The veterinary stereotactic radiosurgery systems market size in 2026 is estimated at USD 4.13 billion, growing from 2025 value of USD 3.71 billion with 2031 projections showing USD 7.07 billion, growing at 11.34% CAGR over 2026-2031. Demand rises as companion-animal owners seek the same precision oncology options available in human medicine, while growing corporate ownership of referral hospitals improves capital access for high-cost radiation platforms. Linear accelerators remain the workhorse modality, yet proton and heavy-ion solutions gain traction as facilities look to differentiate with superior dose conformity. Rising pet-insurance reimbursement for high-cost care lowers economic barriers to treatment, and ongoing convergence of imaging and therapy platforms reduces procedure time, enhancing throughput. Supply-side bottlenecks persist because fewer than 100 board-certified veterinary radiation oncologists worldwide can operate these systems, constraining near-term capacity expansion.

Key Report Takeaways

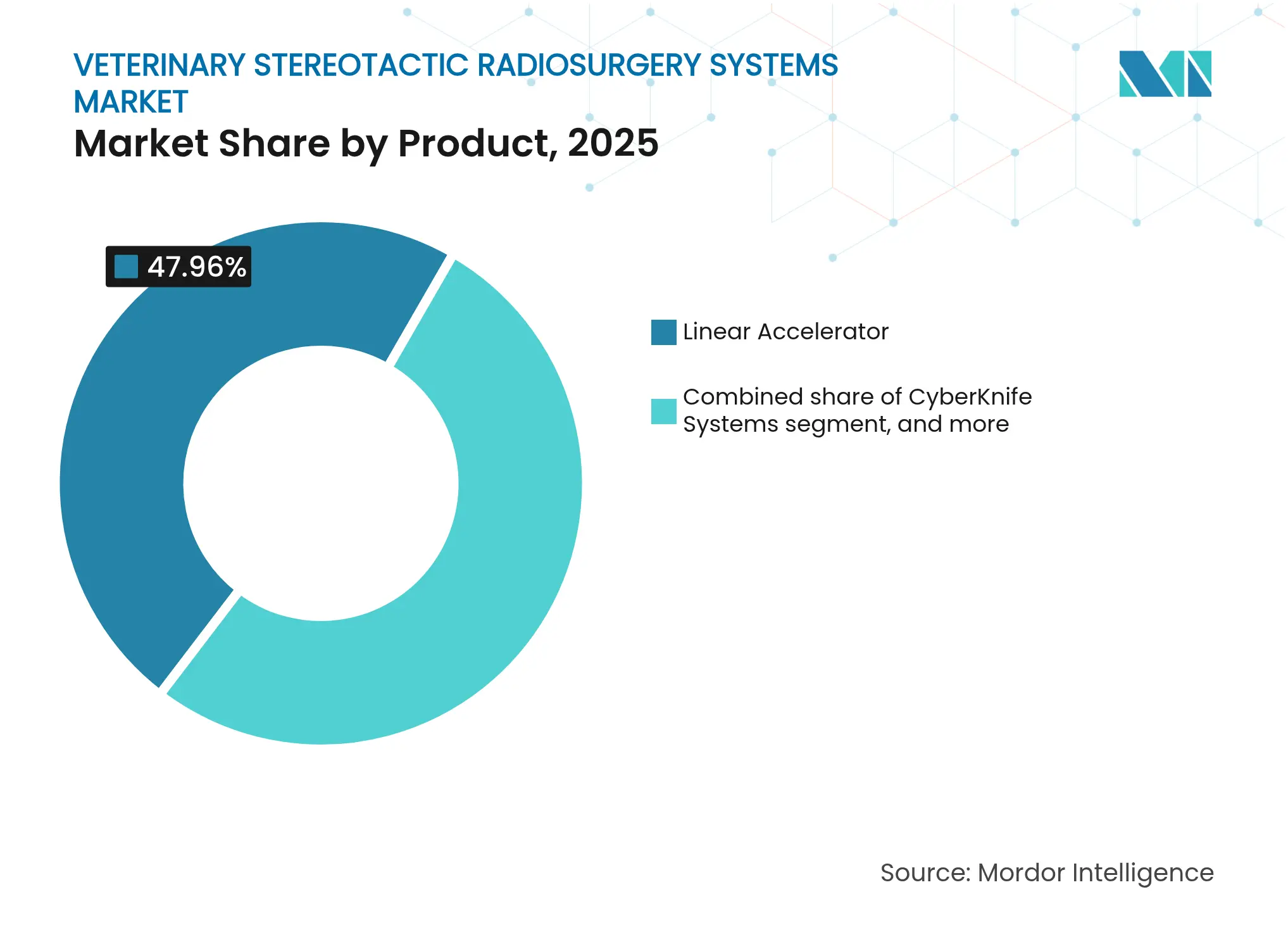

- By product, linear accelerators led with 47.96% revenue share in 2025, while proton and heavy-ion platforms are projected to expand at 13.26% CAGR to 2031.

- By application, brain-tumor cases accounted for 40.98% of the Veterinary stereotactic radiosurgery systems market share in 2025 and head-and-neck treatments are advancing at a 13.15% CAGR through 2031.

- By end user, hospitals held 52.05% of the Veterinary stereotactic radiosurgery systems market size in 2025 and research institutions post the fastest growth at 13.44% CAGR to 2031.

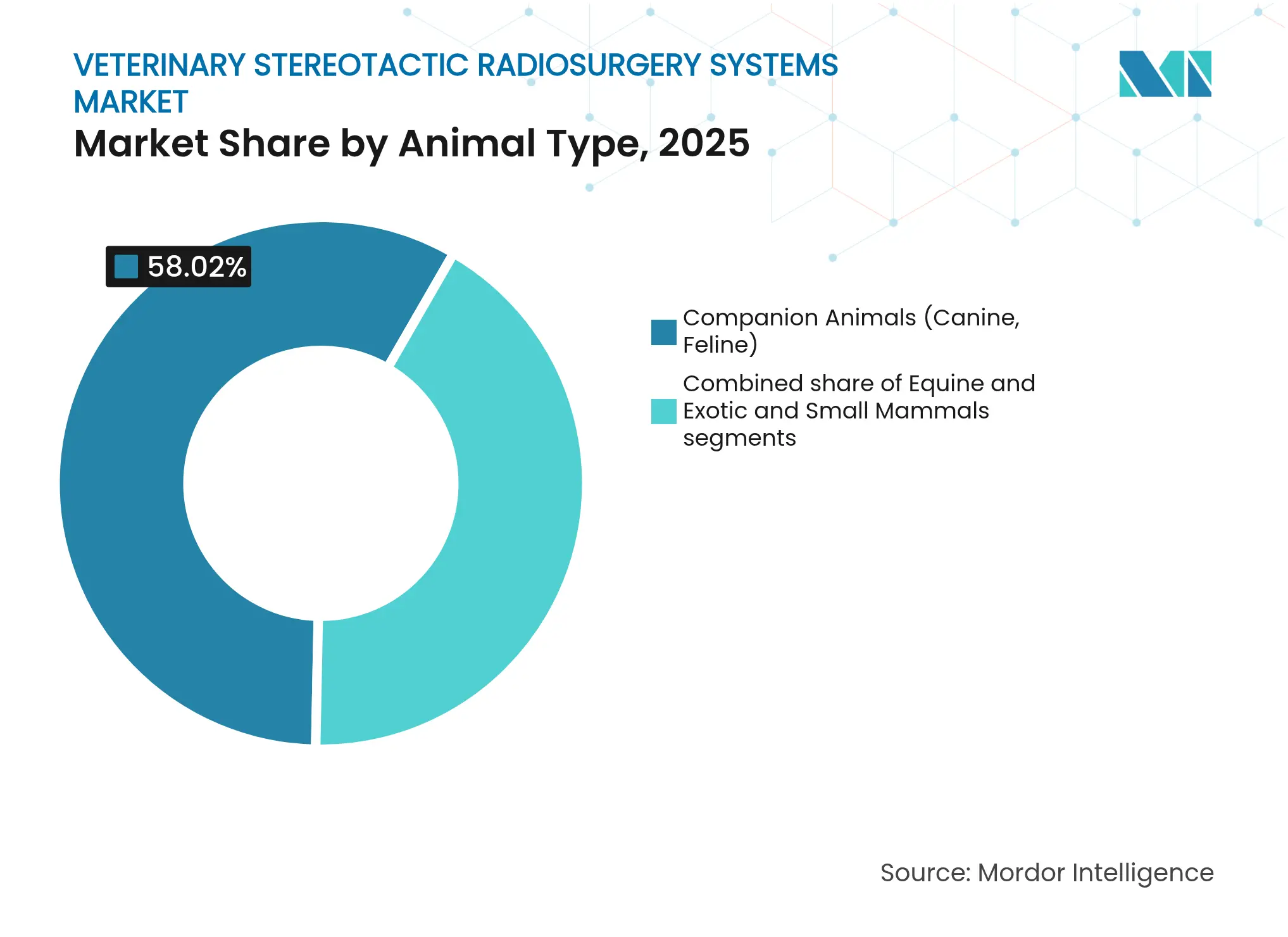

- By animal type, companion-animal cases captured 58.02% share in 2025; equine indications are projected to rise at a 12.71% CAGR between 2026 and 2031.

- By beam technology, photon delivery retained 45.12% share in 2025, whereas proton and heavy-ion beams are gaining at 12.16% CAGR to 2031 IBA.

- By geography, North America led with 38.22% share in 2025; the Asia-Pacific region is expanding at 12.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Stereotactic Radiosurgery Systems Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing companion animal oncology caseload Growing companion animal oncology caseload | +3.2% | Global (strongest in North America & Europe) | Long term (≥4 years) | % Impact on CAGR Forecast:+3.2% | Geographic Relevance:Global (strongest in North America & Europe) | Impact Timeline:Long term (≥4 years) |

Expansion of veterinary specialty referral networks Expansion of veterinary specialty referral networks | +2.8% | North America & EU core; spill-over to APAC | Medium term (2-4 years) | |||

Technological convergence of imaging and radiotherapy platforms Technological convergence of imaging and radiotherapy platforms | +2.1% | Global, led by developed markets | Medium term (2-4 years) | |||

Increasing availability of pet insurance for high-cost procedures Increasing availability of pet insurance for high-cost procedures | +1.9% | North America & EU; emerging in APAC | Long term (≥4 years) | |||

Emerging demand for precision oncology in equine and exotic species Emerging demand for precision oncology in equine and exotic species | +1.3% | Global, early uptake in performance-horse markets | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Companion-Animal Oncology Caseload

One in four dogs develops cancer during its lifetime, making malignancy the principal cause of death in senior pets. Early-detection tools such as IDEXX’s USD 15 Cancer Dx blood test broaden the pool of treatable cases by identifying lymphoma before clinical signs appear. Precision radiosurgery offers sub-millimeter dose targeting that spares healthy tissue, allowing treatment of brain and spinal tumors previously deemed inoperable. Higher caseloads create network effects: as hospitals perform more procedures, outcomes improve and referral confidence rises. This volume-driven model underpins the investment rationale for multi-million-dollar platforms, reinforcing upward demand for equipment and skilled staff.

Expansion of Veterinary Specialty Referral Networks

Corporate groups such as Mars Petcare operate around 3,000 clinics worldwide, many of which funnel complex oncology cases into flagship centers equipped with stereotactic systems. Consolidation aggregates caseloads, improving asset utilization and financing terms for capital purchases. Real-estate investment funds focused on veterinary specialty developments indicate growing outside investor interest, further accelerating infrastructure build-out. Expanded networks shorten client travel distance, reducing a historical barrier to advanced care adoption, and create regional training hubs that enhance workforce capability.

Technological Convergence of Imaging and Therapy

Elekta’s AI-driven Evo linear accelerator integrates high-definition imaging, enabling real-time adaptive planning that compensates for intra-fraction motion. Varian’s HyperSight option halves cone-beam CT acquisition time, addressing anesthesia-duration constraints in veterinary practice. RefleXion’s biology-guided X1 platform links PET imaging and therapy in a single gantry, tracking tumors based on metabolic signals rather than external markers. These innovations cut setup time, streamline workflows, and widen the addressable clinic base by lowering operational complexity. As platforms co-evolve, software upgrades extend hardware life cycles, supporting steady revenue streams for manufacturers and enabling mid-sized hospitals to enter the market.

Increasing Availability of Pet Insurance for High-Cost Procedures

Products from carriers such as Fetch and Healthy Paws reimburse up to 90% of radiation-oncology invoices, removing a key affordability barrier. Average course-of-care costs between USD 3,000 and USD 12,000 move within reach for a growing insured population. Insurers recognize that curative stereotactic regimens can reduce long-term palliative expenses, creating pricing alignment between payers and providers. Predictable reimbursement promotes bank financing of equipment purchases, supporting further diffusion across private referral centers.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital expenditure and operating costs High capital expenditure and operating costs | -2.7% | Global; most acute in emerging markets | Short term (≤2 years) | (~) % Impact on CAGR Forecast:-2.7% | Geographic Relevance:Global; most acute in emerging markets | Impact Timeline:Short term (≤2 years) |

Limited supply of board-certified veterinary radiation oncologists Limited supply of board-certified veterinary radiation oncologists | -2.1% | Global; most severe in APAC & emerging regions | Long term (≥4 years) | |||

Uncertain long-term radiobiological outcomes across species Uncertain long-term radiobiological outcomes across species | -1.4% | Global | Long term (≥4 years) | |||

Limited reimbursement coverage in emerging markets Limited reimbursement coverage in emerging markets | -1.2% | APAC, Latin America, Middle East & Africa | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital Expenditure and Operating Costs

A single linear accelerator requires USD 2–4 million in upfront hardware outlay, plus shielding-room construction that can add USD 1–2 million. Annual service contracts typically equal 3.1% of original cost, while mandatory quality-assurance programs add staffing and dosimetry expenses. In low-volume regions, payer mix and caseload rarely deliver breakeven throughput, curbing new-unit placements. Smaller practices increasingly seek joint-venture or corporate ownership structures to share capital risk, which accelerates consolidation but restricts entry for independent clinics.

Limited Supply of Board-Certified Veterinary Radiation Oncologists

Fewer than 100 specialists are currently credentialed worldwide, with most concentrated in North America and Western Europe. Residency programs span four years beyond veterinary school, and limited faculty capacity constrains annual graduate numbers. Teleconsulting mitigates access gaps but cannot replace on-site expertise for complex adaptive protocols. Recruiting foreign-trained oncologists is hampered by licensing reciprocity hurdles, intensifying salary inflation and reinforcing geographic disparities in treatment availability.

Segment Analysis

By Product: Linear Accelerators Maintain Commanding Lead

Linear accelerators held 47.96% of Veterinary stereotactic radiosurgery systems market share in 2025, reflecting their clinical versatility and favorable cost-to-performance ratio. Proton and heavy-ion systems are projected to expand at 13.26% CAGR as compact designs such as IBA’s Proteus ONE lower footprint and shielding requirements. The Veterinary stereotactic radiosurgery systems market sees continuing preference for platforms offering upgradeable software, multi-energy photon beams, and integration with AI-guided imaging. CyberKnife keeps a niche in frameless intracranial work, while gamma-knife adoption remains limited by single-purpose design.

Upgradability drives replacement cycles, encouraging established users to remain in the linear-accelerator ecosystem. Vendors now offer anesthesia-compatible couches and species-specific immobilization devices, reinforcing the modality’s dominance. Proton installations, although few, become regional referral magnets able to command premium case fees, pushing the Veterinary stereotactic radiosurgery systems market toward a stratified service structure.

Note: Segment shares of all individual segments available upon report purchase

By Application: Brain Tumors Continue to Dominate

Brain lesions accounted for 40.98% of total case volume in 2025 as stereotactic radiosurgery offers non-invasive control where craniotomy carries prohibitive morbidity. Head-and-neck disease lines are rising at 13.15% CAGR, driven by improved immobilization techniques and dose-sculpting algorithms that protect adjacent critical structures. The Veterinary stereotactic radiosurgery systems market size attributed to spinal tumors is also increasing as motion-management tools mature.

Evidence demonstrates median canine survival exceeding two years following stereotactic treatment of intracranial tumors, far outperforming traditional fractionated protocols. Expanding indication sets broaden utilization, enhancing return on equipment investment and stabilizing workflow for treatment teams.

By End User: Hospitals Capture Majority Share

Hospitals delivered 52.05% of all procedures in 2025 as comprehensive oncology departments consolidate surgery, chemotherapy, and radiation under one roof. Research institutions, growing at 13.44% CAGR, secure grant funding to pioneer species-specific protocols, later disseminated to private practice. The Veterinary stereotactic radiosurgery systems market size for clinics with fewer than 10 oncology beds remains constrained by limited capital and staffing, reinforcing acquisition by corporate chains.

Academic partnerships with equipment vendors facilitate early-access studies, accelerating regulatory acceptance of new beam technologies. These collaborations position universities as reference centers, indirectly promoting manufacturer brand equity across the referral network.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Animal Type: Companion-Animal Dominance with Equine Upside

Companion-animal cases represented 58.02% share in 2025, chiefly comprising geriatric dogs and cats with brain or nasal tumors. Equine demand, climbing at 12.71% CAGR, derives from the high economic value of performance horses and breeders’ willingness to invest in limb-sparing interventions. Colorado State University’s adaptation of stereotactic techniques for ferrets, birds, and other exotics highlights a broader diversification trend.

Species-specific immobilization hardware and tailored anesthesia protocols create incremental revenue streams for device manufacturers. As clinical evidence accumulates, insurers may extend coverage beyond dogs and cats, potentially unlocking new share for the Veterinary stereotactic radiosurgery systems market in niche animal segments.

Note: Segment shares of all individual segments available upon report purchase

By Beam Technology: Photon Leads, Proton Advances

Photon platforms delivered 45.12% of treatments in 2025 thanks to entrenched clinical familiarity and lower operating costs. Proton and heavy-ion beams are advancing at 12.16% CAGR, favored for pediatric and ocular indications where dose-sparing is paramount. Veterinary trials reveal comparable local-control rates with reduced acute dermatitis relative to photon plans.

Compact proton units and modular shielding solutions reduce capital barriers, yet high maintenance outlays restrict diffusion to high-volume hubs. As price curves decline, several second-tier referral centers plan installations after 2027, signalling the next growth wave for the Veterinary stereotactic radiosurgery systems market.

Geography Analysis

North America retained a 38.22% revenue share in 2025, underpinned by mature insurance adoption and the presence of large multi-hospital networks able to amortize USD-multimillion equipment costs. Early adoption of technologies such as CyberKnife validates the clinical model and supplies training pipelines for new specialists. Market expansion remains steady as pet-owner awareness rises and early-screening tests feed higher case volumes.

Europe shows mid-single-digit growth buoyed by robust veterinary school infrastructure and harmonized device regulations. Facilities like Dick White Referrals invested GBP 15 million to triple capacity, integrating 0.35-T MRI simulators to streamline adaptive planning. Regional insurers cap out-of-pocket costs, further supporting uptake.

Asia-Pacific, posting 12.28% CAGR, benefits from rising disposable income and evolving regulations that now accept CE-marked radiotherapy systems with limited local testing, accelerating import pathways. China’s urban middle class increasingly views advanced pet care as a lifestyle marker, yet specialist shortages remain acute. Joint-training programs with US and EU colleges are underway to build regional expertise.

South America, the Middle East, and Africa remain nascent markets where import duties and currency volatility hinder equipment procurement. Pilot installations in Mexico signal gradual improvement as governments prioritize companion-animal welfare, but widespread adoption awaits stronger insurance penetration and workforce development.

Competitive Landscape

Market Concentration

Siemens Healthineers’ USD 16.4 billion acquisition of Varian in 2021 formed a vertically integrated powerhouse combining diagnostics, treatment planning, and therapy delivery under one corporate roof. Elekta competes through AI-enabled adaptive features and has won multi-site tenders in Mexico and India, demonstrating appeal in cost-sensitive settings. Accuray’s CyberKnife remains the reference platform for frameless intracranial cases but faces rising photon-linac sophistication that narrows its differentiation.

Disruptors leverage biology-guided or injectable solutions. RefleXion’s X1 received FDA clearance under the expanded-use pathway and is in pre-clinical veterinary trials for moving lung tumors. Vivos’ IsoPet radiogel, an injectable yttrium-90 hydrogel, offers tumor-conforming beta therapy that could reduce or replace external-beam sessions for certain indications.

Competitive pressure concentrates on software ecosystems, workflow automation, and post-sale service rather than brute hardware power. Manufacturers able to bundle cloud-based quality assurance and tele-oncology support stand to win a larger slice of the Veterinary stereotactic radiosurgery systems market.

Veterinary Stereotactic Radiosurgery Systems Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Siemens Healthineers unveiled the “New Ambition” phase of Strategy 2025, prioritizing AI-enhanced precision therapy with explicit veterinary oncology extensions.

- February 2025: Varian partnered with Sun Nuclear to integrate the SunCHECK QA platform, reinforcing safety compliance across small-animal radiotherapy suites.

- January 2025: IDEXX rolled out the Cancer Dx blood test at USD 15 per sample for early canine lymphoma detection, targeting 20 million at-risk dogs in North America.

- December 2024: PetCure Oncology published its 2025 outlook highlighting workflow digitalization and shorter treatment protocols in pet radiotherapy.

- October 2024: Elekta announced a breakthrough adaptive protocol for high-grade gliomas that integrates volumetric MRI data into real-time planning.

- September 2024: RefleXion completed the first multi-modality treatment plan that merged PET signaling with photon delivery, opening the door to biology-guided veterinary applications.

Table of Contents for Veterinary Stereotactic Radiosurgery Systems Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Companion Animal Oncology Caseload

- 4.2.2Expansion of Veterinary Specialty Referral Networks

- 4.2.3Technological Convergence of Imaging And Radiotherapy Platforms

- 4.2.4Increasing Availability of Pet Insurance For High-Cost Procedures

- 4.2.5Emerging Demand for Precision Oncology in Equine And Exotic Species

- 4.3Market Restraints

- 4.3.1High Capital Expenditure and Operating Costs

- 4.3.2Limited Supply of Board-Certified Veterinary Radiation Oncologists

- 4.3.3Uncertain Long-Term Radiobiological Outcomes Across Species

- 4.3.4Limited Reimbursement Coverage in Emerging Markets

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter's Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Linear Accelerator Systems

- 5.1.2CyberKnife Systems

- 5.1.3Gamma Knife Systems

- 5.1.4Proton / Heavy-ion Systems

- 5.2By Application

- 5.2.1Brain Tumours

- 5.2.2Spinal Tumours

- 5.2.3Head & Neck Tumours

- 5.2.4Soft-Tissue / Other Tumours

- 5.3By End User

- 5.3.1Veterinary Hospitals (≥10 oncology beds)

- 5.3.2Veterinary Specialty Clinics (<10 oncology beds)

- 5.3.3Research & Academic Institutions

- 5.4By Animal Type

- 5.4.1Companion Animals (Canine, Feline)

- 5.4.2Equine

- 5.4.3Exotic & Small Mammals

- 5.5By Beam Technology

- 5.5.1Photon Beam

- 5.5.2Gamma Photon

- 5.5.3Proton / Heavy-ion

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East & Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East & Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Accuray Inc.

- 6.3.2Varian Medical Systems Inc.

- 6.3.3Elekta AB

- 6.3.4ViewRay Inc.

- 6.3.5Siemens Healthineers AG

- 6.3.6RefleXion Medical

- 6.3.7ZAP Surgical Systems

- 6.3.8Best Theratronics Ltd.

- 6.3.9Xstrahl Ltd.

- 6.3.10Avante Health Solutions

- 6.3.11Canon Medical Systems Corp.

- 6.3.12United Imaging Healthcare

- 6.3.13Brainlab AG

- 6.3.14PetCure Oncology

- 6.3.15Nanovi A/S

- 6.3.16Medtronic plc

- 6.3.17IntraOp Medical

- 6.3.18VCA Animal Hospitals

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Veterinary Stereotactic Radiosurgery Systems Market Report Scope

As per the scope of the report, the veterinary stereotactic radiosurgery (SRS) systems market involves specialized medical devices used to treat animals with cancer or other abnormal growths through high-precision radiation therapy. These systems target tumors with focused radiation beams, minimizing damage to surrounding healthy tissue.

The veterinary stereotactic radiosurgery systems market is segmented by product, application, end user, and geography. The product segment is further divided into linear accelerator, cyber knife, and gamma knife. The application segment is further segmented into brain tumors, spinal tumors, and other applications. The end user segment is further divided into veterinary hospitals, veterinary specialty clinics, and research and academic institutions. The geography segment is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the market sizes and forecasts in value (USD) for the above segments.