Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 4.16 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Occupancy Sensor Market Analysis by Mordor Intelligence

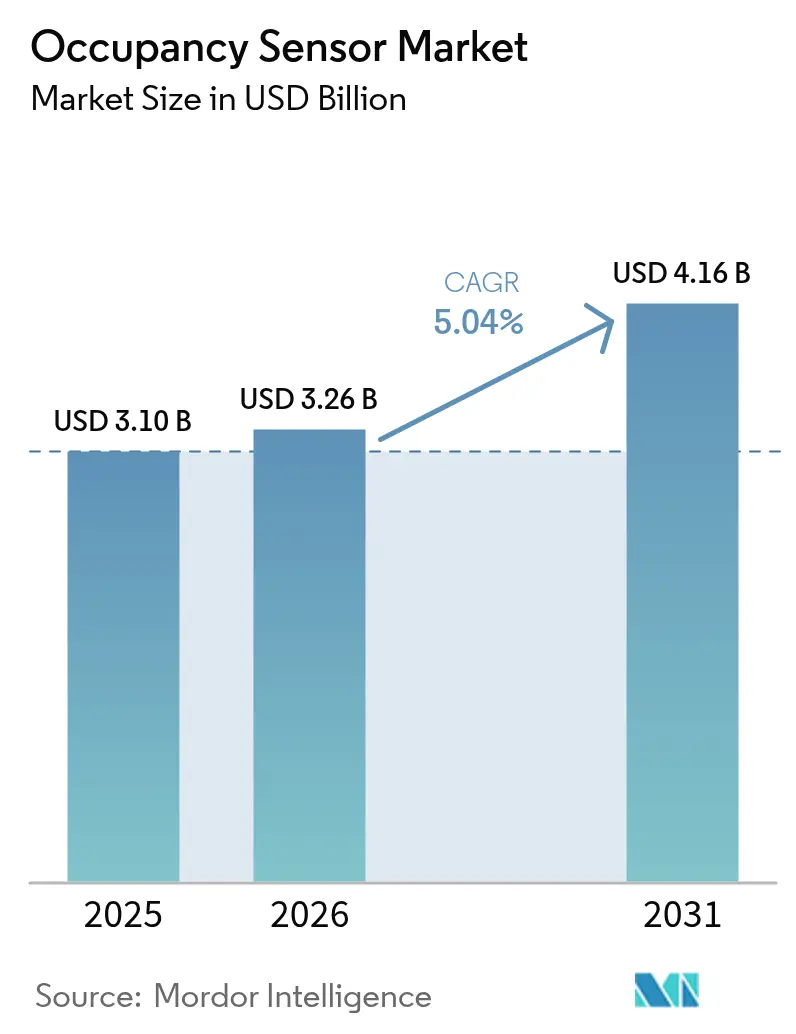

The Occupancy Sensor Market size was valued at USD 3.10 billion in 2025 and estimated to grow from USD 3.26 billion in 2026 to reach USD 4.16 billion by 2031, at a CAGR of 5.04% during the forecast period (2026-2031).

Stricter net-zero building codes in the United States and European Union, China’s dual-carbon roadmap, and expanding healthcare compliance programs are turning occupancy detection from a discretionary energy-savings measure into a legal requirement f-t.com. Corporate demand has shifted from trial deployments to systematic roll-outs that integrate sensors with building management platforms. Commercial property owners now prioritize data analytics that optimize space utilization and HVAC loads, while residential adoption gains pace as smart homes become mainstream. Technology convergence is visible: wired networks still command 62% of deployments for reliability, yet wireless nodes are advancing at a 12.4% CAGR as mesh protocols mature.

Key Report Takeaways

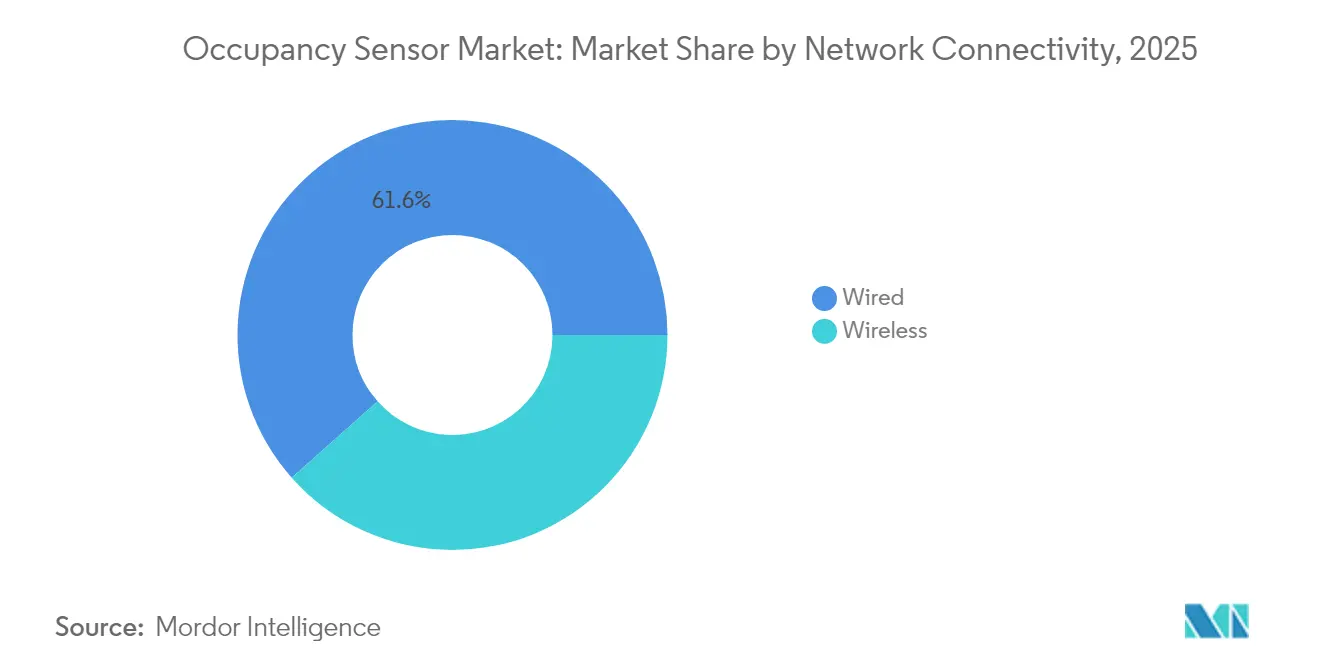

- By network connectivity, the wired segment led with 61.55% of the occupancy sensor market share in 2025, whereas wireless nodes are set to expand at a 12.18% CAGR through 2031.

- By technology, passive infrared retained 49.72% revenue share in 2025; dual/multi-technology sensors are forecast to post a 13.12% CAGR to 2031.

- By mounting type, ceiling-mounted units captured 44.55% of the occupancy sensor market size in 2025, while desk-integrated designs record the fastest 14.58% CAGR to 2031.

- By installation, retrofits accounted for 54.35% of deployments in 2025; new construction grows at 12.93% CAGR through 2031.

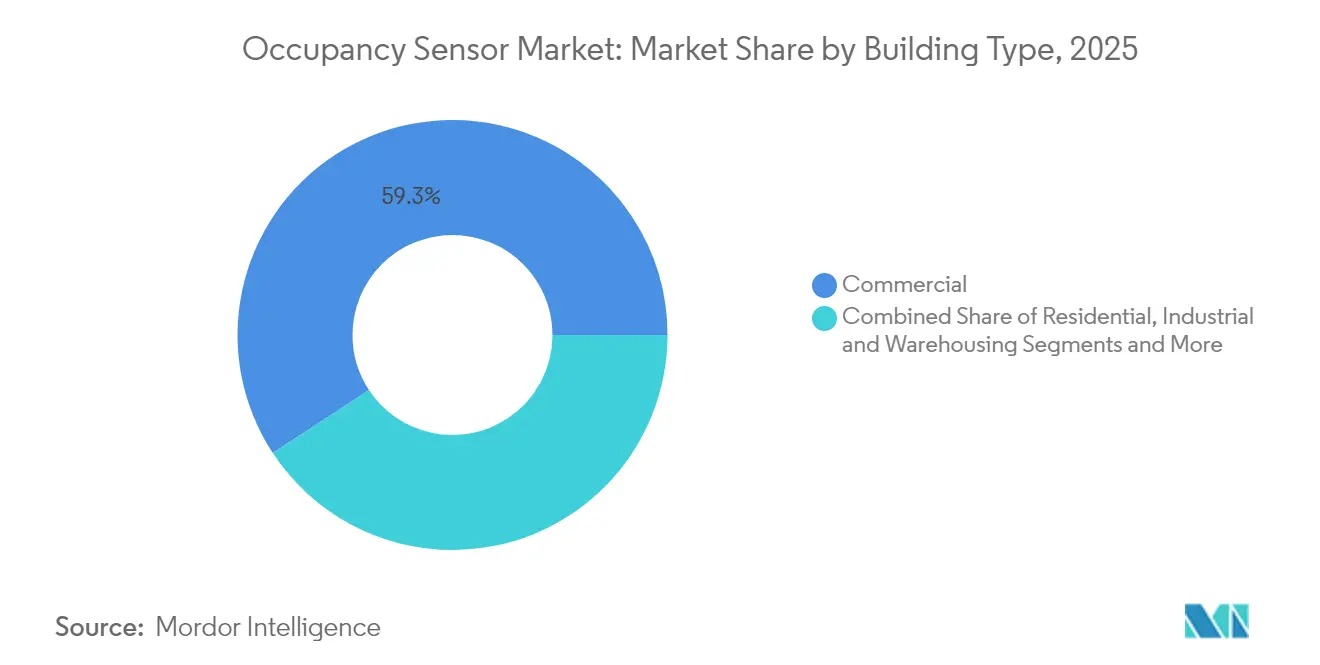

- By building type, commercial facilities held 59.25% of the occupancy sensor market share in 2025, while residential demand rises at 12.55% CAGR to 2031.

- By application, lighting control dominated with 45.40% share in 2025; HVAC and ventilation control advance at 13.88% CAGR.

- Johnson Controls, Signify, Honeywell, and Schneider Electric collectively controlled about 29.45% of 2025 global revenues, reflecting a moderately concentrated field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Occupancy Sensor Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stricter Net-Zero Building Codes in U.S./EU Mandating Occupancy‐Based Shut-off | +1.2% | North America & EU | Medium term (2-4 years) |

| China "Dual-Carbon" Roadmap Boosting Smart Lighting IoT | +0.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| IoT-Driven Space Utilization Analytics Upselling Sensors | +0.7% | Global | Short term (≤ 2 years) |

| Healthcare Bed-Occupancy Programs Under CMS & MDR | +0.5% | North America & EU | Medium term (2-4 years) |

| Multi-Sensor Chipset Cost Decline Opening HVAC OEM Channel | +0.6% | Global | Short term (≤ 2 years) |

| AI-Enhanced Sensor Integration for Predictive Building Analytics | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter net-zero building codes in U.S./EU mandating occupancy-based shut-off

California’s Title 24 now requires occupancy sensing for receptacle and ventilation shut-off within 20 minutes of vacancy, while the 2021 International Energy Conservation Code mandates automatic controls in enclosed spaces. European renovation programs targeting 35 million buildings by 2030 echo these rules, making compliance rather than energy savings the primary adoption trigger. Commercial owners therefore embed sensors in construction documents rather than adding them post-build. This dynamic lifts baseline demand across the occupancy sensor market.[1] Energy Code Ace, “SECTION 120.1 – Requirements for Ventilation and Indoor Air Quality,” energycodeace.com

China dual-carbon roadmap boosting smart lighting IoT

China’s goal of a 2030 carbon peak and 2060 neutrality propels smart building retrofits that favor sensor-based automation. Case studies in public institutions show energy savings above 20% after IoT lighting overhauls that rely on motion detection. Provincial disparity means turnkey packages that combine hardware and software succeed better than component sales, especially in tier-1 cities where budgets and technical skills align.[2]MDPI, “Digital Intelligence Transformation of Energy Conservation Management in China's Public Institutions,” mdpi.com

IoT-driven space utilization analytics upselling sensors

Vendors now position detectors as data endpoints that feed dashboards for real-time occupancy analytics. Schneider Electric’s SpaceLogic Touchscreen Room Controller couples sensor data with AI algorithms, cutting HVAC energy by up to 35% and maintenance costs by 25%. Hybrid work trends make granular seat-level data valuable for rightsizing corporate real estate portfolios, adding a revenue motivation that accelerates refresh cycles within the occupancy sensor market.

Healthcare bed-occupancy programs under CMS & MDR

The U.S. Acute Hospital Care at Home program, covering 328 hospitals and 23,000 discharges by April 2024, incentivizes remote patient monitoring with integrated bed-occupancy detection. European MDR alignment standardizes performance thresholds, lowering procurement risk for hospital administrators and opening a new vertical beyond lighting and HVAC automation.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| RF congestion & battery drain in 2.4 GHz mesh networks | -0.4% | Global | Short term (≤ 2 years) |

| False-positive events in high-heat data centers | -0.3% | Global | Medium term (2-4 years) |

| Fragmented wireless standards hindering EU retrofits | -0.2% | Europe | Medium term (2-4 years) |

| GDPR/CCPA compliance cost for AI people analytics | -0.3% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

RF congestion & battery drain in 2.4 GHz mesh networks

Zigbee networks carrying 192 nodes keep sub-200 ms latency under clean radio conditions, yet packet loss rises sharply when Wi-Fi channels overlap. Frequent retransmits shorten coin-cell lifespan, raising maintenance costs for battery-powered devices. Building owners therefore hesitate to shift critical loads to wireless unless spectrum planning tools are in place.

False-positive events in high-heat data centers

Equipment heat signatures mislead passive infrared detectors, causing unnecessary HVAC cycling in AI compute halls. mmWave radar offers higher precision but faces reflections from metallic racks, forcing multi-sensor fusion that lifts bill-of-materials costs. For operators focused on power usage effectiveness, these false positives dampen the business case.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Network Connectivity: Reliability Sustains Wired Dominance

The wired category accounted for 61.55% of global 2025 revenues, confirming its central role in core building systems within the occupancy sensor market. Facility managers value immunity to radio interference and easier power delivery, so Ethernet-based digital addressable networks anchor lighting and HVAC controls in new commercial construction. Retrofit environments with limited conduit space lean toward wireless nodes that reduce installation labor, which explains the 12.18% CAGR forecast for mesh-based products through 2031. Hybrid designs are emerging: a wired backbone feeds PoE luminaires while Thread or Zigbee sensors populate the periphery, balancing reliability and flexibility.

Wireless growth is driven by protocol convergence. Matter-over-Thread eliminates prior vendor lock-in, and vendors like Aqara released presence sensors that self-commission across Apple, Amazon, and Google ecosystems. Philips Hue demonstrated a software update that lets light bulbs double as motion sensors, hinting at an architecture where every luminaire becomes a data node. This blurs the lines between connectivity classes and broadens addressable installations for the

By Technology: Sensor Fusion Elevates Accuracy

Passive infrared achieved a 49.72% share in 2025, reinforcing its cost advantage inside the occupancy sensor market. Demand for higher fidelity propels dual-technology modules at a 13.12% CAGR, combining PIR with ultrasonic or mmWave radar to catch minor movements and stationary occupants. Texas Instruments’ AWRL6844 radar lowers per-node cost by USD 20, expanding adoption beyond premium installations.

AI-enabled edge processing reduces nuisance alarms by learning site-specific occupancy patterns. Bosch Sensortec targets 10 billion intelligent sensors by 2030, with 90% embedding AI engines that distill raw waveforms on-chip. These developments increase bill-of-material value and reinforce platform stickiness inside the occupancy sensor market.

By Mounting Type: Aesthetics and Coverage Shape Decisions

Ceiling installations held 44.55% share in 2025 because they deliver 360-degree coverage while blending with luminaires, a critical factor for specifiers focused on interior design. Ceiling nodes also simplify wiring by piggybacking on lighting circuits. Desk-level sensors are gaining traction at a 14.58% CAGR as companies seek seat-level occupancy analytics to manage hybrid work. Wall-mounted devices stay common in retrofits that lack plenum access, whereas in-fixture models grow through partnerships between lighting OEMs and sensor vendors.

Lutron’s embedded fixture platform removes control wiring, lowering copper use while enabling distributed wireless control that aligns with sustainability goals. Acuity Brands’ RESENSE Move ceiling sensor merges motion detection with Bluetooth beacons for workplace services, widening revenue opportunities beyond energy savings

By Installation Type: Retrofit Volume Meets New-Build Sophistication

Retrofit projects supplied 54.35% of 2025 revenues, reflecting the vast existing stock of inefficient buildings the occupancy sensor market must address. However, these projects contend with asbestos ceilings, mixed voltage, and outdated BMS protocols, often limiting sensor density. New construction is set to grow 12.93% CAGR thanks to codes that mandate smart controls during design phases. Builders pre-wire PoE networks, allowing higher sensor counts that feed digital twins and AI analytics from day one.

California’s Title 24 treats sensors as baseline features, integrating them into spec schedules rather than change orders. European developers also embed sensors early to claim green building certifications, reducing lifecycle cost and boosting the occupancy sensor market size for new projects.

By Building Type: Commercial Core, Residential Upswing

Commercial properties generated 59.25% of 2025 demand. Office owners pursue net-zero targets and employee wellness, justifying upgrades to AI-driven sensing suites. Warehouses adopt mmWave arrays for safety interlocks and forklift navigation. The residential segment, while smaller, is climbing at a 12.55% CAGR as smart speakers normalize connected-home expectations. Healthcare facilities add a new pull, driven by CMS reimbursements for remote monitoring.

Mixed-use towers now combine hotel, retail, and apartments, requiring scalable platforms that tailor sensing logic per zone. Vendors that supply API-centric solutions can therefore capture multiple verticals with a single SKU, enlarging their total addressable occupancy sensor market.

By Application: Lighting Control Cedes Growth to HVAC Intelligence

Lighting control still commanded 45.40% of 2025 revenue because payback remains visible and near-term. HVAC and ventilation, however, grow at 13.88% CAGR because CO₂-aware occupancies unlock deeper energy savings. Cisco and Schneider Electric co-created a system that ingests live occupancy counts to trim air-handling loads, showing 35% energy reduction in pilot sites.

People-count analytics now sit atop raw detection data to inform cleaning schedules and lease planning. Security integration is also expanding as access control firms ingest occupancy streams to refine threat detection. The application hierarchy is shifting from single-purpose motion triggers to multiservice data layers, a trend that keeps expanding the occupancy sensor market.

Geography Analysis

North America held the largest revenue share in 2025. The United States anchors demand with Title 24 and the 2021 IECC requiring automated shut-off across commercial spaces. Canada follows similar patterns and shows strong interest in occupancy-based heating due to long heating seasons. Ongoing retrofits contend with dense 2.4 GHz spectrum in urban cores, driving hybrid deployments that mix wired backbones and sub-GHz wireless.

Europe registers solid growth under the Renovation Wave program that targets 35 million buildings by 2030. Germany, the United Kingdom, and France institute national building codes that embed occupancy-triggered lighting and ventilation cut-offs. GDPR compliance adds cost and slows AI analytics roll-outs, yet platform vendors that offer on-premise data processing mitigate these barriers. Fragmented wireless protocols force integrators to rely on multiprotocol gateways, elevating system complexity but also boosting services revenue inside the occupancy sensor market.

Asia-Pacific records the fastest CAGR to 2031. China’s dual-carbon policy accelerates smart building mandates, especially in tier-1 metros where public-sector projects showcase 20% energy reduction after sensor installations. Japan and South Korea emphasize premium solutions that pair mmWave with AI for comfort optimization. In India and Southeast Asia, cost-efficient PIR nodes dominate, yet commercial office parks in Bengaluru and Singapore adopt platform architectures that align with global corporate ESG goals. This heterogeneity offers multi-tiered entry points for vendors across the occupancy sensor market.

Regulatory Landscape

Building energy codes and standards increasingly require occupancy-based controls as part of compliance programs across major regions, shifting the category from discretionary energy savings to mandated functionality. In the United States, the California Energy Commission 2025 Building Energy Efficiency Standards took effect on January 1, 2026 and incorporate occupant sensing controls for functions such as shut-off. ANSI/ASHRAE/IES Standard 90.1-2025 also tightens requirements for enclosed spaces (including private offices, storage rooms, and restrooms) and adds more granular control expectations in larger offices. At the federal level, U.S. DOE building energy code determinations continue to affect state adoption cycles that shape retrofit and new-build specifications.

In Europe, the EU Recast Energy Performance of Buildings Directive (EU) 2024/1275 elevates building automation and indoor environmental quality monitoring, with provisions requiring integrated technical building systems capabilities in non-residential buildings by May 29, 2026. Technical standards are also refining interoperability and functional definitions, including IEC 62386-303 (DALI), which specifies occupancy sensor requirements for lighting control data exchange (including the April 2024 AMD update), plus ISO 16484-2:2025 and ISO 16484-4:2025, which define BACS hardware requirements and functional blocks for occupancy-related control applications across heating, cooling, and lighting.

Value Chain Analysis

The value chain runs from sensing components (PIR elements, ultrasonic transducers, microwave/mmWave radios, and microcontrollers) to module design and firmware, then assembly and certification, and finally system integration into lighting controls and building management platforms. Interoperability and form-factor standards influence upstream design decisions, including IEC 62386-303 for DALI-connected lighting controls, the Bluetooth Mesh Occupancy Sensor NLC Profile 1.0.1 (2024) for networked lighting controls, and Zhaga Book 20 for luminaire-sensor mechanical and electrical interfaces. As a result, reference designs, certification testing, and gateway or multiprotocol integration work performed by OEMs and controls specialists carry more weight.

Downstream, channels split between direct enterprise and project-based sales for large facility portfolios, and indirect distribution through electrical and electronics distributors (for example, Wesco International and Arrow Electronics) serving contractors and integrators. Supply-chain strategy has also been shaped by trade frictions, including 2025 tariff adjustments affecting semiconductor-related inputs, which is pushing redesign toward modular BOMs and more regionalized sourcing and assembly. Product roadmaps further shift value toward edge-compute and platform-ready nodes, reflected in enterprise-grade announcements such as PointGrab's battery-powered CogniPoint 2 Flex using Thread networking and edge AI for building automation deployments.

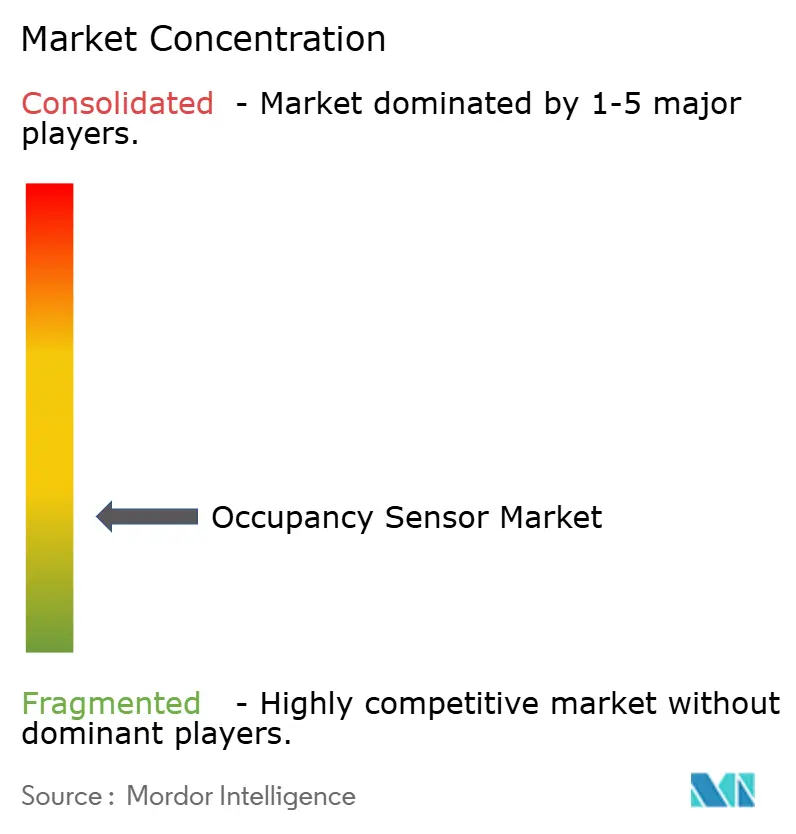

Competitive Landscape

Competition remains moderate. Signify leverages its Interact platform, bundling sensor-equipped luminaires for plug-and-play retrofits. Schneider Electric’s portfolio integrates SpaceLogic controllers with EcoStruxure software, offering end-to-end coverage from sensor to cloud. Honeywell excels in large-campus deployments by combining security, HVAC, and lighting under the Honeywell Forge analytics layer. Johnson Controls capitalizes on a USD 12.6 billion backlog, integrating sensors with the OpenBlue digital twin to offer predictive maintenance and visitor analytics.

Emerging players target specialized use cases. Origin Wireless AI uses Wi-Fi signal perturbations to deliver 99.9% detection accuracy without dedicated hardware, lowering BOM cost. Butlr Technologies employs thermal-pixel sensors for anonymous people tracking and secured funding via Ricoh to scale its workplace analytics service. Semiconductor suppliers such as Infineon and NXP push reference designs that accelerate time-to-market for OEMs, tightening timeframes for competitive differentiation.

Strategic themes center on AI, cybersecurity, and open APIs. Vendors that can combine heterogeneous sensor data streams, secure them under SOC 2 frameworks, and expose analytics via RESTful services are winning multi-year master service agreements. The occupancy sensor market therefore rewards platform depth and ecosystem partnerships rather than standalone hardware price wars.

Occupancy Sensor Industry Leaders

Signify (Philips Lighting)

Honeywell International

Schneider Electric

Johnson Controls

Acuity Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory enforcement and standardization are expanding the white space for compliance-driven upgrades that require more granular, interoperable sensing for both lighting and HVAC. The EU EPBD Recast (EU) 2024/1275 reached full application on May 29, 2026, pushing non-residential buildings toward integrated building automation and indoor environmental quality monitoring, which increases the role of occupancy data in controls logic rather than treating occupancy as a standalone trigger. On interoperability, tighter alignment around DALI (IEC 62386-303), ISO 16484-2/16484-4 for BACS, and networked lighting profiles (Bluetooth Mesh NLC occupancy profile) supports multi-vendor deployments and services-led integration work in retrofits.

Technology evolution also creates opportunities in privacy-first people sensing and higher-fidelity presence detection that can reduce false positives while enabling space-utilization analytics. In 2026, XY Sense launched Area Pro with wide-area coverage and wired PoE connectivity aimed at permanent commercial installations, while PointGrab introduced CogniPoint 2 Flex as an enterprise Thread-based, battery-powered edge AI occupancy sensor. Semiconductor and component advances broaden design options for OEMs, including Infineon’s AIROC UWB TSL100 (June 2026) for high-precision presence detection and secure access control, and Panasonic Industry’s PaPIRs+ motion sensor technology (July 2026) with redesigned pyroelectric elements intended to raise thermal sensitivity for building automation and HVAC optimization. Together, these moves support solution positioning around multi-modal sensing (PIR, mmWave/UWB, and environmental data) and on-device analytics that fit stricter privacy and data-handling requirements in commercial buildings.

Recent Industry Developments

- March 2026: XY Sense launched Area Pro, an occupancy sensor positioned for wide-area commercial coverage with on-device AI and wired PoE connectivity. The product targets permanent installations where power and networking reliability are prioritized over battery life. It also reinforces the shift toward infrastructure-grade sensing nodes that feed workplace analytics and building automation workflows.

- February 2026: PointGrab introduced CogniPoint 2 Flex, a battery-powered occupancy sensor combining edge AI with Thread networking for enterprise building automation. Thread support aligns the sensor layer with emerging IP-based building networks and can reduce integration friction across multi-vendor environments. The announcement highlights growing emphasis on edge processing to extract actionable occupancy data without relying solely on cloud compute.

- November 2025: Signify released a new mains-powered motion and daylight DALI sensor designed to work within the Signify Interact connected lighting platform. Pairing occupancy and daylight inputs supports tighter closed-loop control for site managers and integrators deploying DALI-based upgrades. The launch strengthens platform-based differentiation by bundling sensors, controls, and software under a unified connected-lighting offer.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The occupancy sensor market covers revenue from sensors and related control units that detect presence or movement, then trigger actions such as switching lights, adjusting HVAC, or enabling security functions in commercial and residential buildings.

Scope exclusions: We exclude broader building automation software platforms and non-occupancy sensing devices that do not measure presence for control purposes.

Segmentation Overview

- By Network Connectivity

- Wired

- Wireless

- Wi-Fi

- Zigbee

- Z-Wave

- By Technology

- Passive Infrared (PIR)

- Ultrasonic

- Microwave

- Dual / Multi-Technology (PIR + mmWave, etc.)

- mmWave / FMCW Radar

- By Mounting Type

- Ceiling-Mounted

- Wall-Mounted

- Desk / Furniture-Integrated

- In-Fixture / Embedded Luminaire

- By Installation Type

- Retrofit

- New Construction

- By Building Type

- Residential

- Commercial

- Industrial and Warehousing

- Healthcare and Assisted Living

- Government and Education

- By Application

- Lighting Control

- HVAC and Ventilation

- Security and Surveillance

- People Counting and Space Utilization

- Bed / Restroom Occupancy Monitoring

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Nordics (Sweden, Norway, Denmark, Finland)

- Rest of Europe

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by anchoring demand indicators for buildings and energy use, since occupancy sensors are mostly installed to reduce wasted lighting and HVAC loads. We used public references such as US DOE and ENERGY STAR materials, IEA building energy statistics, US Census construction data, Eurostat construction indicators, and standards and code references published by bodies such as ASHRAE and the ICC.

Next, we checked product and pricing signals using company filings and investor presentations, product catalogs and spec sheets, customs and trade statistics where relevant, and reputable press coverage on smart building rollouts. In a few places, we also relied on paid subscriptions for company financials and news screening, and on patent databases to understand where sensing technology is moving and which commercial claims are being prioritized. These desk sources are illustrative only, and many other public and paid references were used to collect, validate, and clarify the final assumptions.

Primary Interviews and Surveys

Primary work focused on validating what is actually being bought and installed, and how budgets move across retrofit versus new construction and across building types. We spoke with a mix of manufacturers, distributors, system integrators, and building owners or facility teams across the Americas, EMEA, and APAC so pricing ranges, adoption rates, and replacement cycles could be cross-checked against the desk signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 42% |

| Mid tier: 52% | Functional/Unit leaders: 35% | EMEA: 34% |

| Smaller Players: 17% | Managers: 51% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool that reconstructs how many sensors get pulled into buildings each year based on construction additions and retrofit intensity, then translated into value using typical device counts and average selling price bands. To keep totals realistic, we corroborated the top-down estimates with selective bottom-up approximations, including sample vendor revenue coverage checks, channel mix sanity checks, and a sampled ASP multiplied by implied unit volumes for key use cases.

A few practical inputs we used include non-residential and residential construction activity, retrofit share by building type, average sensors per 1,000 square feet for common layouts, the split of PIR versus ultrasonic or microwave in typical projects, and wired versus wireless attach rates where cabling constraints matter. For forecasting, we ran scenario analysis so the base case could reflect likely code and energy-efficiency pull, while alternative cases test slower retrofit cycles or faster wireless adoption. Where a bottom-up signal was missing for smaller geographies, we filled the gap through proxy ratios tied to building stock and construction spend, then adjusted based on interview input.

Data Validation & Update Cycle

Outputs were triangulated against independent signals such as building energy-efficiency program activity, construction trends, and observed pricing bands, then checked for abrupt jumps that would not match installation cycles. When variances appeared, we revisited assumptions and used follow-up calls to confirm whether the change was driven by scope, pricing, or timing.

Before sign-off, the model and narrative go through multi-step analyst reviews so definitions, math, and cross-segment totals stay consistent. The study is refreshed annually, and interim updates are made when material events occur, such as major code changes or large shifts in construction activity, followed by a final pass right before delivery so clients receive the latest view.

Mordor Intelligence's Occupancy Sensor Market Size Versus Other Published Estimates

Published market sizes for occupancy sensors often do not match because analysts use different cutoffs on what counts as an occupancy sensor sale and when it is recognized, then apply different pricing and adoption assumptions. Differences also show up when one estimate relies more on shipment growth while another leans on building automation spending trends.

The main gap drivers in this market are usually scope and timing, such as whether controls and sensor-integrated luminaires are included, how retrofit penetration is treated versus new construction, and how ASPs are moved over time when wireless adoption rises. The table highlights this spread, where sensor-only revenue tied to lighting, HVAC, and security demand pools is separated from adjacent automation spend, reflecting a scope choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.26 B (2026) | |

| Global Consultancy A | USD 2.53 B (2023) | Uses an earlier base year and a faster growth window, and the headline value appears tied to a revenue-plus-volume framing that can undercount later-year pricing uplift and higher-value commercial retrofits. |

| Industry Publisher B | USD 2.75 B (2025) | Likely applies a broader growth case across smart building demand and may blend adjacent automation and control spend, which can inflate totals when sensor-only revenue is separated by application. |

Taken together, the differences mainly come from how tightly the product scope is defined and how adoption and ASP progression are moved through the forecast years. By keeping inputs traceable to construction activity, retrofit intensity, and application-level sensor counts, the final number stays explainable and repeatable even when assumptions are updated.

Key Questions Answered in the Report

What is the current size of the occupancy sensor market?

The Occupancy Sensor Market stood at USD 3.26 billion in 2026 and is forecast to reach USD 4.16 billion by 2031 at a 5.04% CAGR.

Which connectivity segment leads the occupancy sensor market?

Wired solutions lead with 61.55% share in 2025 thanks to their reliability, although wireless nodes are growing at a 12.18% CAGR.

What application area is growing fastest?

HVAC and ventilation control shows the highest growth at a 13.88% CAGR as building owners widen focus from lighting to full environmental optimization.

Why is healthcare an emerging opportunity?

CMS and MDR regulations reward hospitals that deploy bed-occupancy monitoring, expanding sensor adoption beyond traditional lighting and HVAC uses.

Which regions will drive future demand?

Asia-Pacific exhibits the fastest CAGR to 2031 due to China’s dual-carbon targets and rapid urbanization, while Europe and North America maintain strong baseline demand through regulatory mandates.

How fragmented is the competitive landscape?

The top five players hold about 29.45% share in 2025, indicating moderate consolidation yet persistent entry opportunities for AI-driven startups.

Page last updated on: