Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.24 Billion |

| Market Size (2026) | USD 4.46 Billion |

| Market Size (2031) | USD 5.75 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Upholstered Furniture Market Analysis by Mordor Intelligence

The Europe Upholstered Furniture Market size is expected to grow from USD 4.24 billion in 2025 to USD 4.46 billion in 2026 and is forecast to reach USD 5.75 billion by 2031 at 5.22% CAGR over 2026-2031.

With Europe’s furniture market expanding steadily through 2030 and residential furniture accounting for the majority of total demand, high-value categories such as sofas and upholstered beds continue to capture a disproportionate share of incremental furniture spending. This trajectory underscores the sector’s resilience as European households continue to refresh interiors, while commercial buyers accelerate refurbishment cycles ahead of major sporting events. Consumers across the region prioritize comfort-focused designs, modular configurations, and sustainability credentials, prompting manufacturers to redesign supply chains for traceability and circularity compliance. Digital-first shopping behaviors further reshape the competitive landscape, with augmented-reality tools, virtual showrooms, and next-day delivery promises pushing legacy retailers to adopt omnichannel models. At the same time, raw-material price volatility forces producers to hedge wood and foam costs or pivot to engineered substitutes, intensifying cost-management pressures. Finally, institutional investments in build-to-rent housing and hospitality renovations unlock high-volume procurement opportunities, balancing the market’s traditional reliance on discretionary household spending.

Key Report Takeaways

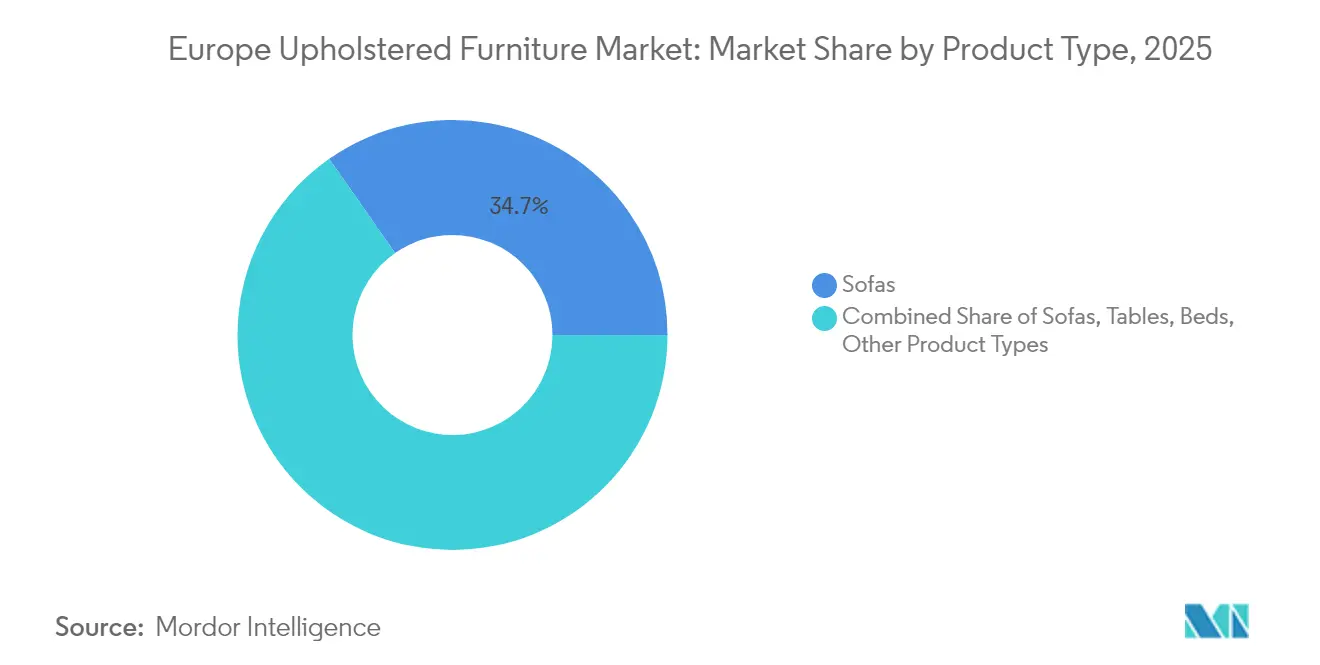

- By product type, sofas commanded 34.72% of Europe upholstered furniture market share in 2025, while beds are projected to post the fastest 6.78% CAGR to 2031.

- By application, the residential segment held 67.10% of the market share in 2025, whereas commercial applications are expected to register a 6.42% CAGR through 2031.

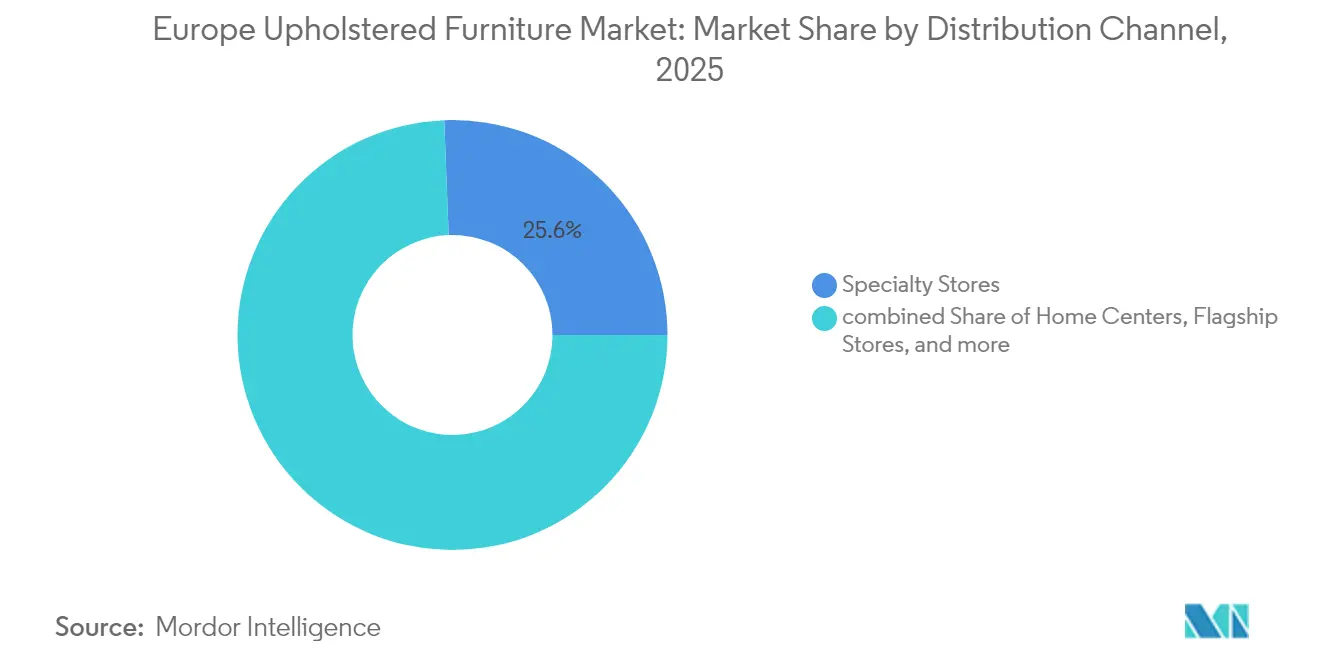

- By distribution channel, specialty stores led with 25.61% share of the market size in 2025, but online platforms are forecast to expand at a 8.84% CAGR to 2031.

- By geography, the United Kingdom, France and Germany accounted for 46.85% of the Europe upholstered furniture market in 2025, while the NORDICS are set to record the highest 5.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Upholstered Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing home-renovation & replacement cycle | +1.2% | UK, Germany, France, Italy, Spain | Medium term (2-4 years) |

| Premiumisation among Gen-Y & Gen-Z buyers | +0.9% | Germany, UK, NORDICS, BENELUX | Long term (≥ 4 years) |

| Build-to-rent residential projects expansion | +0.7% | Germany, UK, Netherlands, Spain | Medium term (2-4 years) |

| Hospitality refurbishment wave (Olympics/EURO) | +0.5% | France, Germany, Spain, Italy | Short term (≤ 2 years) |

| Furniture subscription & “as-a-service” models gaining traction | +0.6% | UK, Germany, Netherlands, Nordics | Medium term (2–4 years) |

| Digitally printed performance fabrics enabling mass-customisation | +0.8% | Germany, Italy, UK, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Home-Renovation & Replacement Cycle

Home-improvement spending continues to climb as hybrid work routines make living spaces multifunctional, shrinking the renovation interval from 7–10 years to roughly 5–7 years. Furniture retailers across Germany reported double-digit growth in replacement purchases during 2024, with ergonomic sofas and height-adjustable loungers topping wish lists [1]Source: FederlegnoArredo, “Italian Furniture Industry Annual Report 2024,” federlegnoarredo.it. The shorter cycle benefits the Europe upholstered furniture market by boosting volume demand at mid- and premium price bands. It also pressures manufacturers to accelerate model refresh rates, adopt modular platforms, and shorten development lead times. Government incentives for energy-efficient refurbishments further nudge consumers toward new furnishings that meet eco-label criteria. Consequently, supply chains invest in fast-response capabilities, enabling just-in-time upholstery production aligned with seasonal décor shifts.

Premiumisation Among Gen-Y & Gen-Z Buyers

Young European consumers allocate up to 30% more per upholstered item than older demographics, valuing sustainable materials and bespoke aesthetics over entry-level pricing. Their preference for modular sectional sofas, convertible daybeds, and smart-fabric finishes lifts average selling prices across the Europe upholstered furniture market. Social-media influence accelerates trend cycles, driving micro-collections and limited-edition collaborations that keep showrooms fresh. Retailers counter assortment complexity by expanding digital configurators, allowing shoppers to mix fabrics, leg designs, and accessory add-ons in real time. Brands with transparent sourcing stories win loyalty, as Gen-Z buyers check traceability labels and carbon-footprint scores before checkout. The shift to higher-value transactions raises margins but also heightens expectations for durability and end-of-life take-back programs.

Build-to-Rent Residential Projects Expansion

Institutional capital poured more than USD 17.60 billion into European build-to-rent (BTR) schemes in 2024, each unit typically demanding furniture packages, of which upholstered pieces account for roughly 40% [2]Source: FederlegnoArredo, “Italian Furniture Industry Annual Report 2024,” federlegnoarredo.it. Developers favor suppliers who can standardize SKUs, guarantee on-site installation within tight construction schedules, and provide replacement services during tenancy turnovers. The Europe upholstered furniture market thus captures long-term, multi-unit contracts that stabilize factory utilization rates. Manufacturers with ISO-certified durability testing and stain-resistant performance fabrics gain competitive edges. Although BTR demand concentrates in metropolitan hubs like Berlin, London, and Amsterdam, spillover orders reach regional plants, supporting cross-border logistics networks. The segment also spurs innovation in knock-down designs that navigate freight elevators and narrow staircases common in urban buildings.

Hospitality Refurbishment Wave Ahead of Major Events

Hotels in France, Germany, and Spain are refreshing lobbies and guest rooms ahead of the 2028 Olympics and Euro 2032 tournaments, compressing their furniture-replacement timelines from 8–10 years to about 6–8 years. Commercial-grade sofas must now pass rigorous fire-resistance and abrasion tests, encouraging suppliers to adopt advanced coatings and high-density foams. Procurement teams prioritize design coherence across chains, creating block orders that reward manufacturers with scalable cut-and-sew capacities. The Europe upholstered furniture market benefits from elevated order sizes, but lead-time certainty remains critical as hotels aim to avoid refurbishment overruns. While event-driven spending peaks in 2026–2027, ongoing tourism recovery is expected to sustain demand thereafter. Players able to bundle design, manufacturing, and installation services capture the lion’s share of renovation contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-linked squeeze on discretionary spending | –1.1% | Europe-wide, especially Spain, Italy | Short term (≤ 2 years) |

| Volatile wood & foam input prices | –0.8% | Europe-wide, manufacturing hubs | Medium term (2-4 years) |

| Rising sustainability-compliance costs under EU Ecodesign rules | –0.9% | EU-wide, particularly Germany, France, and Nordics | Long term (≥ 4 years) |

| Shortage of skilled upholsterers in Western Europe | –0.6% | Western Europe, notably Italy, UK, and Germany | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Inflation-Linked Squeeze on Discretionary Spending

Persistent inflation drives a wedge between nominal wage growth and real purchasing power, prompting many households to postpone big-ticket furniture acquisitions[3]Source: Cushman & Wakefield, “European Build-to-Rent Market Report 2024,” cushmanwakefield.com. Retail sales volumes for household furnishings dipped 12–15% in Spain and Italy during 2024, even as headline revenues rose on price hikes. The Europe upholstered furniture market thus witnesses polarizing demand: luxury brands record steady orders, value chains push aggressive promotions, and mid-market labels struggle to differentiate. Retailers deploy 0% financing and buy-now-pay-later schemes to stimulate turnover, but credit-risk profiles tighten under macro-economic uncertainty. Manufacturers hedge by diversifying into commercial contracts to offset softer retail demand. As inflation moderates, pent-up replacement demand could unlock a rebound, yet consumer confidence remains the swing factor for the next two years.

Volatile Wood & Foam Input Prices

OSB and MDF panel prices have swung up to 25% quarter-on-quarter, while polyurethane foam costs track petrochemical volatility, squeezing gross margins [4]Source: Eurostat, “Retail Trade and Manufacturing Statistics 2025,” ec.europa.eu. Suppliers explore bio-based foam alternatives and engineered-wood substitutes, but scaling these materials requires significant capital and compliance testing. Cost-plus pricing clauses in B2B contracts partly mitigate exposure, whereas retail lines face competitive ceilings that limit pass-through potential. The Europe upholstered furniture market thus intensifies its focus on lean manufacturing, yield optimization, and digital inventory forecasting to counter raw-material shocks. Some players lock in annual supply deals with regional mills, trading price certainty for volume commitments. Regulatory moves to curb deforestation and toxic chemicals further complicate sourcing strategies, adding compliance costs that must eventually flow into price tags or operating efficiencies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sofas Anchor Revenue While Beds Accelerate

Sofas generated 34.72% of Europe upholstered furniture market share in 2025, underscoring their role as living-room centerpieces across European households. Modular configurations, built-in USB chargers, and stain-proof performance fabrics keep the category at the forefront of design innovation. Beds, meanwhile, are projected to post a 6.78% CAGR on the back of heightened consumer focus on sleep health, adjustable frames, and smart-sensor integrations. The Europe upholstered furniture market size for beds is forecast to reach USD 1.57 billion by 2031, reflecting consumers’ willingness to pay premiums for wellness-oriented features. Chairs and recliners benefit from hybrid work norms, with ergonomic certifications turning into must-have selling points for home offices. Niche items such as storage ottomans and convertible sofas cleverly address shrinking urban dwellings, reinforcing demand for space-efficient solutions across the product spectrum.

Continuous product differentiation propels repeat purchases as fabrics, finishes, and modular add-ons refresh the aesthetic appeal of standard SKUs. Digital-printing technology from suppliers such as Limonta enables rapid customization without large minimum orders, giving mid-sized brands an affordable path to personalization. Cross-category design language shared leg profiles coordinated color palettes helps manufacturers streamline component sourcing and cut downtime between model transitions. Meanwhile, end-of-life considerations influence new product development, with easy-to-disassemble frames and mono-material cushions facilitating recycling compliance. These trends push R&D teams to pursue cradle-to-cradle certifications that resonate with eco-conscious buyers. As a result, product-level innovation remains a decisive lever in sustaining premium pricing and combating commoditization pressures.

By Application: Residential Dominates Amid Commercial Upswing

The residential segment held 67.10% of Europe upholstered furniture market share in 2025, buoyed by ongoing home-improvement culture and the longevity of hybrid work trends. Households continue to allocate discretionary budgets toward comfort-enhancing sofas, daybeds, and lounge chairs that double as remote-work seats. Renovation grants in Germany and energy-efficiency tax credits in France further stimulate living-space upgrades, keeping retail showrooms busy even during macro-economic headwinds. Meanwhile, the commercial segment is forecast to grow at 6.42% CAGR, propelled by corporate office redesigns, hospitality refurbishments, and healthcare investments. Workplace strategies now emphasize collaborative areas with soft seating, driving incremental volume for contract-grade sectionals and acoustic lounge pods.

Contracts in commercial channels prioritize durability metrics such as Martindale abrasion counts and CAL-117 fire standards, pressing manufacturers to invest in laboratory testing and third-party certifications. The Europe upholstered furniture market size devoted to commercial spaces is expected to climb steadily as property owners bundle furniture procurement into broader wellness and ESG upgrades. Growth in purpose-built student housing and senior-living facilities introduces additional niches that demand tailor-made seating ergonomics and safety features. Blended procurement models blur traditional application boundaries, as build-to-rent units source furniture at commercial scale but require residential aesthetics to attract tenants. This convergence challenges suppliers to maintain SKU coherence while meeting divergent compliance regimes.

By Distribution Channel: Omnichannel Strategies Gain Ground

Specialty stores retained 25.61% of Europe upholstered furniture market share in 2025, leveraging curated assortments and in-store design consultations to command premium price points. Yet online platforms are projected to log a robust 8.84% CAGR, underpinned by advances in augmented-reality visualization, free-returns policies, and last-mile logistics suited for bulky items. The Europe upholstered furniture market size transacted through e-commerce channels is set to nearly double by 2031, forcing legacy retailers to integrate click-and-collect services and 3D product configurators. Flagship stores shift toward experiential showrooms emphasizing sensory fabric displays, virtual room planners, and sustainability storytelling corners. Home-center chains revamp aisles with QR-code-enabled catalogs and mixed-reality kiosks to bridge physical and digital journeys.

Direct-to-consumer disruptors employ social-commerce tactics and influencer collaborations to capture mindshare among younger demographics, often bypassing wholesale markups. Subscription models pioneered by firms like NORNORM enable corporate clients to lease furniture, adding recurring-revenue streams to the market. Logistics innovation remains critical; flat-pack designs and recyclable packaging reduce damage rates and emissions. Retailers that master data-driven inventory allocation minimize markdown risks, particularly for trend-sensitive colorways. In parallel, omnichannel returns infrastructures gain strategic importance, as customers expect effortless pick-ups for exchanges or repairs.

Geography Analysis

The United Kingdom, France and Germany accounted for 46.85% of the Europe upholstered furniture market in 2025 with Germany holding a share of 20.12% of the market, supported by its robust economy, diversified retail formats, and expanding build-to-rent developments. German consumers demand eco-labels, high build quality, and modular designs that accommodate tight urban layouts, pushing suppliers to emphasize engineering precision. Nevertheless, growth momentum moderates as inflation tempers discretionary spending, prompting retailers to broaden entry-level assortments. By contrast, the NORDICS region is projected to grow at a 5.05% CAGR, thanks to high disposable incomes, design-centric cultures, and strong circular-economy policies. Scandinavian consumers exhibit high brand loyalty toward manufacturers that marry minimalist aesthetics with documented sustainability credentials.

The United Kingdom faces currency volatility yet remains a key import market where comfort-driven, sectional sofas resonate with compact apartment living. France’s appetite for artisanal craftsmanship sustains premium price bands, while Spain and Italy lean on tourism-fueled hospitality demand to energize commercial sales. BENELUX markets, though small in population, punch above their weight in per-capita furniture spending, rewarding suppliers adept at fulfilling bespoke orders quickly. Eastern European countries such as Poland and Czechia gain share in manufacturing outsourcing, offering cost advantages and near-shoring benefits to Western brands. These geographic nuances underscore the necessity for localized product assortments and multi-speed supply chains within the Europe upholstered furniture market.

Regulatory Landscape

EU-wide product and chemical compliance is tightening for upholstered furniture placed on the single market. The General Product Safety Regulation (EU) 2023/988 applies from 29 May 2026, reinforcing safety, traceability, and recall obligations for consumer goods. Commission Implementing Decision (EU) 2026/901 supports conformity by listing relevant European standards, including standards referenced for childrens furniture safety within the broader product-safety framework.

Materials and circularity rules are directly affecting frames, panels, and upholstery inputs. Under REACH Annex XVII, a formaldehyde-emission limit for furniture and wood-based articles applies from 6 August 2026 (0.062 mg/m3), which pushes manufacturers toward formal testing regimes and tighter component specifications. The European Commissions ESPR working plan (2025-2030) identifies furniture and mattresses as priority product groups for upcoming ecodesign measures, with delegated acts signposted for adoption by 2028. Separately, ECHA is processing PFAS-related restriction work covering textiles, upholstery, leather, apparel, and carpets, raising the urgency for supply-chain audits and alternative chemistries.

Value Chain Analysis

The upholstered-furniture value chain in Europe runs from raw materials (timber and wood-based panels, metals, polyurethane and alternative foams, textile or leather upholstery, adhesives and finishes) into component conversion (cut-and-sew covers, foam shaping, frame fabrication), assembly and upholstery, then packaging, logistics, and retail or contract distribution. Extra-EU sourcing has become more prominent, with imports accounting for about 22% of the European market (up from 18% in 2019), which increases exposure to external supply shocks and intensifies price competition against Europe-based manufacturers.

Compliance and data requirements are starting to sit across upstream tiers, changing supplier qualification and operating processes. Traceability obligations for wood and wood-based inputs under the EU Deforestation Regulation (EUDR) and sustainability due diligence duties tied to the Corporate Sustainability Due Diligence Directive (national implementation due by July 2026) extend documentation, risk screening, and reporting deeper into component and material supply networks. The ESPR direction of travel, including Digital Product Passport preparations (with initial rollout starting in other product groups such as batteries from 2027), also accelerates investment in interoperable product data, testing, and labeling workflows that connect material suppliers, manufacturers, and omnichannel retailers.

Competitive Landscape

The Europe upholstered furniture market remains fragmented, with the five largest players led by IKEA, Steinhoff, Natuzzi, DFS, and Roche Bobois collectively holding only a modest portion of the total market. IKEA leverages scale efficiencies, a vertically integrated supply chain, and buy-back initiatives that closed the loop on 495,000 products in 2024, reinforcing brand equity among eco-conscious buyers. Steinhoff and DFS strengthen omnichannel footprints via store refurbishments and co-branded VR room-planners that simulate fabric swatches under different lighting conditions. Natuzzi doubles down on Italian craftsmanship, launching quick-ship “ready-to-live” collections that balance customized options with faster delivery times. Roche Bobois capitalizes on designer collaborations, keeping high-margin limited editions in constant rotation to protect exclusivity.

Strategic differentiation increasingly centers on sustainability credentials, digital capability building, and supply-chain agility. Market leaders invest in blockchain traceability platforms that map wood origin and carbon intensity, satisfying EU ecolabel requirements and Gen-Z transparency expectations. Investments also pour into AR-enabled configurators and logistics automation, enabling two-man delivery crews to assemble sectionals within 30 minutes, bolstering customer satisfaction. Direct-to-consumer entrants chip away at incumbents by offering simplified value propositions, no-middleman pricing, and subscription or buy-back guarantees. In response, legacy players test flexible rental schemes, forging alliances with fintechs to underwrite residual-value risk. The race to embed recycled PET fabrics and bio-based foams further intensifies as raw-material legislation tightens.

A notable competitive battleground lies in contract channels where hotel chains and build-to-rent developers demand turnkey solutions. Firms with dedicated B2B divisions secure multi-year framework agreements, ensuring predictability in plant utilization and mitigating retail demand swings. White-label manufacturing for private-label retailers grows as mid-tier brands seek margin expansion without in-house production overheads. Consolidation pressures persist, evidenced by targeted acquisitions of niche upholstery specialists that add artisanal capabilities or regional footprint synergies. However, antitrust scrutiny, supply-chain complexity, and cultural integration hurdles slow mega-merger prospects, keeping the Europe upholstered furniture market open for agile challengers.

Europe Upholstered Furniture Industry Leaders

IKEA Group

Steinhoff International

Natuzzi S.p.A.

DFS Furniture Plc

Poltrona Frau

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Circular design and compliance-led product differentiation are creating opportunities for upholstered-furniture players across materials, data, and services. The Ecodesign for Sustainable Products Regulation (EU) 2024/1781 entered into force on 18 July 2024, and the 2025-2030 working plan flags furniture as a priority product group, pushing manufacturers toward designs that support disassembly, repairability, and improved transparency. The REACH formaldehyde limit that applies from 6 August 2026 also increases the value of low-emission panel choices, supplier testing capability, and component-level compliance documentation that can be reused across SKUs.

Channel and business-model shifts support opportunities in modular, parcel-friendly formats and subscription-style utilization models, particularly where retailers and workplace buyers want flexibility. Digital-first modular seating brands such as Swyft and Noah Living illustrate how configuration-led assortments and e-commerce-first discovery are taking share alongside omnichannel retailers, and the report scope also reflects growing furniture-as-a-service adoption in parts of Europe. With extra-EU imports rising and demand described as soft at the start of 2026 in key markets, manufacturers and retailers are leaning into logistics innovation (including compression technologies), localized lead-time advantages, and contract programs tied to build-to-rent and hospitality refurbishment cycles to balance discretionary retail volatility with repeatable B2B volumes.

Recent Industry Developments

- July 2026: DFS Furniture Plc issued a trading update for the year ending 28 June 2026, pointing to improved profitability and lower net bank debt. The update emphasized intensified focus on operational discipline and cost control as furniture demand stayed uneven in several European markets. For competitors, it raised the bar on productivity and margin management in value-led upholstered categories.

- May 2026: Ingka Group (IKEA) opened a compact IKEA store in Limoges, France as part of its France investment plan and broader omnichannel expansion. The smaller-format footprint supports closer-to-home shopping and can be paired with digital ordering and fulfillment for bulky upholstered items. This format shift increases competitive pressure on specialty chains and mid-market retailers that rely on large stores for traffic.

- December 2024: IKEA launched a large mattress recycling facility in France with capacity to process 750,000 mattresses per year. The project strengthened circular-economy infrastructure for bulky sleep products and signals investment in end-of-life pathways adjacent to upholstered beds and related categories. It also supports retailer take-back and recycling propositions that align with tightening EU sustainability expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers upholstered furniture sold in Europe, meaning seating and related furniture where cushioning and coverings (fabric or leather) are a key part of the finished product, and value is measured at the point of sale into end users.

Scope exclusions: We exclude non-upholstered furniture, floor coverings, and standalone textiles or foam sold as raw materials.

Segmentation Overview

- By Product Type

- Chairs

- Sofas

- Tables

- Beds

- Other Product Types

- By Application

- Residential

- Commercial

- By Distribution Channel

- Home Centers

- Flagship Stores

- Specialty Stores

- Online Platforms

- Other Distribution Channels

- By Geography

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building the demand context for home and commercial furniture spending in Europe, then narrowing it to upholstered furniture using product mix signals and trade markers. We referred to public datasets such as Eurostat household expenditure tables (COICOP), Eurostat structural business statistics for furniture manufacturing, and UN Comtrade and EU customs releases that show furniture import and export flows by product code.

To keep the market model grounded in real activity, we also reviewed official macro indicators, including construction and housing renovation statistics from national statistical offices, plus inflation and consumer price index series that help explain price movement. These inputs were complemented with company annual reports, investor presentations, and reputable trade press coverage to pick up demand shifts, channel changes, and sourcing updates. Where needed, we used paid subscriptions for company financials and shipment-level import and export checks to validate directional trends. This desk source list is illustrative only, and many other public references were used during data collection and clarification.

Primary Interviews and Surveys

Primary work focused on validating what sits inside the upholstered furniture boundary, then checking the split across residential and commercial demand and offline versus online sales. We spoke with manufacturers, distributors, retailers, and material buyers, and the discussions covered major European demand centers and smaller import-led markets, so assumptions did not rely on one geography alone.

Respondent input also helped confirm which upholstered items are typically captured in channel reporting versus excluded items that are often sold as semi-finished components.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | |

| Mid tier: 44% | Functional/Unit leaders: 27% | |

| Smaller Players: 19% | Managers: 58% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach, where furniture demand in Europe was reconstructed from household spending patterns, commercial fit-out activity indicators, and trade and production signals that indicate upholstered product intensity. After establishing those totals, we adjusted them using checks on upholstered category mix, the share of imported versus locally produced supply, and typical pricing bands discussed by channel participants.

To keep the final number realistic, we corroborated the totals with selective bottom-up approximations, such as sample country roll-ups, retailer and distributor channel checks, and a simple volume times average selling price build for a few common upholstered items. Housing completions and renovation activity, consumer spending and confidence, import penetration by furniture product codes, raw material driven price movement (foam and textiles), and the pace of online share change were the most influential inputs.

Forecasts were produced using scenario analysis, where the base path was tied to macro demand indicators and then stress-tested for price normalization and housing slowdowns. Where bottom-up coverage was thin for smaller countries, gaps were handled through share-based allocation from regional totals, followed by another round of interview validation.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including trade direction, manufacturing activity, and whether implied per-household spending stayed within reasonable bounds across countries. Outliers were reviewed in a second analyst pass, and any large variance triggered follow-up outreach to re-check channel mix, pricing movement, and one-off project demand.

The dataset is refreshed annually, and interim updates are made when there are material events such as sharp input cost swings, regulatory changes affecting materials, or major demand shocks. Before delivery, we complete a final review to ensure the latest public releases and recent interview feedback are reflected in the market numbers.

Mordor Intelligence's Europe Upholstered Furniture Market Size Versus Other Published Estimates

It is normal to see different market sizes for upholstered furniture in Europe because publishers often draw the boundary in different places, and they do not always use the same price point, channel coverage, or country set. Timing also matters, since furniture pricing and demand can move quickly with housing and consumer confidence.

By tracking import and production signals, refreshing currency timing and inflation adjustments, and then applying an upholstered-only product boundary, Mordor Intelligence avoids counting wider furniture baskets or adjacent home categories that can inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.24 B (2025) | |

| Industry Data Publisher A | USD 20.70 B (2025) | Uses an industry value that is reported in EUR and covers production, consumption, and trade across a broader European country set, which can represent a wider value pool than end-market sales of upholstered items only. |

| Consumer Demand Tracker B | USD 201.00 B (2025) | Measures household spending across furniture, furnishings, and floor coverings for a fixed multi-country Europe basket, so it captures a much broader consumer category and is not limited to upholstered furniture products. |

The spread in the table is mainly explained by scope and what is being counted, since some sources report total consumer furniture baskets or industry-wide value pools instead of upholstered-only sales. With clear inclusions, consistent pricing logic, and repeatable checks against trade and demand indicators, the estimate stays traceable and easier to reuse for planning.

Key Questions Answered in the Report

How large is the Europe upholstered furniture market in 2026?

The Europe upholstered furniture market size stood at USD 4.46 billion in 2026 and is projected to reach USD 5.75 billion by 2031.

What is the expected growth rate for upholstered furniture in Europe?

The market is forecast to grow at a steady 5.22% CAGR between 2026 and 2031 as residential renovations and commercial refurbishments boost demand.

Which product category leads sales across Europe?

Sofas remain the revenue leader, accounting for 34.72% of market share in 2025, supported by modular designs and performance fabrics.

Which distribution channel is expanding fastest?

Online platforms are projected to post a 8.84% CAGR to 2031, driven by AR visualization tools and improved last-mile delivery.

Why are beds the fastest-growing product segment?

Rising consumer focus on sleep wellness and smart-bed technology propels beds at a 6.78% CAGR, outpacing traditional categories.

Page last updated on: