Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

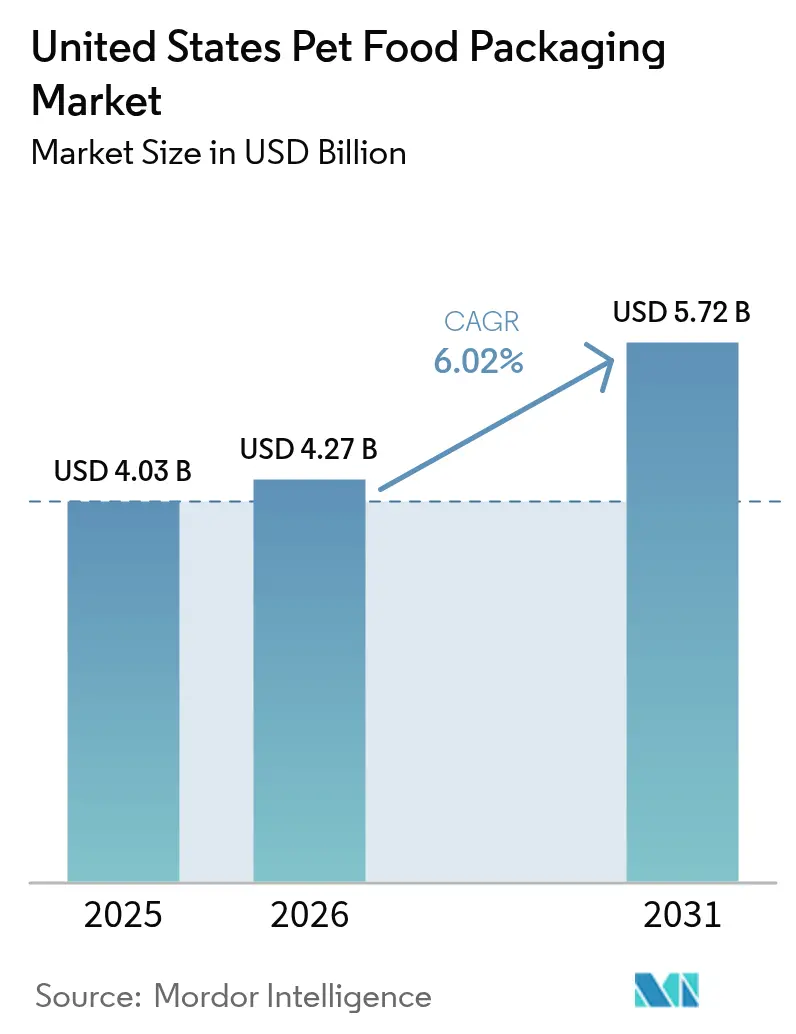

| Base Year Market Size (2025) | USD 4.03 Billion |

| Market Size (2026) | USD 4.27 Billion |

| Market Size (2031) | USD 5.72 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

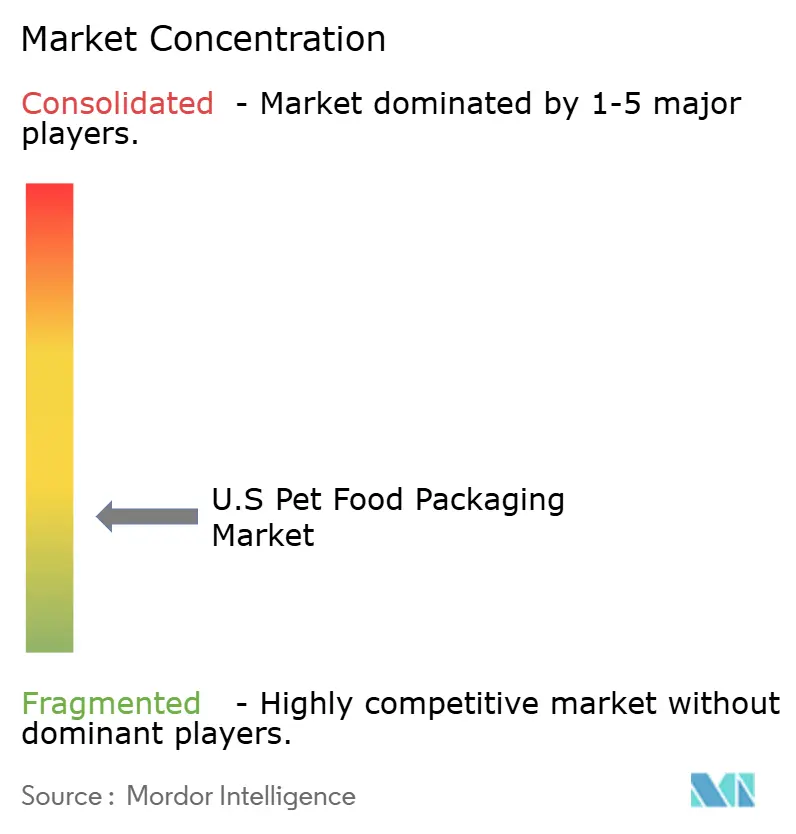

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Pet Food Packaging Market Analysis by Mordor Intelligence

The United States pet food packaging market size was valued at USD 4.03 billion in 2025 and estimated to grow from USD 4.27 billion in 2026 to reach USD 5.72 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031). Persistent regulatory scrutiny, rising sustainability expectations, and premium-brand competition are steering investment toward barrier-enhanced, recyclable formats. FDA’s 30-month extension of the Food Traceability Rule is giving manufacturers time to embed smart codes and serialized identifiers, while state-level PFAS bans are accelerating material changeovers toward fluorine-free barrier films.[1]FDA, “FDA Intends to Extend Compliance Date for Food Traceability Rule,” fda.gov E-commerce growth is intensifying demand for lightweight packs that can survive parcel-shipping stress without sacrificing shelf life. Simultaneously, raw-material cost spikes—polyethylene up 5¢/lb in January 2025 and corrugated cardboard up USD 70 per ton—are forcing converters to pursue downgauging, mono-material solutions, and vertical integration to protect margins.

Key Report Takeaways

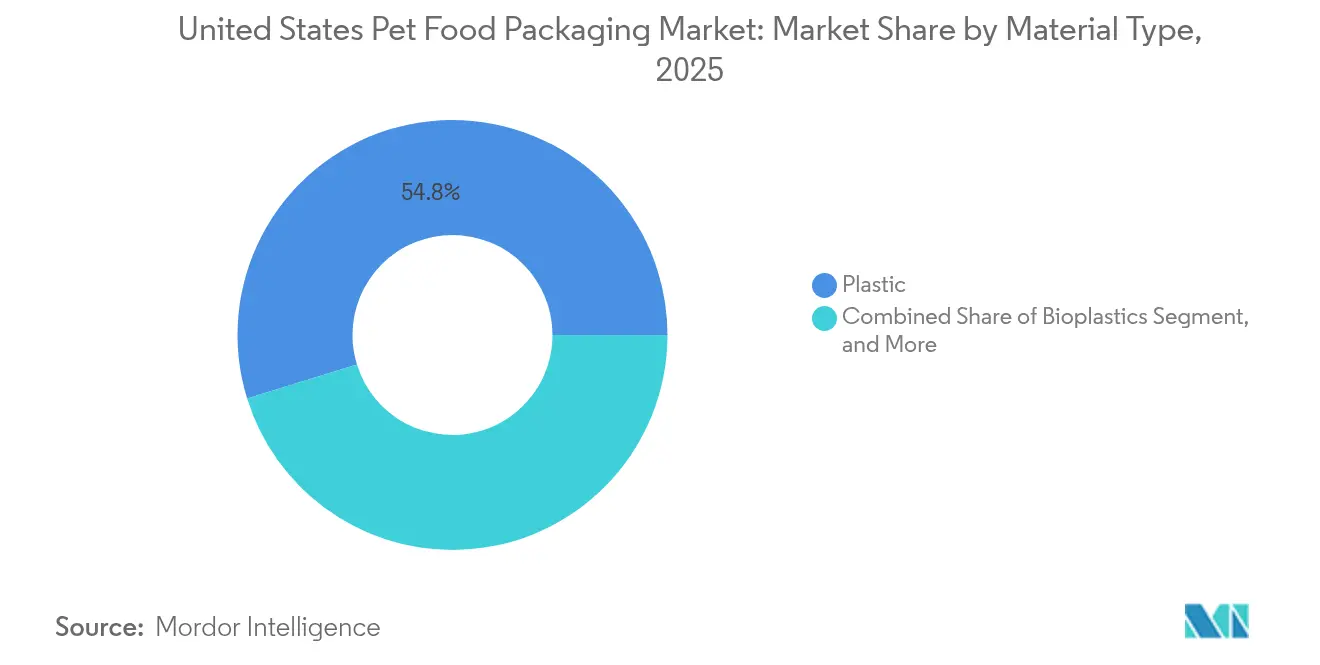

- By material type, plastic held 54.78% of the US pet food packaging market share in 2025, whereas bioplastics are projected to grow at a 9.05% CAGR to 2031.

- By product type, pouches accounted for 35.10% of the US pet food packaging market size in 2025 and are advancing at an 8.11% CAGR through 2031.

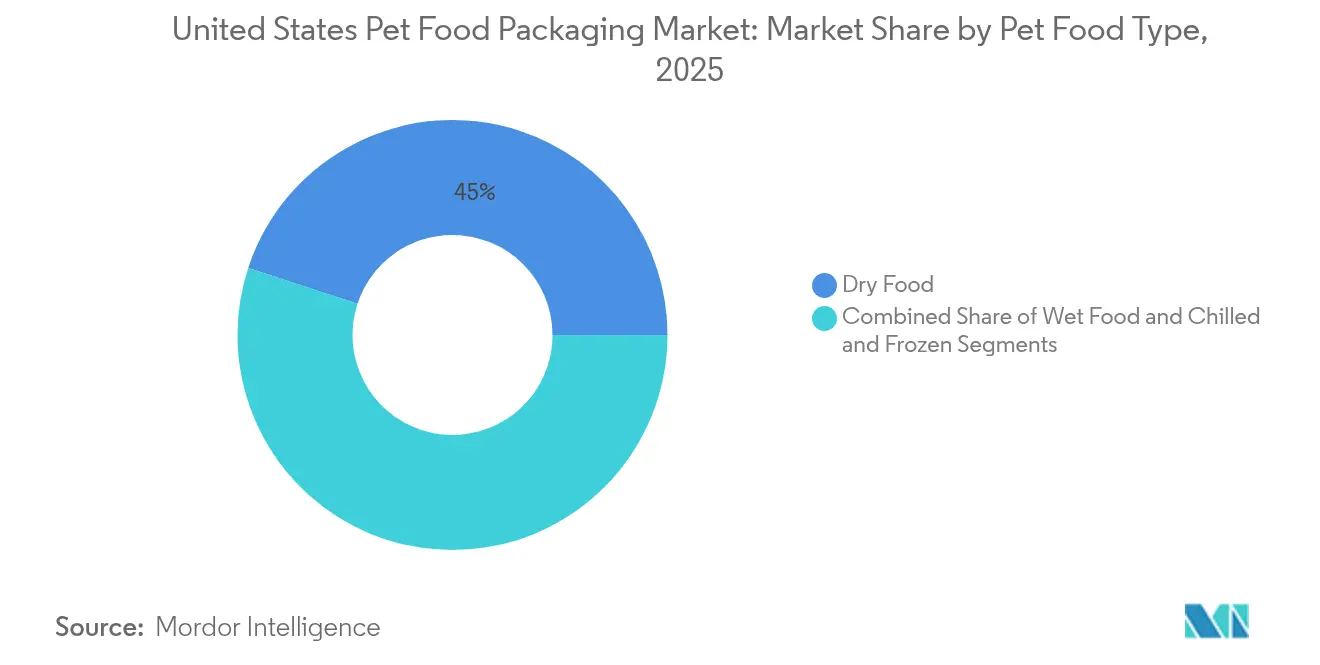

- By pet food type, dry food captured 44.95% of the US pet food packaging market share in 2025; wet food is forecast to expand at a 9.02% CAGR to 2031.

- By pet type, dog food led with 54.74% revenue share in 2025, while cat food is rising fastest at a 8.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Pet Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-brand focus on packaging differentiation | +1.2% | National, concentrated in urban markets | Medium term (2-4 years) |

| Functional/fortified foods need high-barrier packs | +0.8% | National, with premium segment focus | Long term (≥ 4 years) |

| E-commerce drives durable, lightweight formats | +1.5% | National, accelerated in suburban/rural areas | Short term (≤ 2 years) |

| FDA food-traceability rule pushes smart packs | +0.9% | National, phased implementation | Medium term (2-4 years) |

| Sustainability pledges spur mono-material films | +1.1% | National, driven by corporate commitments | Long term (≥ 4 years) |

| Rise of fresh/frozen meal subscriptions | +0.7% | National, concentrated in metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium-brand focus on packaging differentiation

Premium marketers are redesigning packs to defend price points and strengthen shelf stand-out. Merrick Pet Care’s 2024 overhaul replaced muted graphics with ingredient photography, resealable sliders, and fully printable gussets, which boosted on-shelf recognition and conveyed nutritional transparency. Brands are upgrading to matte-varnish laminations combining 40% post-consumer-recycled (PCR) content with clear windows so pet owners can inspect kibble freshness. With 70% of owners worried about rising prices, visual cues and functional closures become decisive value signals. Premium positioning also justifies added cost from multi-layer structures that offset a 28% surge in raw-material prices since 2021. The US pet food packaging market therefore sees a noticeable trading-up trend that favors innovative converters offering premium finishes.

Functional/fortified foods need high-barrier packs

Fortified recipes containing probiotics, omega oils, and heat-sensitive vitamins require oxygen transmission rates below 0.3 cc/m²-day, leading producers to migrate from standard coextrusions to vacuum-metallized films and retortable flexibles. Rhodes Pet Science’s Goodlands line adopted a Smart Trace Technology laminate that protects active ingredients while enabling batch-specific QR traceability through distribution. High-barrier adoption raises conversion complexity and creates moat effects for suppliers with extrusion-lamination depth. As functional SKUs claim higher margins, brand owners embrace the incremental pack cost, reinforcing a premiumization loop within the US pet food packaging market.

E-commerce drives durable, lightweight formats

Parcel shipping exposes packs to compression, drop, and vibration events exceeding ISTA 6 standards, propelling redesign toward reinforced seals and downgauged PE/PA blends. TC Transcontinental reports 40% cost reductions when using proprietary shrink-films that maintain pouch integrity under fulfilment center automation. Amcor’s labs now test flexibles against Amazon SIOC protocols, noting that many store-shelf packs fail after three drops.[2]Amcor, “The Growing Importance of Recyclable Pet Food Packaging,” amcor.comSubscription models favor flat-bottom pouches with portion-control markings and easy-tear notches. The US pet food packaging market therefore channels R&D funds into impact resistance and cube efficiency for omnichannel commerce.

FDA food-traceability rule pushes smart packs

Although pet food is not on FDA’s Food Traceability List, manufacturers are pre-emptively embedding GS1 Digital Link QR codes to build readiness and satisfy retailer scorecards. BL.INK’s pilot showed line-speed serialization at 600 packs per minute without bottlenecks, delivering harvest-to-bowl provenance in seconds during recall drills. Smart codes double as consumer-engagement portals, offering feeding guides and recycling instructions—features that resonate with digitally savvy pet parents. As compliance deadlines draw closer, smart printing capacity becomes a competitive lever within the US pet food packaging market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trade-off between sustainability and shelf-life | -0.8% | National, affecting premium segments | Medium term (2-4 years) |

| Volatile resin and metal input prices | -1.3% | National, supply chain dependent | Short term (≤ 2 years) |

| State-level PFAS packaging bans | -0.6% | State-specific, expanding nationally | Short term (≤ 2 years) |

| Weak film-recycling infrastructure | -0.4% | National, rural areas most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Trade-off between sustainability and shelf-life

Mono-material PE pouches are welcomed by recyclers yet often compromise grease and oxygen barriers essential for meat-based formulas. The EPA estimates USD 36.5–43.4 billion is required to modernize US recycling infrastructure, underscoring a systemic gap that slows eco-design adoption. Amcor’s recyclable retort pouch took years of heat-seal R&D to match legacy aluminum-foil performance. Meanwhile, 300 million lb of pet-food flexible waste enters landfills annually, stoking NGO pressure for rapid change. Brand owners are navigating formulation adjustments, additive barrier coatings, and cost premiums that weigh on the growth outlook for the US pet food packaging market.

Volatile resin and metal input prices

January 2025 saw high-density polyethylene jump 5¢/lb, while aluminum sheet quotes spiked 15-20% after new tariffs. Corrugated cardboard climbed USD 70/ton, straining secondary-pack budgets. Converters are countering with light-weighting, recycled content, and long-term resin hedges, but volatility siphons capital from innovation budgets. Frequent price renegotiations unsettle brand-converter relations, introducing forecasting uncertainty across the US pet food packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastic Dominance Faces Bioplastic Disruption

Plastic accounted for 54.78% of the US pet food packaging market in 2025, led by PE and PP laminations prized for cost-effective barrier performance. Bioplastics, however, are scaling fastest at a 9.05% CAGR as brands align with zero-carbon pledges and PFAS exit deadlines. Coca-Cola’s demo of 100% bio-PET illustrates upstream momentum likely to influence pet-sector resin availability. Siegwerk’s oil-resistant mono-PE ink system removes the need for aluminumized layers, aligning with curbside-collection criteria. The US pet food packaging market size for bioplastics is expected to close the cost gap as fermentation yields improve and carbon-credit subsidies expand.

Regulatory headwinds hasten material shifts. Eleven states now restrict PFAS, forcing converters to test nanoporous silica, EVOH, and metallized OPP as substitute barriers. While incumbent multi-material films still dominate wet-food lines, R&D spend is tilting toward recyclable mono-structures anticipated to meet 2027 corporate sustainability targets. Supply-chain resilience further validates domestic PET and PCR supply deals, reducing exposure to freight volatility from Asia.

By Product Type: Pouches Lead Innovation and Growth

Pouches held 35.10% of the US pet food packaging market size in 2025 and are registering an 8.11% CAGR through 2031 due to their balance of barrier protection, shelf impact, and lower logistics cost. Quad-seal and flat-bottom formats provide billboard space for nutritional claims while maintaining cube efficiency. TC Transcontinental’s vieVERTe range integrates 30% PCR and meets How2Recycle “Store Drop-off” requirements. Bags and sacks remain essential for value-oriented bulk dry food, but their CAGR trails at low single digits.

Pouch formats also underpin direct-to-consumer subscriptions, enabling portion control and freshness seals critical for premium positioning. ProAmpac’s thermochromic inks alert owners to temperature abuse during delivery, while integrated humidity absorbers prolong kibble crunch. As omnichannel sales grow, rigid cans cede share except where retort heat requirements persist. The US pet food packaging market therefore rewards converters fluent in both flexible design and end-of-life validation.

By Pet Food Type: Wet Food Growth Outpaces Dry Food Dominance

Dry food still represented 44.95% market share in 2025, benefiting from established extrusion lines and ambient storage logistics. Wet food, though smaller, is expanding at 9.02% CAGR as owners seek higher moisture diets that mimic ancestral feeding. Tetra Recart cartons reduce freight emissions by packing 10 times more empties per pallet than cans while cutting carbon footprint 72%. Wet formulations demand oxygen and light barriers, steering packaging into retortable pouches and lacquered steel cans.

Chilled and frozen meals are the smallest slice but display double-digit growth alongside fresh-food subscriptions. The Farmer’s Dog ships recyclable cardboard shippers with water-soluble insulation and BPA-free barrier packs that meet doorstep-delivery durability. Cold-chain integrity requirements spark innovation in vacuum-skin packs and compostable bio-liners, offering new revenue nodes within the US pet food packaging market.

By Pet Type: Cat Food Growth Challenges Dog Food Leadership

Dog food dominated with 54.74% share in 2025 due to higher consumption volumes per animal and dense retail distribution. Yet cat food is accelerating at 8.86% CAGR as feline ownership rises in urban apartments and owners trade up to functional formulas. Amcor’s survey found 90% of pet owners willing to pay more for sustainable packs, with cats driving the highest switch intention. Portion-controlled, easy-tear pouches suit smaller daily servings, while aluminum trays with peelable lidding create premium single-meal experiences.

Bird, fish, and small-animal categories remain niche but require moisture-barrier sachets and oxygen-scavenger labels to maintain seed and flake freshness. These specialized lines offer margin upside for contract packers that can accommodate shorter runs, expanding the overall opportunity landscape in the US pet food packaging market.

Geography Analysis

Manufacturing footprints cluster around grain belts and intermodal corridors in the Midwest and Southeast. Mars Petcare’s Mattoon, Illinois plant remains the continent’s largest dry-food facility, while Nestlé Purina’s USD 450 million Eden, North Carolina site added 1.3 million ft² of automated capacity in 2024. Forty-three major producers anchor operations within a 600-mile radius of corn-soy feedstock supply, reducing inbound freight and supporting just-in-time film deliveries.

Regulatory diversity shapes packaging decisions. California’s AB 1200 prohibits PFAS in food packaging, pushing nationwide pack redesign because national brands avoid dual SKUs. Washington State takes a phased safer-alternative approach, signaling a likely tightening of permissible barrier chemistries. The US pet food packaging market thus converges on solutions meeting the strictest state mandates to preserve scale economics.

Distribution strategy is evolving. Blue Buffalo’s 730,000 ft² Olathe, Kansas warehouse centralizes inventory for two-day delivery across 85% of the population. E-commerce growth in the Southeast and Southwest triggers regional fulfillment center builds, incentivizing local pouch-printing capacity to shorten lead times. These geographic patterns reinforce a resilient supply network that underpins long-run growth of the US pet food packaging market.

Competitive Landscape

The market remains moderately fragmented, with converters jockeying for innovation leadership while pursuing consolidation to secure volume leverage. Sonoco’s USD 3.9 billion acquisition of Eviosys in 2024 created the world’s largest metal food-can platform, unlocking cross-selling to pet-food retort customers and an expected USD 100 million in synergies.[3]Sonoco Products Company, “Sonoco to Acquire Eviosys,” sonoco.com Crown Holdings responded by installing high-speed can lines in Minnesota and Pennsylvania dedicated to pet-food customers, aiming to shave six weeks off lead times.

Technology investments differentiate players. TOPPAN Holdings’ USD 1.8 billion purchase of Sonoco’s Thermoformed & Flexible Packaging business grants access to PCR-rich mono-material IP and a foothold in North American pet-food accounts. Huhtamaki’s new CEO pledged accelerated R&D spending on recyclable barrier films and design-for-recycling consultation services. Contract-pack specialists such as PurPak group are adding freeze-dry lines with integrated pouching to court boutique premium brands.

Start-ups target sustainability white space. Flexible-film newcomers promote water-soluble barrier coatings and compostable bio-resins certified for pet-food contact, betting on retailer mandates for recyclable packaging by 2027. Legacy players counter with in-house recycling pilots and mass-balance PCR sourcing. Competitive intensity therefore pivots on the ability to reconcile cost, barrier integrity, and recyclability within the evolving rules of the US pet food packaging market.

United States Pet Food Packaging Industry Leaders

Amcor Plc.

Sonoco Products Company

Mondi Group

Huhtamaki Oyj

Smurfit WestRock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Huhtamaki appointed Ralf K. Wunderlich as President and CEO to drive sustainable-packaging growth initiatives.

- January 2025: PurPak Group began installing an optimized packaging line for freeze-dried pet food.

- December 2024: TOPPAN Holdings closed its USD 1.8 billion acquisition of Sonoco’s Thermoformed & Flexible Packaging business.

- June 2024: Sonoco agreed to acquire Eviosys for approximately USD 3.9 billion.

United States Pet Food Packaging Market Report Scope

Packaging is vital in the modern food industry and plays a crucial role in influencing consumers' buying decisions. Packaging imagery and design are the primary instruments to convey a company's core value to the targeted consumer base. Pet food packaging must anticipate the reactions of pet owners about the graphics, colors, and utility factors. The report offers a comprehensive analysis of the United States Pet Food Packaging Market is segmented by material type, product type, pet food type, and the type of animal.

By Material Type

| Paper and Paperboard |

| Plastic |

| Metal |

| Bioplastics |

By Product Type

| Pouches |

| Bags and Sacks |

| Metal Cans |

| Other Product Type |

By Pet Food Type

| Dry Food |

| Wet Food |

| Chilled and Frozen |

By Pet Type

| Dog Food |

| Cat Food |

| Bird Food |

| Fish Food |

| Other Pet Type |

| By Material Type | Paper and Paperboard |

| Plastic | |

| Metal | |

| Bioplastics | |

| By Product Type | Pouches |

| Bags and Sacks | |

| Metal Cans | |

| Other Product Type | |

| By Pet Food Type | Dry Food |

| Wet Food | |

| Chilled and Frozen | |

| By Pet Type | Dog Food |

| Cat Food | |

| Bird Food | |

| Fish Food | |

| Other Pet Type |

Key Questions Answered in the Report

What is the current value of the US pet food packaging market?

The market is worth USD 4.27 billion in 2026 and is forecast to reach USD 5.72 billion by 2031 at a 6.02% CAGR.

Which packaging format is growing fastest?

Pouches are expanding at an 8.11% CAGR because they deliver barrier protection, convenience, and e-commerce durability.

How are PFAS bans influencing material choice?

State-level PFAS restrictions are pushing converters toward fluorine-free barrier technologies such as EVOH-coated films and recyclable mono-PE structures.

Why is cat food packaging growing quicker than dog food?

Feline ownership is rising in urban areas, and owners prefer premium single-serve wet formats that demand high-barrier, portion-controlled packaging.

What role does the FDA’s traceability rule play in packaging?

Although pet food is not yet on the mandatory list, brands are adopting smart codes to future-proof compliance and enhance recall readiness.

How are raw-material price swings affecting innovation?

Volatile resin and metal costs divert capital from R&D, prompting converters to emphasize light-weighting and PCR use to offset margin pressure.

Page last updated on: