Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

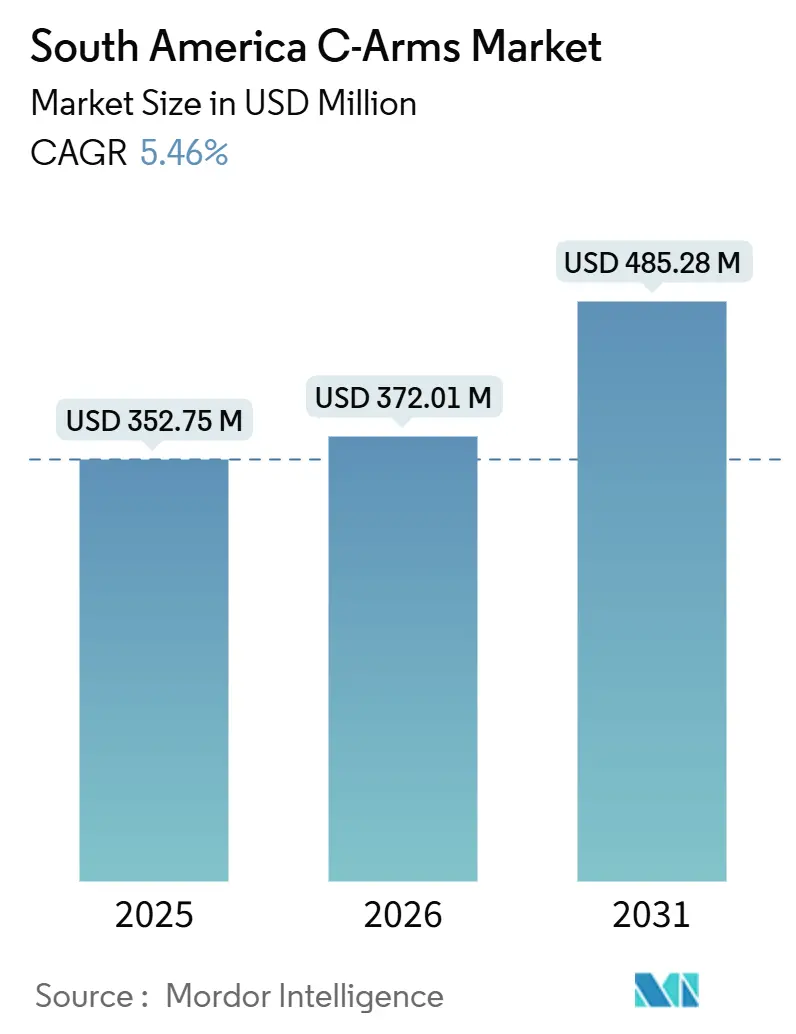

| Base Year Market Size (2025) | USD 352.75 Million |

| Market Size (2026) | USD 372.01 Million |

| Market Size (2031) | USD 485.28 Million |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America C-Arms Market Analysis by Mordor Intelligence

The South America C-Arms Market size is expected to increase from USD 352.75 million in 2025 to USD 372.01 million in 2026 and reach USD 485.28 million by 2031, growing at a CAGR of 5.46% over 2026-2031.

Currency fluctuations, an aging population, and a persistent backlog in elective surgeries are shaping growth trajectories. Simultaneously, supply-side challenges, such as technologist shortages and import price volatility, are slowing the pace of equipment replacement cycles. In São Paulo and Buenos Aires, large tertiary hospitals and hybrid operating rooms primarily rely on fixed systems. Conversely, mobile units are gaining traction in ambulatory surgical centers emerging across Brazil's interior and secondary cities in Colombia. The adoption of flat-panel detectors is accelerating as regulatory authorities, including ANVISA and ANMAT, enforce stricter dose-monitoring regulations, reducing the appeal of image intensifiers. The competitive landscape remains moderately concentrated, with four major global players accounting for approximately 60% of the installed-base value through bundled service contracts. However, Chinese competitors are increasingly capturing market share by offering lower prices and maintenance services, particularly in Peru and Colombia.

Key Report Takeaways

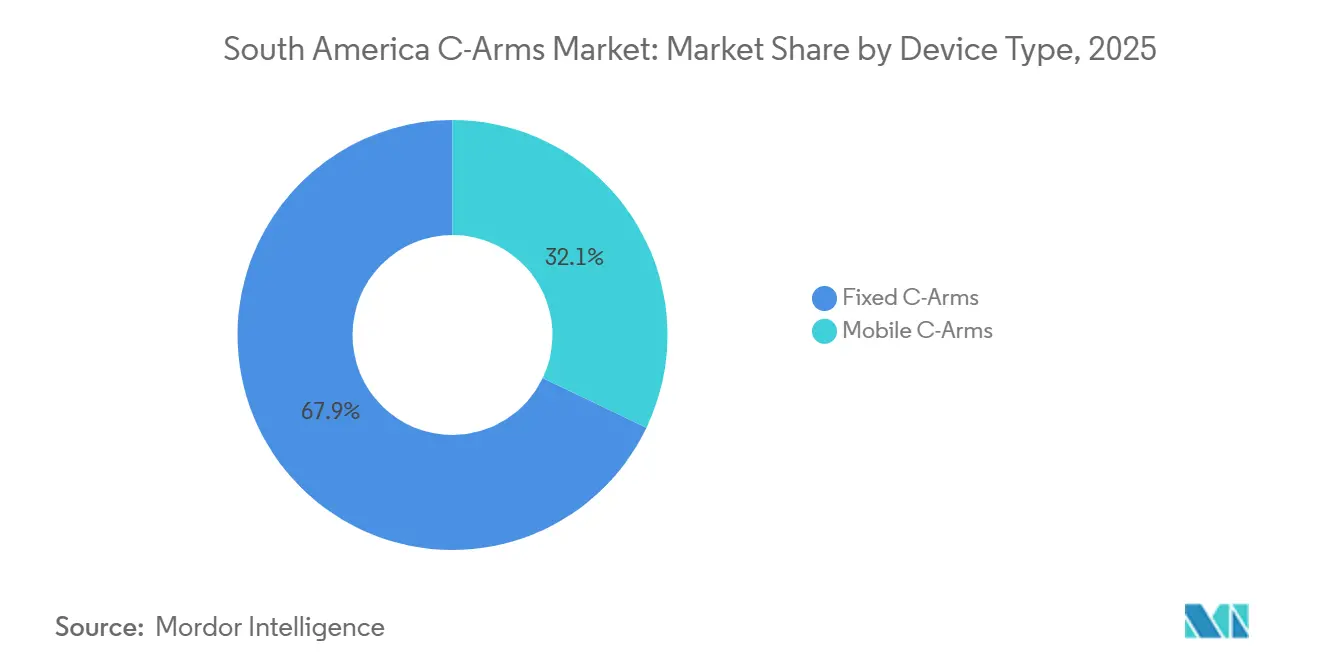

- By device type, fixed C-Arms led with 67.91% of the South America C Arms market share in 2025; mobile systems are projected to expand at a 5.82% CAGR to 2031.

- By detector technology, flat-panel detectors accounted for 63.02% share of the South America C Arms market size in 2025 and are advancing at a 5.65% CAGR through 2031.

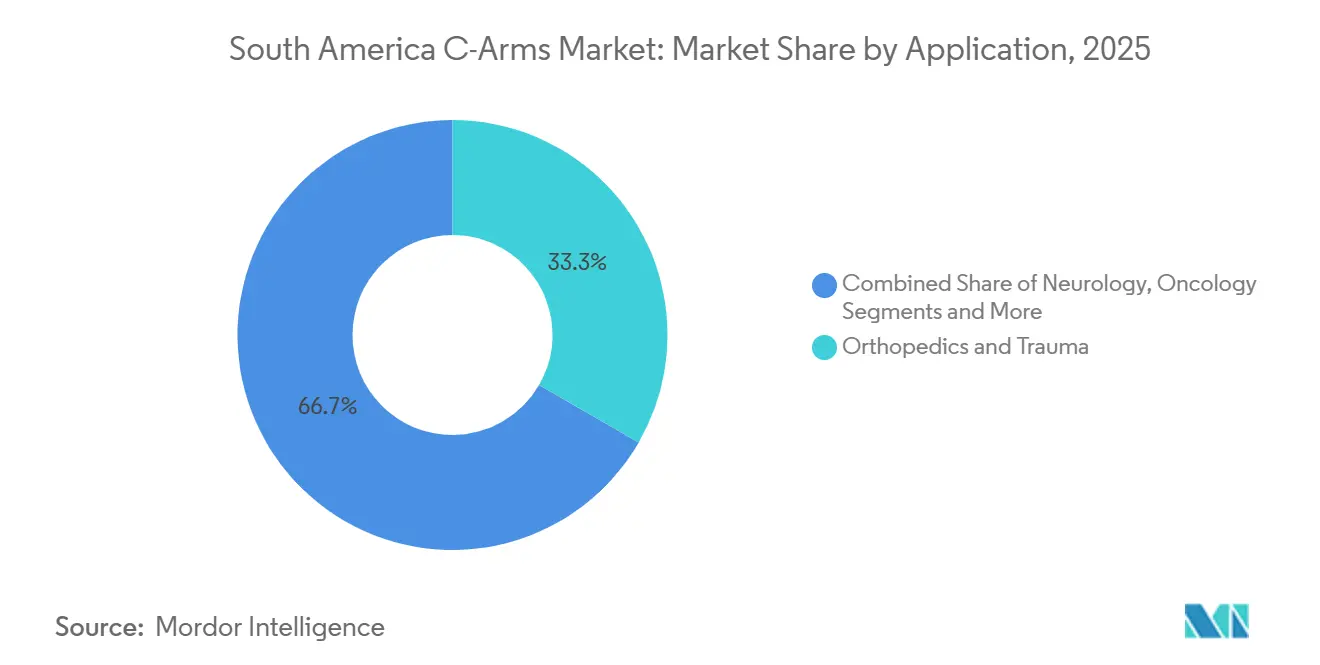

- By application, orthopedics & trauma accounted for 33.34% of the revenue share in 2025, while neurology posted the fastest-growing CAGR of 6.01% through 2031.

- By end user, hospitals held 71.56% of the South America C Arms market share in 2025; ambulatory surgical centers recorded the highest projected CAGR at 5.73% through 2031.

- By geography, Brazil dominated with 51.87% share of the South America C Arms market size in 2025, whereas Argentina is forecast to grow at 5.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America C-Arms Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising geriatric population and chronic disease burden | +0.9% | Brazil, Argentina, Chile urban centers | Long term (≥ 4 years) |

| Adoption of minimally invasive, image-guided surgeries | +1.1% | Brazil, Colombia, Argentina tier-1 cities | Medium term (2-4 years) |

| Technological advances in flat-panel and 3D imaging | +0.8% | Global, early uptake in Brazil and Chile private hospitals | Medium term (2-4 years) |

| Post-COVID backlog of elective surgeries | +0.7% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Expansion of ambulatory surgical centers | +0.6% | Interior São Paulo, Minas Gerais; Medellín, Cali | Medium term (2-4 years) |

| OEM financing and leasing models | +0.8% | Argentina, Peru, Colombia public sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population and Chronic Disease Burden

Colombia is expected to perform 39,270 arthroplasties annually by 2050, a 52.7% jump that will require more intra-operative imaging cycles.[2]Siemens Healthineers, “Siemens Healthineers launches CIARTIC Move,” siemens-healthineers.com Brazil recorded 202,940 traumatic amputations between 2008 and 2023, costing USD 54.87 million in yearly reimbursements, reinforcing continual capital outlays for high-throughput systems.[4]Projeções da População do Brasil e Unidades da Federação por Sexo e Idade: 2010-2060,” IBGE – Instituto Brasileiro de Geografia e Estatística, ibge.gov.br Between 2000 and 2023, Brazil experienced a significant increase in its population aged 60 and above, rising from 8.7% to 15.6%. This demographic shift has driven higher demand for image-guided procedures in orthopedics, vascular care, and oncology. Argentina and Chile, with similar aging trends and chronic disease prevalence, are also seeing increased utilization of fluoroscopy for stenting, vertebroplasty, and tumor ablation. Public imaging facilities in metropolitan Brazil are operating at 70-80% capacity, resulting in extended wait times and prompting insured patients to seek services at private clinics equipped with mobile C-arms. To address bed shortages and upgrade outdated systems, state authorities in São Paulo and Minas Gerais are co-investing in ambulatory surgical centers. Despite budget constraints, this mismatch between demographic needs and technological capabilities continues to sustain demand for medical equipment.

Adoption of Minimally Invasive, Image-Guided Surgeries

Minimally invasive spine procedures are expanding across South America, aided by regional training hubs in Bogotá that improve surgeon proficiency. In Brazil, bone-anchored hearing implant operations cut complication rates by 49% and operating times by half.[1]Leonardo Di Santana Cruz, “Minimally invasive surgery as a new clinical standard for bone anchored hearing implants—real-world data from 10 years of follow-up and 228 surgeries,” Frontiers in Surgery, frontiersin.org when performed with image-guided tools. Robotic thoracic programs now operate on 41 da Vinci systems concentrated in São Paulo and Rio de Janeiro, confirming hospital demand for real-time fluoroscopy that syncs with robotics. As more surgeries migrate to outpatient environments, the South America C Arms market benefits from compact, mobile platforms that dock easily into hybrid ORs, ensuring workflow continuity without permanent infrastructure changes.

Technological Advances in Flat-Panel and 3D Imaging

CMOS flat-panel detectors now deliver ≥30 fps at a 14-bit dynamic range, eliminating geometric distortions previously associated with image intensifiers. Advanced systems, such as Philips’ Azurion line, incorporate dose-tracking software to alert operators as exposure thresholds approach regulatory limits. GE’s OEC 3D systems generate volumetric datasets from 190-degree sweeps, enabling orthopedic teams to verify screw trajectories without requiring CT scans. Although flat-panel systems involve 40-50% higher upfront costs, their extended detector lifespan and reduced maintenance expenses make them cost-effective over time. This value proposition resonates strongly with Brazil’s private hospitals, where operating room efficiency directly impacts revenue.

Post-COVID Backlog of Elective Surgeries

Brazil canceled 828,429 elective surgeries between April and December 2020, creating a backlog that continues to strain orthopedic, cardiac, and oncology departments. Argentina experienced a 35% decline in surgeries during 2020-2021, further exacerbated by currency devaluation that delayed equipment imports. Colombia’s ambulatory centers absorbed some of the overflow but lacked sufficient flat-panel detectors to meet demand. Hospitals are now replacing decade-old image-intensifier units with flat-panel models to improve procedural efficiency, with a significant replacement wave anticipated between 2026 and 2027.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High acquisition and maintenance costs | -0.7% | Argentina, Peru, Colombia public networks | Medium term (2-4 years) |

| Shortage of skilled imaging technologists and surgeons | -0.5% | Interior Brazil, Peru, Colombia tier-2/3 cities | Long term (≥ 4 years) |

| Currency volatility impacting import pricing | -0.9% | Argentina, Brazil election cycles | Short term (≤ 2 years) |

| Growth of refurbished equipment channel | -0.6% | Peru, Colombia, Brazil public hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Maintenance Costs

Brazil imposes 20-60% tariffs on imported medical devices, escalating capital budgets for tertiary hospitals even after extended 60-day payment terms were introduced in 2024. Argentine peso devaluation deepens price uncertainty, compelling facilities to prioritize essential consumables over elective imaging upgrades. Flat-panel C-Arms range from USD 50,000 to USD 175,000, deterring smaller clinics that lack volume guarantees. Access inequities persist in Chile, where privately insured patients enjoy 2.8-times greater orthopedic surgery rates than their public counterparts, highlighting the affordability divide.

Shortage of Skilled Imaging Technologists and Surgeons

Brazil lacks an estimated 8,000-10,000 certified imaging technologists, a deficit most acute in northern and interior regions. Colombia’s 2024 workforce survey found that 35% of public hospitals lacked staff trained in advanced fluoroscopy protocols, resulting in utilization roughly 60% of potential. Peru fields fewer than 200 dual-certified technologists nationwide, choking neurovascular and cardiac programs. OEMs reply with AI-assisted positioning and simplified UIs, but those features raise system prices by another 10-15% and cannot fully bridge the competency gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Fixed Systems Anchor Hybrid ORs

Fixed systems held 67.91% of the South American C-Arms market share in 2025, driven by high-throughput trauma centers that demand ceiling-mounted stability and large detector sizes. Mobile platforms are, however, forecast to outpace at a 5.82% CAGR because outpatient units prize maneuverability for multi-disciplinary theater rosters. Siemens Healthineers’ autonomous CIARTIC Move, launched in 2024, reduces position setup time by half, underscoring why mobile innovation resonates at staff-constrained sites.

Implementation of cone-beam CT within mobile footprints is closing the capability gap with fixed fluoroscopy suites, allowing advanced trauma and spinal workflows in lower-acuity facilities. As refurbish-friendly regulations take hold in Brazil and Argentina, mini C-Arm adoption is accelerating among orthopedists treating extremity injuries in ambulatory settings. Continuous cross-pollination of software features across fixed and mobile lines blurs category boundaries, yet installation cost and theater configuration remain the dividing line for capital budgeting.

By Detector Technology: Flat-Panel Dominance Driven by Dose Mandates

Flat-panel detector systems, accounting for 63.02% of 2025 sales, are expected to grow at a 5.65% CAGR. The shift from image intensifiers is being driven by 2024 dose-tracking regulations in Brazil and similar mandates in Argentina. CMOS flat panels, with higher quantum efficiency, reduce exposure by 25-30% compared to amorphous-silicon alternatives. Image-intensifier tubes, which still represent about one-third of the installed base, face challenges such as limited availability of replacement parts and high costs ranging from USD 18,000 to 22,000 per tube. These factors make flat panels more cost-effective in terms of total ownership. Furthermore, trade-in programs offering up to 30% credit on legacy systems encourage faster adoption of flat panels. As public networks in South America introduce leasing options to avoid upfront payments, the market share of image-intensifier systems in the C-Arms segment is anticipated to decline steadily.

By Application: Neurology Interventions Outpace Orthopedics

Orthopedics & trauma accounted for 33.34% of the South America C Arms market in 2025, as fracture care and joint replacements dominate surgical lists across Brazil, Argentina, and Colombia.[3]Yesika Natali Fernández-Ortiz, “Lower Limb Arthroplasties in Colombia: Projections for 2050 Based on Official Records,” Epidemiologia, mdpi.com The South America C Arms market catering to orthopedics is expected to maintain its leadership. At the same time, neurology is forecast to post the fastest CAGR of 6.01%, driven by rising minimally invasive spine procedures and interventional pain blocks. Adoption of oblique and lateral 45-degree spinal views requires rapid, multi-angle fluoroscopy that image-intensifier units struggle to deliver, steering surgeons toward flat-panel C-Arms.

Cardiology remains a secondary consumer, yet hybrid OR build-outs in tertiary centers include floor-mounted C-Arms with cardiac presets for endovascular aneurysm repair. Gastroenterology and oncology leverage mobile units for ERCP and tumor ablation cases, illustrating the technology’s reach across specialties. Training programs such as the Cali-based minimally invasive surgery courses are broadening physicians' comfort with C-Arm navigation, thereby indirectly supporting diversification of applications.

By End-User: Hospitals Dominate, ASCs Accelerate

Hospitals accounted for 71.56% of South America's C Arms market share in 2025, driven by their role as referral hubs for complex trauma and neurological procedures. Ambulatory surgical centers, however, are growing at a 5.73% CAGR as insurers incentivize shorter stays, making compact mobile units critical for same-day throughput. Specialty orthopedic clinics use mini C-Arms for extremity work, while diagnostic imaging centers rarely purchase C-Arms unless bundled with vascular labs.

Rede D’Or’s near-term expansion of 5,200 beds illustrates continued hospital capital demand, yet the financing community is channeling favorable lease lines toward ASCs to spread fixed asset risk. Service contracts bundled into multiyear leases ensure uptime in resource-poor geographies, lowering perceived operational complexity for ASC investors.

Geography Analysis

In 2025, Brazil accounted for 51.87% of the regional revenue. With ANVISA's dose regulations driving detector upgrades and the expansion of ASCs (Ambulatory Surgical Centers) distributing imaging assets beyond São Paulo and Rio de Janeiro, Brazil is expected to align closely with the market-wide CAGR. Tier-2 cities like Campinas and Uberlândia are now granting licenses to ASCs at an annual rate of 12-15%. This trend not only complicates service network planning but also expands the potential market for maintenance contracts. Private chains are standardizing on Siemens and Philips platforms, while public networks are adopting usage-based leases. This approach converts capital expenditures (capex) into operational expenditures (opex), reducing risks associated with currency fluctuations.

Argentina, despite facing 211% inflation in 2023 and a 50% devaluation of the peso that December, is projected to achieve the region's fastest CAGR of 5.94%. Public hospitals in Argentina are increasingly opting for OEM leasing and deferred-payment plans denominated in U.S. dollars. This strategy mitigates foreign exchange risks and facilitates smoother budget approvals.

In 2024, Colombia expanded its ASC accreditation, enabling private operators in cities such as Medellín, Cali, and Barranquilla to deploy mobile C-arms for outpatient orthopedic procedures and pain management. Consequently, Colombia's share in the South American C-Arms market is expected to increase, as insurers incorporate orthopedic day surgeries into capitation models.

Peru and other regions in South America are experiencing slower growth due to infrastructure deficits and a shortage of technologists. However, the availability of refurbished imports is improving baseline access and creating future upgrade opportunities for OEMs, contingent on economic stabilization.

Competitive Landscape

Global multinationals dominate a moderately consolidated arena, where the top five players command the majority of the share, yet agile regional assemblers thrive under Brazil’s tariff preferences. Siemens Healthineers spearheads automation, rolling CIARTIC Move to cut manual maneuvering and doubling daily procedure capacity in pilot sites. GE HealthCare leverages AWS and NVIDIA alliances to embed generative AI and edge computing that automate positioning and dose settings, targeting facilities with chronic staffing gaps. Ziehm Imaging extended its Medtronic partnership to bundle navigation-ready C-Arms into spine centers, reflecting a pivot toward procedure-specific ecosystem selling.

Domestic assemblers in Brazil exploit local content rules to supply price-sensitive public tenders; however, they face technology lag as flat-panel components still rely on imported sub-assemblies. Strategic moves during 2024-2025 include OEM-bank finance programs that wrap service and training into predictable monthly outflows, lowering adoption barriers for mid-tier clinics. AI-assisted intra-operative 3D imaging and real-time anatomical segmentation are emerging as the next competitive battleground, with early proof points in the neurosurgical suites of São Paulo’s top private hospitals.

White-space opportunities center on autonomous systems that alleviate radiographer shortages, refurb-grade offerings for secondary hospitals, and fully integrated hybrid OR packages for consolidated health networks. Vendors differentiating through low-dose performance and wider isocentric clearance gain are gaining notable traction in orthopedic segments where patient BMI averages are rising.

South America C-Arms Industry Leaders

GE Healthcare

Ziehm Imaging GmbH

Canon Medical Systems Corporation

Koninklijke Philips NV

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE Healthcare unveiled the Revolution Vibe CT featuring AI-driven cardiac workflows to broaden advanced diagnostics access across South America.

- March 2025: GE Healthcare and NVIDIA announced a collaboration on autonomous X-ray and ultrasound platforms aimed at easing radiology staff shortages.

- February 2025: Siemens Healthineers posted Q1 FY 2025 imaging-segment growth of 7.6%, reflecting sustained global and regional demand for premium imaging solutions.

South America C-Arms Market Report Scope

As per the scope of the report, the C-arm is a medical imaging device that is based on X-ray technology and can be used in several diagnostic and interventional procedures. The South America C-arms market is segmented by type, application, end user, and geography. By type, the market is segmented into fixed C-arms and mobile C-arms (full-size C-arms and mini C-arms). By application, the market is segmented into cardiology, gastroenterology, neurology, orthopedics and trauma, oncology, and other applications. By end user, the market is segmented into hospitals, ambulatory surgical centers, and specialty clinics & diagnostic centers. By geography, the market is segmented into Brazil, Argentina, Chile, Colombia, Peru and the rest of South America. The report offers market size and forecasts in value (USD) for the above segments.

By Device Type

| Fixed C-Arms | |

| Mobile C-Arms | Full-Size C-Arms |

| Mini C-Arms |

By Detector Technology

| Image-Intensifier Systems |

| Flat-Panel Detector Systems |

By Application

| Cardiology |

| Gastroenterology |

| Neurology |

| Orthopedics & Trauma |

| Oncology |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty Clinics & Diagnostic Centres |

By Country

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Device Type | Fixed C-Arms | |

| Mobile C-Arms | Full-Size C-Arms | |

| Mini C-Arms | ||

| By Detector Technology | Image-Intensifier Systems | |

| Flat-Panel Detector Systems | ||

| By Application | Cardiology | |

| Gastroenterology | ||

| Neurology | ||

| Orthopedics & Trauma | ||

| Oncology | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Specialty Clinics & Diagnostic Centres | ||

| By Country | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the South America C-Arms market today and where is it heading?

It measured USD 372.01 million in 2026 and is projected to reach USD 485.28 million by 2031, growing at a 5.46% CAGR.

Which device type generates most revenue?

Fixed C-arms led with 67.91% of 2025 turnover, underpinned by cardiac cath labs and hybrid ORs.

What detector technology is gaining ground fastest?

Flat-panel systems, already 63.02% of 2025 sales, are expanding at a 5.65% CAGR thanks to new dose-monitoring rules.

Which clinical application will outpace others through 2031?

Neurology interventions are forecast to post the fastest 6.01% CAGR as stroke-center certifications spread.

Why are ambulatory surgical centers important to vendors?

ASCs are advancing at 5.73% CAGR, purchasing mobile and mini C-arms for outpatient orthopedics and pain management, creating a fresh revenue stream.

How concentrated is vendor competition?

The top four OEMs control roughly 60% of installed-base value, giving the market a moderate concentration score of 6.

Page last updated on: