Europe Spectator Sports Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

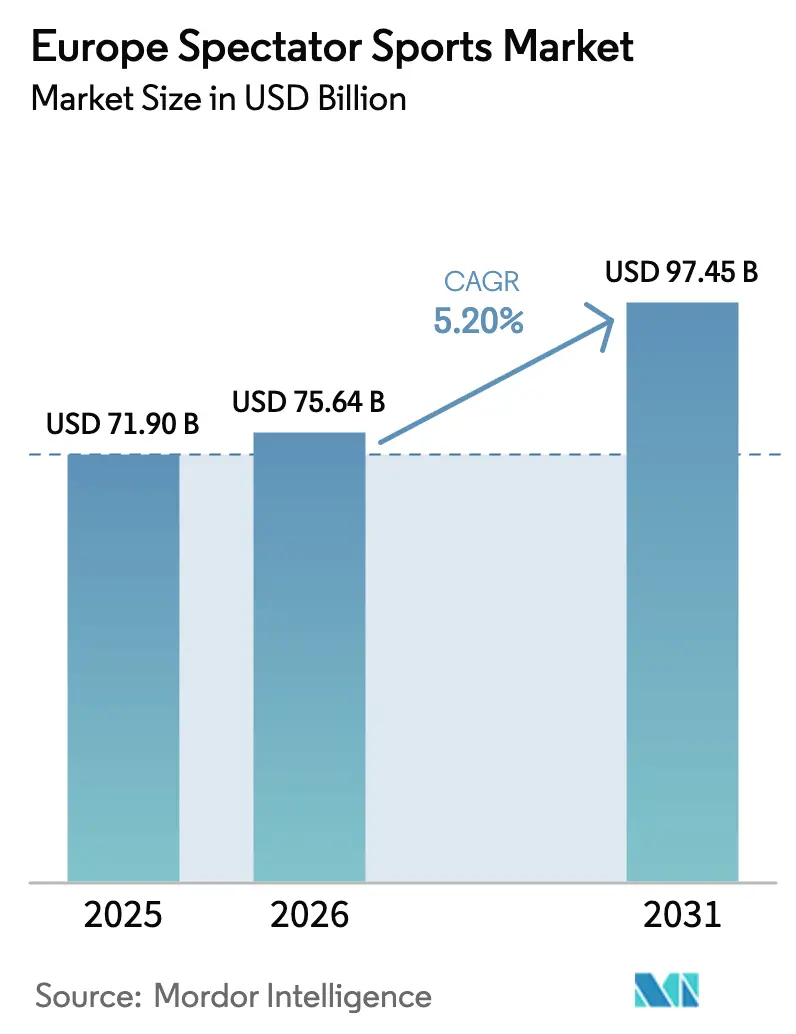

| Base Year Market Size (2025) | USD 71.90 Billion |

| Market Size (2026) | USD 75.64 Billion |

| Market Size (2031) | USD 97.45 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Spectator Sports Market Analysis by Mordor Intelligence

The European spectator sports market size was valued at USD 71.90 billion in 2025 and estimated to grow from USD 75.64 billion in 2026 to reach USD 97.45 billion by 2031, at a CAGR of 5.2% during the forecast period (2026-2031). This upward path reflects the sector’s ability to pivot from pure volume expansion toward value-centric monetization as rights holders package scarce premium content for both traditional and streaming distributors. Surging over-the-top investments, stadium upgrades oriented toward high-margin hospitality, and heightened sponsor appetite for continent-wide activations reinforce dependable revenue visibility. Rights fees continue to underpin the European spectator sports market even as sponsors capture fresh share by demanding data-rich engagement programs. Meanwhile, disciplined clubs gain structural leverage as UEFA intensifies Financial Fair Play enforcement, elevating the cost of non-compliance and tilting competitive balance toward financially prudent organizations[1]Adidas entered Formula 1 through a multi-year partnership with Mercedes-AMG PETRONAS, expanding its motorsport footprint.

Key Report Takeaways

- By type, sports teams and clubs led with 56.12% revenue share of the European spectator sports market in 2025, while racing posted the fastest 9.38% CAGR outlook to 2031.

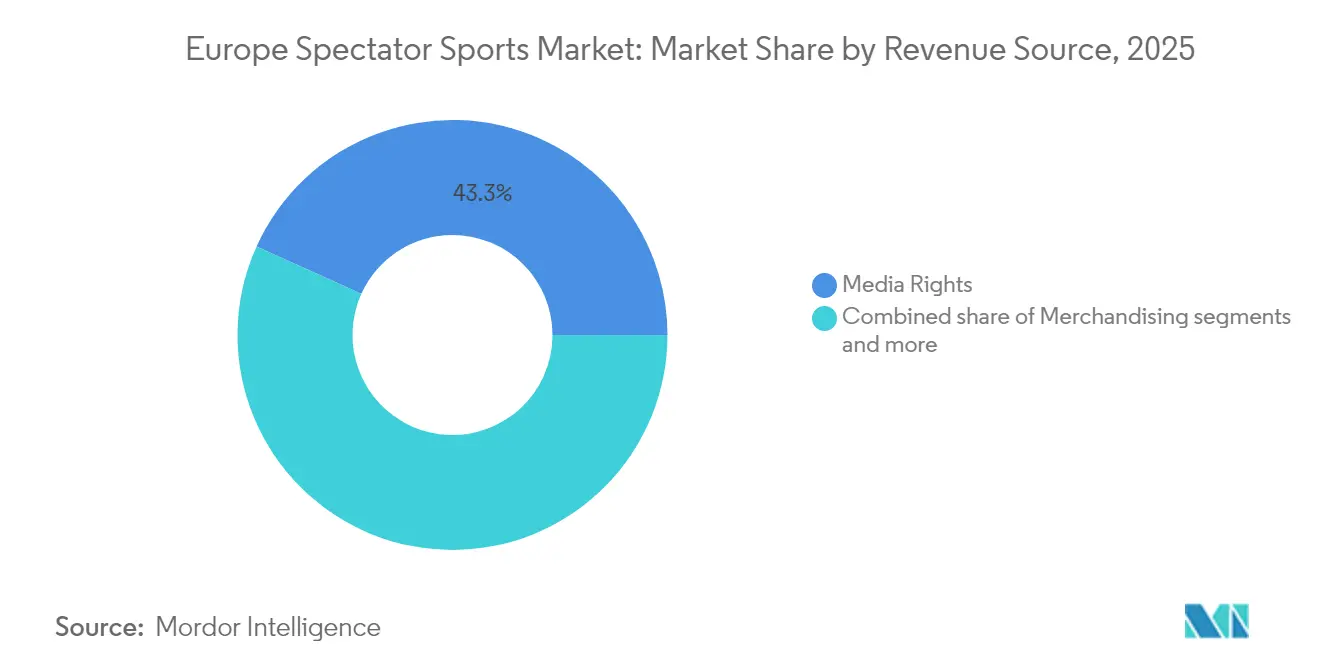

- By revenue source, media rights supplied 43.25% of the 2025 revenue of the European spectator sports market, yet Sponsorship is primed for the quickest expansion at an 11.39% CAGR through 2031.

- By type of sport, soccer retained a 65.74% share of the European spectator sports market, whereas women’s soccer tracks a 13.85% CAGR that significantly outpaces every other discipline.

- By geography, the United Kingdom accounted for 28.05% of the 2025 revenue of the European spectator sports market, while the Nordic bloc is set to deliver the highest 8.05% regional CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global spectator sports market size report represents that cumulative total.

Europe Spectator Sports Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging OTT platform investments | +1.2% | Global, with a concentration in the UK, Germany, and France | Medium term (2-4 years) |

| Expansion of pan-European sponsorship deals | +0.8% | EU core markets, spillover to BENELUX and Nordics | Long term (≥ 4 years) |

| Stadium modernization & premium seating upgrades | +0.6% | UK, Germany, Spain, Italy | Long term (≥ 4 years) |

| Growing popularity of women's professional leagues | +0.9% | Global, with early gains in the UK, Germany, Netherlands | Medium term (2-4 years) |

| Emergence of micro-betting & in-play wagering | +0.7% | EU-regulated markets, excluding restricted jurisdictions | Short term (≤ 2 years) |

| Carbon-neutral event mandates by EU regulators | +0.4% | EU member states, with national implementation variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging OTT Platform Investments

Streaming entrants reshaped European sports economics by bidding aggressively for marquee rights to secure subscriber growth, even at compressed near-term margins. DAZN’s winning of Belgian Pro League packages at USD 87.5 million (EUR 84.2 million) annually through 2030, despite trailing the prior USD 107 million (EUR 103 million) contract, illustrates the strategic willingness to trade profitability for scale[2]Chambers and Partners, “Sports Law 2025 – Belgium,” practiceguides.chambers.com . Global actors such as Amazon and Disney exploit vast customer ecosystems to position sport as a loyalty anchor, not a standalone profit silo. As legacy broadcasters adjust, many must either raise rights spend or diversify content slates, catalysing new bidding cycles that continue to elevate asset values. The power shift ultimately accelerates the convergence of media, commerce, and data analytics across the European spectator sports market.

Expansion of Pan-European Sponsorship Deals

Multinational brands increasingly prefer continent-spanning partnerships that streamline activation costs while guaranteeing cohesive storytelling across borders. PepsiCo’s comprehensive renewal with UEFA Women’s Football embodies this strategic pivot by bundling multiple beverage brands across all women’s competitions through 2030[3]PepsiCo, “PepsiCo extends UEFA Women’s Football partnership through 2030,” pepsico.com . Such broad agreements grant rights holders predictable, inflation-indexed cash flows that support long-range planning. Economies of scale in creative production and media buying deliver measurable return on investment for sponsors even amid economic volatility. Adidas secured a multi-year exclusive kit supply agreement with Liverpool FC, demonstrating the strategic value of leveraging a single contract to address both domestic and international markets. This approach reinforces competitive barriers, providing an advantage to sports organizations capable of monetizing their assets on a pan-regional scale.

Stadium Modernization & Premium Seating Upgrades

Prominent European sports venues are implementing large-scale redevelopment projects to diversify and expand revenue streams beyond traditional ticket sales. Real Madrid's redevelopment of the Bernabéu stadium incorporates advanced features such as retractable pitch systems, mixed-reality zones, and high-value 360-degree hospitality lounges designed to attract premium pricing. Similarly, Barcelona's Camp Nou renovation includes upgraded VIP suites, Net-Zero design initiatives, and infrastructure optimized for year-round event hosting. These strategic investments address shifting consumer demands for enhanced comfort and digital integration, enabling clubs to achieve higher revenue per attendee. Additionally, improved sustainability measures position these venues as attractive partners for corporations prioritizing ESG objectives. The significant capital requirements of these projects reinforce the financial stability of established franchises within the European spectator sports market.

Growing Popularity of Women’s Professional Leagues

High-visibility media windows, improved athlete remuneration, and corporate focus on diversity propelled women’s competitions from niche status to scalable commercial engines. BBC’s free-to-air coverage of the Women’s Super League, coupled with dedicated UEFA broadcast slots, expanded reach to new demographics. Brands leverage authentic storytelling to engage female fans and socially conscious millennials, translating into rising sponsorship valuations. Reinforced revenue flows fund enhanced production quality and grassroots development, fostering a virtuous cycle of fan growth and performance improvement. The 14.73% CAGR attached to women’s soccer underscores its outsized momentum relative to mature male competitions within the European spectator sports market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating player salary inflation | -0.9% | Global, with a concentration in top-tier leagues | Short term (≤ 2 years) |

| Saturation of traditional broadcast slots | -0.7% | Mature markets: UK, Germany, France, Italy | Medium term (2-4 years) |

| Heightened concussion-related litigation risk | -0.5% | EU-wide, with the UK leading legal precedents | Long term (≥ 4 years) |

| Stricter state-aid & Financial Fair-Play enforcement | -0.8% | EU member states under UEFA/FIFA jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Concussion-Related Litigation Risk

Legal actions initiated by former rugby and soccer athletes in the United Kingdom, alleging negligence in head-injury protocols, represent a significant potential liability for governing bodies. These lawsuits highlight concerns over historical practices and the adequacy of measures implemented to address player safety. In response, governing organizations have introduced extended substitution rules and mandatory pitch-side concussion assessments. However, the plaintiffs argue that these measures fail to address past shortcomings, calling for retrospective accountability. The rising cost of insurance premiums further compounds the issue, particularly for smaller organizations with limited or undiversified revenue streams, which may struggle to absorb the increasing expenses associated with risk management. Additionally, advancements in scientific research related to head injuries could broaden the scope of potential claimants, creating further financial strain. This scenario poses a risk to the long-term cash flows required to sustain grassroots investments, potentially impacting the development and growth of these sports at foundational levels.

Stricter State-Aid & Financial Fair Play Enforcement

UEFA levied a USD 36.5 million (EUR 31 million) fine on Chelsea in 2024 for accounting irregularities, while FC Barcelona faces sanctions tied to wage-to-revenue thresholds[4]UEFA, “Financial Fair Play update 2024,” uefa.com . Increased regulatory oversight imposes constraints on leveraged expansion models, restricts roster investments, and reduces strategic flexibility for clubs. However, organizations that adopt fiscally disciplined approaches gain a competitive advantage by allocating resources toward youth academy development and enhancing digital fan engagement initiatives. As regulatory enforcement becomes more consistent, the growth potential of the European spectator sports market is expected to moderate. Nevertheless, this shift is likely to foster improved financial stability over the long term, creating a more sustainable operational environment for market participants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Teams, Anchor Ecosystem, Monetization

Sports Teams and Clubs captured 56.12% of Europe's spectator sports market share in 2025, reflecting their unrivalled capacity to generate year-round content and monetize omni-channel fan touchpoints. Their licensing control over athlete IP, stadium access, and historical branding forms entry barriers unattainable for individual sports collectives. Europe's spectator sports market is poised for a steady ascent, fuelled by the rise of subscription OTT channels, dynamic ticketing strategies, and global merchandise releases. Simultaneously, Racing entities register a 9.38% CAGR as Formula 1 exploits Netflix-era storytelling and introduces Las Vegas-style destination grands prix that appeal to tourists and corporate hospitality buyers.

Teams exploit transfer windows, off-season tours, and academy content to sustain engagement outside competition calendars, underpinning sponsorship renewals and data-driven upselling. Racing’s acceleration invites cross-industry partnerships—Adidas’ entrance with Mercedes-AMG PETRONAS F1 grants brand exposure to an affluent, tech-savvy audience. Individual Sports sustain steady cash flow via lower cost structures and niche fan loyalty but lack the leverage to command super-premium rights fees, capping their relative expansion within the European spectator sports market.

By Revenue Source: Sponsorship Outpaces Media Rights

In 2025, Media Rights accounted for the largest share at 43.25%, reflecting its continued dominance in the revenue mix. However, the 11.39% CAGR projected for Sponsorships highlights a strategic shift in revenue generation, emphasizing activation-focused initiatives. Sponsors are increasingly prioritizing access to intellectual property, customized content creation, and the integration of first-party data over traditional logo placements. This evolving preference is driving a reallocation of sponsorship budgets, with companies opting for fewer but more strategically significant partnerships to maximize value and engagement.

Merchandise channels face commodification as e-commerce giants squeeze margins, prompting clubs to differentiate via limited-edition drops and sustainable materials. Ticketing evolves toward mobile-first, algorithmic pricing that maximizes occupancy while mining behavioural data for incremental monetization. Entities possessing proprietary ticketing platforms retain higher customer lifetime value and resilience against broadcasting volatility.

By Sport: Women’s Soccer Drives New Growth Layers

Soccer dominated with 65.74% share in 2025, reinforcing its role as the Europe spectator sports market’s commercial backbone. Yet Women’s Soccer delivers a standout 13.85% CAGR, buoyed by dedicated broadcast slots and sponsor inclusivity objectives. Newly mandated equal-production standards assure high-quality coverage, increasing average minute ratings and commanding premium advertising CPMs. The Europe spectator sports market size for women’s competitions, while starting from a smaller base, is slated to triple by 2030, reflecting strong demand elasticity.

Cricket, Rugby, and Tennis maintain loyal yet segmented followings, generating steady rights income through exclusive pay-TV contracts. Regulatory initiatives such as UEFA’s menstrual-health research further augment athlete well-being and brand reputations, reinforcing long-term engagement. Emerging sports like padel and esports leverage cost-efficient event formats to tap Gen Z audiences, supplying diversification avenues for broadcasters seeking differentiated content portfolios within the European spectator sports market.

Geography Analysis

The United Kingdom retained leadership with 28.05% of 2025 revenue, supported by the Premier League’s worldwide syndication and deeply entrenched subscription culture. Sky Sports' expanded 215-match package exemplifies domestic capacity to absorb premium inventory without dampening demand. Currency hedging and sophisticated financial intermediation ease global commercialization for British clubs.

The football markets in France, Spain, and Italy, while holding a significant share in the global industry, are encountering notable obstacles. These markets are witnessing a steady outflow of skilled players to leagues offering more lucrative financial packages, which undermines their ability to retain top talent and maintain competitive strength. Furthermore, macroeconomic challenges, such as declining consumer spending, are creating additional pressure on revenue generation and overall market stability. To address these issues, stakeholders are increasingly adopting innovative sponsorship strategies. For instance, France has implemented multi-club cryptocurrency partnerships, which serve as a strategic approach to diversifying income streams and enhancing financial resilience amidst ongoing economic uncertainties. Nordic markets emerge as the fastest-growing bloc at an 8.05% CAGR through 2031 thanks to ubiquitous broadband, club-member ownership models fostering loyalty, and governmental grants for carbon-neutral venue retrofits. BENELUX leverages multilingual capabilities to syndicate content across adjacent territories efficiently, while the Rest of Europe, encompassing Poland, Greece, and the Balkans, offers long-run upside as middle-class consumption converges with Western standards. High cross-border digital penetration reduces logistical barriers, ensuring that the Europe spectator sports market maintains a region-wide addressable base.

Coverage of the spectator sports market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia and North America, alongside detailed country-level intelligence for United Kingdom and India, each shaped by local operating conditions.

Competitive Landscape

The European spectator sports market remains moderately fragmented, with leading entities such as UEFA Events SA, Formula One Group, Premier League Ltd, Real Madrid CF, and Manchester United PLC collectively accounting for a limited share of the overall revenue. This fragmented structure sustains competitive dynamics in bidding processes for broadcasting and sponsorship rights, while also enabling smaller leagues to maintain bargaining leverage. The entry of private-equity firms, including CVC and Apollo, has introduced a strategic focus on undervalued franchises, driving selective consolidation efforts without significantly disrupting the market's diverse composition.

Technological advancements are reshaping the competitive landscape within the market. Sports clubs are increasingly adopting AI-driven tools for performance analytics and personalized fan engagement applications, which are designed to optimize average revenue per user. Simultaneously, leagues are integrating innovative technologies such as connected-ball sensors, first showcased during the UEFA Women’s EURO 2025, to enhance their data licensing capabilities and unlock new revenue streams.

Regulatory changes are introducing potential systemic challenges to the market. The Court of Justice of the European Union's Diarra ruling, which addresses back-dated compensation claims, has the potential to significantly impact the distribution of transfer fees across the ecosystem. Clubs that have proactively diversified their revenue models through subscription-based platforms and multi-faceted event programming are better positioned to mitigate the risks associated with regulatory shifts while capitalizing on emerging growth opportunities within the European spectator sports market.

Europe Spectator Sports Industry Leaders

Manchester United plc

FC Barcelona

Real Madrid CF

Formula One Group (Europe events)

FC Bayern Munich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: UEFA introduced connected-ball technology at Women’s EURO 2025.

- April 2025: PepsiCo has extended its partnership with UEFA to remain a sponsor of women's football through 2030. This strategic collaboration underscores PepsiCo's commitment to fostering the growth of the sport by engaging players, fans, and communities on a global scale.

- March 2025: Adidas has entered into a multi-year agreement with Liverpool Football Club, under which the sportswear company will serve as the club's official kit partner starting from the 2025/26 season.

- January 2025: Adidas entered Formula 1 through a multi-year partnership with Mercedes-AMG PETRONAS, expanding its motorsport footprint.

Europe Spectator Sports Market Report Scope

A spectator sport is one in which spectators, or observers, attend matches such as American football, association football, baseball, basketball, Canadian football, cricket, field hockey, Formula 1, ice hockey, rugby league, rugby union, team handball, and volleyball. Types of spectator sports Sports teams and clubs Racing Individual sports Revenue sources Media rights Merchandise Ticket sales Sponsorship Types of sports Soccer Cricket Rugby/football Tennis Other Europe Spectator Sports Market is segmented By Type (Sports Team And Clubs, Racing, Individual Sports), By Revenue Source (Media Rights, Merchandising, Tickets, Sponsorship), By Type Of Sport (Soccer, Cricket, Rugby/Football, Tennis, Other Types Of Sports), By Countries (Germany, United Kingdom, France, Italy, Russia, Spain, Rest Of Europe). The report offers market sizes and forecasts for the Europe Spectator Sports Market in value (USD) for all the above segments.

| Sports Team and Clubs |

| Racing |

| Individual Sports |

| Media Rights |

| Merchandising |

| Tickets |

| Sponsorship |

| Soccer |

| Cricket |

| Rugby/Football |

| Tennis |

| Other Types of Sports |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX |

| NORDICS |

| Rest of Europe |

| By Type | Sports Team and Clubs |

| Racing | |

| Individual Sports | |

| By Revenue Source | Media Rights |

| Merchandising | |

| Tickets | |

| Sponsorship | |

| By Type of Sport | Soccer |

| Cricket | |

| Rugby/Football | |

| Tennis | |

| Other Types of Sports | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe |

Key Questions Answered in the Report

What is the forecast value of the European spectator sports market by 2031?

It is projected to reach USD 97.45 billion, reflecting a 5.2% CAGR from 2026.

Which revenue stream is growing fastest within European sports?

Sponsorship revenue is set to expand at 11.39% CAGR as brands seek data-rich, pan-European partnerships.

Why are women’s leagues important to future growth?

Women’s soccer delivers a 13.85% CAGR, driven by dedicated broadcast slots and corporate inclusion mandates that attract new sponsors.

Which region shows the highest growth momentum?

The Nordic countries are expected to post an 8.05% CAGR through 2031 thanks to strong digital adoption and public funding for sustainable venues.

How will stricter Financial Fair Play rules affect clubs?

They favour financially disciplined organizations by limiting leveraged spending, thereby shaping a more sustainable competitive environment across Europe.

Page last updated on: