Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

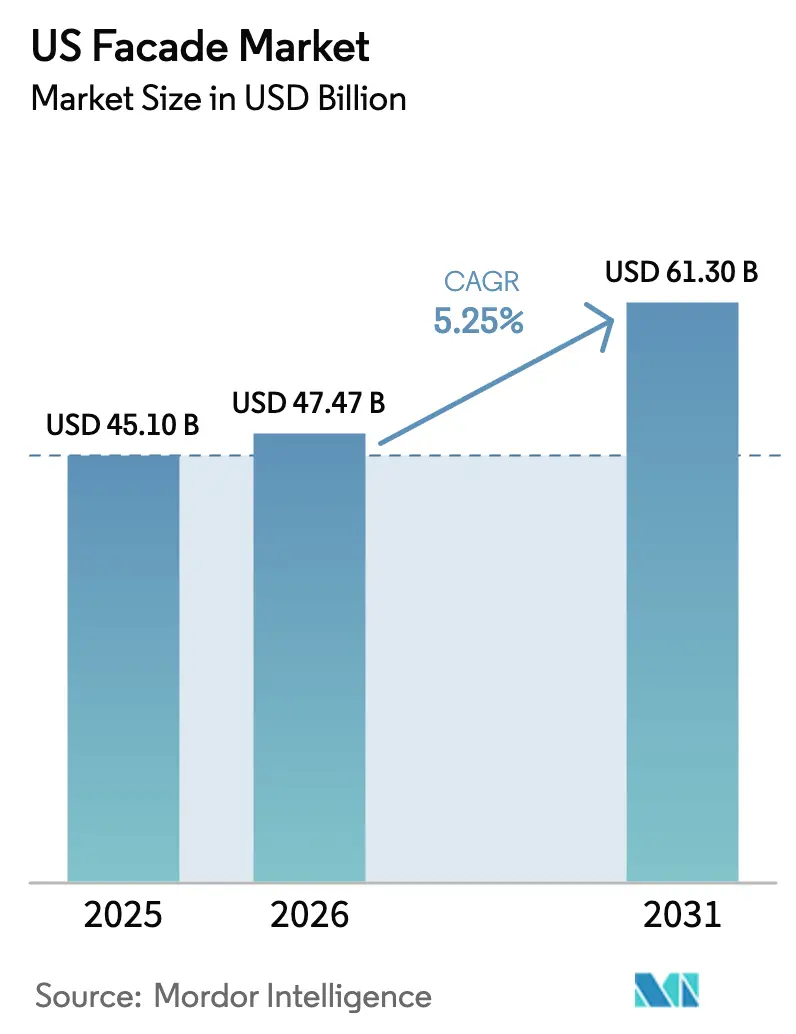

| Base Year Market Size (2025) | USD 45.10 Billion |

| Market Size (2026) | USD 47.47 Billion |

| Market Size (2031) | USD 61.30 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Facade Market Analysis by Mordor Intelligence

The US Facade Market size is projected to be USD 45.10 billion in 2025, USD 47.47 billion in 2026, and reach USD 61.30 billion by 2031, growing at a CAGR of 5.25% from 2026 to 2031.

Three structural shifts propel this expansion, including the rebound in non-residential construction after pandemic-era delays, the nationwide roll-out of stricter 2024 International Energy Conservation Code (IECC) and ASHRAE 90.1-2022 building-envelope standards, and a wave of hyperscale data-center investments requiring specialized blast-resistant and thermally efficient assemblies.[1]American Institute of Architects, “Architecture Billings Index Data Dashboard,” aia.orgTogether, these forces boost demand for high-performance curtain walls, ventilated rainscreen cladding, and low-carbon aluminum framing. At the regional level, the South accounted for 35.32% of the US facade market in 2025, while the West is projected to be the fastest-growing region at 5.46% CAGR through 2031, aided by California’s Buy Clean Act and seismic mandates. Commercial end-users dominated with 67.65% of demand in 2025 as office-tower modernizations and data-center campuses accelerated orders for unitized systems that cut on-site labor by 25-30%.

Key Report Takeaways

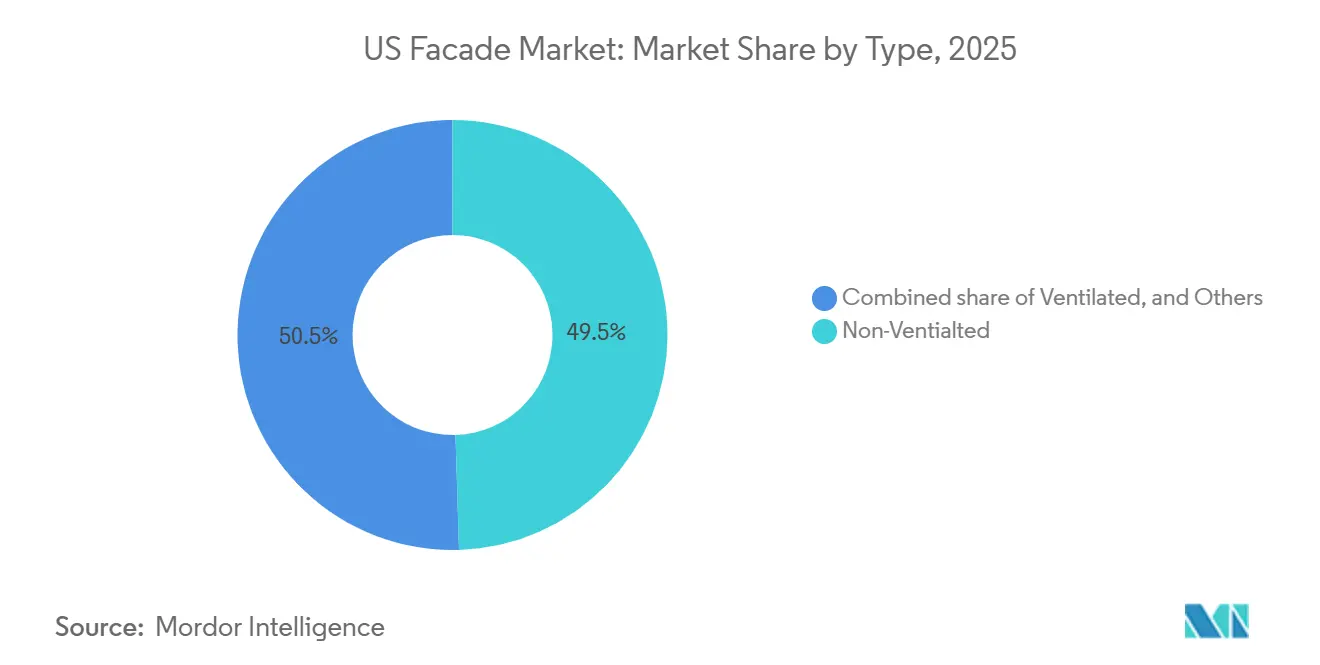

- By type, non-ventilated captured 49.52% of the US facade market share in 2025, and ventilated is growing at a 5.01% CAGR through 2031.

- By facade system type, curtain walls led with 52.40% of the US facade market share in 2025, whereas rainscreen cladding is the fastest-rising system at 5.08% CAGR to 2031.

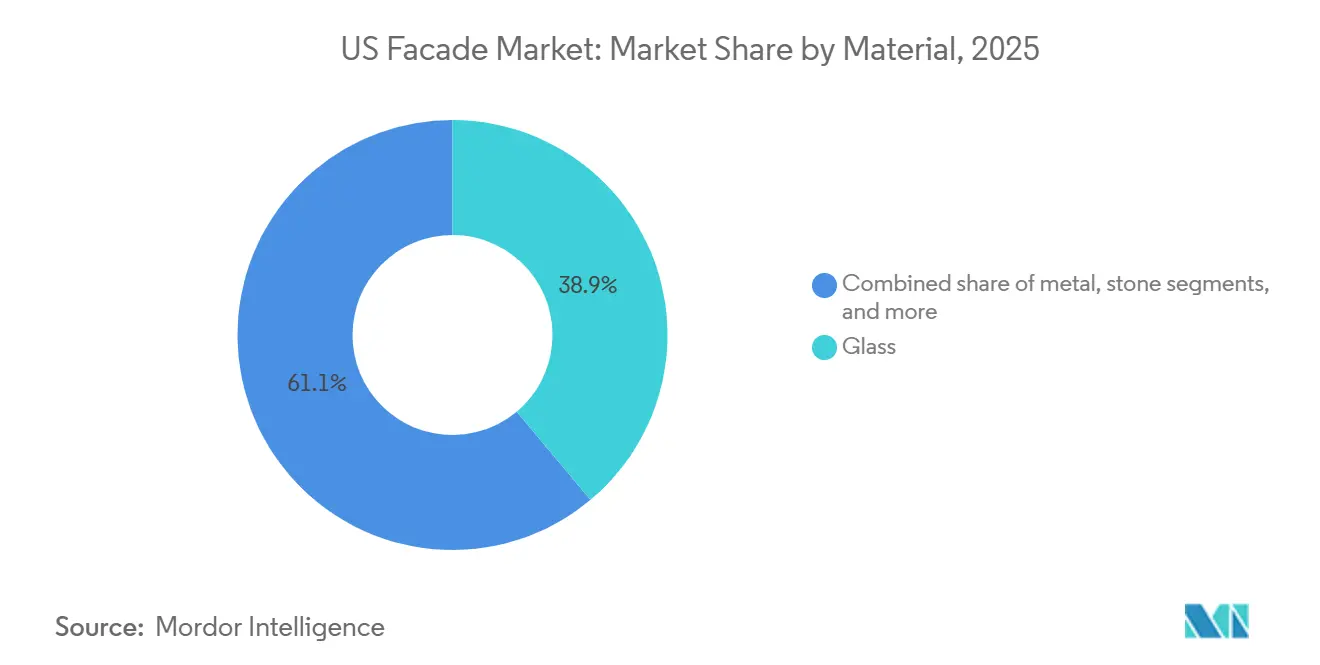

- By material, glass contributed 38.89% of the US facade market size in 2025, but metal cladding is advancing at a 4.80% CAGR on embodied-carbon advantages.

- By installation, new-build captured 63.82% of the US facade market size in 2025, yet renovation and retrofit activity is growing at a 5.18% CAGR through 2031.

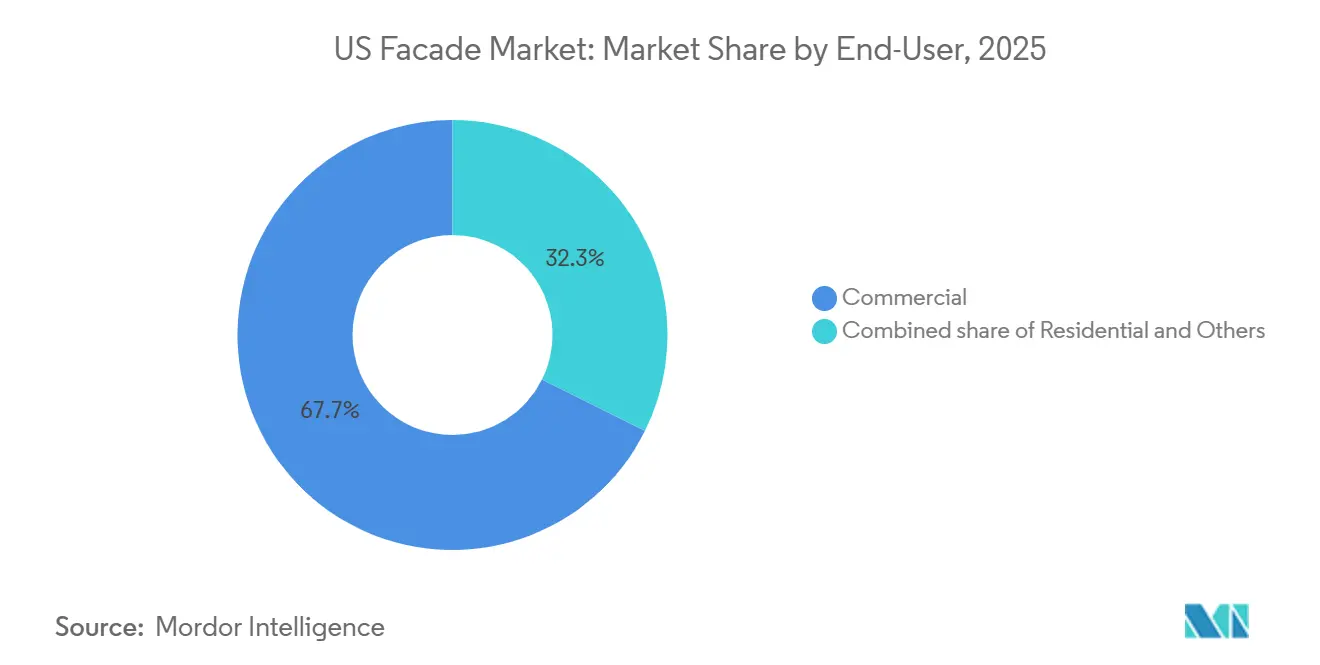

- By end-user, commercial buildings accounted for 67.65% of the US facade market size in 2025 and are projected to expand at a 5.29% CAGR over 2026-2031.

- By region, the South held 35.32% of the US facade market share in 2025, while the West is forecast to register a 5.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US Facade Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rebound in non-residential construction increases demand for advanced facade systems | +1.2% | National, with a concentration in the South and West regions | Medium term (2-4 years) |

| Stricter IECC and ASHRAE 90.1 building envelope codes drive high-performance facade adoption | +1.0% | National, early adoption in California, New York, and Massachusetts | Long term (≥ 4 years) |

| Aging commercial building stock triggers large-scale facade retrofit and modernization projects | +0.9% | Northeast and Midwest legacy metros, spillover to secondary markets | Medium term (2-4 years) |

| Rising demand for high-performance glazing improves building energy efficiency outcomes | +0.8% | National, accelerated in IECC Climate Zones 4-7 | Medium term (2-4 years) |

| Expansion of hyperscale data centers increases investment in specialized facade structures | +0.7% | West (California, Oregon), South (Texas, Virginia), Midwest (Wisconsin, Ohio) | Short term (≤ 2 years) |

| FEMA resilience grants encourage the installation of hurricane-rated and disaster-resistant facades | +0.5% | Gulf Coast (Texas, Louisiana, Florida), Atlantic seaboard (Carolinas, Mid-Atlantic) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rebound in Non-Residential Construction Increases Demand for Advanced Facade Systems

Design billings strengthened throughout 2025, with the AIA Index averaging 51.2, foreshadowing a sustained pipeline of office towers and mixed-use projects across Sunbelt metros. Developers favor unitized curtain-wall assemblies that cut installation time by up to 30%, helping contain labor costs amid skilled-trade shortages. Class A+ buildings now routinely target LEED Platinum or WELL certification, which encourages facade U-factors below 0.30 and visible-light transmittance above 40%. A marquee example is the 1.1 million-sq-ft Pioneer Natural Resources headquarters in Irving, Texas, clad with 3,000 high-performance curtain-wall units featuring Viracon glass that delivers 44% VLT and 0.26 SHGC. Taken together, these projects amplify orders for thermally broken framing, low-e insulated glass, and robust anchorage systems. The trend is expected to continue through 2027 as developers race to future-proof assets against tightening energy benchmarks.

Stricter IECC and ASHRAE 90.1 Building-Envelope Codes Drive High-Performance Facade Adoption

The 2024 IECC tightened curtain-wall U-factor limits to 0.36-0.40 in colder zones, while ASHRAE 90.1-2022 cut allowable air leakage by 25%. Compliance now demands triple-glazed IGUs, continuous air barriers, and advanced gaskets that raise assembly costs by 12-15%. Yet state utility programs in California, New York, and Massachusetts rebate USD 8-12 per sq ft for facades that outperform code by 20%, shrinking payback periods to less than nine years. Oldcastle BuildingEnvelope’s Series 3000 XT storefront achieves U-factors of 0.20, well below code, highlighting how fabricators are repositioning toward premium, high-performance products. As 38 states had adopted the 2024 IECC by early 2026, a uniform national baseline now accelerates widespread adoption of advanced envelope technologies.

Aging Commercial Building Stock Triggers Large-Scale Facade Retrofit and Modernization Projects

Roughly 60% of U.S. commercial buildings were built before 1990, and worn seals, spandrel failures, and thermal bridging push owners toward envelope upgrades. Benchmarking ordinances such as New York City’s Local Law 97 impose carbon caps that necessitate facade replacements, especially for Class B and C offices. Retrofit strategies include over-cladding with ventilated rainscreens and swapping single-pane glass for low-e IGUs, cutting energy use by 30-40%. The 3M Center Building 220 renovation, completed in 2025, saved 35% in annual energy, underlining a compelling business case. Major contractors like Turner Construction report double-digit growth in climate-resilient facade projects, confirming sustained momentum in the retrofit segment.

Rising Demand for High-Performance Glazing Improves Building Energy-Efficiency Outcomes

Advanced glazing triple-silver low-e coatings, vacuum IGUs, and electrochromic glass are moving mainstream as energy codes tighten. Cardinal Glass’s LoĒ³-366 delivers a center-of-glass U-factor of 0.11 and 65% VLT, balancing daylight and insulation. Vitro’s Solarban R77, launched in 2024, offers SHGC 0.25 with 47% VLT, tailored to ASHRAE zones 4-7. Corning’s 0.5-mm-thick Enlighten Glass halves weight, enabling larger spans in curtain-wall designs. The U.S. Department of Energy calculates that nationwide adoption of triple-glazed low-e units could trim commercial HVAC demand by up to 25%, reinforcing glazing’s vital role in decarbonization.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in aluminum and glass prices raises facade system project costs | -0.6% | National, acute pressure in South and West high-growth markets | Short term (≤ 2 years) |

| Shortage of certified facade installers delays project execution and increases labor costs | -0.5% | National, most severe in Northeast and West coastal metros | Medium term (2-4 years) |

| Insurance exclusions for combustible cladding under NFPA 285 limit material choices | -0.3% | National, concentrated in mid-rise residential and mixed-use projects | Medium term (2-4 years) |

| City-level embodied carbon regulations such as Buy Clean policies increase compliance costs | -0.2% | California, Colorado, New York, Massachusetts, Minnesota, Oregon, Denver | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Aluminum and Glass Prices Raises Facade System Project Costs

Aluminum spot prices climbed 30.5% year-over-year in early 2025 due to curtailments in Chinese smelting, while a 25% U.S. tariff on imported metals added further strain. Float-glass producers faced 15% cost hikes as natural-gas prices spiked, sending contract prices for oversized IGUs sharply higher. Facade contractors lost 200-300 basis points of margin and renegotiated fixed-price deals, delaying some mid-rise office and multifamily starts. YKK AP America mitigated risk by signing long-term deals with low-carbon aluminum smelters for 80% of its demand, stabilizing input pricing yet limiting its ability to exploit short-lived market dips. Vertically integrated majors such as Apogee, with in-house glass and finishing, weathered volatility better than regional independents, widening competitive gaps.

Shortage of Certified Facade Installers Delays Project Execution and Increases Labor Costs

The construction sector needs an extra 349,000 workers in 2026 to meet backlog, yet trade-school enrollment dropped 8% between 2020 and 2024.[2]Associated Builders and Contractors, “2026 Workforce Shortage Report,” abc.org Facade assembly is especially labor-intensive: curtain-wall alignment, silicone glazing, and waterproofing require three to five years of apprenticeship. Union wage scales climbed 14-16% in 2025 for certified glaziers, versus 8% overall construction wage inflation. Engineering News-Record reported that 18% of commercial projects in 2025 suffered delays tied to facade trades. Contractors are therefore switching to fully unitized panels and piloting robotic sealant applicators, but such technology still carries premium capex that only large firms can absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ventilated Systems Emerge as the Preferred Solution in Humid Regions

Ventilated rainscreen assemblies captured 50.48% of the US facade market share in 2025 and are projected to expand at a 5.01% CAGR through 2031 as code bodies prioritize moisture management in coastal climates. The design introduces a 0.75-1.5-inch cavity that drains vapor, cutting condensation risk by up to 50% relative to barrier walls. Adoption accelerates in IECC Climate Zones 4A-5A, covering the Eastern seaboard, where wind-driven rain challenges traditional sealed facades. Insurance carriers offer 5-10% premium discounts when ventilated cavities are documented, reinforcing financial motivation for owners.

Non-ventilated systems remain dominant in the arid Southwest, where low humidity keeps failure rates minimal, and cost efficiency trumps performance. Hybrid products, such as Kingspan’s QuadCore panels that integrate continuous insulation inside a drained cavity, blur the lines between categories and allow designers to meet both energy and moisture objectives. As investors demand resilient and low-carbon assets, ventilated designs are expected to become the baseline specification in all but the driest regions, ensuring their steady ascent within the broader US facade market.

By Facade System: Rainscreen Cladding Advances on Retrofit Appeal

Curtain walls accounted for 52.40% of the US facade market size in 2025, owing to their stronghold in high-rise construction. However, rainscreen cladding is projected to grow fastest at 5.08% CAGR to 2031, riding a wave of retrofit projects that favor lightweight over-cladding with minimal tenant disruption. Decoupling of structural and weatherproofing layers reduces thermal bridging by 60-70%, meeting stringent IECC 2024 targets for U-factor performance.

High-rise office towers, such as Montebello Gateway in California, still depend on custom curtain walls to achieve panoramic glass façades. Yet for aging Class B stock, rainscreens offer a practical upgrade path, and regional players like Dextall provide prefabricated kits that slash on-site labor by 30%. Looking ahead, hybrid systems that merge operable vents and drainage cavities into curtain-wall frames could neutralize the competitive gap, but for now, rainscreens enjoy a structural growth advantage in the US facade market.

By Material: Metal Cladding Gains Ground on Embodied-Carbon Benefits

Glass remained the single-largest material with 38.89% revenue share in 2025, yet metal facades, largely aluminum composite panels (ACP) and insulated metal panels (IMP), are poised for 4.80% CAGR growth through 2031. Aluminum’s infinite recyclability aligns with Buy Clean policies demanding transparent carbon accounting, and lead times of 10-12 weeks beat the 16-20 weeks typical for custom glazing. CENTRIA’s Formawall delivers Class A fire performance and R-values over 20, making it a frequent choice for data centers and manufacturing hubs.

Plastic and fiber-cement panels fill niche roles in corrosive coastal zones, whereas stone veneers endure in luxury and institutional projects despite seismic and weight constraints. Terracotta and bio-based composites, buoyed by RAF Equity Partners’ 2026 purchase of Boston Valley Terra Cotta, expand the palette for heritage renovations at premium price points. Over the forecast horizon, embodied-carbon disclosure will steadily tilt specifications toward low-carbon aluminum and high-performance coatings, consolidating metal’s share in the US facade market.

By Installation: Retrofit Activity Accelerates as Building Stock Ages

New construction represented 63.82% of the US facade market size in 2025 on the back of Sunbelt office campuses and gigantic data centers. Nonetheless, renovation and retrofit installations are projected to rise at a 5.18% CAGR. Upgrades typically combine over-cladding rainscreens with triple-glazed IGUs, reducing heating-cooling loads by one-third and curbing carbon penalties under local benchmarking laws.

Oldcastle BuildingEnvelope’s retrofit-optimized Series 3000 XT storefront installs into existing openings with minimal structural alterations, easing compliance for occupied towers. Building owners chasing rapid paybacks to satisfy environmental, social, and governance (ESG) investors find that utility rebates truncate return periods to nine years or less. Consequently, retrofit momentum will outpace new-build volume growth within the US facade market by late-decade.

By End-User: Commercial Buildings Sustain Leadership in Share and Growth

Commercial facilities commanded 67.65% of revenue in 2025 and are set to expand at a 5.29% CAGR, benefiting from AI-driven data-center rollouts, office-tower repositioning, and experiential retail spaces. Vantage Data Centers’ USD 15 billion Wisconsin campus alone represents a multiyear pipeline for blast-resistant panels and insulated metal enclosures.

Residential demand is tempered by NFPA 285 constraints and elevated insurance premiums, while institutional buyers in healthcare and education adopt continuous-insulation EIFS (Exterior Insulation and Finish Systems) such as StoTherm ci to meet energy and infection-control requirements. Despite headwinds in speculative multifamily starts, the sheer scale and capital intensity of commercial megaprojects ensure that the segment retains dominance in the US facade market through 2031.

Geography Analysis

The South dominated the US facade market with 35.32% revenue share in 2025, propelled by booming commercial corridors in Texas and Florida that combine favorable permitting, population inflows, and hurricane-code premiums on impact-rated glazing. Texas alone represented roughly 14% of national demand, buoyed by the Dallas–Austin tech corridor and affordable land for hyperscale data-center parks. Florida’s coastal exposure categories require wind-load compliance up to 180 mph, steering architects toward laminated glass and reinforced frames that command premium pricing.[3]Florida Building Commission, “Wind Load Code Revisions,” floridabuilding.org Looking forward, the South’s business-friendly climate anchors its share, even as input-cost volatility nudges some owners to negotiate longer procurement lock-ins.

The West is projected to be the fastest-growing region at 5.46% CAGR to 2031, underwritten by California’s Title 24 energy code and Buy Clean embodied-carbon mandates that accelerate turnover of legacy facades. Seismic drift criteria further incentivize flexible curtain-wall systems with slip joints, adding 10-15% to material budgets yet lowering earthquake-loss risk. Silicon Valley life-science campuses and Los Angeles entertainment studios often specify high-VLT glazing paired with electrochromic tinting to balance daylight with heat load, creating steady pull for premium IGUs. Manufacturers with low-carbon aluminum supply chains gain an edge in this regulatory environment and deepen penetration in the US facade market.

The Northeast and Midwest emphasize retrofit over greenfield starts. New York City’s Local Law 97 and Boston’s BERDO 2.0 push owners to slash operational carbon or face steep fines, prompting envelope upgrades across skyscraper canyons. Turner Construction logged a 22% rise in climate-resilient facade contracts in 2025, spotlighting the retrofit surge. Meanwhile, data-center construction in Wisconsin and Ohio injects fresh new-build volume into the Midwest, but overall growth lags coastal peers. Colder IECC zones force triple-glazed, thermally broken frames that raise costs by nearly one-fifth yet utility rebates partly cushion the blow, ensuring a measured pace of facade investment across heartland markets.

Competitive Landscape

The US facade market remains moderately concentrated. Vertically integrated majors such as Apogee Enterprises leverage an internal glass-to-installation ecosystem spanning Viracon fabrication to Harmon field services to manage quality and squeeze costs competitors cannot match. Oldcastle BuildingEnvelope and YKK AP America retain broad catalogs and robust technical-support arms, offering digital twin modeling that simplifies code compliance for architects and secures specification loyalty.

Strategic activity accelerated in 2025-2026. Permasteelisa North America’s January 2025 purchase of Benson Industries delivered West Coast capacity and custom-metal expertise that fortifies its seismic-resilient portfolio. Trulite Glass & Aluminum’s Insulite acquisition expanded insulated-glass unit (IGU) capacity by 200,000 sq ft, enabling faster turnaround in Sunbelt hotspots. February 2026 saw RAF Equity Partners buy Boston Valley Terra Cotta, signaling investor interest in artisanal cladding priced at 30-40% premiums. Each deal underscores a tilt toward specialty products and geographic fill-ins to win differentiated margin in the US facade market.

Technology adoption further tilts competitive dynamics. Oldcastle’s Series 3000 XT storefront, boasting a U-factor of 0.20, typifies product innovation that answers IECC 2024 while trimming field labor. Leading firms deploy prefabricated, unitized assemblies that reduce site labor by 25-30%, a decisive edge amid glazing-trade shortages. New entrants bet on insulated metal panel solutions; CENTRIA and Kingspan target data-center verticals where fire performance and speed trump crystalline aesthetics. Compliance with NFPA 285 and ASTM E1996 testing remains a high barrier to entry, reinforcing market power among incumbents with certified labs and well-oiled code-official relationships.

US Facade Industry Leaders

Oldcastle BuildingEnvelope

YKK AP America

Kawneer North America

Permasteelisa North America

Apogee Enterprises Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: RAF Equity Partners acquired Boston Valley Terra Cotta, expanding into heritage restoration cladding with 30-40% premium pricing.

- February 2026: Oldcastle BuildingEnvelope renewed its American Institute of Architects partnership to fund continuing-education courses on thermal bridging mitigation.

- January 2026: YKK AP opened its N-CueB testing facility in Japan to support AAMA 501 and ASTM E1996 certification for U.S. curtain-wall products.

- August 2025: Performance Contracting Inc. bought LYMO Construction to widen turnkey facade-installation reach across the Midwest and Southeast.

US Facade Market Report Scope

By Type

| Ventilated |

| Non-Ventilated |

| Others |

By Façade System Type

| Rainscreen Cladding |

| Curtain-Wall Systems |

| Others |

By Material

| Glass |

| Metal |

| Plastic & Fibres |

| Stone |

| Others |

By Installation

| New Construction |

| Renovation & Retrofit |

By End-User

| Commercial |

| Residential |

| Others |

By Region

| Northeast |

| Midwest |

| South |

| West |

| By Type | Ventilated |

| Non-Ventilated | |

| Others | |

| By Façade System Type | Rainscreen Cladding |

| Curtain-Wall Systems | |

| Others | |

| By Material | Glass |

| Metal | |

| Plastic & Fibres | |

| Stone | |

| Others | |

| By Installation | New Construction |

| Renovation & Retrofit | |

| By End-User | Commercial |

| Residential | |

| Others | |

| By Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

How big is the US facade market in 2026?

It is valued at USD 47.47 billion, on track to reach USD 61.3 billion by 2031.

Which facade system is growing fastest in the United States?

Rainscreen cladding is projected to post a 5.08% CAGR through 2031 because it suits cost-effective over-cladding retrofits.

Why is metal cladding gaining popularity?

Aluminum composite and insulated metal panels meet Buy Clean embodied-carbon rules, offer Class A fire ratings, and deliver shorter lead times.

What region will outpace others in facade spending?

The West is set to grow at a 5.46% CAGR, spurred by California’s energy code and seismic requirements.

How are labor shortages affecting facade projects?

A lack of certified glaziers is raising wages 14-16% and driving adoption of prefabricated unitized panels that cut on-site labor by up to 30%.

Page last updated on: