Vaccine Adjuvants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

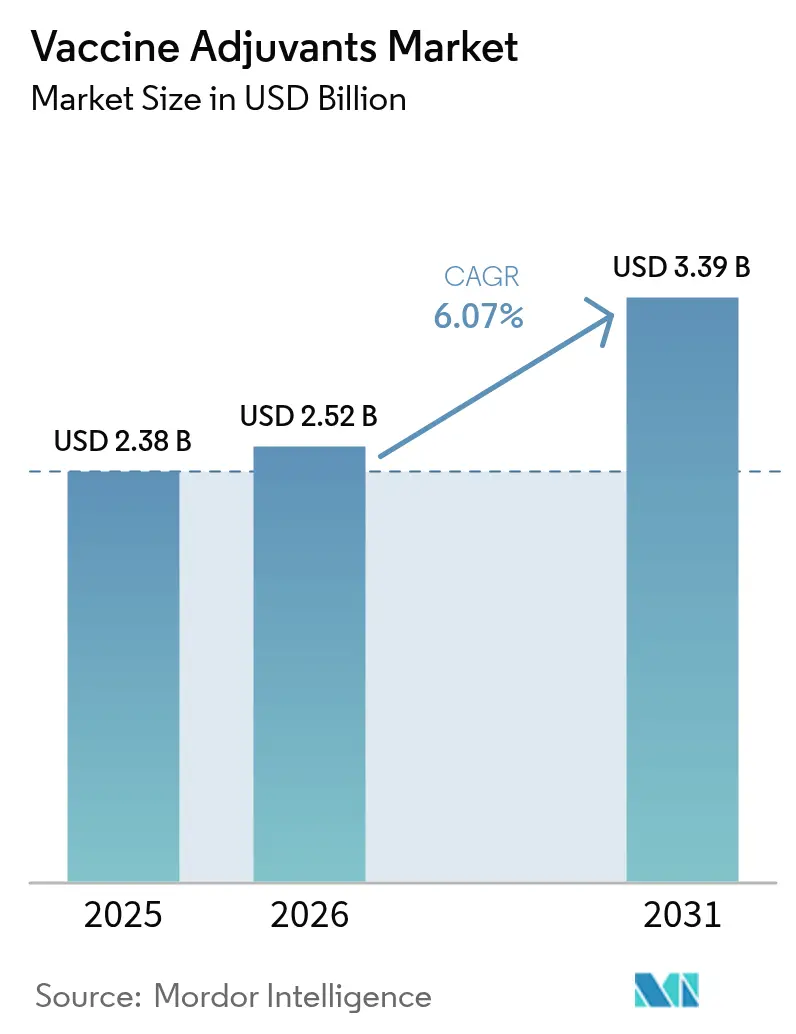

| Market Size (2026) | USD 2.52 Billion |

| Market Size (2031) | USD 3.39 Billion |

| Growth Rate (2026 - 2031) | 6.07% CAGR |

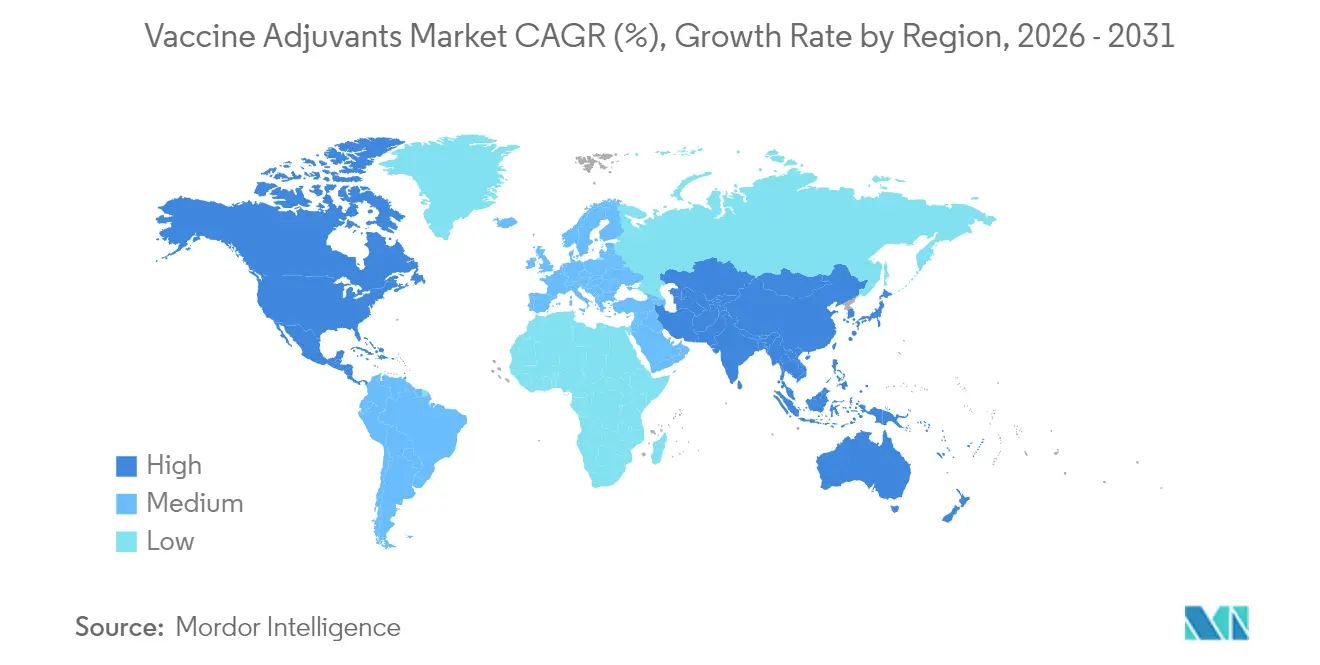

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

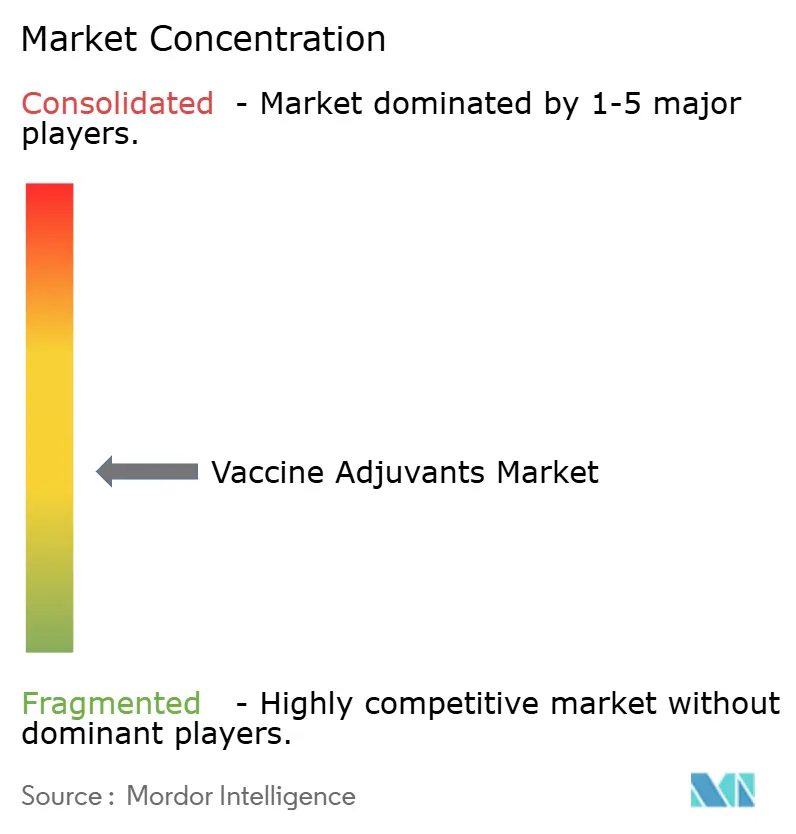

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vaccine Adjuvants Market Analysis by Mordor Intelligence

Vaccine adjuvants market size in 2026 is estimated at USD 2.52 billion, growing from 2025 value of USD 2.38 billion with 2031 projections showing USD 3.39 billion, growing at 6.07% CAGR over 2026-2031. This sustained expansion reflects the pharmaceutical sector’s pivot toward next-generation immunization platforms that need sophisticated adjuvant technologies to amplify immune responses, enable novel antigen formats, and support thermostable formulations. Government commitments to pandemic preparedness add predictable purchase volumes, while AI-guided design shortens formulation cycles and reduces cold-chain dependence, lowering distribution costs and widening global access. Intensifying research into mRNA, self-amplifying RNA, and virus-like particle (VLP) vaccines further lifts demand, as these platforms rely on potent adjuvants to offset the low intrinsic immunogenicity of purified or synthetic antigens [1]Nature, "Vaccine innovation moves beyond COVID-19," nature.com. Supply security for saponin and triterpenoid inputs and regulatory clarity for novel pathways such as STING agonism remain watchpoints, yet continued capital inflows into biotech innovation signal confidence in the long-term attractiveness of the vaccine adjuvants market.

Key Report Takeaways

- By product type, saponin and triterpenoid systems led with 26.12% revenue share in 2025, while virus-like particles are projected to grow at a 6.88% CAGR through 2031.

- By usage type, active immunostimulants held 47.49% of the vaccine adjuvants market share in 2025; vehicle adjuvants record the highest forecast CAGR at 6.79% to 2031.

- By disease type, infectious-disease vaccines accounted for 71.92% of the vaccine adjuvants market size in 2025, whereas oncology applications are set to expand at 6.83% CAGR.

- By application, commercial vaccines captured 67.71% share of the vaccine adjuvants market size in 2025; research applications are advancing at a 7.01% CAGR through 2031.

- By geography, North America commanded 40.62% share in 2025, while Asia-Pacific is forecast to accelerate at a 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vaccine Adjuvants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding government immunization recommendations | +1.0% | Global, strongest in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Unmet vaccine needs for emerging zoonoses | +0.8% | Tropical and subtropical regions | Short term (≤2 years) |

| Rising adoption of recombinant & synthetic antigens | +1.1% | North America and EU leading, Asia-Pacific following | Medium term (2-4 years) |

| Accelerating mRNA-platform demand for novel adjuvants | +1.4% | North America and EU as early adopters | Long term (≥4 years) |

| Expansion of microbial-derived TLR agonist pipelines | +0.5% | Global, concentrated in biotechnology hubs | Long term (≥4 years) |

| AI-designed nano-alum formulations enabling cold-chain-free distribution | +0.9% | Global, highest impact in resource-limited settings | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expanding Government Immunization Recommendations

Broader national vaccine schedules now target adolescents, adults, and the elderly, steadily enlarging the eligible base for adjuvanted products. The 2024 FDA approval of an adjuvanted H5N1 vaccine for pandemic stockpiling and the EMA’s recommendation of MF59-enhanced influenza formulations for adults over 65 illustrate policy momentum that rewards manufacturers with reliable volume offtake [2]Peter Malfertheiner, "Safety, Tolerability, and Immunogenicity of aH5N1 Vaccine in Adults with and Without Underlying Immunosuppressive Conditions," MDPI, mdpi.com. Public-health authorities also highlight cost-avoidance benefits tied to reduced hospitalization rates, reinforcing budget allocations for adjuvant-rich products. This alignment between health economics and procurement creates a stable demand floor for the vaccine adjuvants market.

Unmet Vaccine Needs for Emerging Zoonoses

Climate-linked habitat shifts, intensified urban–wildlife interfaces, and global trade facilitate spillover events, heightening demand for fast-acting vaccines that rely on potent adjuvants for rapid immunogenicity. Self-amplifying RNA candidates show antigen-dose reductions of up to 40-fold when paired with optimized adjuvants, enabling emergency surge manufacturing [3]Thomas Vallet, "Self-Amplifying RNA: Advantages and Challenges of a Versatile Platform for Vaccine Development," MDPI, mdpi.com. The WHO’s Disease X framework explicitly lists broad-spectrum adjuvant platforms as priority technologies, signaling multi-lateral funding support that lifts near-term purchase certainty.

Rising Adoption of Recombinant & Synthetic Antigens

Synthetic biology provides precise antigen constructs but often weak innate stimulus, making adjuvants indispensable for protective titers. The Matrix-M-enhanced recombinant spike vaccine demonstrated 90% efficacy in pivotal trials, confirming how tailored adjuvants can transform purified proteins into high-performance vaccines. Scalable cell-culture production and absence of pathogen handling bolster gross-margin potential, stimulating further recombinant pipeline expansion and reinforcing structural growth for the vaccine adjuvants market.

Accelerating mRNA-Platform Demand for Novel Adjuvants

Beyond COVID-19, mRNA pipelines now span influenza, RSV, and personalized cancer vaccination. New lipid-nanoparticle chemistries such as poly(carboxybetaine) improve endosomal escape and mitigate anti-PEG responses, while trans-amplifying mRNA architectures cut payload needs forty-fold, decreasing batch-capacity constraints. Each breakthrough requires adjuvant–delivery co-optimization, underpinning long-range growth of the vaccine adjuvants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Local & systemic toxicity concerns | -0.5% | Global, heightened scrutiny in EU and North America | Short term (≤2 years) |

| High discovery & pre-clinical screening costs | -0.8% | Global, highest impact on biotechnology companies | Medium term (2-4 years) |

| Scale-up challenges for squalene & QS-21 supply chains | -0.4% | Global, concentrated in established manufacturing regions | Medium term (2-4 years) |

| Regulatory uncertainty around novel STING agonists | -0.6% | North America and EU, with spillover effects globally | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Local & Systemic Toxicity Concerns

Post-marketing surveillance increasingly detects rare inflammatory events, compelling regulators to tighten data requirements. Class B CpG constructs, for instance, destabilize protein antigens and may heighten off-target reactivity, prompting extended toxicology panels and pharmacovigilance. Heightened safety thresholds elongate timelines and raise capital demands, tempering the vaccine adjuvants market’s near-term growth.

High Discovery & Pre-Clinical Screening Costs

Mechanistic studies across multiple species, formulation stress testing, and complex analytics can consume USD 50–100 million before a first-in-human trial. Such outlays exceed the financing bandwidth of many early-stage developers, concentrating innovation within large pharmas that can amortize risk over broad portfolios. The resulting capital hurdle inhibits pipeline diversity and stalls some high-potential candidates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Saponin Dominance Faces VLP Disruption

Saponin and triterpenoid systems controlled 26.12% of the vaccine adjuvants market size in 2025, anchored by QS-21 and AS01 deployments in shingles, malaria, and tuberculosis programs. Their dual induction of humoral and cellular immunity sustains demand, yet natural-source extraction risks and rising sustainability mandates propel investment in semi-synthetic analogs. Virus-like particles, though holding a smaller base, will rise at a 6.88% CAGR through 2031, propelled by BacFreets contamination-reduction technology that simplifies scale-up.

Manufacturers increasingly assess supply diversification to mitigate saponin harvest volatility, while synthetic biology labs refine VLP scaffolds that co-display multivalent antigens and intrinsic pattern-recognition motifs, potentially sidelining separate adjuvant components. Aluminum-salt, emulsion, and liposome formulations continue anchoring routine pediatric schedules, whereas carbohydrate and bacterial-derived TLR agonists address niche indications that require tailored immune polarization. This coexistence of legacy and disruptive technologies ensures the vaccine adjuvants market retains a heterogeneous product landscape.

By Usage Type: Active Immunostimulants Lead Vehicle Innovation

Active immunostimulants secured 47.49% of the vaccine adjuvants market share in 2025, underpinned by mechanistically defined agents such as Dynavax’s CpG 1018 and GSK’s MPL. Regulatory familiarity with these pathways accelerates review timelines and fosters platform approvals across multiple antigens. Vehicle adjuvants, encompassing lipid nanoparticles and polymeric carriers, are projected to grow at 6.79% CAGR through 2031 as developers demand integrated delivery–stimulation solutions.

The vaccine adjuvants market increasingly values vehicles that co-encapsulate antigens and immunopotentiators, maintaining colloidal stability across temperature excursions. Recent manganese-lipid hybrid particles demonstrated stronger CD8+ responses against varicella-zoster versus alum comparators, highlighting functional gains that drive substitution waves. Carrier adjuvants maintain relevance for mucosal or slow-release applications, ensuring each modality retains a defined opportunity space within the broader vaccine adjuvants market.

By Disease Type: Cancer Applications Accelerate Beyond Infectious-Disease Base

Established infectious-disease programs represented 71.92% of the vaccine adjuvants market size in 2025, backed by government procurement for influenza, pneumococcal, and H5N1 reserves. Despite this dominance, oncology candidates will post a 6.83% CAGR to 2031 as neoantigen and tumor-associated antigen pipelines mature. Personalized vaccines demand adjuvants that orchestrate robust CD4+ and CD8+ activation while avoiding regulatory T-cell expansion, spurring exploration of STING agonists and TLR7/8 modulators.

Clinical readouts show adjuvanted melanoma vaccines achieving durable response rates when combined with checkpoint inhibitors, suggesting cross-portfolio synergies that elevate total addressable value. Beyond cancer, autoimmune desensitization and allergy prophylaxis remain exploratory territories, holding incremental upside for the vaccine adjuvants market if safety-efficacy trade-offs can be resolved.

By Application: Research Momentum Catalyzes Commercial Pipelines

Commercial supply accounted for 67.71% of the vaccine adjuvants market size in 2025, driven by influenza, pediatric combination, and travel-health franchises. However, research applications will outpace with a 7.01% CAGR, reflecting post-pandemic R&D budgets that prioritize rapid-response platforms. Grants from BARDA, CEPI, and Horizon Europe specifically earmark funds for adjuvant discovery, ensuring a steady influx of preclinical data that de-risks later commercial launches.

Academic–industry consortia now employ high-content screening, AI-assisted molecular design, and systems immunology to uncover novel adjuvant–antigen synergies, shortening lead-optimization cycles. This iterative feedback loop means today’s laboratory breakthroughs seed tomorrow’s licensed formulations, embedding a virtuous innovation cycle inside the vaccine adjuvants market.

Geography Analysis

North America preserved its leadership with 40.62% share in 2025, supported by mature manufacturing capacity, public-health procurement budgets, and FDA regulatory precedents that streamline platform reviews. Under Operation Warp Speed and successor initiatives, federal funding subsidizes scale-up of mRNA-optimized adjuvant systems, further entrenching regional dominance. Clustered academic centers in Boston, San Francisco, and Toronto forge translational pipelines that feed commercial portfolios, ensuring the vaccine adjuvants market remains anchored in the region.

Asia-Pacific is projected to record a 7.12% CAGR through 2031, propelled by China’s biopharma capacity additions, India’s contract-manufacturing economies of scale, and ASEAN immunization-program expansions. Government subsidies for thermostable adjuvant R&D address tropical cold-chain constraints, while Japan’s chemical-industry strength accelerates lipid-nanoparticle innovations. Local regulatory harmonization under ASEAN’s Vaccine Regulatory Mechanism reduces approval redundancies, improving speed-to-market for regional developers and elevating the vaccine adjuvants market in Asia-Pacific.

Europe maintains steady mid-single-digit growth as the EMA’s adaptive-pathways framework supports conditional licensing for priority adjuvant platforms. Cross-border procurement mechanisms under the EU Joint Procurement Agreement aggregate demand, giving suppliers predictable volumes while enabling price negotiations that preserve margin discipline. Chemical-specialty infrastructure in Germany and the Netherlands sustains high-purity excipient supply, supporting export of adjuvant intermediates to other regions.

Regulatory Landscape

Vaccine adjuvant development and commercialization sit under stringent safety and quality expectations from regulators and standards bodies, including the US Food and Drug Administration (FDA), the European Medicines Agency (EMA), and the World Health Organization (WHO). EMA guidance on adjuvants in vaccines for human use and WHO TRS No. 987 (Annex 2) stress that adjuvants must be justified scientifically, supported by fit-for-purpose nonclinical packages, and controlled through robust CMC and characterization approaches comparable to other active components of an adjuvanted vaccine.

Recent decisions show how these requirements apply to both routine label and storage updates and newer adjuvant systems. In November 2025, the FDA approved a supplemental BLA for Emergent BioSolutions Cyfendus (Anthrax Vaccine Adsorbed, Adjuvanted) that updated labeling and storage requirements, reinforcing lifecycle oversight for licensed adjuvanted vaccines. In January 2026, the Center for Drug Evaluation of China NMPA granted clinical trial authorization for a herpes zoster program using a ZMF59/CpG adjuvant system, reflecting ongoing regulatory throughput for next-generation combinations with safety, reactogenicity, and platform comparability remaining key review points.

Competitive Landscape

The vaccine adjuvants industry exhibits moderate concentration. GSK leverages its AS-series portfolio across shingles, malaria, and RSV programs, while Dynavax’s CpG platform anchors hepatitis B and COVID-19 offerings. Novavax pairs Matrix-M with VLP and recombinant constructs, demonstrating how proprietary adjuvants elevate antigen value. Collectively, the top five companies hold around 60–65% of global revenues, leaving a competitive corridor for mid-cap biotech entrants.

Strategic acquisitions reinforce platform control: Croda’s USD 185 million purchase of Avanti Polar Lipids secured high-grade lipids essential for mRNA products, whereas SK Bioscience’s USD 244 million absorption of IDT Biologika integrated fill-finish capacity with adjuvant manufacturing. Partnerships proliferate, with large pharmas licensing TLR7/8 or STING agonists from specialty firms to diversify pipeline risk. White-space opportunities center on thermostable nano-alum, personalized adjuvant selection based on HLA haplotypes, and combination formulations that synchronize innate-immune triggers.

Barriers to entry remain significant due to regulatory complexity, toxicology costs, and supply-chain validation, yet venture investment into first-in-class mechanisms signals sustained appetite for disruptive differentiation. Companies able to prove both immunological superiority and cost-effective scalability are positioned to capture incremental share as the vaccine adjuvants market expands toward 2030.

Vaccine Adjuvants Industry Leaders

-

Adjuvatis

-

Merck KGaA

-

GlaxoSmithKline plc

-

Novavax Inc.

-

Croda International plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Supply-chain qualification and alternative sourcing for high-impact adjuvants remain an observable whitespace, especially for QS-21. GMP-grade output has been cited at roughly 10 kg per year globally, and capacity expansions are underway. Commercial availability initiatives also point to opportunities for broader R&D access and supplier diversification, including SaponiQx making cultured plant cell QS-21 (cpc QS-21) available via InvivoGen (April 2024), which supports preclinical evaluation and formulation screening for smaller developers.

There is also ongoing demand for adjuvant master file and quality documentation pathways that enable specialized suppliers to meet rising CMC requirements. Amaran Biotech received US FDA Type II DMF acknowledgement for its high-purity AB-801 vaccine adjuvant, positioning it as a qualified starting-material source from Taiwan for developers focused on compliant inputs. Separately, geographic manufacturing build-outs tied to next-generation vaccines, such as the VNVC and Sanofi partnership for a new high-tech vaccine factory in Vietnam with operations starting in 2028, can expand downstream requirements for formulated adjuvants and associated excipients.

Recent Industry Developments

- January 2026: Novavax announced a non-exclusive license agreement with Pfizer to use Novavax Matrix-M adjuvant in up to two disease areas. The deal expands Matrix-M into additional large-pharma development programs and further sharpens competitive positioning around proprietary adjuvant access for subunit and recombinant vaccines.

- September 2025: Novavax amended its collaboration and license agreement with Sanofi to include Matrix-M use in Sanofi's pandemic influenza vaccine candidate program through Phase 2. The expansion strengthens Matrix-M in preparedness-focused indications where governments and public health systems prioritize rapid immunogenicity and dose-sparing options.

- May 2024: Merck KGaA held a groundbreaking ceremony for its EUR 300 million Bioprocessing Production Center in Daejeon, South Korea. The investment adds regional capacity for complex biologics manufacturing, supporting resilience in vaccine and advanced-therapy supply chains that rely on consistent access to specialized raw materials and process know-how.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues earned from vaccine adjuvants that are added to vaccine formulations to improve or direct the immune response, covering both research use and commercial use, across major regions.

Scope exclusions: We exclude finished vaccines, delivery devices, contract fill-finish services, and general immunostimulant drugs that are not used as vaccine adjuvants.

Segmentation Overview

-

By Product Type

- Mineral-salt Adjuvants

- Saponin and Triterpenoid

- Emulsion-based

- Liposome and Virosome

- Carbohydrate & Polysaccharide

- Bacteria-derived TLR agonists

- Virus-Like Particles

- Other Product Types

-

By Usage Type

- Active Immunostimulants

- Carriers

- Vehicle Adjuvants

-

By Disease Type

- Infectious Diseases

- Cancer

- Others

-

By Application

- Research Applications

- Commercial Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean list of adjuvant types and their typical use in vaccine formulations. We then map where demand originates across infectious disease and oncology programs. For sources, we rely on public materials such as FDA and EMA product labels and assessment documents, WHO immunization resources and vaccine-prequalification materials, the US CDC immunization schedules, and published studies indexed in PubMed for adjuvant composition and dose patterns.

To turn these inputs into a sizing backbone, we review company annual reports, investor presentations, and press releases to understand manufacturing scale, partnership activity, and pipeline timing. Where needed, we cross-check patent activity using a paid patent database subscription. For trade and supply signals, we validate using an import-export shipment-level database, especially for adjuvant inputs that can be traced through customs descriptions. These desk sources are not exhaustive, and additional public documents and datasets are pulled during data collection and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the demand pool, because adjuvant usage can shift based on platform choices, dose-sparing needs, and regulatory expectations. We spoke with a mix of adjuvant developers, vaccine manufacturers, researchers, and procurement and quality stakeholders, and we spread coverage across major regions so the assumptions did not get anchored to a single market reality. Inputs from these discussions were used to confirm which adjuvant classes are actively commercialized versus still mostly research-grade, and to align on realistic price progression and adoption timelines.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 12% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 31% | EMEA: 33% |

| Smaller Players: 15% | Managers: 57% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down reconstruction where vaccine output and program activity are translated into adjuvant demand using typical adjuvant dose-per-dose relationships, formulation penetration rates, and platform mix shifts. We then value the resulting demand using blended pricing by adjuvant class. To keep the model anchored, we corroborate totals with selective bottom-up checks, including sampled supplier revenue roll-ups, a volume times average selling price cross-check for key adjuvant categories, and channel checks on research versus commercial pull.

Key inputs in this market include the share of adjuvanted vaccines within total vaccine volumes, changes in dose schedules, the mix between aluminum salts, emulsions, liposomes, and newer immunostimulants, and the pace of approvals that mention specific adjuvant systems in label language. When a data gap appears, we use conservative ranges agreed during expert calls, then tighten them by aligning with observable signals such as approvals, procurement announcements, and manufacturing expansions. Forecasting is done using scenario analysis, with the base case anchored to expected vaccine launches and platform adoption, and sensitivities that capture how quickly specific adjuvant classes move from research into routine commercial use.

Data Validation & Update Cycle

Outputs are triangulated by comparing modeled revenues against independent signals, with checks that include regional demand patterns, product-label disclosures, and consistency of implied pricing over time. Any large variance triggers an analyst review, followed by a re-check of assumptions and, when required, re-contact with industry participants to confirm what changed.

The report is refreshed annually, with interim updates when there are material events such as major approvals, supply constraints, or policy shifts affecting immunization programs. Before delivery, a final analyst pass is completed so the latest public disclosures and validated shifts are reflected in the numbers.

Mordor Intelligence's Vaccine Adjuvants Market Size Measured Against Other Published Estimates

Published values for vaccine adjuvants often do not match because the market can be counted from different angles, and each angle changes what is treated as revenue versus what is treated as upstream inputs. Differences also show up when one estimate focuses only on commercialized adjuvants, while another blends research demand, or when the time window and currency timing do not align.

Finished vaccine sales sit outside Mordor Intelligence's scope, and that exclusion is one reason the spread appears when some publishers implicitly anchor their math to vaccine market totals and then apply broad adjuvant ratios. Gaps are also created when smaller studies exclude in-house usage, apply aggressive platform adoption assumptions for newer immunostimulants, or use a short refresh cycle that does not re-check label-level adjuvant disclosures and regional rollouts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.52 B (2026) | |

| Global Consultancy A | USD 0.70 B (2024) | Counts only externally supplied adjuvants sold by specialized manufacturers, which can understate totals where adjuvants are sourced through integrated vaccine supply chains or captured differently in reporting. |

| Industry Publisher B | USD 1.30 B (2024) | Uses an earlier base year and a different demand pool, and the estimate appears more sensitive to broad platform adoption assumptions rather than being reconciled to dose schedules, label disclosures, and region-wise rollout timing. |

The comparison mainly shows that scope and the demand pool definition drive most of the difference, followed by how pricing and adoption are handled across adjuvant classes. By keeping inclusions explicit, tying demand to vaccine dosing and platform mix, and then cross-checking with supplier and labeling signals, the resulting market size stays easier to reproduce and explain.

Key Questions Answered in the Report

What is the current value of the vaccine adjuvants market?

The market is valued at USD 2.52 billion in 2026 and is forecast to reach USD 3.39 billion by 2031.

Which product category leads the vaccine adjuvants market?

Saponin and triterpenoid systems dominate with 26.12% share in 2025, reflecting widespread use in shingles and malaria vaccines.

What segment is growing fastest within the vaccine adjuvants market?

Virus-like particle adjuvants show the quickest rise, registering a 6.88% CAGR to 2031 due to scalable nanostructure platforms.

Which region is advancing most rapidly?

Asia-Pacific is projected to grow at a 7.12% CAGR as China, India, and Southeast Asia expand immunization programs and local manufacturing.

Why are adjuvants crucial for mRNA vaccines?

MRNA constructs require delivery particles that ensure endosomal escape and balanced innate activation; optimized adjuvants boost antigen expression while moderating inflammation.

How concentrated is the competitive landscape?

The top five companies control a bit more than 60% of revenue, producing a moderate concentration level that still leaves room for disruptive entrants.

Page last updated on: