Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

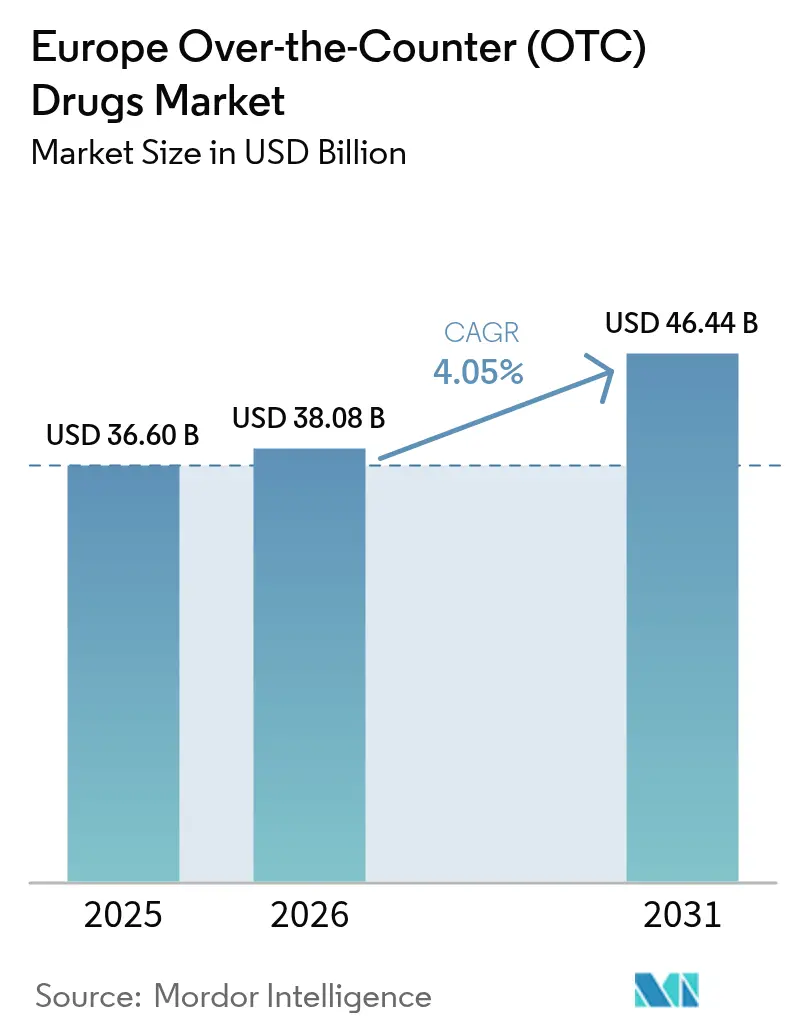

| Base Year Market Size (2025) | USD 36.60 Billion |

| Market Size (2026) | USD 38.08 Billion |

| Market Size (2031) | USD 46.44 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Over-the-Counter (OTC) Drugs Market Analysis by Mordor Intelligence

The Europe Over-the-Counter Drugs Market size is projected to be USD 36.60 billion in 2025, USD 38.08 billion in 2026, and reach USD 46.44 billion by 2031, growing at a CAGR of 4.05% from 2026 to 2031.

Chronic self-care categories are displacing the historic cold-and-flu focus, and higher-margin segments such as joint-mobility analgesics, healthy-ageing vitamins, and digital-first e-pharmacy channels are setting the growth tempo. Germany remains the revenue anchor, yet Spain is accelerating fastest as recent e-pharmacy legalization unlocks online traffic. Formulation preferences are also shifting: tablets still dominate, but gummies and dissolvable films are rising as manufacturers resolve stability challenges and appeal to pill-fatigued users. Demographic change underpins demand: ageing Europeans prefer convenient OTC supplements that reduce prescription counts, and adults in the working-age band sustain preventive self-medication habits.

Key Report Takeaways

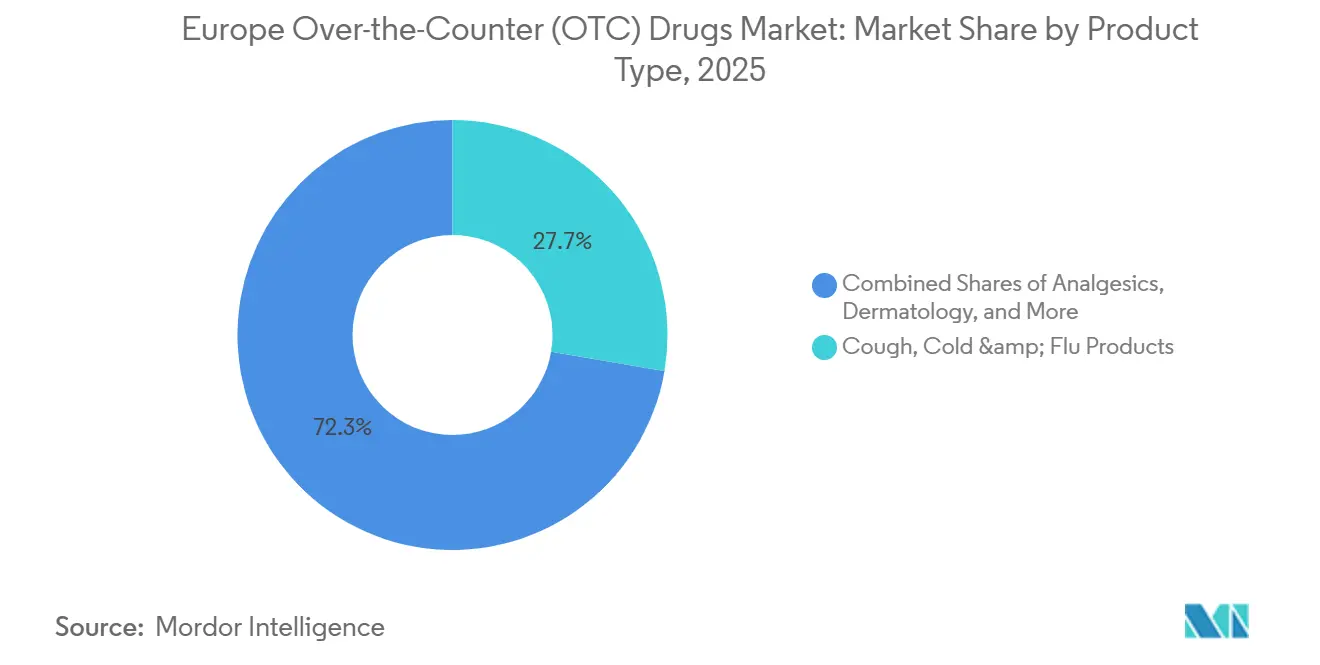

- By product type, cough, cold & flu retained 27.68% of the Europe over-the-counter (OTC) drugs market share in 2025, yet Analgesics are on track for the fastest climb at a 7.20% CAGR through 2031.

- By formulation, tablets & caplets commanded 47.12% of the Europe over-the-counter (OTC) drugs market in 2025, while gummies, lozenges & dissolvable Films are forecast to grow at 10.83% annually to 2031.

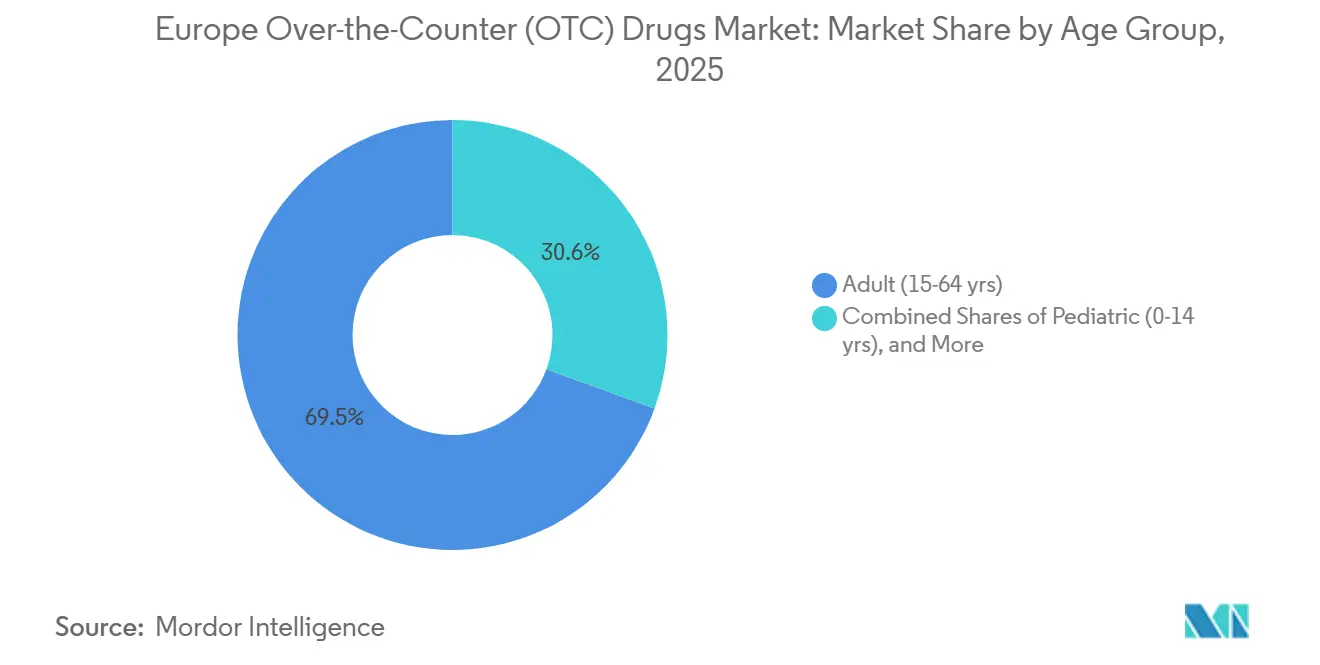

- By age group, adults accounted for 69.45% of revenue in 2025; the geriatric segment posts the fastest expansion at a 7.72% CAGR to 2031.

- By sales format, branded products held 67.85% of revenue in 2025, yet private-label lines are advancing at a 9.78% CAGR.

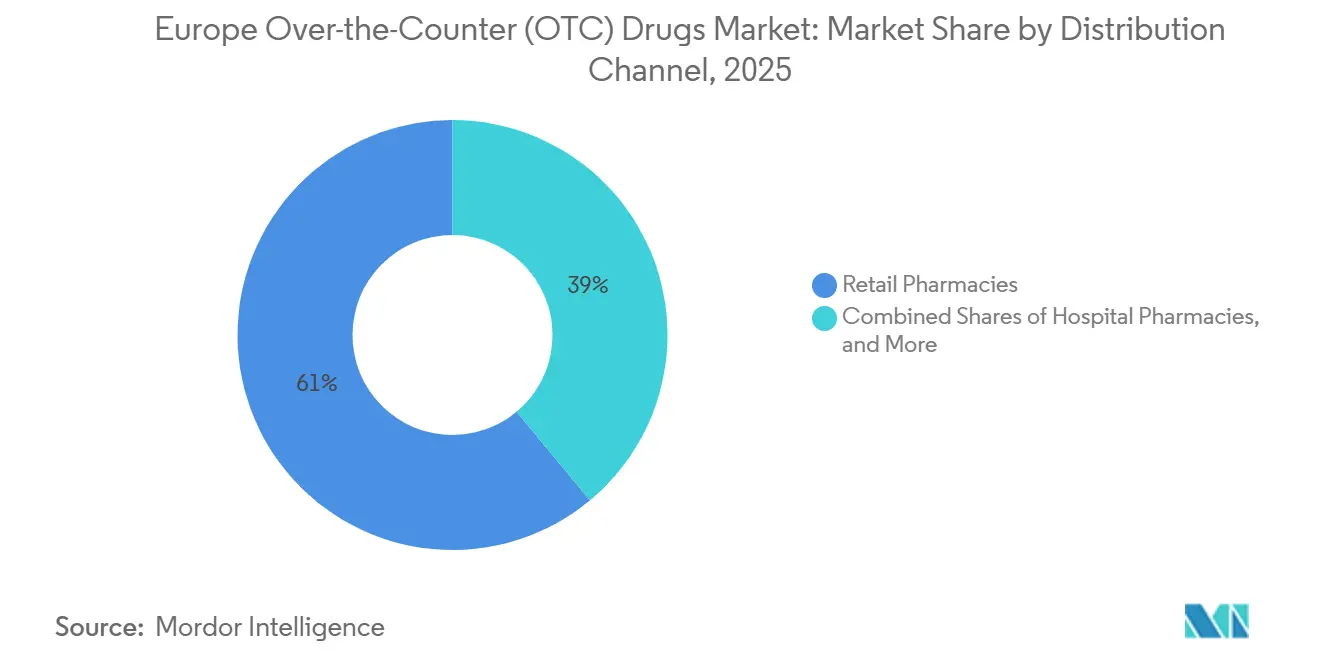

- By distribution channel, retail pharmacies accounted for 61.05% of turnover in 2025, whereas online pharmacies are expanding at 12.18% per year through 2031.

- Germany captured 25.27% of 2025 revenue; Spain is the growth front-runner with a 7.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Over-the-Counter (OTC) Drugs Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Ageing European population boosting chronic self-care demand | +0.8% | Germany, Italy, France, Spain—highest median ages | Long term (≥ 4 years) |

| Rx-to-OTC switch momentum for allergy, migraine, and women's health molecules | +0.6% | UK (MHRA fast-track), Germany, France (ANSM approvals) | Medium term (2-4 years) |

| Digital symptom-checker apps accelerating e-pharmacy conversion | +0.7% | Germany, UK, Netherlands—mature digital health infrastructure | Short term (≤ 2 years) |

| Post-COVID trust in pharmacists is fueling premium VMS uptake | +0.5% | Global, with the strongest effect in Southern and Central Europe | Medium term (2-4 years) |

| Pharmacy service-fee reimbursement schemes incentivizing OTC recommendation | +0.4% | UK (Pharmacy First), Germany (vaccination fees), Netherlands, Spain (pilots) | Short term (≤ 2 years) |

| AI-driven demand forecasting reduces stock-outs and widens category loyalty | +0.3% | Germany, France, UK—large pharmacy chains with digital infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ageing European Population Boosting Chronic Self-Care Demand

Europe’s greying demographics are converting episodic purchases into habitual chronic-care routines. Older consumers seek OTC glucosamine, omega-3, and calcium-vitamin D that sidestep prescription polypharmacy risks. Germany and Italy, where the median age exceeds 47 years, favor easy-to-swallow liquids and dissolvable films. IBSA responded in 2025 by extending FilmTec vitamin D3 and iron + folic acid strips across eight countries, adding a premium convenience layer.[1]IBSA Group, “IBSA launches orodispersible film supplements in new European countries,” ibsagroup.com National payers are reinforcing the trend; Germany’s 2024 policy added specific probiotics and deficiency-state vitamins to reimbursable OTC lists, subsidizing self-care and reducing general-practitioner visits.

Rx-to-OTC Switch Momentum for Allergy, Migraine, and Women’s-Health Molecules

Regulators are fast-tracking prescription reclassifications to widen patient access and ease healthcare costs. The UK MHRA cleared fluticasone furoate nasal spray for adolescents in December 2025, capturing seasonal allergy demand. Germany moved select triptans to pharmacy-only status in 2024, shifting migraine relief to community outlets. The AESGP recorded 26 national switches between 2020 and 2024, dominated by emergency contraception and low-dose proton-pump inhibitors. Although post-market surveillance now requires stringent patient-leaflet updates, the wider shelf exposure elevates revenue opportunities for category leaders.

Digital Symptom-Checker Apps Accelerating E-Pharmacy Conversion

AI-driven apps from Germany’s DocMorris and Shop Apotheke guide users from vague symptoms to curated OTC baskets with same-day delivery. These tools rely on anonymized data from the European Health Data Space, ensuring alignment with EMA indications and local protocols. France remains cautious; ANSM rules compel a live-pharmacist chat layer, which limits conversion and keeps online penetration below 5%. The resulting two-speed landscape fuels double-digit online growth in Germany, the Netherlands, and the UK, while Southern Europe remains pharmacy-centric.

Post-COVID Consumer Trust in Pharmacies Driving Premium VMS Uptake

During the pandemic, community pharmacists became trusted health advisers, and that reputation now lifts premium VMS sales. In November 2024, the European Food Safety Authority[2]European Food Safety Authority, “Guidance for Establishing and Applying Tolerable Upper Intake Levels for Vitamins and Essential Minerals,” efsa.onlinelibrary.wiley.com issued guidance on upper intake levels, giving pharmacists clear talking points on safe nutrient levels. Brands that align their formulations with these guidelines earn prime counter space and are granted permission to charge premium prices even in budget-sensitive regions. Store audits reveal that when pharmacists proactively discuss immune support with shoppers, customers often purchase a three-month pack rather than a trial size, doubling basket value. Bricks-and-mortar chains are pairing this advisory strength with subscription refill programs originally native to pure-play e-pharmacies, thereby locking in repeat revenue.

Restraints Impact Analysis of Europe Over-the-Counter (OTC) Drugs Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented, country-specific advertising bans inflate launch costs | -0.4% | France, Italy, Spain—strictest advertising rules; Germany more permissive | Long term (≥ 4 years) |

| Rising NSAID safety alerts are curbing repeat analgesic purchases | -0.5% | EU-wide (EMA jurisdiction); Germany, UK highest NSAID consumption | Medium term (2-4 years) |

| Parallel-trade leakage from low-price markets is eroding margins | -0.3% | Germany (destination), Eastern Europe (source markets: Poland, Romania, Bulgaria) | Short term (≤ 2 years) |

| API supply disruptions linked to Asia's environmental clampdowns | -0.4% | Global, with acute impact on generic OTC manufacturers in Germany, Italy, Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented, Country-Specific Advertising Bans Inflate Launch Costs

The European Directorate for the Quality of Medicines & HealthCare[3]World Health Organization, “Ageing and Health in Europe,” who.int reported in 2024 that close to half of the region’s regulators split non-prescription medicines into sub-classes, each carrying its own marketing rules. These fragmented requirements force marketers to create separate ads, pack warnings, and even taglines for each jurisdiction, turning a pan-European campaign into an expensive choreography of micro-versions. Digital-first brands versed in social media find themselves re-editing influencer videos or geo-blocking content to avoid non-compliance fines. To reduce risk, many companies shift spending toward pharmacy education kits and doctor-detailing leaflets, where the compliance hurdles are lower. The result is a quiet re-empowerment of healthcare professionals as gatekeepers to consumer awareness, particularly in categories such as weight management, where education is critical.

Rising NSAID Safety Alerts Curbing Repeat Analgesic Purchases

An uptick in safety notices about long-term or high-dose NSAID use is prompting pharmacists to counsel shoppers on safer dosing intervals or alternative formats. Consumers increasingly reach for topical gels, heat patches, or combination products that promise effective relief with less systemic exposure. Retailers are dedicating separate shelf tags to “gentle pain management,” steering vulnerable groups toward lower-risk choices. In response, manufacturers reformulate existing best-sellers into fast-dissolving or reduced-dose tablets, pairing analgesic power with gastro-protective agents. The intensified focus on safe use is also widening interest in non-NSAID active ingredients, broadening research pipelines beyond the historical ibuprofen–paracetamol axis. Germany and France already require prescriptions for higher-strength diclofenac, and OTC daily ibuprofen doses are limited to 1,200 mg. Long-term joint-pain patients migrate either to topical gels or to prescription COX-2 inhibitors, shaving revenue from the high-volume oral category.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Over-the-Counter (OTC) Drugs Market Segment Analysis

By Product Type:

Chronic-Care Categories Outpace Acute TreatmentsCough, cold & flu held 27.68% of 2025 revenue, yet mild flu seasons and post-pandemic household stockpiles tempered replenishment. Analgesics, buoyed by positioning around joint mobility and healthy ageing, are climbing at a 7.20% CAGR. Voltaren’s topical and systemic combinations spearhead the pivot toward long-term musculoskeletal health. Vitamins, minerals & supplements add breadth; Centrum Vital+ and personalized Daily Kits attract seniors seeking proactive wellness. CBD-infused oils, first listed at Boots in 2025, illustrate new-age relaxation niches. Demand spikes no longer follow only winter patterns; micro-peaks align with school term openings and sudden weather swings, forcing supply chains to react in near real time.

By Formulation:

Novel Delivery Systems Command Premium PricingTablets, the heritage backbone, still represented 47.12% of sales in 2025. Yet gummies, lozenges, and dissolvable films are sprinting ahead at a 10.83% CAGR as stability barriers fall. Sirio Pharma’s XtraGummies, launched in March 2025 with 1,800 mg creatine per serving, underscored the potency leap possible in confectionery formats. Consumers welcome the chewable convenience, and retailers highlight higher basket values.

These innovations broaden the Europe over-the-counter (OTC) Drugs market by attracting pill-fatigued adults and dysphagic seniors. Liquids and syrups, especially sugar-free variants, are regaining favor among diabetics and weight-watchers. The moves, taken together, diversify delivery platforms, buffering the Europe over-the-counter (OTC) Drugs market share of legacy tablets.

By Age Group:

Geriatric Segment Drives PremiumizationAdults aged 15-64 accounted for 69.45% of 2025 revenue, as workplace wellness programs subsidized cold-and-flu kits and VMS bundles. Growth momentum, however, lies with seniors: the 65-plus bracket is expanding at 7.72% annually, nearly double the pace of the broader Europe over-the-counter (OTC) Drugs industry. Swallow-free formats, large-print labels, and unit-dose sachets play directly to ageing consumers.

The Europe over-the-counter (OTC) Drugs market for geriatric-focused products is set to expand further as concerns about polypharmacy nudge seniors toward OTC solutions that lower prescription counts. Pediatric demand remains modest amid declining birth rates and tighter EMA safety rules on under-12 usage.

By Sales Format:

Private Label Disrupts Branded FortressBranded lines still own 67.85% of revenue, but pharmacy and grocery chains are fast-tracking private-label rollouts at a 9.78% CAGR. Walgreens Boots Alliance expanded its store-brand line of pain relievers and antihistamines in 2025, placing them at eye level and pricing them 20% below national brands. Generic OTC commoditizes high-volume APIs such as paracetamol and cetirizine.

As private-label quality converges with national brands, only clinically differentiated SKUs or dentist-endorsed franchises defend a premium. The Europe over-the-counter (OTC) Drugs market must therefore balance retailer bargaining power with sustained investment in innovation and professional education.

By Distribution Channel:

E-Pharmacy Reshapes Margin PoolsRetail pharmacies generated 61.05% of 2025 sales, protected by trusted advice and physical reimbursement workflows. Online pharmacies, although just 12-15% of the total, are scaling at 12.18% per year, propelled by Germany’s mature e-prescription rails. Hospital outlets serve inpatient needs but stay margin-thin.

The Europe over-the-counter (OTC) Drugs market size attributed to e-pharmacy will rise sharply as Spain’s 2021 liberalization and the UK’s digital health apps cultivate new buying habits. Manufacturers are tailoring web-only pack sizes and subscription bundles to secure digital shelf prominence.

Geography Analysis

Germany Over-the-Counter (OTC) Drugs Market

Germany accounted for 25.27% of 2025 revenue, underpinned by more than 19,000 community pharmacies and permissive online rules. Berlin’s 2024 decision to reimburse specific probiotics and deficiency-state vitamins has entrenched pharmacist-led counseling and elevated Germany's share of the Europe over-the-counter (OTC) drugs market.

Spain Over-the-Counter (OTC) Drugs Market

Spain, now the fastest climber, benefits from 2021 e-pharmacy legalization, rising per-capita health outlays, and pilot pharmacy service-fees that reward OTC resolution of minor ailments. Its 7.75% CAGR positions it as the star contributor to incremental gains in Europe's over-the-counter (OTC) drug market share.

Broader European Markets

The United Kingdom, France, and Italy together supply over one-third of regional revenue. Post-Brexit, the MHRA’s standalone path speeds Rx-to-OTC switches, yet divergent packaging and pharmacovigilance demands swell compliance costs. France’s strict advertising curbs and mandatory live-pharmacist digital chats restrain online uptake, while Italy’s pharmacy monopoly keeps OTC outside supermarkets. Smaller Northern and Central-Eastern markets add steady, mid-single-digit growth, with Poland’s rising disposable income and the Netherlands’ pharmacist-service fees standing out

Competitive Landscape

The European OTC arena remains moderately concentrated, historically dominated by Bayer, GSK, Johnson & Johnson, and Sanofi through their sweeping brand portfolios. Strategic shifts are reshaping that hierarchy: Sanofi plans to spin off a controlling stake in its consumer-health arm, Opella, mirroring earlier moves by Johnson & Johnson and Novartis to separate consumer assets from prescription businesses. As global majors streamline, specialized players and private-equity roll-ups are seizing niches in digestive health, dermatology, and women’s wellness.

Competition intensity varies by product class. Analgesics act as traffic drivers and face margin-squeezing price battles, whereas emerging categories such as menopause support or microbiome-focused gut health still permit premium tags. Multi-country compliance complexity dissuades small entrants; navigating language, label, and marketing rules across thirty nations requires capital and expertise. Consequently, medium-sized firms increasingly pool regulatory resources through shared services, freeing internal bandwidth for incremental formulation tweaks that keep SKUs fresh without the cost of new active ingredients.

Digital commerce introduces a second competitive axis centered on data control. Pure-play e-pharmacies capture every click, search, and reorder, selling that granular insight back to brands as retail-media placements. Manufacturers without direct consumer touchpoints must pay for banner positions to match their offline visibility, compressing margins yet further. The likely steady state is a dual model in which scientific innovation must go hand in hand with data-driven merchandising strategies, or even the most substantial historical equity may fade from search results.

Europe Over-the-Counter (OTC) Drugs Industry Leaders

Bayer AG

Reckitt Benckiser Group plc

Sanofi

GSK plc

Johnson & Johnson Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Europe Over-the-Counter (OTC) Drugs Market Companies Covered in this Report

- Angelini Pharma

- Bayer

- Boehringer Ingelheim Intl. GmbH

- Boiron SA

- Cardinal Health

- Cooper Consumer Health

- Grunenthal GmbH

- GlaxoSmithKline

- HRA Pharma

- Ipsen

- Johnson & Johnson

- MENARINI Group

- Novartis

- Omega Pharma NV

- Perrigo Company

- Pfizer

- Procter & Gamble

- Reckitt Benckiser Group

- Sanofi

- Stada Arzneimittel

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Viatris

- Walgreens Boots Alliance Inc.

Read Analysis of Europe Over-the-Counter (OTC) Drugs Companies

Recent Industry Developments in Europe Over-the-Counter (OTC) Drugs Market

- March 2026: Bayer has received new regulatory approvals for Aspirin Complex in Europe, bolstering its status as a preferred over-the-counter remedy for cold symptoms and headaches.

- December 2025: Cooper Consumer Health and Dr. Reddy’s completed the roll-out of Nicotinell nicotine-replacement therapy across France, Spain, Portugal, Belgium, and Luxembourg following the September launch in Germany and Austria.

- August 2025: IBSA extended its FilmTec orodispersible vitamin and mineral films to eight additional European markets, targeting seniors and dysphagic patients with swallow-free dosing.

- March 2025: Sirio Pharma introduced XtraGummies, a six-SKU high-strength gummy line featuring 1,800 mg creatine and 125 mg DHA options, responding to rising potency demand.

Europe Over-the-Counter (OTC) Drugs Market Report Scope and Research Methodology

Market Definition and Coverage

Our study treats Europe's over-the-counter drugs market as the revenue generated from finished pharmaceutical products cleared for sale without a doctor's prescription and intended for self-managed relief of common acute or minor chronic conditions across Germany, the United Kingdom, France, Italy, Spain, and the rest of the region. Products span simple analgesics, cough-and-cold preparations, digestive aids, dermatology creams, and vitamins or mineral supplements, provided they carry an OTC authorization in at least one European jurisdiction.

Scope exclusion: Prescription-only medicines, nutrition supplements marketed solely as foods, and veterinary formulations remain outside the frame.

Segments Covered in This Report

- By Product Type

- Cough, Cold & Flu Products

- Analgesics

- Dermatology Products

- Gastrointestinal Products

- Vitamins, Minerals & Supplements (VMS)

- Allergy & Respiratory Care

- Smoking-Cessation Aids

- Weight-Loss / Dietary Products

- Ophthalmic Products

- Sleep Aids

- Other Product Types

- By Formulation

- Tablets & Caplets

- Liquids & Syrups

- Topical Creams & Ointments

- Powders & Granules

- Sprays & Inhalers

- Gummies, Lozenges & Dissolvable Films

- By Age Group

- Pediatric (0-14 yrs)

- Adult (15-64 yrs)

- Geriatric (65+ yrs)

- By Sales Format

- Branded OTC

- Generic OTC

- Private-Label OTC

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Supermarkets & Hypermarkets

- Convenience Stores

- Other Channels

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Primary Research

We interviewed pharmacists, OTC category managers, and regulatory consultants across Western and Central Europe, then surveyed consumers to cross-check self-medication habits and online channel uptake. These insights let us refine price corridors and stress-test model assumptions.

Desk Research

We began with EMA and national medicines-agency OTC registers, Eurostat health-expenditure files, UN Comtrade shipment codes, and trade association dashboards such as AESGP to benchmark retail sell-out. Company 10-K filings, investor decks, and trusted business press supplied brand context and average selling price clues, while subscription sources like D&B Hoovers and Dow Jones Factiva enriched firm-level intelligence. This is where Mordor Intelligence's proprietary cross-country pricing tracker adds an extra layer of clarity. The sources listed are illustrative; many other public and paid references informed data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid was built. Regional demand was reconstructed from retail sales, import values, and Rx-to-OTC switch approvals, and then checked against sampled supplier roll-ups and channel feedback. According to Mordor analysts, variables such as pack-level price swings, seasonal cold-and-flu incidence, e-pharmacy penetration, disposable income, switch pipeline volume, and aging ratios carry the greatest weight. Multivariate regression, supported by scenario analysis, anchors forecasts to 2030. When channel splits were partial, missing pieces were prorated through elasticity factors derived from analogous markets.

Data Validation & Update Cycle

Our outputs pass anomaly flags, variance thresholds, and multi-step peer review before sign-off. Mordor Intelligence refreshes models annually, with interim updates whenever major recalls, tax shifts, or switch authorizations materially move the market.

How Mordor Intelligence's Europe Over-the-Counter (OTC) Drugs Market Size Compares to Other Published Estimates

Published estimates often diverge because firms pick differing product baskets, price anchors, and refresh cadences. It is through disciplined scope choices and constant dialogue with front-line stakeholders that we deliver a balanced midpoint.

Key gap drivers include the inclusion of herbal nutraceutical lines by some publishers, the omission of private-label volumes by others, and varied treatment of online mark-ups and currency conversions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 36.6 B (2025) | Mordor Intelligence | |

| USD 55.5 B (2025) | Global Consultancy A | Counts impending Rx-to-OTC switch pipeline and classifies nutraceuticals as drugs |

| USD 27.7 B (2024) | Trade Journal B | Excludes private-label brands and online pharmacy revenue |

The comparison shows that, while others lean aggressive or conservative, our carefully validated midway estimate, anchored to transparent variables and repeatable steps, offers decision-makers the most dependable baseline for strategy planning.

Key Questions Answered in the Report

How big will the Europe Over-the-Counter (OTC) Drugs market be by 2031?

It is forecast to reach USD 46.44 billion, expanding at a 4.05% CAGR from 2026-2031.

Which product segment is growing fastest?

Analgesics are projected to rise at 7.20% a year, driven by chronic joint-mobility positioning.

Why is Spain the quickest-growing geography?

Recent e-pharmacy legalization, higher health spending, and pharmacist service-fee pilots are pushing a 7.75% CAGR.

What is the main channel shift in distribution?

Online pharmacies, though still modest, are climbing 12.18% annually and reshaping margin pools.

How are delivery formats evolving?

Gummies and dissolvable films are the fastest-rising formats, growing 10.83% per year as consumers seek swallow-free options.

Who leads the competitive landscape?

Haleon maintains the largest share at about 12%, leveraging Voltaren, Sensodyne, and Centrum portfolios.

Page last updated on: