Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

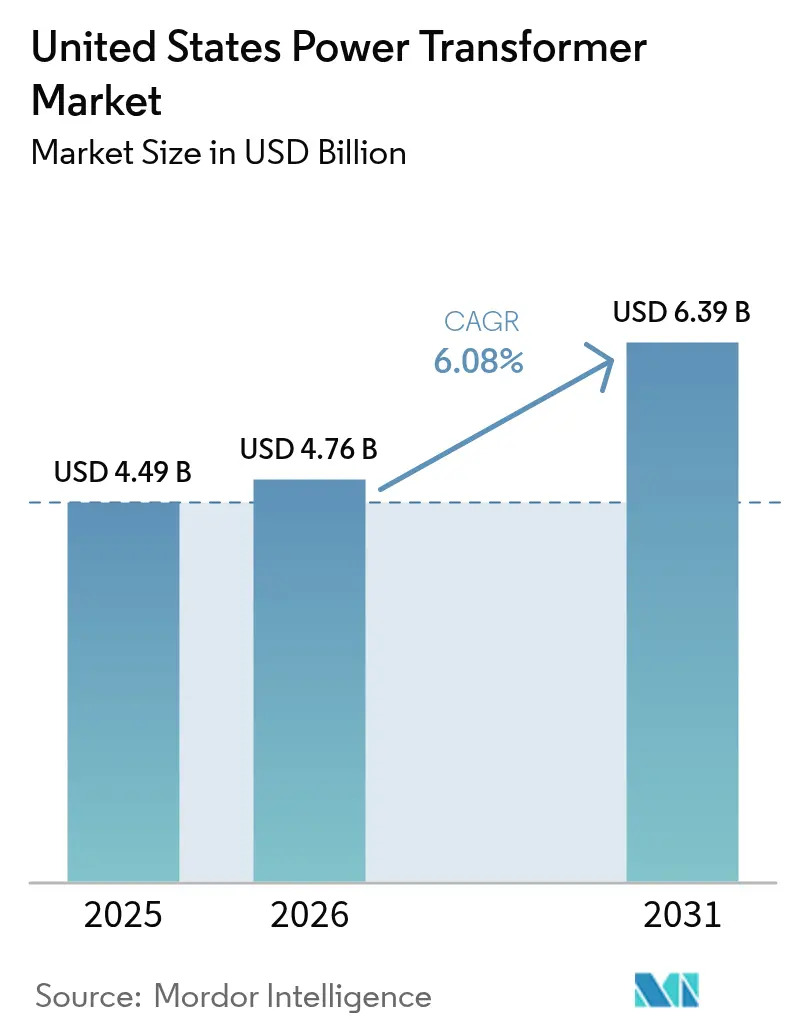

| Base Year Market Size (2025) | USD 4.49 Billion |

| Market Size (2026) | USD 4.76 Billion |

| Market Size (2031) | USD 6.39 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Power Transformer Market Analysis by Mordor Intelligence

The United States Power Transformer Market size was valued at USD 4.49 billion in 2025 and estimated to grow from USD 4.76 billion in 2026 to reach USD 6.39 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031).

Vigorous growth stems from the mandatory replacement of aging grid assets, the federal government’s USD 10.5 billion grid modernization outlay, and the explosive build-out of hyperscale data centers that follow the demand for artificial-intelligence computing. More than 70% of the transmission-class fleet exceeds 25 years of service, creating a non-discretionary replacement pipeline that lifts baseline demand for the United States power transformer market.{1]U.S. Department of Energy, “Grid Modernization and Asset Age Statistics,” energy.gov Federal production-tax-credit bonuses linked to domestic content tilt purchasing toward U.S. factories, unleashing over USD 2 billion in announced capacity additions and shortening delivery lead times. Simultaneously, renewable-energy interconnections, heavy-transport electrification, and tighter efficiency standards raise specification complexity, allowing manufacturers to capture higher average selling prices. Currently, domestic plants supply only 20% of large-unit requirements, and quotations indicate lead times of 115 to 130 weeks, underscoring the persistent supply gap in the United States power transformer market.[2]Engineering News-Record, “Transformer Lead-Time Tracker,” enr.com

Key Report Takeaways

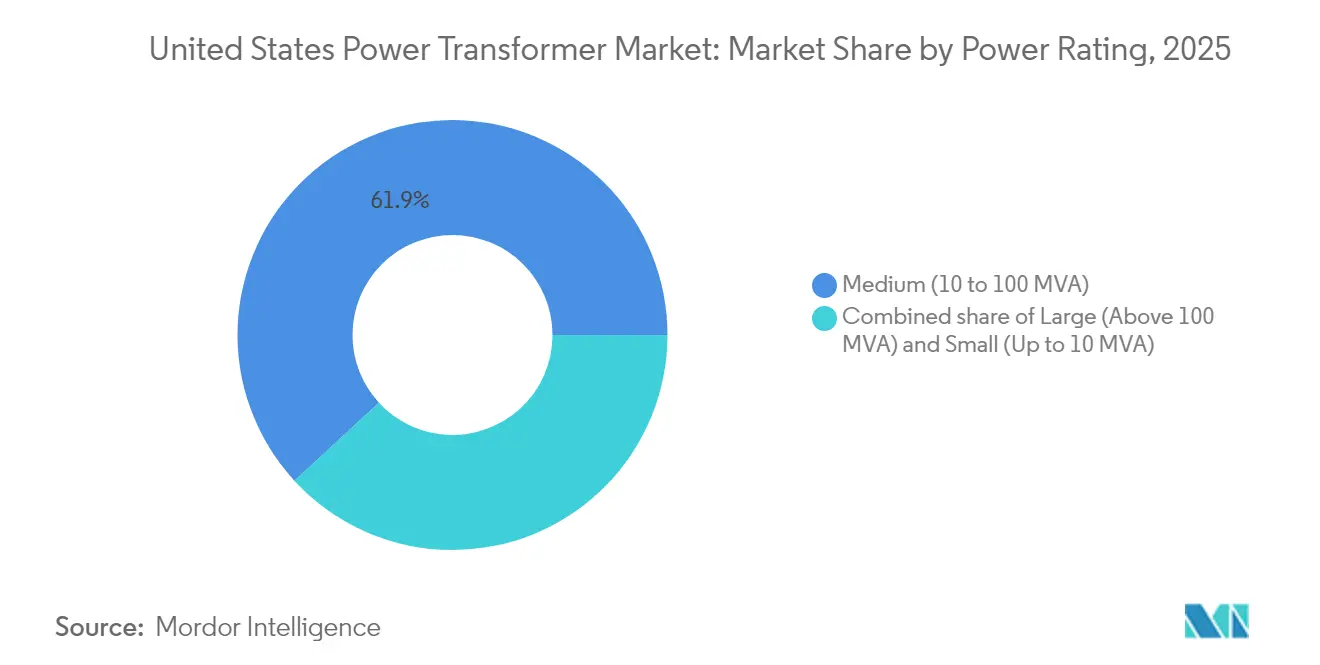

- By power rating, medium-capacity units (10-100 MVA) held 61.85% of the United States power transformer market share in 2025, while the same segment is projected to expand at a 6.95% CAGR through 2031.

- By cooling type, oil-cooled equipment dominated the United States power transformer market with a 76.55% share in 2025; air-cooled designs are expected to record the fastest growth at a 6.62% CAGR.

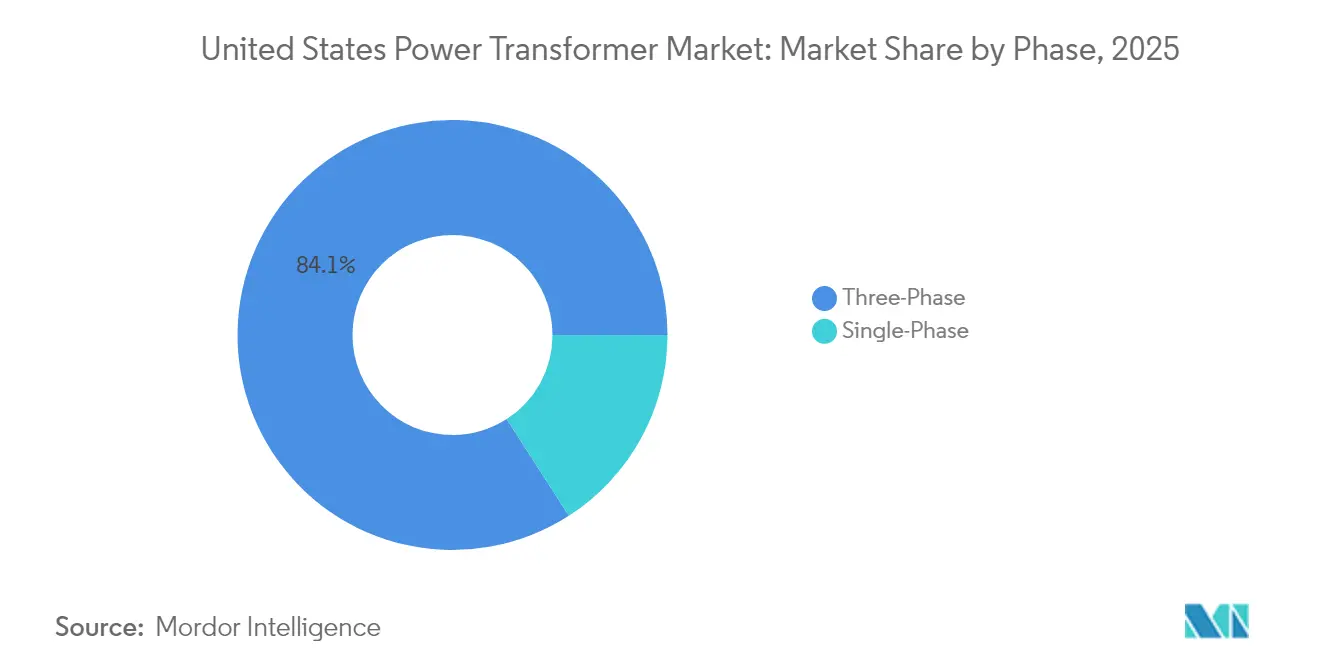

- By phase, three-phase transformers accounted for 84.10% of the United States' power transformer market size in 2025, and single-phase deployments are expected to grow at a 6.18% CAGR through 2031.

- By end user, power utilities led with a 58.35% revenue share in 2025; the segment is forecast to post a robust 6.85% CAGR as grid modernization mandates accelerate replacement cycles.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Power Transformer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated replacement of aging grid assets | +1.7% | National, with concentration in Northeast, Midwest legacy grids | Medium term (2-4 years) |

| Surge in renewable energy interconnections | +1.4% | Texas, California, Plains states with high wind/solar capacity | Short term (≤ 2 years) |

| Federal grid-modernization funding (IIJA) | +1.2% | National, prioritizing rural and underserved regions | Medium term (2-4 years) |

| Hyperscale data-center build-out | +1.0% | Virginia, Texas, North Carolina, Oregon data center hubs | Short term (≤ 2 years) |

| Heavy-transport electrification projects | +0.8% | California, Northeast corridor, major freight routes | Long term (≥ 4 years) |

| Domestic-content incentives under IRA | +0.6% | National, with manufacturing concentration in Southeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Replacement of Aging Grid Assets

Four-decade-old transformers now dominate many regional networks, creating a reliability gap as failure rates approach 0.5% of the installed base annually. DOE data indicate that 55% of distribution-class units surpass 33 years of age, while transmission-class averages reach 40 years. New efficiency standards effective in 2027 classify many legacy designs as non-compliant, compelling utilities to adopt fleet-wide swap-out programs rather than one-off repairs. Rising electric-load intensity from AI-driven data centers and electric-vehicle charging elevates operational stress on aging machines, compressing the replacement timetable. Consequently, the United States power transformer market gains a predictable floor of baseline demand that cushions against macroeconomic swings.

Surge in Renewable-Energy Interconnections

Utility-scale wind and solar plants require collector transformers that can handle bidirectional power flow, harmonic distortion, and fluctuating load cycling. California ISO’s twenty-year transmission outlook highlights USD 30 billion of projects with advanced monitoring and tap-changing requirements. ERCOT expects 40 GW of incremental load by 2030, largely tied to renewable interconnections that rely on bespoke step-up transformers.[3]Utility Dive, “ERCOT Load Growth Forecast,” utilitydive.com Such technical needs reshape specification sheets, allowing suppliers to embed smart-sensor packages and command premium margins inside the United States power transformer market.

Federal Grid-Modernization Funding (IIJA)

The USD 10.5 billion Grid Resilience and Innovation Partnerships program has already disbursed USD 2.2 billion to eight multi-state projects featuring climate-resilient designs. Funding criteria prioritize underserved areas and Justice40 communities, redirecting capital toward regions that have long been neglected by private investment. Awardees must adhere to domestic-content thresholds, giving manufacturers with U.S. plants a wide bidding advantage. Parallel FITT grants fund nine next-generation prototypes, seeding demand for transformers that integrate power electronics, condition-monitoring, and cyber-secure interfaces. This policy cocktail supports a structural uplift in the United States power transformer market.

Hyperscale Data-Center Build-Out

AI training clusters now require tens of megawatts per building, surpassing the loads of legacy data centers. Northern Virginia alone has seen a five-fold increase in power-delivery requests, while Texas utility Oncor has 59 GW of data center demand in its queue. Each campus often orders more than 250 MVA autotransformers, plus N+1 redundancy, thereby doubling the volume per site. Hyperscalers also demand advanced diagnostics and fire-safe cooling media, further enlarging order values in the United States power transformer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper & electrical-steel price volatility | -0.6% | National, with higher impact on cost-sensitive segments | Short term (≤ 2 years) |

| Global core-steel supply-chain bottlenecks | -0.4% | National, affecting all capacity ratings | Medium term (2-4 years) |

| Stricter mineral-oil spill regulations | -0.3% | National, with stricter enforcement in California, Northeast | Long term (≥ 4 years) |

| Emerging solid-state transformer pilots | -0.2% | Regional pilots in smart grid demonstration areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Copper & Electrical-Steel Price Volatility

Copper price bands widened 40% year-on-year in 2024, and grain-oriented electrical steel (GOES) quotes have doubled since 2020. Cleveland-Cliffs remains the only domestic GOES smelter, creating a single-supplier pinch point. Price swings complicate bid validity and inflate inventory carrying costs, forcing utilities to pre-purchase or escrow contracts, moves that erode capital budgets earmarked for modernization.

Stricter Mineral-Oil Spill Regulations

EPA SPCC thresholds trigger containment mandates for equipment holding more than 55 gallons of oil.[4]U.S. Environmental Protection Agency, “SPCC Guidance,” epa.gov States such as California add even tighter rules, prompting urban substations and data center campuses to favor air-cooled or natural-ester-filled units despite higher acquisition costs. While this regulatory trend spurs innovation, it also dampens demand for traditional mineral-oil models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Medium-Capacity Dominance Drives Market Growth

Medium-capacity units (10-100 MVA) captured 61.85% of the United States power transformer market in 2025. Utilities prefer this range because it strikes a balance between factory throughput, shipping weight, and substation footprint. The segment also records the briskest 6.95% CAGR as transmission owners deploy modular substations that can scale capacity by adding identical bays rather than installing single large monoliths. Up-rating feeders from 138 kV to 230 kV often lands in the mid-capacity sweet spot, ensuring repeat orders. Large-capacity machines (over 100 MVA) service 765 kV corridors and hyperscale data center campuses. Demand spikes in Texas, where regulators have just green-lit the state’s inaugural 765 kV lines, stretch the domestic build queue for units exceeding 500 MVA. Small transformers (<10 MVA) hold niche relevance in distributed generation, microgrids, and EV fast-charging plazas. Although volume is high, revenue share remains modest due to lower unit pricing. The United States power transformer market size for mid-capacity equipment is forecast to rise steadily, supported by a fleet-average replacement strategy that favors uniform ratings for easier inventory management.

By Cooling Type: Oil-Cooled Leadership with Air-Cooled Innovation

Oil-cooled designs held 76.55% share of the United States power transformer market in 2025, underpinned by proven thermal performance at high nameplate ratings and comparatively low upfront cost. Mineral-oil systems remain the default for bulk-power interconnection and petrochemical complexes where land is plentiful and spill-containment basins are standard practice. Yet, city-center substations, data-center halls, and offshore wind platforms face stringent fire and environmental rules that benefit air-cooled and natural-ester variants. Air-cooled models log a 6.62% CAGR as utility planners trade off lower power density for simplified permitting. National Electrical Code updates now recognize less-flammable liquids, allowing hybrid solutions that marry forced-oil cooling with fire-inhibited esters. This design innovation bridges the performance gap while maintaining compliance, thereby widening the addressable use cases for non-mineral-oil alternatives. Over the forecast period, the United States power transformer market is expected to see a gradual shift in share toward air-cooled and ester-filled products, particularly in jurisdictions with stringent spill-prevention enforcement.

By Phase: Three-Phase Efficiency Drives Market Leadership

Three-phase equipment dominated 84.10% of the United States power transformer market in 2025. Balanced phase loading minimizes line losses and enables smaller conductor cross-sections, vital for long-haul transmission. Industrial motors, synchronous condensers, and bulk storage inverters also run on three-phase power, reinforcing segment hegemony. Single-phase units nevertheless carve out a niche for resilience, serving rooftop solar arrays, pole-mounted residential feeders, and isolated rural circuits. As EV charging proliferates, some utilities upgrade single-phase circuits to meet 400% load surges during peak home-charging windows. Distribution automation tools such as adaptive volt-var controllers now interface directly with intelligent single-phase transformers, extending asset life and justifying premium pricing. Although share shifts will be incremental, technology convergence ensures that even single-phase offerings embed digital monitors, narrowing the functionality divide within the broader United States power transformer industry.

By End-User: Power Utilities Lead Market Expansion

Power utilities absorbed 58.35% of shipments in 2025 and will expand at a 6.85% CAGR through 2031. Mandated reliability standards, public-policy renewable targets, and congestion-relief projects combine to sustain a multi-billion-dollar buying pipeline. Investor-owned utilities typically embed transformer replacement costs in rate-based filings, whereas cooperatives often utilize federal grants for resilience upgrades. Industrial customers, particularly steel mills and petrochemical complexes, install bespoke high-MVA units, which offer concentrated but lumpy demand. Commercial buyers, led by hyperscale data center developers, now compete with utilities for limited factory slots, prompting some to sign multi-year framework agreements. The residential slice grows as rooftop solar adoption requires bi-directional distribution transformers capable of safe reverse power flow. Across all categories, digital monitoring and predictive-maintenance dashboards become table stakes, further enhancing the value of hardware. Thus, the United States power transformer market continues to shift toward integrated hardware-software solutions that align with advanced grid management paradigms.

Geography Analysis

Texas ranks first in absolute demand for the United States power transformer market, underpinned by ERCOT’s 40 GW load-growth forecast and approvals for 765 kV corridors linking the Permian Basin to Gulf Coast load centers. Fast-track data-center campuses around Dallas–Fort Worth require large blocks of more than 250 MVA capacity, compressing lead-time tolerance and amplifying the pull on domestic production. California follows closely, with the California ISO mapping USD 30 billion of transformer-heavy upgrades to integrate 25 GW of solar, 5 GW of offshore wind, and 3 GW of battery storage. Environmental regulations push the state toward air-cooled or natural-ester units, reshaping vendor scorecards.

The Northeast corridor, home to aging 115 kV and 138 kV networks, focuses on replacement rather than expansion. Utilities here favor plug-and-play smart transformers that minimize outage duration during change-outs, justifying premium prices. Midwestern states combine heavy industrial loads with wind-farm build-outs, sustaining consistent medium-capacity demand. The Southeast emerges as a manufacturing hub, with Siemens Energy in North Carolina, Eaton in South Carolina, and Hitachi Energy in Virginia collectively adding more than 1.5 GW of annual transformer output by 2027, thereby slashing freight-plus-tariff costs for regional buyers.

In the Pacific Northwest, hydropower turbine uprates and the Columbia Basin’s offshore wind corridor necessitate both generator step-up and intertie autotransformers that can withstand wide reactive power swings. Alaska and islanded microgrids in Hawaii illustrate niche geographies that adopt modular, skid-mounted units with Arctic or saline protection packages. Collectively, geographic demand diversity compels suppliers to maintain a flexible product portfolio, reinforcing the structural attractiveness of the United States power transformer market.

Competitive Landscape

The United States power transformer market exhibits moderate concentration, with the top five manufacturers holding a roughly 55-60% combined revenue share. Hitachi Energy has announced a capital expenditure (capex) of USD 250 million for its Mississippi and Virginia sites, part of a USD 4.5 billion global build-out that aims to double North American output by 2027. Siemens Energy commits USD 150 million to expand its Charlotte, North Carolina, plant, earmarking capacity for 230 kV and 500 kV units that fulfill domestic-content criteria. Eaton’s USD 340 million South Carolina greenfield facility targets three-phase, medium-capacity models aimed at data centers and investor-owned utilities.

Strategic differentiation centers on lead-time reliability, digital-twin integration, and lifecycle service contracts. Hitachi Energy markets its TXpert platform, bundling dissolved-gas-analysis sensors, fiber-optic winding thermometry, and AI-driven asset analytics. GE Vernova pursues vertical integration via Prolec GE’s USD 645 million purchase of SPX Transformer Solutions, securing core-steel lamination capacity and adding high-voltage test bays. Cleveland-Cliffs’ USD 150 million electrical-steel plant in West Virginia offers OEMs a domestic alternative to Asian GOES, potentially easing supply bottlenecks but also elevating competitive entry barriers.

Technology-wise, solid-state transformer pilots command R&D attention. DOE’s FITT program funds Clemson University’s hybrid unit and GE Vernova’s SiC-based SST prototype, signaling a future pivot toward power-electronics-heavy architectures. In the interim, demand outstrips supply, and procurement award criteria increasingly reward guaranteed delivery over marginal cost differences. As a result, the United States power transformer market favors incumbents with deep capital pools, multi-site production footprints, and forward-integrated digital-service offerings.

United States Power Transformer Industry Leaders

-

Hitachi Energy Ltd.

-

Siemens Energy AG

-

ABB Ltd.

-

GE Vernova (GE Grid Solutions)

-

SPX Transformer Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hitachi Energy has earmarked USD 250 million to boost transformer output across its sites in Virginia, Missouri, and Mississippi, recruiting 100 new employees to deepen supply-chain resilience.

- February 2025: Eaton announced a USD 340 million three-phase transformer factory in Jonesville, South Carolina, projected to create 700 jobs and help mitigate domestic shortages.

- December 2024: The DOE selected nine initiatives for USD 20 million under the FITT scheme to accelerate the development of smart and solid-state transformers.

- October 2024: The DOE awarded USD 1.5 billion through the Transmission Facilitation Program to four HVDC projects, including Southern Spirit, each of which required bespoke high-voltage transformers.

United States Power Transformer Market Report Scope

A power transformer's function is to change the voltage on a transmission line from high to low (consumer). The transformer is a piece of electrical equipment that uses electromagnetic induction to transmit electric energy.

The United States power transformer market is segmented by type and phase. By type, the market is segmented into oil-insulated and air-insulated. By phase, the market is segmented into a single phase and three phases. For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

By Power Rating

| Large (Above 100 MVA) |

| Medium (10 to 100 MVA) |

| Small (Up to 10 MVA) |

By Insulation Type

| Air-cooled |

| Oil-cooled |

By Phase

| Single Phase |

| Three Phase |

By End-User

| Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial |

| Commercial |

| Residential |

| By Power Rating | Large (Above 100 MVA) |

| Medium (10 to 100 MVA) | |

| Small (Up to 10 MVA) | |

| By Insulation Type | Air-cooled |

| Oil-cooled | |

| By Phase | Single Phase |

| Three Phase | |

| By End-User | Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

What is the current value of the United States power transformer market?

The United States power transformer market is valued at USD 4.76 billion in 2026.

How fast is the market expected to grow?

It is projected to reach USD 6.39 billion by 2031, registering a 6.08% CAGR.

Which transformer segment holds the largest share?

Medium-capacity units (10-100 MVA) hold 61.85% of market revenue as of 2025.

Why are data centers influencing transformer demand?

Hyperscale campuses require >250 MVA capacity and duplicate units for redundancy, sharply increasing order volumes.

How are federal policies supporting domestic manufacturing?

IIJA grants and IRA bonus credits tied to domestic content have triggered more than USD 2 billion in new U.S. transformer-plant investments.

What is the main supply-chain bottleneck for manufacturers?

Grain-oriented electrical steel shortages and copper price volatility extend lead times and elevate costs.

Page last updated on: