Market Overview

| Study Period | 2020 - 2031 |

|---|---|

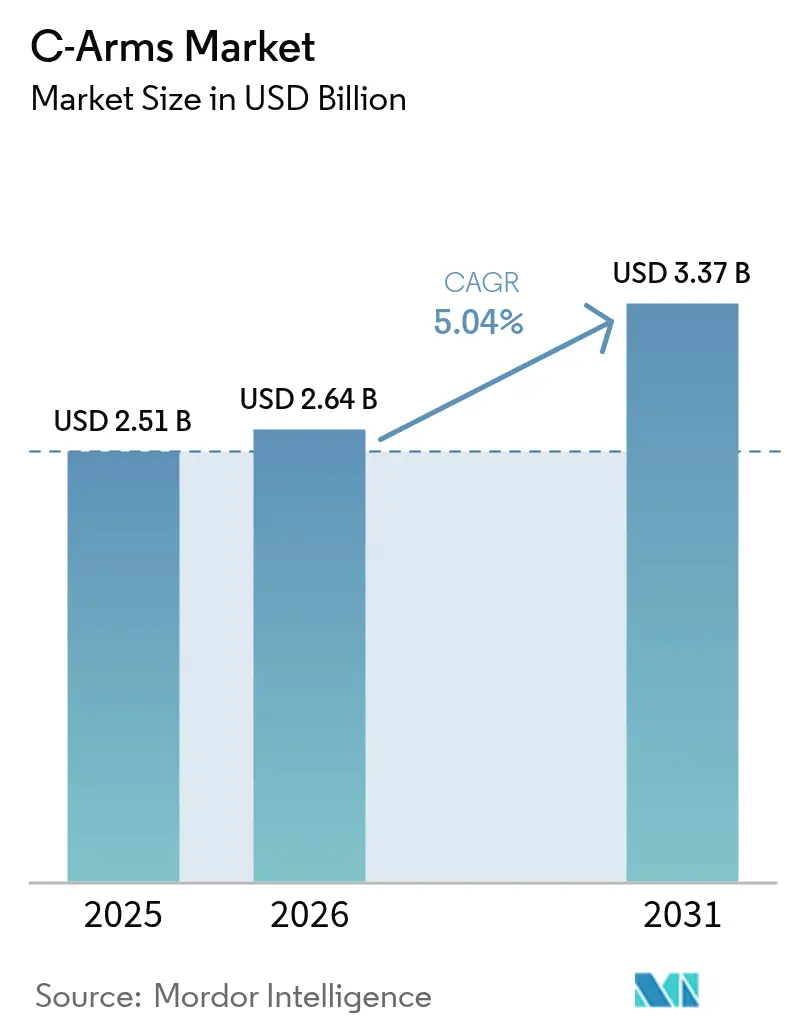

| Market Size (2026) | USD 2.64 Billion |

| Market Size (2031) | USD 3.37 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

C-Arms Market Analysis by Mordor Intelligence

The C-arms market size is expected to grow from USD 2.51 billion in 2025 to USD 2.64 billion in 2026 and is forecast to reach USD 3.37 billion by 2031 at 5.04% CAGR over 2026-2031. Demand accelerates as hospitals and ambulatory centers increase minimally invasive procedures, driving replacement cycles for flat-panel detector systems that lower dose while improving image quality. Rapid AI integration supports real-time navigation, which shortens operating times and broadens the range of complex interventions possible in outpatient suites. Vendors also gain from government incentives that favor site-neutral payments, while self-driving mobile units reduce labor constraints and open new workflow efficiencies. Supply-chain risk remains a cost headwind, yet service-oriented business models help providers finance upgrades without large upfront capital.

Key Report Takeaways

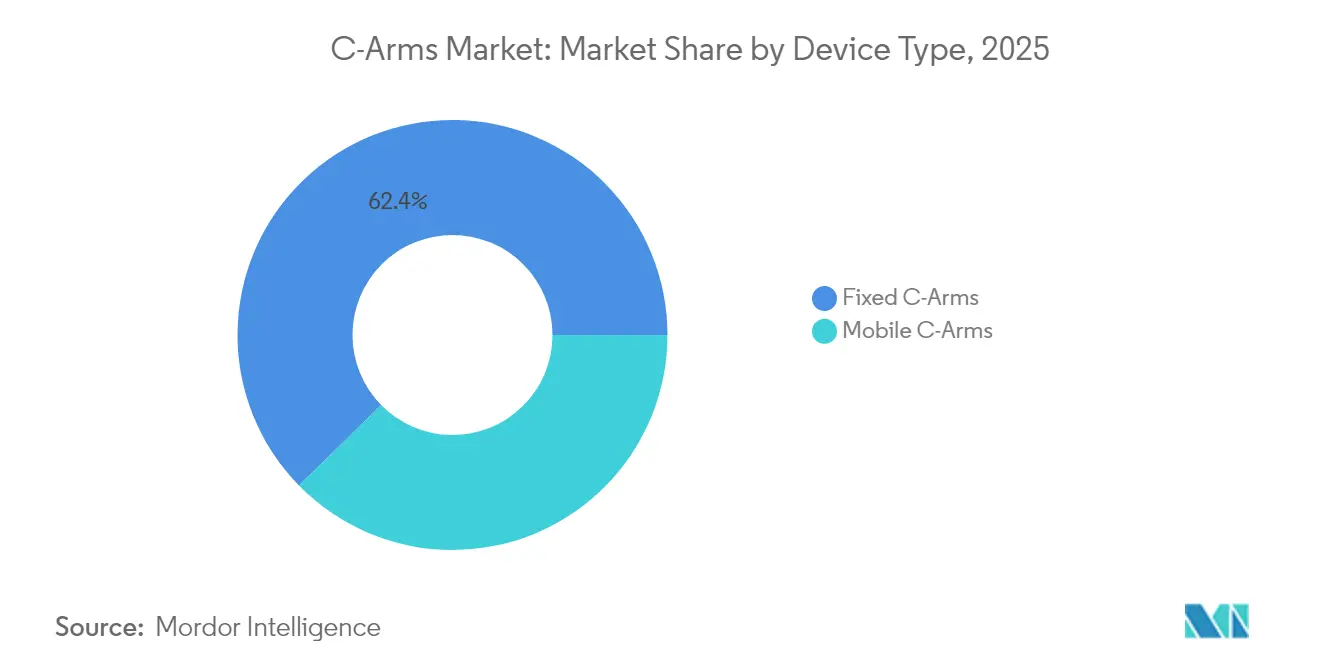

- By type, Fixed C-Arms captured 62.35% of the C-arms market share in 2025; Mobile C-Arms are projected to expand at the highest CAGR of 5.72% through 2031.

- By detector technology, Flat-Panel Detectors accounted for 57.74% share of the C-arms market size in 2025, and the segment is forecast to grow at the fastest pace of 5.56% CAGR to 2031.

- By application, Orthopedics & Trauma led with 29.55% revenue share in 2025, while Neurology is poised for the fastest 6.02% CAGR to 2031.

- By end-user, hospitals held 68.85% of revenue in 2025; ambulatory surgical centers showed the strongest 5.81% CAGR through 2031.

- By geography, North America commanded 35.12% of revenue in 2025, whereas Asia-Pacific is projected to log a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global C-Arms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Procedural shift toward minimally-invasive & image-guided surgery | +1.8% | Global, led by developed markets | Medium term (2-4 years) |

| Rising geriatric population & chronic disease burden | +1.2% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Strong demand for mobile systems in outpatient & ASC settings | +1.1% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Transition from image intensifiers to flat-panel detectors | +0.9% | Developed economies, expanding to emerging markets | Short term (≤ 2 years) |

| AI-enabled dose-optimization & navigation | +0.7% | Global, concentrated in developed markets | Medium term (2-4 years) |

| OEM discontinuation of image-intensifier production forces flat-panel upgrades | +0.5% | Global, acute in facilities with legacy systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Procedural shift toward minimally invasive and image-guided surgery

Minimally invasive interventions now account for a larger share of spinal, vascular, and pulmonary procedures, which places mobile C-arms at the center of intraoperative imaging workflows. Real-time 3D cone-beam CT and AI-guided navigation shorten fluoroscopy times and reduce radiation exposure for both staff and patients. Hospitals report lower post-operative complications[1]Endovascular Today, “Radial Neurointerventions Advance,” evtoday.com and shorter recovery windows, trends that improve cost effectiveness and encourage reimbursement agencies to reward image-guided approaches. The result is sustained demand for premium platforms capable of multi-plane reconstruction and automated positioning. Within advanced centers, self-driving C-arms slash setup intervals, enabling higher daily procedure counts. These workflow benefits reinforce a continuous upgrade cycle, especially as new software releases remain backward compatible with existing hardware.

Rising geriatric population and chronic disease burden

Population aging translates directly into higher volumes of orthopedic fracture repair, stroke thrombectomy, and cardiac electrophysiology, all of which depend on high-resolution fluoroscopy. Medicare spending on ambulatory surgical centers increased again in 2025 as procedure counts continued their double-digit climb[2]ASC Focus, “Outlook 2025: ASC Volume Growth,” ascfocus.org. Providers therefore choose systems with dose-tracking dashboards that safeguard elderly patients with lower bone density and comorbid conditions. Institutional planners schedule earlier equipment replacement to guarantee uptime, while service contracts now bundle detector recalibration and AI dose-optimization software. These actions magnify recurrent revenue opportunities for manufacturers and create a virtuous feedback loop that sustains the C-arms market.

Strong demand for mobile systems in outpatient and ASC settings

Ambulatory Surgical Centers perform procedures at less than half the cost of hospital outpatient departments and drive procurement toward maneuverable C-arms that can serve multiple rooms each day. Recent payment updates from the Centers for Medicare & Medicaid Services improved site-neutral reimbursements, further tilting the economic case in favor of ASC deployment. To exploit this shift, manufacturers offer compact footprints, battery power options, and intuitive user interfaces that reduce the need for a dedicated technologist. Accelerated learning curves also support same-day discharge protocols that are popular with patients. Together, these factors push the C-arms market into new outpatient niches such as office-based labs and pain management suites.

Transition from image intensifiers to flat-panel detectors

Original-equipment makers have phased out image intensifiers in most premium models, driving hospitals to adopt flat-panel systems that cut radiation and enable digital subtraction angiography without visible image lag. Complementary metal-oxide semiconductor (CMOS) sensors dominate the upper tier due to rapid readout speed and low noise, while indium gallium zinc oxide (IGZO) panels reduce cost for value-oriented buyers. Facilities still operating analog detectors plan upgrades within two budget cycles to comply with dose-monitoring statutes. This transition underpins a stable replacement pipeline that benefits vendors offering flexible financing. Continuous software updates further extend product life, enhancing total cost-of-ownership economics.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & lifecycle costs | -0.8% | Global, particularly affecting smaller facilities | Long term (≥ 4 years) |

| Expanding refurbished-equipment ecosystem | -0.6% | Emerging markets, cost-sensitive segments | Medium term (2-4 years) |

| Shortage of trained intra-operative imaging technologists | -0.4% | Global, acute in developed markets | Long term (≥ 4 years) |

| Semiconductor supply-chain risk for detector substrates | -0.3% | Global, concentrated in Asia-dependent supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High acquisition and lifecycle costs

Full-sized mobile units list between USD 100,000 and USD 150,000, while service contracts often add 15% of original price annually. Software licenses for 3D reconstruction or dose analytics impose additional recurring fees. Such expense can deter community hospitals that operate on thin capital budgets, leading them to extend replacement cycles beyond manufacturer recommendations. Providers also bundle equipment procurement within group purchasing contracts to extract volume discounts, yet upfront cash outlays remain significant. Deferred purchases weigh on order intake during macroeconomic downturns, which softens revenue visibility for suppliers.

Expanding refurbished-equipment ecosystem

A mature refurbishment network offers C-arms at 10–30% lower prices, making secondary sales attractive for start-up imaging centers and hospitals in lower-income regions. Refurbishers often include detector upgrades and limited warranties that mitigate perceived risk. Although these units broaden technology access, they can delay adoption of the latest AI navigation features, slowing top-line growth for original manufacturers. Vendors therefore market subscription software that can run on prior-generation hardware, aiming to capture revenue even when hardware sales shift to the secondary channel. Regulatory agencies also publish stricter refurbishment guidelines, yet compliance costs remain lower than new-build expenses, which preserves the pricing gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Mobile systems drive procedural flexibility

Fixed C-Arms retained 62.35% of revenue in 2025 because cardiac catheterization labs and hybrid operating rooms rely on ceiling-mounted gantries for high-acuity work. The segment still posts steady replacement as hospitals trade analog detectors for digital panels and add robotic tables that synchronize with X-ray motion. Mobile systems, however, record a stronger 5.72% CAGR to 2031 as outpatient migration accelerates. Self-propelled platforms now navigate corridors autonomously and dock at preset isocenters, which trims turnover time between cases. Compact models serve extremity orthopedics and pediatric trauma, while full-size mobiles handle vascular and spinal cases that require larger field of view. Leasing programs lower the barrier for ambulatory centers that prioritize quick payback. Consequently, the C-arms market gains breadth as mobile fleets multiply across metropolitan and rural regions.

Mobile systems also underpin the procedural expansion of stroke thrombectomy into community hospitals without fixed angio suites. Manufacturers integrate AI collision-avoidance and voice commands to reduce operator burden. Image quality approaches that of ceiling-mounted systems, closing the gap that once confined mobile units to basic fluoro tasks. With device prices trending lower and detector life extending, the C-arms market size for mobile platforms is projected to grow at 5.72% CAGR through 2031. Vendors that bundle training and remote diagnostics stand to capture annuity revenue, reinforcing the strategic importance of this segment.

By Detector Technology: Flat panels reshape premium demand

Flat-panel detectors accounted for 57.74% of revenue in 2025 and remain on a 5.56% CAGR path to 2031 as hospitals accelerate analog retirements. CMOS sensors dominate the upper tier, offering spatial resolution suited to neurovascular work and cardiac electrophysiology. IGZO panels close the performance gap at a lower price, making them popular in growth markets across Southeast Asia and Latin America. Amorphous-silicon arrays remain in value layers where image lag is acceptable, though their share erodes as costs fall elsewhere. Detector reliability now reaches 10-year service life, reassuring administrators wary of early pixel drop-out.

The shift improves clinical throughput because flat panels enable quick rotation between fluoroscopy and high-frame-rate acquisition without manual mode changes. Integrating 3D cone-beam CT on a single platform eliminates patient transfers to fixed imaging suites, improving safety. Vendors also activate deep-learning reconstruction that halves noise without increasing dose, a feature valued during pediatric procedures. As a result, the C-arms market continues moving toward digital uniformity. Flat-panel upgrades also drive service revenue from calibration and cybersecurity packages that ensure network compliance.

By Application: Neurology emerges as growth leader

Orthopedics & Trauma generated 29.55% of 2025 revenue by virtue of high fracture incidence and joint-replacement volumes that rely on real-time imaging. Procedures such as intramedullary nailing and vertebral augmentation require perpendicular projections that mobile units provide quickly. Yet Neurology posts the strongest 6.02% CAGR because stroke centers expand beyond tertiary hospitals into spoke facilities that need angiographic capability. AI-assisted road-mapping shortens clot retrieval time, a metric closely tracked in national quality registries. Mobile 3D spin also supports minimally invasive spinal decompression conducted in outpatient theaters.

Cardiology continues to migrate select electrophysiology cases to mobile imaging, especially when integrated with electro-anatomical mapping for atrial fibrillation ablation. Gastroenterology leverages low-dose fluoro during endoscopic retrograde cholangiopancreatography, while Pain Management grows with radiofrequency ablation for chronic back pain. Oncology benefits from percutaneous microwave ablation that depends on cone-beam CT guidance. Application diversity solidifies C-arm relevance across specialties, reinforcing vendor strategies that offer modular software tailored to each clinical line.

By End-User: ASCs accelerate outpatient migration

Hospitals held 68.85% of revenue in 2025, owing to large installed bases and the breadth of complex cases performed. Nonetheless, Ambulatory Surgical Centers outpace other channels with a 5.81% CAGR because site-neutral payments have narrowed reimbursement gaps. ASCs focus on high-throughput orthopedics, pain management, and vascular procedures, all of which benefit from quick setup and small operating rooms. Mobile C-arms with intuitive touchscreen interfaces allow nurses to cross-train, countering the shortage of specialized technologists.

Specialty clinics also invest as surgeons shift partial knee arthroplasty and carpal tunnel release to office settings. Financing models that wrap equipment, maintenance, and software into a monthly fee match the cash-flow profile of small practices. As a result, the C-arms market sees deeper penetration into secondary cities where hospital access is limited. Vendors cultivate loyalty by offering cloud analytics that benchmark radiation dose and room utilization, data that help centers negotiate payer contracts.

Geography Analysis

North America maintained 35.12% of revenue in 2025 and is forecast to expand at a 4.49% CAGR to 2031. Hospitals replace aging analog units and add mobile fleets to accommodate growing orthopedic and spine caseloads. Tariff-related component costs lifted the average selling price in 2025, yet vendors partially offset this burden through service bundles and performance-based payment schedules. Ambulatory Surgical Centers add dual-panel systems to support same-day discharge protocols for complex spine surgery. Government incentives for rural hospital modernization open opportunities for compact mobiles that fit small operating rooms.

Asia-Pacific is the fastest-growing region with a 6.05% CAGR through 2031, fueled by infrastructure investments and rising insurance coverage. Large urban hospitals in China replace analog labs with digital systems to meet new quality accreditation standards. Domestic manufacturers capture share in the mid-tier, yet GE, Siemens, and Philips still dominate the premium segment. India’s public-private partnership hospitals procure mobile C-arms for trauma and orthopedic centers that support a rising volume of road-accident cases. Southeast Asian nations leverage medical-tourism demand to justify high-specification imaging suites. Japan’s mature installed base focuses on AI upgrades and radiation-dose analytics. Collectively, these trends expand the C-arms market size in the region while diversifying the competitive field.

Europe follows a 4.74% CAGR path as public systems allocate capital toward dose-reduction technology aligned with the latest Council Directive on radiation safety. Hybrid operating rooms gain funding through cross-disciplinary projects, driving demand for ceiling-mounted units with 3D capabilities. Several countries expand national stroke networks, which boosts neurovascular imaging installations. The European market also benefits from rigorous cybersecurity directives that favor vendors offering secure connectivity. The Middle East & Africa records a moderate CAGR as governments invest in specialty care hubs and medical-tourism corridors. Saudi Arabia’s Vision 2030 allocates capital for orthopedic centers that require advanced imaging. South America also sees moderate CAGR buoyed by economic stabilization and growth in private health plans. Brazil leads regional volume because orthopedic surgeons adopt outpatient joint-replacement pathways that rely on mobile units with navigation software.

Competitive Landscape

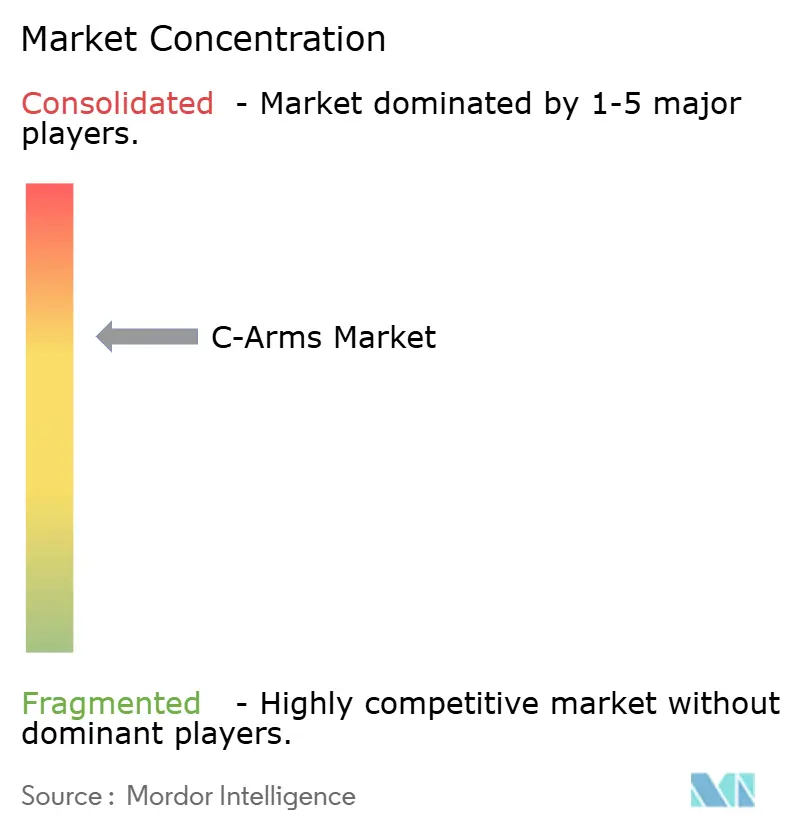

The C-arms market exhibits moderate concentration. GE HealthCare, Siemens Healthineers, and Philips together account for a majority of premium-segment shipments, yet specialty and regional manufacturers carve out share in value tiers. GE HealthCare focuses on AI-enabled workflow, acquiring MIM Software for imaging analytics and Intelligent Ultrasound’s AI group for automated measurement tools. The company also announced a seven-year Care Alliance with Sutter Health that covers more than 300 facilities, highlighting a move from transactional sales toward integrated service partnerships.

Siemens Healthineers emphasizes automation, with the Ciartic Move self-driving C-arm demonstrating a 50% reduction in imaging time during spine and pelvic surgeries. The feature set includes lidar-based navigation, collision avoidance, and automatic trajectory alignment, all of which cut staff workload. Service contracts bundle remote diagnostics and predictive maintenance, locking in recurring revenue. Philips invests in AI image enhancement across its Zenition platform, securing FDA clearance for the Zenition 30 mobile unit that offers table-side controls and workflow personalization.

Regional players in Asia and Latin America compete on price and after-sales support. Some partner with detector suppliers to integrate IGZO panels that offer acceptable performance at lower cost. Software-only entrants target dose analytics and post-processing, integrating their applications onto vendor-neutral hardware. The competitive battleground increasingly revolves around clinical productivity, user experience, and ecosystem connectivity rather than raw image metrics. Vendors that package hardware, software, and managed-service contracts gain strategic advantage as providers seek predictable operating budgets.

C-Arms Industry Leaders

Canon Medical Systems Corporation

GE Healthcare

Koninklijke Philips N.V.

Siemens Healthineers AG

Ziehm Imaging GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare completed acquisition of the remaining 50% stake in Nihon Medi-Physics, expanding its presence in Japan’s USD 7 billion molecular-imaging market.

- January 2025: GE HealthCare and Sutter Health announced a seven-year Care Alliance covering more than 300 facilities with AI-powered imaging solutions.

- October 2024: Radon Medical Imaging acquired Alpha Imaging, extending cardiovascular and interventional equipment distribution across 24 U.S. states.

- April 2024: Philips received FDA 510(k) clearance for the Zenition 30 mobile C-arm featuring enhanced flexibility and reduced reliance on support personnel.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the C-arms market as all newly manufactured, X-ray-based C-shaped fluoroscopy systems, fixed or mobile, full-size or mini, that provide real-time imaging for surgical, orthopedic, cardiovascular, neurological, and emergency procedures across hospitals and ambulatory centers. According to Mordor Intelligence, the review spans five regions and the period 2019-2030.

We clarify that refurbished units, standalone fluoroscopic tables, hybrid-OR infrastructure, and related service contracts sit outside our scope.

Segmentation Overview

- By Device Type

- Fixed C-Arms

- Mobile C-Arms

- Full-size

- Mini

- By Detector Technology

- Image Intensifier

- Flat-Panel Detector

- a-Si

- IGZO

- CMOS

- By Application

- Orthopedics & Trauma

- Cardiology

- Gastroenterology

- Neurology

- Oncology

- Pain Management & Vascular

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty & Orthopedic Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with radiology chiefs, biomedical engineers, and procurement leads across North America, Europe, Asia-Pacific, and Latin America. These discussions clarified replacement intervals, price spreads between detector technologies, and mobility preferences, letting us validate and refine assumptions.

Desk Research

We began with hospital-equipment censuses from the American Hospital Association, Eurostat device counts, and UN Comtrade import codes, benchmarking unit flows. Procedure volumes were drawn from OECD Health Data, the Australian Institute of Health and Welfare, and India's National Health Portal, while US FDA 510(k) and EU MDR filings revealed product launches driving replacement waves. Company filings, investor decks, peer-reviewed journals, plus paid datasets such as Dow Jones Factiva and D&B Hoovers helped us size revenues. The sources named are illustrative; numerous others informed data checks.

Market-Sizing & Forecasting

A top-down procedure-pool build converted global surgery counts into potential imaging demand, which we then adjusted by penetration rates and renewal ratios. Selective bottom-up supplier roll-ups served as reality checks. Key inputs include elective orthopedic surgery volumes, geriatric population growth, average selling prices by detector type, radiation-dose caps, and private-hospital capital budgets. Multivariate regression projected these drivers to 2030, with scenario buffers for regulatory or reimbursement shocks. Only after cross-checks satisfied consensus did the model exit calibration, giving us the 2025 baseline.

Data Validation & Update Cycle

We run anomaly screens against import data and hospital-capex signals, and any variance triggers re-checks before sign-off. Models refresh each year, with interim tweaks for material events. A fresh analyst pass precedes every delivery so clients receive the latest view.

Why Mordor's C-Arms Baseline Commands Confidence

Published estimates often diverge because firms adopt different device scopes, price mixes, and refresh rhythms, and we surface these factors so buyers can align figures to their needs.

Key gap drivers include some publishers folding surgical-imaging consoles into C-arm totals, others applying list prices without channel discounts, and a few relying on single-region shipment extrapolation rather than balanced global procedure pools.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.51 B (2025) | Mordor Intelligence | - |

| USD 3.44 B (2025) | Global Consultancy A | Broader scope adds hybrid-OR arms; uses list prices |

| USD 2.03 B (2024) | Industry Journal B | Excludes mini systems; conservative replacement cycle |

The comparison shows that Mordor's blended scope, realistic pricing, and annual refresh cadence create a balanced, transparent baseline clients can trust.

Key Questions Answered in the Report

What clinical trend is most responsible for rising demand for advanced C-arm systems?

An ongoing shift toward minimally invasive, image-guided procedures drives hospitals and ambulatory centers to upgrade to platforms that deliver real-time 3D imaging and AI-assisted navigation.

Why are ambulatory surgical centers prioritizing mobile C-arms over fixed installations?

Mobile units can be wheeled between procedure rooms, support multiple specialties in a single day, and align with reimbursement policies that reward lower-cost outpatient care.

How is detector technology influencing purchasing decisions in the C-arms market?

Facilities increasingly favor flat-panel detectors because they provide clearer images at lower radiation dose, support cone-beam CT, and integrate easily with AI software for dose optimization.

What competitive strategy are leading vendors using to differentiate their C-arm offerings?

Market leaders package hardware with software subscriptions, remote diagnostics, and workflow automation features such as self-driving positioning to lock in long-term service revenue.

How are refurbished C-arms affecting sales of new equipment?

A mature refurbishment network offers lower-priced units with warranty coverage, delaying some new purchases but simultaneously broadening technology access in cost-sensitive regions.

Which workforce issue is influencing the design of next-generation C-arms?

A shortage of trained intra-operative imaging technologists is pushing manufacturers to build systems with intuitive user interfaces, voice commands, and automated positioning to reduce operator workload.

Page last updated on: