Automatic Curtain Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.07 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

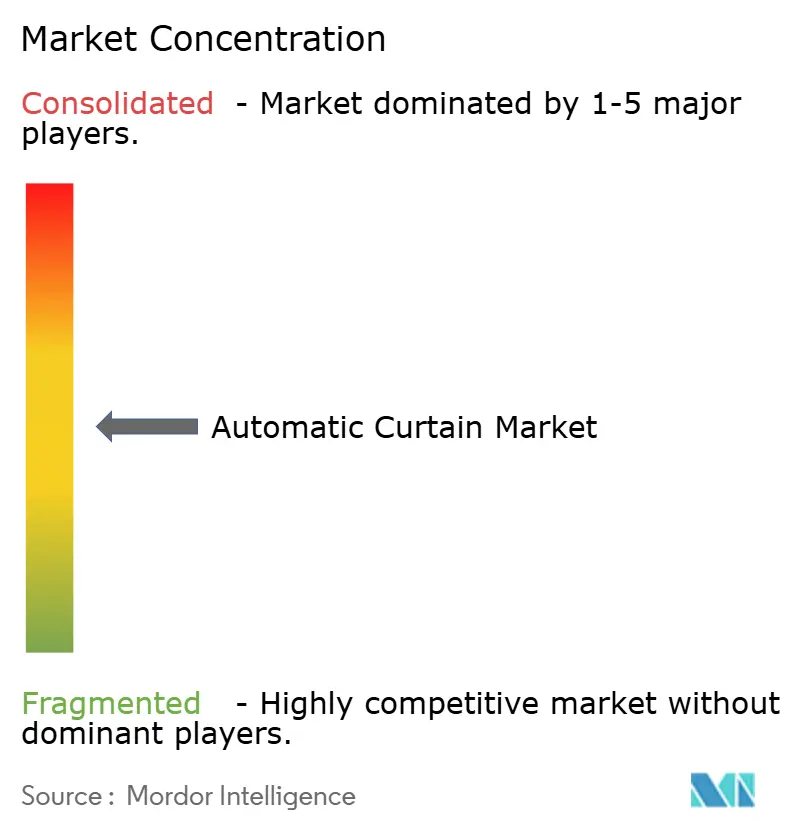

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automatic Curtain Market Analysis by Mordor Intelligence

The Global automatic curtains market size was valued at USD 3.86 billion in 2025 and estimated to grow from USD 4.07 billion in 2026 to reach USD 5.31 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031). Smart-home adoption, energy performance mandates, and stricter child-safety rules are the primary growth catalysts. Matter protocol interoperability is removing long-standing device compatibility barriers, allowing window coverings to work with lighting, HVAC, and security platforms[1]Connectivity Standards Alliance, “Matter Standard v1.2,” connectivitystandardsalliance.org . Regulatory agencies such as the U.S. Consumer Product Safety Commission have accelerated the phase-out of manual cords, pushing consumers toward automated solutions. Energy codes that reward dynamic shading are reinforcing demand, while retrofittable battery-powered products are easing installation hurdles in existing homes and commercial retrofits.

Key Report Takeaways

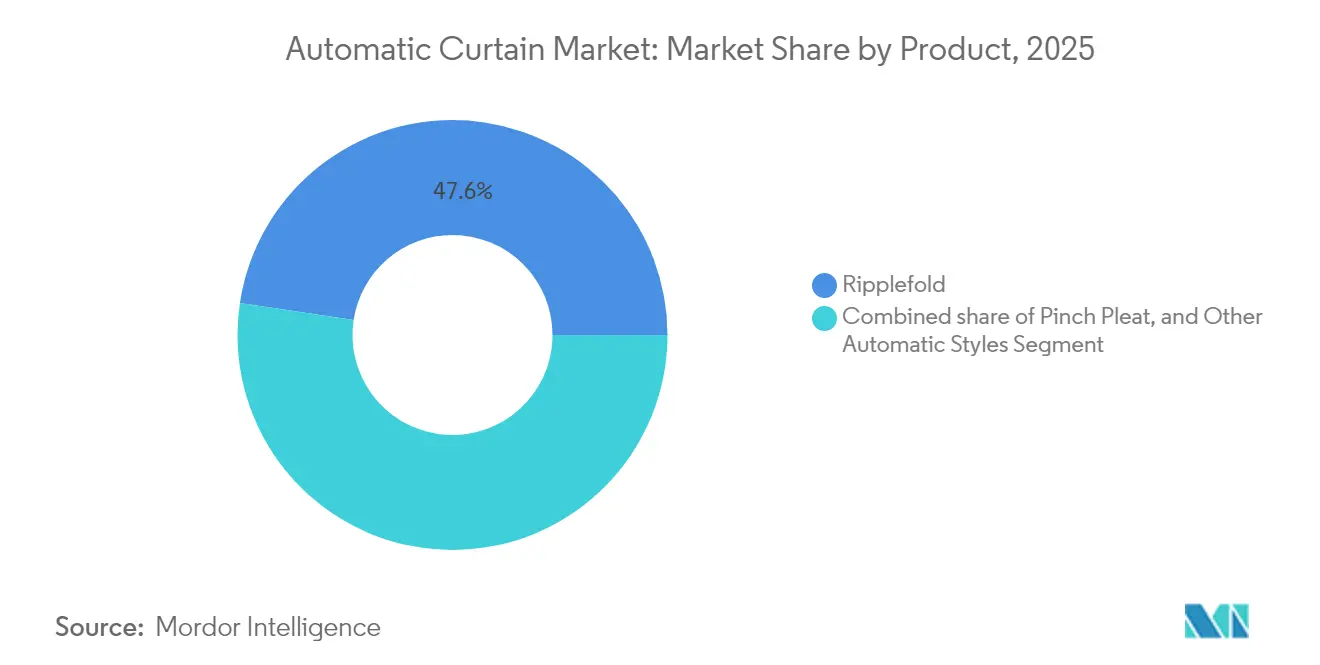

- By product type, Ripplefold curtains led with 47.62% revenue share in 2025, whereas Other Automatic Curtain Styles are projected to expand at a 6.94% CAGR to 2031

- By control type, motorized systems held 71.55% of the automatic curtains market share in 2025, while smart IoT-enabled systems are growing at 8.52% through 2031

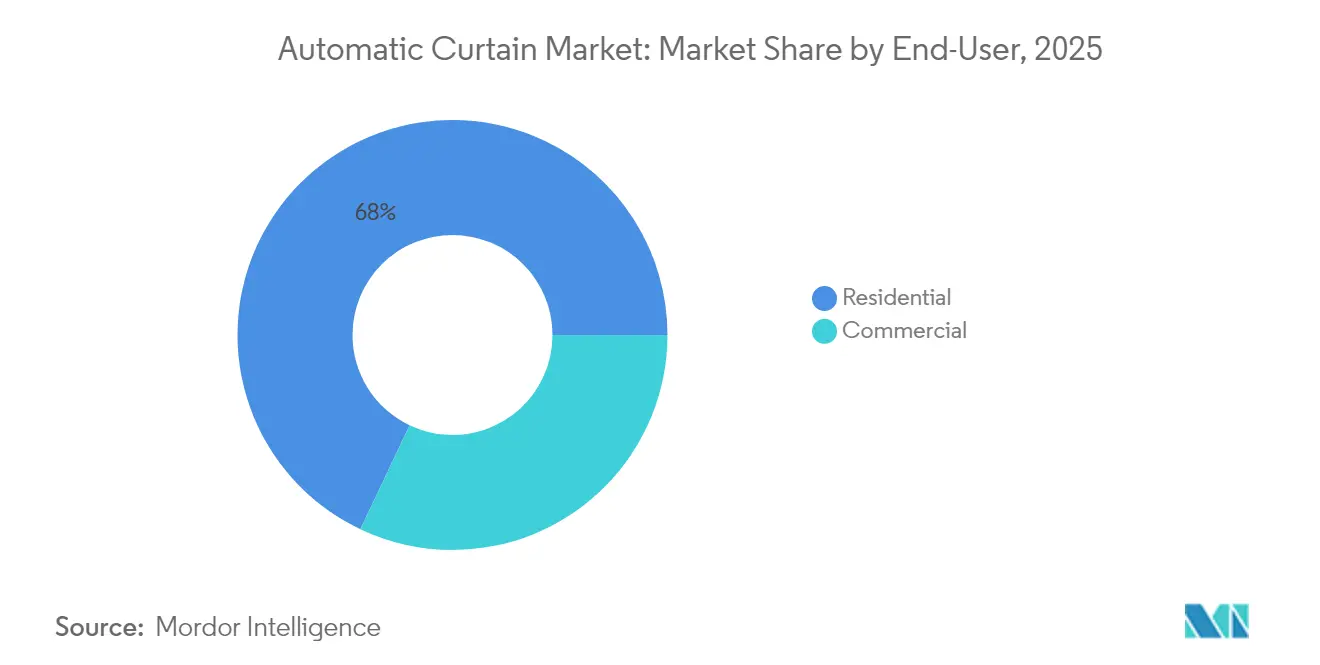

- By end-user, residential applications accounted for 67.95% of the automatic curtains market size in 2025; commercial installations are advancing at 6.12% CAGR to 2031.

- By distribution channel, B2C retail commanded 71.80% of 2025 revenue, whereas direct B2B sales are set to rise at 6.55% CAGR through 2031.

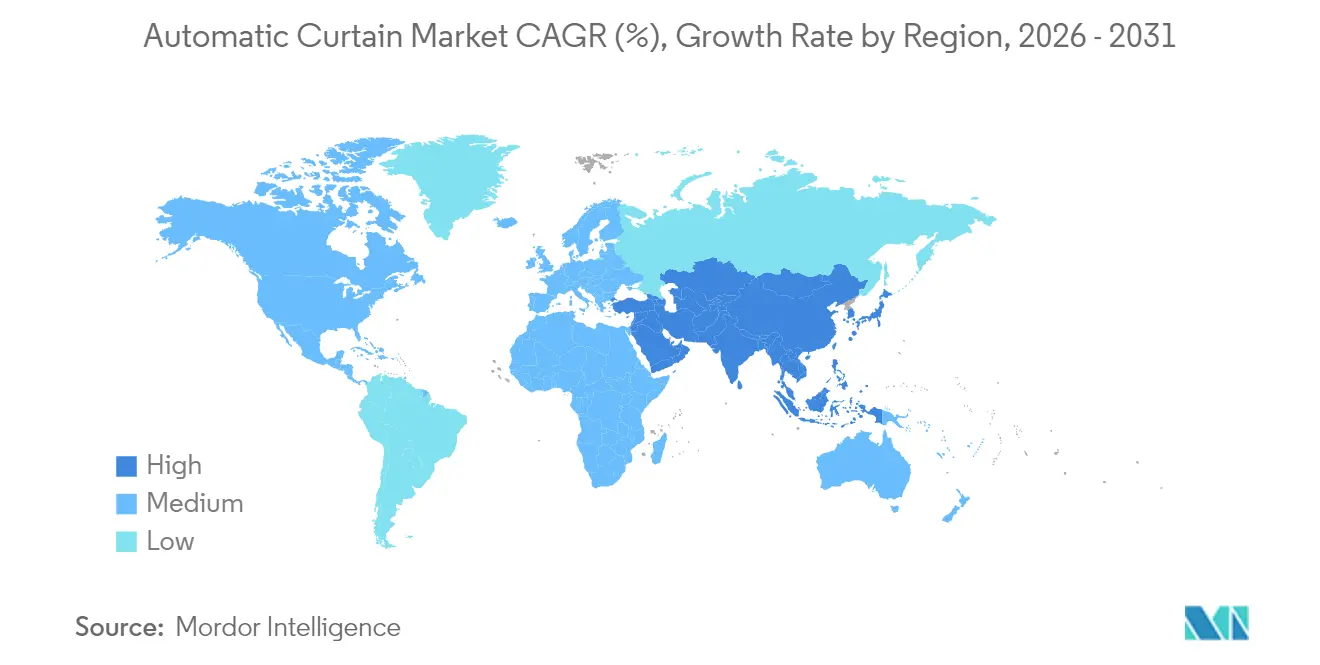

- By Geography, North America accounted for 35.62% of the market size in 2025, and Asia-Pacific is advancing at 8.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automatic Curtain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of smart-home automation systems | +1.2% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Rising demand for energy-efficient window coverings in green buildings | +0.8% | North America and Europe, expanding into Asia-Pacific | Long term (≥ 4 years) |

| Increasing hospitality & commercial construction projects incorporating automation | +0.6% | Global urban centers | Medium term (2-4 years) |

| Integration of Matter & Thread standards enabling interoperability | +0.4% | Early adoption in North America & Europe, global rollout underway | Short term (≤ 2 years) |

| Regulatory moves are phasing out manual cords for child safety | +0.3% | North America & Australia, widening to other regions | Short term (≤ 2 years) |

| Emergence of retrofittable battery-powered curtain robots | +0.2% | Global, the strongest appeal in retrofit markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Smart-Home Automation Systems

Voice assistants and unified mobile apps have set a new baseline for connected living spaces. Automatic curtains are increasingly bundled with lighting and climate controls so homes can react to occupancy, sunrise, or weather data. The Matter protocol now treats window coverings as a core device class, letting products pair with Apple, Google, and Amazon ecosystems without proprietary bridges. In hotels, Lutron’s myRoom platform shows how integrated shading boosts guest comfort while trimming energy use across thousands of rooms. Predictive adjustment algorithms that read weather forecasts or sensor inputs further raise the perceived value of automated drapery.

Rising Demand for Energy-Efficient Window Coverings in Green Buildings

Dynamic shading lessens reliance on HVAC by blocking solar heat gain in summer and retaining warmth in winter. The U.S. Department of Energy cites automated shades as a leading passive strategy for cutting heating and cooling bills. ASHRAE Standard 90.1-2022 now references automatically controlled glazing and shading, formalizing their role in code compliance. Manufacturers respond with high-R-value fabrics and cellular designs that earn AERC energy ratings; Hunter Douglas products even qualify for federal tax incentives. Solar-panel accessories, such as SwitchBot’s Curtain 3 Solar kit, turn window treatments into micro-generators that sustain battery power while moderating indoor temperatures.

Increasing Hospitality & Commercial Construction Projects Incorporating Automated Interiors

Hotel, office, and healthcare operators increasingly specify automatic curtains to differentiate properties and lower operating expenses. Lutron reports more than 40,000 guest rooms globally using its integrated lighting, temperature, and shading network. Centralized management lets staff reset rooms remotely, while occupancy sensors close drapes in vacant spaces to curb solar load. Offices pair automated shades with daylight harvesting to earn LEED credits and cut lighting energy. Hospitals value touch-free operation that supports infection-control protocols.

Integration of Matter & Thread Standards Enabling Interoperability

Fragmented wireless standards have long hampered multi-brand installations. Matter’s certification framework ensures secure, consistent performance across vendors, and Thread’s low-power mesh keeps hard-to-reach windows online. SwitchBot’s Curtain 3 became one of the first battery-powered drapery motors to receive Matter validation, working natively with major smart-home hubs while retaining local-network fallback. For commercial facilities, open standards simplify upgrades and avoid vendor lock-in, shortening project cycles and reducing maintenance complexity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installation and motor costs | -0.7% | Global, most acute in cost-sensitive regions | Medium term (2-4 years) |

| Lack of standardization & interoperability among smart-home platforms | -0.4% | Global, with greater fragmentation in emerging markets | Short term (≤ 2 years) |

| Cybersecurity & privacy concerns with IoT-enabled curtain systems | -0.3% | Primarily North America & Europe | Long term (≥ 4 years) |

| Limited awareness in price-sensitive emerging markets | -0.2% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation and Motor Costs

Motorized tracks, power wiring, and professional labor can triple or quadruple project budgets versus manual drapes. In India, complete smart-home packages often span INR 500,000 to INR 10 million (USD 6,000–120,000), limiting uptake to premium developments. Retrofit-friendly battery units relieve wiring expenses but still struggle with heavy fabrics in large spans. Leasing models and utility rebates for energy-saving equipment remain nascent in the automatic curtains industry, muting cost-mitigation options. As a result, many mid-tier consumers opt for partial automation—motorizing only key rooms or select curtain panels. Broader affordability may hinge on standardized hardware kits and bundled installation services from ecosystem partners like lighting or security providers.

Cybersecurity & Privacy Concerns with IoT-Enabled Curtain Systems

Connected drapery can reveal occupancy patterns or provide gateways to other devices if left unsecured. NIST Special Publication 800-213 lists mandatory encryption, authentication, and update mechanisms for federal IoT procurement, offering a benchmark for consumer products too[2]National Institute of Standards and Technology, “NIST SP 800-213: IoT Device Cybersecurity Guidance,” nist.gov. The forthcoming U.S. Cyber Trust Mark will label compliant devices, but most window-covering brands are still evaluating certification pathways. Building managers are segmenting networks and mandating periodic firmware audits to contain risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Ripplefold Dominance Faces Style Diversification

Ripplefold systems retained a 47.62% share of the automatic curtains market in 2025, anchored by their minimalist profile and compatibility with long motorized tracks. Architects prefer the uninterrupted fabric wave for wide glazing in hotels, offices, and luxury homes. The automatic curtains market size for Other Automatic Curtain Styles, including wave fold and Euro pleat, is forecast to climb 6.94% CAGR as designers pursue distinctive aesthetics and functional fabrics.

Style diversification reflects demand for acoustic damping, flame retardancy, and specialty coatings. Energy-harvesting solar rails are appearing first in niche designs, feeding small batteries that support IoT radios. Commercial buyers seek fire-rated or antimicrobial textiles, adding value to non-Ripplefold options. Over the forecast horizon, Ripplefold retains volume leadership, yet its share narrows as new specialty formats proliferate.

By Control Type: Smart Systems Challenge Motorized Incumbents

Traditional motorized units captured 71.55% of 2025 market size, leveraging proven mechanics and lower price points. However, the automatic curtains market size for smart IoT-enabled motors is expanding at an 8.52% CAGR on the back of app control, voice integration, and cloud analytics. Established motor solutions remain dominant in commercial and institutional settings where reliability, durability, and centralized control outweigh smart features. Yet, in the residential segment, especially among tech-savvy users, expectations for automation and remote access are reshaping purchasing criteria. Construction firms still specify hard-wired motors for synchronized movement on large façades, but consumer appetite tilts toward Wi-Fi or Thread-based kits.

The automatic curtains industry is moving toward hybrid architectures that pair hard-wire reliability with upgradeable wireless modules. Matter endorsement reduces app fatigue, while over-the-air updates add features such as sun-tracking algorithms. These hybrid models allow retrofitting in both new and existing buildings without complete rewiring, offering flexibility to contractors and homeowners alike. As ecosystems like Apple HomeKit, Google Home, and Alexa expand, compatibility becomes a key differentiator. Cost, integration support, and perceived security will dictate how fast smart devices erode legacy motor dominance.

By End-User: Commercial Acceleration Challenges Residential Dominance

Residential buyers delivered 67.95% of 2025 sales, yet commercial deployments post a faster 6.12% CAGR. Hotels install centralized curtain control to trim staffing and elevate guest experiences. Offices couple shades with daylight sensors to reduce artificial lighting, aligning with LEED v4.1 credits. Healthcare’s infection-control push favors hands-free drapes that staff can operate remotely.

The automatic curtains market share of commercial projects increases as larger-scale developments standardize on automated interiors. Facility managers quantify payback via labor savings and energy cuts, offsetting upfront costs. Residential demand continues to grow in unit terms, buoyed by falling motor prices and DIY installation kits.

By Distribution Channel: Direct Sales Gain Ground on Retail Dominance

B2C retail outlets such as multi-brand showrooms, specialty dealers, and e-commerce sites maintained a 71.80% share in 2025. Shoppers value fabric samples and local installation services. Physical retail remains essential for tactile decisions, especially in premium segments where buyers seek coordinated interiors. E-commerce platforms, meanwhile, capture convenience-driven customers with virtual consultations and quick delivery options. Direct B2B orders from manufacturers to builders, integrators, and facility owners are rising at a 6.55% CAGR as project complexity grows.

Commercial buyers prefer direct engagement for custom sizes, project management, and post-installation analytics. Online pure-plays thrive where battery-powered units eliminate electrician visits. These solutions appeal to property managers seeking minimal disruption during retrofit cycles, especially in hospitality and office environments. Integrators often bundle automatic curtains with lighting and HVAC control as part of broader smart-building packages. Expanded warehouse networks let brands ship pre-configured tracks within days to smaller towns, broadening reach without large storefront investments.

Geography Analysis

North America held 35.62% of global revenue in 2025. High household adoption of smart-home hubs, strict child-safety rules that effectively ban accessible cords, and steady commercial construction all keep demand for automated curtains strong. Canada and Mexico add to regional growth through cross-border manufacturing and a rising number of automated offices and hotels. A mature broadband network and widespread familiarity with IoT gear make it easy for installers to integrate curtain motors with popular home-automation platforms. Energy codes, including ASHRAE 90.1-2022 provisions on dynamic glazing and shading, further support uptake by tying window-covering automation to building-performance targets.

Asia-Pacific shows the fastest growth and is forecast to expand at 8.28% CAGR between 2026 and 2031. Urbanization, local manufacturing depth, and policy incentives drive large-volume demand in China, where subsidies for high-efficiency appliances include automated curtain systems. In India, luxury buyers now treat motorised drapes and basic lighting control as standard features, with 80% of new high-end projects specifying these elements. Rapid e-commerce expansion, expected to reach USD 300 billion by 2030, gives suppliers an online route into smaller cities that lack specialist showrooms. Japan, South Korea, and Australia add premium demand for advanced building-automation features, while Southeast Asian markets are starting to adopt affordable retrofit kits.

Europe maintains moderate but stable growth as regulators and consumers prioritise energy efficiency. Building codes across the region credit dynamic shading for lowering heating and cooling loads, and solar-powered track systems align well with national sustainability goals. South America, the Middle East, and Africa remain earlier in the adoption curve. Brazil leads regional uptake thanks to luxury high-rise projects, while the UAE and South Africa invest in smart commercial spaces. Battery-powered curtain motors, which avoid costly electrical work, are opening new opportunities where skilled installers are scarce.

Competitive Landscape

The sector remains moderate. Hunter Douglas, Somfy, and Lutron blend global distribution with proprietary control systems, holding a collective mid-double-digit revenue share. Somfy’s 70% stake in Ningbo Dooya expanded its low-cost motor portfolio and deepened reach in China. Hunter Douglas continues to emphasize AERC-certified shades, aligning environmental messaging with consumer incentives.

Technology-focused entrants such as SwitchBot and Aqara court DIY consumers through app-centric platforms and battery-first designs. SwitchBot’s Curtain 3 Solar combo combines on-board PV with Matter support, carving a niche in retrofit apartments. Aqara concentrates on Zigbee hubs that unify sensors, cameras, and drapery motors. Price competition intensifies, yet differentiation now hinges on firmware features, voice-assistant response times, and cybersecurity assurances aligned with NIST baselines.

Lutron, Somfy, and Crestron target high-end commercial tenders with PoE motors and cloud dashboards. Somfy’s SDN Connect feeds real-time motor diagnostics to facility managers, shrinking service downtime. Resideo’s Snap One acquisition enhances distribution for mid-market installers seeking a single source for cameras, thermostats, and window gear. Overall, software skills, standards compliance, and energy-management analytics are eclipsing hardware alone as winning factors.

Automatic Curtain Industry Leaders

Somfy

HunterDouglas

Lutron Electronics

Dooya Tubular Motor

Coulisse (Motionblinds)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Forterro acquired BM Group to deepen software support for automated fenestration workflows.

- October 2024: NIST released IR 8425A outlining cybersecurity requirements for consumer routers, a key backbone for smart-home curtain deployments.

- August 2024: Resideo completed its acquisition of Snap One, broadening smart-living product distribution.

- May 2024: SwitchBot launched Curtain 3 Solar Matter combo enabling months of off-grid operation with simple plug-and-play setup.

Global Automatic Curtain Market Report Scope

Motorized or automatic curtains are window coverings that are operated by an electric motor, allowing them to be opened and closed automatically at the push of a button or with the use of a remote control. A complete background analysis of the global automatic curtain market, which includes a qualitative and quantitative assessment of the parent market, market dynamics, emerging trends in the segments and regional markets, and insights into various product and application types. Also, it analyses the key players and the competitive landscape in the global automatic curtain market.

The global automatic curtain market is segmented by product (ripplefold, pinch pleat), application (residential, commercial), and geography (North America, Asia-Pacific, Europe, Latin America, the Middle East, and Africa).

The report offers market size and forecasts for the automatic curtain market in terms of revenue (USD) for all the above segments.

| Ripplefold |

| Pinch Pleat |

| Other Automatic Curtain Styles |

| Motorized |

| Smart (IoT-enabled) |

| Residential | |

| Commercial | Hospitality |

| Offices | |

| Healthcare | |

| Other Commercial End-Users |

| B2C / Retail Channels | Multi-Brand Stores |

| Specialty Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly From Manufacturers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product | Ripplefold | |

| Pinch Pleat | ||

| Other Automatic Curtain Styles | ||

| By Control Type | Motorized | |

| Smart (IoT-enabled) | ||

| By End-User | Residential | |

| Commercial | Hospitality | |

| Offices | ||

| Healthcare | ||

| Other Commercial End-Users | ||

| By Distribution Channel | B2C / Retail Channels | Multi-Brand Stores |

| Specialty Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly From Manufacturers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size of the automatic curtains market?

The market generated USD 4.07 billion in 2026 and is projected to reach USD 5.31 billion by 2031.

Which product style holds the largest share?

Ripplefold curtains led with a 47.62% share in 2025, thanks to their clean aesthetic and compatibility with long motorized tracks.

How fast are smart IoT-enabled curtain systems growing?

Smart systems are expanding at an 8.52% CAGR through 2031, outpacing traditional motorized units as Matter standardizes connectivity.

How are cybersecurity concerns being addressed?

Manufacturers are adopting NIST-aligned encryption, authentication, and update protocols, and devices will soon display the U.S. Cyber Trust Mark for easy consumer reference.

Page last updated on: