Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 309.72 Billion |

| Market Size (2031) | USD 401.21 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Facade Market Analysis by Mordor Intelligence

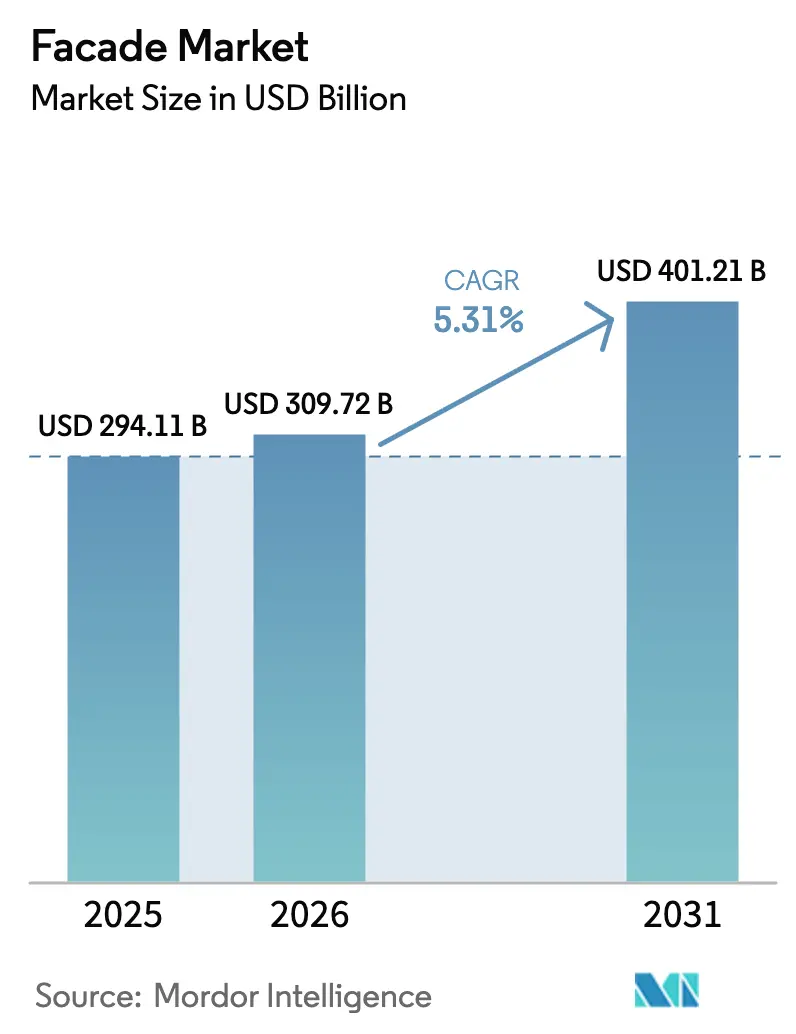

The Facade Market size is projected to expand from USD 294.11 billion in 2025 and USD 309.72 billion in 2026 to USD 401.21 billion by 2031, registering a CAGR of 5.31% between 2026 to 2031.

Accelerating urbanization, stricter energy codes, and the shift toward factory-built envelope solutions are reinforcing demand as developers seek faster project delivery and better thermal, acoustic, and fire performance. High-rise pipelines in Asia-Pacific and the Middle East continue to specify premium curtain walls, while North American and European owners replace aging cladding to comply with zero-carbon targets. Volatility in aluminum and float-glass costs compressed contractor margins during 2025, yet price-adjustment clauses and procurement hedges are helping stabilize bid activity. At the same time, suppliers with in-house testing facilities are gaining an advantage as jurisdictions broaden NFPA 285 and similar fire-test mandates.

Key Report Takeaways

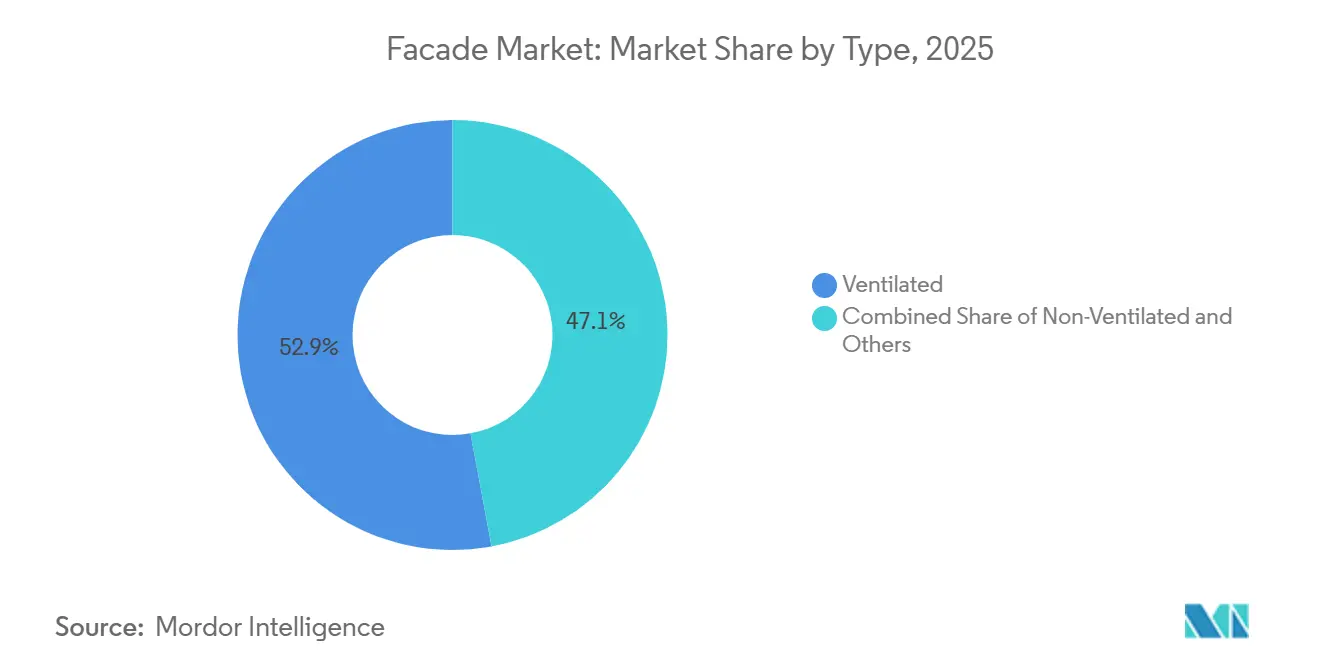

- By type, ventilated facades accounted for 52.9% of the facade market in 2025 and are projected to grow at a 5.98% CAGR through 2031.

- By facade system, curtain walls accounted for 41.6% of the facade market in 2025, while rainscreen cladding is forecast to expand at a 6.08% CAGR through 2031.

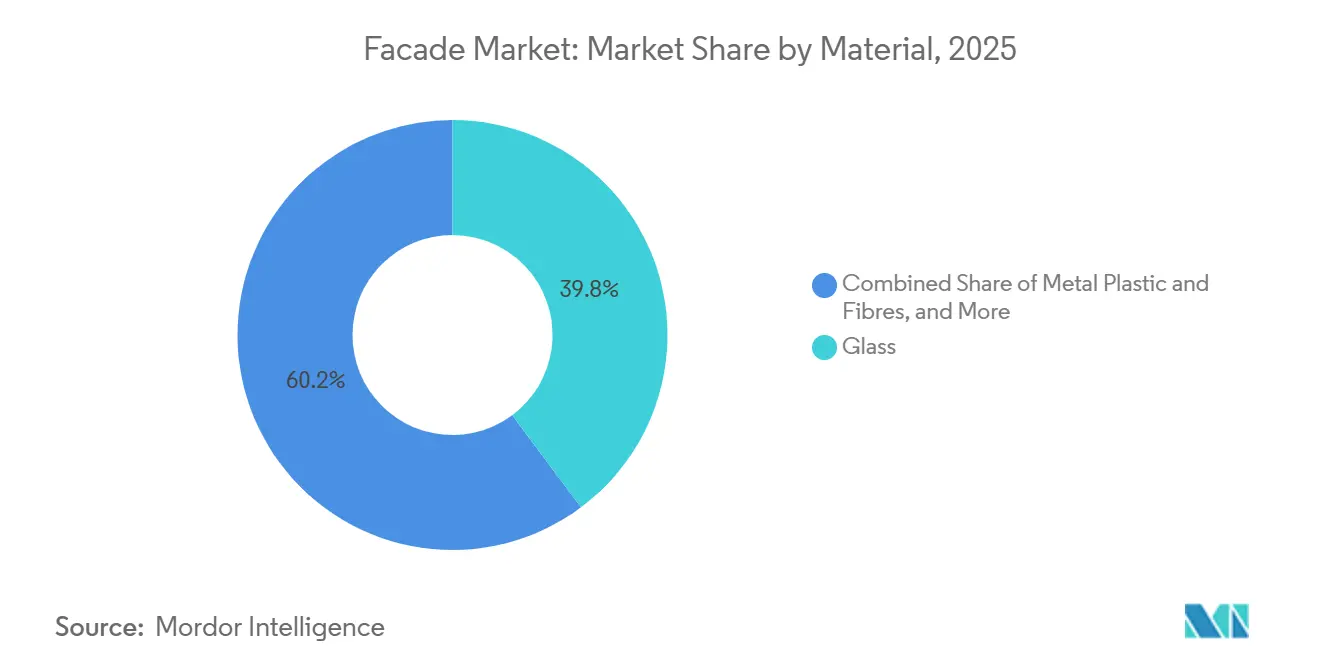

- By material, glass accounted for 39.8% of the facade market in 2025 and is projected to grow at a 5.90% CAGR through 2031.

- By installation mode, new construction accounted for 64.2% of the facade market in 2025; retrofit installations are advancing at a 6.29% CAGR through 2031.

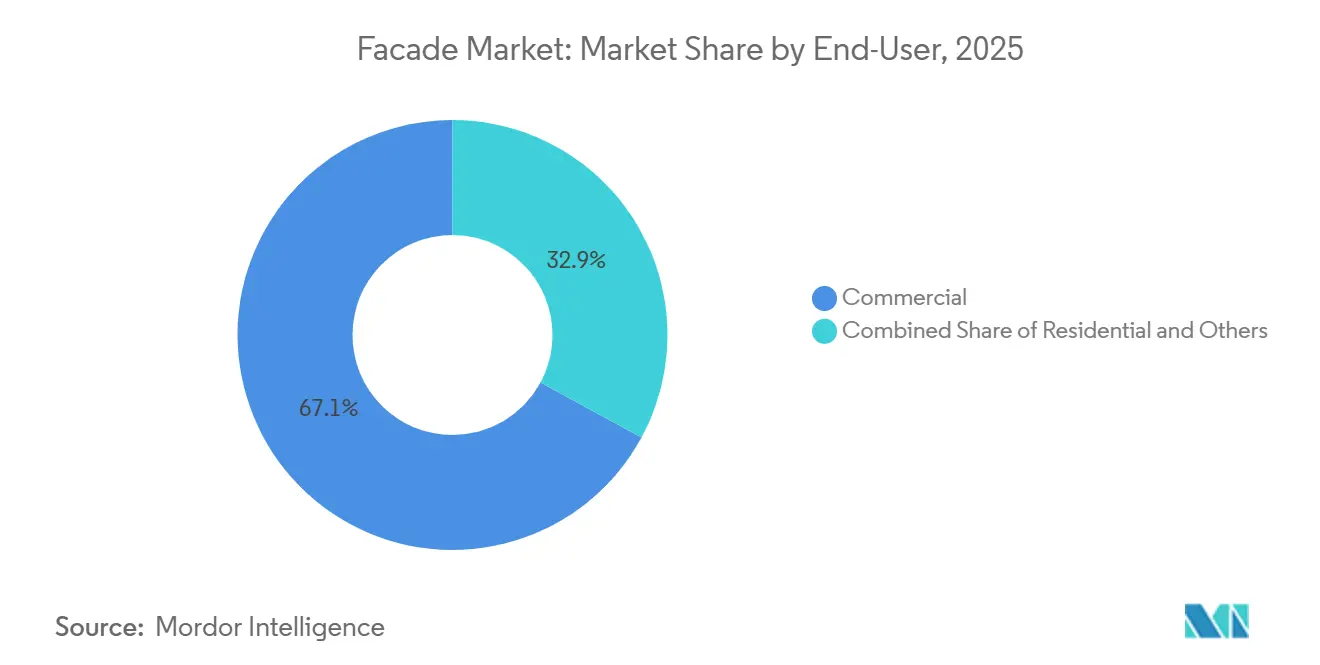

- By end user, the commercial segment held 67.1% of the facade market share in 2025, whereas residential projects are set to grow at a 6.18% CAGR through 2031.

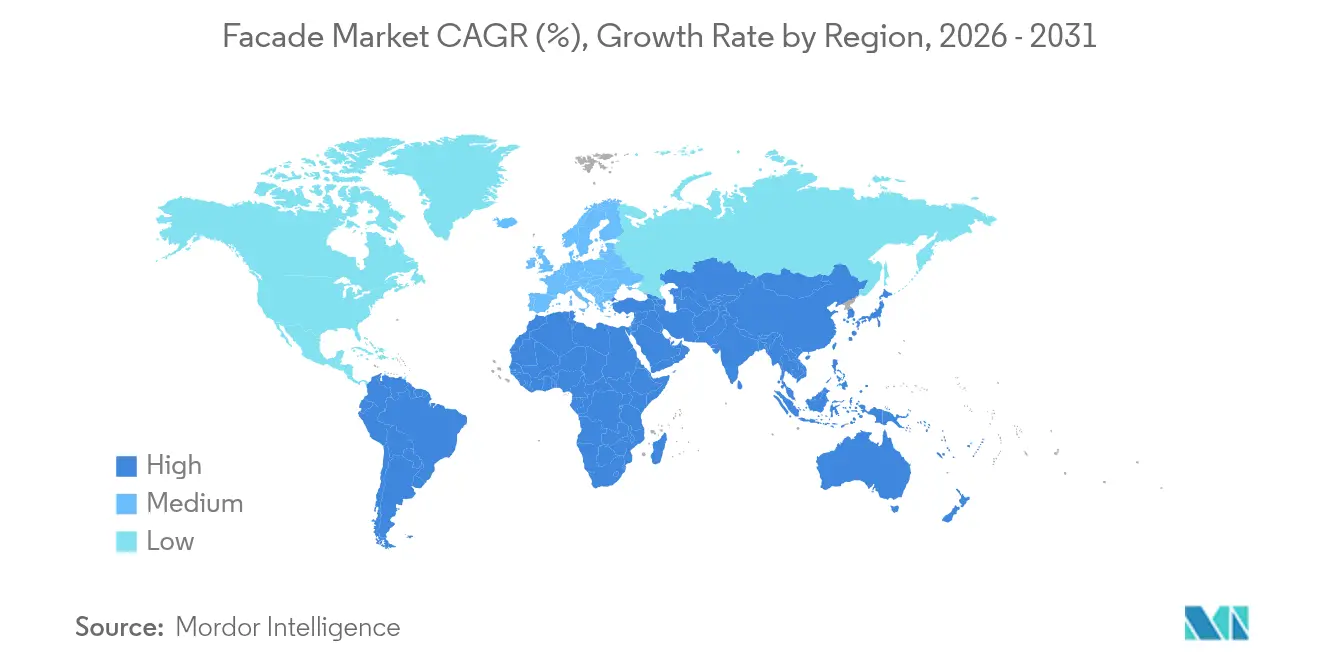

- By geography, Asia-Pacific accounted for 38.5% of the facade market share in 2025, but the Middle East and Africa region is expected to register the fastest CAGR of 6.48% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Facade Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Code-driven demand for non-combustible and fire-rated façade assemblies | +1.10% | North America, Europe, Australasia | Short term (≤ 2 years) |

| Increasing retrofit of aging buildings with insulated overcladding | +1.00% | North America, Europe, Developed Asia-Pacific | Long term (≥ 4 years) |

| Large-scale mixed-use and high-rise projects requiring premium curtain wall systems | +0.90% | Asia-Pacific, Middle East | Medium term (2–4 years) |

| Rising use of unitized systems to shorten construction schedules | +0.80% | North America, Western Europe | Medium term (2–4 years) |

| Higher adoption of high-performance glass for thermal and solar control | +0.70% | Middle East, Tropical Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Code-Driven Demand for Non-Combustible and Fire-Rated Facade Assemblies

Cladding-fire incidents have triggered rapid code escalation. The 2024 International Building Code now applies NFPA 285 to many mid-rise projects, New York City mandates cavity barriers at every floor, and the United Kingdom bans combustible materials above 18 m. Australia introduced a deemed-to-satisfy route for non-combustible façades, but performance-based options now face longer reviews. These overlapping rules lengthen approval cycles yet push demand toward suppliers with certified mineral-core panels and in-house test rigs. For newcomers, the testing expense can exceed USD 150,000 per configuration, creating high barriers to entry.

Increasing Retrofit of Aging Buildings with Insulated Overcladding

North American and European building owners are racing to meet decarbonization targets without displacing tenants. U.S. Department of Energy studies show that adding 100 mm of mineral wool overcladding can cut heating loads by 35-50% in single-pane buildings[1]U.S. Department of Energy, “Insulated Overcladding Guide,” energy.gov. Toronto’s Tower Renewal retrofits reduced energy use by 120 kWh/m² yearly across 12 multi-family blocks. Germany earmarked USD 2.7 billion in 2025 for façade upgrades that bundle insulation with fire-rated panels, while the United Kingdom’s Social Housing Decarbonisation Fund imposes non-combustibility rules on every publicly financed retrofit. Specialized contractors using modular scaffolds and prefabricated panels are capturing this high-growth niche.

Large-Scale Mixed-Use and High-Rise Projects Requiring Premium Curtain Wall Systems

Supertall towers in New York, Chongqing, Dubai, and Riyadh continue to favor unitized curtain walls that compress enclosure schedules and deliver column-free interiors. JPMorgan Chase’s 270 Park Avenue used 90,000 m² of panels to meet a 42-month program, while Chongqing International Land-Sea Center paired photovoltaic spandrels with glass to cut grid demand by 18%. Updated energy codes in the Gulf now cap envelope transmittance at 1.2 W/m²·K, driving the adoption of triple-glazed and thermally broken frames. The global pipeline of buildings over 200 m hit 147 in 2025, sustaining demand for high-spec facades. Developers view premium envelopes as a lease-up differentiator that justifies higher fit-out rents even amid commodity price swings.

Rising Use of Unitized Systems to Shorten Construction Schedules

Factory-assembled façade units trim on-site labor by up to 40% and mitigate weather delays, an advantage in tight labor markets such as Chicago and London. The 400 Lake Shore Drive tower sourced panels from a plant 200 km away and avoided winter stoppages entirely, demonstrating the scheduling upside. Prefabrication also raises quality via water testing before shipment and reduces callbacks. Developers in Singapore now require unitized envelopes for projects with timelines of 30 months or less, balancing an 8-12% cost premium with earlier revenue recognition. Investment in automated lines, such as Permasteelisa’s 25,000 m² Suzhou plant, shows how scale players are industrializing curtain-wall production.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in aluminum, glass, and coating input costs | -0.6% | Global | Short term (≤ 2 years) |

| Lengthy approval and testing cycles for facade materials | -0.4% | North America, Europe, Australasia | Medium term (2–4 years) |

| Capacity constraints for custom and high-spec components | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Aluminum, Glass, and Coating Input Costs

Primary aluminum futures fluctuated between USD 2,280 and USD 2,610 per metric ton in 2025 as Chinese hydropower shortages and European smelter closures squeezed supply. Soda-ash and natural-gas cost spikes lifted float-glass production expenses, while semiconductor-grade target scarcity lengthened low-E coating lead times. Mid-tier fabricators lacking hedges saw fixed-price contracts turn loss-making and invoked force-majeure clauses on several U.S. projects. Developers now add price-adjustment clauses indexed to commodity benchmarks, but that dampens competitive tension at tender.

Lengthy Approval and Testing Cycles for Facade Materials

An NFPA 285 test costs up to USD 150,000 and must be repeated for any material change, adding 12-18 months to launch times[2]National Fire Protection Association, “NFPA 285 Cost Estimates,” nfpa.org. European Technical Assessments average 14 months, while Australia’s CodeMark program has a testing backlog that slows the testing of novel hybrid systems. These lags deter incremental innovation; most suppliers fall back on standard “platform” assemblies rather than optimizing performance per project. Smaller firms without regulatory teams find entry prohibitive, effectively ceding share to incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ventilated Facades Anchor Demand in Humid Climates

Ventilated systems captured 52.9% of the facade market share in 2025, reflecting their ability to remove vapor from the wall and protect against interstitial condensation in monsoon and mixed-humid zones. Adoption is projected to rise at a 5.98% CAGR as India’s tier-2 cities embed cavity ventilation into local green codes. Regulators are reinforcing uptake: Germany’s Energy Saving Ordinance grants a 0.05 W/m²·K credit for ventilated rainscreens, and several U.S. coastal states now favor back-ventilated terracotta for hurricane resilience. Prefabricated ventilated panels integrate insulation, cavity, and cladding into a single module, reducing site labor and quality risk. As unit volumes scale, cost premiums versus sealed assemblies are narrowing, encouraging wider deployment across mid-rise residential and healthcare projects.

While non-ventilated façades remain common in arid low-rise builds, pressure-equalized hybrids are emerging that marry moisture drainage with slim cavity depths. Value engineering sometimes removes ventilation, yet long-term maintenance data show higher moisture-related failures in sealed systems, prompting insurers to favor ventilated designs. Major suppliers such as Kingspan and Rockwool now bundle fire-rated mineral-wool insulation with ventilated cladding, giving specifiers a single-source option that satisfies thermal, moisture, and combustion criteria[3]. As climate zones migrate poleward, the addressable base for ventilated envelopes is expected to widen further, sustaining their leadership in the facade market.

By Facade System: Curtain Walls Retain the Lead, Rainscreen Accelerates Retrofits

Curtain walls held 41.6% of the facade market share in 2025, owing to their dominance in Grade-A office towers and luxury hotels, where large sightlines and quick dry-in are critical[3]American Institute of Architects, “Facade Systems Market Tracker,” aia.org. Unitized variants are now standard for projects above 25 stories in Asia-Pacific, North America, and the Gulf, helping contractors shave months off schedules. Continuous R&D delivers slimmer mullions and integrated PV spandrels that improve energy performance without aesthetic compromise. Fabricators with automated lines, such as Schüco’s new FWS 35 PD.HI, report lead-time reductions of 15-20% compared with stick-built curtain walls.

Rainscreen cladding is forecast to be the fastest-growing system, with a 6.08% CAGR through 2031, on the back of deep-energy retrofits. Its decoupled cladding layer simplifies overcladding of occupied buildings, avoids structural load penalties, and accommodates thermal movement. Public subsidies in Germany and the U.K. prioritize mineral-wool-backed rainscreen panels for carbon and fire compliance, accelerating volume. Boutique fabricators are exploiting computational design to deliver parametric rainscreens that differentiate office leases in competitive metros. Fire-testing obligations remain a constraint for combustible cores, yet adoption of mineral-core aluminum and fiber-cement is removing that hurdle and keeping rainscreen trajectory intact.

By Material: Glass Maintains a Clear Edge

Glass accounted for 39.8% of the facade market in 2025 and is projected to compound at 5.90% as coating technology balances daylight, glare, and energy efficiency. Triple-silver low-E and dynamic electrochromic units drive performance gains; Saint-Gobain’s 2025 line in Poland produces IGUs with 0.28 W/m²·K U-values for the European retrofit wave. surpassed 1 million m² of smart glass deployments, highlighting occupant comfort as a pull factor. Developers in the Middle East and Texas cite HVAC downsizing of up to 20% when combining high-performance glazing with reflective coatings.

Metal cladding is diversifying beyond aluminum as owners seek lower embodied carbon and distinctive finishes. Recycled-content aluminum profiles, zinc, and weathering steel offer favorable life-cycle costs and patina aesthetics. Norsk Hydro’s Reduxa range logs a 4.2 kg CO₂-eq/kg footprint, half the industry average, helping projects achieve LEED and BREEAM credits. Fiber-cement and phenolic resin panels are growing in residential towers where fire codes prohibit combustible cores, while stone veneer retains a niche in heritage refurbishments thanks to new thin-slab technologies that cut weight. Together, these trends ensure material diversification even as glass keeps its numeric lead in the facade market.

By Installation: New Construction Dominates, Retrofit Expands Fastest

New builds accounted for 64.2% of the facade market size in 2025, driven by greenfield urban projects across Asia-Pacific and the Gulf. High-rise pipelines in Riyadh, Shenzhen, and Mumbai sustain demand for curtain walls and unitized panels that speed delivery. Contractors favor prefabricated façades to offset skilled-labor gaps and avoid weather delays, as illustrated by Enclos Corp.’s year-round fabrication for Chicago’s 400 Lake Shore Drive. Government energy codes increasingly specify envelope performance targets from the outset, embedding high-performance façades in base designs.

Renovation and retrofit installations are the fastest-growing track at a 6.29% CAGR. Overcladding allows owners to meet net-zero roadmaps without full tenant decant and shields aging stock from fire-safety liabilities. U.S. DOE research confirmed 35-50% heating-load cuts with mineral-wool overcladding, while Germany’s USD 2.7 billion subsidy accelerates similar upgrades. Prefabricated retrofit kits, often hoisted into place via mast climbers, minimize site disruption and compress project timelines. Suppliers that can bundle engineering, panels, and installation support are positioning to capture this profitable growth pocket of the facade market.

By End-User: Commercial Still Rules, Residential Steps Up

Commercial properties held 67.1% of the facade market share in 2025, reflecting continued investment in expressive glass skins for offices, retail, and hospitality. Trophy towers in Shanghai, London, and Dubai specify integrated PV spandrels, smart glass, and operable vents that boost tenant attraction and command premium rents. Recent U.S. Urban Land Institute surveys show 42% of developers incorporating electrochromic glazing in at least one 2025 project to enhance comfort and ESG scores. Industrial users are less visible but specify insulated metal panels with low infiltration rates for cold storage and pharma plants.

Residential façades are projected to post a 6.18% CAGR, supported by urban multi-family demand and unitized panel adoption that tempers labor shortages. Singapore, Hong Kong, and Toronto now require fast-track delivery, pushing developers toward factory-finished envelope modules despite higher upfront cost. Fire codes banning combustible cladding above 18 m in the U.K., Australia, and multiple U.S. states are steering residential towers toward mineral-core aluminum and fiber-cement rainscreens. As green mortgage programs tie financing to energy performance, high-spec façades are becoming a differentiator in competitive rental markets, reinforcing residential momentum in the global facade market.

Geography Analysis

Asia-Pacific supplied 38.5% of the facade market share in 2025, propelled by China’s urban-core redevelopment and India’s Smart Cities Mission. Even with China’s residential slowdown, Shenzhen and Shanghai office and mixed-use towers kept curtain-wall demand buoyant. India shows a dual-speed profile: Grade-A offices in Mumbai install premium glazing, while tier-2 municipalities adopt ventilated rainscreens to tackle monsoon humidity under the Energy Conservation Building Code. Japan’s Tokyo Metropolitan Government plans to retrofit 30% of pre-2000 offices by 2030, stimulating orders for insulated overcladding, and South Korea’s G-SEED program grants envelope credits for U-values below 0.8 W/m²·K, pushing advanced glazing uptake.

North America and Europe remain sizable but more mature. The United States expanded NFPA 285 triggers to structures as low as 12 m, prompting façade replacements across mid-rise hotels and apartments. Toronto’s Tower Renewal projects illustrate Canada’s retrofit orientation, while Germany’s USD 2.7 billion subsidy accelerates rainscreen adoption with continuous mineral-wool insulation. The United Kingdom’s ban on combustible cladding above 18 m is reshaping material choices toward mineral-core aluminum and stone wool panels. France and Spain pilot circular take-back programs for glass and aluminum that align with EU recycling targets, underscoring a pivot to life-cycle stewardship.

The Middle East and Africa region is forecast to grow the fastest at a 6.48% CAGR through 2031. Saudi Arabia’s Vision 2030 megaprojects, including NEOM, specify PV-integrated curtain walls and strict 1.2 W/m²·K transmittance caps. Dubai continues to showcase computational-design façades such as the Museum of the Future, signaling appetite for parametric skins. South Africa’s Green Building Council reports a 22% rise in facade-related credits, driven by commercial developers pursuing tenant differentiation. Latin America lags as tariffs and weak currencies elevate import costs, yet Brazil and Mexico still import high-performance glass and aluminum for landmark mixed-use towers. Across these geographies, suppliers capable of navigating diverse codes and logistics stand to consolidate share in the global facade market.

Competitive Landscape

Competition is moderate, with global envelope specialists—Permasteelisa, Schüco, Enclos—competing against vertically integrated materials giants such as Saint-Gobain, Kingspan, and AGC Glass. Scale players leverage in-house extrusion, coating, and testing to capture margin and assure compliance as codes tighten. Patent filings reveal strategic bets on phase-change glazing and PV spandrels, indicating a focus on energy-positive façades that bolster tenant ESG credentials.

Regional fabricators carve profitable niches in bespoke geometries and rapid prototyping. Partnerships with computational-design firms enable parametric panels that legacy production lines struggle to replicate, granting boutique players premium margins on signature towers in Dubai, Kuala Lumpur, and Miami. Yet capacity constraints in jumbo-lite processing and custom extrusion often force these specialists to ally with multinational glass or aluminum groups for critical inputs, reinforcing a web of co-opetition within the facade market.

M&A remains selective due to project-based revenues and differing local codes, but targeted acquisitions are rising. Kingspan’s 60% stake in a Guangdong insulated-panel maker secures a foothold in the Pearl River Delta, while Saint-Gobain’s capacity addition in Poland readies it for Europe’s retrofit surge. Automation investments, such as Permasteelisa’s Suzhou robotics line, and Norsk Hydro’s renewable-powered extrusion joint venture, show how leaders aim to lower cost, cut carbon, and lock in technical advantage as the facade industry pivots to performance-driven specifications.

Facade Industry Leaders

Saint-Gobain S.A

Permasteelisa S.p.A

Kingspan Group

Schüco International KG

Enclos Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Saint-Gobain committed USD 195 million to add a triple-silver low-E sputtering line in Poland, targeting Europe’s deep-retrofit demand .

- December 2025: Kingspan bought 60% of a Guangdong insulated-panel maker to localize fire-rated façade production for China’s GB 8624 code.

- November 2025: Permasteelisa landed a USD 240 million unitized curtain-wall contract for a 92-story Kuala Lumpur tower featuring electrochromic glass and PV spandrels.

- October 2025: Schüco unveiled its FWS 35 PD.HI unitized system with a 0.79 W/m²·K frame Uf-value, targeting labor-scarce Western markets.

Global Facade Market Report Scope

By Type

| Ventilated |

| Non-Ventilated |

| Other Types |

By Façade System Type

| Rainscreen Cladding |

| Curtain Wall Systems |

| Others |

By Material

| Glass |

| Metal |

| Plastic & Fibres |

| Stones |

| Other Materials |

By Installation

| New Construction |

| Renovation & Retrofit |

By End-User

| Commercial |

| Residential |

| Other End-Users |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific |

| By Type | Ventilated | |

| Non-Ventilated | ||

| Other Types | ||

| By Façade System Type | Rainscreen Cladding | |

| Curtain Wall Systems | ||

| Others | ||

| By Material | Glass | |

| Metal | ||

| Plastic & Fibres | ||

| Stones | ||

| Other Materials | ||

| By Installation | New Construction | |

| Renovation & Retrofit | ||

| By End-User | Commercial | |

| Residential | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the facade market today and how fast is it growing?

The facade market size reached USD 309.72 billion in 2026 and is projected to achieve USD 401.21 billion by 2031, advancing at a 5.31% CAGR over 2026-2031.

Which facade system is gaining ground the quickest?

Rainscreen cladding is the fastest-growing system, expected to expand at a 6.08% CAGR as it dominates deep-energy retrofit projects needing mineral-wool insulation and non-combustibility.

What factors most influence facade specification decisions in new high-rise towers?

Developers prioritize construction speed, code compliance, and energy performance, which is why unitized curtain walls with high-performance glass and fire-tested assemblies are favored.

Why is retrofit work drawing more attention in North America and Europe?

Aging post-war buildings must meet zero-carbon and fire-safety mandates, and insulated overcladding can cut heating loads by up to 50% without displacing occupants, making retrofits attractive.

How are commodity price swings affecting facade contractors?

Sharp moves in aluminum and glass prices squeeze fixed-price contracts, prompting many owners to insert price-adjustment clauses, and pushing fabricators to hedge or renegotiate terms mid-project.

Which regions will drive facade demand through 2031?

Asia-Pacific remains the largest purchaser, but the Middle East and Africa will post the fastest 6.48% CAGR on the strength of Saudi Vision 2030 and ongoing tower developments in the UAE.

Page last updated on: