Healthcare Architecture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

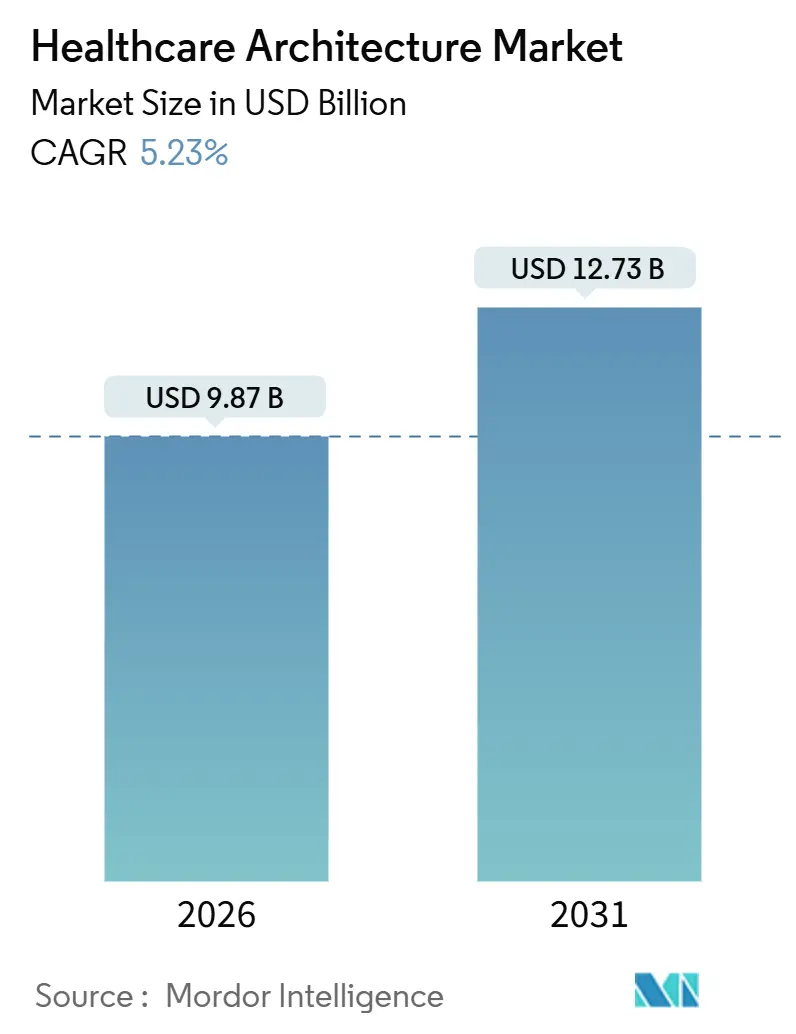

| Market Size (2026) | USD 9.87 Billion |

| Market Size (2031) | USD 12.73 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

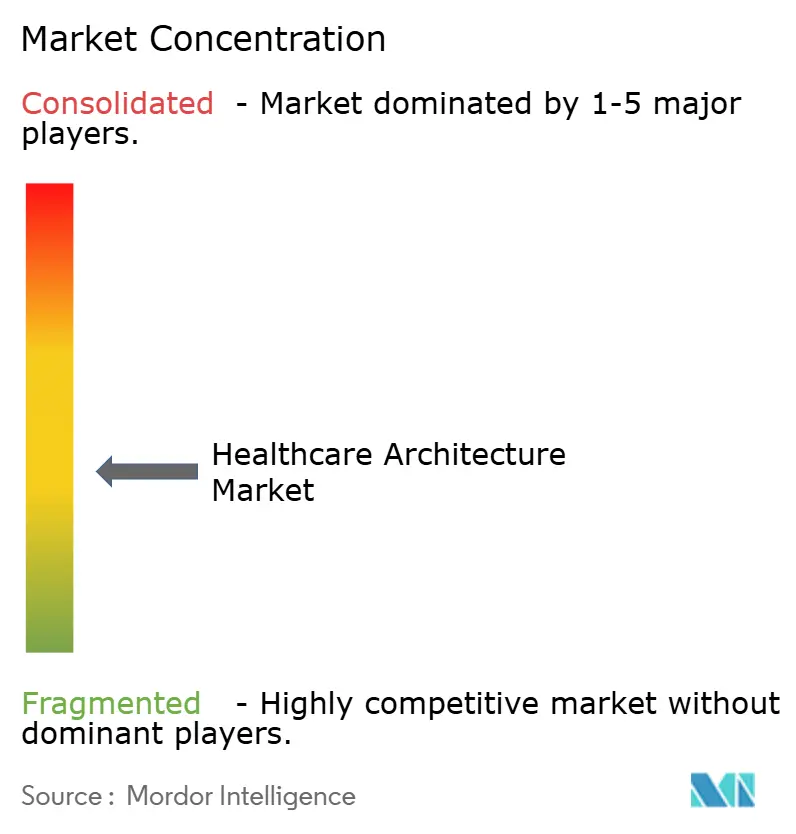

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Architecture Market Analysis by Mordor Intelligence

The Healthcare Architecture Market size is estimated at USD 9.87 billion in 2026, and is expected to reach USD 12.73 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031).

Continued capital re-allocation from large acute-care hospitals toward distributed outpatient hubs is reshaping the healthcare architecture market as owners seek lower operating costs, quicker patient throughput, and leaner staffing models. Renovation spending dominates because retrofitting legacy assets delivers faster payback than greenfield construction amid tight capital budgets. Smart-building platforms that merge digital-twin modeling with energy analytics are emerging as a differentiator, especially in North America, where labor shortages and utility cost inflation persist. Competitive intensity is accelerating as design-build consortia promise turnkey delivery schedules that compress timelines by up to 40% through off-site fabrication and modular assemblies.

Key Report Takeaways

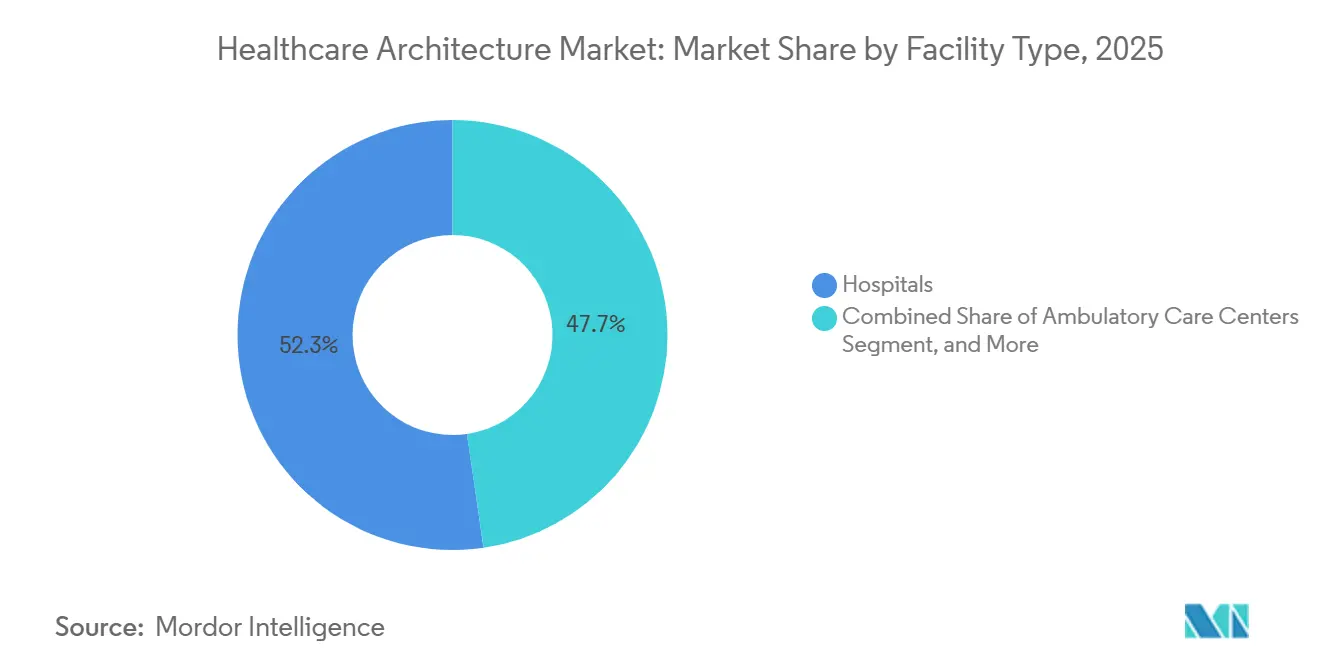

- By facility type, hospitals led with 52.31% of healthcare architecture market share in 2025, and ambulatory care centers are forecast to expand at a 6.48% CAGR through 2031, the fastest growth among facility categories.

- By service type, renovation and remodeling accounted for 46.57% of the healthcare architecture market size in 2025, and interior design and planning services are advancing at a 7.12% CAGR between 2026 and 2031.

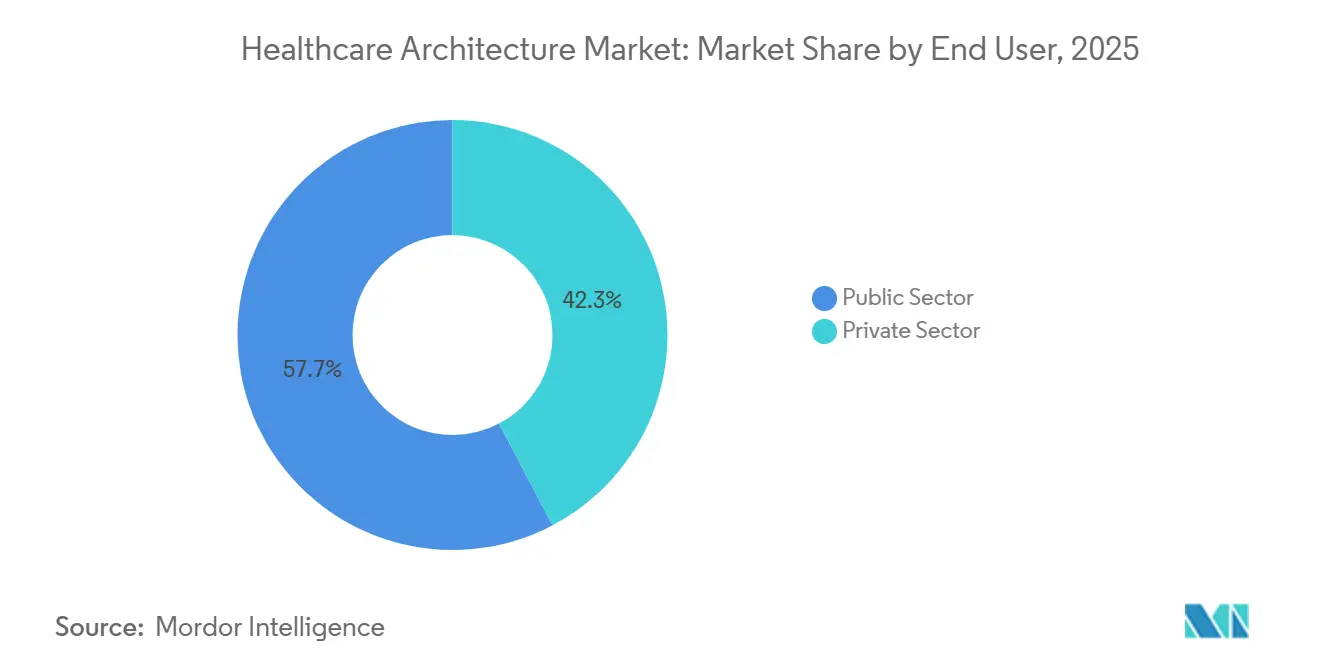

- By end user, the public sector accounted for 57.72% of 2025 spending, while private operators are growing at an 8.87% CAGR through 2031.

- By geography, North America captured 38.83% of 2025 revenue; Asia-Pacific is climbing at a 9.39% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Architecture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Patient-Centric Healing Environments | +0.8% | Global, with early adoption in North America and Northern Europe | Medium term (2-4 years) |

| Shift Toward Outpatient & Ambulatory-Care Facilities | +1.2% | North America, Western Europe, urban APAC markets | Short term (≤ 2 years) |

| Increased Government Spending on Healthcare Infrastructure | +1.5% | APAC core (China, India, Indonesia), GCC, Sub-Saharan Africa | Long term (≥ 4 years) |

| Integration of Smart-Building & IoT Technologies | +0.7% | North America, EU, GCC, Australia | Medium term (2-4 years) |

| Climate-Resilient Hospital-Design Standards | +0.5% | Global, with regulatory urgency in EU, California, Australia | Long term (≥ 4 years) |

| Retail-Health Micro-Clinic Prototypes | +0.4% | North America urban corridors, select EU metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Patient-Centric Healing Environments

Evidence-based design research links private rooms, daylight access, and acoustic control to lower hospital-acquired infection rates and shorter average length of stay, prompting retrofits even in cash-constrained systems. A 2024 meta-analysis reported that single-patient rooms cut infections by 28% and trimmed stays by 0.6 days, yielding tangible ROI under value-based payment models.[1]Alex Keenan, “Retrofit Projects Rise as Budgets Tighten,” modernhealthcare.com Capital budgets now routinely include circadian-tuned LED lighting, noise-absorbing finishes, and biophilic elements as baseline specifications, not luxury add-ons. Behavioral-health facilities implement trauma-informed layouts, remove ligature points, and add outdoor therapy gardens that comply with Joint Commission safety alerts, thereby improving patient engagement. The trend reinforces demand for specialized interior design services that translate clinical outcomes into spatial metrics, a skill set commanding premium fees in RFP evaluations.

Shift Toward Outpatient & Ambulatory-Care Facilities

Payer reimbursement reforms now reimburse total knee arthroplasty and certain cardiac catheterizations in ambulatory surgery centers, unlocking USD 2.3 billion of annual construction demand in the United States alone.[2]Robert Allen, “CMS Expands ASC Procedure List,” cms.gov ASCs require 40% less floor area per procedure than hospital ORs and favor modular exam pods that adapt to fluctuating volumes, thereby lowering capital intensity and accelerating break-even timelines. Developers cluster ASCs with imaging and physical-therapy suites, forming integrated outpatient campuses that appeal to private-equity investors seeking predictable cash flows. The 2025 Facility Guidelines Institute update, however, mandates discrete air-handling systems for sterile zones, adding USD 1.2–1.8 million to a 15,000 square-foot ASC and underscoring the importance of early MEP coordination. Architects adept in iterative digital-twin modeling can reconcile cost pressures with code compliance, winning contracts on both speed and certainty metrics.

Increased Government Spending on Healthcare Infrastructure

China’s 14th Five-Year Plan allocates USD 72 billion to upgrades of county-level hospitals and community health centers, targeting 1,200 facilities by 2027.[3]National Development and Reform Commission, “14th Five-Year Health Plan,” ndrc.gov.cn India’s Ayushman Bharat mission allocates USD 7.8 billion for nearly 30,000 primary-care sites to be operational by 2026. Saudi Arabia’s Vision 2030 allocates USD 40 billion to six medical cities and 130 clinics, favoring consortia capable of delivering turnkey projects under public-private partnership (PPP) structures. Such sovereign outlays underwrite the long-term pipeline for the healthcare architecture market and mitigate cyclical slowdowns in North America and Europe. International design firms form joint ventures with local contractors to navigate labor rules, procurement thresholds, and localization mandates, expanding service lines in master planning and sustainability consulting.

Integration of Smart-Building & IoT Technologies

Hospitals adopting IoT-enabled building-management systems reported 22% energy savings and 15% lower equipment replacement costs in a 2025 Cleveland Clinic pilot, proving the business case for sensor-rich facilities. Continuous monitoring of temperature, pressure, and humidity supports real-time infection control, prompting the International Code Council to add digital compliance pathways to the 2024 International Building Code amendments. Design teams harness aggregated operating data to accurately size mechanical systems, eliminating over-specification that inflates both capital and lifecycle costs. Predictive maintenance algorithms flag filter and pump degradation, cutting unplanned downtime that can disrupt surgical schedules and revenue cycles. Owners now request open-protocol BMS platforms during schematic design, elevating architects and MEP engineers into IT-integration roles that consultants traditionally handled.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Construction-Material Costs | -0.9% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Complex & Varying Healthcare-Facility Regulations | -0.6% | Global, fragmented enforcement in emerging markets | Medium term (2-4 years) |

| Capital-Expenditure Freezes by Cash-Strapped Health Systems | -1.1% | North America, Western Europe | Short term (≤ 2 years) |

| Shortage of Skilled Healthcare Architects in Emerging Markets | -0.5% | APAC (ex-Japan, Australia), Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Construction-Material Costs

Structural steel prices jumped 18% and medical-grade HVAC components climbed 22% between mid-2024 and early 2025, forcing 38% of North American hospital projects to exceed budget by more than 10%. Fixed-price contracts have all but disappeared, replaced by cost-plus terms with escalation clauses that shift risk to owners and dampen bid competition. Architects specify multiple approved manufacturers and modular systems to hedge supply-chain shocks, reducing schedule risk but adding design coordination hours that erode fee margins. Prefabrication gains traction because manufacturers can lock raw-material prices earlier in the value chain, offering cost certainty at the expense of longer lead times for shop drawing approval. Owners also explore substituting domestic materials to bypass import tariffs, though code certifications can limit viable alternatives.

Capital-Expenditure Freezes by Cash-Strapped Health Systems

Median U.S. hospital operating margins fell to 2.1% in 2025, down from 4.3% pre-pandemic, prompting 54% of systems to postpone or cancel expansion projects. Rising municipal-bond yields have pushed financing costs up by 140 basis points since 2023, further shrinking the feasible project scale. The UK’s National Health Service delayed USD 2.7 billion of maintenance backlogs under fiscal austerity, constraining new-build activity yet channeling limited funds toward urgent infection-control retrofit. Architects pivot to smaller-scope renovations that meet immediate compliance mandates, such as negative-pressure isolation rooms, while preserving design teams and client relationships for when capital loosens. Adaptive reuse of non-clinical space becomes attractive because it leverages existing utilities and reduces first costs, aligning with tightened debt covenants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Ambulatory Networks Reshape Infrastructure Priorities

Ambulatory centers are growing at a 6.48% CAGR through 2031, outpacing the healthcare architecture market average as owners migrate procedures out of acute-care hospitals to mitigate overhead and insurer scrutiny. The segment’s momentum contrasts with hospitals, which retained 52.31% of 2025 revenue yet face slower growth due to stringent code requirements and capital-intensive footprints. Long-term care facilities are registering moderate expansion in aging societies such as Japan and Southern Europe. At the same time, behavioral health sites gain policy support through mental health parity laws in the United States and Canada. Specialty clinics, oncology, dialysis, and orthopedics are expanding in suburban corridors where land costs are lower, and parking is abundant, refining the mixed-use prototype that integrates retail conveniences with clinical efficiency.

Developers rapidly convert retail and office assets into ambulatory hubs, shaving 20–35% off construction budgets compared with greenfield projects, yet still meeting infection-control and life-safety codes through extensive MEP retrofits. The 2025 FGI Guidelines allow corridor width reductions and shared recovery bays when continuous electronic monitoring is installed, cutting circulation area by 15–20% and freeing rentable space for revenue-producing services. Conversely, hospital projects confront escalating complexity, as seismic, flood, and backup-power provisions raise costs by USD 8–15 million on a 200-bed facility. As a result, owners increasingly phase hospital master plans, deferring tower additions until demand stabilizes and bond markets recover.

By Service Type: Renovation Dominates as Systems Optimize Legacy Assets

Renovation and remodeling accounted for 46.57% of the healthcare architecture market share in 2025 as systems opted for targeted interventions rather than full replacements. Interior design and planning services exhibit a stronger 7.12% CAGR, as evidence-based mandates require reconfiguring nurse stations, patient flows, and virtual-care pods to enhance outcomes and staff efficiency. New construction remains substantial but trails renovation growth, constrained by lender caution and payer reluctance to reimburse higher depreciation charges. Ancillary offerings, master planning, sustainability consulting, WELL, and LEED certification illustrate owners’ shift toward holistic asset-life strategies. In this niche, international firms can differentiate through advanced analytics and carbon accounting.

Retrofits often unlock immediate revenue; Mayo Clinic’s 2024 emergency-department upgrade boosted throughput 18% and lifted annual revenue by USD 9.6 million against a USD 12 million investment, validating the financial appeal of smaller-scope projects. Interior designers now co-design with clinical operations to reduce staff walking distances, an ergonomic gain tied to lower nurse turnover and higher HCAHPS scores. Master-planning engagements incorporate demographic and payer-mix modeling, letting boards align phased capital allocation with 10- to 15-year cash-flow projections. Net-zero energy certifications trimmed utility expenses by 35% and increased employee retention by 12% in 2025 benchmarking, underscoring how sustainability now intersects directly with workforce economics.

By End User: Private Sector Gains as Public Systems Face Budget Constraints

Public entities captured 57.72% of 2025 outlays, yet operate within strict procurement and budgeting frameworks that emphasize primary and emergency care rather than premium finishes. Private entities, expanding at an 8.87% CAGR through 2031, are expanding into elective, specialty, and high-acuity niches, emphasizing concierge amenities and rapid appointment scheduling to attract commercially insured patients. Employer-sponsored clinics from corporate giants such as Amazon and JPMorgan Chase further bolster private demand, requiring on-site primary care facilities with tight integration with IT security.

PPP models blur the public-private line; in the United Kingdom, Australia, and Canada, entities outsource hospital development to private consortia that design, build, finance, and maintain facilities over 25- to 30-year terms. While PPPs can accelerate delivery, they may hinder future reconfiguration and invoke penalty structures if service scopes change, complicating life-cycle flexibility. Private operators often demand early contractor involvement, aggressive schedules, and bespoke IT platforms, requiring architecture firms to maintain specialized healthcare-IT competencies. Public owners, conversely, stress cost transparency, community consultation, and resilience standards, extending approval cycles but ensuring universal-service alignment.

Geography Analysis

North America generated 38.83% of global 2025 revenue due to replacement demand for aging 1960s-era hospitals and stringent seismic requirements in California and the Pacific Northwest. CMS augmented capital add-on payments by USD 1.8 billion annually for projects embedding infection-control and climate-resilient features, sustaining the renovation pipeline even amid operating-margin compression. Canada’s CAD 3.2 billion, five-year infrastructure fund prioritizes Indigenous health services and rural telehealth nodes, influencing design briefs toward cultural inclusion and long-distance care models. Mexico’s social-security institute is tendering 14 regional hospitals under PPP contracts, inviting international teams with design-build credentials and bilingual regulatory fluency.

Asia-Pacific remains the fastest-growing region at a 9.39% CAGR, fueled by China’s approval of 87 tertiary hospitals in 2025, each costing USD 200–400 million and leveraging modular construction to accelerate delivery. India faces a 2.3 million-bed deficit, steering investment toward specialty chains with standardized clinical protocols that allow architectural templates to scale across multiple cities. Japan’s declining population drives hospital consolidation and floor-area conversions from acute care to rehabilitation, a demand that incentivizes flexible interior partitioning strategies. Australia’s private operators commit AUD 4.1 billion to brownfield expansions, emphasizing day-surgery theaters and integrated cancer centers that align with payer shifts toward outpatient models.

Europe balances decarbonization mandates with fiscal austerity. Germany’s Hospital Future Act provides EUR 4.3 billion for digital infrastructure and emergency upgrades, linking funds to interoperability and renewable-energy benchmarks. The United Kingdom’s New Hospital Programme, despite cost revisions, aims to build 40 net-zero hospitals by 2030 through standardized kit-of-parts construction. France’s EUR 19 billion Ségur de la Santé plan funnels investment into EDs, ICUs, and mental-health wards, with design competitions favoring low-carbon materials and adaptable floorplates. The GCC region is building showcase medical cities, including an 800-bed LEED Platinum hospital within Saudi Arabia’s NEOM mega-project, while Sub-Saharan Africa faces financing constraints and a shortage of specialist architects, slowing execution.

Competitive Landscape

The top players capture a moderately fragmented healthcare architecture industry where both international conglomerates and regional boutiques thrive. Integrated firms such as HDR, HKS, and Gensler leverage multidisciplinary teams and in-house engineering to win multibillion-dollar medical center campuses that require single-source accountability. HDR’s generative-design tool trimmed circulation by 12% in a 2025 medical-center project, freeing 18,000 square feet for higher-yield clinical services. CannonDesign and Perkins&Will differentiate through peer-reviewed research and deep clinical partnerships that translate workflow data into spatial layouts, a value proposition prized by academic-medical-center clients.

Construction giants are integrating design studios to secure design-build or integrated project delivery deals that guarantee maximum prices and compressed schedules. Turner Construction’s modular patient-room system cut on-site labor by 40% and reduced average schedule overruns to below 3% on hospital projects initiated in 2025. Skanska AB’s in-house prefabrication facilities now deliver fully plumbed bathroom pods, slicing eight days per room off critical path schedules. Behavioral-health and ambulatory-surgery niches present white-space growth opportunities; firms offering templated yet adaptable prototypes can replicate designs across multiple locales, aligning with private-equity roll-up strategies. Regulatory expertise remains a moat, as inconsistent local codes elevate the importance of architects who can navigate approval processes without costly redesigns.

Healthcare Architecture Industry Leaders

HDR Inc.

HKS Inc.

Perkins&Will

CannonDesign

Stantec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Northern Health named EllisDon the preferred proponent for the University Hospital of Northern British Columbia Acute Care Tower, a significant expansion that will modernize tertiary services for the Prince George community.

- October 2025: Nabla Bio signed a second multiyear research partnership with Takeda, demonstrating how biotech collaborations spur demand for specialized R&D facilities within the healthcare architecture market.

- September 2025: HED appointed Peter Patsouris as Associate Principal to expand its Boston healthcare practice, adding three decades of clinical design experience and reinforcing the firm’s regional footprint.

- March 2025: Microsoft launched Dragon Copilot, a unified voice AI assistant that influences future space planning by reducing clinician documentation time and reshaping clinical support zones.

Global Healthcare Architecture Market Report Scope

The Healthcare Architecture Market Report is Segmented by Facility Type (Hospitals, Ambulatory Care Centers, Long-term Care Facilities, Behavioral Health Facilities, Specialty Clinics, Others), Service Type (New Construction, Renovation & Remodeling, Interior Design & Planning, Others), End User (Public Sector, Private Sector), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hospitals |

| Ambulatory Care Centers |

| Long-term Care Facilities |

| Behavioral Health Facilities |

| Specialty Clinics |

| Others |

| New Construction |

| Renovation & Remodeling |

| Interior Design & Planning |

| Others (Master Planning, Sustainability & Green-Building Consulting, etc.) |

| Public Sector |

| Private Sector |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Facility Type | Hospitals | |

| Ambulatory Care Centers | ||

| Long-term Care Facilities | ||

| Behavioral Health Facilities | ||

| Specialty Clinics | ||

| Others | ||

| By Service Type | New Construction | |

| Renovation & Remodeling | ||

| Interior Design & Planning | ||

| Others (Master Planning, Sustainability & Green-Building Consulting, etc.) | ||

| By End User | Public Sector | |

| Private Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current healthcare architecture market size?

The healthcare architecture market size stood at USD 9.87 billion in 2026 and is on track to reach USD 12.73 billion by 2031.

Which facility category is expanding the fastest?

Ambulatory care centers are expanding at a 6.48% CAGR through 2031, driven by payer shifts toward lower-cost outpatient settings.

Which facility category is expanding the fastest?

Ambulatory care centers are expanding at a 6.48% CAGR through 2031, driven by payer shifts toward lower-cost outpatient settings.

Why are renovation projects dominant right now?

Renovation and remodeling captured 46.57% of 2025 revenue because retrofitting existing buildings delivers quicker ROI amid capital constraints.

Which region is growing most rapidly?

Asia-Pacific leads with a 9.39% CAGR as China, India, and GCC nations fund massive hospital and clinic expansions.

Page last updated on: