Unsaturated Polyester Resin (UPR) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

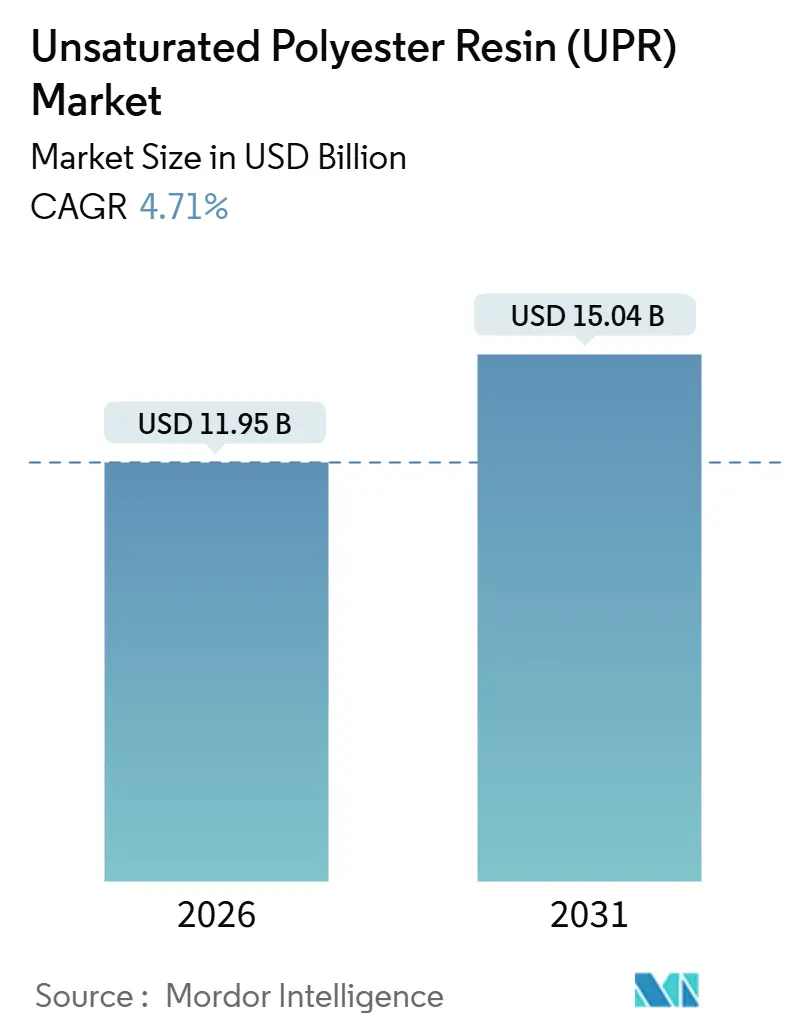

| Market Size (2026) | USD 11.95 Billion |

| Market Size (2031) | USD 15.04 Billion |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

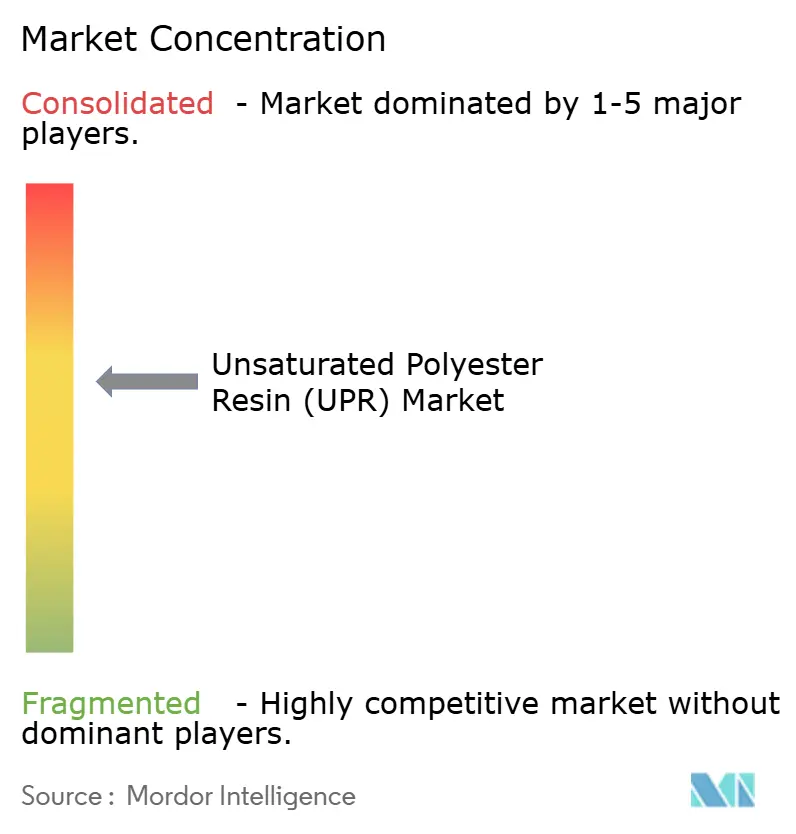

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unsaturated Polyester Resin (UPR) Market Analysis by Mordor Intelligence

The Unsaturated Polyester Resin Market size is estimated at USD 11.95 billion in 2026, and is expected to reach USD 15.04 billion by 2031, at a CAGR of 4.71% during the forecast period (2026-2031). Wind-energy blade fabrication, electric-vehicle lightweighting, and large-scale Asian infrastructure projects collectively sustain demand, yet rising scrutiny of life-cycle emissions and tightening volatile-organic-compound ceilings are moderating expansion. Maleic anhydride feedstock swings, together with European REACH pressure for low-styrene grades, continue to reshape cost structures and sourcing strategies. Automotive original-equipment manufacturers favor closed-mold sheet-molding-compound and bulk-molding-compound processes that demand tighter specification control and ultra-low emission profiles. Asia-Pacific remains the volume backbone, while North America and Europe focus on premium, low-styrene, and bio-content variants. Competitive focus is shifting toward integrated feedstock control, powder formulations for battery enclosures, and recycled-PET-based polyol chemistries that reduce the embedded-carbon burden.

Key Report Takeaways

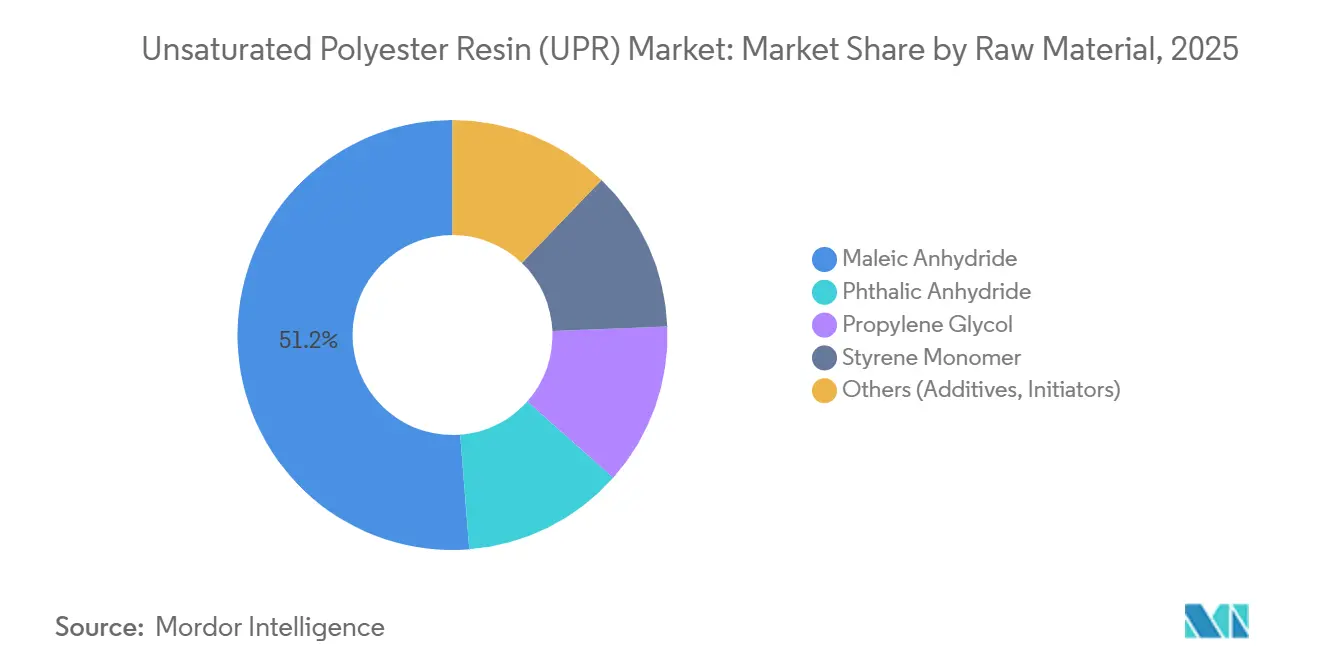

- By raw material, maleic anhydride led with 51.26% of the unsaturated polyester resin market share in 2025, while propylene glycol is on track to expand at a 5.70% CAGR to 2031.

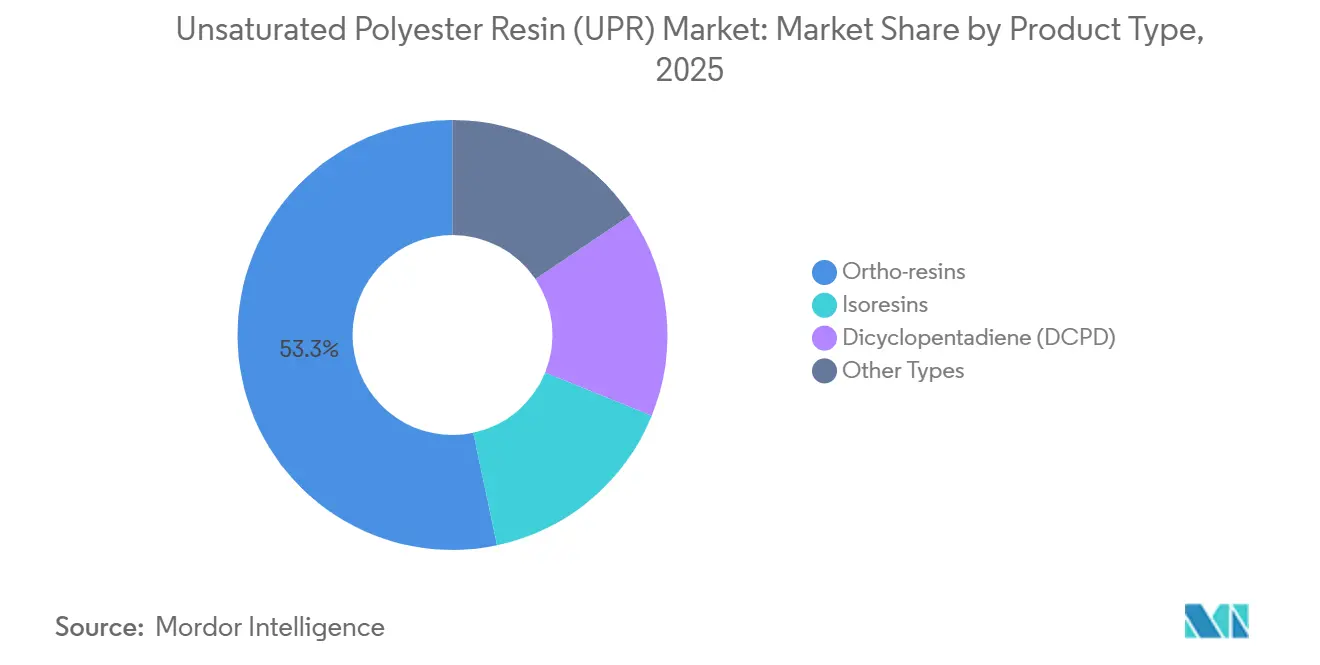

- By product type, ortho-resins captured 53.31% revenue share in 2025, whereas isoresins are projected to grow at a 6.56% CAGR through 2031.

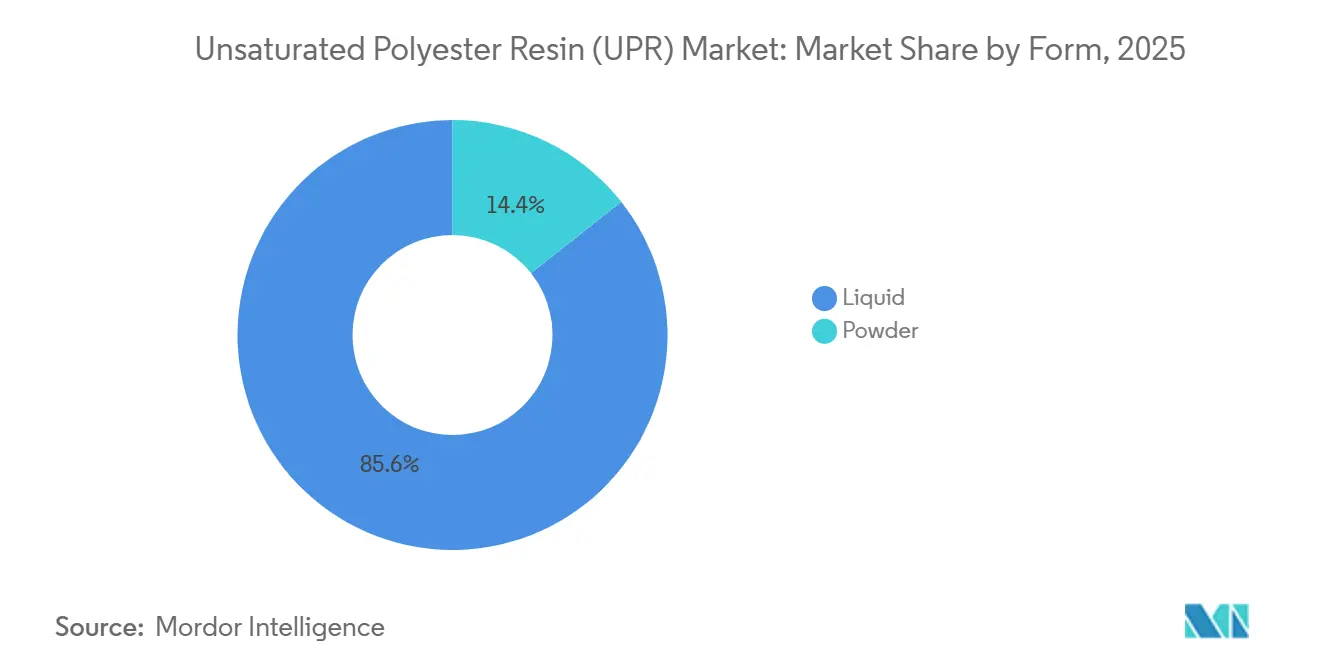

- By form, liquid commanded 85.64% share of the unsaturated polyester resin market size in 2025, and powder is advancing at a 6.16% CAGR to 2031.

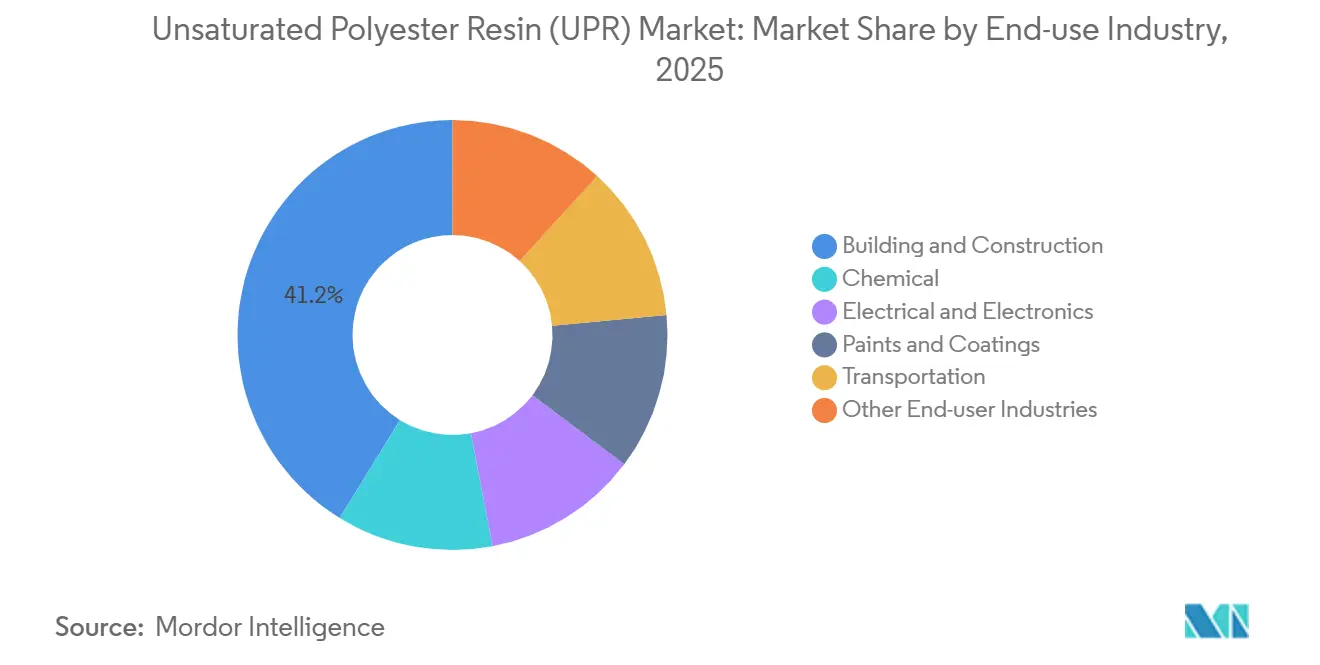

- By end-use industry, building and construction accounted for 41.22% of 2025 revenue, while electrical and electronics is forecast to expand at a 6.24% CAGR up to 2031.

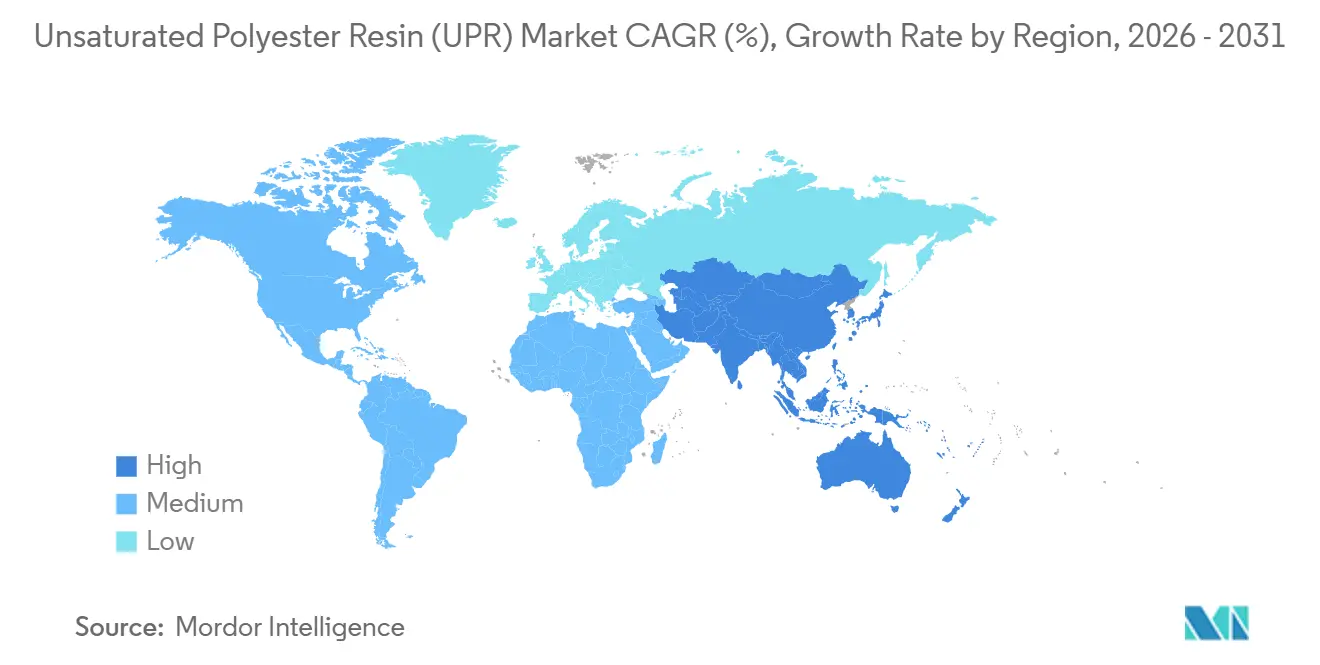

- By geography, Asia-Pacific generated 43.45% of global revenue in 2025 and is poised to rise at a 5.78% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unsaturated Polyester Resin (UPR) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption in Wind-Turbine Blades | +1.2% | Global, with concentration in Europe and APAC | Medium term (2-4 years) |

| Growth of Automotive and Transportation Sectors | +1.0% | North America, Europe, APAC | Short term (≤ 2 years) |

| Construction and Infrastructure Boom in Emerging Asia | +1.5% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| EU REACH Pressure for Low-Styrene Resins | +0.6% | Europe, gradual adoption in North America | Medium term (2-4 years) |

| OEM Shift to Closed-Mold SMC/BMC for E-Mobility | +0.8% | North America, Europe, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Adoption in Wind-Turbine Blades

Offshore installations lifted global blade-composite demand by 22% in 2025 as average rotor lengths moved beyond 85 meters in the North Sea andthe Taiwan Strait in the unsaturated polyester resin market [1]. Unsaturated polyester resin remains the default matrix for spar-cap and shell laminates because vacuum-infusion delivers attractive cost-per-kilowatt figures versus epoxy systems. European circular-economy mandates now require end-of-life blade recovery pathways by 2030, which is prompting trials of UPR blends incorporating recycled-PET polyols that can cut decommissioning logistics costs by up to 15%. China’s National Energy Administration allocated USD 18 billion for new offshore capacity in 2025, confirming Asia-Pacific as the primary growth engine through 2031. Blade makers therefore seek resins with documented recyclability, low exotherm, and fatigue durability suitable for 20-year service intervals.

Growth of Automotive and Transportation Sectors

Automotive manufacturers processed roughly 1.8 million t of composite resins in 2025 in the unsaturated polyester resin market, and 40% of that volume relied on unsaturated polyester resin-based sheet-molding-compound for underbody shields, battery trays, and Class-A body panels. Electric-vehicle platforms need electromagnetic-interference shielding and flame retardancy while maintaining low mass; isoresin and dicyclopentadiene grades therefore gain share. General Motors and Stellantis lifted SMC press capacity by 30% during 2025 to support curb-weight reduction targets that improve driving range by 10–15%. Closed-mold presses eliminate styrene emissions and already comply with California rules that limit volatile-organic compounds to 50 g L⁻¹ for composite parts. Supply contracts increasingly stipulate UL 94 V-0 flame-retardant performance and dimensional stability from −40 °C to 120 °C across a decade of service.

Construction and Infrastructure Boom in Emerging Asia

China started 1.2 billion m² of new residential floor area in 2025, while India earmarked USD 1.4 trillion for roads, railways, and water systems through 2030 in the unsaturated polyester resin market. Corrosion-resistant unsaturated polyester resin pipes offer 50-year service life at half the installed cost of stainless steel for wastewater, desalination, and chemical-transport lines. Indonesia and Vietnam expect combined infrastructure spending above USD 200 billion by 2027, encouraged by urbanization rates above 3% annually. Municipal owners increasingly demand ISO 14001 documentation of carbon footprints and recyclability, pressuring resin suppliers to publish verified environmental-product declarations.

OEM Shift to Closed-Mold SMC/BMC for E-Mobility

Battery-electric-vehicle output exceeded 14 million units in 2025 in the unsaturated polyester resin market and now relies on compression-molded composite housings that resist thermal runaway and absorb crash energy. Closed-mold routes eliminate open-surface emissions and deliver sub-3-minute cycle times compatible with high-volume automotive lines. Purpose-formulated unsaturated polyester resin SMC compounds incorporate halogen-free flame retardants and reach glass-transition temperatures above 150 °C, satisfying UL 94 V-0 and IEC 61249 requirements. Polynt and INEOS co-located compounding and press capacity next to Tier-1 suppliers in Michigan and Baden-Württemberg during 2025, shrinking logistics costs and enabling rapid formulation changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Maleic Anhydride Price Volatility | -0.9% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Environmental and Regulatory Challenges | -0.5% | Europe, North America, expanding to APAC | Medium term (2-4 years) |

| Rising LCA Scrutiny Favoring Bio-Epoxy Systems | -0.7% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Maleic Anhydride Price Volatility

Spot prices swung between USD 1,400 and USD 2,100 t⁻¹ in 2025 in the unsaturated polyester resin market as crude-oil and benzene disruptions rippled through the value chain. Resin makers without long-term supply contracts faced margin compression of 200–300 basis points, prompting vertical-integration moves such as Polynt’s 50,000 t y⁻¹ maleic-anhydride acquisition in Italy. China controls 55% of global maleic-anhydride capacity, exposing Western buyers to freight and tariff risks under Section 301 measures in the United States. Alternative bio-based pathways remain pilot-scale and carry 40–60% cost premiums, limiting broad adoption.

Environmental and Regulatory Challenges

The European Industrial Emissions Directive cut allowable styrene emissions from composites manufacturing to 5 mg Nm⁻³ in 2024, compelling small laminators to retrofit solvent-capture systems or shift to closed-mold technologies at capital costs above EUR 0.5 million in the unsaturated polyester resin market.[2]. California’s Proposition 65 styrene listing triggers warning-label obligations that complicate distribution, and China’s updated Air Pollution Prevention Law imposes real-time monitoring for facilities processing more than 10 t y⁻¹ of volatile organics. End-of-life disposal remains contentious because thermosets resist mechanical recycling and incineration produces hazardous gases; the Ellen MacArthur Foundation excludes conventional unsaturated polyester resin from circular-economy frameworks unless chemical-recovery routes are demonstrated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Demand Concentrated in Maleic Anhydride

Maleic Anhydride held 51.26% of 2025 revenue within the unsaturated polyester resin market share, underscoring its central role in ortho-phthalic and iso-phthalic backbones that balance cost and mechanical strength. Propylene Glycol is expanding at a 5.70% CAGR through 2031, driven by processors who seek lower viscosity and better wet-out during vacuum-infusion of wind-turbine spar caps. Phthalic Anhydride continues to serve general-purpose ortho grades, while Styrene Monomer remains indispensable as a cross-linking diluent, despite pressure for recovery systems that cap emissions.

Propylene Glycol growth mirrors wider substitution toward neopentyl glycol and dipropylene glycol co-reactants that enhance hydrolytic stability in marine and chemical-processing equipment. China expanded propylene-glycol capacity by 18% in 2025 on the back of coal-to-olefin routes, reducing delivered costs within Asia. OEM audits now require ISO 9001 certification and batch traceability, reinforcing quality expectations for raw-material suppliers targeting aerospace and medical components.

By Product Type: Isoresins Capture Corrosive-Service Growth

Ortho-resins captured 53.31% of 2025 revenue in the unsaturated polyester resin market because broad formulation latitude keeps prices competitive across construction and sanitary-ware uses. Isoresins, however, are projected to climb 6.56% CAGR through 2031, propelled by marine vessels, desalination plants, and chemical-processing equipment that demand elevated temperature and corrosion resistance. Dicyclopentadiene resin occupies a niche in wind-turbine nacelles and large storage tanks, where low exotherm enables thick-section casting without cracking.

Isoresin uptake aligns with the expansion of liquefied-natural-gas terminals, offshore production platforms, and industrial wastewater facilities that specify fiberglass-reinforced equipment meeting EN 13121 flexural-strength thresholds. Suppliers such as AOC and Ashland launched iso-NPG grades in 2025 that provide corrosion resistance while processing on unheated molds, enabling adoption by fabricators with limited capital investment.

By Form: Powder Grades Gain Momentum in Automotive

Liquid commanded 85.64% of form-based revenue in 2025 because hand lay-up, spray-up, and vacuum-infusion remain widespread. Powder is forecast to grow at 6.16% CAGR through 2031 as in-mold-coated sheet-molding-compound eliminates separate painting steps and embodies zero volatile-organic-compound releases.

Electric-vehicle battery enclosures increasingly specify powder-resin SMC underbody shields that blend crash protection with electromagnetic shielding. Allnex and Polynt introduced pre-impregnated powder-resin compounds in 2025, which simplify handling and shorten cure cycles, thereby expanding access for Tier-2 suppliers in Asia. U.S. EPA hazardous-air-pollutant standards classify open-mold composite operations as major styrene sources, so powder systems help processors avoid costly vapor-capture retrofit.

By End-use Industry: Electronics Leads Growth Curve

Building and Construction generated 41.22% of 2025 revenue, reflecting the widespread use of corrosion-resistant unsaturated polyester resin tanks, pipes, and cooling-tower structures that offer 50-year life cycles. Electrical and Electronics is the fastest-growing end use industry at a 6.24% CAGR through 2031 as data-center expansion, renewable-energy grids, and 5G infrastructure require flame-retardant transformer housings, printed-circuit-board laminates, and cable trays.

China’s State Grid Corporation invested USD 50 billion in ultra-high-voltage links during 2025 and specified glass-fiber-reinforced unsaturated polyester resin bushings able to handle 1,000 kV operating voltages. Transportation demand remains steady because lightweight, corrosion-resistant exterior panels and underbody elements help carmakers meet fuel-economy and range mandates. Paints and Coatings leverage fast-cure orthophthalic resins for industrial floorings, while chemical-process vessels rely on bespoke isoresin or vinyl-ester hybrids for aggressive media.

Geography Analysis

Asia-Pacific led the unsaturated polyester resin market with a delivered 43.45% of global revenue in 2025 and is forecast to grow at a 5.78% CAGR to 2031, driven by Chinese infrastructure outlays, India’s housing boom, and Southeast Asian industrial expansion. China allocated USD 800 billion in 2025 for urban rail, water systems, and renewable energy installations that consume corrosion-resistant piping and blade-grade composites. India’s production-linked incentives attracted USD 30 billion in foreign investment, spurring component demand in electric two-wheelers, appliances, and telecom equipment. Regulatory frameworks in the region remain fragmented, yet local compounders adept at navigating GB and BIS standards win share against multinational incumbents.

North America’s share is anchored by United States demand in automotive composites, wind-energy blades, and chemical-processing equipment. The Inflation Reduction Act unlocked USD 15 billion in composite capital expenditure during 2025 across resin compounding, SMC presses, and blade-molding plants. California Air Resources Board rules speed the migration to closed-mold and low-styrene resin systems, opening premium segments for suppliers with ultra-low emission portfolios. Mexico’s vehicle assemblies exceeded 4 million units in 2025, and local Tier-1s expanded SMC capacity to serve North American and European electric-vehicle programs.

Europe focuses on high-value marine, automotive, and wind-energy uses in the unsaturated polyester resin market. Germany’s carmakers consumed 180,000 t of composite resins in 2025 as Volkswagen, BMW, and Mercedes-Benz integrated SMC battery enclosures and structural components. The Circular Economy Action Plan and stricter Industrial Emissions rules push suppliers toward recyclable, bio-based chemistries. South America and Middle East and Africa remain smaller but fast-growing in the unsaturated polyester resin market, buoyed by Brazilian sanitation investments, Saudi chemical diversification, and South African mining infrastructure, each favoring fiberglass-reinforced equipment that lowers total life-cycle costs versus metals.

Competitive Landscape

Moderate concentration defines the unsaturated polyester resin market, with Polynt, AOC, Ashland, INEOS, and Allnex collectively holding nearly 64% of global capacity. Regional suppliers in China, India, and Southeast Asia win price-sensitive construction and transportation contracts through localized technical service and quick delivery. Integrated feedstock control is now central; Polynt’s maleic-anhydride acquisition and AOC’s glycol joint venture highlight moves to buffer cost swings.

Technology differentiation focuses on styrene-emission reduction, with ultra-low-styrene grades from Ashland and Scott Bader capturing building-certified projects in Scandinavia and the Benelux region. Patent activity accelerated, with the European Patent Office granting 47 filings in 2025 covering flame-retardant synergies, nanoparticle dispersion, and hybrid thermoplastic-thermoset structures. Smaller players such as Crystic Resins India, Zhejiang Tianhe Resin, and Swancor target niche, bio-based, or high-temperature segments, progressively eroding incumbent service advantages.

Industrial buyers in the unsaturated polyester resin market now mandate ISO 9001 and ISO 14001 certification, scope-3 emissions disclosures, and documented recycling options. Suppliers that showcase recycled-PET polyol chemistries or powder-resin SMC systems gain faster pre-qualification for electric-vehicle and wind-energy programs. The competitive field therefore balances cost leadership, feedstock security, and sustainability innovation, with partnerships between resin formulators, glass-fiber producers, and compounders becoming commonplace.

Unsaturated Polyester Resin (UPR) Industry Leaders

Polynt S.p.A.

AOC

INEOS

Ashland

Allnex GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: UK-based chemical distributor Bowden Chemicals was awarded a government grant to develop unsaturated polyester resins (UPR) using bio-based materials.

- September 2024: Exel Composites finalized a purchasing agreement with resin supplier INEOS for over 100 tonnes of its Envirez bio-based unsaturated polyester resin system. This agreement supported the company's transition away from hydrocarbon-derived resins.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the unsaturated polyester resin market as global revenues from fresh production of ortho, iso, DCPD, and other unsaturated polyester resins converted into composite matrices, gel coats, or cast parts for building and construction, transportation, electrical and electronics, marine, pipes and tanks, wind energy, and allied uses.

Scope Exclusion: Saturated polyesters, vinyl ester resins, and recycled feedstock tolling sit outside the scope.

Segmentation Overview

- By Raw Material

- Maleic Anhydride

- Phthalic Anhydride

- Propylene Glycol

- Styrene Monomer

- Others (Additives, Initiators)

- By Product Type

- Ortho-resins

- Isoresins

- Dicyclopentadiene (DCPD)

- Other Types

- By Form

- Liquid

- Powder

- By End-use Industry

- Building and Construction

- Chemical

- Electrical and Electronics

- Paints and Coatings

- Transportation

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Our analysts spoke with plant engineers, distributors, raw-material suppliers, and composite fabricators across Asia-Pacific, Europe, and the Americas. Those interviews confirmed utilization rates, contract price corridors, and early traction for bio-based grades, closing gaps left by published data.

Desk Research

We mined open datasets from UN Comtrade, Eurostat, and national chemical statistics, plus trade bodies such as the American Chemistry Council and PlasticsEurope, to map cross-border flows, demand nodes, and regulatory markers. Annual reports, 10-Ks, and verified press releases furnished capacity, investment, and average selling price clues, while patent abstracts signaled technology shifts.

To tighten numbers, we tapped snapshots from D&B Hoovers and Questel for producer revenues, pipeline grades, and forward-integration moves. The sources listed are illustrative, while many additional repositories fed the desk work.

Market-Sizing and Forecasting

A top-down reconstruction of production and trade volumes, adjusted for captive consumption, set the first market total, which we then cross-checked through selective bottom-up roll-ups of producer capacity multiplied by sampled ASPs. Key variables include maleic anhydride spreads, global housing starts, wind turbine blade installations, light vehicle build, and liquid resin indices. Multivariate regression with scenario overlays projects values to 2030, and missing supplier disclosures are bridged with region-specific consumption coefficients gleaned from interviews.

Data Validation and Update Cycle

Outputs pass a two-step peer review, variance triggers re-checks, and material events prompt mid-cycle revisions. Mordor refreshes each dataset annually and issues an interim update before client delivery.

Why Mordor's Unsaturated Polyester Resin Baseline Commands Confidence

Published estimates diverge because firms apply different resin mixes, pricing anchors, and currency bases. Mordor's disciplined scope and dual path modeling temper optimism and prevent undervaluation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.90 bn (2025) | Mordor Intelligence | N/A |

| USD 8.50 bn (2024) | Global Consultancy A | Narrower end use coverage and FOB price basis |

| USD 12.90 bn (2023) | Industry Publisher B | Older baseline, no trade normalization |

| USD 13.93 bn (2024) | Research House C | Includes saturated polyesters in total |

These contrasts show that our method delivers a balanced, transparent baseline that decision makers can trace to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the unsaturated polyester resin market in 2026?

The market stands at USD 11.95 billion in 2026, with a projected value of USD 15.04 billion by 2031.

Which segment is expanding the fastest within resin forms?

Powder is rising at a 6.16% CAGR as automotive and electrical producers adopt in-mold-coated SMC to cut emissions and cycle times.

Why is Asia-Pacific the leading consumer region?

China, India, and Southeast Asian nations channel large infrastructure budgets and manufacturing investments into corrosion-resistant composite pipes, panels, and wind-energy blades.

What drives electronics demand for unsaturated polyester resin?

Data-center construction and renewable-energy grids require flame-retardant transformer housings, printed-circuit-board laminates, and cable-management systems that use specialty resin grades.

Page last updated on: