United States Tinea Versicolor Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

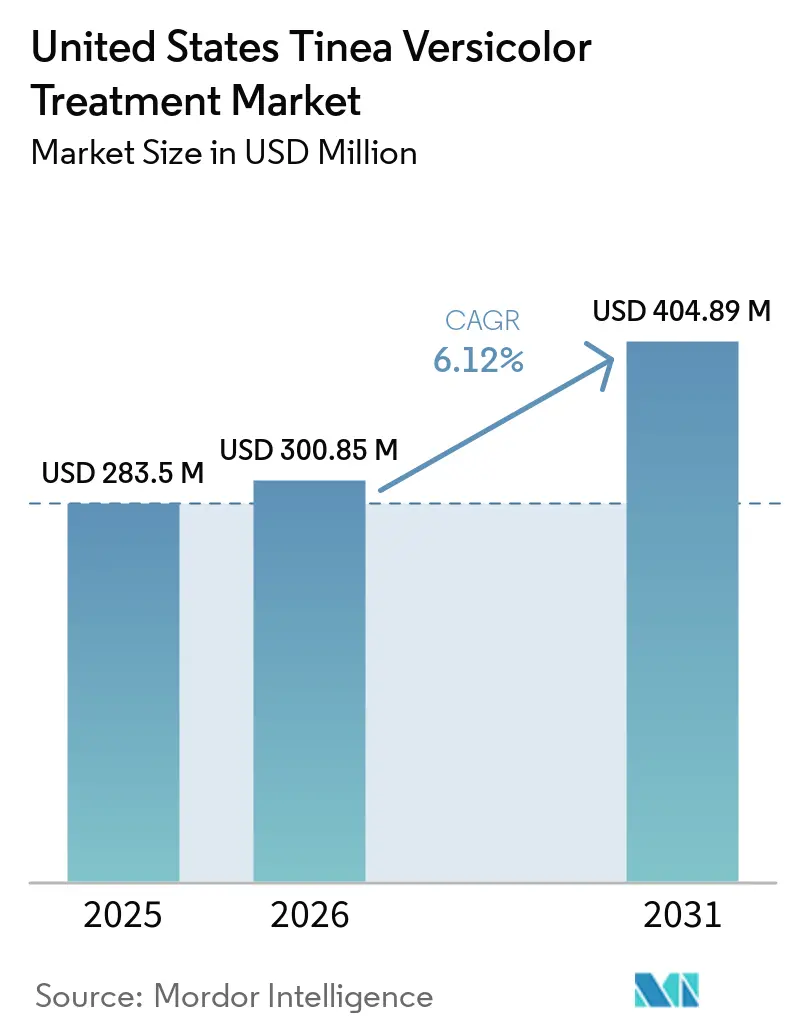

| Base Year Market Size (2025) | USD 283.5 Million |

| Market Size (2026) | USD 300.85 Million |

| Market Size (2031) | USD 404.89 Million |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Tinea Versicolor Treatment Market Analysis by Mordor Intelligence

The United States Tinea Versicolor Treatment Market size was valued at USD 283.5 million in 2025 and is estimated to grow from USD 300.85 million in 2026 to reach USD 404.89 million by 2031, at a CAGR of 6.12% during the forecast period (2026-2031).

In the market, recurrence changes the category from a one-time treatment purchase into an ongoing maintenance pattern because patients often return to medicated cleansers and topical products after symptoms reappear or pigment changes remain visible for longer periods. Younger patients also support steady demand because the condition is common in adolescents and young adults, with commercial insurance data showing the highest incidence in the 18 to 24 age group. Treatment decisions in the United States tinea versicolor treatment market are also shaped by persistent dyspigmentation after fungal clearance, since visible color change can last for weeks or months and often keeps patients in the treatment pathway even after the infection itself has improved. The United States tinea versicolor treatment market is further being influenced by broader digital access and by stronger demand from skin-of-color patient groups, where diagnosis patterns and concern around visible pigment changes are pushing brands and channels toward more targeted product positioning.

Key Report Takeaways

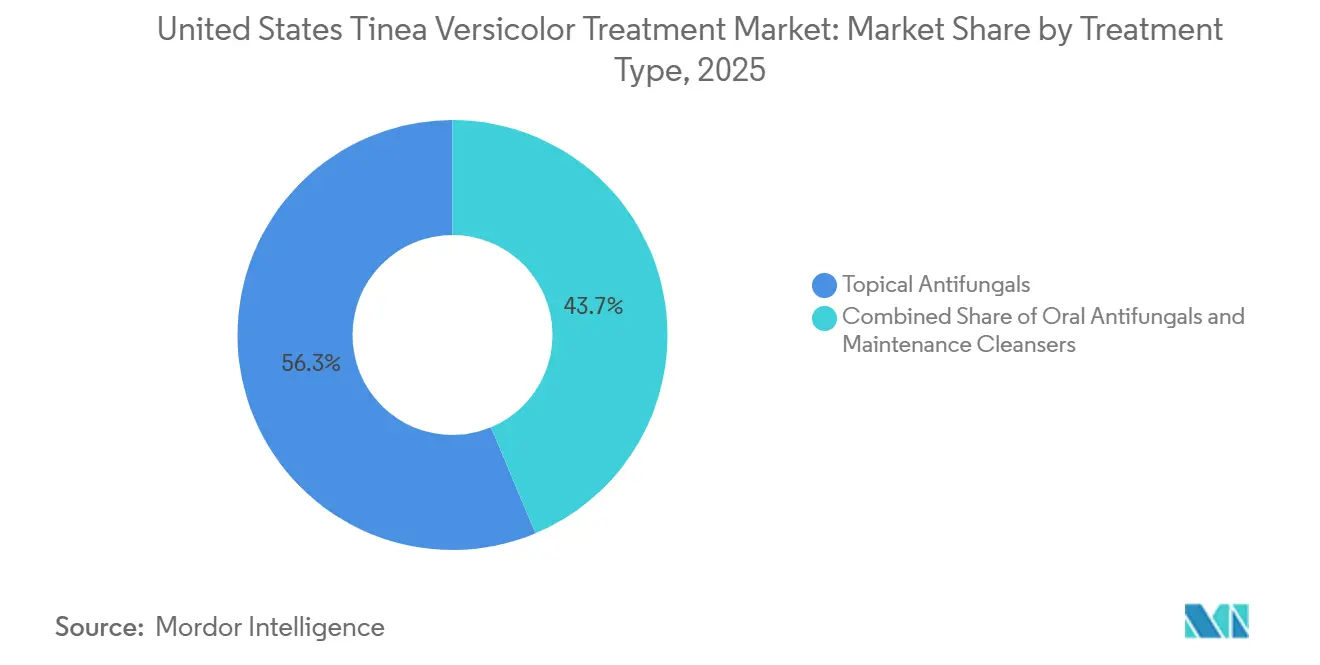

- By treatment type, topical antifungals remained the largest segment in 2025, and this category is projected to expand at 6.9% CAGR through 2031.

- By drug class, azoles held 69.2% revenue share in 2025, while the draft indicates rising interest in non-azole alternatives but does not provide a numeric CAGR for the fastest-growing drug-class segment.

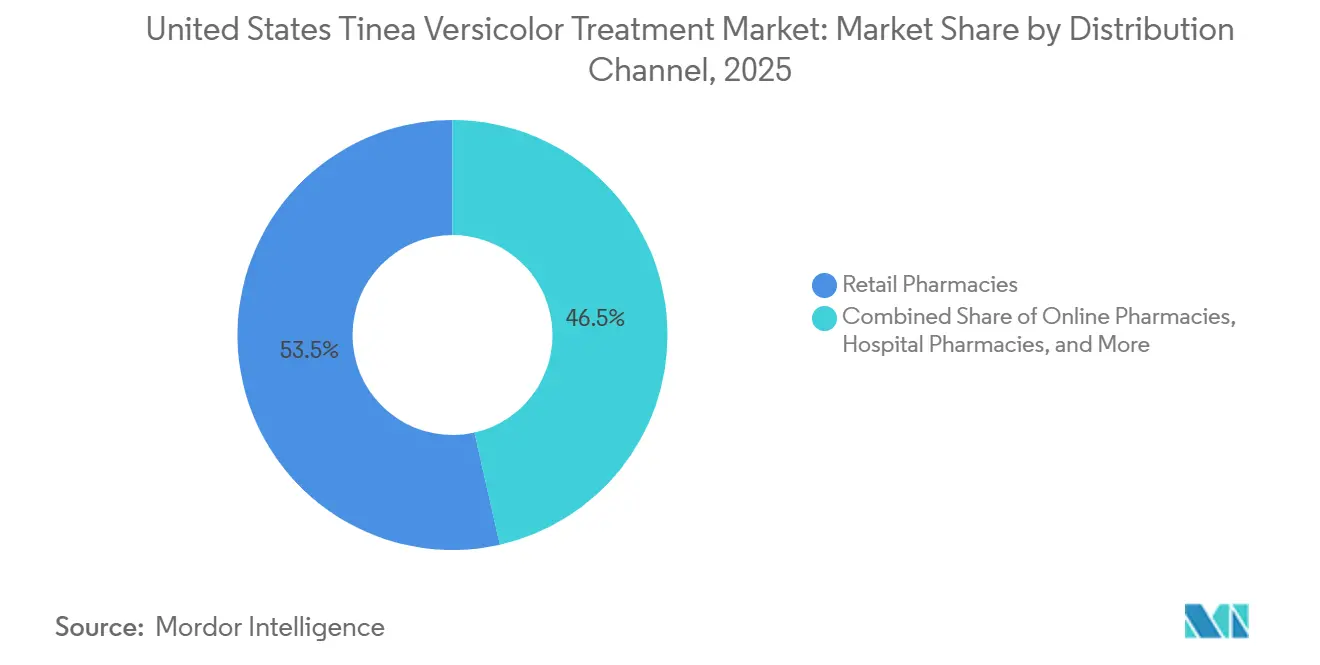

- By distribution channel, retail pharmacies held 53.5% in 2025, while online pharmacies are projected to expand at 8.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Tinea Versicolor Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High recurrence and prophylactic cleanser demand | +1.5% | National, with pronounced gains in humid regions (Southeast, Gulf Coast) | Short term (≤ 2 years) |

| OTC-to-Rx treatment ladder broadens spend capture | +1.2% | National | Medium term (2-4 years) |

| Broad ketoconazole generic availability improves access | +0.8% | National, with early urban gains | Short term (≤ 2 years) |

| Teledermatology accelerates mild-case diagnosis and refill cycles | +0.7% | National, with outsize impact in rural and underserved areas | Medium term (2-4 years) |

| Pigment-first care seeking lifts conversion in skin-of-color patients | +0.9% | National, concentrated in high-diversity metros (South Atlantic, Pacific, New England) | Medium term (2-4 years) |

| Summer-season visibility and humid microclimates sustain demand | +0.5% | Southeast, Gulf Coast, Pacific Northwest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Recurrence and Prophylactic Cleanser Demand

Recurrence is one of the strongest structural supports for the United States tinea versicolor treatment market because successful first-line treatment often does not end the care cycle. Clinical references note that recurrence is frequent, and both monthly topical antifungal use and regular use of pyrithione zinc cleansers are recommended to reduce the chance of return, especially in warm and humid settings[1]“Tinea Versicolor, Diagnosis and Treatment,” American Academy of Dermatology, aad.org. StatPearls also describes preventive use of selenium sulfide 2.5% or ketoconazole 2% shampoo once per month, which supports a recurring purchase pattern for maintenance products rather than a single acute treatment event. This recurring cleanser loop matters commercially because a large part of maintenance demand sits in OTC channels, so continued spending can happen without a repeat office visit or a new prescription. In the United States tinea versicolor treatment market, that makes prophylactic cleansing one of the most stable sources of repeat demand, particularly in humid regions where relapse pressure is higher and seasonal visibility tends to increase patient vigilance. The same pattern also protects volume when insurer controls become tighter, because patients can keep buying maintenance shampoos and washes through retail and online channels.

OTC-to-Rx Treatment Ladder Broadens Spend Capture

The United States tinea versicolor treatment market benefits from a clear treatment ladder that begins with OTC shampoos and cleansers, then moves to prescription topicals, and only later reaches oral therapy for more difficult cases. The American Academy of Dermatology lists selenium sulfide, ketoconazole, and pyrithione zinc among common topical treatment options, while oral antifungal pills are reserved for more extensive, thick, or frequently recurring presentations. Merck and StatPearls similarly place topical therapy first and keep oral use for extensive disease or resistant cases, which means a patient can move across several price points over one recurrence cycle rather than staying within a single purchase category. This structure widens spend capture because incomplete visible recovery often keeps patients engaged longer, even when the underlying fungal burden has already fallen. In the United States tinea versicolor treatment market, lingering pigment changes matter commercially because they can look like treatment failure to patients and can trigger another OTC purchase or a step-up into the prescription channel. That pattern supports both low-cost mass products and higher-value prescribed therapies without requiring a major change in the disease burden itself.

Broad Ketoconazole Generic Availability Improves Access

Broad generic participation supports the United States tinea versicolor treatment market by lowering the cost of standard therapy and widening the number of channels through which patients can fill prescriptions. Teva continues to list ketoconazole 2% cream as an AB-rated generic in its U.S. catalog, which confirms that generic azole options remain available and clinically substitutable for reference products[2]Teva Pharmaceuticals USA, “Ketoconazole Cream,” Teva Generics Catalog, tevausa.com. This matters because the Mycoses database study found that uninsured patients had only 0.42 times the adjusted odds of a pityriasis versicolor diagnosis compared with insured patients, which points to suppressed diagnosis and treatment conversion rather than lower biological incidence. Lower out-of-pocket exposure can therefore lift fill rates and improve persistence once patients enter the formal care pathway. The United States tinea versicolor treatment market also becomes more resilient when generic supply broadens, because price compression on basic topical azoles expands access even while it reduces the ability of manufacturers to hold premium pricing. Within routine office practice, that combination tends to favor volume and availability over brand-led differentiation.

Teledermatology Accelerates Mild-Case Diagnosis and Refill Cycles

Teledermatology is becoming a practical growth support for the United States tinea versicolor treatment market because this condition is largely visual and often does not require invasive confirmation in straightforward cases. Commercial insurance data showed the highest incidence in 18 to 24 year olds, and that age group is also one of the most digitally comfortable patient groups for remote consultation and refill management. Faster digital triage can shorten the path from symptom recognition to a prescribed topical product, especially when discoloration rather than discomfort is the main reason for seeking care. That same workflow also supports recurring refill behavior, since patients dealing with relapse or with incomplete visible recovery can re-enter care without the same friction as a traditional in-person visit. In the United States tinea versicolor treatment market, this matters most for mild and moderate cases that can be managed with standard topical protocols and recurring cleanser use rather than complex systemic therapy. The digital shift also supports underserved areas where dermatologist access is thinner and where underdiagnosis has historically limited formal treatment capture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Benign cosmetic perception suppresses prescription uptake | -0.8% | National | Short term (≤ 2 years) |

| Oral azole interaction and hepatotoxicity concerns limit escalation | -0.6% | National | Long term (≥ 4 years) |

| Low diagnostic confirmation rates increase misdiagnosis risk | -0.5% | National, more severe in rural and underserved areas | Medium term (2-4 years) |

| Persistent dyspigmentation after cure reduces perceived efficacy | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Benign Cosmetic Perception Suppresses Prescription Uptake

A major brake on the United States tinea versicolor treatment market is that many patients still view the condition as a cosmetic issue rather than a clinical condition that deserves structured treatment and recurrence prevention. In the large U.S. commercial insurance analysis, 44.9% of patients saw a dermatologist, 21.9% saw a general practitioner, and 15.4% were seen by nurse practitioners or physician assistants, which shows that a meaningful share of affected people never enters specialist care at all. That behavior limits prescription capture because many patients choose prolonged OTC self-management instead of moving to a clinician-guided regimen. The low sense of urgency is reinforced by the fact that lesions are usually more visible than painful, so treatment delay does not carry the same everyday burden seen in symptomatic inflammatory disorders. In the United States tinea versicolor treatment market, this perception also interacts with access disparities, because patients with darker skin may be more motivated to seek care due to visible contrast changes, yet the same populations still show signs of diagnosis and access barriers that can interrupt conversion into treated demand. As a result, awareness and education remain important, but they are not yet strong enough to fully close the gap between disease presence and prescription uptake.

Oral Azole Interaction and Hepatotoxicity Concerns Limit Escalation

The United States tinea versicolor treatment market faces a clear ceiling on oral therapy because physicians remain cautious about moving beyond topical care for a condition that is usually superficial and visually managed. StatPearls states that oral ketoconazole is not recommended because of severe adverse effects, and it also notes that oral terbinafine is ineffective for this condition. Merck and the American Academy of Dermatology keep oral therapy for extensive disease, resistant cases, or frequent recurrence, which leaves fluconazole and itraconazole as narrower second-line options rather than broad volume drivers. This prescribing caution keeps many moderate cases in extended topical protocols, even when patients are frustrated by recurrence or delayed repigmentation. In the United States tinea versicolor treatment market, that means the oral segment remains the smallest treatment category through the forecast period, not because the need disappears, but because the safety and interaction profile of available oral agents narrows the set of patients for whom escalation looks worthwhile.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Topical Formulations Define Market Cadence

Topical antifungals are projected to expand at 6.9% CAGR through 2031, which keeps them at the center of the United States tinea versicolor treatment market. Within the United States tinea versicolor treatment industry, topical therapy remains the default starting point because it matches first-line clinical guidance, carries low systemic risk, and is available through both prescription and OTC formats. This dual-channel structure gives the segment unusual depth, since physician-prescribed products handle broader or stubborn cases while OTC products support early self-care and recurring maintenance. StatPearls reports that ketoconazole 2% shampoo produced mycologic cure in around 80% of patients under both single-day and three-day regimens, which helps explain why topical options continue to dominate treatment pathways. Even after fungal clearance, patient satisfaction does not always improve at the same pace because visible pigment changes can persist for months, so topical use often extends beyond the point where the infection itself has already responded.

The fastest-moving recurring purchase pattern inside this segment is the prophylactic and maintenance cleanser subcategory, which adds continuity to the United States tinea versicolor treatment market even when acute episodes are not active. Monthly selenium sulfide or ketoconazole shampoo protocols are explicitly described in clinical references, and the American Academy of Dermatology also recommends once- or twice-monthly medicated cleanser use to help prevent recurrence during warm and humid periods. That maintenance logic is commercially powerful because a patient using a cleanser every month can create a long run of recurring purchases, while acute therapy usually produces only a few purchase events around a flare. It also leaves a meaningful part of demand outside insurer management because many of these products can be bought directly at retail or through digital channels without a new office visit. By contrast, oral antifungals remain the smallest treatment segment in the United States tinea versicolor treatment market because their role is largely limited to resistant, widespread, or frequently recurring cases, and even there prescribers stay cautious because safer topical pathways often remain available.

By Drug Class: Azoles Anchor Revenue but Alternatives Retain Clinical Relevance

Azoles held 69.2% of the United States tinea versicolor treatment market share in 2025, which reflects their long-standing place as the main therapeutic backbone for both prescription and many routine care pathways. Merck and the American Academy of Dermatology continue to list ketoconazole and other topical azoles among standard treatment choices, which supports volume across creams, shampoos, and repeat-use regimens. Generic availability keeps the class deeply embedded in regular practice, and Teva’s active listing of AB-rated ketoconazole 2% cream shows that the class remains supported by a broad generic supply base rather than by a narrow branded set. That structure makes the azole layer volume-driven, because lower pricing improves fill access and supports repeat prescriptions even while it narrows margins for manufacturers. Oral fluconazole and itraconazole add an escalation route, but their use remains more selective, so most class value still rests on topical azoles rather than on oral expansion.

Alternative drug classes still matter in the United States tinea versicolor treatment market because they support OTC self-care, maintenance use, and patient choice outside a prescription-first model. Selenium sulfide and pyrithione zinc are both recognized in clinical and association guidance as standard topical ingredients for treatment and recurrence control. DailyMed shows active selenium sulfide 1% Selsun Blue product labeling updated in February 2026, which confirms continued commercial presence for this cleanser-based alternative in U.S. self-care channels. Within the United States tinea versicolor treatment industry, these non-azole options are important because they support a maintenance pattern that is often driven by routine cleanser use rather than by a physician-directed short course. Other topical antifungals such as ciclopirox fill smaller clinical niches, while oral terbinafine does not strengthen this segment because StatPearls identifies it as ineffective for pityriasis versicolor.

By Distribution Channel: Digital Growth Builds on a Retail Base

Online pharmacies are projected to expand at 8.3% CAGR through 2031, making them the fastest-growing outlet in the United States tinea versicolor treatment market. Their growth is closely tied to digital care pathways, since remote consultation, e-prescribing, and automated refill workflows fit a condition that is usually assessed visually and often managed with standard topical products. This channel also matches the age profile of demand, because younger adults represent the highest-incidence group and are more comfortable using digital health and fulfillment tools for recurring needs. The online model is especially attractive for repeat cleanser and maintenance purchases, where convenience and subscription-like refill behavior matter more than immediate in-person counseling. In the United States tinea versicolor treatment market, that means digital channels are not only winning prescription volume, but are also gaining from recurring OTC demand that can be reordered with minimal friction.

Retail pharmacies led 53.5% of the United States tinea versicolor treatment market share because immediate access continues to shape purchase behavior for this condition. Their advantage comes from shelf visibility, same-day product availability, and pharmacist guidance, all of which matter when patients first notice visible patches and want treatment without delay. Retail remains important for both standard OTC shampoos and short-course prescription topicals because it connects self-selection and clinician-directed care within one familiar setting. Hospital and clinic pharmacies play a smaller role, but they remain relevant for immunocompromised patients and other more closely managed cases, which aligns with the higher odds of pityriasis versicolor seen in transplant recipients, people living with HIV, and patients with other immunocompromising conditions in U.S. claims data. A further layer sits outside conventional tracking because some dermatology practices route patients toward in-house dispensing or compounding partners, which modestly widens the cleanser and topical revenue base in the United States tinea versicolor treatment market.

Geography Analysis

The Northeast showed the highest commercial insurance-based incidence of pityriasis versicolor at 3.5 per 1,000 person-years, which makes it the clearest diagnosed demand cluster inside the United States tinea versicolor treatment market[3]Jeremy A. W. Gold, Kaitlin Benedict, and Shari R. Lipner, “Pityriasis Versicolor Epidemiology, Disease Predictors, and Health Care Utilization, Analysis of 32,679 Cases in a Large Commercial Insurance Database,” Journal of the American Academy of Dermatology, stacks.cdc.gov. That pattern looks unusual at first because warm and humid climates are often linked with higher prevalence, yet diagnosis intensity depends on more than climate alone. Dense urban populations, a large insured young-adult base, and stronger dermatologist availability help explain why the Northeast produces a high rate of formally captured cases. The South and Gulf Coast likely carry heavier biological risk because heat and humidity support the shift of Malassezia from a normal skin commensal to a pathogenic form. Even so, lower specialist access in parts of those regions can keep diagnosed and treated volume below the underlying burden, which leaves meaningful room for retail-led education and virtual care expansion.

Skin-of-color population concentration also shapes the United States tinea versicolor treatment market across major urban corridors in the South Atlantic, Pacific Coast, and metropolitan Texas. The Mycoses national database study found higher adjusted odds among Black patients and also pointed to elevated odds in other non-White patient groups, which supports stronger demand from populations where pigment contrast makes lesions more noticeable. That matters because the color change can remain lighter or darker than surrounding skin for weeks to months after treatment, so the visible burden often lasts longer than the active fungal episode. As a result, product messaging in diverse metro areas is moving closer to pigment recovery, appearance, and maintenance rather than focusing only on fungal clearance.

The Sun Belt provides a persistent climate-driven demand base for the United States tinea versicolor treatment market because warm conditions increase the need for recurring cleanser use and relapse prevention. Rural parts of the South and Midwest still represent underdiagnosed space, since lower access can suppress treatment capture even when disease burden is present. The United States tinea versicolor treatment market will therefore see the best incremental gains in areas where warm climate, younger populations, and easier digital access overlap. Geography in this category is shaped not only by where the yeast thrives, but also by where patients can obtain a diagnosis quickly and where visible pigment change is more likely to prompt continued product use.

Competitive Landscape

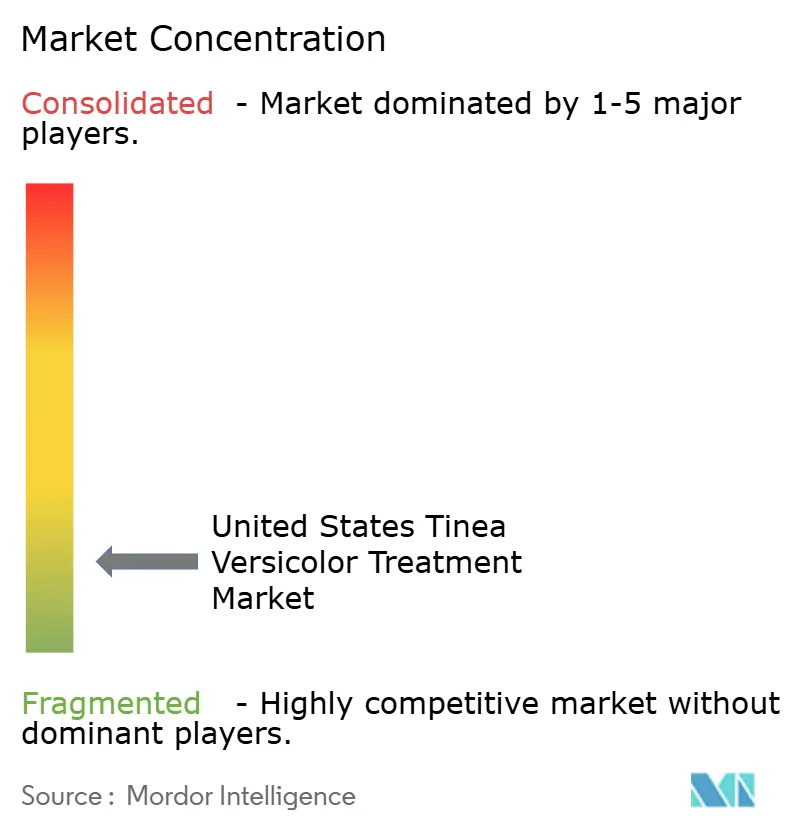

The United States tinea versicolor treatment market has a fragmented structure that combines branded OTC consumer health companies with a broad field of generic topical suppliers. Branded presence remains visible through companies such as Procter & Gamble, Perrigo, Bayer, and Opella, while generic manufacturers compete through standard topical formats sold into retail and online channels. Teva’s active listing of AB-rated ketoconazole 2% cream illustrates the role of generics in keeping the market accessible and price-sensitive rather than tightly concentrated around a small branded group. This balance keeps competition focused on shelf presence, distribution reach, and refill continuity, because basic antifungal efficacy is widely available and difficult to defend with premium pricing alone.

Several recent company moves show how competition is evolving inside the United States tinea versicolor treatment market. DailyMed listed Head & Shoulders Bare Minimal Ingredients Itchy Scalp Relief pyrithione zinc shampoo in January 2025, which supports the view that Procter & Gamble is extending medicated cleanser positioning through cleaner-label style formats that can attract broader self-care users. Perrigo launched a two-year Operational Enhancement Program targeting USD 80 million to USD 100 million in annualized savings, with most benefits expected in 2026, which shows a clear push toward cost discipline and a more resilient OTC platform. Perrigo also moved ahead with the divestiture of its dermacosmetics business for up to EUR 332.6 million (USD 361.9 million), which signals a sharper portfolio focus on core self-care categories rather than a wider dermatology mix. Together, these steps suggest that scale, channel control, and efficient brand support matter more than broad product breadth when companies compete for recurring cleanser and topical demand.

Competitive pressure is also coming from adjacent antifungal brand building and from digital care models. Karo Healthcare entered an exclusive licensing agreement with Moberg Pharma in November 2025 for MOB-015, to be commercialized under the Lamisil brand in 19 European markets, which does not directly change U.S. tinea versicolor sales but does show a continued effort to strengthen antifungal brand equity around dermatology use cases. At the same time, telehealth-integrated prescription services are compressing the path from symptom recognition to product fulfillment, which puts pressure on slower clinic-based pathways for mild and moderate cases. Because oral escalation remains constrained and topical generics are widely available, lasting differentiation in the United States tinea versicolor treatment market is shifting toward convenience, visibility, trusted labeling, and repeat-purchase systems rather than toward breakthrough therapy claims. That leaves room for share movement, but it also keeps the category structurally resistant to durable pricing power.

United States Tinea Versicolor Treatment Industry Leaders

Taro Pharmaceuticals U.S.A., Inc.

Padagis US LLC

Bayer AG

Opella Healthcare Group SAS

Teva Pharmaceuticals USA, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Perrigo Company plc officially completed the divestiture of its Dermacosmetics branded business to Karo Healthcare.

- February 2026: DailyMed records reflect revised February 2026 labeling for multiple Selsun Blue selenium sulfide 1% products, reflecting ongoing formulation and claims updates for the key prophylactic cleanser brand used in pityriasis versicolor maintenance therapy.

United States Tinea Versicolor Treatment Market Report Scope

As per the scope of the report, Tinea Versicolor, also known as pityriasis versicolor, is a common fungal skin infection caused by the Malassezia species. It is characterized by the appearance of discolored patches on the skin, which may be lighter or darker than the surrounding skin. Tinea Versicolor treatment refers to the medical interventions aimed at eliminating the fungal infection caused by Malassezia species.

The segmentation of the United States tinea versicolor treatment market is based on treatment type, drug class, and distribution channel. By treatment type, the market is divided into topical antifungals, oral antifungals, and prophylactic/maintenance cleansers. By drug class, it is categorized into azoles, selenium sulfide, zinc pyrithione, and other topical antifungals. By distribution channel, the market is segmented into retail pharmacies, online pharmacies, hospital and clinic pharmacies, and other distribution channels. For each segment, the market size and forecast are provided in terms of value (USD).

| Topical Antifungals |

| Oral Antifungals |

| Prophylactic / Maintenance Cleansers |

| Azoles |

| Selenium Sulfide |

| Zinc Pyrithione |

| Other Topical Antifungals |

| Retail Pharmacies |

| Online Pharmacies |

| Hospital and Clinic Pharmacies |

| Other Distribution Channels |

| By Treatment Type | Topical Antifungals |

| Oral Antifungals | |

| Prophylactic / Maintenance Cleansers | |

| By Drug Class | Azoles |

| Selenium Sulfide | |

| Zinc Pyrithione | |

| Other Topical Antifungals | |

| By Distribution Channel | Retail Pharmacies |

| Online Pharmacies | |

| Hospital and Clinic Pharmacies | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the 2026 value of the United States tinea versicolor treatment space?

It stands at USD 300.85 million in 2026 and is forecast to reach USD 404.89 million by 2031 at a 6.12% CAGR, supported by repeat treatment demand and maintenance cleanser use.

Why do topical products account for most demand in the United States?

Topical antifungals remain first-line therapy, carry low systemic risk, and are available in both prescription and OTC forms. That combination keeps them as the largest treatment type and supports a 6.9% CAGR through 2031.

Why is recurrence so important for sales growth?

Recurrence is common, and clinical references recommend regular preventive cleanser use in many patients. This turns spending into a recurring pattern rather than a one-time acute purchase cycle.

Which drug class leads revenue in 2025?

Azoles lead the category with 69.2% revenue share in 2025 because ketoconazole and related agents remain central to routine treatment pathways and generic access is strong.

Which sales channel is expanding the fastest?

Online pharmacies are growing the fastest, with an 8.3% CAGR through 2031. Their growth is supported by telehealth workflows, refill automation, and recurring maintenance product purchases.

Why does oral therapy remain a smaller part of care?

Oral agents are usually reserved for resistant or widespread cases, while safety concerns and interaction risk keep many patients on topical protocols. That limits the expansion potential of oral antifungals.

Page last updated on: