US Smart PPE Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

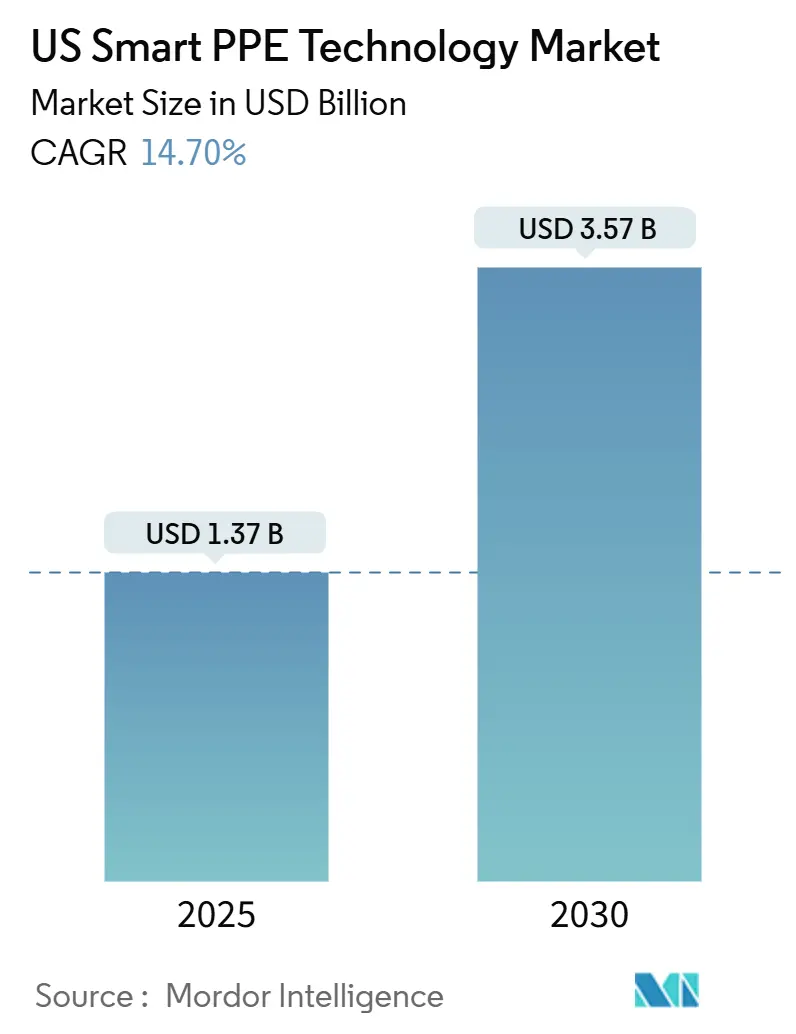

| Market Size (2025) | USD 1.37 Billion |

| Market Size (2030) | USD 3.57 Billion |

| Growth Rate (2025 - 2030) | 14.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Smart PPE Technology Market Analysis by Mordor Intelligence

The United States Smart PPE Technology market size stood at USD 1.37 billion in 2025 and is projected to reach USD 3.57 billion by 2030, registering a 14.7% CAGR. Growing regulatory scrutiny, rising fatality rates in high-risk industries, and insurance incentives are accelerating the adoption of safety solutions across construction, oil and gas, and warehousing applications. Federal infrastructure funding is stimulating demand for connected worker solutions on road and bridge projects, while Fortune 500 firms integrate wearable safety metrics into ESG reports. Rapid sensor innovation, declining hardware prices, and edge computing are driving the US Smart PPE Technology market toward predictive safety models that minimize downtime and lower workers’ compensation costs. Competitive intensity is expanding as traditional PPE leaders partner with IoT specialists, creating an ecosystem crowded with multi-vendor platforms vying for interoperability wins. South-region oil and gas operations, West-region renewable projects, and dense Northeast construction sites together keep the United States Smart PPE Technology market on a steep growth trajectory through the forecast window.

Key Report Takeaways

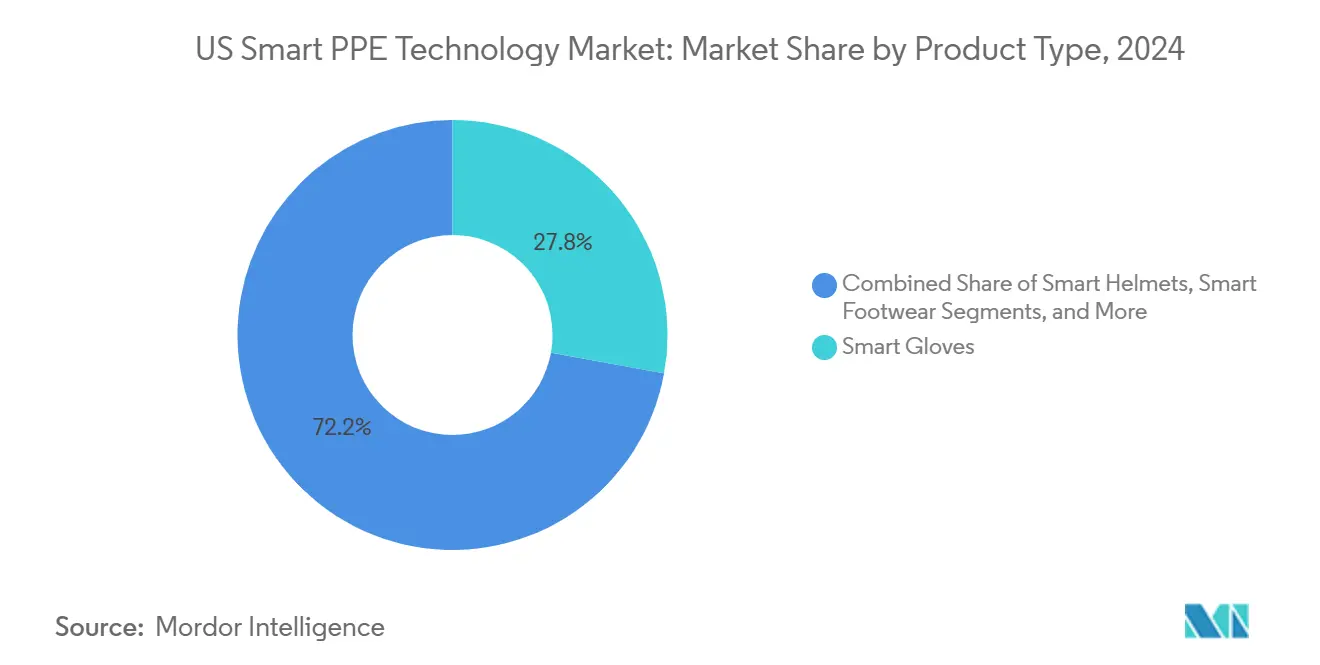

- By product category, smart gloves led with a 27.84% revenue share in 2024 in the US Smart PPE Technology market, while smart helmets are forecast to expand at a 15.22% CAGR through 2030.

- By sensor type, proximity and motion sensors accounted for a 30.83% share of the US Smart PPE Technology market size in 2024 and biometric sensors are advancing at a 15.44% CAGR to 2030.

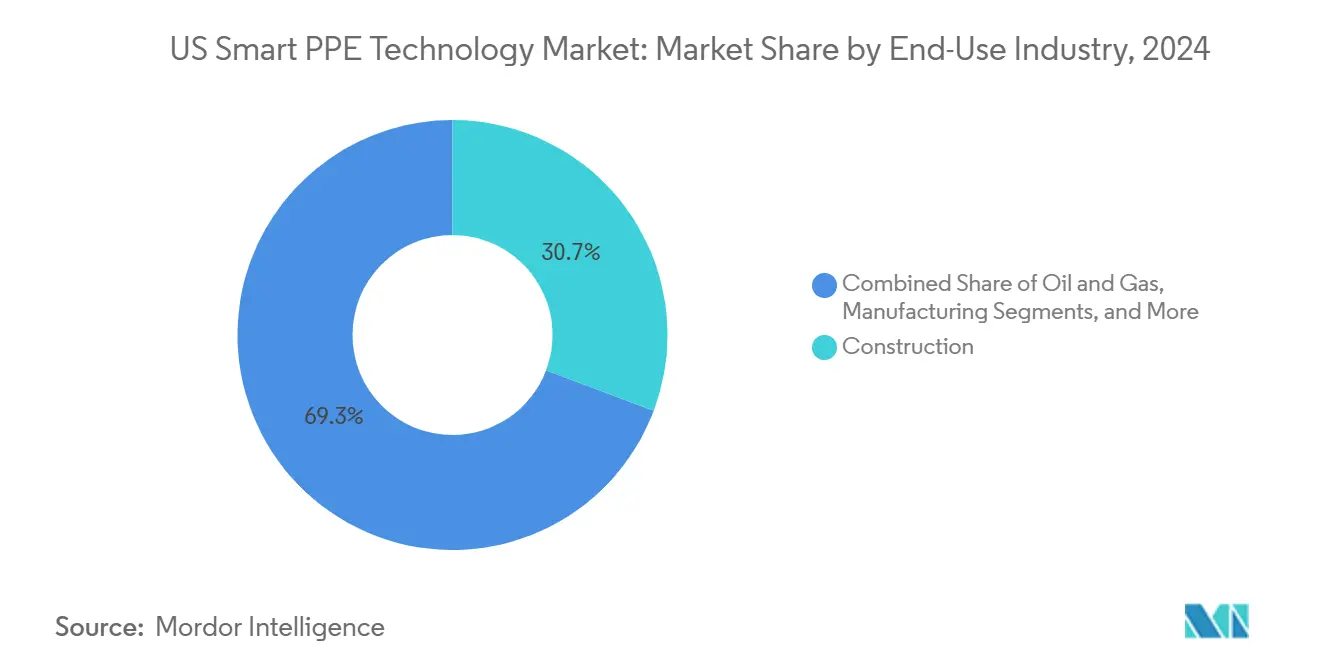

- By end-use industry, construction commanded 30.73% of the US Smart PPE Technology market share in 2024, whereas warehousing and logistics is rising at a 15.47% CAGR through 2030.

- By distribution channel, direct B2B sales retained 43.84% share in 2024 in the US Smart PPE Technology market, yet e-commerce platforms are climbing at a 15.88% CAGR as digitized procurement gains favor.

US Smart PPE Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OSHA emphasis on connected-worker safety compliance | +3.2% | National, concentrated in high-risk states | Medium term (2-4 years) |

| Rising workplace fatalities in construction and oil/gas | +2.8% | South and West regions primarily | Short term (≤ 2 years) |

| Integration of IoT and AI enabling real-time hazard alerts | +3.5% | Global, early adoption in tech-forward states | Long term (≥ 4 years) |

| Insurance premium discounts for smart-PPE adopters | +2.1% | National, varies by state regulations | Medium term (2-4 years) |

| ESG reporting push for wearable safety metrics | +1.8% | National, Fortune 500 concentration | Long term (≥ 4 years) |

| Federal infrastructure stimulus for road and bridge projects | +1.4% | Northeast and Midwest corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OSHA Emphasis on Connected-Worker Safety Compliance

OSHA’s 2025 electronic injury-reporting mandate moves compliance from paper to digital, steering firms toward smart PPE that automates data capture.[1]Occupational Safety and Health Administration, “Electronic Injury Reporting Requirements,” osha.gov Third-party representatives now join inspections, so employers deploy wearable monitoring to pre-empt violations. Construction crews on federally funded projects adopt temperature-sensing wearables to satisfy new heat-injury standards, while contractors facing penalty risks view connected PPE as essential, not optional. The rule’s reach across heavy industry makes the US Smart PPE Technology market a primary channel for meeting compliance obligations.

Rising Workplace Fatalities in Construction and Oil/Gas

Construction deaths totaled 1,069 in 2022, more than one-fifth of all US workplace fatalities, and oil and gas extraction posted a fatality rate 6.8 times above the national average.[2]Bureau of Labor Statistics, “Census of Fatal Occupational Injuries 2022,” bls.gov Falls and struck-by incidents dominate incident logs, encouraging widespread use of smart helmets, proximity sensors, and gas detection wearables. Eighty-four percent of construction firms intend to invest in connected PPE by 2026, illustrating that prevention motives complement regulation.[3]National Safety Council, “Work to Zero Adoption Survey,” nsc.org These dynamics keep the US Smart PPE Technology market entrenched in capital-project budgets despite broader macro volatility.

Integration of IoT and AI Enabling Real-Time Hazard Alerts

Edge-enabled IoT nodes process sensor data in milliseconds, granting frontline workers instant alerts without cloud latency. Machine learning predicts heat stress and fatigue by correlating biometric streams, pushing safety strategies from reactive to predictive. Chevron’s roll-out of connected hydration patches validates real-world efficacy and demonstrates how AI converts sensor feeds into actionable insights. The outcome is a data-rich US Smart PPE Technology market poised to overlay analytics onto every high-risk task.

Insurance Premium Discounts for Smart-PPE Adopters

Workers’ compensation carriers now offer 5%–15% premium reductions when employers furnish verified connected PPE programs. Dynamic risk-scoring platforms adjust premiums in real time, turning safety investment into a cash-flow benefit rather than a compliance cost. This mechanism underwrites a portion of smart PPE budgets, letting CFOs connect capital outlays to insurance savings. As more underwriters embed IoT data into actuarial models, the US Smart PPE Technology market gains a durable financial catalyst.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device costs | -2.3% | National, acute in SME segments | Short term (≤ 2 years) |

| Data-privacy and cyber-security concerns | -1.7% | National, varies by industry sector | Medium term (2-4 years) |

| Limited battery life and reliability issues | -1.4% | Global, extreme environment focus | Medium term (2-4 years) |

| Interoperability gaps in multi-vendor ecosystems | -1.1% | National, enterprise deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device Costs

Smart helmets priced near USD 1,000 outstrip conventional units by a tenfold margin, limiting uptake among small contractors. Total cost of ownership balloons with software fees and data services, extending payback periods to 18–36 months. Rental subscriptions from United Rentals soften the blow and keep equipment current, but price sensitivity remains a hurdle for the lower half of the addressable base. Hardware cost declines are moderating the barrier, yet price parity with standard PPE stays outside the short-term horizon.

Data-Privacy and Cyber-Security Concerns

Biometric streams such as heart rate, motion data, and location tracking invite surveillance fears among unionized workforces.[4]National Institute of Standards and Technology, “Cybersecurity Framework for IoT,” nist.gov IoT devices add attack surfaces that adversaries could leverage to halt operations or exfiltrate IP. Early adopters deploy zero-trust architectures and on-device processing to restrict cloud exposure, but compliance with emerging state-level data-protection laws raises deployment complexity. For now, privacy anxiety tempers adoption speed in sensitive industries such as defense and pharmaceuticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Gloves Anchor Early Momentum

Smart gloves held a 27.84% share of the US Smart PPE Technology market size in 2024, positioning the category as the backbone of manufacturing and construction deployments. Robust sensor arrays inside gloves issue vibration alerts yet preserve dexterity, which drives immediate safety ROI for hand-intensive tasks.

Further growth will lean on smart helmet adoption, advancing at a 15.22% CAGR as firms seek multi-sensor coverage from a single wearable. Smart suits, glasses, footwear, and respirators fill niche hazards such as chemical exposure and airborne contaminants, but consolidated form factors will likely dominate procurement cycles. Device makers now embed thermal, gas, and proximity sensors in one shell, which trims device counts, minimizes user fatigue, and sustains the larger US Smart PPE Technology market.

By Sensor Type: Proximity Modules Guard Congested Sites

Proximity and motion sensors led with 30.83% share of the US Smart PPE Technology market in 2024, protecting workers from strikes and vehicle collisions on busy job sites. Real-time geofencing creates dynamic buffer zones, halting equipment before impact.

Biometric sensor demand is surging at a 15.44% CAGR, propelled by corporate wellness KPIs and heat-stress mandates. Gas, chemical, temperature, and pressure sensors diversify product lines for oil and gas, mining, and fire service scenarios. Multi-sensor fusion minimizes false alarms, reinforcing trust and ensuring the US Smart PPE Technology market keeps progressing from single-function devices toward holistic safety networks.

By End-Use Industry: Construction Tops, Logistics Accelerates

Construction captured 30.73% of 2024 demand after OSHA intensified fall-protection enforcement on federal projects. High-rise and infrastructure contractors require location tracking, fall detection, and high-heat alarms on one platform.

Warehousing and logistics shows the fastest pace at 15.47% CAGR, fueled by e-commerce throughput targets and co-bot operations. Oil and gas firms emphasize explosive atmosphere certification, while manufacturing plants embed ergonomics analytics into lean programs. Healthcare and first responder verticals apply infection control and situational tracking, keeping the US Smart PPE Technology market diversified across economic cycles.

By Distribution Channel: Direct Sales Prevail in Complex Rollouts

Direct B2B channels seized 43.84% share in 2024 because enterprise buyers favor vendor engineering support for integrations and training. National distributors supply blended carts of standard and smart PPE, answering day-to-day replenishment needs.

E-commerce’s 15.88% CAGR growth demonstrates that buyers now pilot connected equipment in small lots before enterprise scale-up. Specialized integrators bundle wearables, analytics platforms, and change-management services, carving out a consulting-oriented niche inside the growing US Smart PPE Technology market.

Geography Analysis

The South leads shipments, driven by Texas-centered oil and gas projects that call for intrinsically safe wearables suited to explosive atmospheres. State heat-stress rules encourage temperature-sensor adoption, and population growth keeps construction pipelines active. Edge-connected smart helmets thus see steady repeat orders, reinforcing the broader US Smart PPE Technology market.

The West is expanding quickly on the back of solar and wind farm construction across California, Arizona, and Nevada, where workers spread across remote sites depend on 5G-backed location tracking. California’s stringent Cal/OSHA code accelerates real-time monitoring mandates, while Silicon Valley venture funding nurtures home-grown startups that enrich local supply chains and shorten innovation cycles.

Northeast and Midwest corridors absorb federal infrastructure outlays earmarked for bridge rehabilitation and rail modernization. Dense urban projects require proximity detection to manage multi-contractor zones, and Midwest manufacturing plants integrate ergonomic wearables to support robot collaboration. Established insurance ecosystems in both regions boost premium-discount programs, securing consistent expansion for the overall US Smart PPE Technology market.

Competitive Landscape

The competitive arena blends legacy PPE giants and agile IoT entrants, leaving the field moderately fragmented. Honeywell, 3M, and MSA Safety retrofit connectivity into trusted product lines, granting them distribution reach and brand equity. Smaller players such as Jarsh Safety and StrongArm Technologies carve footholds with AI-enabled cooling helmets and ergonomic sensors that solve niche pain points.

Strategic alliances define go-to-market playbooks. Honeywell’s software-as-a-service suite links third-party sensors, while MSA Safety’s edge gateway ingests multi-vendor data for centralized dashboards. Telecom providers like Verizon supply private 5G to bridge device and cloud layers, embedding network services into the US Smart PPE Technology market value chain.

Differentiation tilts toward power management, sensor precision, and data analytics. Firms race to achieve one-day battery life with continuous streaming and to offer API-ready platforms for enterprise safety software. As procurement teams pivot to platform standardization, vendors that prove interoperability and lower total cost of ownership will consolidate share in the US Smart PPE Technology market.

US Smart PPE Technology Industry Leaders

Honeywell International Inc.

3M Company

MSA Safety Incorporated

Ansell Limited

Vuzix Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Guardio released Quin Armet PRO, a smart helmet with integrated comms, environmental sensing, and impact detection for construction workers.

- October 2024: Innovative Eyewear rolled out ANSI Z87.1 smart glasses enabling hands-free data overlays during industrial inspections.

- September 2024: Chevron scaled Epicore Biosystems’ hydration patches across refineries to curb heat stress risk.

- August 2024: i.safe MOBILE and RealWear co-developed Navigator Z1, an intrinsically safe wearable computer for explosive zones.

US Smart PPE Technology Market Report Scope

| Smart Helmets |

| Smart Glasses and Face Shields |

| Smart Protective Clothing and Suits |

| Smart Gloves |

| Smart Footwear |

| Smart Respirators |

| Temperature Sensors |

| Proximity and Motion Sensors |

| Gas and Chemical Sensors |

| Pressure Sensors |

| Location and Environmental Sensors |

| Biometric and Health Monitoring Sensors |

| Construction |

| Oil and Gas |

| Manufacturing |

| Mining |

| Healthcare |

| Firefighting and First Responders |

| Utilities and Energy |

| Warehousing and Logistics |

| Other End-Use Industries |

| Direct Sales (B2B) |

| Industrial Distributors |

| E-commerce Platforms |

| Safety Equipment Integrators |

| By Product Type | Smart Helmets |

| Smart Glasses and Face Shields | |

| Smart Protective Clothing and Suits | |

| Smart Gloves | |

| Smart Footwear | |

| Smart Respirators | |

| By Sensor Type | Temperature Sensors |

| Proximity and Motion Sensors | |

| Gas and Chemical Sensors | |

| Pressure Sensors | |

| Location and Environmental Sensors | |

| Biometric and Health Monitoring Sensors | |

| By End-Use Industry | Construction |

| Oil and Gas | |

| Manufacturing | |

| Mining | |

| Healthcare | |

| Firefighting and First Responders | |

| Utilities and Energy | |

| Warehousing and Logistics | |

| Other End-Use Industries | |

| By Distribution Channel | Direct Sales (B2B) |

| Industrial Distributors | |

| E-commerce Platforms | |

| Safety Equipment Integrators |

Key Questions Answered in the Report

How large is the U.S. Smart PPE Technology market in 2025?

The US Smart PPE Technology market size is USD 1.37 billion in 2025.

What growth rate is expected through 2030?

The market is forecast to post a 14.7% CAGR and reach USD 3.57 billion by 2030.

Which product category currently dominates purchases?

Smart gloves command the leading share at 27.84% of 2024 revenue.

Which connectivity option is most common in industrial settings?

Bluetooth Low Energy holds 31.73% share thanks to its low-power mesh capability.

Which end-use sector is growing fastest?

Warehousing and logistics is advancing at a 15.47% CAGR as e-commerce expands.

Page last updated on: