United States Oat Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

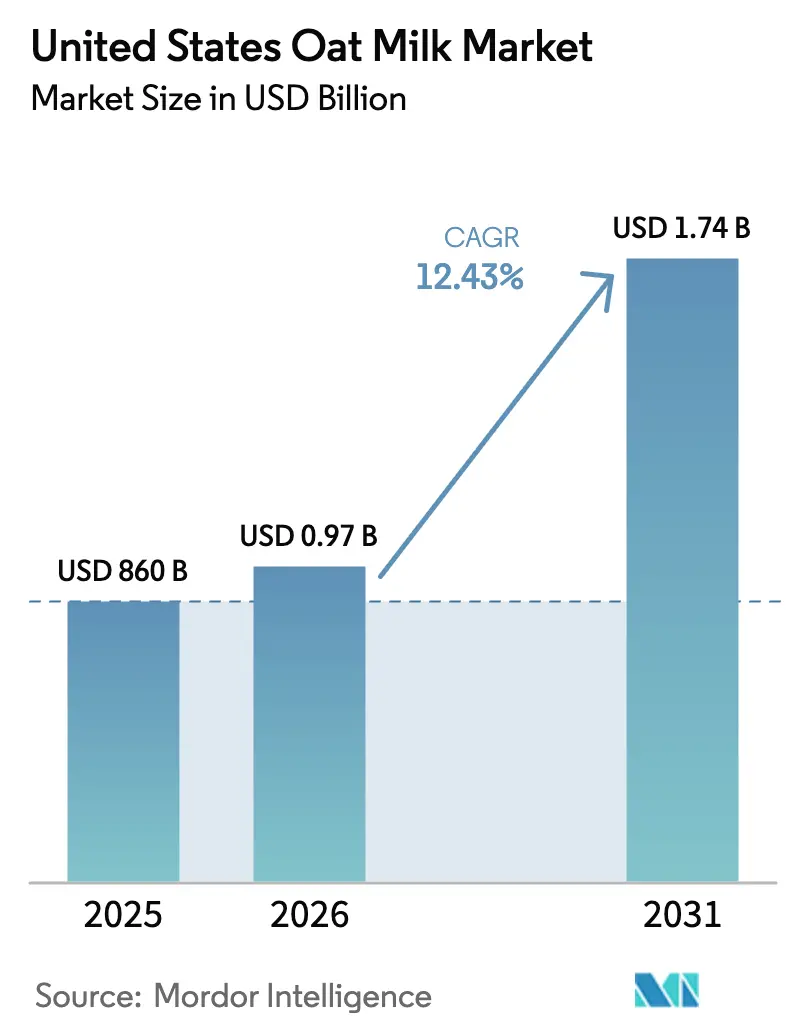

| Base Year Market Size (2025) | USD 860 Billion |

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.74 Billion |

| Growth Rate (2026 - 2031) | 12.43% CAGR |

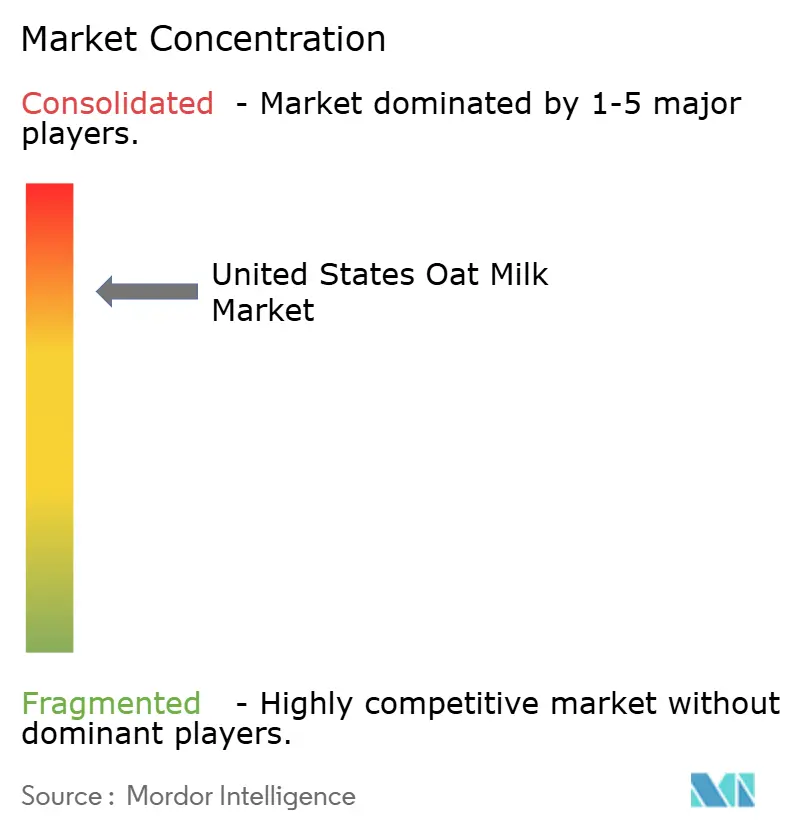

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Oat Milk Market Analysis by Mordor Intelligence

United States oat milk market size in 2026 is estimated at USD 967.9 million, growing from 2025 value of USD 860 million with 2031 projections showing USD 1.74 billion, growing at 12.43% CAGR over 2026-2031. This significant growth highlights a clear shift in consumer preferences from traditional dairy products to plant-based alternatives, driven by the increasing demand for cholesterol-free and lactose-free options. The appeal of oat milk has been further enhanced by its adoption in barista applications and advancements in shelf-stable processing, making it more accessible and convenient for a wider audience. Oat milk's natural maltose sweetness, which reduces the need for added sugars compared to almond or soy milk, resonates with clean-label trends and encourages repeat purchases in both supermarkets and cafés. Furthermore, strategic partnerships with quick-service chains have amplified oat milk's visibility, leading to a 50% year-over-year increase in mentions on United States menus and fostering its trial in previously untapped geographic markets. Amid this growing demand, competition among leading brands remains intense as they prioritize scaling up manufacturing capabilities, securing reliable oat supply contracts, and innovating proprietary enzyme systems to deliver superior texture without relying on stabilizer blends.

Key Report Takeaways

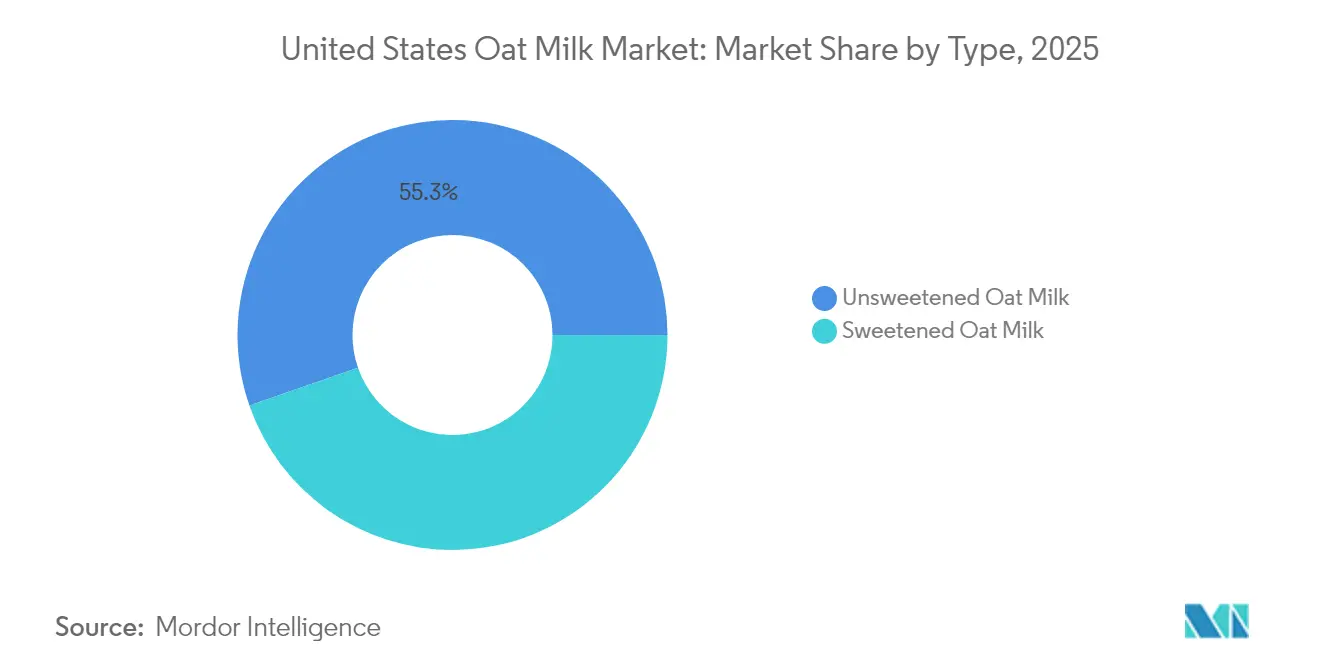

- By type, unsweetened variants led with 55.31% share in 2025 and are forecast to expand at a 14.74% CAGR through 2031, surpassing the United States oat milk market CAGR.

- By flavor, flavored offerings commanded 61.45% share in 2025 and are projected to grow at a 13.98% CAGR to 2031 on the back of new creamer and shake launches

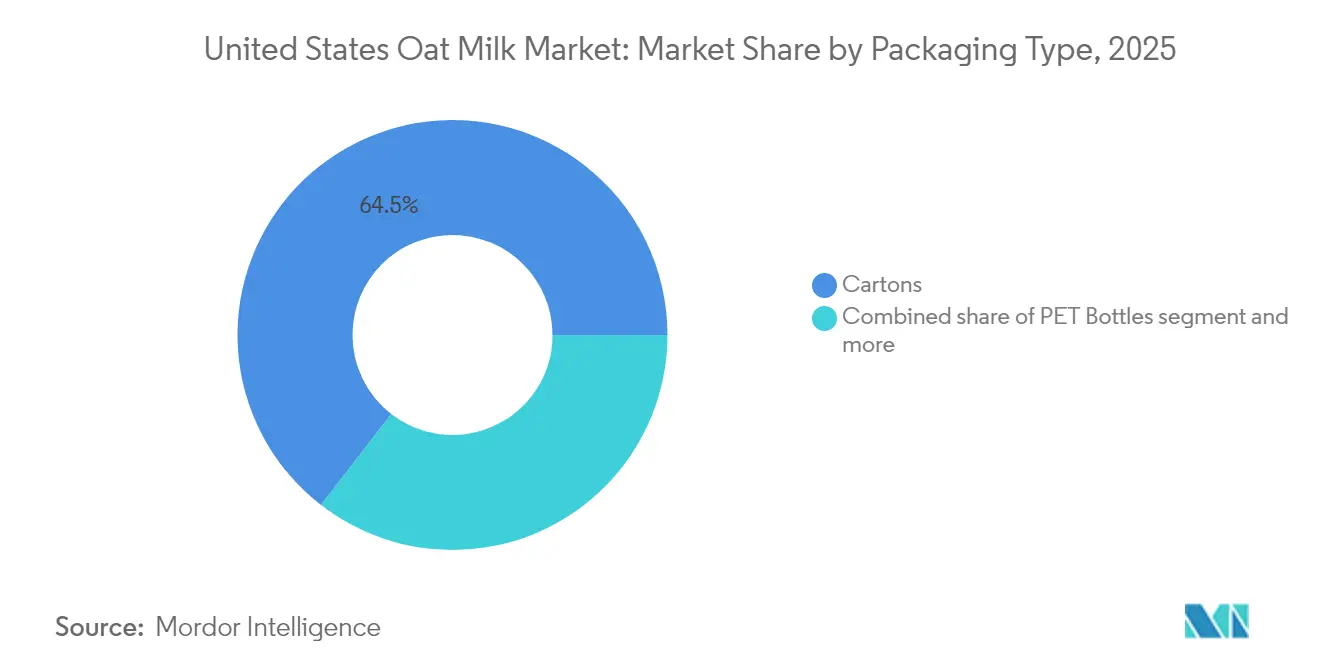

- By packaging, cartons held 64.52% share in 2025, while cans recorded the fastest 12.71% CAGR and are gaining ground through convenience-store and gym placement.

- By distribution channel, off-trade captured 81.95% share in 2025 and is advancing at a 13.72% CAGR as mass grocery chains normalize oat milk positioning in refrigerated dairy aisles.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Oat Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased health consciousness among consumers seeking cholesterol-free and lactose-free options | +2.8% | National, with higher penetration in West Coast and Northeast urban centers | Medium term (2-4 years) |

| Growth of veganism and plant-based diets | +2.1% | National, led by California, New York, Oregon, Washington | Long term (≥ 4 years) |

| Perceived digestive benefits of oat milk relative to other milk alternatives | +1.9% | National, with early adoption in health-focused metropolitan areas | Medium term (2-4 years) |

| Versatility of oat milk in culinary applications | +2.3% | National, concentrated in foodservice hubs and specialty coffee markets | Short term (≤ 2 years) |

| Organic and non-GMO labeling capturing niche health-oriented segments | +1.4% | National, strongest in Pacific Northwest and Northeast | Long term (≥ 4 years) |

| Growth of ready-to-drink and convenience oat beverages for on-the-go use | +1.8% | National, urban centers and college towns | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increased Health Consciousness Among Consumers Seeking Cholesterol-Free and Lactose-Free Options

Lactose intolerance impacts a significant portion of the American population; however, the transition to plant-based milk alternatives is largely influenced by a focus on preventive health rather than medical necessity. Oat milk, known for its beta-glucan fiber content, has been demonstrated in peer-reviewed studies to effectively lower low-density lipoprotein (LDL) cholesterol levels when consumed daily. This health benefit distinguishes oat milk from almond milk, which does not contain soluble fiber, and soy milk, which continues to face consumer apprehensions about phytoestrogens. To broaden its appeal, manufacturers are enriching oat milk with essential nutrients like vitamin D and calcium, ensuring its nutritional value aligns closely with that of traditional dairy milk. This strategy resonates with flexitarian consumers who seek comparable alternatives without compromising on quality or nutrition. Furthermore, the Food and Drug Administration's (FDA) decision in 2023 to officially allow the term "milk" for plant-based beverages has enhanced the perception of oat milk among mainstream shoppers, many of whom previously considered it a specialty product [1]Source: United States Food & Drug Administration, “Foods Program Guidance Under Development,” fda.gov.

Growth of Veganism and Plant-Based Diets

According to Gallup's 2024 survey, 4 percent of Americans identify as vegetarian and 1 percent as vegan, with these figures remaining steady over time. Meanwhile, plant-based milk represented 15 percent of total milk dollar sales in 2024, reflecting growth driven largely by individuals reducing their meat and dairy consumption and health-conscious omnivores rather than strict vegans. This trend is influencing product innovation, such as Califia Farms' introduction of Oatmilk + Protein in 2024. This product, which includes pea protein isolate to provide 8 grams of protein per serving, is designed for gym-goers and individuals seeking meal-replacement options who previously relied on whey-based shakes. The Plant Based Foods Institute found that 50 percent of plant-based milk buyers prioritize health as their main motivation, followed by 28 percent who are driven by environmental concerns. This indicates that sustainability messaging alone may not be enough to encourage product trials [2]Source: Plant Based Foods Association,“PBFI Report Shows Continued Trend of Shoppers Shifting from Animal to Plant-Based Foods,” plantbasedfoods.org. To address this, retailers are allocating more shelf space for oat milk in the refrigerated dairy aisle rather than restricting it to the natural-foods section, a strategy aimed at normalizing the category and capturing impulse purchases.

Perceived Digestive Benefits of Oat Milk Relative to Other Milk Alternatives

Oat milk's soluble fiber content helps support gut microbiome diversity, a benefit that almond milk, which is primarily made up of water and emulsifiers, does not provide. A study published in *Nutrients* in 2024 found that beta-glucan from oats increases short-chain fatty acid production in the colon, which is linked to reduced inflammation and improved insulin sensitivity. This positions oat milk as a functional beverage rather than just a dairy substitute, a message that brands are incorporating into marketing campaigns aimed at consumers with irritable bowel syndrome or general digestive issues. However, the enzymatic process that breaks down oat starch into maltose raises the glycemic index of oat milk to approximately 60, which is comparable to white bread and may discourage its use among individuals with diabetes and those following ketogenic diets. Unsweetened versions address this concern, but consumer education remains a challenge, as many shoppers mistakenly equate "plant-based" with "low-carbohydrate."

Versatility of Oat Milk in Culinary Applications

Barista blends, specifically formulated with added oils and stabilizers to replicate the foaming and steaming characteristics of dairy, have become the fastest-growing subcategory within the oat milk market. This growth is primarily driven by partnerships with Starbucks, Dunkin', and independent specialty coffee shops. Oatly's barista edition, launched in the United States in 2018, now contributes significantly to the brand's revenue. Competitors such as Califia Farms and Minor Figures introduced their own barista-specific stock-keeping units (SKUs) in 2024. Beyond coffee, oat milk's versatility has made it a preferred ingredient among chefs for béchamel sauces, baked goods, and dairy-free ice creams, owing to its neutral flavor and creamy texture. Starbucks' planned 2025 launch of ready-to-drink oat milk Frappuccinos in grocery stores reflects a strategic effort to capitalize on oat milk's functional properties in shelf-stable convenience formats, a category historically led by almond milk.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited consumer familiarity with oat milk versus established dairy-based alternatives | -1.2% | National, more pronounced in rural and Southern states | Short term (≤ 2 years) |

| Labeling confusion regarding natural, organic, and gluten-free claims | -0.9% | National, with regulatory scrutiny in California and New York | Medium term (2-4 years) |

| Technological barriers to improving shelf-life without preservatives | -0.7% | National, impacting refrigerated SKUs | Medium term (2-4 years) |

| Supply chain volatility, including seasonal fluctuations and crop yield | -1.1% | National, concentrated in Midwest oat-growing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Consumer Familiarity with Oat Milk Versus Established Dairy-Based Alternatives

Oat milk has experienced significant growth in urban markets; however, its penetration in rural areas and Southern states remains lower compared to almond and soy milk, which have benefited from decades of distribution and strong brand recognition. Recent data indicates that oat milk accounts for a smaller share of plant-based milk dollar sales compared to almond milk, underscoring the advantage held by more established categories. Consumer education continues to be a challenge, as many shoppers mistakenly associate oat milk with oatmeal, expecting a thicker, grain-based texture, and are surprised by its lighter consistency. Retailers are working to address this issue through in-store sampling and cross-merchandising with coffee and cereal, but conversion rates remain below expectations in regions where dairy consumption is deeply rooted in cultural practices. Furthermore, the absence of a unified industry body to promote oat milk—similar to the Almond Board of California—places the responsibility of consumer education entirely on individual brands, limiting the category's ability to effectively scale awareness.

Labeling Confusion Regarding Natural, Organic, and Gluten-Free Claims

Oats are naturally gluten-free; however, cross-contamination can happen during harvesting, transportation, and milling, introducing gluten from wheat, barley, or rye. The United States Food and Drug Administration allows products to be labeled as "gluten-free" only if the final product contains less than 20 parts per million of gluten. To meet this requirement, manufacturers often need to use dedicated processing facilities or implement strict cleaning protocols. Brands such as Oatly and Califia Farms rely on purity-protocol oats, which are grown, harvested, and milled in gluten-free environments. However, these oats are considerably more expensive than regular oats, which can affect manufacturers' profit margins. At the same time, the lack of a formal definition for the term "natural" by the United States Food and Drug Administration has led to consumer skepticism, particularly when oat milk ingredient lists include stabilizers like dipotassium phosphate and gellan gum. Furthermore, California's Proposition 65 requires warnings for products containing chemicals linked to cancer or reproductive harm. While oat milk itself is not directly impacted, these strict labeling requirements in California have increased consumer scrutiny of all plant-based beverages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Unsweetened Variants Lead on Clean-Label Demand

Unsweetened oat milk accounted for 55.31% of the market share in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 14.74% through 2031, significantly outpacing the overall market growth rate of 12.43%. This impressive growth underscores a broader consumer movement toward healthier dietary choices, particularly the reduction of sugar intake. The American Heart Association has set clear guidelines, recommending a daily limit of 25 grams of added sugar for women and 36 grams for men . These recommendations are increasingly influencing purchasing decisions, as health-conscious consumers actively monitor their sugar consumption.

Unsweetened oat milk naturally contains maltose, a type of sugar that is produced through the enzymatic breakdown of oat starch. This provides a mild, natural sweetness without the need for added sugars, making it an appealing clean-label option for a variety of uses, including coffee, smoothies, and cereals. Recognizing this demand, brands such as Oatly and Califia Farms have expanded their unsweetened product portfolios. Oatly's unsweetened barista blend, in particular, has gained significant traction in specialty coffee shops that prioritize ingredient transparency and cater to consumers seeking healthier alternatives.

By Flavour: Innovations Drive Flavoured Segment Dominance

Flavored oat milk accounted for 61.45% of the market share in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 13.98% through 2031. This growth is being driven by product innovations that go beyond traditional vanilla and chocolate flavors, introducing options such as coffee, caramel, and seasonal varieties. For instance, in February 2024, Oatly launched four new creamers—Sweet & Creamy, Vanilla, Caramel, and Mocha—specifically targeting the coffee-creamer segment. This segment has historically been dominated by dairy and non-dairy creamers from established brands like Coffee-Mate. Oatly's strategic approach recognizes that consumers in the creamer category prioritize flavor intensity and convenience over nutritional purity. This shift in consumer preferences creates an opportunity for oat milk to capture market share from almond and coconut creamers, which have been prominent in the non-dairy space.

Furthermore, the flavored oat milk category is making inroads into impulse-purchase channels, traditionally dominated by dairy-based products. A notable example is f'real's September 2024 launch of the Choco Chip Oat Shake, which is distributed through convenience stores and movie theaters. This product introduction demonstrates how flavored oat milk is successfully penetrating high-traffic retail environments where dairy milkshakes have long been the preferred choice. By offering innovative and appealing options, flavored oat milk continues to expand its presence across diverse consumer touchpoints.

By Packaging Type: Cans Emerge as Fastest-Growing Format

Cartons accounted for 64.52% of the market share in 2025, supported by decades of consumer familiarity and their compatibility with both refrigerated and shelf-stable distribution systems. Aseptic cartons, such as those produced by Tetra Pak and SIG Combibloc, provide the ability to extend shelf life without the use of preservatives. This feature is particularly advantageous for retailers who need to manage a growing number of stock-keeping units (SKUs) and for consumers who prioritize longer usability of products after purchase. The widespread adoption of cartons reflects their established role in the market, offering a balance between functionality and consumer trust built over time.

However, cans are emerging as the fastest-growing packaging type, with a compound annual growth rate (CAGR) of 12.71% projected through 2031. This growth is primarily driven by the increasing demand for on-the-go consumption and the recyclability of aluminum cans. Aluminum cans boast a recycling rate of 70% in the United States, significantly higher than the 25% recycling rate for cartons, which require specialized facilities to separate their paper, plastic, and foil layers. For instance, RISE Brewing Company’s oat milk lattes, packaged in 7-ounce cans, have become a popular choice in convenience stores and gyms. In these settings, the portability of single-serve cans often takes precedence over per-ounce cost efficiency, highlighting the growing consumer preference for convenience and sustainability.

By Distribution Channel: Off-Trade Dominance with Online Retail Surge

Off-trade channels accounted for 81.95% of the market share in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 13.72% through 2031. This growth highlights the transition of oat milk from being a niche product in specialty health stores to becoming a widely available option in mainstream supermarkets and hypermarkets. Major retailers such as Walmart, Kroger, Target, and Albertsons have significantly increased oat milk shelf space by 30% to 40% since 2024. By positioning oat milk in refrigerated aisles alongside traditional dairy milk, rather than confining it to natural-food sections, these retailers are helping to normalize oat milk as a household staple. This strategic placement encourages trial purchases among consumers who might not typically shop in specialty aisles, further driving the adoption of oat milk in everyday diets.

Within the off-trade segment, online retail has emerged as the fastest-growing sub-channel for oat milk sales. E-commerce platforms such as Amazon Fresh, Instacart, and direct-to-consumer subscription services are capturing an increasing share of the market. Thrive Market, an online membership-based retailer, reported that oat milk was among its top 10 best-selling grocery items in 2024. This success is attributed to bulk-purchase discounts and carefully curated product selections that resonate with health-conscious households. The convenience of online shopping, combined with targeted offerings, has made it easier for consumers to incorporate oat milk into their regular grocery purchases, further fueling its growth in the market.

Geography Analysis

The United States oat milk market demonstrates notable regional variation, with the West Coast and Northeast accounting for a significant share of consumption. This trend is largely driven by the higher concentration of health-conscious and environmentally aware consumers in these regions, as well as the presence of well-established specialty coffee cultures. California, in particular, plays a pivotal role, contributing an estimated 25% to 30% of national oat milk sales. This is supported by the dense networks of vegan restaurants, juice bars, and specialty grocers such as Whole Foods Market and Sprouts Farmers Market in metropolitan areas like Los Angeles and San Francisco, which cater to the growing demand for plant-based alternatives.

In contrast, the Midwest and Southern regions of the United States exhibit slower adoption rates for oat milk. This can be attributed to deeply rooted dairy consumption habits and comparatively lower awareness of plant-based alternatives among consumers in these areas. However, these regions represent significant growth opportunities for the oat milk market. Major retailers, including Walmart and Kroger—headquartered in Arkansas and Ohio, respectively—are actively expanding their oat milk assortments within their Midwest and Southern store networks. This strategic expansion aims to tap into the untapped potential of these regions and introduce plant-based options to a broader audience.

Furthermore, the Midwest's strong agricultural economy, particularly in oat-producing states such as North Dakota and Minnesota, positions the region as a potential hub for oat milk manufacturing. Establishing production facilities in these areas could help reduce transportation costs and align with local-sourcing preferences, which resonate strongly with regional consumers. Leading brands, including Danone's Silk and HP Hood's Planet Oat, have recognized this potential and are prioritizing distribution in these regions. By leveraging existing dairy-distribution infrastructure, these companies aim to achieve cost efficiencies while meeting the growing demand for oat milk in emerging markets.

Competitive Landscape

The United States oat milk market is characterized by a high level of concentration, with a few key players dominating revenue and shelf space. However, the market remains dynamic as private-label brands and niche entrants gradually erode the market share of established players. Oatly, the Swedish company that popularized oat milk globally, faces growing competition from Califia Farms, Danone's Silk, and HP Hood's Planet Oat. Each competitor employs distinct strategies: Oatly focuses on brand storytelling and dominance in the barista channel, Califia Farms emphasizes product innovation and premium positioning, Silk leverages Danone's extensive distribution network and cross-category portfolio, and Planet Oat competes through value pricing and accessibility to the mass market.

Oatly reported third-quarter 2024 revenue of USD 201.1 million, with the Americas contributing USD 84.2 million, highlighting its scale and market presence. However, the company's restructuring program, which aims to achieve annual savings of USD 35 million to USD 45 million, reflects the challenges posed by margin pressures. These pressures are primarily driven by increased promotional spending and intensifying competition within the oat milk category.

Opportunities are emerging in the functional oat milk segment, including protein-fortified, probiotic-enhanced, and vitamin-enriched variants that cater to specific consumer needs beyond basic dairy replacement. For instance, Califia Farms introduced Oatmilk + Protein in 2024, which provides 8 grams of protein per serving through pea protein isolate. This product is designed to appeal to fitness enthusiasts and individuals seeking meal-replacement options, addressing a segment where oat milk has historically underperformed compared to alternatives such as soy and pea milk.

Technological advancements are also influencing the competitive landscape. Innovations such as enzymatic processing to control maltose levels, high-pressure processing for extended shelf life, and precision fermentation to produce dairy-identical proteins are being explored by smaller, venture-backed startups. Ripple Foods, known for its pea-protein milk, has filed patents for blended oat-pea formulations. This approach aims to combine the taste profile of oat milk with the nutritional benefits of pea protein, potentially disrupting single-ingredient platforms.

United States Oat Milk Industry Leaders

Oatly Group AB

HP Hood LLC

Califia Farms LLC

Danone SA

Chobani LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Oatly launched a limited-edition hot cocoa oat milk drink in the United States for the festive season. The product was available nationwide at Whole Foods Market. It was plant-based, glyphosate-residue-free, gluten-free, and fortified with vitamins, addressing the increasing consumer demand for health-focused oat milk beverages.

- August 2024: Milkadamia has launched the first 2D-printed flat-pack oat milk in the United States, marking an innovative packaging development. This eco-friendly, space-saving design aims to enhance convenience and sustainability in the plant-based milk segment, catering to growing consumer demand.

- January 2024: Oatly Group expanded its US oat milk range with Unsweetened Oatmilk and Super Basic Oatmilk, emphasizing diverse nutritional options and simplicity. These new varieties target health-conscious consumers and those shifting from dairy, supporting Oatly’s mission to grow oat milk adoption in the United States market.

United States Oat Milk Market Report Scope

Off-Trade, On-Trade are covered as segments by Distribution Channel.| Sweetened Oat Milk |

| Unsweetened Oat Milk |

| Flavoured |

| Un-flavoured |

| PET Bottles |

| Cans |

| Cartons |

| Others |

| On-trade | |

| Off-trade | Convenience Stores |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| On-line Retail | |

| Others |

| By Type | Sweetened Oat Milk | |

| Unsweetened Oat Milk | ||

| By Flavour | Flavoured | |

| Un-flavoured | ||

| By Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| On-line Retail | ||

| Others | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms