Veterinary Intravenous Solutions Market Size and Share

Market Overview

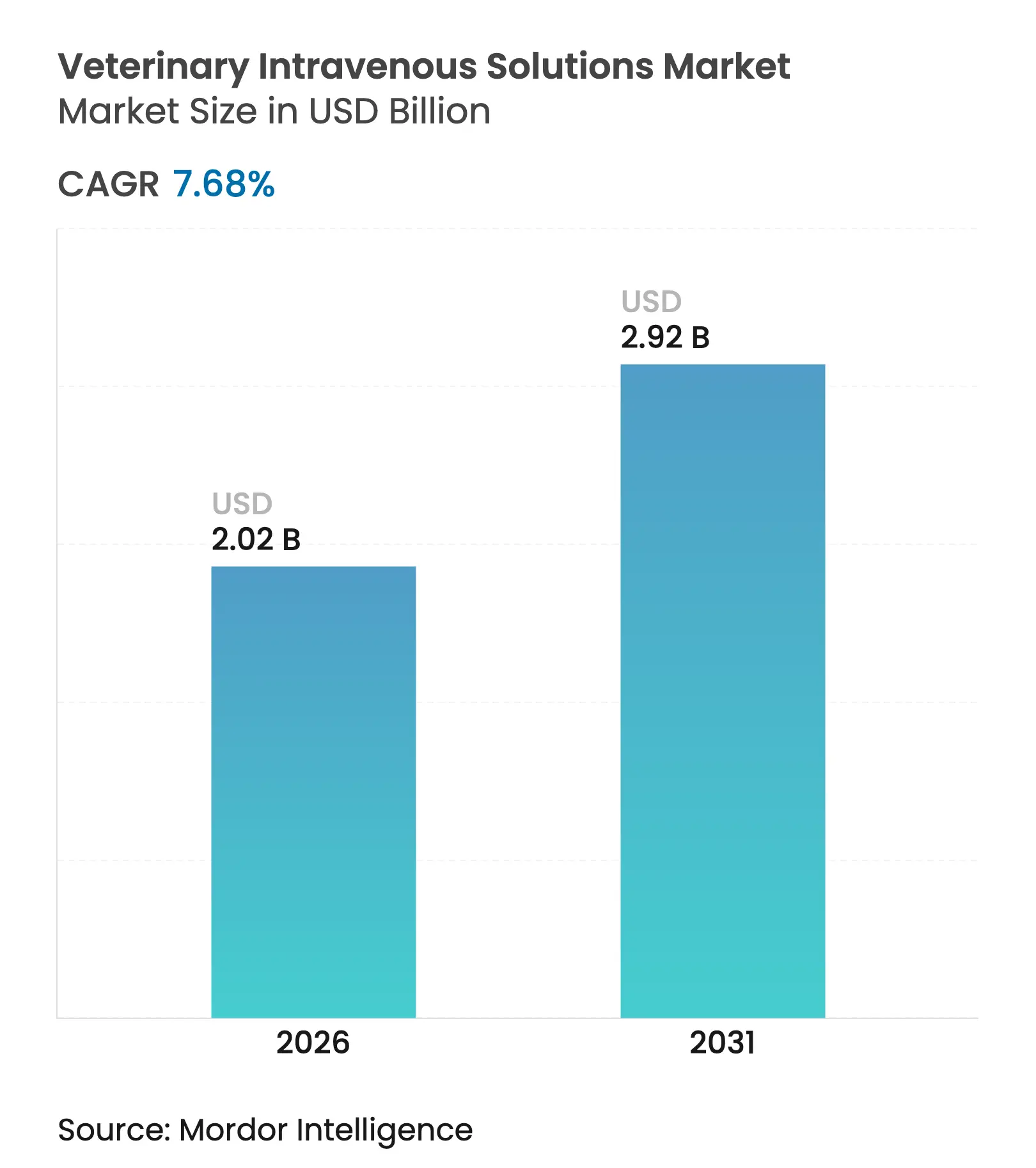

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.92 Billion |

| Growth Rate (2026 - 2031) | 7.68 % CAGR |

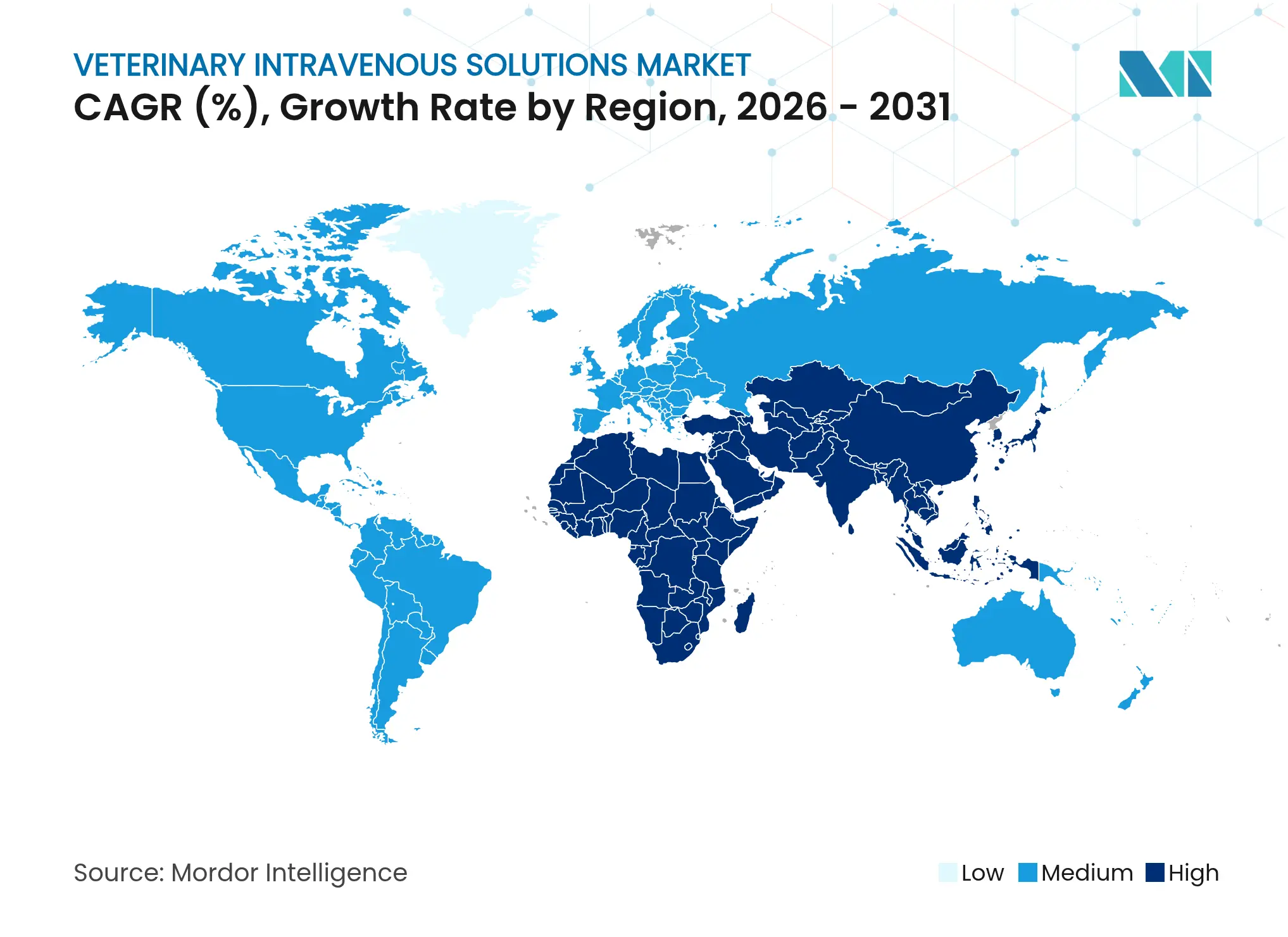

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Veterinary Intravenous Solutions Market Analysis by Mordor Intelligence

Robust pet medicalization, rising production-animal welfare mandates and shifting clinical protocols toward balanced crystalloids jointly sustain demand for precision-formulated fluids. Infrastructure risk became highly visible after Hurricane Helene damaged a Baxter facility supplying 60% of US IV fluids, forcing regulators to fast-track alternative sources and pushing manufacturers to diversify production footprints. Momentum is further reinforced by insurance coverage that now reimburses hospital IV therapies and by a steady flow of complex surgical cases requiring peri-operative fluid management. Industry leaders are responding with heavy capital outlays; B. Braun alone committed USD 1 billion to expand US capacity and add 20% more IV fluid output, signalling long-term confidence in the veterinary intravenous solutions market.

Key Report Takeaways

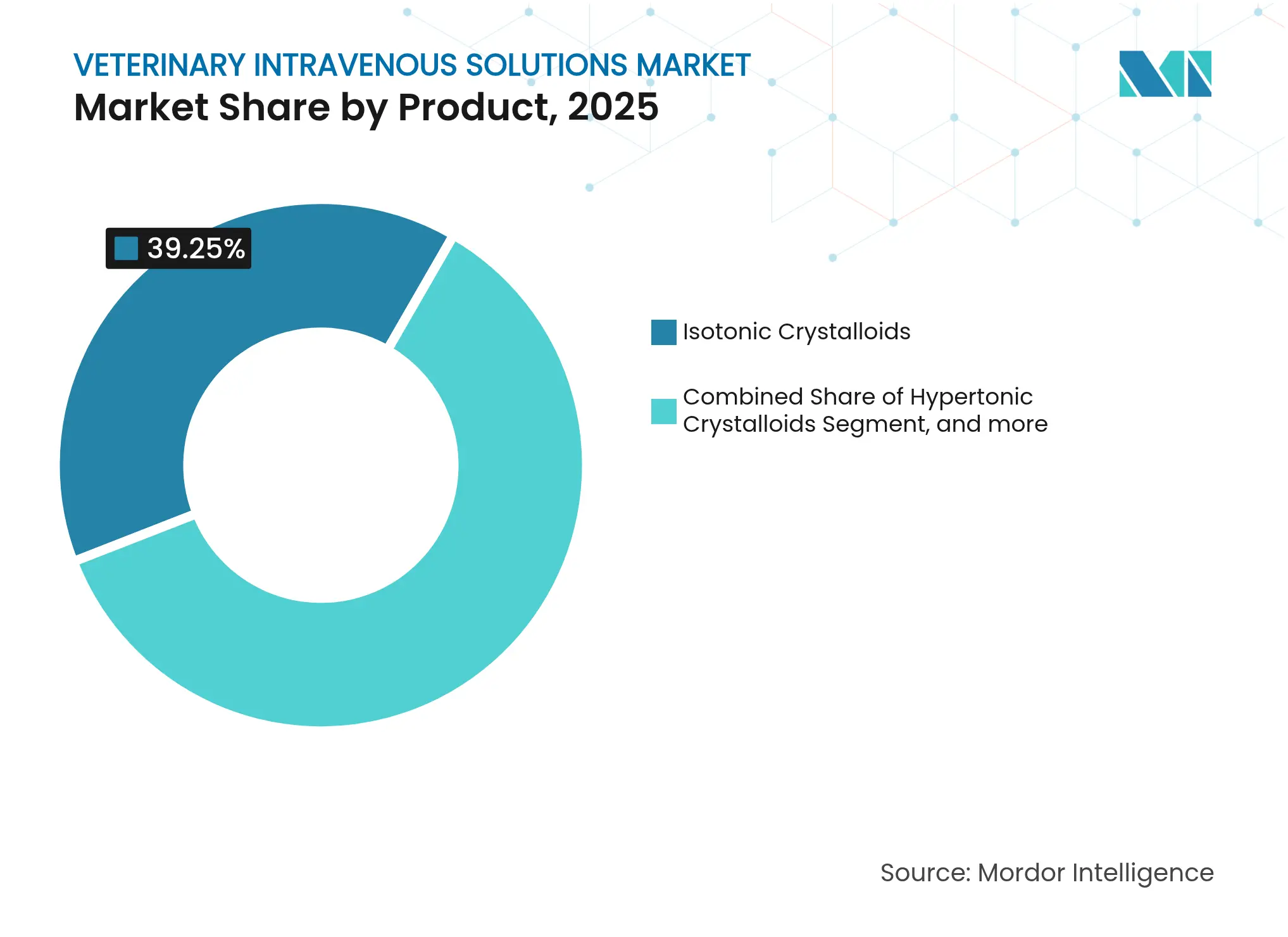

- By product, isotonic crystalloids led with 39.25% of veterinary intravenous solutions market share in 2025; parenteral nutrition is advancing at a 9.62% CAGR through 2031.

- By indication, chronic kidney disease indication commanded 25.62% of the veterinary intravenous solutions market size in 2025; anthrax & septic shock is projected to expand at 10.21% CAGR to 2031.

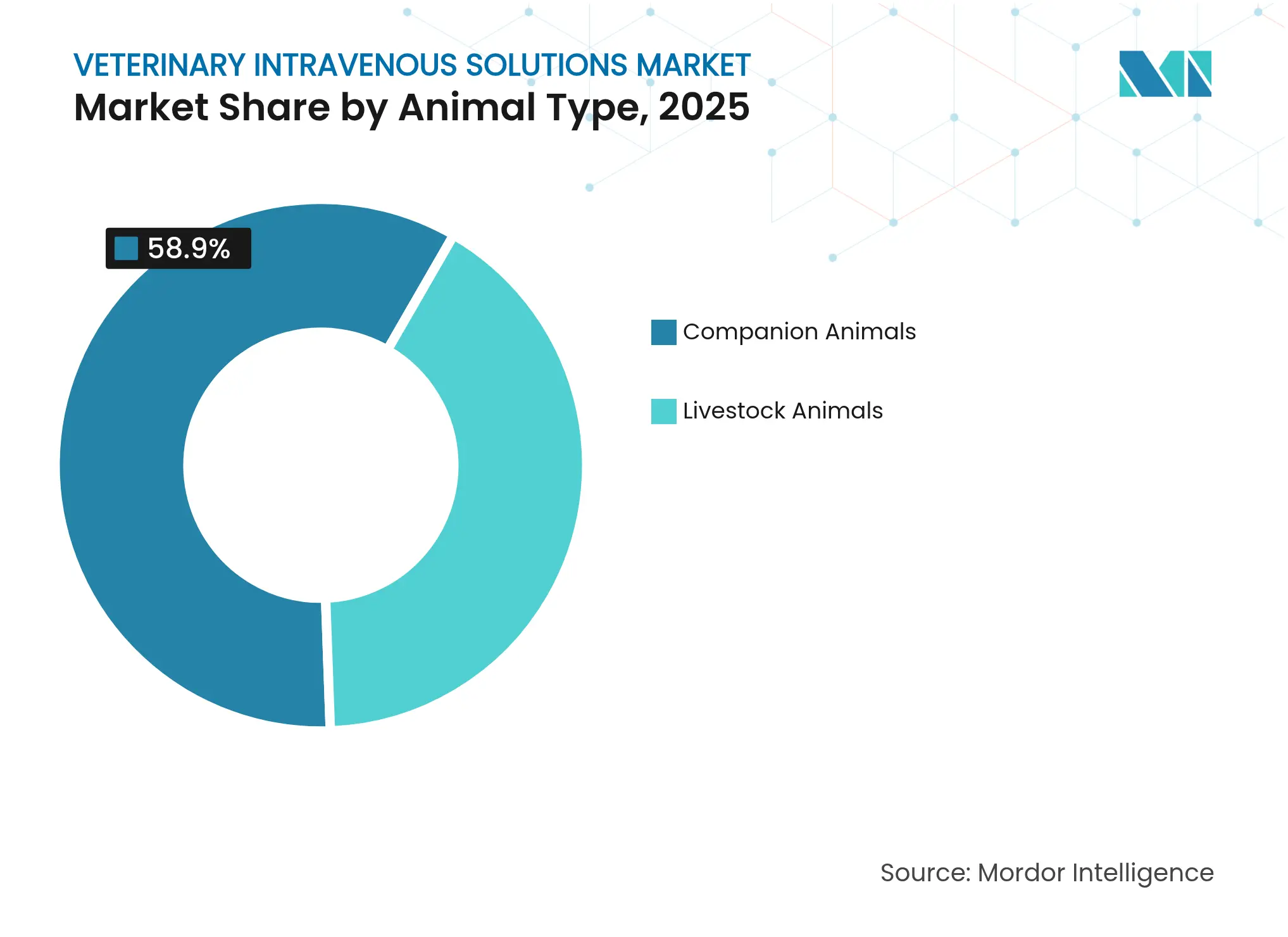

- By animal type, companion animals captured 58.90% revenue share in 2025, while the same segment is forecast to grow at 8.95% CAGR through 2031.

- By end user, veterinary hospitals held 64.10% share of the veterinary intravenous solutions market size in 2025; specialty and emergency clinics exhibit the highest projected CAGR at 10.74% through 2031.

- By geography, North America accounted for 37.95% of 2025 revenue, yet Asia-Pacific is on track for the fastest 11.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Intravenous Solutions Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Soaring

Adoption of Point-Of-Care IV Fluid Therapy Devices in Companion-Animal

Clinics

Soaring

Adoption of Point-Of-Care IV Fluid Therapy Devices in Companion-Animal

Clinics

| +1.8% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

+1.8%

|

Geographic

Relevance

:

North America

& Europe, expanding to APAC

|

Impact

Timeline

:

Medium term

(2-4 years)

|

Expansion of

Production-Animal Welfare Standards Mandating Parenteral Rehydration

Capability

Expansion of

Production-Animal Welfare Standards Mandating Parenteral Rehydration

Capability

| +1.5% | Global, early uptake in EU and North America | Long term (≥ 4 years) | |||

Rise in

Complex Surgical Procedures Driving Peri-Operative Fluid Demand

Rise in

Complex Surgical Procedures Driving Peri-Operative Fluid Demand

| +1.3% | North America & Europe core, spill-over to APAC | Short term (≤ 2 years) | |||

Growth in Pet

Insurance Reimbursements for Hospital IV Therapies

Growth in Pet

Insurance Reimbursements for Hospital IV Therapies

| +1.0% | North America, Australia, moving into Europe | Medium term (2-4 years) | |||

Mainstreaming

of Balanced Isotonic Crystalloids Over Normal Saline

Mainstreaming

of Balanced Isotonic Crystalloids Over Normal Saline

| +0.9% | Global veterinary practice adoption | Short term (≤ 2 years) | |||

Emergence of

Precision Electrolyte-Tailored Fluids for Exotic Species

Emergence of

Precision Electrolyte-Tailored Fluids for Exotic Species

| +0.7% | North America & Europe specialty practices | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Soaring Adoption of Point-Of-Care IV Fluid Therapy Devices in Companion-Animal Clinics

Portable pumps and automated infusion systems now sit beside examination tables, giving clinicians real-time control over bolus delivery and allowing immediate stabilization without outside referral. Practices that invested in these devices during 2024 reported shorter procedure turnaround times, improved labor allocation and higher client retention as critical cases remained in-house.[1]Roberta Leonardi, “Acetate-Buffered Crystalloids in Small-Animal Resuscitation,” frontiersin.org Evidence that acetate-buffered fluids more effectively reduce plasma lactate than traditional lactate formulations has accelerated product turnover toward balanced solutions. This device-driven workflow evolution boosts the specialty and emergency clinic channel’s CAGR and raises per-patient fluid volumes in small-animal medicine.

Expansion of Production-Animal Welfare Standards Mandating Parenteral Rehydration Capability

European directives now obligate commercial farms to maintain IV fluid therapy readiness, compelling even mid-size operations to stock crystalloid solutions formulated for ruminant acid-base profiles.[2]“Fluid Therapy Guidelines for Ruminants,” sciencedirect.com Compliance spending includes refrigerated storage, catheter kits and staff training on large-animal cannulation, spawning a secondary service niche for mobile veterinarians who supply fluids on-site. The policy shift widens the veterinary intravenous solutions market by embedding fluid therapy into everyday herd management instead of crisis response alone.

Rise in Complex Surgical Procedures Driving Peri-Operative Fluid Demand

Elective orthopedics, oncologic resections and cardiovascular interventions have moved from university hospitals to private referral centers. Use of plethysmographic variability index monitoring replaces static central venous pressure readings, sharpening titration accuracy and raising demand for precision-balanced crystalloids. Comparative trials show Plasma-Lyte may provoke transient hypotension relative to Lactated Ringer’s, prompting individualized fluid selection based on procedure length, expected blood loss and patient comorbidities.[3]Carlo Ricciuti, “Hemodynamic Effects of Plasma-Lyte vs Lactated Ringer’s,” mdpi.com These data-driven protocols reinforce Isotonic Crystalloids’ leadership while sustaining double-digit growth for higher-margin balanced formulations.

Growth in Pet Insurance Reimbursements for Hospital IV Therapies

Policy expansions now cover IV infusions given during routine dentals, chronic kidney disease flare-ups and pancreatitis admissions. With cost barriers reduced, clinicians prescribe multi-day fluid plans that include electrolyte panels and infusion pump rentals, raising per-visit revenue and broadening the veterinary intravenous solutions market footprint. The trend reinforces segmentation between value-tier fluids for uninsured owners and premium acetate-buffered products favored by insured clients, encouraging manufacturers to differentiate via safety profiles and packaging innovations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Intermittent

Shortages of Veterinary-Grade IV Bags & Giving Sets

Intermittent

Shortages of Veterinary-Grade IV Bags & Giving Sets

| -1.2% | Global, especially North America & Europe | Short term (≤ 2 years) |

(~) %

Impact on CAGR Forecast

:

-1.2%

|

Geographic

Relevance

:

Global,

especially North America & Europe

|

Impact

Timeline

:

Short term (≤

2 years)

|

Regulatory

Scrutiny of Synthetic Colloids Over Renal Safety

Regulatory

Scrutiny of Synthetic Colloids Over Renal Safety

| -0.8% | Global, with EU and North America leading reviews | Medium term (2-4 years) | |||

Low Clinician

Awareness in Low-Income Livestock Regions

Low Clinician

Awareness in Low-Income Livestock Regions

| -0.6% | APAC, Sub-Saharan Africa, Latin America rural zones | Long term (≥ 4 years) | |||

Price

Sensitivity Among Small-Holder Farmers Limiting Uptake

Price

Sensitivity Among Small-Holder Farmers Limiting Uptake

| -0.5% | Global small-scale agriculture; most acute in APAC & Africa | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Intermittent Shortages of Veterinary-Grade IV Bags & Giving Sets

Hurricane Helene disabled Baxter’s North Carolina plant and removed a critical 60% of US output, forcing clinics to ration fluids, delay elective surgeries and switch borderline cases to oral rehydration. The crisis illuminated high supplier concentration and persuaded regulators to permit cross-label use of human-grade solutions under cascade provisions. Manufacturers now dual-source film resins and mold injection ports in-region, while distributors increase safety-stock thresholds, a logistics revamp expected to normalize supply by mid-2025.

Regulatory Scrutiny of Synthetic Colloids Over Renal Safety

The FDA and EMA demand post-marketing renal safety data on hydroxyethyl starch, and some teaching hospitals have pre-emptively removed colloids from crash carts. Clinics migrating toward high-sodium crystalloids and hypertonic boluses reduce synthetic colloid volumes, shrinking that niche while opening innovation lanes for alginate-based or protein-stabilized expanders.

Segment Analysis

By Product: Isotonic Crystalloids Dominate Amid Innovation Push

Isotonic Crystalloids held 39.25% of the veterinary intravenous solutions market in 2025, cementing their role as the universal first-line fluid across species. Accelerated guideline updates favoring balanced acetate formulations sustain top-line expansion even as mature penetration levels off in North America. Parenteral Nutrition, with a 9.62% CAGR, benefits from improved awareness of negative energy balance during critical illness, prompting clinicians to initiate amino-acid infusions earlier in hospitalization. Hypertonic Crystalloids remain indispensable for rapid resuscitation, especially in field trauma where transport times exceed 30 minutes. Dextrose Solutions fill metabolic support niches, doubling as carriers for antimicrobials in small-volume syringes. Synthetic Colloids experience headwinds as renal safety reviews continue, driving some facilities to treat colloid stock purely as reserve inventory. Blood Products and Plasma Expanders serve specialty centers where transfusion medicine is offered on-site, a sub-market stabilizing after multiple canine plasma recalls tightened sourcing standards. Comparable outcome trials between customized ionic solutions and standard Hartmann’s demonstrate clinical parity, yet premium pricing and inventory complexity temper adoption.

The product mix evolution keeps the veterinary intravenous solutions market responsive to ongoing shifts in clinical evidence, regulatory scrutiny and supply availability. Manufacturers differentiate by offering PVC-free bags, unit-dose micro-infusion pouches and bar-coded labels that integrate with electronic medical records. Collectively, these innovations reinforce a procurement focus on quality and traceability as much as on cost.

Note: Segment shares of all individual segments available upon report purchase

By Indication: Chronic Kidney Disease Leads Clinical Applications

Chronic kidney disease accounted for 25.62% of 2025 revenue, reflecting aging pet demographics and the reliance on isotonic or hypotonic crystalloids to manage uremic crises. Repeat hospitalizations and at-home subcutaneous fluid protocols make CKD a predictable, high-volume demand source within the veterinary intravenous solutions market size for this indication. Anthrax & Septic Shock shows the fastest 10.21% CAGR, driven by proactive fluid resuscitation strategies embedded in livestock biosecurity plans.

Diabetic Ketoacidosis management standards endorse buffered crystalloids with careful potassium supplementation, lifting premium fluid demand during seasonal spikes. Pancreatitis cases draw on balanced isotonic infusions that mitigate third-spacing and electrolyte drift, becoming routine in small-animal internal-medicine wards. Trauma & Haemorrhage still leans on hypertonic solutions and blood products; however, transfusion triggers now integrate viscoelastic testing, sharpening dosing precision. Cumulatively, diverse indication growth trajectories sustain a broad product portfolio, insulating the veterinary intravenous solutions market against single-disease volatility.

By Animal Type: Companion Animals Drive Market Growth

Companion animals represented 58.90% of sales in 2025 and will post a 8.95% CAGR through 2031 as pet humanization boosts willingness to pursue intensive care. Dogs dominate volume, particularly in orthopedics and oncology requiring multi-day infusions, while feline CKD keeps cats a steady second. Exotic pets, though statistically minor, influence product innovation toward micro-bag packaging and calcium-tuned formulations, enhancing brand halo across the veterinary intravenous solutions industry.

Livestock fluids grow steadily on the back of welfare mandates; cattle remain the largest consumers by sheer volume, with per-case bag counts that dwarf companion-animal protocols. Swine breeding units integrate IV therapy for farrowing complications, whereas equine practices require rapid-flow, large-bore ports matched to high-volume shock doses. Poultry applications emerge in intensive farms combating heat stress, signalling additional upside once cost barriers ease.

Note: Segment shares of all individual segments available upon report purchase

By End User: Specialty Clinics Accelerate Growth

Veterinary hospitals captured 64.10% of the veterinary intravenous solutions market size in 2025, leveraging 24-hour staffing, in-house labs and surgical suites that demand continuous fluid availability. Specialty and emergency clinics, however, grow fastest at 10.74% CAGR as referrals for neurology, cardiology and oncology surge.

Highly skilled staff and advanced monitoring gear elevate per-procedure fluid volumes, favouring high-margin balanced crystalloids with low endotoxin counts. Research institutes, while a small slice, act as testbeds for new formulations such as lipid-free parenteral nutrition blends now progressing through clinical trials. On-farm and mobile practices meet livestock demand where transport logistics make clinic visits impractical; these providers value ruggedized packaging and longer shelf-life as they manage ambient-temperature excursions.

Geography Analysis

North America delivered 37.95% of 2025 revenue, underpinned by dense clinic networks, high pet-insurance uptake and rapid adoption of point-of-care infusion technologies. Persistent capacity investments by US manufacturers, including B. Braun’s expansion, improve supply resilience and shorten lead times. Europe ranks second, with stringent animal-welfare directives anchoring steady demand and driving early transition to PVC-free bags. Asia-Pacific is set for an 11.12% CAGR, the fastest globally, as urbanization enlarges the regional pet base and livestock operators adopt international welfare standards.

China’s companion-animal boom fuels small-animal clinic proliferation, while Japanese practitioners lead saline-to-balanced fluid transitions. Australia hosts Zoetis’ growing manufacturing hub near Melbourne, ensuring regional supply redundancy and positioning the firm to capture incremental sales as veterinary intravenous solutions market penetration rises. India’s veterinary infrastructure modernization programs focus on district hospitals and mobile livestock units that collectively widen addressable demand. South America and the Middle East & Africa remain nascent but attractive; Brazil’s bovine sector tests buffered crystalloids in heat-stress mitigation trials, whereas Gulf States invest in equine referral centers catering to a thriving performance-horse industry.

Competitive Landscape

Market Concentration

Global supply turbulence shifted competitive dynamics toward capacity, reliability and regulatory agility rather than price alone. Established pharmaceutical firms leverage vertically integrated resin sourcing, in-house sterilization and multi-country registration portfolios to shield customers from stock-outs. B. Braun’s USD 1 billion commitment to US production, expected to lift its domestic output by 20%, exemplifies a strategy geared toward just-in-time fulfillment and local content assuranc. Baxter re-engineers facility layouts with modular cleanrooms that can be sealed independently, aiming to restart output more rapidly after disruptions.

Zoetis scales its Australian plants fivefold, blending vaccine and fluid manufacturing to share utilities and attain economies of scope. Smaller innovators pursue point-of-care compounding systems that enable clinics to mix acetate-buffered fluids on demand, though regulatory clearance hurdles and sterility validation costs temper immediate uptake. Product differentiation pivots on PVC-free film, twist-off ports that minimize coring risk and bar-coded bag labels compatible with closed-loop medication administration. Intellectual-property filings tilt toward anti-leachate bag materials and algorithmic infusion pumps that auto-adjust flow via hemodynamic feedback. Collectively, these maneuvers suggest a medium-to-high concentration structure where scale remains advantageous yet pockets of niche innovation persist.

Veterinary Intravenous Solutions Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Merck Animal Health received FDA approval for Bravecto Quantum (Fluralaner for Extended-Release Injectable Suspension), the first injectable treatment providing 8-12 months of flea and tick protection for dogs, expanding the company's parasiticide portfolio and demonstrating continued innovation in long-acting veterinary therapeutics.

- October 2024: B. Braun announced plans to ramp up IV fluid production by 20% in response to increased demand following Hurricane Helene's impact on competitor manufacturing facilities, positioning the company to capture market share during supply shortages.

- March 2024: Zoetis purchased a 21-acre manufacturing site in Melbourne, Australia, expanding its manufacturing footprint fivefold and enhancing vaccine production capabilities for livestock and companion animals, following the company's 2022 acquisition of Jurox which added another Australian manufacturing facility.

- February 2024: B. Braun launched Heparin Sodium 2,000 units in 0.9% Sodium Chloride Injection, 1,000 mL, expanding its heparin portfolio and demonstrating commitment to improving supply security for catheter maintenance applications in veterinary and human medicine.

Table of Contents for Veterinary Intravenous Solutions Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Soaring Adoption of Point-of-Care IV Fluid Therapy Devices in Companion-Animal Clinics

- 4.2.2Expansion of Production-Animal Welfare Standards Mandating Parenteral Rehydration Capability

- 4.2.3Rise in Complex Surgical Procedures Driving Peri-Operative Fluid Demand

- 4.2.4Growth in Pet Insurance Reimbursements for Hospital IV Therapies

- 4.2.5Mainstreaming of Balanced Isotonic Crystalloids Over Normal Saline

- 4.2.6Emergence of Precision Electrolyte-Tailored Fluids for Exotic Species

- 4.3Market Restraints

- 4.3.1Intermittent Shortages of Veterinary-Grade IV Bags & Giving Sets

- 4.3.2Regulatory Scrutiny of Synthetic Colloids Over Renal Safety

- 4.3.3Low Clinician Awareness in Low-Income Livestock Regions

- 4.3.4Price Sensitivity Among Small-Holder Farmers Limiting Uptake

- 4.4Porter’s Five Forces Analysis

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Product

- 5.1.1Isotonic Crystalloids

- 5.1.2Hypertonic Crystalloids

- 5.1.3Synthetic Colloids

- 5.1.4Blood Products & Plasma Expanders

- 5.1.5Dextrose Solutions

- 5.1.6Parenteral Nutrition

- 5.2By Indication

- 5.2.1Diabetic Ketoacidosis

- 5.2.2Pancreatitis

- 5.2.3Anthrax & Septic Shock

- 5.2.4Chronic Kidney Disease

- 5.2.5Trauma & Haemorrhage

- 5.2.6Other Indications

- 5.3By Animal Type

- 5.3.1Companion Animals

- 5.3.1.1Dogs

- 5.3.1.2Cats

- 5.3.2Livestock Animals

- 5.3.2.1Cattle

- 5.3.2.2Swine

- 5.3.2.3Equine

- 5.3.2.4Poultry

- 5.4By End User

- 5.4.1Veterinary Hospitals

- 5.4.2Specialty & Emergency Clinics

- 5.4.3Research Institutes

- 5.4.4On-farm / Mobile Practices

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1B. Braun SE

- 6.3.2Baxter International Inc.

- 6.3.3Dechra Pharmaceuticals PLC

- 6.3.4Fresenius Kabi AG

- 6.3.5Zoetis Inc.

- 6.3.6Merck Animal Health

- 6.3.7Elanco Animal Health

- 6.3.8Boehringer Ingelheim Animal Health

- 6.3.9Vetoquinol SA

- 6.3.10Covetrus Inc.

- 6.3.11Henry Schein Animal Health

- 6.3.12Patterson Veterinary

- 6.3.13ICU Medical Inc.

- 6.3.14Aspen Veterinary Resources Ltd

- 6.3.15Sypharma Pty Ltd

- 6.3.16Animalcare Group PLC

- 6.3.17Rusoma Laboratories Pvt. Ltd

- 6.3.18Akina Animal Health

- 6.3.19Piramal Pharma Solutions

- 6.3.20Bimeda Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Veterinary Intravenous Solutions Market Report Scope

As per the scope of the report, veterinary IV solutions are specialized intravenous fluid therapies designed to maintain hydration, restore electrolyte balance, and deliver medications to animals in clinical settings. These solutions are essential for the treatment of various medical conditions and support optimal health and recovery in animals.

The veterinary IV solutions market is segmented by product, indication, animal type, and end user. Based on the product, the market is segmented into isotonic crystalloids, synthetic colloids, blood products, dextrose solutions, and parenteral nutrition. By indication, the market is segmented as diabetic ketoacidosis, pancreatitis, anthrax, chronic kidney disease, and other indications. By animal type, the market is segmented into companion animals and production animals. By end user, the market is segmented as veterinary hospitals, research institutes, and other end users. The report also covers the market sizes and forecasts for the veterinary intravenous solutions market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).