Medical Writing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.33 Billion |

| Market Size (2031) | USD 6.97 Billion |

| Growth Rate (2026 - 2031) | 9.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

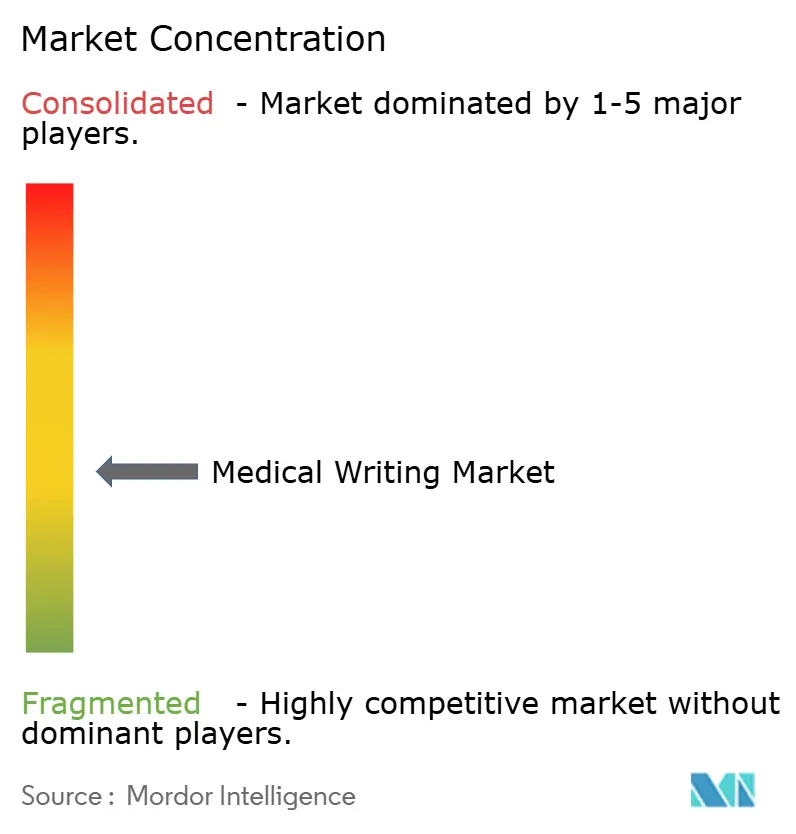

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Medical Writing Market Analysis by Mordor Intelligence

The medical writing market size is expected to grow from USD 3.94 billion in 2025 to USD 4.33 billion in 2026 and is forecast to reach USD 6.97 billion by 2031 at 9.98% CAGR over 2026-2031. Rapid guidance updates, the rise of advanced biologics, and a surge in decentralized trials are all intensifying documentation workloads, prompting sponsors to pursue specialized partners with proven regulatory fluency [1]U.S. Food and Drug Administration, “New Drug Therapy Approvals 2024,” fda.gov . Consolidation among contract research organizations (CROs) is reshaping competitive dynamics as integrated platforms offer end-to-end support that keeps pace with compressed development timelines. Asia-Pacific’s double-digit growth underscores an industry pivot toward multilingual protocol development and region-specific submission templates, even as North America retains the deepest pool of experienced writers. The talent shortage remains a critical bottleneck that fuels wage inflation and stimulates adoption of generative AI solutions that still require expert oversight for compliance assurance.

Key Report Takeaways

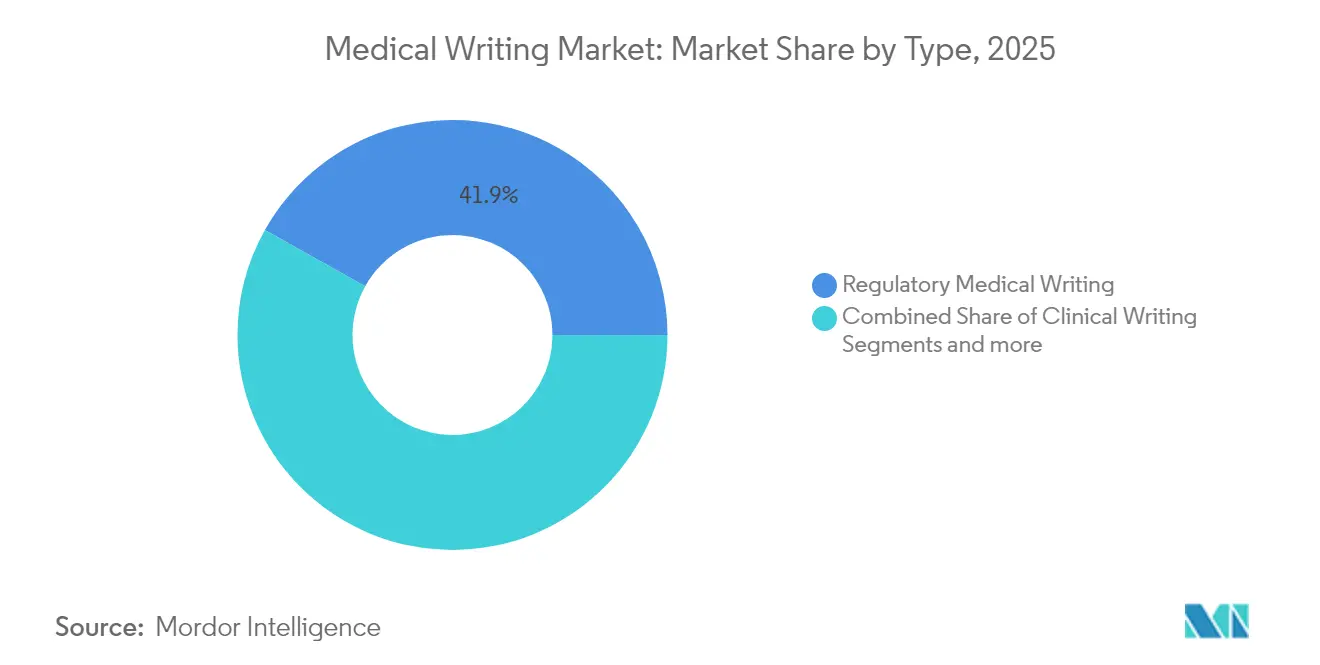

- By type, Regulatory Medical Writing captured 41.88% of the medical writing market share in 2025; Scientific and HEOR Writing is forecast to advance at a 10.74% CAGR through 2031.

- By end user, Pharmaceutical Companies accounted for 49.20% of the medical writing market size in 2025; Biotechnology Companies are projected to grow at a 10.6% CAGR to 2031.

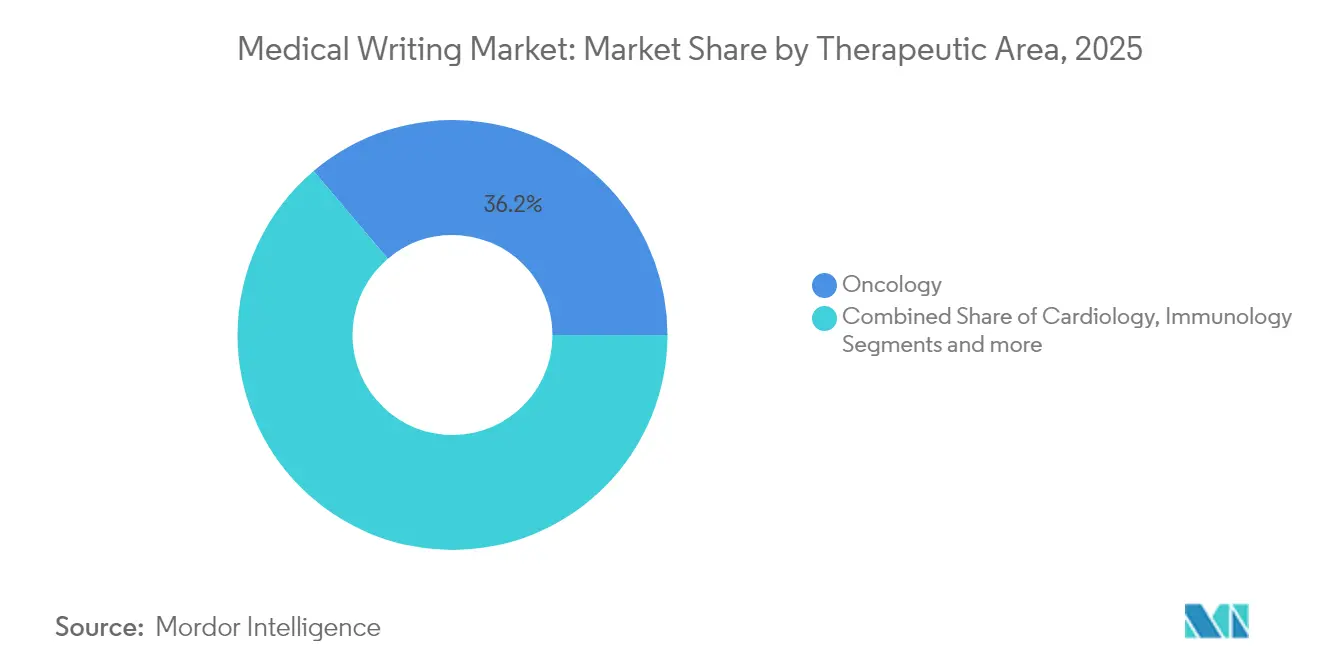

- By therapeutic area, Oncology held 36.18% revenue share in 2025; Immunology is set to post an 10.77% CAGR through 2031.

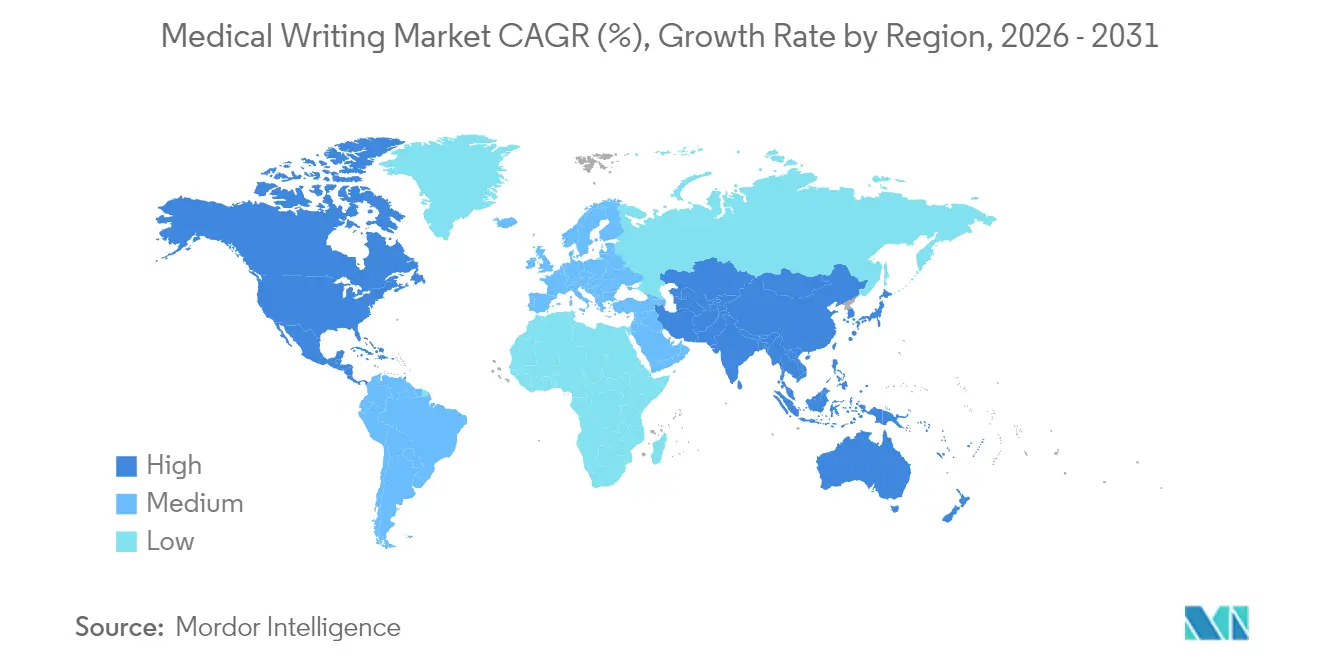

- By region, North America commanded 39.75% of the medical writing market size in 2025; Asia-Pacific is expected to rise at an 10.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Writing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing R&D expenditure and development of new therapeutics | +2.1% | Global, focus on North America & EU | Long term (≥ 4 years) |

| Expansion of CRO outsourcing models | +1.8% | Global, faster uptake in APAC | Medium term (2-4 years) |

| Increasing regulatory complexity & documentation volume | +2.3% | Global, highest in North America & EU | Short term (≤ 2 years) |

| Rising adoption of biologics & personalized medicine | +1.9% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| AI-enabled content automation requiring expert oversight | +1.4% | Global, early use in North America | Short term (≤ 2 years) |

| Decentralized/virtual trials driving adaptive multilingual protocols | +0.7% | Global, emphasis on APAC & emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing R&D Expenditure and Development of New Therapeutics

Global life-sciences revenue climbed to about USD 1.9 trillion in 2024, with pharmaceuticals representing nearly 70% of sales, which translates into larger study pipelines that require meticulous documentation. The FDA cleared 50 new drugs in 2024 and anticipates up to 70 approvals in 2025, a trend that compresses writing timelines while widening the scope of submission dossiers. Advanced modalities such as cell and gene therapies demand more extensive chemistry, manufacturing, and controls (CMC) sections and robust risk-benefit narratives. Heightened investment also extends to post-approval evidence programs, expanding the lifespan of writing assignments well beyond initial licensure. These factors collectively add momentum to the medical writing market as sponsors vie to optimize approval cycles amid rising development costs [2]Abraham Viju Ipe, "The Orphan Drug Act and rare cancers: a retrospective analysis of oncologic orphan drug designations and associated approvals from 1983-2022," Expert Opinion on Orphan Drugs, tandfonline.com.

Expansion of CRO Outsourcing Models

The worldwide CRO sector reached roughly USD 82 billion in 2024, driven by sponsors that favor functional service provider arrangements to balance cost efficiency with operational control. Large deals, including Indegene’s acquisition of Trilogy Writing & Consulting in March 2024, illustrate how platforms are enhancing integrated capabilities to attract global programs that require cohesive documentation support. Outsourcing penetration is advancing fastest in Asia-Pacific where evolving regulatory systems and cost advantages spur adoption of external partners. Sponsors that deploy flexible FSP contracts can scale writer pools in line with pipeline fluctuations, improving budget predictability. As more trials incorporate decentralized components, CROs that bundle regulatory, clinical, and writing services hold a strategic edge, boosting the medical writing market.

Increasing Regulatory Complexity & Documentation Volume

In 2024, the FDA issued more than 25 new guidance documents spanning electronic submissions, AI-enabled devices, and decentralized trial oversight, pushing overall writing workloads upward by an estimated 25-30% [3]U.S. Food and Drug Administration, "Artificial Intelligence-Enabled Device Software Functions: Lifecycle Management and Marketing Submission Recommendations," fda.gov. The transition to eCTD v4.0 and enhanced Module 1 requirements heighten demands for cross-regional harmonization. China’s 24-point reform roadmap, slated for full adoption by 2027, compels sponsors to update templates and create Chinese-language dossiers that incorporate new transparency standards. Europe’s Clinical Trial Information System similarly introduces step-changes in data granularity and public disclosure obligations. Together, these updates intensify reliance on specialist writers who can bridge differing jurisdictional expectations, a dynamic that propels the medical writing market in the near term.

Rising Adoption of Biologics & Personalized Medicine

The Center for Biologics Evaluation and Research expanded guidance for gene and cell therapies in 2025, outlining data expectations that surpass traditional small-molecule norms. Personalized medicine pipelines require adaptive trial protocols that stratify participants by biomarker and integrate real-world evidence, driving greater page counts and iterative updates. Biosimilar developers must generate head-to-head comparability narratives that address interchangeability and manufacturing changes, creating recurring documentation needs over the product life cycle. Expedited pathways such as the Regenerative Medicine Advanced Therapy designation compress review windows, obligating writers to deliver comprehensive dossiers on accelerated schedules. These trends underpin sustained growth for the medical writing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled medical-writing professionals | -1.6% | Global, acute in APAC & emerging markets | Short term (≤ 2 years) |

| Pricing pressure from procurement consolidation | -0.9% | Global, highest in North America & EU | Medium term (2-4 years) |

| Regulatory scrutiny on ghost-writing & author transparency | -0.8% | Global, with strong oversight in North America & EU | Medium term (2-4 years) |

| High compliance cost for region-specific submission templates | -0.7% | Global, highest burden in APAC & emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Medical-Writing Professionals

Eighty-three percent of life-sciences companies reported difficulty filling medical writing roles in 2024, and forecasts predict a 35% talent deficit by 2030. Wage inflation and project delays are common as sponsors compete for senior writers who can manage complex products. Academic pipelines lag market needs despite new certificate programs launched by institutions such as the University of Chicago in 2024 aimed at upskilling scientists for regulatory writing careers. Asia-Pacific faces sharper deficits because rapid biopharma expansion outpaces local training capacity, leading to higher expatriate costs or longer timelines. The squeeze on talent slows project throughput and tempers growth in the medical writing market.

Pricing Pressure from Procurement Consolidation

Large pharmaceutical companies are centralizing vendor management to extract volume discounts, compressing margins for specialized writing boutiques. Standardized rate cards and longer procurement cycles tilt negotiations toward integrated CROs capable of bundling services, reducing smaller firms’ bargaining power. Inflationary operating costs intensify margin pressure, compelling providers to automate routine tasks and focus on high-value, niche deliverables. Competitive bidding for generic documents drives commoditization; however, premium pricing persists for advanced therapeutic dossiers that require deep subject-matter expertise. This dichotomy constrains overall revenue uplift within the medical writing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Regulatory Expertise Commands Premium Positioning

Regulatory Medical Writing led the segment with 41.88% of the medical writing market share in 2025, underscoring the premium placed on compliance-centric deliverables amid proliferating guidance documents. Scientific and HEOR Writing is projected to record the fastest 10.74% CAGR to 2031 as payers request real-world evidence and health-economic justifications alongside regulatory submissions.

Growth in the medical writing market is further buoyed by steady demand for Clinical Writing, which supports decentralized protocols that must satisfy regional language and privacy statutes. Emerging categories now include AI-assisted authoring support for digital health technologies, signalling how providers diversify portfolios to address evolving client needs. Regulatory specialists command higher billing rates, but cross-training into HEOR and digital modalities widens revenue streams and mitigates project-pipeline volatility.

By End User: Biotech Innovation Drives Outsourcing Acceleration

Pharmaceutical Companies controlled 49.20% of the medical writing market size in 2025, sustained by large pipelines that require continuous global dossier updates. Biotechnology Companies, however, are forecast to expand at a 10.6% CAGR through 2031 as lean organizations opt to outsource nearly all documentation tasks to stay focused on core R&D activities.

Biotech sponsors developing cell and gene therapies outsource advanced CMC sections and risk-benefit analyses that exceed their internal capacity, fueling overall medical writing market growth. CROs and specialist firms position themselves as long-term partners by embedding writers within sponsor teams, improving knowledge retention and operational agility. Medical Device Manufacturers and Academic Institutes represent supplementary demand pools that stabilize revenue during small-molecule funding cycles.

By Therapeutic Area: Oncology Leadership Faces Immunology Challenge

Oncology retained the largest segment at 36.18% of 2025 revenues, supported by the FDA’s streamlined tissue-agnostic approval pathways and a record number of Phase II/III oncology trials requiring elaborate endpoint narratives. Immunology is anticipated to grow at an 10.77% CAGR as gene-edited therapies and autoimmune biologics amplify dossier complexity.

The medical writing market benefits from rising documentation needs in CNS and Rare Disease portfolios, which frequently involve adaptive designs and surrogate endpoints. Therapeutic diversification prompts writers to cultivate multi-disciplinary expertise that integrates biomarker strategy, patient-reported outcomes, and regulatory science. Providers with oncology pedigree are leveraging cross-training initiatives to capture broader therapeutic contracts and sustain topline expansion.

Geography Analysis

North America generated 39.75% of 2025 revenue, anchored by the United States, which issued over 25 new guidance documents in 2024 that expanded dossier length and demanded rapid compliance updates. Canada and Mexico participate through harmonized initiatives that streamline submissions but still rely on U.S. precedents, which reinforces the region’s leadership in the medical writing market.

Asia-Pacific is set to record an 10.82% CAGR, reflecting China’s multi-year overhaul that adds 24 reform measures and mandates localized templates by 2027. Japan’s preference for indigenous clinical data and India’s fast-tracking rules both create sustained demand for specialized writers who can reconcile global sections with country-specific standards. Australia’s 2025 rolling submission pathway for priority medicines further drives engagement with experienced providers.

Europe remains pivotal as the EMA’s Clinical Trial Information System obliges sponsors to submit harmonized dossiers that meet new public transparency thresholds. Germany, France, and the United Kingdom require meticulous adaptation of global sections to local labelling statutes, extending writing cycles. Latin America and the Middle East & Africa show steady adoption of ICH guidelines, signalling future growth nodes that providers are targeting through regional hubs.

Regulatory Landscape

Regulatory requirements for clinical and regulatory documentation continue to tighten across major agencies, increasing both the volume and specificity of submission-ready writing. In the United States, the US Food and Drug Administration (FDA) advanced device-facing documentation expectations with its final guidance on the Content of Human Factors Information in Medical Device Marketing Submissions, published in the Federal Register in May 2026, and also issued a draft guidance in January 2026 on the Use of Bayesian Methodology in Clinical Trials of Drugs and Biologics. Together, these developments add specialized statistical and usability evidence narratives to authoring workflows.

In Europe, the European Medicines Agency (EMA) continues to align submission formats and lifecycle change management through the harmonised eCTD guidance (version 6.0 effective March 2025) and the revised variations framework (applicable from January 2026). On global trial conduct standards, ICH E6(R3) is reshaping clinical documentation toward a more risk-proportionate, technology-aware approach, with the Principles and Annex 1 effective from July 2025 and Annex 2 reaching Step 4 on June 3, 2026, followed by CHMP adoption on June 25, 2026. These changes raise the bar for compliant authoring, document governance, and cross-region harmonization in medical writing engagements.

Competitive Landscape

The medical writing market shows moderate fragmentation with a mix of global CROs and niche consultancies competing for share. Leaders such as IQVIA, ICON, and Parexel leverage integrated platforms that blend clinical operations, regulatory strategy, and writing expertise, capturing large multiregional programs. Specialist firms like Trilogy Writing & Consulting, now part of Indegene after a March 2024 acquisition, focus on deep therapeutic knowledge and agile delivery models that resonate with mid-cap sponsors.

Technology remains a pivotal differentiator as providers deploy controlled generative AI engines to accelerate drafting and version control while retaining human oversight for scientific integrity. Indegene’s post-acquisition rollout of a proprietary AI-assisted platform promises cycle-time reductions of up to 25% without compromising regulatory compliance. Strategic partnerships with eCTD vendors and translation houses create one-stop solutions that appeal to sponsors pursuing global filings under tight timelines.

Talent curation is a critical competitive lever because scarcity of senior writers affects delivery capacity. Firms invest in global training academies and mentorship programs to cultivate regulatory fluency and therapeutic depth, an approach showcased by ICON’s 2025 writer residency initiative. Providers that can secure skilled teams while maintaining cost competitiveness are poised to grow share within the medical writing market.

Medical Writing Industry Leaders

-

Paraxel International

-

IQVIA Inc

-

Laboratory Corporation of America Holdings

-

Icon Plc

-

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are expanding where sponsors and CROs need scalable, audit-ready authoring that keeps pace with evolving submission standards and multi-region requirements. The shift toward updated electronic submission standards creates specific whitespace for providers that can operationalize XML-based, region-specific delivery at scale, including Japan where PMDA mandated eCTD version 4.0 as of April 2026. Providers that can bundle regulatory writing with submission operations, lifecycle maintenance, and transparency-ready versions of documents are positioned to support larger, longer-duration programs as EMA and FDA guidance updates increase rewrite and update cycles.

Consolidation and AI-enabled workflows are also opening space for differentiated offerings in regulatory and clinical documentation production. In April 2026, Veristat announced an agreement to acquire Certara's Regulatory and Medical Writing business (up to USD 135 million), adding a pool of regulatory and medical writing specialists and signaling demand for integrated platforms that combine writing with broader development services. In June 2026, TrialAssure and Cancer Research UK entered a collaboration to evaluate AI-supported authoring (with a structured human-in-the-loop process), reinforcing near-term commercial interest in governed generative AI that accelerates drafting while keeping expert accountability for compliance and quality.

Recent Industry Developments

- May 2026: Parexel launched ParexelAI, a suite of human-led AI services designed to accelerate clinical development deliverables, including faster clinical study report preparation for medical writing teams. The launch formalizes AI-enabled authoring as a commercial service layer within a large CRO, increasing competitive pressure on providers to pair automation with documented quality controls.

- April 2026: Veristat announced its agreement to acquire Certara's Regulatory and Medical Writing business for up to USD 135 million, adding more than 200 regulatory and medical writing experts and associated capabilities. The acquisition strengthens Veristat's end-to-end submission support and highlights ongoing consolidation around integrated regulatory, clinical, and writing platforms.

- March 2024: Indegene completed the acquisition of Trilogy Writing & Consulting GmbH, bringing longstanding regulatory writing expertise into its broader life sciences services footprint. The transaction expanded Indegene's ability to support global market authorization documentation while combining specialist writing capacity with its technology-enabled delivery model.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers outsourced and in-house medical writing services used to create clinical, regulatory, and scientific documents that support drug, biologic, and device development, as well as publication and medical communications work. Revenues are captured for service delivery across major regions.

Scope exclusions: Pure translation, general advertising copy, and routine administrative documentation that is not tied to scientific or regulatory evidence packages are excluded.

Segmentation Overview

-

By Type

- Regulatory Medical Writing

- Clinical Writing

- Scientific and HEOR Writing

- Others

-

By End User

- Pharmaceutical Companies

- Biotechnology Companies

- Contract Research Organizations

- Medical Device Manufacturers

- Academic & Research Institutes

- thers

-

By Therapeutic Area

- Oncology

- Cardiology

- CNS & Neurology

- Immunology

- Rare Diseases

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what counts as medical writing revenue and to understand the demand pool that creates recurring documentation work. We referenced public clinical trial registries such as ClinicalTrials.gov and the WHO ICTRP to track trial starts and study complexity signals that usually lift writing hours. Regulatory agency portals and guidance libraries, such as the US FDA and the EMA, were also reviewed to understand submission pathways and documentation templates that shape service mix.

To support regional demand shaping, we relied on sources such as OECD health statistics and World Bank indicators for R&D intensity, along with association and journal materials that discuss publication practices and authoring standards. Company filings, investor presentations, and reputable press were used to map outsourcing behavior and typical engagement models. A paid subscription for company financials and another for news and deals was used only to cross-check revenue direction and major contract wins. These examples are illustrative, and many other public and paid references were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on confirming which documentation services are purchased, how pricing is structured, and how volumes move with clinical development activity. We spoke with service providers, pharma and biotech outsourcing managers, and documentation-focused leaders across APAC, EMEA, and the Americas to fill gaps from public data and to pressure-test assumptions used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | APAC: 38% |

| Mid tier: 51% | Functional/Unit leaders: 25% | EMEA: 36% |

| Smaller Players: 17% | Managers: 59% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts from a top-down build that reconstructs the demand pool from clinical development and submission activity, then converts it into service revenues using realistic utilization and pricing logic. In practice, we linked writing demand to indicators such as trial initiations by phase, protocol amendment frequency, expected numbers of CSR and regulatory document sets, publication output levels, and the outsourcing share by sponsor type. For adjacent work, the model also considers the mix shift between regulatory writing, clinical writing, and scientific and publication support, because each area follows a different cadence and price pattern.

After the first pass, results are corroborated with selective bottom-up approximations, including sampled price ranges for key document types, provider revenue direction checks, and channel feedback on utilization and turnaround times. Where bottom-up signals are incomplete, such as in smaller geographies or niche therapeutic programs, we filled gaps using conservative peer-region ratios, then rechecked the implied spend per active trial and per submission package. Forecasting is driven mainly through scenario analysis. The baseline outlook is anchored to expected trial activity, R&D budgets, and guidance-driven documentation intensity, and then adjusted using expert feedback on outsourcing and pricing progression.

Data Validation & Update Cycle

Validation is done through repeated checks that compare model outputs against independent signals, including trial volume trends, regulatory submission activity cues, and observed outsourcing behavior discussed in interviews. Outliers are flagged when growth, regional shares, or implied spend per program move outside reasonable ranges, and then assumptions are revisited before sign-off.

Reports are refreshed annually, and interim updates are made when material events occur, such as major guidance changes, noticeable shifts in trial geography, or large outsourcing announcements. Before delivery, an analyst performs a final pass using the latest available public updates so clients receive a current view rather than an older snapshot.

Mordor Intelligence's Medical Writing Market Size Compared With Other Published Estimates

Published market values for medical writing can differ because each source decides its own scope for services, how it treats in-house versus outsourced work, and what it assumes for pricing across regions and document types. Even when the topic label is the same, the counted activities and the year used for currency conversion can shift the total.

Clinical trial registry volumes, regulatory guidance updates, and the implied spend per active development program are the evidence checks that tie Mordor Intelligence's 2025 estimate to a defined documentation workload rather than a broad communications spend bucket. Differences usually come from whether promotional medical communications are blended into the total, how CRO pass-through is treated, and whether aggressive price uplift is assumed for specialized writing areas without a fresh validation cycle.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.94 B (2025) | |

| Global Consultancy A | USD 5.07 B (2025) | Uses a broader service boundary that can include wider medical communications and marketing-related writing, and it may treat outsourced spend and pass-through values less distinctly, which increases the total. |

| Industry Publisher B | USD 4.95 B (2025) | Applies a more expansionary pricing and growth path into the model and tends to rely on a higher assumed outsourcing intensity across sponsors, with fewer transparent cross-checks against implied spend per program. |

Across the three figures, the spread is mainly explained by what is counted as medical writing work and how prices and outsourcing shares are moved year to year. By keeping the demand pool tied to document production drivers and rechecking implied spend against multiple external signals, the estimate stays easier to trace and repeat when new evidence arrives.

Key Questions Answered in the Report

What is the current medical writing market size?

The medical writing market size reached USD 4.33 billion in 2026 and is projected to hit USD 6.97 billion by 2031.

Which segment is growing fastest within the medical writing market?

Scientific and HEOR Writing is expected to post the highest 10.74% CAGR from 2026 to 2031 as sponsors seek real-world evidence and payer-focused analyses.

Why is Asia-Pacific the fastest-growing region for medical writing services?

China’s regulatory reforms and wider adoption of decentralized trials are boosting demand for multilingual protocol development and local submission expertise, driving an 10.82% regional CAGR.

How is AI affecting the medical writing market?

Generative AI accelerates initial drafting and data table creation, but regulators still require human oversight, which elevates demand for senior writers skilled in quality governance.

What are the key challenges limiting market growth?

A global shortage of experienced writers, margin pressure from centralized procurement, and rising compliance costs for region-specific templates are the main restraints.

Page last updated on: