Vertical Cavity Surface Emitting Laser Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

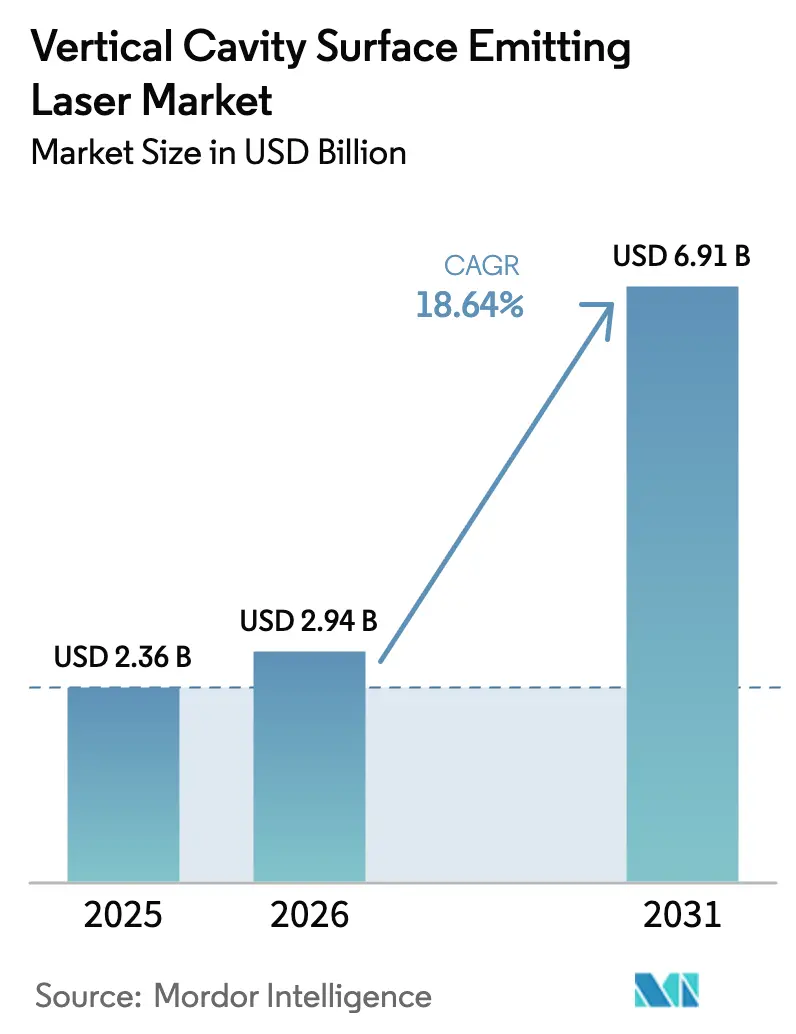

| Market Size (2026) | USD 2.94 Billion |

| Market Size (2031) | USD 6.91 Billion |

| Growth Rate (2026 - 2031) | 18.64% CAGR |

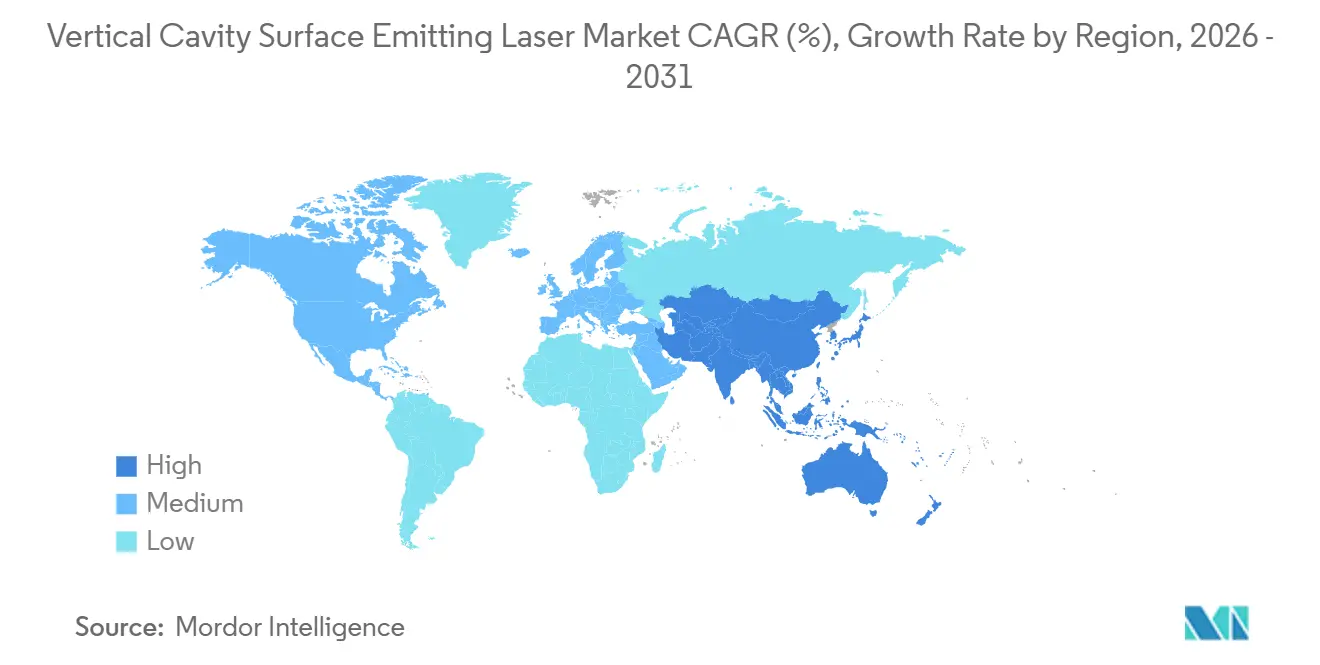

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vertical Cavity Surface Emitting Laser Market Analysis by Mordor Intelligence

The vertical cavity surface-emitting laser market size was USD 2.94 billion in 2026 and is projected to reach USD 6.91 billion by 2031, growing at an 18.64% CAGR. Demand is shifting from legacy 3D sensing toward 200 gigabits-per-lane optical interconnects inside AI-optimized hyperscale data centers, as well as toward multi-junction arrays powering solid-state LiDAR for Level 3 autonomy. Sovereign-AI infrastructure mandates in North America and Europe favor VCSEL links over power-hungry silicon photonics for distances below 300 meters, while automotive original equipment manufacturers embed arrays with power consumption ranging from 70 watts to 400 watts to satisfy forward-collision warning rules. Epitaxial wafer suppliers are reallocating furnace capacity from gallium arsenide to indium phosphide even as yield constraints curb near-term long-wavelength supply. Shortwave-infrared devices are gaining traction due to wider eye-safety windows, and gallium nitride on silicon prototypes promise visible-light cost breakthroughs that could unlock augmented-reality and medical-diagnostic applications.

Key Report Takeaways

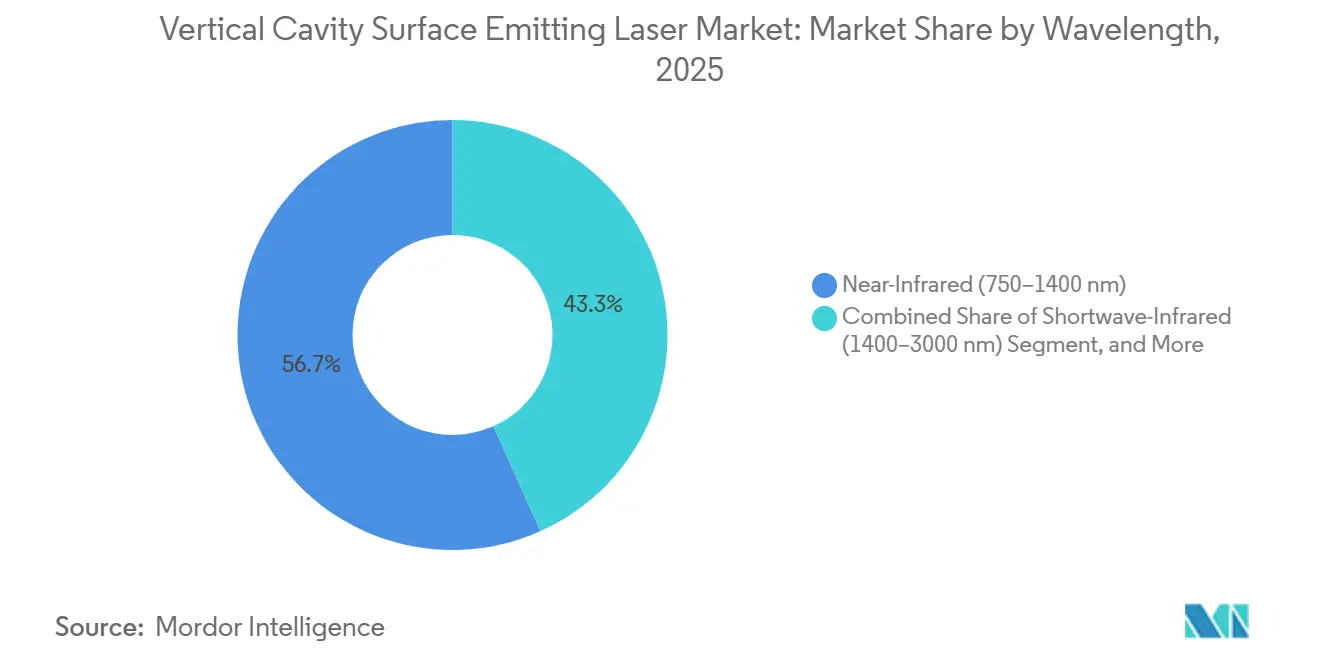

- By wavelength, near-infrared devices held 56.72% revenue share in 2025; shortwave-infrared is forecast to expand at a 19.37% CAGR through 2031.

- By die size, 0.06-0.4 mm² formats commanded 39.14% of the vertical cavity surface emitting laser market share in 2025, while 1.0-7.5 mm² dies are projected to grow at a 19.61% CAGR to 2031.

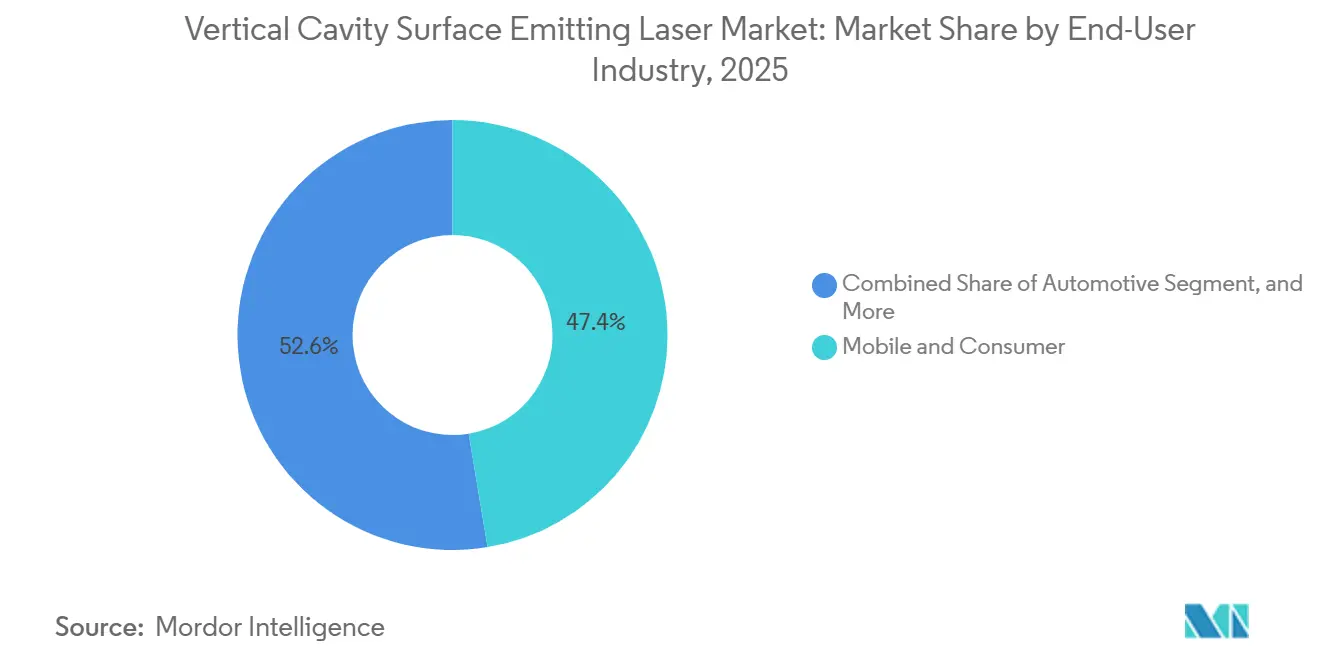

- By end-user industry, mobile and consumer electronics led with 47.39% revenue share in 2025; automotive is set to register the fastest 19.89% CAGR to 2031.

- By application, datacom transceivers accounted for 42.62% of the vertical cavity surface emitting laser market size in 2025, and ADAS LiDAR is advancing at a 20.56% CAGR through 2031.

- By geography, the Asia-Pacific region dominated with a 35.77% share in 2025, whereas the Middle East is poised for the fastest 19.73% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vertical Cavity Surface Emitting Laser Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of VCSEL-based optical links in AI-optimized hyperscale data centers | +4.2% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid integration of 3D sensing VCSEL arrays in flagship and mid-tier smartphones | +3.8% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Transition to long-wavelength (1.3 µm) VCSELs enabling under-display biometric modules | +2.9% | Asia-Pacific and Europe, with early adoption in premium smartphone segments | Medium term (2-4 years) |

| Multi-junction VCSELs powering high-resolution solid-state LiDAR for ADAS | +3.6% | Europe, North America, and China, driven by automotive safety mandates | Long term (≥ 4 years) |

| GaN-on-Si VCSEL platforms lowering cost per emitter and expanding visible-light markets | +2.1% | Global, with manufacturing scale-up in Asia-Pacific | Medium term (2-4 years) |

| Government-backed semiconductor reshoring incentives accelerating new VCSEL fabs | +1.8% | North America and Europe, with spillover to Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of VCSEL-Based Optical Links in AI-Optimized Hyperscale Data Centers

Hyperscale operators are upgrading from 100 gigabit to 200 gigabit lanes to satisfy east-west traffic that scales 4.2 times faster than traditional cloud workloads. Two-dimensional 64-emitter arrays now deliver 1.6 terabit throughput per module, reducing transceiver cost by 18% per gigabit and lowering power draw to 3.8 watts per terabit compared to silicon-photonics alternatives.[1]Coherent Corporation, “Products and Solutions,” coherent.com Front-panel modules are giving way to co-packaged optics that seat VCSEL dies on switch ASICs, cutting hop latency by 12 nanoseconds and driving preference for short-reach multimode links. As Microsoft Azure and other providers strive to achieve power-usage-effectiveness ratios below 1.15, the efficiency advantage of VCSELs bolsters the vertical cavity surface-emitting laser market. Capital-intensive fabs funded by CHIPS Act grants ensure local supply security and accelerate product qualification cycles.

Rapid Integration of 3D Sensing VCSEL Arrays in Flagship and Mid-Tier Smartphones

Smartphone brands have pushed 940-nanometer flood illuminators into devices priced under USD 400, doubling the addressable unit base between 2024 and 2027. New dot projectors exceed 1.2 watts peak power yet unlock faces in under 0.4 seconds under bright sunlight.[2]Lumentum Operations LLC, “VCSEL Products and Applications,” lumentum.com Compact 2.4 mm × 3.2 mm monolithic modules shave 34% board space, easing adoption in foldable hinges and wearables. Depth-map quality supports on-device AR filters and gesture navigation, while cross-industry volumes with automotive cabin cameras erode die cost by USD 0.14 annually. The use case breadth sustains double-digit growth for the vertical cavity surface-emitting laser market, even as overall smartphone shipments plateau.

Transition to Long-Wavelength 1.3 µm VCSELs Enabling Under-Display Biometric Modules

Emission at 1,300 nanometers traverses organic LED stacks with 2.8 dB less loss than 940-nanometer light, enabling secure fingerprint capture beneath 1.2-millimeter displays. Wall-plug efficiency now tops 28%, lowering battery drain to 12 milliwatts per unlock event. However, indium phosphide wafers carry 62% higher cost and yield only 74%-78%, constraining supply.[3]IEEE Xplore Digital Library, “Conference Proceedings and Journals,” ieeexplore.ieee.org Equipment vendors are racing to achieve yields of over 82% by late 2026, a milestone that could open up mass-volume mid-tier smartphones to long-wavelength sensors. Until then, premium devices and medical scanners will anchor demand, ensuring a stable revenue pool for the vertical cavity surface-emitting laser market.

Multi-Junction VCSELs Powering High-Resolution Solid-State LiDAR for ADAS

Three- to five-junction stacks now deliver a peak output of 70 watts to 400 watts, enabling 200-meter pedestrian detection and meeting Euro NCAP 5-star protocols for 2026 vehicles. Automotive original equipment manufacturers prefer solid-state architectures because they reduce sensor costs from USD 1,200 to USD 380 per unit and improve the mean time between failures compared to mechanical scanners. Regulatory momentum, notably the European General Safety Regulation, creates non-discretionary demand that propels the vertical cavity surface-emitting laser market well beyond consumer electronics cycles. Thermal design remains challenging, yet breakthroughs in microchannel cooling hint at the possibility of continuous-wave operation for upcoming highway-speed autonomous vehicles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited yield for InP-based VCSEL epitaxy constrains long-wave supply | -2.4% | Global, with acute impact in Asia-Pacific epitaxial wafer fabs | Short term (≤ 2 years) |

| Short optical reach versus silicon photonics in next-generation data center architectures | -1.8% | North America and Europe, concentrated in hyperscale data centers | Medium term (2-4 years) |

| IP concentration raises licensing costs for emerging VCSEL suppliers | -1.3% | Global, with higher barriers in North America and Europe | Long term (≥ 4 years) |

| Tight eye-safety regulations cap output power in automotive cabin applications | -1.1% | Europe and North America, driven by IEC 60825 compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Yield for InP-Based VCSEL Epitaxy Constrains Long-Wave Supply

Defect densities in indium phosphide wafers remain 2.3 times higher than those in gallium arsenide, suppressing yield and keeping die costs USD 1.80 above those of 940-nanometer equivalents, a burden for price-sensitive consumer gadgets. Substrate prices average USD 420 for a 3-inch wafer, while metal-organic chemical vapor deposition reactors run at only 68% utilization, far from scale economies. Planned expansions worth USD 48 million will not reach full output until late 2027, prolonging shortages for under-display sensors and long-reach datacom links. The bottleneck temporarily hinders the otherwise robust growth of the vertical cavity surface-emitting laser market.

Short Optical Reach Versus Silicon Photonics in Next-Generation Data Centers

VCSEL multimode links top out near 300 meters at 400 gigabit speeds, whereas single-mode silicon photonics spans 2-10 kilometers. Co-packaged silicon photonics modules already consume 4.2 watts per terabit and cut hop latency by 18 nanoseconds. Hyperscalers with campus-scale fabrics must add active optical cables or hybrid architectures when VCSEL reach proves insufficient, inflating capital expenses. Precision-aligned single-mode VCSEL prototypes promise a 2-kilometer reach, but the packaging budget rises by USD 2.40 per transceiver, and volume shipments are unlikely before 2028. This technical gap siphons momentum from the vertical cavity surface-emitting laser market within ultra-large data halls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Wavelength: Eye-Safety Drives Shortwave-Infrared Momentum

Near-infrared devices, ranging from 750 nanometers to 1,400 nanometers, controlled 56.72% of the revenue in 2025, an anchor segment for datacom transceivers and smartphone depth cameras. Shortwave-infrared emitters between 1,400 nanometers and 3,000 nanometers are expanding at a 19.37% CAGR due to looser IEC 60825 limits that allow 10 times higher optical power, a game-changer for cabin monitoring systems that must scan beyond 1.2 meters without triggering retinal-hazard warnings.

Lumentum documented 34% year-over-year growth in shortwave-infrared shipments in 2025, with automotive tier-1 suppliers integrating 1,550-nanometer arrays into head-up displays. Red wavelengths below 750 nanometers continue to fade as optical mice give way to capacitive interfaces. Bifurcated supply chains emerge: gallium arsenide fabs prioritize high-volume orders for 850 nanometer and 940 nanometer, while indium phosphide specialists chase automotive and medical margins, collectively reshaping the vertical cavity surface-emitting laser market.

By Die Size: Large-Format Arrays Satisfy LiDAR Power Budgets

The footprints of 0.06-0.4 mm² held a 39.14% share in 2025, as they balance thermal load with facial-recognition performance inside smartphones. To meet the 8 kW/cm² irradiance threshold required for a 200-meter LiDAR, formats ranging from 1.0 to 7.5 mm² are witnessing an impressive annual growth rate of 19.61%. This growth is driven by the increasing demand for high-performance LiDAR systems in applications such as autonomous vehicles, robotics, and advanced mapping technologies, where precise and efficient sensing capabilities are critical.

ams OSRAM now ships 3.5 mm² multi-junction arrays that reach 100-watt peaks for mid-range passenger cars. TRUMPF’s 7.2 mm² dies demonstrated 400-watt bursts, although limited to 0.8% duty cycles, prompting the implementation of microchannel cooling programs. Larger die areas yield 72% versus 88% for mid-sizes, prompting fabrication-line analytics to mitigate scrap. The scale shift highlights how ADAS adoption reconfigures revenue pools within the vertical cavity surface-emitting laser market.

By End-User Industry: Automotive Becomes the Fastest Climber

Mobile and consumer electronics accounted for 47.39% demand in 2025, fueled by 3D sensing in handsets, tablets, and XR headsets. Driven by Euro NCAP and Chinese mandates, solid-state LiDAR has become indispensable in modern automotive systems. This development has propelled automotive demand to a 19.89% CAGR, significantly outpacing consumer growth by 4.2 percentage points. The increasing emphasis on safety and regulatory compliance has further solidified the role of solid-state LiDAR as a critical component in the automotive market.

The European regulation suite lifts VCSEL dollar content per vehicle from USD 18 in 2024 to USD 64 in 2028. Lumentum reported 52% growth in automotive shipments for fiscal 2025. The telecom and medical segments remain steady, while the industrial processing sector taps into VCSEL energy density for plastic welding and selective laser sintering. Regulatory pull, rather than consumer refresh cycles, is increasingly governing the vertical cavity surface-emitting laser market's trajectory.

By Application: ADAS LiDAR Surges Past Legacy Datacom Growth

Datacom still represents 42.62% deployment volume, anchored by 100 gigabit and 400 gigabit modules in enterprise fabrics. Multi-junction arrays, which enable centimeter-level depth resolution even at highway speeds, are driving significant growth in the ADAS LiDAR market. This technology is contributing to a robust 20.56% CAGR, highlighting its critical role in enhancing advanced driver-assistance systems.

Beyond forward-collision systems, cabins are adopting gesture control cameras to reduce driver distraction by 18%, opening incremental emitter sockets. Facial recognition, proximity sensing, and laser autofocus remain sizable but mature niches, while medical diagnostics pilots leverage 1,550-nanometer light for non-invasive glucose monitoring. The widening application spread keeps the vertical cavity surface-emitting laser market resilient, even if any single end-use stalls.

Geography Analysis

In 2025, the Asia-Pacific region commanded a dominant 35.77% share, buoyed by Taiwanese and Japanese epitaxial fabs running at an impressive 82% utilization rate. This strong performance highlights the region's pivotal role in the global semiconductor market, driven by advancements in manufacturing capabilities and robust demand for cutting-edge technologies. Meanwhile, China's CNY 28 billion investment in its compound semiconductor fund is strategically targeting self-sufficiency in 850-nanometer and 940-nanometer technologies by 2027, reflecting the country's commitment to reducing reliance on imports and strengthening its domestic semiconductor ecosystem.

Coherent and Lumentum have expanded in North America, bolstered by USD 1.8 billion in CHIPS Act grants, which mitigate supply risks for hyperscalers by ensuring a more stable and secure supply chain. This funding supports the development of advanced photonics technologies critical for hyperscale data centers. Meanwhile, Europe, centered in Germany's photonics belt, benefits from its closeness to automotive tier-1 plants, which not only reduces VCSEL lead times from 14 weeks to just 9 but also enhances collaboration opportunities with key automotive manufacturers, fostering innovation in photonics applications.

Sovereign funds are increasingly investing in hyperscale campuses in Saudi Arabia and the UAE, driving a projected 19.73% CAGR in the Middle East and Africa. These investments aim to support the training of localized large-language models, which are critical for advancing regional technological capabilities. Additionally, geographic diversification is playing a key role in mitigating political supply chain risks, thereby strengthening the global vertical cavity surface-emitting laser market and ensuring its resilience against geopolitical uncertainties.

Competitive Landscape

Global epitaxial capacity is moderately concentrated, with the top five companies accounting for approximately 68%. However, downstream packaging remains fragmented, featuring more than 30 integrators. Incumbents extend their advantage through vertically integrated wafer-to-module lines, which shave 14%-18% off the cost compared to fabless peers. Coherent added 14 patents on array thermal management in 2025, bringing its portfolio to 420 families and reinforcing automotive LiDAR moats.

Entrants face a cap on gross margins at 32% due to licensing fees of USD 0.18-0.24 per die for distributed Bragg reflector and oxide-aperture know-how, especially in the absence of cross-licenses. These licensing fees significantly impact the profitability of new players in the market, creating a challenging environment for those without established partnerships or proprietary technologies. Meanwhile, gallium nitride on silicon competitors are luring augmented-reality and medical buyers by slashing visible-light emitter prices by as much as 28%. This aggressive pricing strategy is encouraging buyers to diversify their supplier base, potentially reshaping the competitive landscape in these application areas.

Single-mode architectures for 2-kilometer datacom links remain a white space because silicon photonics dominates today, yet several VCSEL suppliers have joined co-packaged optics consortia to co-develop switch-ASIC-mounted arrays that eliminate front-panel modules. These alliances could shift market share in high-bandwidth AI clusters, adding fresh momentum to the vertical cavity surface-emitting laser market.

Vertical Cavity Surface Emitting Laser Industry Leaders

Coherent Corporation

Lumentum Operations LLC

Hamamatsu Photonics KK

TRUMPF Group

ams OSRAM AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Vertilite secured

- November 2025: Lumentum rolled out M-Series 100 watt and 400 watt arrays aimed at 128-line and 256-line LiDAR, enabling 200 meter vehicle detection.

- October 2025: Coherent announced a USD 180 million indium phosphide expansion in Pennsylvania to increase 1.3 µm and 1.55 µm wafer output by 42%.

- September 2025: ams OSRAM released a 2.4 mm × 3.2 mm proximity sensor that integrates VCSEL and time-of-flight receiver, shrinking board space 34%.

Global Vertical Cavity Surface Emitting Laser Market Report Scope

The Vertical Cavity Surface Emitting Laser Market Report is Segmented by Wavelength (Red, Near-Infrared, Shortwave-Infrared), Die Size (0.02-0.06 mm², 0.06-0.4 mm², 0.4-1.3 mm², 1.0-7.5 mm²), End-User Industry (Telecom, Mobile and Consumer, Automotive, Medical, Industrial, Aerospace and Defense), Application (Datacom, Facial Recognition and Depth Camera, Gesture Recognition, Proximity Sensing, Laser Autofocus, Iris Scan, Medical Diagnostics, ADAS LiDAR, Industrial Processing, Optical Mouse, Other Application), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Red (650–750 nm) |

| Near-Infrared (750–1400 nm) |

| Shortwave-Infrared (1400–3000 nm) |

| 0.02 – 0.06 mm² |

| 0.06 – 0.4 mm² |

| 0.4 – 1.3 mm² |

| 1.0 – 7.5 mm² |

| Telecom |

| Mobile and Consumer |

| Automotive |

| Medical |

| Industrial |

| Aerospace and Defense |

| Datacom |

| Facial Recognition and Depth Camera |

| Gesture Recognition |

| Proximity Sensing |

| Laser Autofocus |

| Iris Scan |

| Medical Diagnostics |

| ADAS LiDAR |

| Industrial Processing |

| Optical Mouse |

| Other Application |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Wavelength | Red (650–750 nm) | ||

| Near-Infrared (750–1400 nm) | |||

| Shortwave-Infrared (1400–3000 nm) | |||

| By Die Size | 0.02 – 0.06 mm² | ||

| 0.06 – 0.4 mm² | |||

| 0.4 – 1.3 mm² | |||

| 1.0 – 7.5 mm² | |||

| By End-User Industry | Telecom | ||

| Mobile and Consumer | |||

| Automotive | |||

| Medical | |||

| Industrial | |||

| Aerospace and Defense | |||

| By Application | Datacom | ||

| Facial Recognition and Depth Camera | |||

| Gesture Recognition | |||

| Proximity Sensing | |||

| Laser Autofocus | |||

| Iris Scan | |||

| Medical Diagnostics | |||

| ADAS LiDAR | |||

| Industrial Processing | |||

| Optical Mouse | |||

| Other Application | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the vertical cavity surface emitting laser market?

The market reached USD 2.94 billion in 2026 and is projected to hit USD 6.91 billion by 2031.

Which application is growing fastest for VCSELs?

ADAS LiDAR leads with a 20.56% CAGR through 2031 as automakers adopt solid-state depth sensing to meet safety mandates.

Why are shortwave-infrared VCSELs gaining traction?

IEC 60825 Class 1 limits allow higher optical output at 1,550 nanometers, providing longer range and safer operation for automotive cabin monitoring.

How are hyperscale data centers using VCSEL technology?

Operators deploy 200 gigabit-per-lane multimode links and co-packaged optics to support bandwidth-intensive AI training clusters with lower power budgets.

Which region is expected to record the highest growth rate?

The Middle East projects a 19.73% CAGR due to sovereign investments in localized AI infrastructure.

What manufacturing hurdle limits long-wavelength VCSEL supply?

Indium phosphide epitaxial yields remain below 78%, raising die costs and constraining 1.3 µm and 1.55 µm device availability.

Page last updated on: