Utility Locator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

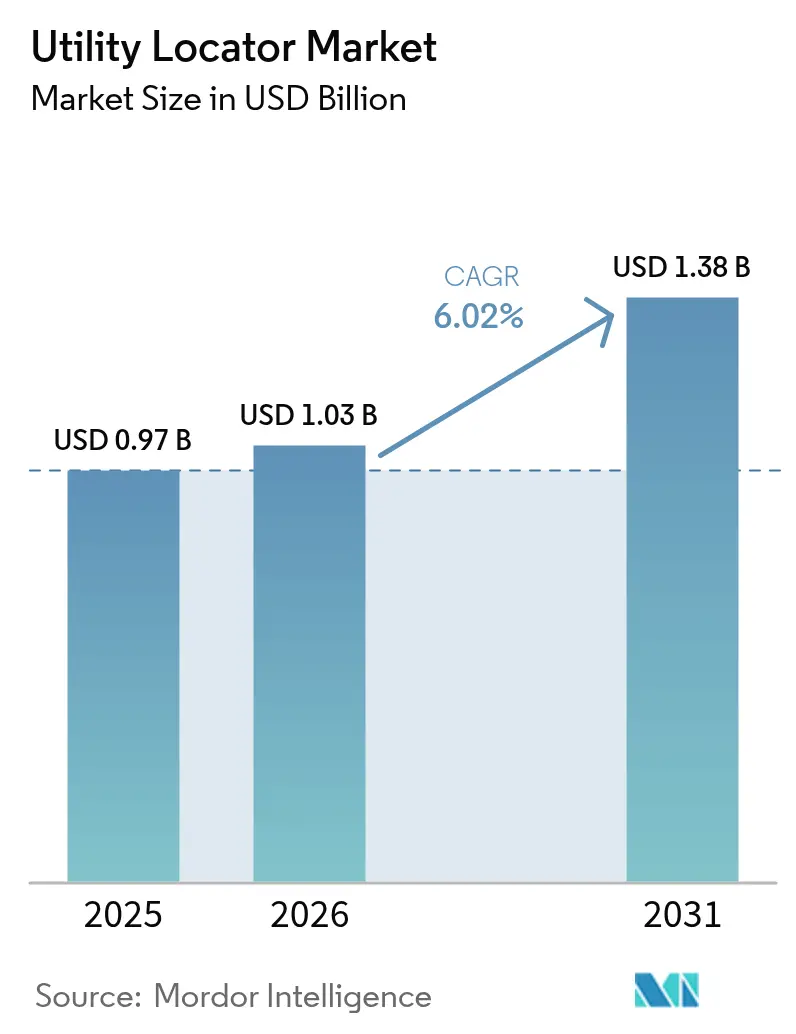

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Utility Locator Market Analysis by Mordor Intelligence

utility locator market size in 2026 is estimated at USD 1.03 billion, growing from 2025 value of USD 0.97 billion with 2031 projections showing USD 1.38 billion, growing at 6.02% CAGR over 2026-2031. Growth is fueled by the collision of aging infrastructure, stricter dig‐safety mandates, and next-generation subsurface imaging that transforms risk management into a continuous, data-driven workflow. Real-time detection expectations, expanding fiber-optic programs, and grid-resilience undergrounding each elevate spend on both equipment and service-based solutions, while copper-price inflation spurs design shifts toward alternative materials. Meanwhile, private equity interest, automation investments, and workforce constraints are reshaping competitive strategies across the utility locator market.

Key Report Takeaways

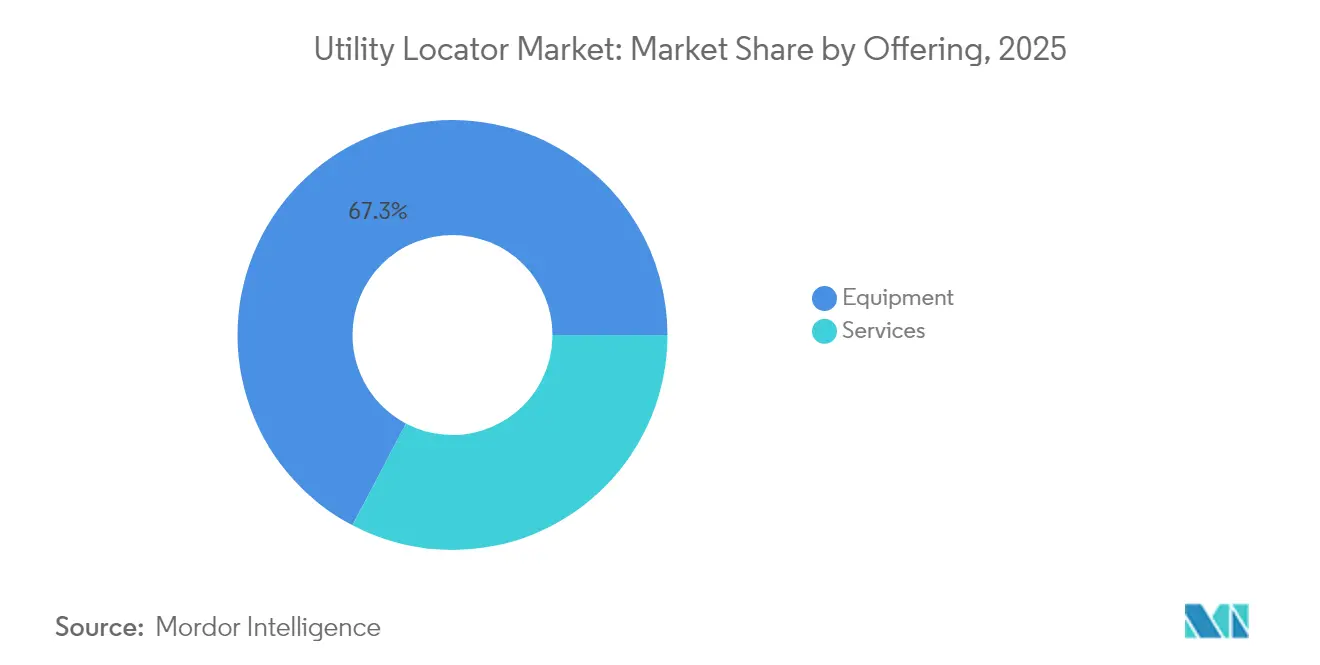

- By offering, equipment led with 67.30% revenue share in 2025; services are projected to expand at a 7.12% CAGR through 2031.

- By target, metallic utilities held 53.40% of the utility locator market share in 2025, while non-metallic detection is forecast to grow at a 6.79% CAGR to 2031.

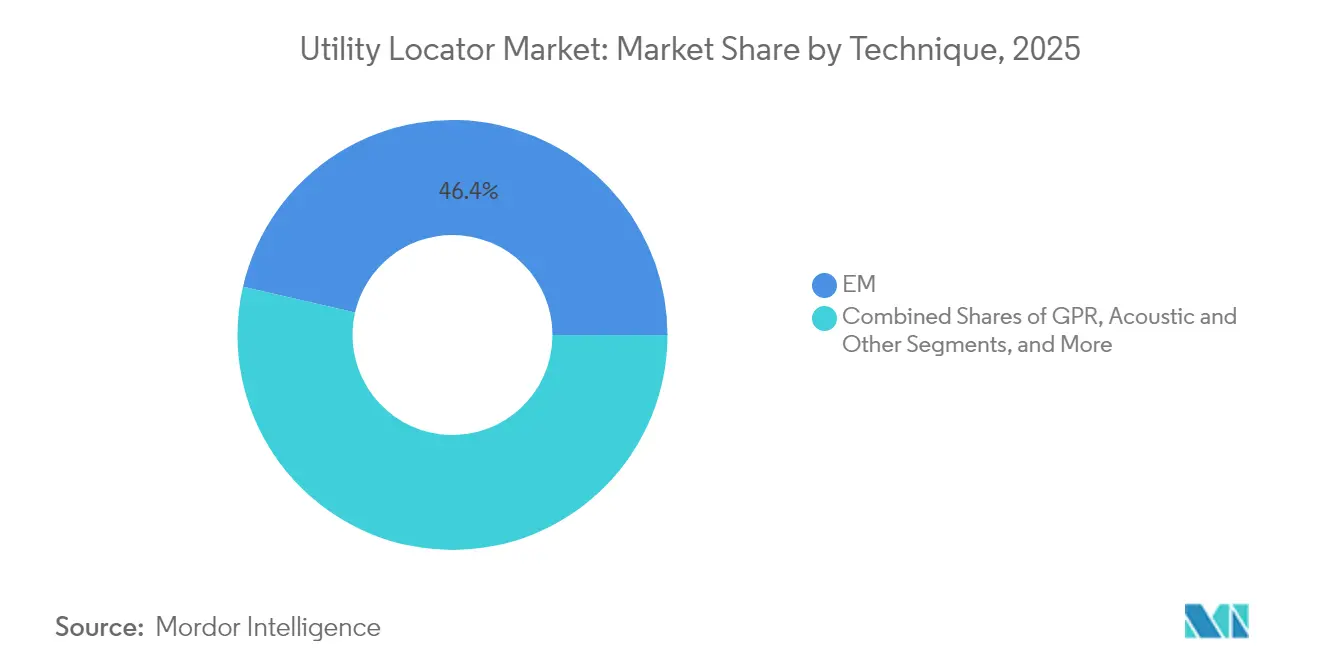

- By technique, electromagnetic detection commanded 46.40% of the utility locator market size in 2025; ground penetrating radar (GPR) is advancing at a 6.52% CAGR.

- By application, oil and gas pipelines accounted for a 28.60% share of the utility locator market size in 2025, whereas telecommunications and fiber deployments are moving at a 7.46% CAGR.

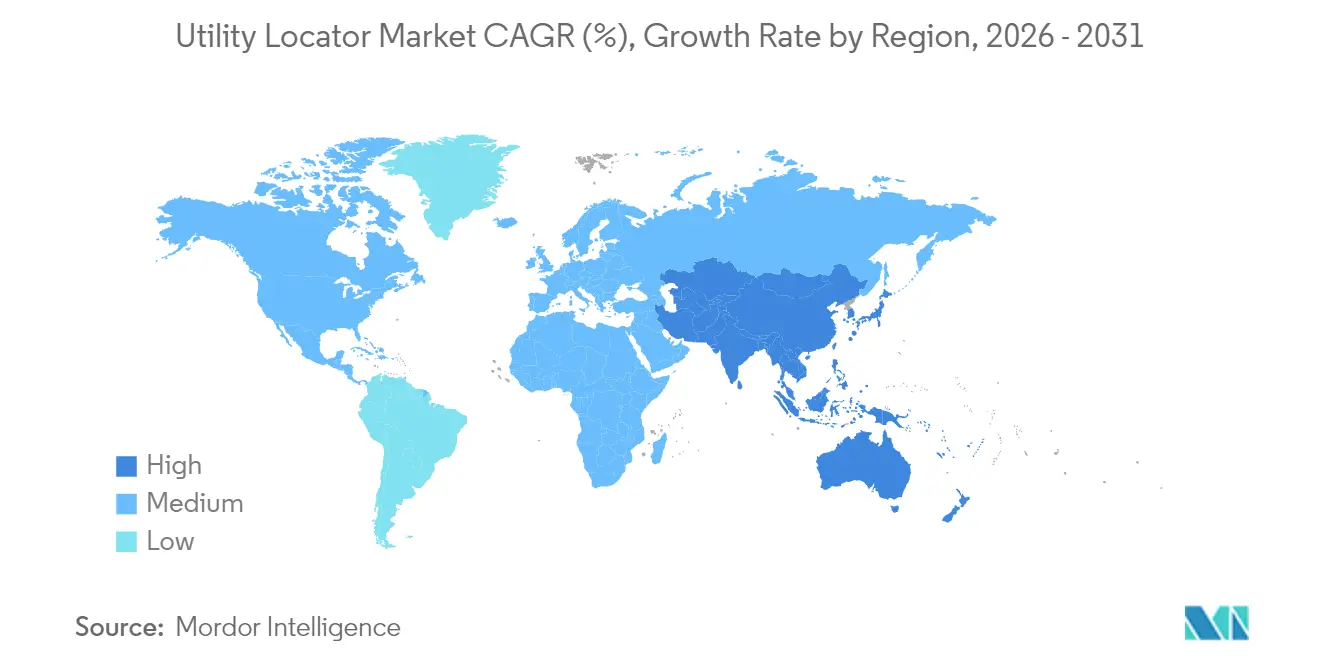

- By geography, North America retained 34.70% share in 2025; Asia Pacific is set to post the fastest 7.46% CAGR

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Utility Locator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in real-time detection demand | +1.2% | Global, led by North America and Europe | Medium term (2–4 years) |

| Infrastructure-age driven inspections | +0.9% | North America and Europe core, expanding to APAC | Long term (≥ 4 years) |

| Mandatory 811 / Call-Before-You-Dig laws | +0.8% | North America dominance, selective EU adoption | Short term (≤ 2 years) |

| Fiber-optic build-outs requiring precise locates | +1.1% | Global, with APAC and North America leading | Medium term (2–4 years) |

| AI-enabled remote utility mapping platforms | +0.7% | North America and Europe early adoption, APAC following | Long term (≥ 4 years) |

| Grid-resilience undergrounding programs | +0.6% | North America and Europe focus, climate-driven expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Real-Time Detection Demand

Construction schedules are compressing while the average utility strike costs USD 56,000 in damages, prompting owners and contractors to shift from pre-dig checks toward continuous, real-time asset verification. AT&T’s AI-driven workflow integration illustrates how major network operators embed predictive locates into daily operations. Distributed fiber-optic sensing now turns in-place fiber into live vibration monitors that flag excavation risks. City projects with dense utilities require instant verification before every trench pull, making cloud-connected electromagnetic receivers and multichannel GPR the default toolkit. Vendors respond with mobile apps that stream field data and alert crews the moment proximity thresholds are breached. This behavior change reframes utility location as an ongoing protection service, not a one-time pre-dig step, enlarging the utility locator market.

Infrastructure-Age Driven Inspections

The Infrastructure Investment and Jobs Act directs USD 550 billion to U.S. projects through 2026, much of it earmarked for underground asset renewal. Machine-learning models now rank pipe sections by failure likelihood, pushing utilities to scan 19% of networks across an 11-year cycle.[1]Fabrizio Arrichiello, “Machine Learning for Water Pipeline Monitoring,” MDPI, mdpi.com Condition assessment demands deeper imaging than legacy locates, so water authorities combine multichannel GPR with electromagnetic verification to gauge wall thickness and corrosion. Fiber-optic strain gauges embedded along mains enable permanent structural health monitoring, tying locators into asset-management platforms. As pipeline lifespans shorten and leak-risk liability rises, demand shifts from basic mark-outs toward data-rich subsurface twins, driving incremental spend inside the utility locator market.

Mandatory 811 / Call-Before-You-Dig Laws

The Common Ground Alliance counts more than 450,000 annual strikes in the United States, motivating regulators to toughen penalties and audit accuracy. Private utility lines, representing more than 60% of all buried assets, often sit outside traditional one-call coverage, opening a large private-locate service niche. Recent water-main breaks in Katy, Texas triggered emergency moratoriums on fiber work, spotlighting the cost of inaccurate locates. Transportation departments now demand survey-grade subsurface maps during project design, forcing contractors to procure high-resolution utility data before bid submission. This policy trend expands the addressable utility locator market and rewards providers that certify accuracy through integrated GPR and GPS workflows.

Fiber-Optic Build-Outs Requiring Precise Locates

Fiber now reaches 55.6% of U.S. households and drives a USD 125-250 billion global network build each year. Micro-trenching in congested rights-of-way needs millimeter-level accuracy to avoid gas, power, and storm lines. Reports linking Arizona fiber rollouts to service disruptions underscore reputational risks when locates go wrong. Contractors, therefore, use hybrid systems pairing electromagnetic locators for metallic plant with AI-enhanced GPR for plastic conduit. Utility owners are codifying fiber-specific separation rules, so advanced detection methods secure premium pricing. These projects significantly increase the utility locator market’s service revenue pool, especially in Asia Pacific, where China’s USD 551 billion underground program accelerates demand.[2]“China Pledges USD 551 Billion for Underground Infrastructure,” South China Morning Post, scmp.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment AND upkeep costs | -0.8% | Global, with acute impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Shortage of trained GPR/EM technicians | -1.1% | North America and Europe acute, expanding globally | Medium term (2–4 years) |

| Urban RF interference degrading accuracy | -0.6% | Urban centers globally, particularly dense metropolitan areas | Medium term (2–4 years) |

| Disparate subsurface data standards | -0.4% | Global, with regional variations in implementation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Equipment and Upkeep Costs

A multichannel GPR array can cost up to USD 100,000, while premium electromagnetic receivers approach USD 5,000; rental fees still tally USD 400 per month for GPR and USD 300 per week for EM devices. Record copper prices at USD 5.20 per pound in 2024 drove 45% spikes in wire costs, pushing manufacturers to explore aluminum substitutes and printed-circuit antennas. Annual calibration contracts, mandated by many public owners, add thousands of dollars in service overhead. Smaller service firms struggle to amortize equipment capital across intermittent work, slowing uptake in price-sensitive regions. Equipment-as-a-service models emerge, yet margins depend on high utilization, limiting viability for rural contractors. The cost hurdle restrains broader adoption within the utility locator market until hardware prices stabilize.

Shortage of Trained GPR/EM Technicians

Fiber construction alone needs 28,000 more workers, but utility locating demands specialized competencies in electromagnetic theory, GPR signal reading, and safety standards. Certification courses run USD 1,000–3,000 and require multiday field practicums, creating entry barriers. Experienced GPR analysts remain scarce because interpretation blends geophysics and civil-engineering knowledge. CASE Construction Equipment now markets productivity‐boosting machines aimed at crews struggling with labor gaps. Vendors are embedding AI auto-classification in GPR software to offset skill shortages, yet complex urban soil conditions still require expert review. Labor scarcity, therefore, limits operational capacity, tempering growth despite an expanding utility locator market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum Despite Equipment Lead

Equipment contributed USD 652.81 million in 2025, translating into a 67.30% slice of the utility locator market. The installed base of electromagnetic transmitters, cable fault locators, and multichannel GPR rigs remains pivotal because contractors cannot perform field work without hardware. However, service revenue is accelerating at a 7.12% CAGR. Telecom carriers, water utilities, and city agencies increasingly outsource the entire locate workflow, favoring turnkey deliverables that blend on-site scanning with data curation and regulatory reports. The utility locator market size for services is projected to reach USD 479.12 million by 2031. Digital twin platforms, AI hit-rate dashboards, and guarantees against damage enhance contract value, enabling service providers to command premium pricing against capital-heavy equipment buyers.

Broader risk-transfer trends also lift services. Insurers now reward developers who use certified locators, steering demand toward third-party specialists. Equipment vendors react by bundling software and field support, shifting their model toward equipment-as-a-service. This hybrid pathway blurs the historical line between gear suppliers and service contractors, intensifying competition and fueling cross-border acquisitions that reshape the utility locator industry.

By Target: Non-Metallic Detection Rises

Metallic pipelines, cables, and conduits still dominated 53.40% of the target landscape in 2025, thanks to steel transmission lines and copper electricity feeders. This share represents USD 517.98 million of the utility locator market size. Yet plastic water mains and fiber conduits are proliferating, causing non-metallic detection revenue to climb 6.79% annually. Advancements in stepped-frequency GPR and pipe-in-pipe acoustic probes deliver reliable depth estimation of PVC and HDPE assets, narrowing historical accuracy gaps. Smart city regulations now compel municipalities to store data for all buried assets regardless of material, boosting the utility locator market.

As replacement cycles pivot toward corrosion-free plastics, locators must refine techniques such as ground-coupled antennas at dual polarizations or traceable wire inserts. Research published on multi-frequency GPR shows depth error reduction below 10 cm for dry soils, reaffirming the technology’s readiness. These technical leaps accelerate adoption for plastic gas laterals and empty duct banks, reinforcing momentum inside the utility locator industry.

By Technique: GPR Advances While EM Retains Core Position

Electromagnetic (EM) field detection held 46.40% revenue in 2025, equal to USD 450.08 million, due to its cost-effectiveness for metallic targets and ease of operator training. Nonetheless, utility locator market demand for high-definition subsurface imagery propels GPR revenue to a 6.52% CAGR, pushing its share toward 37% by 2031. AI-enabled software now creates live tomographic renders, removing the need for expert post-processing. Screening Eagle’s GS9000 update illustrates this feature, live-streaming depth slices to tablets for immediate interpretation.

EM remains indispensable for long linear searches on metallic lines where depth-to-length ratios are favorable. Combined EM+GPR workflows are therefore increasing, with integrated rigs capturing both signals in one pass. Vendors invest in cross-sensor fusion algorithms, feeding cloud engines that assign confidence scores to each detected object. This convergence drives recurring software licenses and positions data analytics as a fresh revenue pillar for the utility locator market.

By Application: Telecom Surges to Challenge Oil and Gas

Oil and gas pipelines accounted for 28.60% of 2025 revenue, translating into USD 277.42 million as operators comply with spill-prevention mandates. However, telecom and fiber projects expand at 7.46% annually on the back of 5G densification and broadband stimulus. Utility locator market share for telecom is expected to eclipse 25% by 2031. Fiber micro-trenching requires near-continuous locates along narrow slits just 2 inches wide, forcing contractors to deploy compact cart-based GPR and electromagnetic sondes.

Electric grid modernization adds steady work as transmission owners place cables underground to mitigate wildfire risk. Water and sewage agencies fund leak-reduction programs, pairing GPR with hydrophone surveys to pin down pipe breakpoints. Rail projects, though niche, demand high-accuracy locates at level crossings and tunnel sections. The resulting multi-sector pull secures volume growth while insulating revenues from single-industry downturns across the broader utility locator market.

Geography Analysis

North America captured 34.70% of 2025 revenue, anchored by mandatory 811 compliance and large-scale replacement of legacy cast-iron gas mains. The United States alone processed more than 38 million one-call tickets, creating a robust baseline for the utility locator market. Wage pressures and a mature rental ecosystem sustain high equipment turnover, supporting premium EM and GPR sales even amid cost inflation.

Asia Pacific, propelled by China’s USD 551 billion underground investment plan, exhibits the fastest 7.46% CAGR through 2031. Megacity metro extensions, smart road corridors, and national fiber backbones demand mass deployment of multichannel GPR vans and drone-mounted sensors. India’s Smart Cities Mission adds further momentum through mandates for comprehensive subsurface records in 100+ urban centers. The region’s accelerating adoption narrows the revenue gap with North America, setting the stage for leadership shifts in the utility locator market.

Europe maintains balanced growth as utility owners digitize century-old asset records. The United Kingdom’s nationwide mapping initiative pushes contractors to achieve survey-grade accuracy, while Germany channels climate-adaptation funds into grid undergrounding. Urban radio-frequency noise, especially in older city cores, challenges EM performance, which in turn boosts GPR demand. Emerging Eastern European markets lean on EU cohesion grants to upgrade water networks, providing fresh service opportunities. Collectively, these programs reinforce a steady long-term outlook for the utility locator market in Europe.

Competitive Landscape

The competitive field blends established hardware makers with software-centric disruptors. Radiodetection, Subsite Electronics, Leica Geosystems, and Vivax-Metrotech leverage broad catalogs and dealer footprints to protect their share. Radiodetection’s partnership with Trimble Catalyst now provides centimeter-level positioning within its Precision Locator range. Subsite introduces semiautonomous GPR carts that self-calibrate between passes, reducing operator workload.

Investment capital continues to flow. Exodigo closed a USD 118 million round to refine AI-driven underground mapping that fuses sensor data into 3D point clouds. 4M Analytics reached 2,500 miles of mapped utilities and cut agency records research time by 95%. Service firms like United States Infrastructure Corporation attracted private-equity backing from Partners Group, signaling confidence in scalable locate outsourcing

Cost pressures trigger materials R&D, with Copperweld promoting bimetallic wires that curb copper consumption. Vermeer’s 2025 launch of the Verifier G3+ FLX locator adds fault-finding to its drill-rig customer base vermeer.com. The interplay of software analytics, sensor miniaturization, and integrated services intensifies competition, positioning data accuracy rather than hardware specs as the defining differentiator within the utility locator market.

Utility Locator Industry Leaders

Vivax-Metrotech

Emerson Electric

Geophysical Survey Systems, Inc

Radiodetection Ltd.

Guideline Geo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vermeer unveiled the Verifier G3+ FLX utility locator featuring advanced fault-finding capabilities.

- March 2025: LAPP Tannehill reported copper at USD 5.20 per pound, driving 45% wire-price hikes that ripple into locator hardware costs

- February 2025: GBD Magazine spotlighted micro-trench infill systems on turnpike fiber networks, underscoring high-precision locate requirements.

- January 2025: Partners Group acquired United States Infrastructure Corporation to expand its infrastructure services portfolio.

Global Utility Locator Market Report Scope

A utility locator identifies, locates, and protects underground utilities by completing tasks such as studying utility maps and performing online investigations, physically walking around the area to look for signs of utilities, using equipment to locate and map out cables, pipes, and other underground elements, and overseeing safe digging practices to protect utilities and those on site.

The Utility Locator Market is segmented by offering (equipment, services), by target (metallic utilities, non-metallic utilities), by techniques (electromagnetic field, ground penetrating radar), by application (oil and gas, electricity, transportation, water, and sewage, telecommunications), and by geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Equipment |

| Services |

| Metallic Utilities |

| Non-Metallic Utilities |

| Electromagnetic Field (EM) |

| Ground Penetrating Radar (GPR) |

| Acoustic and Other |

| Oil and Gas |

| Electricity |

| Transportation and Rail |

| Water and Sewage |

| Telecommunications and Fiber |

| Other Utilities |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Offering | Equipment | |

| Services | ||

| By Target | Metallic Utilities | |

| Non-Metallic Utilities | ||

| By Technique | Electromagnetic Field (EM) | |

| Ground Penetrating Radar (GPR) | ||

| Acoustic and Other | ||

| By Application | Oil and Gas | |

| Electricity | ||

| Transportation and Rail | ||

| Water and Sewage | ||

| Telecommunications and Fiber | ||

| Other Utilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the utility locator market?

The utility locator market stands at USD 1,028.39 million in 2026 and is projected to climb to USD 1.38 billion by 2031.

Which region grows fastest for utility locator services?

Asia Pacific leads with a 7.46% CAGR through 2031, driven by large-scale infrastructure programs in China and India.

Why are services outpacing equipment sales?

Owners prefer turnkey, outcome-based contracts that transfer risk and leverage AI analytics, helping services grow at 7.12% CAGR.

How do fiber rollouts affect demand for utility locators?

Fiber deployment requires millimeter-precision locates to avoid costly strikes, pushing telecom-related locator revenue to a 7.46% CAGR.

What technologies are gaining share in non-metallic utility detection?

Ground penetrating radar with AI-based interpretation and acoustic tracing tools are emerging as key methods for plastic pipes and fiber conduits.

Are labor shortages limiting market growth?

Yes, the need for trained GPR and EM technicians remains acute, curbing capacity even as demand accelerates, though AI-assisted tools are easing the gap.

Page last updated on: