U.S. Formulation Development Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

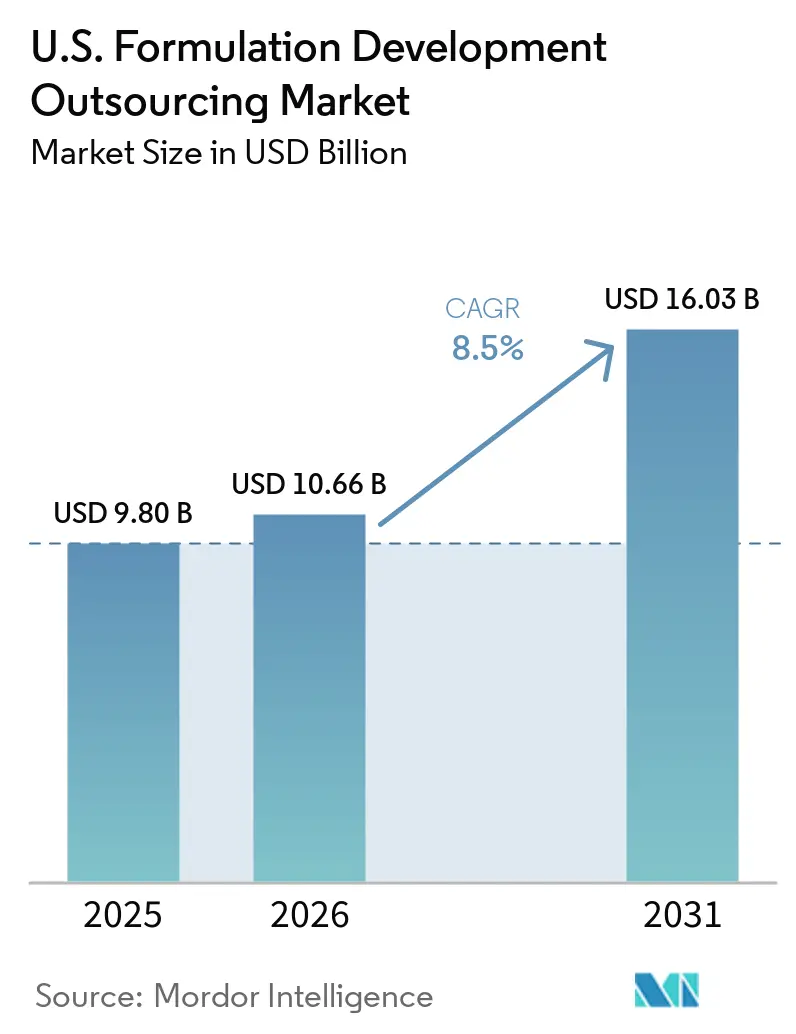

| Base Year Market Size (2025) | USD 9.80 Billion |

| Market Size (2026) | USD 10.66 Billion |

| Market Size (2031) | USD 16.03 Billion |

| Growth Rate (2026 - 2031) | 8.50% CAGR |

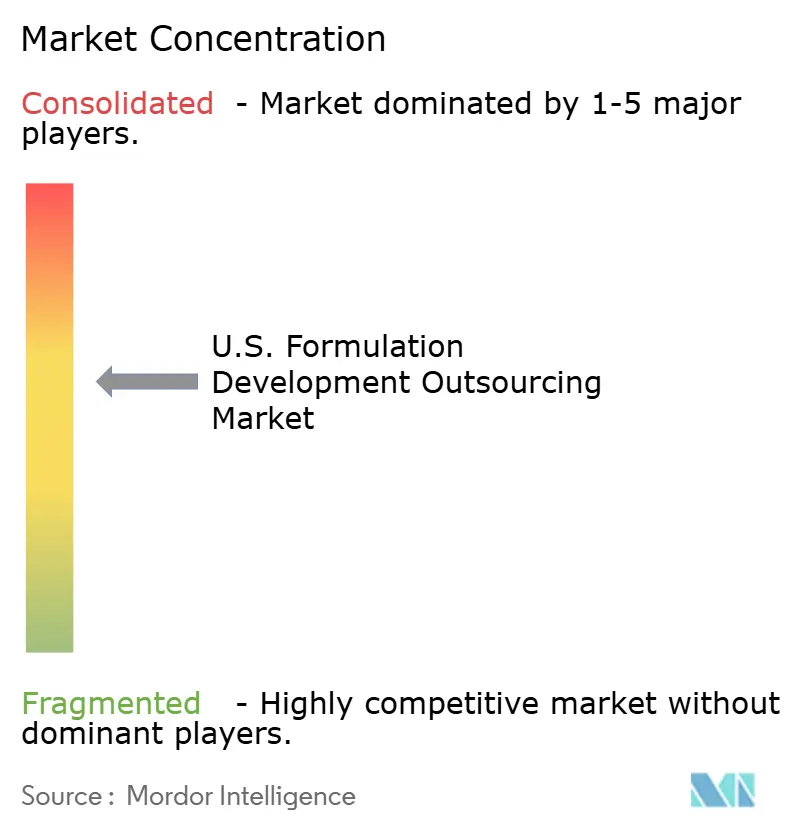

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Formulation Development Outsourcing Market Analysis by Mordor Intelligence

The U.S. Formulation Development Outsourcing Market size is expected to increase from USD 9.80 billion in 2025 to USD 10.66 billion in 2026 and reach USD 16.03 billion by 2031, growing at a CAGR of 8.5% over 2026-2031.

The United States pharmaceutical formulation development services market leads in outsourcing volume due to its strong concentration of IND-stage programs and the FDA's risk-based CMC framework, which encourages sponsors to collaborate with specialist CDMOs instead of investing in internal infrastructure. Another consistent demand driver is 505(b)(2) reformulation activity, which sustains formulation-heavy programs even during slower novel drug cycles, ensuring market activity across various development models. The market is shifting from one-off outsourcing projects to long-term, risk-sharing CDMO partnerships that include milestone and royalty components, aligning service providers' economics with sponsor outcomes.

Key Report Takeaways

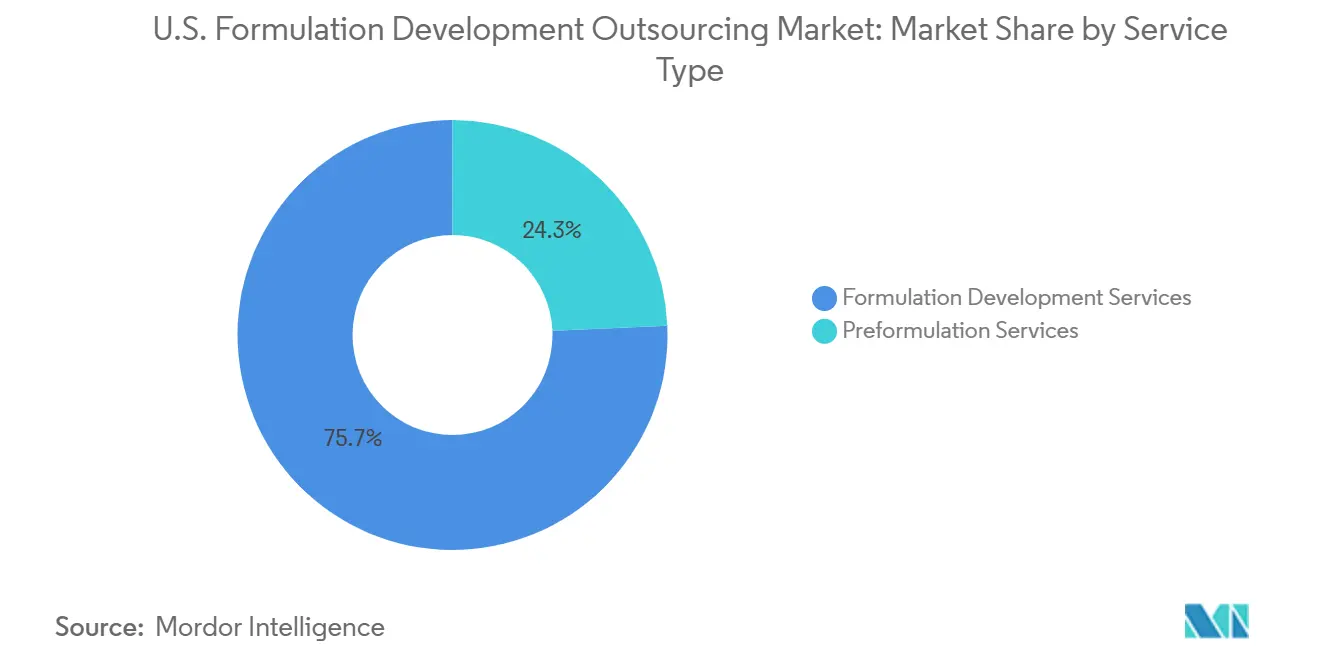

- By service type, formulation development services held 75.69% of revenue in 2025, while preformulation services are projected to grow at a 16.20% CAGR through 2031.

- By dosage form, injectable and parenteral forms recorded the highest projected CAGR at 16.99% through 2031, while the largest 2025 dosage form share was not specified in the supplied draft.

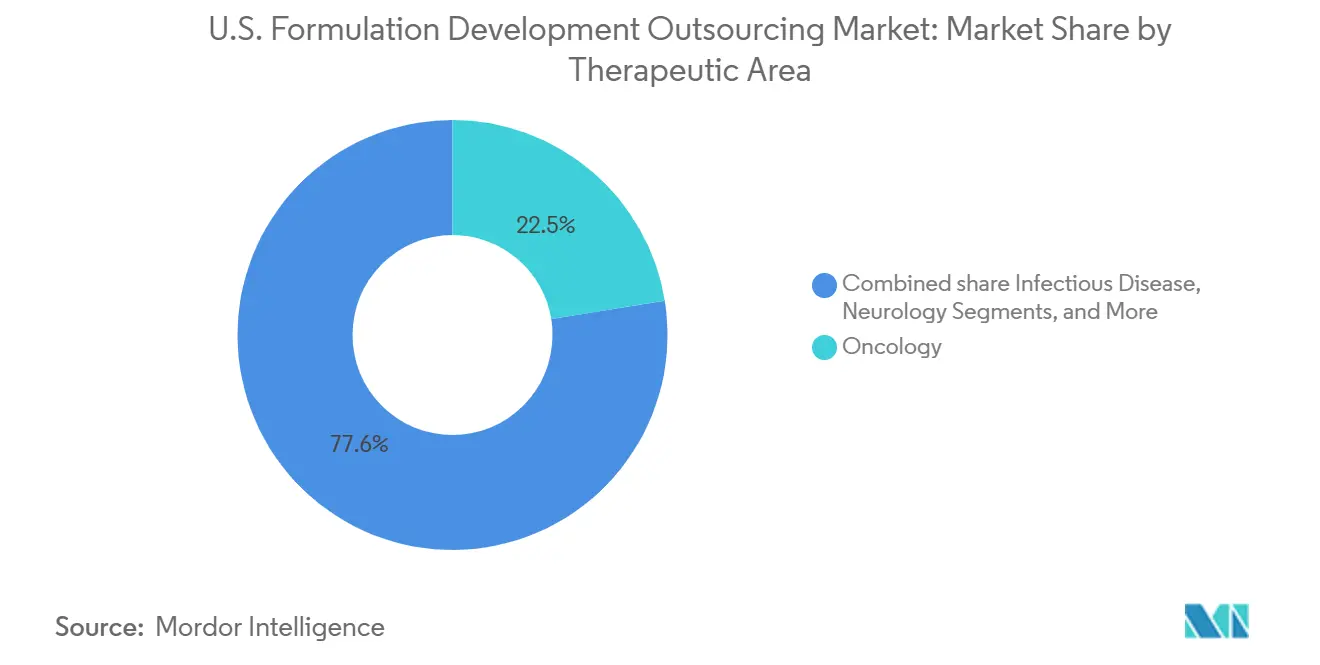

- By therapeutic area, oncology accounted for 22.45% in 2025, while cardiovascular therapies are projected to advance at a 17.34% CAGR through 2031.

- By end user, pharmaceutical and biopharmaceutical companies held 78.89% of revenue in 2025, while government and academic institutes are forecast to expand at a 17.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Formulation Development Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Outsourcing to control cost and access formulation expertise | +2.3% | National, concentrated in the New Jersey pharma corridor, Massachusetts, and North Carolina Research Triangle | Medium term (2-4 years) |

| Rising biologics and injectable complexity | +2.0% | National, with early gains in Boston, San Diego, and the San Francisco Bay Area biologics hubs | Long term (≥ 4 years) |

| Oncology and specialty pipeline expansion | +1.5% | National, concentrated in Northeast oncology CDMO clusters and the Research Triangle | Long term (≥ 4 years) |

| Dense U.S. clinical trial activity and faster development timelines | +1.2% | National, with the highest density in Northeast and West Coast IND clusters | Short term (≤ 2 years) |

| Reshoring and biosecure-driven vendor requalification | +0.9% | National, with reshoring investments concentrated in Midwest and Mid-Atlantic manufacturing corridors | Short term (≤ 2 years) to Medium term (2-4 years) |

| 505(b)(2) Reformulation Opportunity Set | +0.8% | National, with the greatest density in branded specialty pharma hubs such as New Jersey and Chicago | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Outsourcing To Control Cost And Access Formulation Expertise

The United States pharmaceutical formulation development services market is evolving with an asset-light R&D model, concentrating on outsourcing with a few full-service CDMOs. In 2025, 73% of FDA approvals used outsourced API manufacturing, consistent with 74% in 2024, while 65% relied on outsourced finished-dose manufacturing.[1]Food and Drug Administration, “Chemistry, Manufacturing, and Controls Development and Readiness Pilot Program, Program Announcement,” Federal Register, federalregister.gov Large pharmaceutical companies are adopting risk-sharing contracts with milestone and royalty components, favoring providers with strong regulatory performance. This trend is sidelining smaller CDMOs and increasing switching barriers, granting established providers greater pricing power as demand grows across clinical and commercial programs.

Rising Biologics And Injectable Complexity

The United States pharmaceutical formulation development services market is expanding due to the technical demands of biologics and sterile injectables. Biologics accounted for 45% of FDA approvals in 2025, with a focus on advanced therapies like antibody-drug conjugates and lipid nanoparticle RNA therapies.[2]Zhouxi Wang et al., “FDA's Implementation of Knowledge-Aided Assessment and Structured Application for Manufacturing Assessment of Non-Sterile Solid Oral Dosage Form Drug Products,” AAPS Open, doi.org Platforms like WuXi Biologics’ WuXiHigh 2.0 highlight the importance of technical differentiation. Over 20% of monoclonal antibody products now use high-concentration formulations, with self-administered subcutaneous delivery gaining traction. Persistent fill-finish constraints have increased the value of domestic sterile capacity, benefiting CDMOs with advanced aseptic filling capabilities.

Oncology And Specialty Pipeline Expansion

The United States pharmaceutical formulation development services market is supported by oncology and specialty pipelines, particularly in high-containment programs. In 2025, over 200 ADCs were in clinical development, with 250 more in discovery or preclinical stages. Nearly 90% of marketed ADCs rely on lyophilization for stability, limiting qualified vendors to those with specialized expertise. The National Cancer Institute’s focus on targeted therapies sustains formulation demand, while formulation complexity in ADC programs strengthens the position of CDMOs with validated containment platforms and integrated workflows.

Dense US Clinical Trial Activity And Faster Development Timelines

The scale and speed of clinical trials in the United States are driving growth in the pharmaceutical formulation development services market. The FDA’s PDUFA VII framework accelerates development through earlier CMC issue resolution. Despite this, CMC and analytical deficiencies accounted for 74% of complete response letters from 2020 to 2024, emphasizing the importance of formulation quality. CDMOs with regulatory expertise, pre-validated platforms, and Quality by Design packages are gaining traction. The FDA’s structured data-centric review approach further favors capable outsourcing partners, consolidating the market around fewer, more proficient service providers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent FDA CMC and clinical trial compliance | -1.5% | National, with the strongest impact in Northeast and West Coast biotech clusters that have dense first-in-human activity | Medium term (2-4 years) |

| Early-stage biotech funding volatility | -1.2% | National, with the earliest impact in venture-heavy hubs such as Boston, San Francisco, and San Diego | Short term (≤ 2 years) |

| Tariff exposure across excipients and packaging inputs | -0.8% | National, with the highest exposure in sterile injectable and modified-release programs that depend on imported inputs | Short term (≤ 2 years) to Medium term (2-4 years) |

| Bridging study burden after formulation changes | -0.7% | National, concentrated in late-phase scale-up and site-transfer programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent FDA CMC And Clinical Trial Compliance

Stringent FDA compliance continues to challenge the United States pharmaceutical formulation development services market by increasing costs and extending development timelines. From 2020 to 2024, 74% of complete response letters were linked to CMC and analytical gaps, often identified late in the review process after significant investments.[3]Christopher Cole, “CMC and Analytical Gaps in CRLs, Why They Persist Despite FDA Guidance and How You Can Position Yourself for Success,” Pharmaceutical Technology, pharmtech.com For novel biologics, early focus on comparability planning, secondary supplier coverage, and validated cold-chain logistics adds pressure on smaller teams. CDMOs offering bundled regulatory advisory services gain an edge over those providing only laboratory execution. While the FDA's CDRP program accelerates breakthrough-designated programs, its impact remains limited to eligible cases.

Early-Stage Biotech Funding Volatility

Volatile funding conditions significantly impact the United States pharmaceutical formulation development services market, particularly in early phases. In 2025, biotech's share of total United States startup investment fell to just over 8%, the lowest in over two decades. Public biotech funding dropped 57% year-over-year to USD 2.7 billion in May 2025, following a three-year low in April. This decline reduces CDMO mandates from virtual biotechs and small-cap innovators, delaying formulation-heavy IND transition tasks like Phase I CMC package preparation. These delays compress revenue visibility despite steady late-stage and commercial outsourcing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Preformulation Investment Front-Loading Development Risk

In 2025, Formulation Development Services accounted for 75.69% of the United States pharmaceutical formulation development services market, reflecting sponsors' preference for integrated partnerships that consolidate analytical, process, and scale-up tasks within a single quality system. Preformulation Services, growing at a 16.20% CAGR through 2031, highlights a shift toward early risk identification, with sponsors focusing on viscosity, aggregation tendencies, and excipient compatibility in biologics, ADCs, and lipid nanoparticle therapies. This approach minimizes late-stage reformulation and regulatory disruptions.

By Dosage Form: Injectable And Parenteral Forms Define The Capability Premium

Injectable and Parenteral forms are the fastest-growing segment in the United States pharmaceutical formulation development services market, with a projected 16.99% CAGR through 2031. This growth is driven by the biologics-heavy approval landscape and the lack of sterile infrastructure among sponsors for complex development tasks. High-concentration subcutaneous products and proprietary excipient systems are increasingly in demand, rewarding specialized sterile formulation expertise.

By Therapeutic Area: Cardiovascular Pulls Ahead On Innovation Density

In 2025, oncology led the United States pharmaceutical formulation development services market with a 22.45% share, supported by ADC, targeted small-molecule, and immuno-oncology programs requiring specialized handling and integration. These technical demands drive premium pricing and concentrate work among select providers. Other therapeutic areas, including infectious diseases, neurology, and rare disorders, also contribute to the market with distinct formulation needs.

Cardiovascular therapies are the fastest-growing segment, with a 17.34% CAGR through 2031, driven by fixed-dose combination oral products, RNA-based formulations, and long-acting injectables. Providers are expanding their expertise across advanced therapy categories, with partnerships and innovations shaping the market by addressing formulation complexity rather than prescription volume.

By End User: Government And Academic Channels Reshape The Front-End Pipeline

Pharmaceutical and Biopharmaceutical Companies held 78.89% of the United States pharmaceutical formulation development services market in 2025, maintaining market stability through preferred-provider networks and high-value contracts. Government and Academic Institutes are the fastest-growing segment, with a 17.25% CAGR through 2031, driven by NIH translational programs, BARDA initiatives, and academic-originated INDs directly partnering with CDMOs.

Geography Analysis

The United States pharmaceutical formulation development services market is structured around four regional innovation and manufacturing corridors rather than a single dominant cluster. The Northeast is the leading zone for preclinical and early-phase outsourcing, driven by the integration of the Boston-Cambridge biotech base, the New Jersey pharma corridor, and activities in Pennsylvania. This corridor combines venture-backed biotechs, academic medical centers, formulation specialists, and a high concentration of first-in-human programs.

The West Coast is the second-largest region in the United States pharmaceutical formulation development services market and serves as the primary hub for biologics, cell and gene therapy, and ADC outsourcing. California's San Francisco Bay Area and San Diego anchor this activity due to their concentration of advanced therapy developers and specialized talent. Thermo Fisher Scientific's Patheon business has maintained a significant share of small-molecule and finished-dose approvals, supported by operations on both coasts.

The Southeast, centered on North Carolina's Research Triangle Park, is the fastest-growing hub, offering lower operating costs, a strong manufacturing labor pool, and proximity to major research institutions. The BioSecure Act, signed in December 2025, is redirecting outsourcing from Chinese CDMOs to domestic providers, with the Southeast and Midwest capturing a significant share of this requalification work.

Competitive Landscape

The United States pharmaceutical formulation development services market is moderately consolidated at the top, with significant fragmentation among smaller players. From 2015 to 2025, Thermo Fisher Scientific's Patheon, Catalent, and Lonza collectively accounted for nearly 40% of finished-dose approvals, while 19 other providers held less than 5% market share each. The leading companies benefit from scale and regulatory advantages, while the broader market remains competitive with specialist and niche operators. K

White-space opportunities in the United States pharmaceutical formulation development services market are concentrated in early-phase preformulation for government and academic sponsors, continuous manufacturing for modified-release oral forms, and integrated device-combination development for self-administered biologics. Emerging players like National Resilience are focusing on AI-enabled process control, digital twins, single-use biologics suites, and alignment with national security and BARDA priorities. In May 2026, Charles River Laboratories divested its CDMO and Cell Solutions businesses to GI Partners, forming Rose BioSolutions, highlighting a shift toward specialized operators. Similarly, the April 2026 collaboration between Simulations Plus, Lonza, and the United States FDA on predictive frameworks for amorphous solid dispersions could give providers with mechanistic modeling capabilities a competitive edge in model-informed CMC submissions.

U.S. Formulation Development Outsourcing Industry Leaders

Charles River Laboratories International, Inc.

Catalent, Inc.

Lonza Group AG

Thermo Fisher Scientific Inc. (Patheon)

Recipharm AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Catalent and Elpida Therapeutics partnered for late-phase manufacturing of an AAV9 gene therapy and secured exclusive rights to Elpida's AAV programs, expanding Catalent's portfolio to over 80 partnerships.

- May 2026: GI Partners acquired Charles River Laboratories' CDMO and Cell Solutions businesses, forming Rose BioSolutions, an advanced therapy manufacturer with USD 143 million in 2025 revenue.

- May 2026: Nuvation Bio collaborated with Thermo Fisher Scientific for US-based manufacturing of IBTROZI (taletrectinib), completing technology transfer and filing an NDA supplement.

- April 2026: Thermo Fisher Scientific launched the Gibco CTS Compleo Fill and Finish System, an automated platform reducing risks and variability in autologous cell therapy workflows.

- April 2026: Simulations Plus, Lonza Group, and the US FDA collaborated to develop predictive frameworks for amorphous solid dispersion drug products, integrating platforms with experimental data.

U.S. Formulation Development Outsourcing Market Report Scope

As per the scope of the report, formulation development outsourcing is the practice of contracting specialized third-party organizations (typically CDMOs) to design, optimize, and test drug, cosmetic, or supplement recipes. Companies use it to access advanced lab facilities, accelerate time-to-market, and reduce operational costs without needing an in-house laboratory.

The U.S. formulation development outsourcing market is segmented by service type, dosage form, therapeutic area, and end-user. By service type, the market includes preformulation services and formulation development services. By dosage form, the market is segmented into oral, injectable and parenteral, topical and transdermal, inhalation and nasal, ophthalmic, and buccal, sublingual, rectal, and vaginal. By therapeutic area, the market is categorized into oncology, infectious disease, neurology, cardiovascular, respiratory, hematology, dermatology, rare diseases and genetic disorders, autoimmune and inflammatory disorders, and others. By end-user, the market is segmented into pharmaceutical and biopharmaceutical companies, government and academic institutes, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Preformulation Services |

| Formulation Development Services |

| Oral |

| Injectable and Parenteral |

| Topical and Transdermal |

| Inhalation and Nasal |

| Ophthalmic |

| Buccal, Sublingual, Rectal, and Vaginal |

| Oncology |

| Infectious Disease |

| Neurology |

| Cardiovascular |

| Respiratory |

| Hematology |

| Dermatology |

| Rare Disease and Genetic Disorders |

| Autoimmune and Inflammatory Disorders |

| Others |

| Pharmaceutical and Biopharmaceutical Companies |

| Government and Academic Institutes |

| Others |

| By Service Type | Preformulation Services |

| Formulation Development Services | |

| By Dosage Form | Oral |

| Injectable and Parenteral | |

| Topical and Transdermal | |

| Inhalation and Nasal | |

| Ophthalmic | |

| Buccal, Sublingual, Rectal, and Vaginal | |

| By Therapeutic Area | Oncology |

| Infectious Disease | |

| Neurology | |

| Cardiovascular | |

| Respiratory | |

| Hematology | |

| Dermatology | |

| Rare Disease and Genetic Disorders | |

| Autoimmune and Inflammatory Disorders | |

| Others | |

| By End User | Pharmaceutical and Biopharmaceutical Companies |

| Government and Academic Institutes | |

| Others |

Key Questions Answered in the Report

What is the 2031 value of the US pharmaceutical formulation development services space?

The US pharmaceutical formulation development services market is forecast to reach USD 16.03 billion by 2031, rising from USD 10.66 billion in 2026 at an 8.50% CAGR.

Which service category contributes the most revenue?

Formulation Development Services is the largest service type, holding 75.69% of revenue in 2025 because sponsors continue to favor integrated development partnerships.

Why are preformulation services growing faster than the broader field?

Preformulation Services is projected to grow at 16.20% CAGR through 2031 because sponsors are moving critical characterization work earlier to reduce later regulatory and reformulation risk.

Why are injectables becoming so important in outsourced formulation work?

Injectable and Parenteral forms are projected to grow at 16.99% CAGR through 2031 as biologics, high-concentration subcutaneous products, and long-acting injectables increase demand for sterile expertise.

Which therapeutic area is growing the fastest?

Cardiovascular therapies are expected to post the fastest growth at 17.34% CAGR through 2031, supported by fixed-dose combinations, RNA-based formulations, and long-acting injectable approaches.

Which customer group is expanding the fastest?

Government and Academic Institutes are projected to grow at 17.25% CAGR through 2031 as NIH translational programs, BARDA projects, and academic-originated INDs increasingly use CDMO formulation partners directly.

Page last updated on: