Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.26 Billion |

| Market Size (2026) | USD 4.41 Billion |

| Market Size (2031) | USD 5.18 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Outdoor Furniture Market Analysis by Mordor Intelligence

The Europe outdoor furniture market size is projected to be USD 4.26 billion in 2025, USD 4.41 billion in 2026, and reach USD 5.18 billion by 2031, growing at a CAGR of 3.32% from 2026 to 2031. The growth path reflects a sector aligning with circular design and Extended Producer Responsibility obligations that are reshaping competition around refurbishment networks and mono-material construction rather than price alone. Hospitality-led contracts still anchor revenues, yet residential applications are set to grow faster as hybrid-work routines keep patios and balconies active through most of the year. The European outdoor furniture market is influenced by material substitution toward aluminum and recycled composites, where forestry audits introduce friction during procurement. France is forecast to grow the fastest, while Germany remains the largest country by share due to a premium garden culture that treats outdoor settings as decade-scale investments. These conditions support steady replacement cycles and open the door for digital and subscription-led models that reframe ownership and lifecycle value in the European outdoor furniture market.

Key Report Takeaways

- By product type, in the Europe outdoor furniture market, chairs led with 41.22% revenue share in 2025, while loungers and daybeds are projected to expand at a 5.62% CAGR through 2031.

- By material, in the Europe outdoor furniture market, wood held a 40.42% share in 2025, while recycled plastic is forecast to grow at a 4.72% CAGR through 2031.

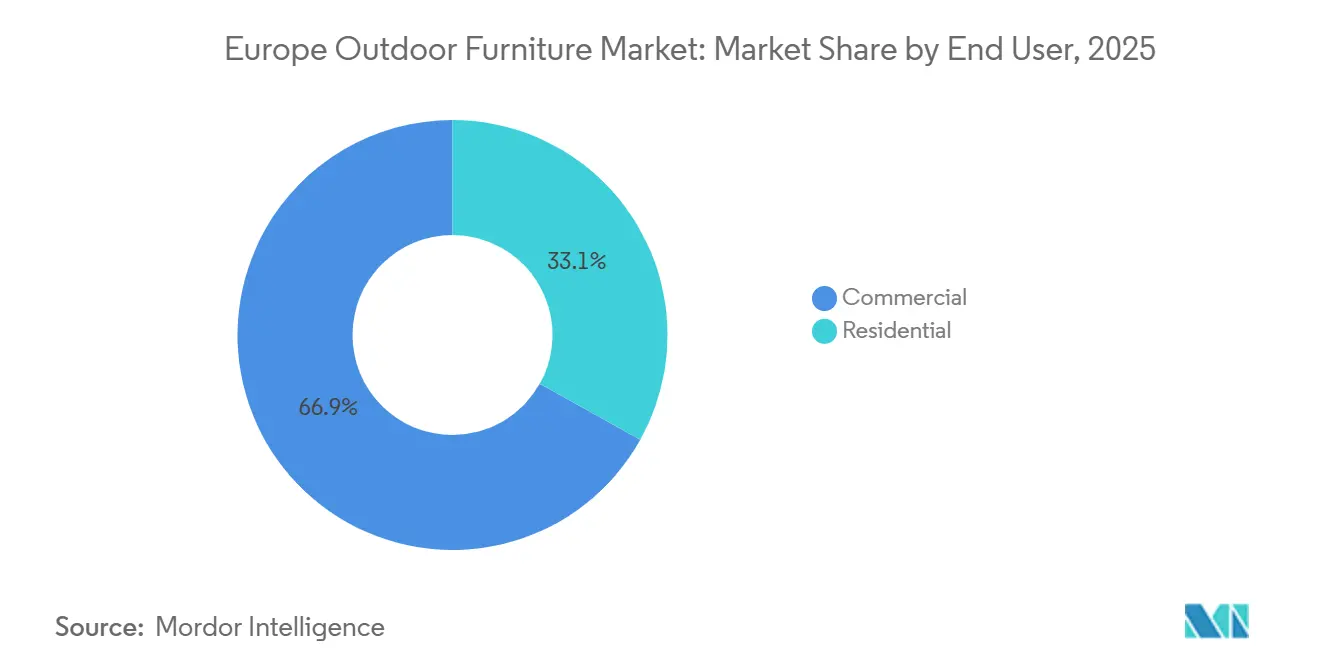

- By end user, in the Europe outdoor furniture market, commercial applications commanded 66.92% of revenue in 2025, while residential is projected to grow at a 5.43% CAGR through 2031.

- By distribution channel, in the Europe outdoor furniture market, B2B accounted for 57.92% of revenue in 2025, while B2C is projected to grow at a 4.01% CAGR through 2031.

- By geography, in the Europe outdoor furniture market, Germany held the largest country share at 16.97% in 2025, while France is projected to expand at a 4.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Outdoor Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outdoor Living as an Additional Room Elevates Spend | +0.6% | NORDICS, BENELUX, United Kingdom, Germany, France | Long term (≥ 4 years) |

| Hospitality Outdoor Upgrades and Al Fresco Seating Expansion | +0.8% | Spain, Italy, France, Germany, NORDICS | Medium term (2-4 years) |

| Material and Fabric Innovation Improving Durability and Aesthetics | +0.4% | Germany, NORDICS, BENELUX, United Kingdom | Medium term (2-4 years) |

| E-Commerce Configuration and DTC Personalization for Outdoor | +0.5% | Germany, United Kingdom, France, BENELUX | Short term (≤ 2 years) |

| Sustainability-Led Demand for Certified Wood and Recycled Resin | +0.4% | Germany, NORDICS, France, BENELUX, Netherlands | Long term (≥ 4 years) |

| Space-Optimized Modularity for Urban Balconies and Small Patios | +0.3% | Urban centers including Paris, Berlin, London, Amsterdam, Milan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Outdoor Living as an Additional Room Elevates Spend

Outdoor zones now function as extensions of the home environment as hybrid work sustains demand for ergonomic seating and indoor-grade comfort features outside. Consumers in the Nordics and Northern Europe view premium teak loungers and weather-adaptive sectionals as long-life purchases, which lifts average selling prices despite energy cost headwinds. Brands are prioritizing solution-dyed fabrics and quick-dry cores that match the look and feel of indoor upholstery while maintaining fade resistance and moisture control. Premium buyers expect components that tolerate freeze-thaw stress and seasonal use without frequent refinishing, which pushes the European outdoor furniture market toward better materials and longer warranties. This pattern supports the shift to modular seating sets that reconfigure for workday needs and weekend entertaining in compact spaces. These dynamics help explain why residential demand outpaces commercial growth in the European outdoor furniture market through 2031.

Hospitality Outdoor Upgrades and Al Fresco Seating Expansion

Hospitality operators are investing in terraces, poolside zones, and courtyards to meet sustained demand for outdoor dining and social spaces across key European destinations. Industry surveys in the UK show diners now favor venues with expanded open-air seating, which reinforces the business case for durable contract-grade furniture across patios and pavements. Café operators in France and Italy are refreshing outdoor areas with powder-coated aluminum frames and performance meshes that resist salt spray and heavy use. These procurement cycles favor mono-material designs and quick lead times as hotels seek consistent finishes across multiple properties. The European outdoor furniture market benefits from refurbishment programs in resorts and urban cafés that prioritize weather resistance, cleanability, and lifecycle cost reduction. Stronger compliance requirements also push buyers toward certified materials and suppliers with documented sustainability credentials[1]Product News, “Tubb Series and Adjustable Shells,” Hartman, hartman.nlSource: Product News, “Tubb Series and Adjustable Shells,” Hartman, hartman.nl.

Material and Fabric Innovation Improving Durability and Aesthetics

Advances in fabrics and engineered materials now close the comfort gap between outdoor and indoor seating, which encourages premium upgrades. Solution-dyed textiles deliver fade resistance and bleach cleanability for contract environments while maintaining a soft hand feel that appeals to residential buyers as well. Recycled high-density polyethylene and aluminum frames are popular due to corrosion resistance and low maintenance, which reduces the total cost of ownership in hospitality settings. The Europe outdoor furniture market also benefits from a design language that pairs ceramics and powder-coated metals for contemporary silhouettes with robust weather performance. Brands are integrating modular platforms and interchangeable components, which simplifies replacement and extends product life. Product launches that showcase adjustable shells, stackable forms, and quick-assembly hardware align well with urban spaces and short installation windows.

Sustainability-Led Demand for Certified Wood and Recycled Resin

Sustainability has become a baseline requirement across public and private procurement, which shapes material choices and supplier selection. Certified forests now cover a very large area worldwide, which strengthens the availability of responsibly sourced wood for premium lines while keeping verification central to brand narratives. Many European municipalities and public agencies favor recycled resin products for benches and tables, which reinforces demand for post-consumer HDPE in commercial contracts. The Europe outdoor furniture market is also adjusting to new deforestation due diligence requirements, which elevate traceability and encourage mono-material designs that simplify end-of-life processing. Vertical integration by premium brands helps secure certified teak and other traceable timbers, which reduces exposure to spot-market volatility. These shifts help recycled plastics and metals capture a share in applications where compliance and circularity drive purchasing decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonality and Weather Exposure Compress Sell-Through Windows | -0.4% | Northern Europe, NORDICS, United Kingdom, Ireland | Medium term (2-4 years) |

| Timber/Raw Material Volatility and Compliance Overhead | -0.7% | EU-wide, particularly Germany, NORDICS, France | Short term (≤ 2 years) |

| End-Of-Life Recovery and Recycling Infrastructure Gaps | -0.2% | Southern and Eastern Europe | Long term (≥ 4 years) |

| Influx of Low-Cost Imports Intensifying Price Competition | -0.3% | EU-wide, strongest in United Kingdom, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonality and Weather Exposure Compress Sell-Through Windows

Northern Europe experiences a short spring and summer window, which concentrates sales in a few months and increases inventory risk. Retailers often front-load buying for March through June, which can lead to discounting in autumn when weather changes reduce footfall. Wet or cold springs suppress demand and can leave seasonal stock stranded, which strains working capital and margins for specialty stores. Supply chains for bulky outdoor sets are sensitive to logistics delays since air freight is not practical for large items. These dynamics reinforce a cautious approach to assortment breadth and replenishment timing in the European outdoor furniture market. Brands that offer flexible replenishment and carryover colorways help retailers manage seasonality with lower obsolescence.

Timber/Raw Material Volatility and Compliance Overhead

Producers face volatility across timber, metals, and coatings, which complicates pricing and contract performance in the near term. New deforestation due diligence rules add compliance steps for timber imports, which raises the bar for traceability and favors suppliers with robust documentation. Certification premiums for FSC and PEFC timber raise input costs for value-segment products, which intensifies price gaps against non-certified alternatives. Energy-linked inputs affect metals and powder-coating costs, which show up in quotations for contract-grade frames. Import competition remains intense, which puts pressure on margins for European manufacturers that compete on design and sustainability. These factors weigh on the Europe outdoor furniture market even as differentiation on durability and lifecycle value helps protect pricing in premium segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Loungers Propel Premium Pivot

Loungers and daybeds are projected to expand at a 5.62% CAGR from 2026 through 2031 as wellness features and ergonomic reclining systems attract both residential and hospitality buyers. Chairs held a 41.22% share in 2025, which reflects café and terrace demand for stackable dining formats that turn space quickly. The Europe outdoor furniture market shows greater emphasis on modular seating sets that reconfigure for small balconies and larger gatherings without committing to fixed dining sets. Ceramic and porcelain table tops continue to carry a premium over laminates due to heat and scratch resistance valued by hotels and restaurants. Storage pieces and accessories make up a smaller revenue slice, yet post healthy gains where space constraints favor integrated planters and under-seat storage. New launches with adjustable shells allow consumers to get lounger-like comfort without buying separate SKUs, which fit compact urban living[2]Editorial Team, “Outdoor Canopies and Dining Preferences,” A&S Landscape, aandslandscape.co.uk.

Chairs will continue to anchor volume in the Europe outdoor furniture market as contract buyers replenish terrace fleets that take heavy seasonal wear. At the same time, loungers lead growth due to premiumization and the comfort-first mindset shaping outdoor living. The Europe outdoor furniture market size for loungers and daybeds is aligned with wellness-led upgrades where quick-dry foams and solution-dyed cushions extend service life at poolside. Modular platforms that share components across lounge and dining formats improve replacement economics for both residential and contract buyers. Innovation cycles are fastest where brands standardize frames and introduce color or fabric updates that refresh assortments with minimal tooling. Premium collections launched in 2026 underscore the move to modular organic forms that link together to serve both small patios and resort decks.

By Material: Plastic Surges on Circular Mandates

Wood accounted for 40.42% of the material share in 2025, supported by buyers who prefer natural finishes and traceable sources in premium price tiers. Recycled-plastic furniture is forecast to grow at a 4.72% CAGR through 2031 as public procurement and municipal programs favor post-consumer content for benches, tables, and loungers. Metal frames, especially aluminum, benefit from low maintenance and corrosion resistance, which suits coastal and rooftop settings across Europe. The Europe outdoor furniture market shows steady substitution toward circular materials, where compliance and recycling outcomes are central to bid evaluations. Scale expansions by recycled-plastic manufacturers are aligning supply with public-sector demand as cities upgrade parks and waterfronts under green criteria. Brands that demonstrate Blue Angel or comparable eco-label compliance have clear advantages in municipal tenders[3]Sustainability Team, “Recycled Plastic Portfolio and Blue Angel,” HAHN Kunststoffe, hahnkunststoffe.com.

Wood remains vital in premium segments where FSC or PEFC certification and long-life finishes justify higher price points and long replacement cycles. The Europe outdoor furniture market size for recycled plastics and aluminum grows alongside mandates that reward mono-material designs and end-of-life recovery. Synthetic rattan and rope continue to displace natural fibers where UV stability and mold resistance matter in humid or coastal climates. Portfolio moves by mainstream brands show that circularity can reach price parity with conventional designs when manufacturing achieves scale. As procurement favors recyclability and traceable sourcing, material choices continue to diversify while wood preserves its aesthetic leadership. These trends support a resilient material mix that balances appearance, compliance, and lifecycle economics in the Europe outdoor furniture market.

By End User: Residential Rises as Hybrid Work Persists

Commercial applications generated 66.92% of revenue in 2025 with hospitality operators refreshing loungers, terrace seating, and daybeds across ongoing renovation cycles. Residential demand is projected to grow at a 5.43% CAGR through 2031 as patios and balconies serve as hybrid work and leisure zones. Premium Nordic buyers continue to allocate higher budgets to durable lounge seating that performs through freeze-thaw conditions and intense UV seasons. The Europe outdoor furniture market, therefore, balances contract-grade durability with residential upgrades that prioritize comfort and design. Direct-to-consumer lines often adopt contract fabrics and aluminum frames, which bring hospitality performance to home settings. Subscription models that emphasize access over ownership are taking hold in dense urban areas where moving frequently is common.

Commercial buyers remain focused on maintainability, quick cleanability, and long warranties, which support slightly higher average selling prices than value-tier residential sets. The European outdoor furniture market share for commercial projects is steady as hotels and cafés standardize on proven SKUs across multi-property portfolios. Residential growth outpaces commercial as homeowners refresh small spaces with modular sets and space-saving dining that convert to lounge setups. Retailers respond with curated assortments that combine planters, storage, and seating to leverage every square meter. The gap between contract and residential performance continues to narrow, which encourages upgrades at home and reduces replacement cycles for businesses. This convergence supports steady growth in residential while preserving contract resilience in the Europe outdoor furniture market.

By Distribution Channel: B2C Digital Gains Amid B2B Dominance

B2B channels and project specifiers captured 57.92% of revenue in 2025 due to bulk orders under green procurement and standardized hospitality programs. B2C is projected to grow at a 4.01% CAGR through 2031 as real-time online configuration and visualization tools raise consumer confidence. The Europe outdoor furniture market shows strong omnichannel moves with retailers blending in-store displays and online fulfillment to manage large assortments. Assortment depth online allows long-tail SKUs such as compact balcony sets and reconfigurable seating to reach urban buyers. Retailers and brands deploy augmented reality and 3D configurators, which reduce fit risk and support higher ticket sizes. Municipal tenders and hotel programs continue to keep B2B in the lead, which helps balance seasonal volatility that is common in consumer channels[4]Category Pages, “Outdoor Furniture Assortment,” Wayfair UK, wayfair.co.uk.

B2C momentum concentrates in Germany, the United Kingdom, and BENELUX, where digital adoption and delivery networks are mature. Specialty stores still play a role in Southern Europe, where consumers prefer tactile inspection and assembly services, and where the climate allows extended outdoor use. The Europe outdoor furniture market benefits from click-and-collect options that reduce last-mile costs for bulky sets. Direct-to-consumer brands educate buyers on lifecycle value, which supports premium fabrics and corrosion-resistant frames. Subscription options that spread costs monthly fit well with transient urban populations and help brands manage asset utilization. As digital experience improves, B2C gains complement B2B stability and raises the overall addressable base for the Europe outdoor furniture market.

Geography Analysis

Germany held 16.97% of revenue in 2025, which makes it the largest country market due to a premium garden culture and long-life outdoor investments. Municipal procurement and certifications remain influential, which benefits suppliers that can document recycled content and circularity in benches and tables. Manufacturers that added recycled-plastic capacity expanded their relevance in public tenders aligned with Blue Angel criteria and similar eco-labels. France is projected to grow at a 4.88% CAGR from 2026 through 2031 as cafés refresh terraces for tourism and homeowners upgrade al fresco spaces with premium finishes. The Europe outdoor furniture market aligns with these shifts by pairing certified teak, ceramic tops, and powder-coated aluminum to deliver both aesthetics and compliance. Germany and France together anchor a large share of the residential and contract demand that drives steady growth into the next decade.

Spain shows strong momentum across resorts and urban hospitality, which sustains demand through a longer outdoor season. Contract buyers emphasize UV-stable meshes and corrosion-resistant metal frames, which reduces annual maintenance on coasts and islands. The Europe outdoor furniture market benefits from a design vocabulary in Spain and Italy that blends lightweight metals with premium ceramics for terraces and rooftops. Urban cores across Western Europe continue to adopt compact and modular furniture for small balconies, which lifts penetration of stackable and foldable forms. Germany and the United Kingdom lead in online assortment depth, while Southern markets rely more on specialty showrooms for tactile validation. Where compliance and sustainability are central to purchasing, certified timber and recycled resins remain the default choices.

BENELUX markets favor multifunctional modular sets that suit dense apartment living, along with affluent households that invest in durable pieces. The Nordics show the highest per-capita spending due to consumer preference for engineered longevity and premium lounging, even with shorter summers. The rest of Europe shows a mixed picture, with Eastern markets adopting entry-level modular kits as new residential projects add balconies and shared terraces. These regional behaviors point to sustained opportunities for compact modular systems and premium materials that showcase durability and low upkeep. The Europe outdoor furniture market, therefore, scales on a foundation of compliance-led materials and design formats suited to both small and large spaces. Suppliers that build traceability and circularity into their product development can participate across public tenders and premium retail.

Competitive Landscape

IKEA is investing heavily in automation and footprint optimization, which supports cost leadership and progress toward carbon reductions by 2028. Kettler, Hartman, and Fermob maintain a strong mid-tier presence with designs that emphasize color variety, stackability, and contract-grade finishes. Specialist brands such as Royal Botania, Dedon, Tribù, and Manutti serve premium segments with vertical integration and meticulous material control. Royal Botania advanced long-term supply security through managed teak plantations, which backstop FSC-compliant sourcing for flagship lines. Dedon continues to differentiate with proprietary fibers and specialized weaving that underpin outdoor collections across residential and contract settings.

Circular materials are a white-space accelerator as recycled plastics scale under municipal procurement. One manufacturer expanded recycled-plastic throughput to meet public-sector demand under eco-label criteria, which increases penetration in parks and civic spaces. Subscription models pioneered in office settings are now visible in residential outdoor categories in BENELUX cities, where flexibility is valued over ownership. The Europe outdoor furniture market also sees progress on omnichannel execution with AR-enabled showrooms and digital configurators that reduce selection friction. For premium portfolios, design-led ceramics and powder-coated metals provide distinct aesthetic signatures without compromising durability. These moves aim to balance pricing pressure from imports with brand-led differentiation on lifecycle and design.

Strategic priorities cluster around certification velocity, omnichannel reach, and materials innovation. Certification velocity matters in public tenders where compliance often outweighs price, which shapes eligibility and win rates. Omnichannel capabilities expand the consideration set and allow long-tail SKUs to find buyers beyond showroom constraints. Material innovation remains active as brands test bio-based resins and recycled composites that open new design possibilities while reducing reliance on virgin inputs. Fermob continues to evolve its palette and accessories while integrating connected lighting through partnerships that serve entertaining and hospitality use cases. IKEA strengthened its European footprint with selective retail acquisitions that improve market access and service levels. Across these moves, the Europe outdoor furniture market is set to reward suppliers that connect design, compliance, and digital experience.

Europe Outdoor Furniture Industry Leaders

Keter Group

Nardi S.p.A.

Fermob

Hartman Outdoor Products

IKEA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DEDON introduced five new collections at Salone del Mobile, including MDEAR, a modular lounging system with organic shapes by Sebastian Herkner.

- July 2024: Royal Botania introduced the Carés chair line, combining FSC-certified teak with recyclable aluminum frames to bolster sustainability appeal.

Europe Outdoor Furniture Market Report Scope

The European outdoor furniture market is involved in the creation, distribution, and sale of furniture specifically designed for outdoor environments such as gardens, patios, balconies, and terraces. This market includes a broad array of products, including seating options (chairs, benches, loungers), dining sets, tables, and decorative items made from materials such as wood, metal, plastic, wicker, and textiles. It serves both residential and commercial segments, focusing on providing durable, weather-resistant, and visually appealing furniture for enhancing outdoor living spaces.

The European outdoor furniture market is segmented by material, product, end user, distribution channel, and country. By material, the market is segmented into wood, metal, plastic, and other materials. By product, the market is segmented into chairs, tables, seating sets, loungers and daybeds, dining sets, and other products. By end user, the market is segmented into commercial and residential. By distribution channel, the market is segmented into multi-brand stores, specialty stores, online platforms, and other distribution channels. By country, the market is segmented into Germany, the United Kingdom, France, Italy, and the Rest of Europe. The report provides market sizes and forecasts in terms of value (USD) for all the above segments.

By Product Type

| Chairs |

| Tables |

| Seating Sets |

| Loungers and Daybeds |

| Dining Sets |

| Other Products |

By Material

| Wood |

| Metal |

| Plastic |

| Other Materials |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C Channels | Specialty Stores |

| Home Centers | |

| Online | |

| Other Distribution Channels | |

| B2B Channel/Contractors |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product Type | Chairs | |

| Tables | ||

| Seating Sets | ||

| Loungers and Daybeds | ||

| Dining Sets | ||

| Other Products | ||

| By Material | Wood | |

| Metal | ||

| Plastic | ||

| Other Materials | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C Channels | Specialty Stores |

| Home Centers | ||

| Online | ||

| Other Distribution Channels | ||

| B2B Channel/Contractors | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the Europe outdoor furniture market size and growth outlook to 2031

The Europe outdoor furniture market size is USD 4.41 billion in 2026 and is expected to reach USD 5.18 billion by 2031 at a 3.32% CAGR

Which segments are leading growth in the Europe outdoor furniture market

Loungers and daybeds are expanding at a 5.62% CAGR (2026-2031), while chairs remain the largest segment with a 41.22% share in 2025.

What materials are gaining traction in the Europe outdoor furniture market

Recycled plastics and aluminum are gaining share due to circular procurement and low-maintenance performance while wood maintains a 40.42% share in premium aesthetics.

Which end user will grow faster in the Europe outdoor furniture market

Residential is projected to grow at a 5.43% CAGR through 2031 as outdoor spaces serve as hybrid work and leisure zones.

Which countries are key to the Europe outdoor furniture market through 2031

Germany holds the largest share at 16.97% in 2025 while France is projected to grow at a 4.88% CAGR through 2031 as cafés and homeowners upgrade terraces and patios.

Page last updated on: