Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 29.35 Billion |

| Market Size (2026) | USD 30.39 Billion |

| Market Size (2031) | USD 36.02 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Textile Market Analysis by Mordor Intelligence

The Europe home textile market size stood at USD 30.39 billion in 2026, up from USD 29.35 billion in 2025, and is projected to reach USD 36.02 billion by 2031 at a 3.46% CAGR. Momentum is supported by steady household replacement cycles, the normalization of travel and lodging activity, and stronger procurement needs from hospitals and municipalities that now specify certified sustainable linens in tenders. The policy push for traceable and circular textiles, including Digital Product Passports, is elevating compliance requirements for importers and EU manufacturers while creating a product differentiation pathway for brands with credible environmental data. Cotton remains the dominant fiber in 2026, while linen grows faster on the back of record European flax acreage and a clear sustainability narrative that resonates with premium buyers[1]European Commission, “Green Public Procurement,” European Commission, environment.ec.europa.eu . Germany provides the largest country contribution, while the Nordics advance at the fastest pace through 2031.

Key Report Takeaways

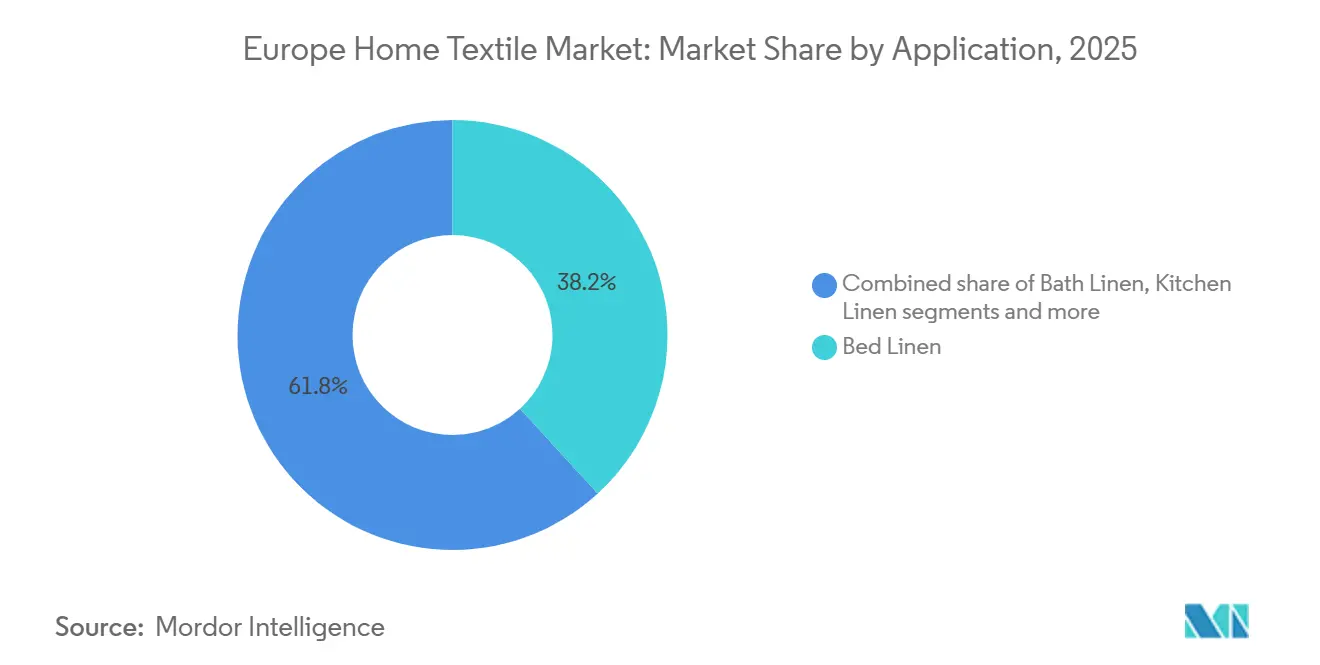

- By application, bed linen captured a 38.20% share in 2025 in the Europe home textile market. Bath linen is projected to grow at the fastest-growing pace, with a 4.42% CAGR through 2031.

- By material, cotton led with 52.65% revenue share in 2025 for the Europe home textile market, whereas Linen is forecast to expand at a 3.83% CAGR through 2031.

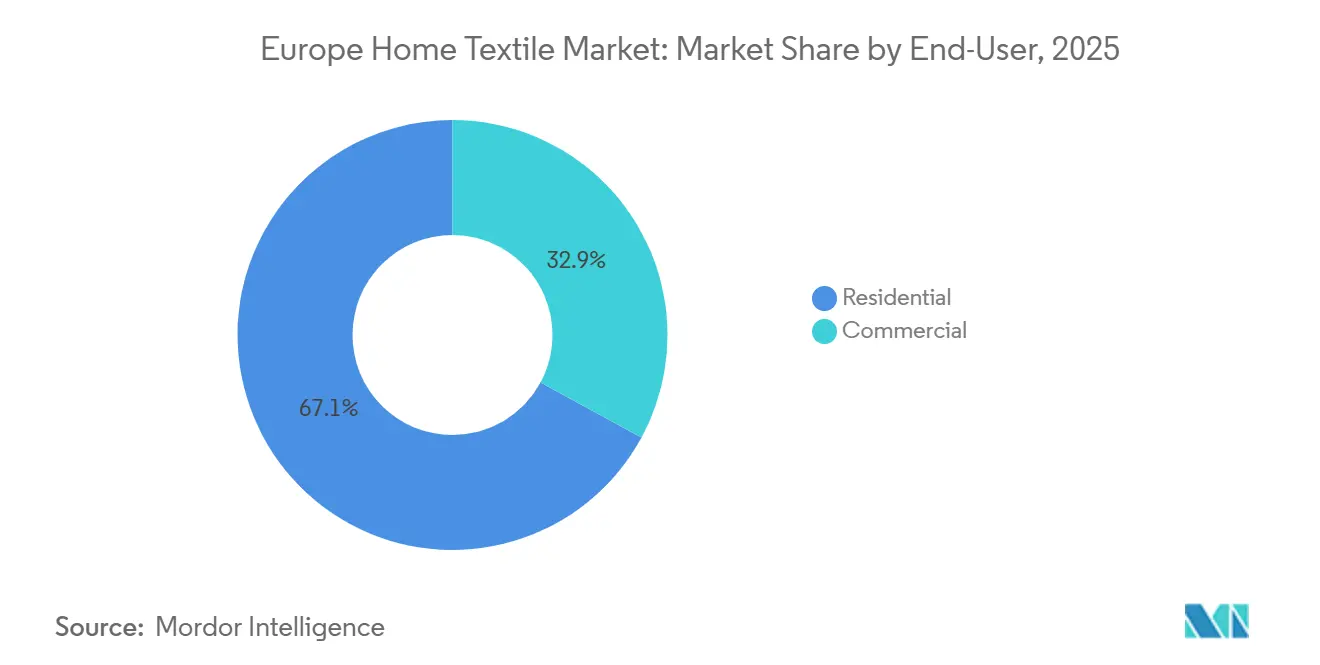

- By end-user, residential accounted for 67.10% of 2025 revenue in the Europe home textile market. The commercial segment is projected to grow at a 3.57% CAGR through 2031.

- By distribution channel, B2C retail commanded 72.75% of 2025 revenue in the Europe home textile market. B2B direct channels are set to be the fastest, with a 4.06% CAGR through 2031.

- By geography, Germany led with 22.10% in 2025 in the Europe home textile market. The Nordics region is forecast to post the fastest growth at a 5.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation-Driven Replacement Demand in EU Housing | +0.8% | Germany, France, United Kingdom | Medium term (2–4 years) |

| E-Commerce and Omnichannel Expansion in Home Textiles | +1.1% | Pan-European, strongest in Nordics and Benelux | Short term (≤ 2 years) |

| Sustainability-Led Premiumization (Eco-Labels, Organic, Recycled Fibers) | +1.2% | Nordics, Germany, France | Medium term (2–4 years) |

| Hospitality and Short-Stay Rebound Lifting Commercial Linen Turnover | +0.7% | Spain, Italy, France | Short term (≤ 2 years) |

| EU Green Public Procurement Boosting Certified Textile Demand | +0.6% | EU-27 with early adopters in Denmark, Austria, Netherlands | Long term (≥ 4 years) |

| EU Digital Product Passports Enabling Traceability-Led Differentiation | +0.5% | EU-27, with first movers in France and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renovation-Driven Replacement Demand in EU Housing

Home-improvement activity, which had peaked after the pandemic, stabilized yet continued to support soft-furnishings refresh cycles in 2025 and into 2026. The upgrade path favors premium thread counts, certified organic options, and verified chemical safety, as households allocate a portion of their décor budgets to durability and environmental assurances. Retailers that streamlined discovery and fit confirmation through guided digital tools also saw smoother conversion and fewer returns, a pattern seen in the growth of digitally assisted sales in large home retailers. In the United Kingdom, Dunelm reported gains in market share and higher digital participation, underscoring how omnichannel journeys shorten time-to-purchase for complex items like curtains and bed sets. As EU Extended Producer Responsibility rules move into implementation phases, design-for-circularity and durability features in home linens gain strategic weight in assortment planning[2]Dunelm Group, “FY25 Preliminary Results and H1 FY26 Update,” Dunelm Group plc, corporate.dunelm.com .

E-Commerce and Omnichannel Expansion in Home Textiles

Retailers in 2026 operate unified commerce models that blend online inspiration with store pickup and returns, reducing friction for bulky or touch-dependent products like quilts and towels. Dunelm stated that online channels accounted for a significantly larger share of sales in fiscal 2025 than pre-2020, reflecting the durability of digital demand even as stores remain central for tactile validation. Augmented reality visualization and guided search reduce color-match uncertainty and help buyers calibrate size and drape before checkout. Supply-chain integration with store networks, parcel lockers, and scheduled delivery improves speed and reliability for weekend renovation timelines. The result is a more predictable demand cadence for frequent-use items, which supports planning for targeted replenishment in the Europe home textile market.

Sustainability-led premiumization (eco-labels, organic, recycled fibers)

Consumer and institutional procurement preferences are shifting toward certified fibers, low-chemical treatments, and verifiable traceability, which supports price premiums for linens bearing recognized badges. European flax cultivation is expanding and benefits from agronomic traits that resonate with eco-conscious buyers, including its suitability for rain-fed growth and its carbon-sequestering potential in the field. The Alliance for European Flax-Linen & Hemp reported consecutive acreage peaks through 2026 sowings, underscoring the growing availability of linen-rich home textile assortments. New certification architectures, such as the Master's of FLAX FIBRE program, formalize traceability through digital credentials that align with upcoming EU Digital Product Passport requirements[3]Alliance for European Flax-Linen & Hemp, “Flax-Linen Market and Certification,” Alliance for European Flax-Linen & Hemp, europeanflax.com . Parallel moves in recycled-cotton supply, including pilots and long-term partnerships between fiber innovators and large apparel retailers, are building capacity that home textile suppliers can leverage for bedding and towel lines.

Hospitality And Short-Stay Rebound Lifting Commercial Linen Turnover

As travel patterns normalized through 2025 and into 2026, hotel and serviced-accommodation operators resumed capital spending on rooms and soft goods, including higher-spec linens designed to withstand frequent industrial laundering. Textile rental and outsourcing models continue to gain traction among hospitality and healthcare facilities, improving hygiene assurance and smoothing operating costs. Rising occupancy intensity in beach and city hubs shortens replacement intervals, which benefits suppliers of durable sateen weaves and high-stability finishes. Short-term rental platforms are also operating under new EU data rules that improve transparency for municipalities, encouraging professionalization among hosts and influencing the adoption of commercial-grade textiles. These vectors combine to lift the commercial refresh rate in the Europe home textile market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Input cost volatility (cotton, energy) compressing margins | -0.9% | Pan-European manufacturing, acute in Italy and Portugal | Medium term (2–4 years) |

| Soft housing cycle and high mortgage rates damping décor spend | -0.7% | United Kingdom, Germany | Short term (≤ 2 years) |

| PFAS and chemical restrictions raising reformulation costs | -0.4% | France and Denmark, with spillovers across EU supply chains | Medium term (2–4 years) |

| Microfibre shedding and microplastics rules tightening on synthetics | -0.3% | France and EU-27 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Input Cost Volatility Compressing Margins

Cotton price oscillation in 2024 created budgeting challenges for mills already working with tight EBITDA profiles, which restrained aggressive new product introductions at the value end of the assortment. Energy expenses for finishing steps also increased in several EU manufacturing hubs, and higher unit costs were difficult to pass through in mass-market bedding categories where import competition is intense. The long-fiber flax segment experienced price spikes in 2025 before easing into late year, yet levels remained above the prior-year baseline. Volatility in flax yields across recent seasons added to the planning complexity for linen-focused weavers, even as acreage expanded. These pressures narrowed flexibility around promotional pricing in the Europe home textile market.

Soft Housing Cycle and High Mortgage Rates Damping Décor Spend

Monetary policy settings in 2025 kept borrowing costs elevated, limiting discretionary outlays on nonessential home upgrades in several large economies. The Bank of England’s policy stance and the European Central Bank’s deposit rate posture delayed some purchases of large-ticket furnishings and slowed the pace of first-home outfitting. Retailers responded with value-led assortments and expanded entry-price options while maintaining premium capsules for higher-income shoppers. The mix shifted toward essentials and away from highly seasonal novelty items in some channels. This backdrop tempered upside for impulse textile refreshes and reinforced a focus on durable, longer-life options as consumers stretched replacement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Anchors Revenue While Bath Linen Gains Share on Hygiene and Service Models

Bed linen accounted for a 38.20% share in 2025, reflecting its role as the most frequently purchased home textile category in both residential and light commercial settings. Hotels and care facilities that reset standards in the wake of the pandemic continue to refresh bed sets, which supports base volumes even as households elongate replacement cycles in a higher-rate environment. Bath linen is projected to be the fastest-growing application to 2031 with a 4.42% CAGR, supported by hospitality demand, healthcare hygiene benchmarks, and textile-rental services that optimize turnover. Increased adoption of antimicrobial verification and industrial-laundry durability standards also lifts specifications for terry and waffle constructions. These shifts encourage suppliers to emphasize cotton-rich blends with verified performance and to develop premium quick-dry and low-pilling options.

Institutional buyers have expanded the use of framework agreements and service contracts across both bed and bath categories, providing end users with predictable quality and volume while pushing suppliers to maintain certifications. The emergence of standardized procurement criteria tied to eco-labels and life-cycle scoring rewards product lines that can document recyclability and compliance with restricted substances. Retail assortments mirror this emphasis by offering curated certified capsules and takeback options that channel end-of-life textiles into reuse or recycling. As this alignment deepens, bath linen’s share gain is expected to outpace bed linen over the forecast period, even as bed sets remain the revenue anchor in the Europe home textile market. This balance preserves scale in core SKUs while creating headroom for innovation in terry constructions and hybrid cotton-linen blends.

By Material: Cotton Retains Leadership While Linen Accelerates on Flax Acreage Expansion

Cotton controls 52.65% of the material mix in the Europe home textile market in 2025, supported by deep supply chains, consumer familiarity, and a wide price ladder that serves both mass and premium tiers. The fiber’s comfort profile, breathability, and finish versatility make it the default for bed and bath lines, and its availability under organic and Better Cotton standards allows retailers to scale certified options. Linen is forecast to expand at a 3.83% CAGR to 2031, benefiting from consecutive peaks in European flax acreage and a rising preference for natural fibers with strong provenance. As sowings remain high through the 2026 harvest period, linen availability supports broader use beyond table and décor into higher-volume bedding and towels with blended constructions.

Regulatory dynamics shape synthetic-fiber adoption across home categories as PFAS reformulation requirements and fiber-shedding scrutiny tighten performance expectations. Suppliers are responding by refining yarn engineering, adjusting finishes, and investing in testing protocols that validate lower shed rates. On the natural side, certification schemes for European flax incorporate digital credentials, which shorten audit cycles for buyers and help verify claims that matter in public tenders. Recycled-cotton capacity additions and partnerships with global retailers demonstrate how scale can drive the integration of circular inputs that ultimately extend to home textiles. These moves are strengthening the premium narrative around natural fibers and verified recycled content in the Europe home textile market.

By End-User: Residential Dominates While Commercial Leads Growth on Professional Standards

Residential accounted for 67.10% of revenue in 2025 as home-centric lifestyles maintained an elevated baseline for comfort and décor refreshes post-2020. The category continues to rely on seasonal updates and targeted promotions that align with payday cycles and holiday periods. The commercial segment is projected to expand to a 3.57% CAGR through 2031 as hotels, short-stay operators, and healthcare facilities refresh more often and to higher standards. Textile-as-a-service continues to appeal to operators seeking bundled supply, laundering, and end-of-life handling, with documentation that supports audits and brand standards. Procurement teams in municipalities and hospitals request labels and verifications that signal compliance with EU and national rules, pushing vendors to provide reliable chain-of-custody and chemical-safety data.

The United Kingdom National Health Service’s hygiene protocols and bed-capacity dynamics support a consistent floor for institutional demand for bed and bath sets, and similar patterns exist across continental systems. Public procurement criteria that incorporate environmental and product-safety parameters move the market toward consistent, scale-wide certification and traceability requirements. In parallel, short-stay rental data-sharing rules in the EU will improve transparency for local authorities, which further raises the bar on consistency and standards among hosts that professionalize their operations. This structural shift strengthens the growth outlook for commercial channels in the Europe home textile market while preserving household-led volumes in the residential base. Suppliers that operate across both end-user groups can smooth volatility by balancing contract-driven and retail-driven demand.

By Distribution Channel: Store-Led B2C Scale Anchors the Base, While B2B Direct Scales Fast

B2C retail channels accounted for 72.75% of 2025 revenue, reflecting the enduring role of stores for touch, color, and drape confirmation as well as the breadth of selection. Online growth has reshaped how shoppers discover and evaluate textiles, with leading retailers reporting a significant increase in digital participation in 2025. Click-and-collect, appointment-based consultations, and curated in-store rooms speed final choice for high-consideration products like curtains and upholstered décor. In the premium segment, specialty players lean into personalization and provenance storytelling to sustain pricing power. This balance of scale from generalists and premium from specialists defines the retail-led foundation of the Europe home textile market.

B2B direct is projected to be the fastest-growing channel with a 4.06% CAGR through 2031 as institutional buyers specify thread count, laundering durability, and certification badges in bulk orders. Direct relationships simplify verification of Digital Product Passport readiness and EPR documentation, which is increasingly requested by municipalities and hospitals in tenders. Marketplace operators and brand portals have added filters that highlight eco-labels and recycled-content claims, which aligns product discovery with procurement scorecards. Suppliers that can configure bulk customization, including monogramming or contract-grade finishes, capture value and stickiness with hotels and care providers. This evolution enhances the resilience of the Europe home textile market by diversifying demand across consumer and institutional pathways.

Geography Analysis

Germany holds a 22.10% share of the European home textile market in 2025, supported by a dense manufacturing ecosystem, a strong DIY and home-improvement culture, and long-established design capabilities. The country’s retail landscape supports both value and premium tiers, which sustains a balanced assortment of certified cotton and linen options. The Nordics are forecast to post the fastest growth at 5.08% CAGR through 2031, underpinned by strong adoption of traceability tools and a premium hospitality pipeline that specifies sustainable linens. These markets also operate advanced digital retail models, which help translate consumer sustainability preferences into higher-value purchases. The combined effect supports a favorable mix shift toward certified and premium SKUs across Northern Europe.

In Southern Europe, tourism-linked demand in resort and city markets sustains a robust floor for commercial lines. Spain and Italy see continued refresh activity as operators align with new service and hygiene expectations, particularly in upscale segments. France’s regulatory path on PFAS and microfibre shedding influences suppliers serving the domestic market and those exporting into France, accelerating reformulation and documentation. Italy and Portugal remain important manufacturing nodes for finishing and cut-and-sew, and energy dynamics in those markets factor into pricing strategies. These trends shape how suppliers allocate capacity across the export and domestic channels in the Europe home textile market[4]Legifrance, “PFAS Decree 2025-1376,” Government of France, legifrance.gouv.fr.

Central and Eastern Europe account for a growing share of regional capacity expansion and logistics investment. JYSK strengthened its footprint across the region and announced plans for a new distribution center in Italy to support broader European growth from 2027. Benelux serves as a logistics hub for Northern and Western Europe, with large, automated facilities that streamline replenishment and returns. The United Kingdom remains a digital bellwether in the region, as major retailers report strong online sales and expanding omnichannel services. Together, these investments improve service levels and responsiveness, which supports steady throughput for bed, bath, and window coverings in the Europe home textile market.

Competitive Landscape

The Europe home textile market is moderately fragmented as import competition remains strong and as category breadth dilutes brand concentration in many countries. Scale retailers continue to expand store networks and omnichannel capabilities, while premium specialists grow through provenance, certification, and bespoke services. Dunelm invested in vertical capabilities and enhanced AI-powered search and recommendations to lift conversion and purchase frequency. IKEA advances its sustainability credentials through renewable energy sourcing and materials targets, reinforcing consumer trust across its value-priced lines.

Strategy is bifurcated between mass retail scale and premium specialization. JYSK expanded its store base and logistics infrastructure to improve availability across Europe, while luxury and upper-mid brands such as Frette maintained a focus on craftsmanship, hotel partnerships, and personalization. Inditex reported progress on lower-impact and recycled fibers across its home and apparel assortments, and partnerships with next-generation material innovators indicate a long-term supply strategy in line with evolving regulations. These moves align with procurement shifts that reward documentation, circularity, and transparency in chemistry. They also create space for certification-led brand positioning in the Europe home textile market.

Innovation in materials and processes remains a core differentiator. Associated Weavers showcased recycled-content carpet and backing systems that contribute to circularity goals in commercial and residential settings. Equipment suppliers introduced weaving and finishing advancements that help mills improve speed, reduce waste, and enhance pattern complexity. Across the value chain, suppliers invest in Digital Product Passport readiness and LCA reporting to shorten audit cycles for both retailers and public-sector buyers. These capabilities support procurement decisions and reduce the risk of regulatory noncompliance as ESPR and related measures phase in, which benefits prepared players in the Europe home textile market.

Europe Home Textile Industry Leaders

IKEA (Ingka Group)

JYSK

Zara Home (Inditex)

NEXT plc (Home)

Dunelm Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The European Commission introduced new rules under the Ecodesign for Sustainable Products Regulation banning the destruction of unsold apparel, clothing accessories, and footwear, effective July 19, 2026, for large companies and 2030 for medium-sized firms, compelling brands to adopt donations, reuse, or alternative retail channels instead of disposal, and mandatory public disclosure of discarded volumes begins February 2027.

- December 2025: JYSK announced plans to open a new distribution center in Italy by the end of 2027 to support growth in Italy and other European markets, and the company celebrated its 100th store opening in Italy in April 2025 and reached 3,575 stores across 50 countries in FY25, welcoming 13.7 million new customers and achieving DKK 46.3 billion turnover.

- November 2025: JYSK installed its largest solar panel farm at its Radomsko, Poland, distribution center, capable of producing up to 30% of its own electricity, and reported that 94% of suppliers by emissions are committed to SBTi-validated climate targets by FY28.

- October 2025: The Revised Waste Framework Directive entered into force, establishing mandatory Extended Producer Responsibility schemes for textile and footwear products across all EU Member States, with producers required to pay eco-modulated fees based on sustainability criteria and with Member States having 20 months to transpose and 30 months to establish operations.

Europe Home Textile Market Report Scope

Home textiles can be defined as fabrics and clothes used specifically for decorative purposes and functional reasons. Quilts, Pillows, Duvet covers, blankets, rugs, and curtains exist among some of the commonly used home textile products.

The study gives a brief description of the European home textile market. It includes details on the market size of European home textiles, investment by home textile firms, technological innovation, and the launch of new home textile products. Europe's home textile market is segmented by product, by distribution channel, and by country. By product, the market is segmented into bed linen, bath linen, kitchen linen, upholstery covering, and floor covering. By distribution channel, the market is segmented into supermarkets and hypermarkets, specialty stores, online distribution channels, and other distribution channels. By country, the market is segmented into the United Kingdom, Germany, France, Italy, and the rest of Europe.

The report also covers the market sizes and forecasts for Europe's home textile market in value (USD) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others (Carpets & Area Rugs) |

By Material

| Cotton |

| Linen |

| Synthetic Fibres |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | |

| Specialty Stores | |

| Other Offline Channels | |

| Online |

By Region

| Germany |

| Italy |

| Spain |

| France |

| United Kingdom |

| Poland |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Application | Bed Linen | |

| Bath Linen | ||

| Kitchen Linen | ||

| Upholstery | ||

| Others (Carpets & Area Rugs) | ||

| By Material | Cotton | |

| Linen | ||

| Synthetic Fibres | ||

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo) | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | Mass Merchandisers (Hypermarkets/Supermarkets) |

| Home Centers | ||

| Specialty Stores | ||

| Other Offline Channels | ||

| Online | ||

| By Region | Germany | |

| Italy | ||

| Spain | ||

| France | ||

| United Kingdom | ||

| Poland | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size and 2031 outlook for the Europe home textile market?

The market is expected to be USD 30.39 billion in 2026 and is projected to reach USD 36.02 billion by 2031, reflecting a 3.46% CAGR.

Which materials and applications drive demand for home textiles across Europe?

Cotton leads materials with 52.65% in 2025, while bed linen is the largest application with 38.20% share; bath linen records the fastest projected growth to 2031.

Which geographies are most important for suppliers active in Europe home textiles?

Germany holds the largest country share at 22.10% in 2025, and the Nordics post the fastest growth at a 5.08% CAGR through 2031.

How are EU policies shaping product requirements for home textiles?

Green Public Procurement, the Ecodesign for Sustainable Products Regulation, and Digital Product Passports are pushing traceability, verified chemistry, and circularity into purchasing criteria and compliance.

Which channels and end users are driving growth in Europe home textiles?

B2C retail remains the largest channel, while B2B direct grows fastest as institutions request certifications; residential leads by share, while commercial growth is faster through 2031.

Which regulations most influence the chemistry and materials choices in home textiles in Europe?

REACH restrictions on microplastics and national PFAS bans, along with upcoming Digital Product Passports and EPR requirements, are reshaping fiber and finish decisions across the value chain.

Page last updated on: