Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

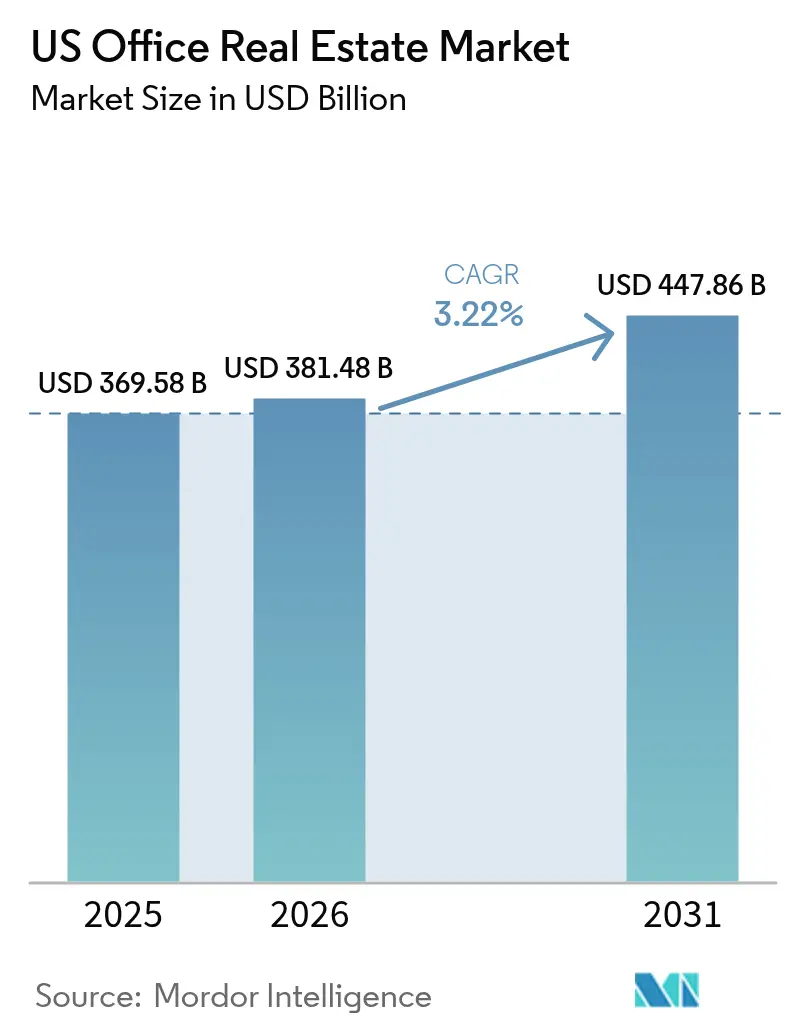

| Base Year Market Size (2025) | USD 369.58 Billion |

| Market Size (2026) | USD 381.48 Billion |

| Market Size (2031) | USD 447.86 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

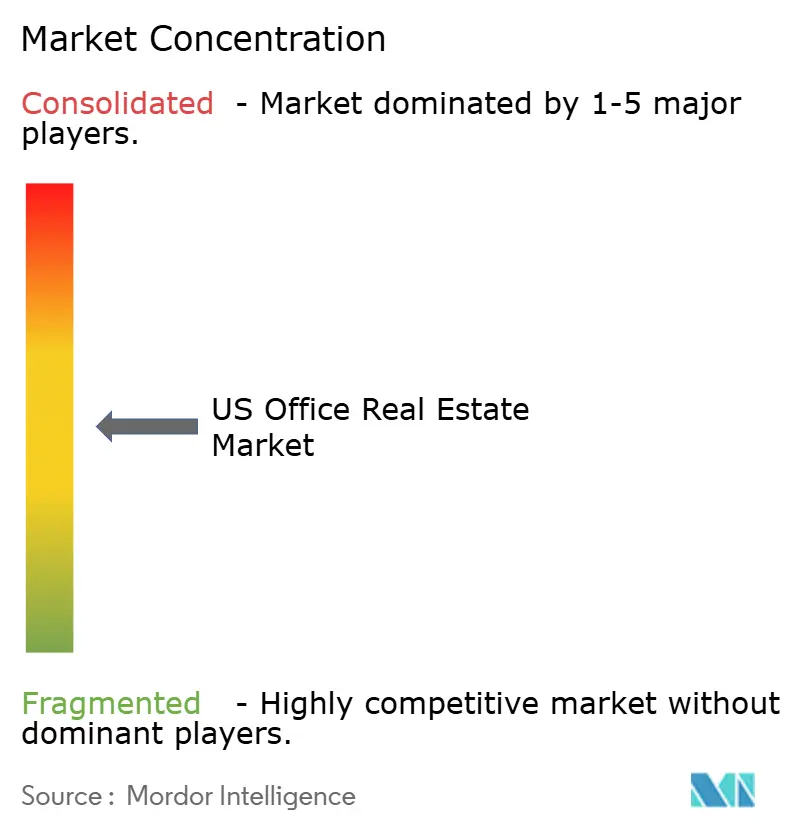

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Office Real Estate Market Analysis by Mordor Intelligence

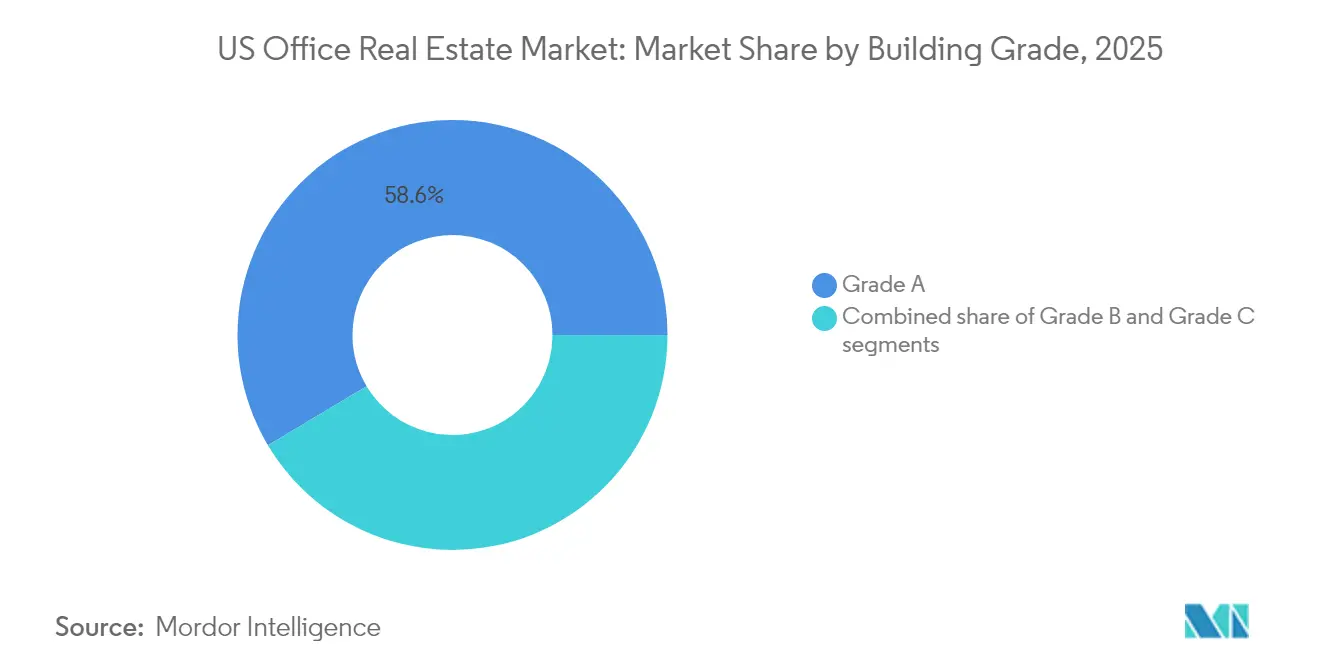

The US Office Real Estate Market size was valued at USD 369.58 billion in 2025 and estimated to grow from USD 381.48 billion in 2026 to reach USD 447.86 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031). Tenant “flight-to-quality” continues to reshape demand as premium, sustainable buildings absorb space while secondary assets struggle to retain tenants. Grade A properties already command 58% of occupied stock and capture nearly all positive net absorption, highlighting a decisive pivot from cost efficiency toward workplace experience. Flexible leasing, resilient demand from knowledge-intensive sectors, and infrastructure upgrades in transit-served districts further bolster the United States office real estate market despite elevated financing costs. At the same time, the bifurcation between prime and obsolete space widens as sustainability mandates accelerate retrofit requirements and hybrid work suppresses demand for outdated suburban offices.

Key Report Takeaways

- By building grade, Grade A stock held 58.56% of the United States office real estate market share in 2025, while Grade A space is projected to expand at a 3.76% CAGR to 2031.

- By transaction type, the rental segment captured 68.21% revenue share in 2025; sales transactions recorded the fastest 3.66% CAGR through 2031.

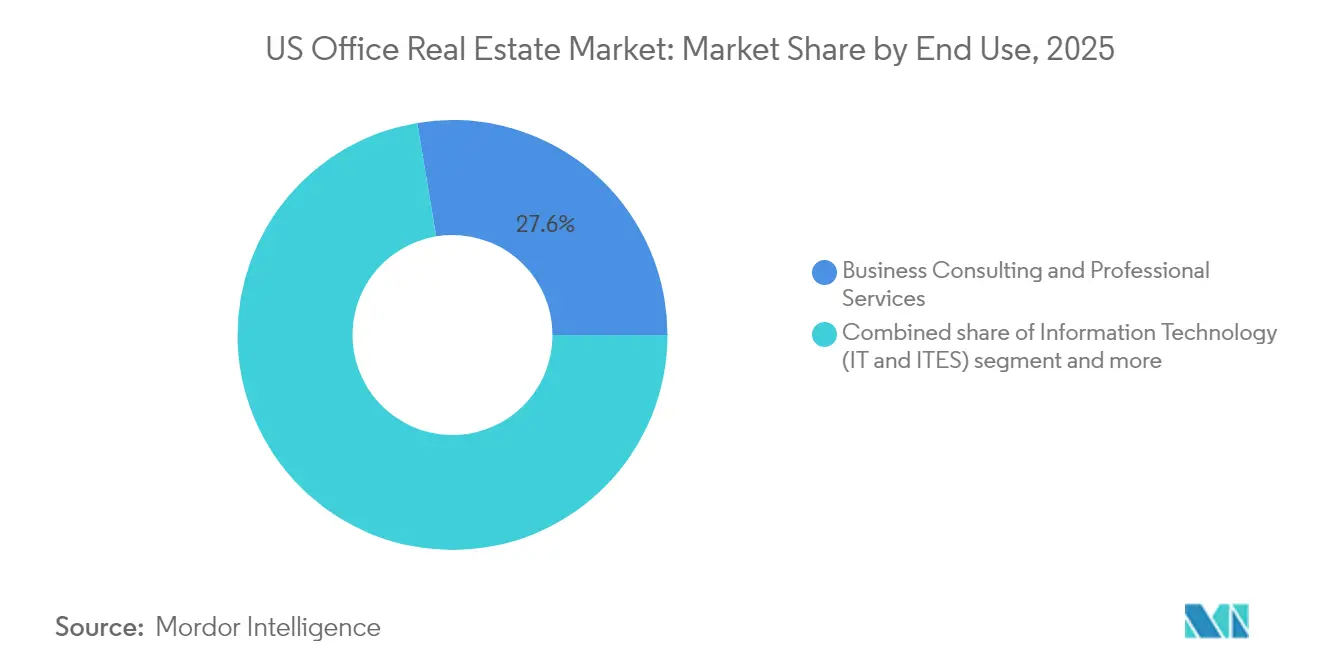

- By end use, Business Consulting & Professional Services accounted for 27.62% share of the United States office real estate market size in 2025, whereas Information Technology advances at a 3.88% CAGR between 2026-2031.

- By state, New York led with a 23.65% share in 2025, while Texas posts the highest forecast growth at 4.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tenant preference for Class A and sustainable buildings | +0.8% | National, strong in New York, San Francisco, Austin | Medium term (2-4 years) |

| Leasing demand from tech, healthcare & finance | +0.7% | Major metropolitan areas | Short term (≤ 2 years) |

| Sustainability mandates and green retrofits | +0.6% | Federal assets set the tone nationwide | Long term (≥ 4 years) |

| Growth of flexible and short-term leases | +0.5% | Secondary markets show higher uptake | Medium term (2-4 years) |

| Urban infrastructure upgrades | +0.4% | Transit-connected CBDs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Tenant Preference for Class A and Sustainable Buildings

Premium offices now serve as recruitment tools that enhance productivity, pushing occupiers to prioritize building quality over rent savings. The General Services Administration’s requirement for LEED Gold certification in new federal projects signals a market-wide baseline for quality and sustainability. Owners of certified assets realize stronger rent growth because tenants view environmental credentials as integral to corporate ESG targets. Prime urban buildings with energy-efficient systems and proximity to transit record higher occupancy and command longer lease commitments. Obsolete assets lacking these features face value erosion, reinforcing the bifurcation within the United States office real estate market.

Leasing Demand Supported by Resilient Sectors

Technology, healthcare, and finance collectively drove more than half of 2024 leasing activity, dispelling fears of structural office demand collapse. Amazon’s 141,000 sq ft Silicon Valley lease with WeWork underscores selective tech expansion in premium space. Financial institutions maintain physical footprints to satisfy regulatory and client interaction needs. Healthcare providers require specialized office layouts to integrate telehealth with in-person services, sustaining demand even as other sectors downsize. The United States office real estate market thus benefits from a resilient core of industries that continue to lease high-specification space.

Increased Adoption of Flexible and Short-Term Lease Structures

Corporate real estate heads seek agility, replacing decade-long leases with terms that include contraction and expansion clauses. In 2024, 42% of occupiers incorporated flexible space into their portfolios, a structural shift rather than a pandemic-era anomaly. Landlords offering turnkey suites and plug-and-play floors capture higher occupancy and can charge rent premiums for optionality. The trend is especially pronounced in secondary markets where tenants value flexibility to scale as local labor pools grow. This leasing innovation underpins stable cash flows for adaptable landlords across the United States office real estate market.

Infrastructure Upgrades Improving Office Accessibility

Transit investments in New York, Chicago, and Austin enhance last-mile connectivity and raise the desirability of adjacent office blocks. Accessibility is paramount in a hybrid work setting where employees commute fewer days but expect convenience when they do. Districts tied into upgraded subway stations or bus rapid transit lines post noticeably faster rent growth and absorption than car-dependent submarkets. City governments increasingly bundle office permits with mobility upgrades, aligning public and private capital to rejuvenate downtowns. These synergies reinforce location premiums in the United States office real estate market.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated vacancy in outdated & suburban stock | -0.9% | Suburban & secondary CBDs | Medium term (2-4 years) |

| High interest rates & tight financing | -0.8% | National, leveraged deals | Short term (≤ 2 years) |

| Delayed return-to-office enforcement | -0.6% | Gateway cities most affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Vacancy Rates in Outdated and Suburban Offices

Functional obsolescence accelerates for buildings with inefficient layouts, limited technology infrastructure, or poor ESG credentials. National vacancy hit record highs in early 2025, with Class C suburban parks posting double-digit vacancy premiums over downtown Class A stock. Reduced daily commuting weakens footfall that once supported suburban retail amenities, further depressing tenant demand. Landlords face difficult investment decisions: undertake expensive upgrades or accept declining cash flows. The drag from obsolete space tempers overall growth in the United States office real estate market[1]Lawrence Yun, “Commercial Real Estate Market Insights January 2025,” National Association of Realtors, nar.realtor.

Delayed Return-to-Office Trends Hindering Space Absorption

Only 17% of firms enforce attendance rules despite 80% having formal policies, keeping average physical occupancy below 50%. This “shadow vacancy” delays lease restructurings as tenants hesitate to commit to long-term footprints[2]Thomas Bisacquino, “Office Space Demand Forecast Q2 2025,” NAIOP Research Foundation, naiop.org. Landlords must recalibrate revenue forecasts, stretching payback periods on capital projects. The uncertainty also weighs on investor sentiment, widening bid-ask spreads for transactions. These dynamics restrain short-term momentum within the United States office real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Assets Consolidate Power

Grade A buildings represented 58.56% of occupied stock in 2025, underscoring their dominance within the United States office real estate market. Prime assets posted 3.76% forecast CAGR through 2031—well above the broader market—due to a decisive flight-to-quality by tenants. Positive net absorption for Grade A space surpassed 2 million sq ft in Q1 2025, even as overall market absorption remained flat. The United States office real estate market size for Grade A assets is therefore positioned to expand faster than any other grade category over the forecast horizon.

Superior HVAC systems, touchless technologies, and wellness amenities turn premium workplaces into strategic talent-retention tools. Public-sector standards such as the GSA’s LEED Gold requirement converge with private-sector ESG targets to cement Grade A credentials as the default specification for large occupiers. Investors harness this momentum, funneling capital into trophy towers and core-plus refurbishments, while pricing discounts for secondary assets widen. Consequently, premium stock is likely to seize a larger United States office real estate market share as obsolete buildings exit competitive inventory.

By Transaction Type: Rental Dominance Sustained

Rental agreements controlled 68.21% of transaction value in 2025, affirming their preeminence in the United States office real estate market. Despite that dominance, sales transactions exhibit a stronger 3.66% CAGR through 2031 as opportunistic investors hunt value. The United States office real estate market size attached to rental contracts continues to grow steadily because corporate balance-sheet flexibility outweighs ownership allure in a volatile economic backdrop.

Large renewal deals—68 of the 100 biggest transactions in 2024—illustrate tenant preference for known buildings, upgraded amenities, and landlord concessions over relocation risk. Meanwhile, well-capitalized real estate investment trusts issue unsecured notes, such as BXP’s USD 850 million bond, to fund acquisitions during price dislocations. The coexistence of dominant rentals and accelerating sales highlights a maturing United States office real estate market where leasing and investing serve complementary strategic purposes.

By End Use: Professional Services Anchor Demand

Business Consulting & Professional Services held the largest 27.62% share in 2025, reinforcing the sector’s pivotal role in the United States office real estate market. Information Technology, the fastest-growing end-user segment, is projected to expand at a 3.88% CAGR to 2031 as tech giants selectively add premium space in innovation hubs. The United States office real estate market size attributable to professional services remains stable because these firms rely on client-facing collaboration that favors central locations.

Professional-services occupiers optimize layouts by integrating flexible meeting zones and digital collaboration suites, keeping footprints lean yet high quality. Tech firms, by contrast, consolidate secondary locations while expanding downtown hubs, as shown by Google’s pivot from One Market Plaza to 345 Spear Street. Banking, insurance, and asset-management companies maintain steady leasing tied to compliance requirements and client interactions. Together, these knowledge-based industries underpin revenue stability for landlords in the United States office real estate market.

Geography Analysis

New York retained a commanding 23.65% share in 2025, reflecting its magnetic pull as a global finance and media capital. Twenty-four of the 100 largest office leases last year took place in Manhattan, underscoring sustained appetite for centrally located, transit-rich space even as hybrid work endures. Prime buildings near Penn Station and Grand Central secure the highest rentals because employees value short commute times and abundant neighborhood amenities. Still, elevated operating costs and tax burdens are prompting some firms to explore lower-cost alternatives, pressuring New York landlords to invest aggressively in amenities and ESG upgrades.

Texas charts the fastest 4.15% CAGR through 2031, propelled by corporate relocations to Austin, Dallas, and Houston. Advantageous tax structures, affordable housing, and deep engineering talent pools attract both financial services and technology firms seeking to scale efficiently. Infrastructure investments like Austin’s Project Connect light-rail system further boost office demand by improving access to emerging districts. As a result, the United States office real estate market in Texas is likely to close a portion of the share gap with coastal gateways over the forecast period.

California remains a heavyweight, its performance linked closely to technology sector fortunes in Silicon Valley and media expansion in Los Angeles. Although several tech companies trimmed excess suburban campuses, demand for top-tier collaboration hubs in downtown San Francisco and Sunnyvale persists. Florida leverages favorable tax policy and Miami’s status as a Latin American finance gateway to attract new investment, while Illinois capitalizes on Chicago’s logistics network and diversified economy to retain occupiers. Collectively, these dynamics point to a geographic rebalancing where Sun Belt growth complements the enduring appeal of legacy coastal centers, shaping a more polycentric United States office real estate market.

Competitive Landscape

The US office real estate market is moderately concentrated, with a mix of national REITs, regional developers, and private equity funds vying for tenants through amenity upgrades and sustainability credentials. Large listed landlords such as BXP, SL Green, and Vornado dominate core coastal markets, whereas regionally focused operators maintain an edge in fast-growing Sun Belt cities. Differentiation hinges less on headline rent and more on tenant experience, ranging from smart-building technologies to hospitality-grade services that entice staff back on site.

A clear “flight-to-quality” strategy shapes portfolio actions: BXP’s USD 850 million unsecured note issue funds core acquisitions while divestments target non-core suburban holdings. Blackstone’s USD 4 billion all-cash purchase of ROIC illustrates institutional appetite for repositioning edge-city assets into mixed-use complexes. Meanwhile, flexible-workspace providers partner with owners to operate turnkey floors, enabling landlords to meet tenant agility demands without cannibalizing long-term leases.

Technology is now a decisive battleground. Sensors that monitor air quality, desk occupancy, and energy consumption deliver data-driven optimization and ESG reporting, giving tech-forward buildings a marketing edge. Sustainability retrofits also influence refinancing terms; Office Properties Income Trust renegotiated USD 340 million in notes partly by showcasing its green-building roadmap. As capital gravitates toward premium, future-ready assets, weaker owners of obsolete stock face strategic crossroads—either pursue capital-intensive upgrades or exit at discounts, thereby reinforcing a two-tier competitive structure across the United States office real estate market.

US Office Real Estate Industry Leaders

BXP, Inc.

SL Green Realty Corp.

Brookfield Properties

Vornado Realty Trust

Kilroy Realty Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon leased 141,000 sq ft from WeWork in Silicon Valley to support its return-to-office mandate.

- April 2025: CBRE reported 2.3 million sq ft of positive net absorption in Q1 2025, the fourth straight quarter of demand growth.

- February 2025: The GSA issued new PBS Core Building Standards emphasizing energy efficiency for all federal projects under 50% completion.

- January 2025: BXP finalized a 246,000 sq ft 20-year renewal and expansion with KnitWell Group at 7 Times Square, New York.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the United States office real estate market as the yearly dollar value generated when completed, income-producing office buildings, ranging from multi-tenant CBD towers to suburban flex stock, are leased, re-leased, or sold across all fifty states.

Scope exclusions: Spaces under construction, owner-occupied headquarters, medical or life-science offices, and assets already converted to residential use are not counted.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Life-science, Energy, Legal)

- By States

- Texas

- California

- Florida

- New York

- Illinois

- Rest of US

Detailed Research Methodology and Data Validation

Primary Research

We interviewed investment managers, brokerage directors, corporate occupiers, and prop-tech vendors from the Northeast, Sun Belt, Midwest, and West Coast. Their feedback confirmed vacancy reconciliation rules, clarified premium adjustments for LEED-Gold stock, and highlighted early rent pushback in secondary metros.

Desk Research

The baseline begins with public datasets. Analysts compile quarterly absorption, vacancy, and rent files from the U.S. Census Economic Indicators, Bureau of Labor Statistics, Federal Reserve flow-of-funds tables, and Securities and Exchange Commission 10-Ks. Industry bodies such as the National Association of Realtors, NAIOP, and the Building Owners & Managers Association publish construction cost indices and permitting trends that sharpen metro-level calibrations.

Mordor's access to D&B Hoovers, Dow Jones Factiva, and Questel enriches the desk review with company deal values, real-time news flow, and smart-building patent counts that hint at future demand. The sources named are illustrative; many additional databases and government dashboards inform data gathering, validation, and context building.

Market-Sizing & Forecasting

A top-down build reconstructs annual transaction pools from recorded leased area multiplied by metro-specific effective rents and cross-checks those totals with deed values and capital-market flows, followed by selective bottom-up roll-ups of Grade-A inventories to expose gaps. Key drivers include office-using employment growth, absorption-to-construction ratios, cap-rate spreads, vacancy normalization velocity, retrofit tax incentives, and hybrid-work attendance metrics. A multivariate regression fed with these variables produces the 2025-2030 outlook, while scenario analysis captures shifts in hybrid adoption.

Data Validation & Update Cycle

Parallel analysts run variance checks against NAIOP demand forecasts, CBRE rent trackers, and GAO vacancy alerts, flagging discrepancies above three percentage points. Senior reviewers resolve anomalies before sign-off. The model refreshes every twelve months, with interim updates when policy or rate shocks materially alter the outlook.

Why Mordor's US Office Real Estate Baseline Commands Reliability

Published market estimates often diverge; figures swing because publishers mix asset valuations, leasing flows, and pipeline stock in different ways. By focusing on transacted or leased space only and refreshing annually, Mordor Intelligence supplies a value traceable to verifiable records rather than book-value extrapolations.

Other studies inflate totals by folding in owner-occupied towers, medical offices, or undiscounted book values, while a few understate the market by tracking deed transfers alone or smoothing data through long moving averages. Mordor keeps scope tight, variables current, and assumptions transparent, which delivers a balanced midpoint clients can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 369.58 bn (2025) | Mordor Intelligence | - |

| USD 1.20 tn (2024) | Global Consultancy A | Counts owner-occupied and medical stock; relies on asset book values; irregular refresh |

| USD 135.37 bn (2025) | Trade Journal B | Tracks only closed sales and leases; excludes build-to-suit and pipeline assets |

| USD 1.50 tn (2025) | Data Aggregator C | Estimates standing stock value via sentiment index; no vacancy or concession adjustment |

Taken together, the comparison shows that once scope consistency, timely updates, and dual-path validation are enforced, dispersion narrows and decision-makers gain a transparent, reproducible baseline for budgeting and strategic planning.

Key Questions Answered in the Report

What is the current size of the United States office real estate market?

The market reached USD 381.48 billion in 2026 and is forecast to rise to USD 447.86 billion by 2031.

Which building grade captures the most demand?

Grade A buildings hold 58.56% of market share and are projected to grow at a 3.76% CAGR through 2031, underscoring sustained tenant flight-to-quality.

Which state is the fastest-growing office market?

Texas leads with a forecast 4.15% CAGR to 2031, driven by corporate relocations to Austin, Dallas, and Houston.

How are flexible leases influencing landlord strategies?

Forty-two percent of occupiers now use flexible space, prompting landlords to offer shorter terms, expansion rights, and turnkey suites to capture demand.

What role do sustainability mandates play in office demand?

Federal and corporate ESG requirements accelerate green retrofits and concentrate demand in certified buildings, enhancing pricing power for owners of sustainable assets.

Are high interest rates deterring investment?

Transaction volumes dipped amid tighter financing, but well-capitalized REITs and private equity funds continue to acquire and reposition quality assets during the dislocation.

Page last updated on: