Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

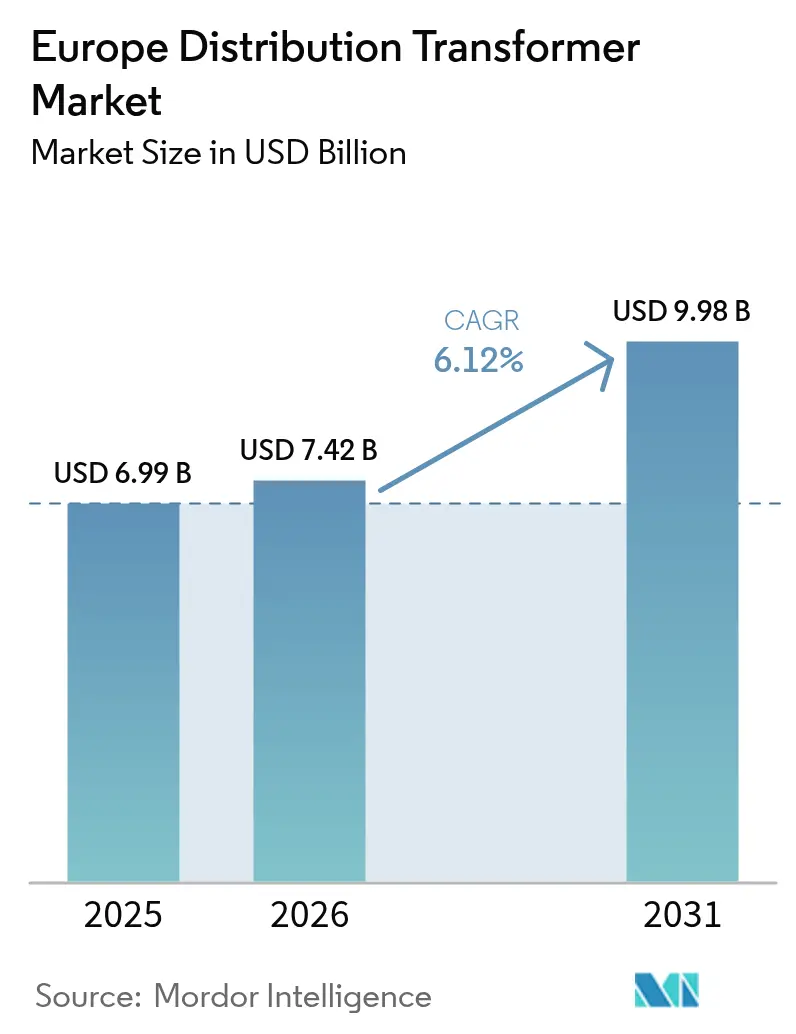

| Base Year Market Size (2025) | USD 6.99 Billion |

| Market Size (2026) | USD 7.42 Billion |

| Market Size (2031) | USD 9.98 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Distribution Transformer Market Analysis by Mordor Intelligence

Europe Distribution Transformer Market size in 2026 is estimated at USD 7.42 billion, growing from 2025 value of USD 6.99 billion with 2031 projections showing USD 9.98 billion, growing at 6.12% CAGR over 2026-2031.

Solid momentum stems from grid modernization funding, stricter EU energy-efficiency rules, and surging demand from electric-vehicle charging hubs and hyperscale data center clusters.[1]European Investment Bank, “Financing the Energy Transition 2025,” eib.org Utility capital-expenditure pipelines are rising after the pandemic pause as operators deploy digital, high-efficiency units to reduce network losses and increase hosting capacity for renewable energy integration. At the same time, specification shifts triggered by the EU Fit-for-55 package are steering procurement toward premium-efficiency cores and biodegradable insulating fluids, inflating average selling prices yet lowering lifetime losses. Supply-chain tightness in electrical steel remains a brake on output; however, strategic stockpiling, dual sourcing, and incremental capacity additions are tempering the impact on short-term deliveries. Mergers and factory expansions by leading OEMs signal growing competition for geographic reach and cost leadership, while utilities consolidate order books with framework agreements to lock in supply.

Key Report Takeaways

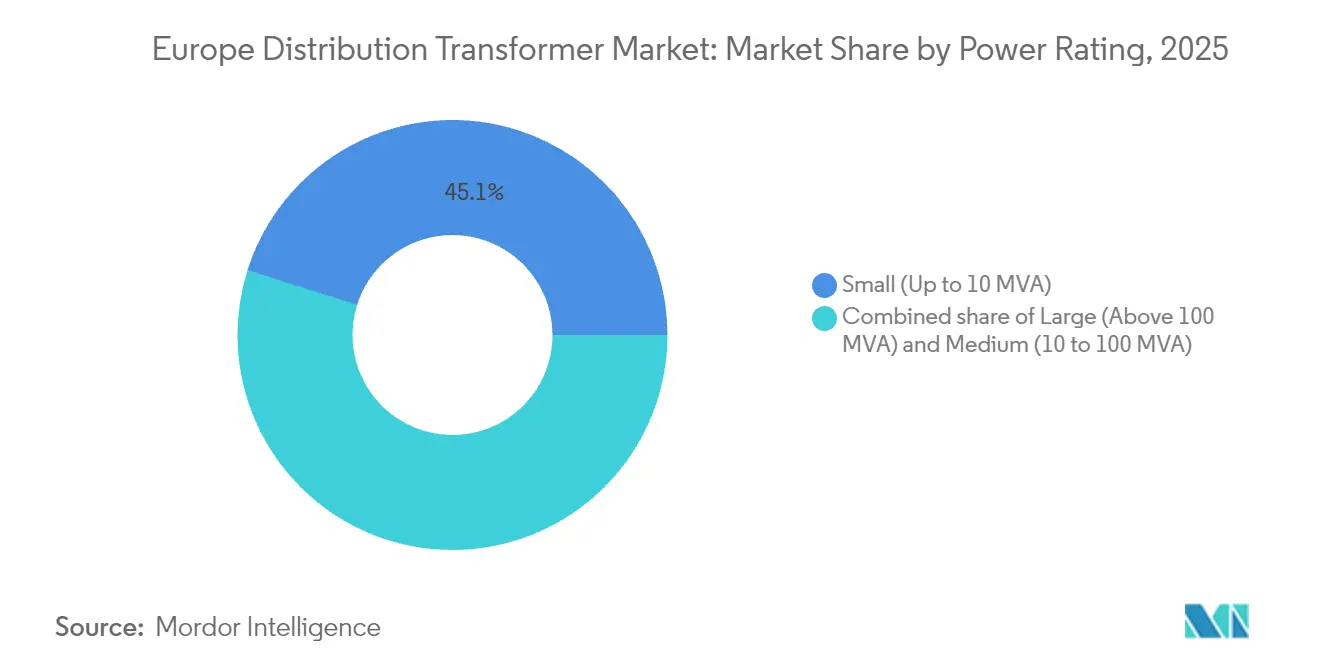

- By power rating, small transformers (≤ 10 MVA) held 45.12% of 2025 revenue; large transformers (> 100 MVA) are projected to register a 6.74% CAGR through 2031.

- By cooling type, oil-cooled units led with 79.85% share in 2025 and are expected to post the fastest 6.18% CAGR over the forecast window.

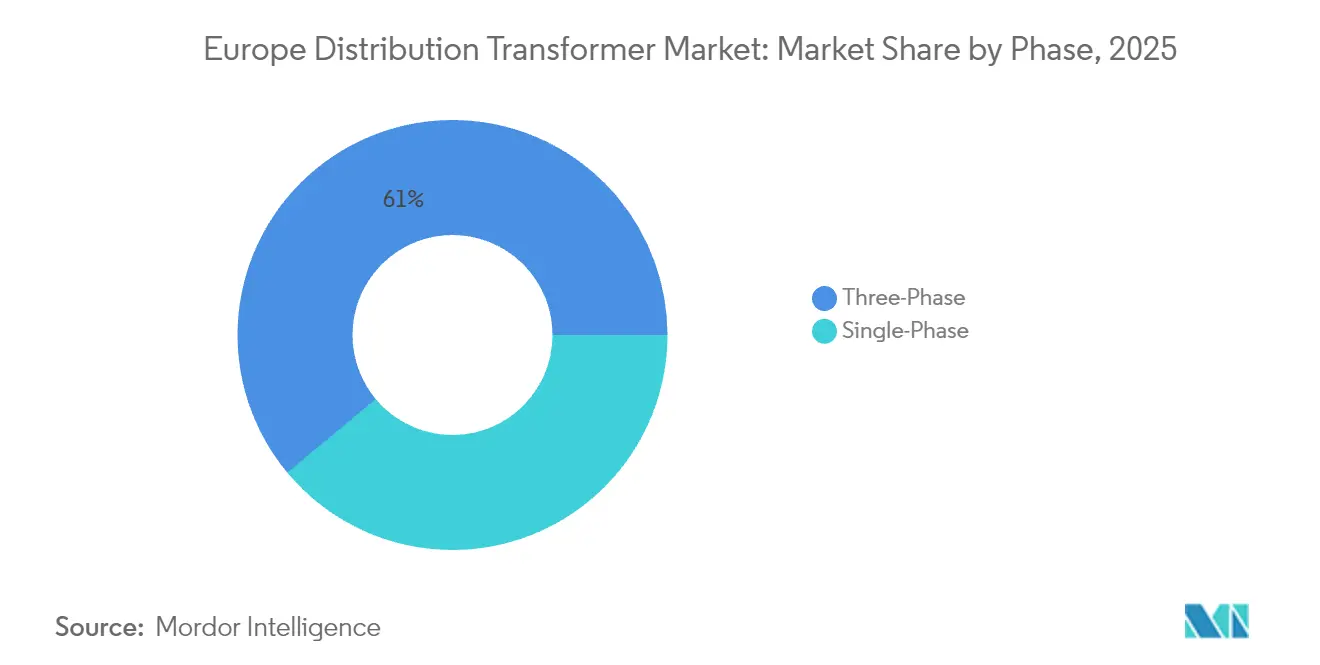

- By phase, three-phase designs accounted for 61.05% of 2025 sales and are forecasted to expand at a 6.41% CAGR through 2031.

- By end-user, power utilities accounted for 40.05% of 2025 revenue, whereas industrial customers are poised for a 7.03% CAGR through 2031.

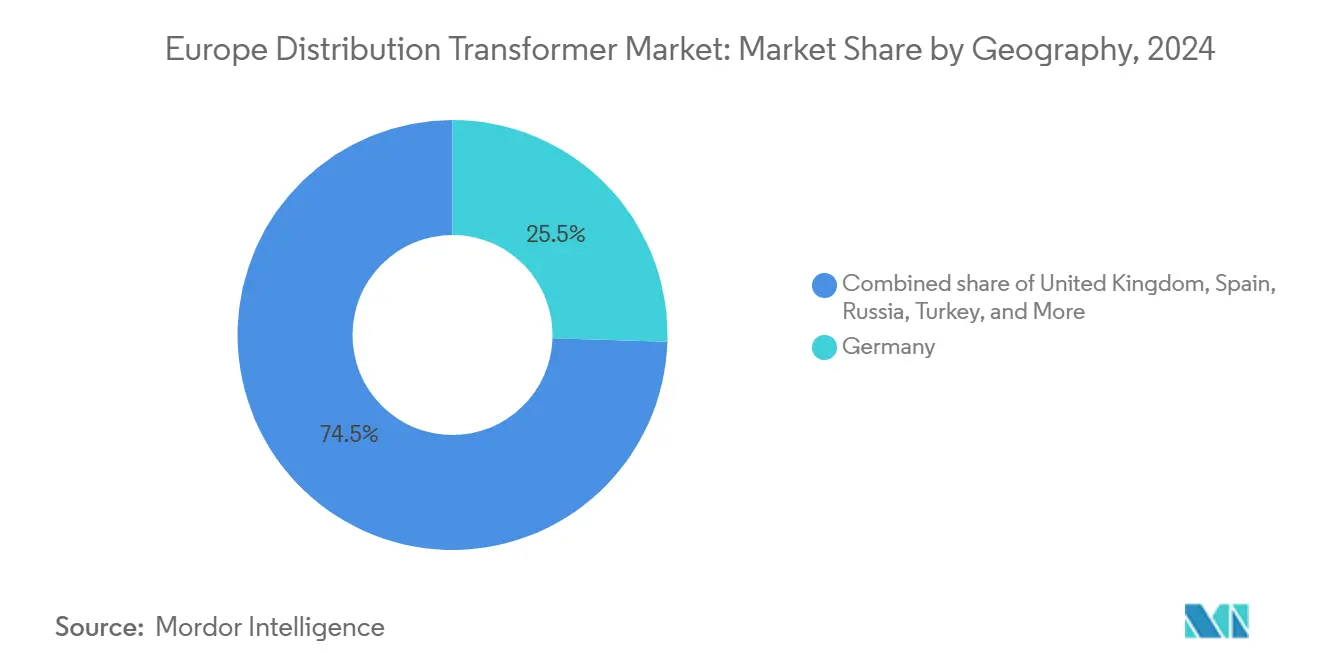

- By geography, Germany captured 25.12% of regional revenue in 2025; Russia is expected to grow the fastest at an 8.37% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Distribution Transformer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization capex rebound post-2024 | +1.8% | Germany, France, Spain, NORDIC Countries | Medium term (2-4 years) |

| EU Fit-for-55 energy-efficiency mandates | +1.2% | Global | Long term (≥ 4 years) |

| Surge in MV/LV transformer retrofits for data-centre clusters | +0.9% | Germany, NORDIC Countries, Netherlands | Short term (≤ 2 years) |

| EV-charge hub roll-outs under TEN-T corridors | +0.7% | Germany, France, Spain, Rest of Europe | Medium term (2-4 years) |

| Fast-tracking of rural RES hybrid micro-grids | +0.5% | Spain, NORDIC Countries, Rest of Europe | Long term (≥ 4 years) |

| Utility-led pilot uptake of biodegradable ester fluids | +0.3% | Germany, NORDIC Countries, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-modernization capex rebound post-2024

The European Investment Bank has earmarked EUR 100 billion (USD 107 billion) for 2025, setting aside EUR 11 billion (USD 11.8 billion) specifically for electrical grid upgrades. High-profile projects include the EUR 400 million (USD 428 million) Czech distribution upgrade and Iberdrola’s EUR 100 million (USD 107 million) redesign of the Valencia network. Such financing revives deferred utility projects, stimulating bulk procurement of medium-capacity units that match standardized, high-efficiency templates favored for rapid roll-out. As orders solidify, OEMs are ramping plant utilization across Germany, Poland, and Italy, shortening delivery cycles for the European distribution transformer market.

EU Fit-for-55 energy-efficiency mandates

The Fit-for-55 legislative package aims for a 55% reduction in greenhouse gases by 2030, compelling utilities to replace legacy Tier 1 equipment with Tier 2-compliant models and prepare for a likely Tier 3 by 2027.[2]Eurelectric, “Shortage of Grain-Oriented Electrical Steel,” eurelectric.org Transformer losses account for 93 TWh, or 2.9% of EU generation, providing a large technical savings pool. Utilities are therefore specifying amorphous-metal cores, advanced step-lap designs, and ester-filled tanks despite 15-20% higher upfront prices. The European distribution transformer market is experiencing longer tender horizons and value-based award criteria that prioritize life-cycle efficiency over initial cost.

Surge in MV/LV transformer retrofits for data-center clusters

Europe is expected to host nearly 25% of the new global hyperscale capacity planned for 2025-2027, with Germany and the Nordics competing for server-farm investment.[3]ENTSO-E, “Ten-Year Network Development Plan 2024,” entsoe.eu Operators require redundant 20-40 MVA feeds with online dissolved-gas monitoring to ensure 99.999% uptime, pushing specialized MV/LV transformer procurement. Digital-native designs with fiber-optic temperature sensors and partial-discharge analytics are gaining share, reinforcing premium pricing and accelerating product differentiation in the European distribution transformer market.

EV-charge hub roll-outs under TEN-T corridors

The TEN-T revision targets 55.6 GW of public charging by 2030, compared to 18 GW installed in 2024, implying more than 150,000 additional three-phase distribution transformers for highway fast-charge stations.[4]European Commission, “Revised TEN-T Regulation 2024,” ec.europa.eu Designs must tolerate load spikes and harmonics from megawatt chargers, prompting utilities to specify low-loss, high-impedance units with wide overload margins. Component lead times are lengthening, so charge-point operators are entering multi-year framework deals to secure their supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthening lead-times for electrical-steel laminations | -1.4% | Global | Short term (≤ 2 years) |

| Tightened noise & footprint limits in urban substations | -0.8% | Germany, France, United Kingdom, urban areas | Medium term (2-4 years) |

| Volatility in base-oil feedstock for mineral-oil transformers | -0.6% | Global, with acute impact in Germany, France, Spain | Short term (≤ 2 years) |

| CAPEX deferment amid DSOs' tariff-freeze negotiations | -0.4% | Germany, United Kingdom, France, Rest of Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthening lead-times for electrical-steel laminations

Global grain-oriented electrical-steel supply remains strained, with lead times stretching to 3-4 years and prices nearly doubling since 2020. Materials now represent 45% of the finished-unit cost, forcing manufacturers to ration allocations and favor high-margin orders. The bottleneck particularly affects the > 100 MVA category, potentially delaying large cross-border interconnection projects that drive demand for the European distribution transformer market.

Tightened noise & footprint limits in urban substations

Urban authorities in Germany, France, and the United Kingdom are imposing stricter 50-dB daytime noise caps and reducing permitted station footprints, which is driving the adoption of compact, low-sound transformers with advanced cooling and acoustic enclosures. Although the shift opens opportunities for dry-type and solid-state variants, higher engineering complexity and cost could deter budget-constrained municipal utilities, restraining growth in densely populated catchments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Grid upgrades tilt toward higher capacities

Small units (≤ 10 MVA) retained the largest 45.12% share of the European distribution transformer market in 2025, serving rooftop solar interconnections, mixed-use real estate electrification, and suburban feeders. Their short production cycles and catalog-based designs support quick deployment. However, capital-intensive transmission reinforcements under the ENTSO-E Ten-Year Network Development Plan are boosting demand for > 100 MVA equipment at a 6.74% CAGR. The European distribution transformer market size for large units is projected to reach USD 3.31 billion by 2031, driven by the development of new 400 kV corridors and offshore wind landing stations. Manufacturers are dedicating separate production halls and high-voltage test bays to shorten factory acceptance testing for these bespoke models. Utilities balance the higher ticket price with 40-year service life and lower relative losses, preserving total-cost-of-ownership economics.

By Cooling Type: Oil immersion dominates yet ester pilots multiply

Oil-cooled designs accounted for 79.85% of the revenue in 2025 and will remain the backbone, thanks to their thermal headroom and cost efficiency. OEMs are upgrading filtration and moisture-monitoring systems to extend oil life to 25 years, helping utilities justify replacements. Pilot projects using natural and synthetic esters are advancing. In 2025, R&S Group shipped a 40 MVA unit filled with Nytro BIO 300X to a Swedish utility, validating field performance. Ester's interest is strongest in fire-sensitive tunnels, ports, and urban substations, where the risk of mineral oil spills is unacceptable. Air-cooled units continue to serve metro rail, semiconductor fabs, and data halls that require zero flammability, but face margin pressure from rising silicon-steel prices. Innovation in solid-state transformer modules, funded by the EU SSTAR program, may open a future niche; however, the high cost keeps deployment marginal for now.

By Phase: Three-phase keeps grid supremacy

The three-phase topology accounted for 61.05% of shipments in 2025 and is forecast to grow at a 6.41% annual rate as utilities standardize on a balanced three-wire architecture for medium-voltage feeders. Digital protection relays and IEC 61850 communication layers are easier to implement on three-phase platforms, thereby reinforcing the preference for new substations. Single-phase designs sustain relevance in rural feeders, ground-mounted PV farms, and pole-mounted service transformers. Tender volumes remain stable, but price sensitivity is acute because small municipals often buy in batches of 10-20 units.

By End-User: Industry surges on electrification

Power utilities retained a 40.05% share of the European distribution transformer market in 2025, but industrial customers are expected to log the fastest 7.03% CAGR through 2031. Decarbonization roadmaps in the chemicals, steel, and food processing industries are shifting from fossil-fired heating to electric arc furnaces and high-temperature heat pumps, which demand additional medium-voltage capacity. OEMs are customizing cast-resin transformers with integrated arc-flash sensors for plant safety compliance. Commercial building retrofits and residential heat pump adoption sustain a steady volume, though average unit ratings remain below 2.5 MVA, limiting the revenue impact.

Geography Analysis

Germany generated 25.12% of Europe's distribution transformer market revenue in 2025, driven by the Energiewende and grid reinforcement, as well as offshore wind interconnections, such as the 5 GW NOR-3 cluster. The national regulator's focus on Tier 2-plus efficiency elevates demand for amorphous-core technology, supporting OEM margins. Bavaria, Baden-Württemberg, and North Rhine-Westphalia account for more than 60% of domestic orders due to their high industrial density. Persistent labor shortages, however, are driving up installed costs, prompting utilities to consider modular skid designs that are assembled offsite.

Russia posted the highest 8.37% CAGR outlook, despite geopolitical headwinds, driven by federal grants for electrification in the Far East and expansion of mineral processing. Domestic producers benefit from import substitution but still rely on European-made sensor packages, creating opportunities for selective export to EU suppliers. Energy-intensive metallurgy and oil refining remain core buyers of > 63 MVA step-down units. France and Spain together held 17.74% of regional sales in 2025. French demand centers on 20 kV feeder upgrades to accommodate rooftop solar, while Spain prioritizes rural hybrid microgrids that combine PV and battery storage. In both countries, noise-reduction mandates under local urban planning laws encourage the adoption of mid-power dry-type equipment. The United Kingdom channels investments into offshore wind landing points and London underground station refurbishments, maintaining a steady appetite for compact three-phase cast-resin designs. Nordic markets, although smaller, outpace the EU average growth as the Finland-Sweden Aurora Line and Baltic Sea HVDC projects trigger secondary substation additions. Turkey, straddling the EU and Middle East trade lanes, imports high-spec units for Istanbul metro extensions while growing a domestic assembly base in Izmir and Kocaeli.

Competitive Landscape

Supplier concentration is moderate: the five largest OEMs—Hitachi Energy, Siemens Energy, Schneider Electric, R&S Group, and SGB-SMIT—collectively controlled roughly 40% of 2024 deliveries. Acquisition activity is tightening the field; R&S Group’s USD 268 million takeover of Kyte Powertech in 2024 extended its footprint across Ireland and the UK, while Siemens Energy purchased a stake in KONČAR Transformer Tanks in 2025 to back-integrate enclosure fabrication. Capacity expansions are running in parallel: Siemens Energy is spending USD 235.4 million to increase Nuremberg output by 50% and add 350 staff, whereas Hitachi Energy has earmarked an additional USD 250 million in 2025 on top of a USD 1.5 billion global package to alleviate supply shortages. Smaller challengers, such as R&S Group’s new 10,000 m² Polish plant and Tamini’s bolt-on acquisition of Transformer Electro Service, illustrate regional scaling tactics. Competitive advantage is increasingly tied to digitalization: Schneider’s EcoStruxure Transformer Connect and Hitachi’s Lumada Asset Performance suites use embedded IoT sensors and AI-based analytics to offer predictive maintenance contracts. Compliance with ISO 14001 environmental management and IEC 61850 data models is now a prerequisite in major tenders, disadvantaging legacy designs.

Europe Distribution Transformer Industry Leaders

Hitachi Energy Ltd.

Siemens Energy AG

Schneider Electric SE

GE Vernova

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Siemens Energy committed EUR 220 million (USD 235.4 million) to double transformer capacity in Nuremberg and hire 350 staff.

- April 2025: R&S Group opened a 10,000 m² plant in Krzeczów, Poland, with an annual capacity exceeding 1,000 distribution units.

- April 2025: Siemens Energy finalized its entry into KONČAR Transformer Tanks to secure enclosure supply for European orders.

- March 2025: Hitachi Energy added USD 250 million for transformer capacity upgrades across its European sites.

Europe Distribution Transformer Market Report Scope

Distribution transformers are devices that step down the voltage at substations to deliver electricity to end customers. Distribution transformers provide the final voltage transformation in the electrical grid.

Europe's distribution transformer market is segmented by type, capacity, phase, and geography. By type, the market is segmented into oil-filled and dry types. By capacity, the market is segmented into below 500 kVA, 500 kVA - 2500 kVA, and above 2500 kVA. By phase, the market is segmented into single-phase and three-phase. The report also covers the market size and forecasts for the distribution transformer market across major countries in the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Power Rating

| Large (Above 100 MVA) |

| Medium (10 to 100 MVA) |

| Small (Up to 10 MVA) |

By Cooling Type

| Air-cooled |

| Oil-cooled |

By Phase

| Single-Phase |

| Three-Phase |

By End-User

| Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial |

| Commercial |

| Residential |

By Geography

| Germany |

| United Kingdom |

| France |

| Spain |

| NORDIC Countries |

| Turkey |

| Russia |

| Rest of Europe |

| By Power Rating | Large (Above 100 MVA) |

| Medium (10 to 100 MVA) | |

| Small (Up to 10 MVA) | |

| By Cooling Type | Air-cooled |

| Oil-cooled | |

| By Phase | Single-Phase |

| Three-Phase | |

| By End-User | Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial | |

| Commercial | |

| Residential | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Spain | |

| NORDIC Countries | |

| Turkey | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What was the value of the Europe distribution transformer market in 2026?

The market stood at USD 7.42 billion in 2026.

What CAGR is projected for European distribution transformers through 2031?

The market is expected to expand at 6.12% annually between 2026 and 2031.

Which power-rating segment is growing the fastest?

Units above 100 MVA are forecast to rise at a 6.74% CAGR.

Why are ester-filled transformers gaining traction?

Utilities are adopting biodegradable fluids to meet stricter environmental and fire-safety rules, especially in urban and sensitive locations.

Which country leads regional demand?

Germany commanded 25.12% of 2025 revenue thanks to large-scale grid modernization.

What is the main supply-chain bottleneck?

Limited availability of high-grade grain-oriented electrical steel is extending transformer lead times.

Page last updated on: