U.S. C-arms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.05 Billion |

| Growth Rate (2026 - 2031) | 4.75% CAGR |

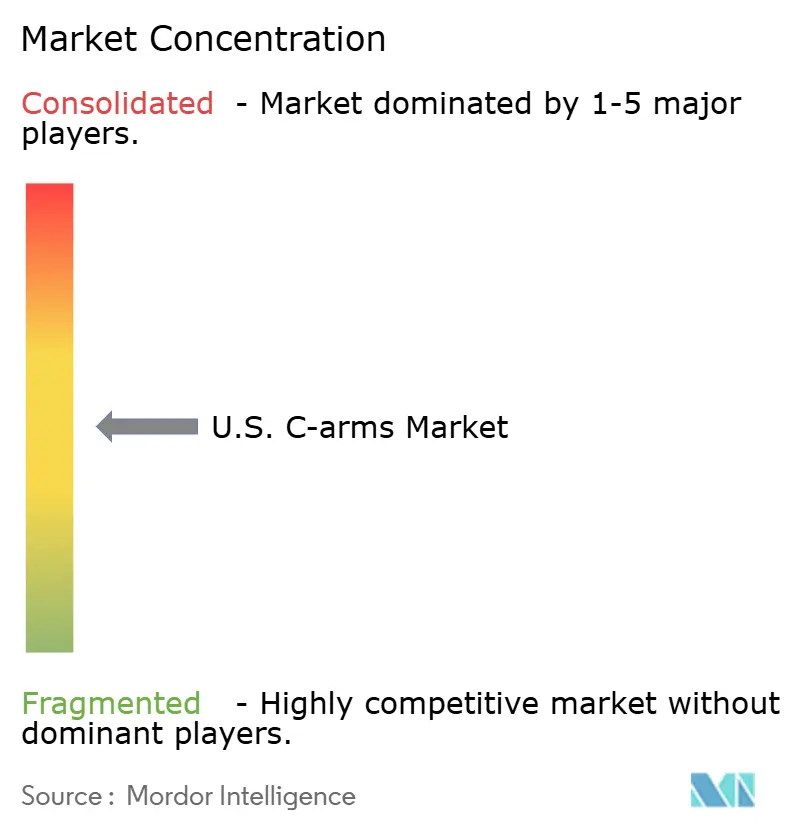

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. C-arms Market Analysis by Mordor Intelligence

The U.S. C-arms Market size is expected to grow from USD 0.79 billion in 2025 to USD 0.83 billion in 2026 and is forecast to reach USD 1.05 billion by 2031 at 4.75% CAGR over 2026-2031.

Hospitals and surgery centers are replacing outdated image-intensifier systems with flat-panel detector platforms that align with clinical imaging needs and FDA performance standards under 21 CFR 1020.32. This transition is driven more by replacement demand than an increase in procedure volumes. The shift of procedures to outpatient settings is boosting demand for compact mobile systems suitable for smaller operating rooms and shared procedure suites. High utilization in procedure categories like orthopedics, trauma, spine, and pain management is supporting capital purchases in hospitals and ambulatory settings.

Key Report Takeaways

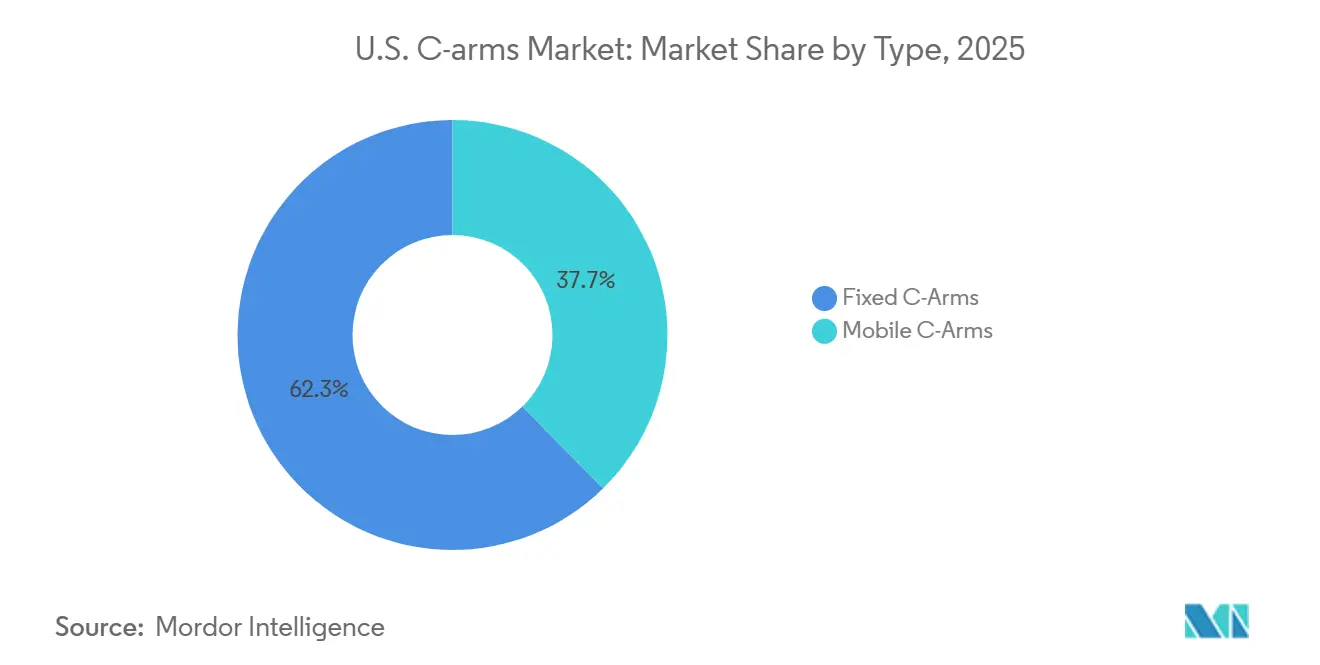

- By type, fixed C-arms held 62.35% of the U.S. C-arms market share in 2025, while mobile C-arms are projected to expand at a 5.98% CAGR through 2031.

- By application, orthopedics and trauma accounted for 29.55% of the U.S. C-arms market size in 2025, while neurology is forecasted to grow at a 5.76% CAGR through 2031.

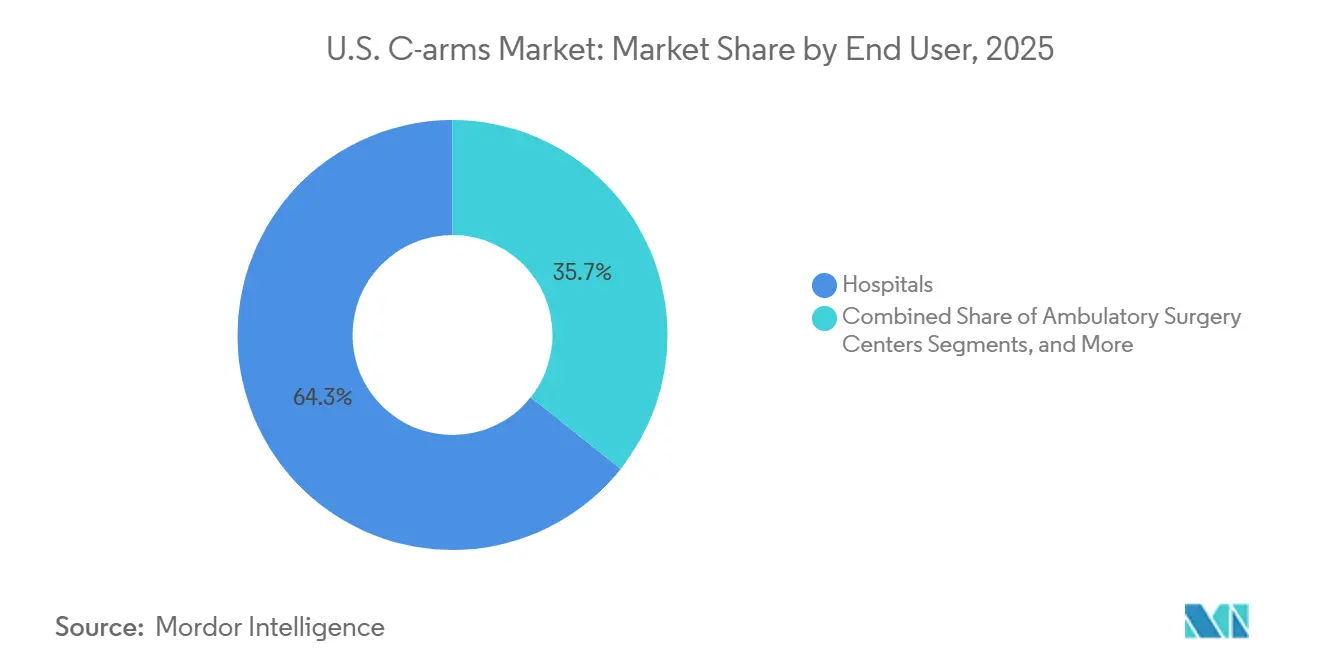

- By end user, hospitals captured 64.34% of the U.S. C-arms market size in 2025, while ambulatory surgery centers are projected to grow at a 6.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. C-arms Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding ambulatory and outpatient procedural volumes | +1.2% | National, with concentration in urban and Sun Belt ASC clusters | Short term (≤ 2 years) |

| Rising U.S. orthopedic and trauma imaging demand | +1.0% | National, with high-volume gains in trauma centers in Southern and Midwestern states | Medium term (2-4 years) |

| Faster adoption of mobile c-arms in hybrid and same-day settings | +0.8% | National, with early gains in metropolitan ASC corridors | Short term (≤ 2 years) |

| Workflow improvements from low-dose and flat-panel imaging upgrades | +0.6% | National | Medium term (2-4 years) |

| Growing use in pain management and image-guided interventions | +0.5% | National, with high concentration in Southeast and Southwest chronic pain markets | Short term (≤ 2 years) |

| Replacement demand from installed base aging in hospitals and surgery centers | +0.4% | National, with earlier replacement cycles in high-volume Northeast and Midwest hospital systems | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Ambulatory and Outpatient Procedural Volumes

The shift of surgical cases from hospital operating rooms to ambulatory care is driving demand in the United States C-arms market. CMS expanded the ASC-covered procedure list by 37 procedures in 2024 and 21 more in 2025, increasing cases requiring fluoroscopic imaging in outpatient settings, such as shoulder and ankle reconstructions and endovascular filter retrievals.[1]American Joint Replacement Registry, “2025 Annual Report,” American Joint Replacement Registry, fs1.hubspotusercontent-na1.net Many of these procedures need intraoperative visualization, and outpatient operators seek systems that meet this demand without requiring fixed imaging rooms. MedPAC reported that moving cases to ASCs reduces patient costs by USD 684 per procedure, further supporting this migration and boosting demand for compact, efficient C-arm systems.

Rising U.S. Orthopedic and Trauma Imaging Demand

Orthopedic and trauma care remain key drivers of the United States C-arms market due to their reliance on real-time imaging for procedures like fracture fixation and spinal work. The American Joint Replacement Registry’s 2025 report reviewed 4.4 million procedures, with primary total knee arthroplasties accounting for 51.2% and total hip arthroplasties for 32.4%. Outpatient trends are evident, with 72% of knee replacements performed in outpatient settings by 2024.[2]Medicare Payment Advisory Commission, “Ambulatory Surgical Center Services Status Report,” Report to the Congress, medpac.gov MedPAC noted a 33% rise in Medicare total knee arthroplasties and a 34% increase in hip arthroplasties at ASCs, highlighting the growing need for mobile imaging solutions in these settings.[3]Medicare Payment Advisory Commission, “Ambulatory Surgical Center Services Status Report,” Report to the Congress, medpac.gov

Faster Adoption of Mobile C-Arms in Hybrid and Same-Day Settings

Mobile C-arms are gaining traction as hospitals and outpatient facilities prioritize compact systems that fit smaller spaces, reduce manual movement, and ensure efficient turnover. Siemens Healthineers introduced CIARTIC Move in 2024, a self-driving mobile C-arm with automated repositioning for 2D fluoroscopy and 3D cone-beam CT workflows. GE HealthCare followed with Allia Moveo in 2026, featuring a cable-free design and AI-supported SmartMove positioning. GE HealthCare highlighted that nearly 50% of interventional procedures face equipment access challenges, driving demand for automated, mobile platforms in same-day and hybrid surgical environments.

Workflow Improvements from Low-Dose and Flat-Panel Imaging Upgrades

The transition from image-intensifier systems to flat-panel detector platforms is accelerating in the United States C-arms market. Buyers seek systems offering consistent imaging, streamlined workflows, and enhanced dose monitoring to meet regulatory standards. The FDA’s 2024 guidance on radiation control emphasized compliance in system upgrades. Shimadzu launched the SC15 in 2026, featuring a high-resolution flat-panel detector and a 43-inch LCD monitor for orthopedic surgery and pain management. These advancements in workflow, dose visibility, and image quality are driving a steady replacement cycle, even amid tight budgets.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital cost and financing scrutiny | -0.8% | National, with greater pressure on community hospitals and rural facilities | Medium term (2-4 years) |

| Radiation safety compliance burden | -0.4% | National | Short term (≤ 2 years) |

| Staff training and positioning complexity | -0.3% | National, with greater impact in high-volume ASCs with lean staffing models | Medium term (2-4 years) |

| Slow replacement cycles in budget-constrained facilities | -0.2% | National, with higher impact in rural and safety-net hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Financing Scrutiny

Capital spending remains a key restraint in the United States C-arms market, particularly for community hospitals, independent centers, and smaller facilities. Buyers evaluate not only scanner prices but also service commitments, software upgrades, room readiness, and training needs. Mobile and fixed fluoroscopy systems compete for capital with robotic surgery systems and digital record investments, leading some providers to extend the use of older image-intensifier units despite the benefits of newer flat-panel systems. Group purchasing agreements ease some financial pressure, but financing scrutiny delays orders when facilities anticipate slow returns from productivity or procedural growth.

Radiation Safety Compliance Burden

Radiation safety requirements create additional challenges for the United States C-arms market, as facilities must address more than hardware acquisition. Providers are responsible for documenting doses, maintaining protective practices, and training staff in fluoroscopy use. This burden is more evident in Ambulatory Surgical Centers (ASCs), where imaging is critical but radiation safety infrastructure is limited. Staff must master pulsed fluoroscopy settings, positioning techniques, and shielding practices to avoid repeat exposures and workflow delays. While these requirements do not hinder market growth, they slow adoption in facilities lacking dedicated imaging support teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fixed Platforms Anchor Revenue, Mobile Systems Set the Pace

In 2025, fixed C-arms accounted for 62.35% of revenue, maintaining their dominance in the United States C-arms market. Their usage is concentrated in catheterization labs, hybrid operating rooms, and interventional suites, where large-field imaging and workflow stability are prioritized over mobility. Although their growth is slower than mobile platforms, fixed systems benefit from replacement cycles as hospitals upgrade from analog to digital flat-panel units to meet modern dose management standards. The FDA's performance standard under 21 CFR 1020.32 further drives this replacement trend.

Mobile C-arms are projected to grow at a 5.98% CAGR through 2031, making them the fastest-growing platform in the United States C-arms market. Their demand is fueled by hospitals, ASCs, and multi-specialty centers seeking flexible intraoperative imaging solutions without permanent infrastructure. Siemens Healthineers advanced this segment with the CIARTIC Move, which automates positioning and improves operating room efficiency. The mini C-arm niche, catering to extremity orthopedics and point-of-care needs, is also expanding, as demonstrated by Turner Imaging Systems' 500th SMART-C installation and 67% sales growth in April 2026.

By Application: Orthopedics Leads Usage, Neurology Builds Faster Momentum

Orthopedics and trauma contributed 29.55% of revenue in 2025, remaining the largest application in the United States C-arms market. This reflects the consistent need for fluoroscopic guidance in fracture repairs, joint procedures, and spine-related workflows. Joint reconstruction plays a significant role, with 4,434,668 procedures reported through 2024, primarily knee and hip replacements. The shift to outpatient settings further supports demand, with ASC knee arthroplasty volume growing 33% and hip arthroplasty volume increasing 34% in one year.

Neurology is expected to grow at a 5.76% CAGR through 2031, outpacing other applications in the United States C-arms market. This growth is driven by the need for precise fluoroscopic support in spine procedures, neurointerventional cases, and pain treatments. Cone-beam CT and 3D guidance features are gaining traction, offering enhanced intraoperative visualization without requiring separate navigation platforms. Cardiology and gastroenterology remain secondary applications, supported by expanding outpatient approvals and procedural flexibility.

By End User: Hospitals Lead Spending, ASCs Add the Fastest Growth

Hospitals accounted for 64.34% of end-user revenue in 2025, making them the largest buyers in the United States C-arms market. This dominance is due to the concentration of fixed systems in catheterization and hybrid rooms and extensive mobile system fleets in orthopedic, trauma, and interventional departments. Structured capital plans and compliance requirements drive hospital purchases, with older systems often replaced to meet modern digital workflow and dose visibility standards. Hospitals remain the volume center of the market despite slower growth rates.

Ambulatory surgery centers are projected to grow at a 6.45% CAGR through 2031, making them the fastest-growing end-user segment in the United States C-arms market. CMS policy expanded the ASC procedure list in 2024 and 2025, increasing fluoroscopy-linked procedures in this setting. ASCs prefer compact, mobile systems with simpler setups and faster positioning to enhance turnover and efficiency. Specialty clinics and office-based settings further contribute to demand by expanding access to fluoroscopy in previously underserved environments.

Geography Analysis

The United States C-arms market exhibits regional demand variations due to differences in procedure volume, care settings, and facility density. Sun Belt and Mountain West states, such as Texas, Florida, Arizona, and Georgia, are key demand centers driven by population growth, outpatient capacity expansion, and strong case volumes in musculoskeletal and cardiovascular care. California, New York, and Florida also lead in orthopedic procedure volumes, as highlighted in the AJRR 2025 Annual Report, sustaining high fluoroscopy demand. Replacement and upgrade activities are strongest in regions with established outpatient growth and orthopedic intensity.

The Northeast and Great Lakes corridor remains a significant market for fixed C-arms, supported by large academic institutions and urban hospitals managing complex cardiovascular, vascular, and neurointerventional procedures. These facilities prioritize premium imaging systems due to procedure complexity, staffing efficiency, and dose documentation needs, despite disciplined procurement cycles. The installation of GE HealthCare’s Allia Moveo at Baylor St. Luke’s Medical Center in Houston in February 2026 demonstrates that advanced deployments are not limited to coastal academic centers.

Rural and smaller community markets in the United States follow a different demand pattern, focusing on essential replacements rather than expansions. Facilities in these areas often delay upgrades until operational challenges with older systems become critical. When purchasing, they prefer compact mobile platforms and lower-footprint systems, which align better with their operational needs. This creates a dual-speed market where metropolitan systems drive early adoption, while smaller markets extend replacement cycles and make selective purchases.

Competitive Landscape

The United States C-arms market is moderately concentrated, with GE HealthCare, Koninklijke Philips N.V., and Siemens Healthineers leading in full-size fixed and mobile systems. Their stronghold is attributed to extensive installed bases, robust service networks, and long-term contracts with U.S. health systems. Competition now focuses on workflow automation, positioning support, dose intelligence, and user-friendly software. GE HealthCare advanced its position with Allia Moveo, which received FDA 510(k) clearance in February 2026, featuring a compact cable-free design and advanced interventional suite functionalities. Siemens Healthineers introduced CIARTIC Move, incorporating self-driving positioning and procedure-based movement patterns into mobile C-arms.

Philips strengthened its position in the United States C-arms market with the Zenition 90 Motorized, which received FDA 510(k) clearance in June 2024. Clinical studies reported a 97% time-saving through automated vascular outlining, reflecting the industry's emphasis on efficiency alongside image quality. While these top-tier players dominate premium full-size systems, competition thrives in niche segments where installation needs, portability, and cost sensitivity are critical. Shimadzu’s SC15, launched in April 2026, targeted orthopedic surgery, pain management, and dialysis access angioplasty, focusing on specific applications rather than broad portfolios.

Orthoscan maintains a strong position in mini C-arms, leveraging its FDA-cleared VERSA platform to compete on portability and specialized use cases. Turner Imaging Systems is gaining momentum in the ultra-portable segment with SMART-C, which is increasingly adopted in orthopedic clinics, sports medicine, and other point-of-care environments. The market also sees opportunities in rural replacements, compact mobile imaging, and software-driven 2D and 3D workflows that reduce reliance on separate navigation tools. While large vendors lead the United States C-arms market, specialized players continue to address specific workflow challenges effectively.

U.S. C-arms Industry Leaders

GE Healthcare

Koninklijke Philips N.V.

Siemens Healthineers AG

Canon Medical Systems Corporation

Hologic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Shimadzu Corporation launched the SC15 mobile C-arm in the U.S., featuring advanced imaging capabilities for orthopedic surgeries, pain management, and dialysis access angioplasty.

- April 2026: Turner Imaging Systems achieved the 500th installation of its SMART-C mini C-arm, reporting a 67% sales growth and its first deployment with LA Galaxy.

- February 2026: GE HealthCare received FDA clearance for Allia Moveo, integrating advanced imaging features in a compact, cable-free design, with its first U.S. installation at Baylor St. Luke's Medical Center.

U.S. C-arms Market Report Scope

As per the scope of the report, a C-arm is a mobile, advanced X-ray imaging device used primarily in operating rooms and interventional suites. Named for its C-shaped arm, it connects an X-ray source on one end to a detector on the other, allowing clinicians to rotate the equipment freely around the patient to capture real-time, high-resolution fluoroscopic images from multiple angles.

The U.S. C-arms market is segmented by type, application, and end-user. By type, the market includes fixed C-arms and mobile C-arms. By application, the market is segmented into cardiology, gastroenterology, neurology, orthopedics and trauma, radiology and oncology, and other applications. By end-user, the market is categorized into hospitals, ambulatory surgery centers, specialty clinics, and other end users. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Fixed C-Arms | |

| Mobile C-Arms | Full-Size C-Arms |

| Mini C-Arms |

| Cardiology |

| Gastroenterology |

| Neurology |

| Orthopedics and Trauma |

| Radiology and Oncology |

| Other Applications |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics |

| Other End Users |

| By Type | Fixed C-Arms | |

| Mobile C-Arms | Full-Size C-Arms | |

| Mini C-Arms | ||

| By Application | Cardiology | |

| Gastroenterology | ||

| Neurology | ||

| Orthopedics and Trauma | ||

| Radiology and Oncology | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty Clinics | ||

| Other End Users | ||

Key Questions Answered in the Report

What is the projected value of U.S. C-arms by 2031?

The U.S. C-arms market is forecast to reach USD 1.05 billion by 2031 from USD 0.83 billion in 2026, with a CAGR of 4.75% over 2026-2031.

Which type is growing faster in the United States?

Mobile C-arms are growing faster, with a projected 5.98% CAGR through 2031, while fixed systems still held the larger 62.35% revenue share in 2025.

Why are ambulatory surgery centers becoming more important for C-arms demand?

ASCs are the fastest-growing end-user group at a 6.45% CAGR through 2031, supported by CMS additions of 37 procedures in 2024 and 21 in 2025 to the ASC-covered list.

Which application area currently leads equipment usage?

Orthopedics and trauma led with 29.55% revenue share in 2025 because these procedures rely heavily on real-time fluoroscopic guidance during fixation, arthroplasty, and spine-related work.

What is pushing hospitals and surgery centers to replace older systems?

Replacement demand is being driven by the move toward flat-panel detector systems, stronger workflow expectations, and the need to align with current FDA radiation control requirements.

Which companies are shaping the competitive environment the most?

GE HealthCare, Philips, and Siemens Healthineers remain the main full-size system leaders, while Orthoscan, Turner Imaging Systems, and Shimadzu are gaining ground in targeted niches such as mini and compact mobile systems.

Page last updated on: