Pharmacovigilance Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

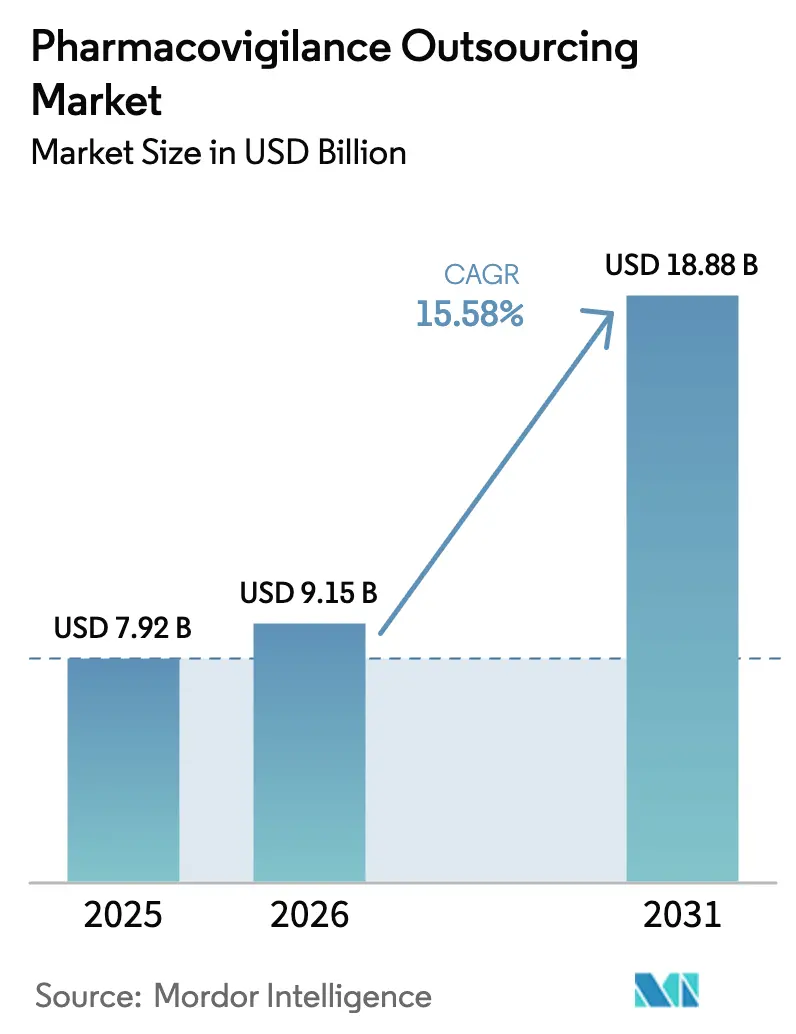

| Market Size (2026) | USD 9.15 Billion |

| Market Size (2031) | USD 18.88 Billion |

| Growth Rate (2026 - 2031) | 15.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmacovigilance Outsourcing Market Analysis by Mordor Intelligence

Pharmacovigilance Outsourcing Market size in 2026 is estimated at USD 9.15 billion, growing from 2025 value of USD 7.92 billion with 2031 projections showing USD 18.88 billion, growing at 15.58% CAGR over 2026-2031.

Heightened regulatory complexity, expanding global drug-development pipelines, and the cost advantages of specialized external partners underpin this outlook. Pharmaceutical companies increasingly view outsourcing as a strategic lever that lets them redeploy internal resources toward core R&D while benefiting from best-in-class safety systems. Adoption of electronic formats such as the FDA’s E2B(R3) standard is accelerating technology investments by service partners. Consolidation among leading vendors is expanding end-to-end capabilities, and artificial-intelligence tools are compressing case-processing timelines, lowering overall cost-per-case. The pharmacovigilance outsourcing market also benefits from rising adverse-event volumes linked to complex biologics, oncology therapies, and orphan drugs, creating sustained demand for specialized signal-detection expertise.

Key Report Takeaways

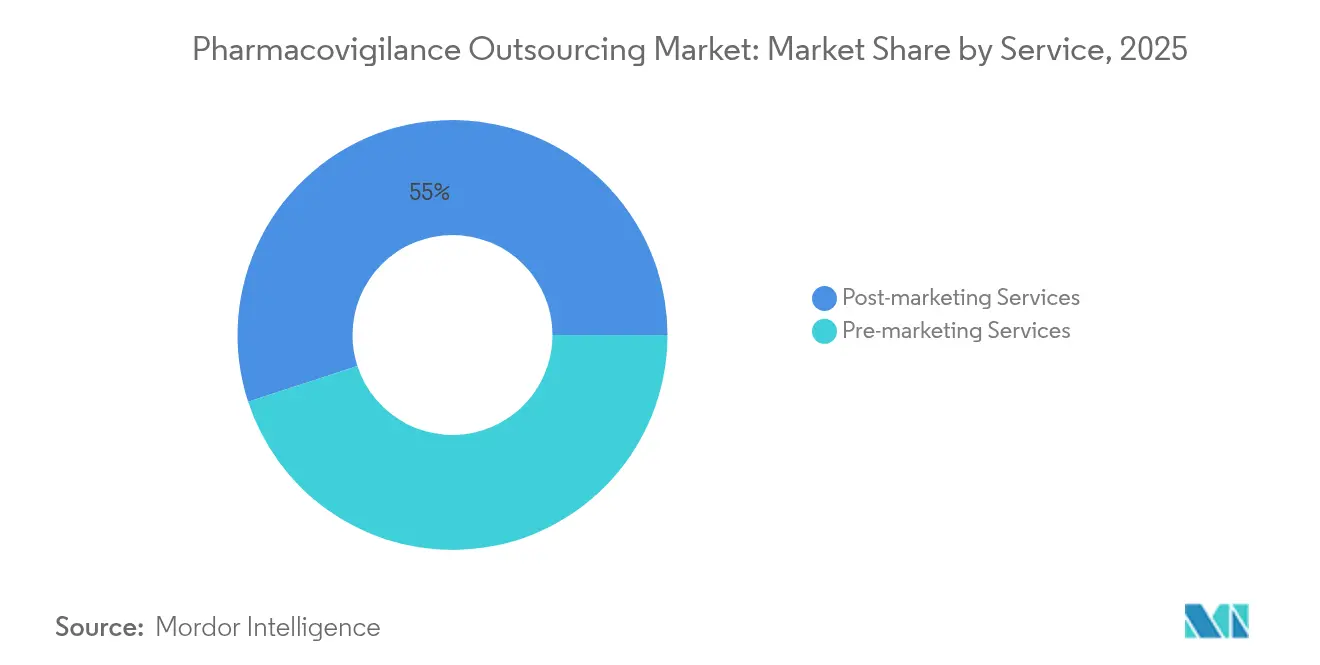

- By service, post-marketing services led with a 55.02% pharmacovigilance outsourcing market share in 2025 and are forecast to grow at a 17.42% CAGR through 2031.

- By therapeutic area, oncology accounted for 26.70% of the pharmacovigilance outsourcing market size in 2025, while the segment’s 18.96% CAGR to 2031 is the fastest among therapeutic areas.

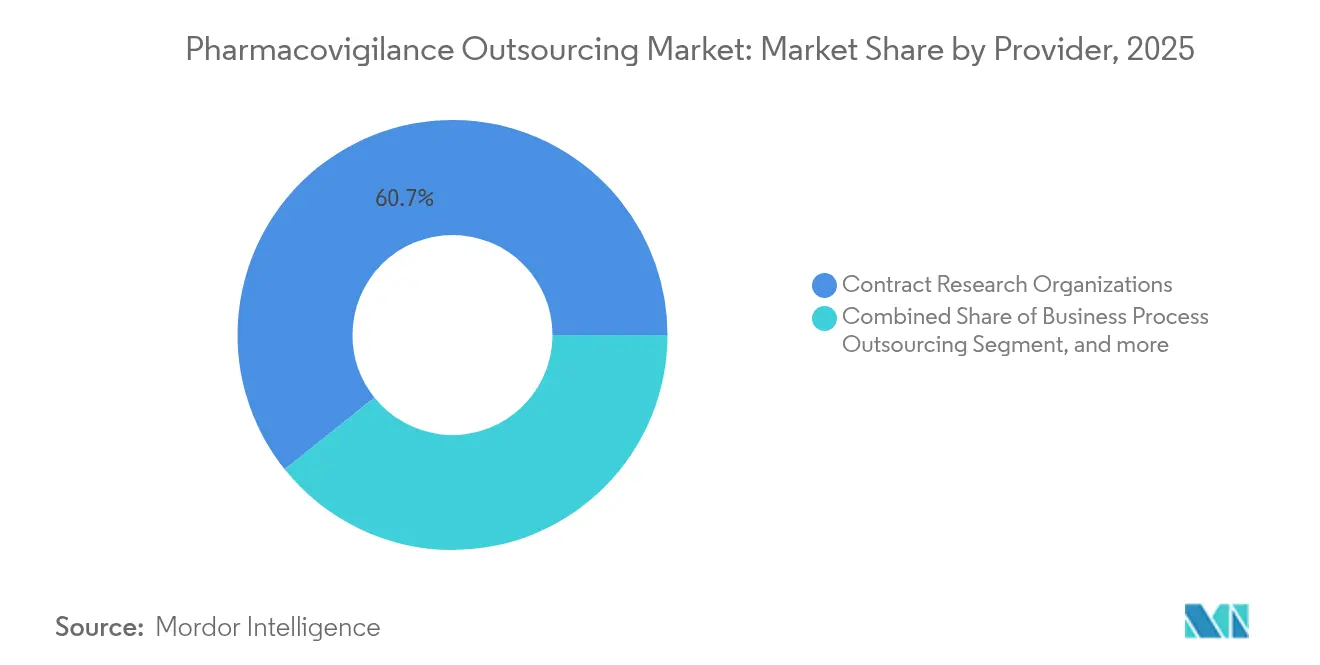

- By provider, contract research organizations held 60.74% of the pharmacovigilance outsourcing market share in 2025; specialized technology vendors represent the fastest-growing provider group at 16.12% CAGR to 2031.

- By end user, biopharmaceutical companies show the highest growth among end users with an 17.86% CAGR, even though pharmaceutical companies still command 52.20% of 2025 revenue.

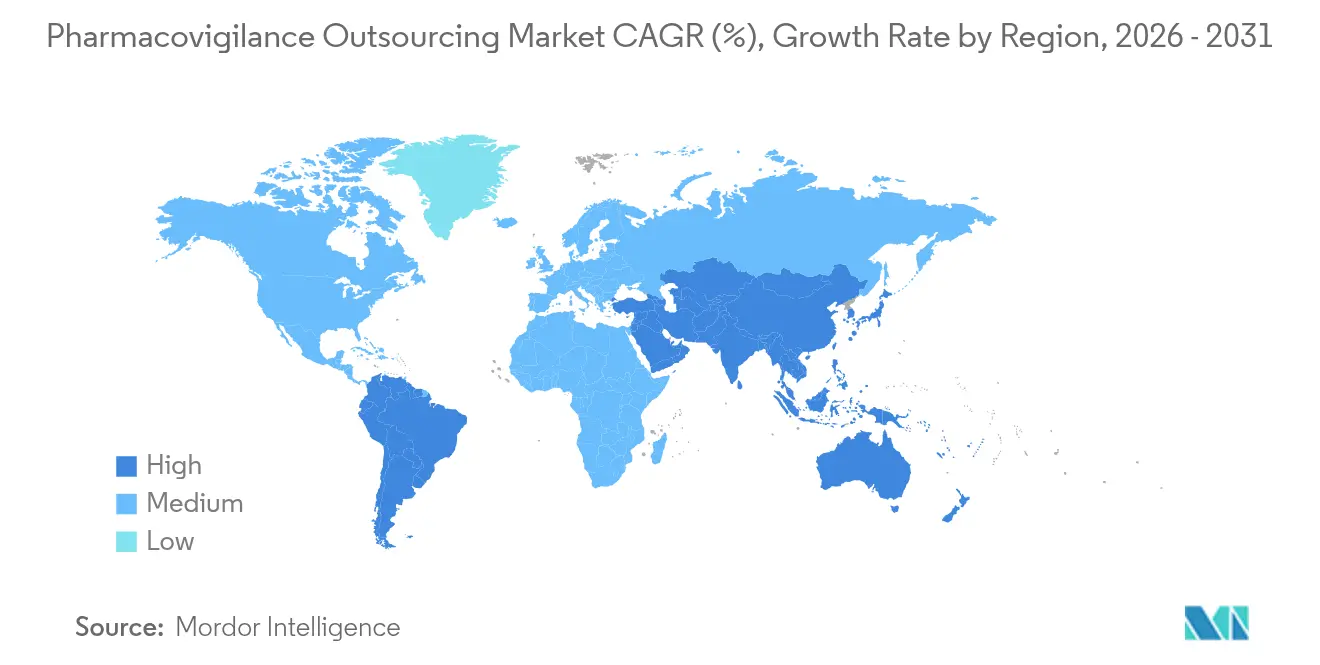

- By geography, North America contributed 38.72% of 2025 revenue, yet Asia Pacific is projected to advance at a 19.64% CAGR, the swiftest regional pace through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmacovigilance Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-profile drug recalls | +2.8% | North America, EU | Short term (≤ 2 years) |

| Rising incidence of adverse drug reactions | +3.1% | Higher reporting in developed markets | Medium term (2-4 years) |

| Expansion of global clinical trials | +2.4% | Core in Asia Pacific; spill-over to MEA & Latin America | Medium term (2-4 years) |

| Stricter real-time safety reporting rules | +3.7% | Global, led by FDA and EMA | Long term (≥ 4 years) |

| Surge in orphan-drug approvals | +1.9% | North America & EU; expanding to Asia Pacific | Long term (≥ 4 years) |

| AI-enabled automation | +2.3% | Early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing High-Profile Drug Recalls due to Safety Concerns

Three thousand seven hundred eighteen recalls from 2012-2023, including 14% Class I events, have intensified scrutiny on quality-control lapses. Each recall affects nearly 400,000 product units and averages 1.3 years in duration, driving manufacturers toward specialist partners that can scale resources quickly. Outsourcing firms provide targeted expertise in impurity analysis, labeling review, and corrective-action planning, mitigating the operational burden for marketing authorization holders. Enhanced FDA post-marketing surveillance guidelines issued in January 2024 reinforce the commercial necessity of external partnerships able to respond rapidly to evolving expectations.[1]U.S. Food and Drug Administration, “Electronic Submission of Individual Case Safety Reports,” fda.gov

Rising Incidence of Adverse Drug Reactions (ADRs)

The FAERS database is processing exponentially higher volumes of individual-case safety reports. For example, montelukast generated 86,732 reports between 2004-2023, while lecanemab accumulated 811 events within its first deployment period. Disproportionality analyses of COVID-19 vaccine events required sophisticated statistical filtering to identify authentic signals. Machine-learning models now reach 76.68% accuracy when predicting ADRs from electronic health records. These analytical burdens exceed many sponsors’ internal capacities, steering them toward vendors offering AI-enabled literature monitoring, natural-language processing, and global regulatory experience.

Expansion of Global Clinical Trial Volume Driving PV Outsourcing

Regional contract-research organizations deliver 30-40% cost savings over Western peers while maintaining ICH compliance. COVID-related decentralization has mainstreamed remote data-capture tools that integrate seamlessly with outsourced pharmacovigilance workflows, reinforcing the preference for single-vendor solutions that cover study oversight and post-trial safety reporting.

Increasing Regulatory Stringency for Real-Time Safety Reporting

The January 2024 start of E2B(R3) electronic submissions and the April 2026 compliance deadline require secure data pipelines, automated format conversion, and dedicated validation frameworks. Draft FDA guidance M14 on real-world data, plus Europe’s Health Data Space regulation adopted in March 2025, collectively raise the compliance bar, rewarding providers with robust informatics platforms and 24/7 audit-ready operations. Sponsors prefer outsourcing to firms whose regulatory teams maintain continuous dialogue with agencies, minimizing the risk of non-compliant submissions.[2]IQVIA Institute, “Advancing Pharmacovigilance with AI,” iqvia.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-professional shortage | -1.8% | Global; acute in emerging APAC hubs | Medium term (2-4 years) |

| Data-privacy & cross-border transfer limits | -1.4% | Mainly EU-US; expanding to APAC-EU corridors | Long term (≥ 4 years) |

| Vendor lock-in from proprietary platforms | -0.9% | Global; sharper in mid-size pharma | Short term (≤ 2 years) |

| Wage inflation in key outsourcing hubs | -1.2% | India, Philippines, Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Skilled Professionals

Turnover in clinical-research roles exceeds 25%, and the global need for pharmacovigilance specialists is around 50,000, with a 5,000-person gap persisting. Emerging markets experience pronounced shortages because they are simultaneously expanding case-processing centers and local regulatory functions. While automation alleviates routine tasks, expert medical reviewers remain indispensable for narrative assessments, risk-benefit evaluations, and regulatory liaison. Outsourcing vendors absorb recruitment pressures by running continuous training programs yet still face wage competition from technology sectors.

Data Privacy & Cross-Border Transfer Restrictions

The European Health Data Space, coming into force in March 2027, introduces granular consent and data-sharing layers that add complexity to multi-region safety operations. EU-US transfers remain under scrutiny, requiring binding corporate rules or equivalent safeguards that escalate compliance costs. Smaller vendors may find the legal burden difficult, prompting some sponsors to limit supplier selection to firms with established global privacy offices.[3]European Data Protection Board, “Guidelines on Health Data Transfers,” edpb.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Integration of Lifecycle Activities Fuels Post-Marketing Dominance

Post-marketing pharmacovigilance outsourcing market size leadership stems from its 55.02% share in 2025 and robust 17.42% CAGR outlook. Mandatory risk-management plans, periodic safety-update reporting, and increasingly common label-update cycles sustain high case volumes long after launch. Sponsors are bundling literature surveillance, social-media tracking, and signal evaluation under knowledge-process-outsourcing umbrellas to gain therapeutic insights without enlarging permanent staff. Pre-marketing safety oversight remains essential for trial-phase submissions but contributes a smaller share, partly because innovative in silico trial-design tools reduce classical case loads. Nevertheless, cross-functional service packages linking clinical and commercial phases are gaining traction as market differentiation levers for vendors.

Knowledge-process analytics and automation deliver measurable efficiency. Vendors highlight 30% lower cost-per-case when predictive algorithms triage narratives before human medical review. Combined with multi-language processing centers, these efficiencies reinforce sponsor reliance on external post-marketing expertise.

By Therapeutic Area: Oncology Complexity Spurs Specialized Demand

Oncology contributes 26.70% of 2025 revenue and is projected to expand at a 18.96% CAGR, reflecting the pharmacovigilance outsourcing market’s gravitation toward therapies with intricate toxicity profiles. The rise of immuno-oncology combinations, antibody-drug conjugates, and cell therapies yields adverse-event patterns requiring deep biologic knowledge and 24/7 monitoring. CROs with oncology-dedicated safety physicians therefore command premium pricing and generate high client-retention rates.

Cardiovascular safety concerns surrounding certain targeted agents further elevate data review complexity, while neurology, driven by disease-modifying Alzheimer’s drugs, is emerging as the next sizable growth pocket. Rare-disease oncology overlaps with orphan-drug mandates, complicating data-collection logistics yet bolstering opportunities for niche specialists capable of managing low-volume, high-risk cohorts.

By Provider: CRO Scale Meets Technology Disruption

Contract research organizations retain 60.74% of 2025 revenue thanks to integrated clinical and post-marketing offerings that shorten vendor-onboarding cycles for sponsors. However, specialized technology vendors, expanding at 16.12% CAGR, are redrawing the value chain. Their cloud-native platforms automate E2B coding, duplicate detection, and real-time dashboards, lowering the marginal cost of each safety report and creating a credible alternative to labor-heavy models. Hybrid firms that blend proprietary software with domain experts are emerging, appealing to sponsors aiming for single-throat-to-choke accountability.

Large CROs are countering disruption through acquisitions, for example, Qinecsa’s purchase of Insife, to fold purpose-built PV software into service portfolios. These moves signal convergence between platform and process expertise as key differentiators.

By End User: Biopharmaceutical Innovators Propel Growth

Pharmaceutical sponsors still represent 52.20% of 2025 revenue, driven by diverse pipelines and global commercialization footprints. Yet biopharmaceutical companies, many pursuing first-in-class modalities, show 17.86% CAGR because limited in-house resources and accelerated approval pathways compel early outsourcing decisions. The pharmacovigilance outsourcing industry benefits because cell-and-gene therapies involve intensive long-term follow-up requirements unsuited to small clinical teams.

Generic-drug makers maintain steady demand, primarily for cost-optimized case-processing support, whereas medical-device firms are engaging PV vendors to comply with expanding combination-product rules. Collectively, these dynamics reinforce the market’s multi-stakeholder client base.

Geography Analysis

North America generated 38.72% of 2025 revenue, anchored by stringent FDA mandates and the region’s large R&D spend. Widespread adoption of the E2B(R3) standard and the April 2026 compliance deadline ensure persistent demand for external technology platforms and regulatory mentorship. Multinational sponsors headquartered in the United States increasingly consolidate safety operations with fewer vendors to manage privacy obligations and benefit from economies of scale. Canada and Mexico contribute incremental growth via harmonized regional frameworks and rising clinical-trial activity.

Asia Pacific, while smaller today, posts the fastest pace at 19.64% CAGR through 2031. China, India, and Japan are investing in national adverse-event databases equivalent to Western benchmarks, boosting data quality and global confidence. India’s contract-research, development, and manufacturing sector supplies a rich pipeline of cases to regional safety hubs. Sponsors report 30-40% cost savings from APAC operations, reinforcing the shift of follow-the-sun case-processing models to the region.

Europe retains a strong presence through the EMA’s EudraVigilance system and upcoming Health Data Space, which unlocks secondary-use data for safety analytics yet imposes strict consent management. Middle East & Africa and South America remain nascent but are attracting early-phase trials and digital-health investments that will eventually require full pharmacovigilance frameworks. APEC-wide surveys underscore heterogeneous local practices, offering openings for vendors with harmonization toolkits and multilingual call-center capability.

Competitive Landscape

The pharmacovigilance outsourcing market shows moderate consolidation. The top five vendors account for more than half of global revenue, giving them capital to deploy generative-AI tools and expand regional language centers. IQVIA processes 800 safety cases annually while translating 130 million words, a scale few competitors match. Sanofi’s partnership with IQVIA’s Project ARTEMIS illustrates how AI triage can reallocate human analysts to complex evaluations.

Acquisition momentum is strong: ProPharma bought iSafety Systems in February 2024, Qinecsa took over Insife in April, and Inovalon added VigiLanz the same month. These deals broaden platform coverage and embed surveillance modules that detect hospital-level safety events in near-real time. Mid-size CROs without proprietary technology risk margin squeeze as sponsors migrate to platform-enabled vendors promising double-digit efficiency gains. Regulatory agencies are accelerating this shift by encouraging AI dialogues through the FDA’s Emerging Drug-Safety Technology Program, reducing uncertainty for early adopters.

White-space opportunities persist in under-served therapeutic domains such as ophthalmology and dermatology, in pharmacogenomic signal detection, and in regional hubs where local-language narrative review remains manual. Vendors that integrate human expertise with explainable AI, satisfy cross-border privacy rules, and deliver transparent metrics are best placed to capture share.

Pharmacovigilance Outsourcing Industry Leaders

Accenture

Qinecsa Solutions

IQVIA Inc.

ICON Plc

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: IQVIA reported Q1 2025 revenue of USD 3,829 million with R&D Solutions revenue at USD 2,102 million, maintaining a contracted backlog of USD 31.5 billion growing 4.8% year-over-year, demonstrating resilience in pharmacovigilance and clinical research services despite macroeconomic uncertainties. The company raised full-year revenue guidance to between USD 16,000 million and USD 16,400 million, reflecting strong demand for integrated safety and clinical development services.

- July 2024: Oracle reported significant updates to its Argus and Safety One Intake solutions, bolstering its pharmacovigilance portfolio with AI-powered features. These AI enhancements cater to the evolving needs of life science organizations, allowing them to navigate increasingly complex regulatory landscapes and manage rising adverse event cases efficiently.

- February 2024: Inovalon acquired VigiLanz, a leading clinical surveillance and patient safety SaaS and data company, to enhance its capabilities in monitoring patient safety and clinical data management. This acquisition demonstrates the strategic value of AI-powered clinical surveillance technologies in the evolving pharmacovigilance landscape.

Global Pharmacovigilance Outsourcing Market Report Scope

As per the scope of the report, pharmacovigilance is the science and activities relating to the detection, assessment, understanding, and prevention of adverse effects or any other medicine-related problem. Pharmacovigilance outsourcing (PVO) transfers the execution of drug safety functions and processes to a third-party provider. The pharmacovigilance outsourcing market is segmented into service, therapeutic area, provider, end user, and geography. By service, the market is segmented into pre-marketing services and post-marketing services. By therapeutic area, the market is segmented into neurology, cardiology, oncology, and other applications (dental and ophthalmic). By end user, the market is segmented into hospitals and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for the above segments.

| Pre-marketing Services | Clinical Pharmacovigilance Services |

| Case Processing Services | |

| Signal Detection & Risk Management Services | |

| Safety Data Management Services | |

| Medical Review Services | |

| Post-marketing Services | Knowledge Process Outsourcing Services |

| IT Solutions & Platforms | |

| Literature Surveillance & Reporting Services | |

| Aggregate Reporting & PSUR/DSUR Preparation |

| Neurology |

| Cardiology |

| Oncology |

| Immunology |

| Respiratory |

| Orthopedic |

| Others |

| Contract Research Organizations (CROs) |

| Business Process Outsourcing (BPO) |

| Specialized PV Technology Vendors |

| Hybrid Service Providers |

| Pharmaceutical Companies |

| Biopharmaceutical Companies |

| Medical Device Companies |

| Generic Drug Manufacturers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service | Pre-marketing Services | Clinical Pharmacovigilance Services |

| Case Processing Services | ||

| Signal Detection & Risk Management Services | ||

| Safety Data Management Services | ||

| Medical Review Services | ||

| Post-marketing Services | Knowledge Process Outsourcing Services | |

| IT Solutions & Platforms | ||

| Literature Surveillance & Reporting Services | ||

| Aggregate Reporting & PSUR/DSUR Preparation | ||

| By Therapeutic Area | Neurology | |

| Cardiology | ||

| Oncology | ||

| Immunology | ||

| Respiratory | ||

| Orthopedic | ||

| Others | ||

| By Provider | Contract Research Organizations (CROs) | |

| Business Process Outsourcing (BPO) | ||

| Specialized PV Technology Vendors | ||

| Hybrid Service Providers | ||

| By End User | Pharmaceutical Companies | |

| Biopharmaceutical Companies | ||

| Medical Device Companies | ||

| Generic Drug Manufacturers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the pharmacovigilance outsourcing market?

The sector is valued at USD 9.15 billion in 2026, with a forecast to reach USD 18.88 billion by 2031.

Which service segment holds the largest share?

Post-marketing services account for 55.02% of 2025 revenue and exhibit a 17.42% CAGR outlook.

Why is Asia Pacific growing fastest?

The region benefits from cost-effective clinical-trial growth, improving regulatory systems, and projected 19.64% CAGR through 2031.

What role does AI play in pharmacovigilance outsourcing?

AI reduces case-processing times, automates data extraction, and improves signal detection, thereby lowering costs and enhancing compliance.

Who are the leading providers?

Large CROs such as IQVIA lead with integrated service models, while specialized technology vendors are the fastest-growing provider category.

Page last updated on: