United States Montelukast API Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

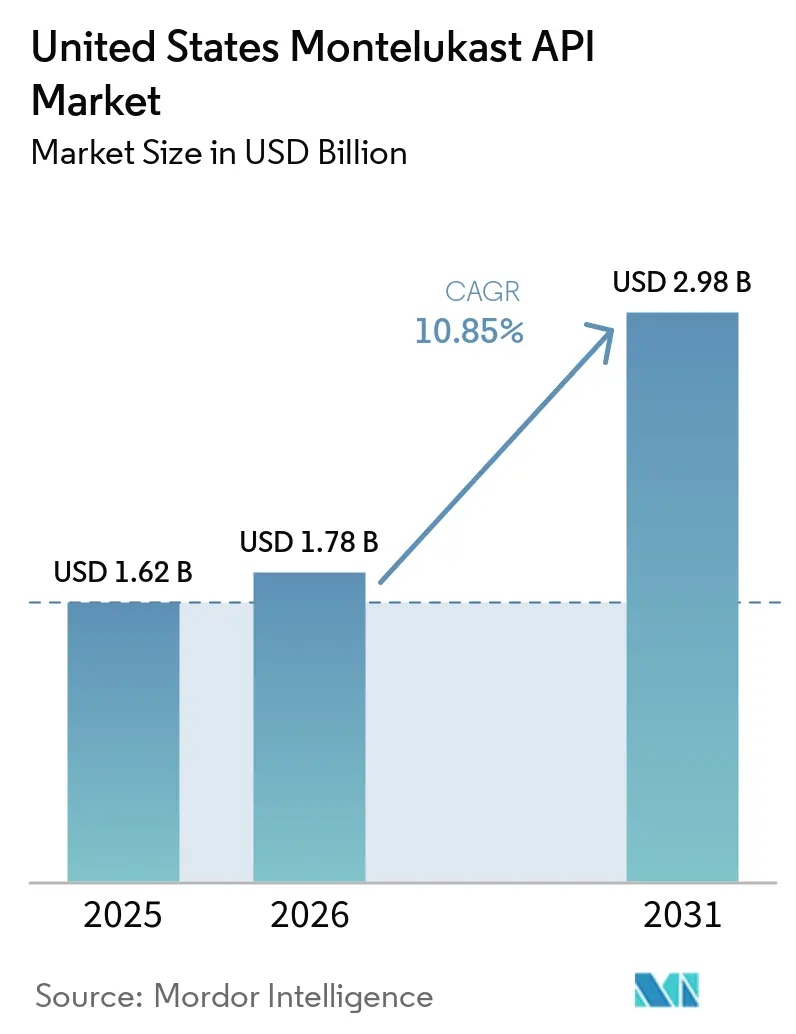

| Base Year Market Size (2025) | USD 1.62 Billion |

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.98 Billion |

| Growth Rate (2026 - 2031) | 10.85% CAGR |

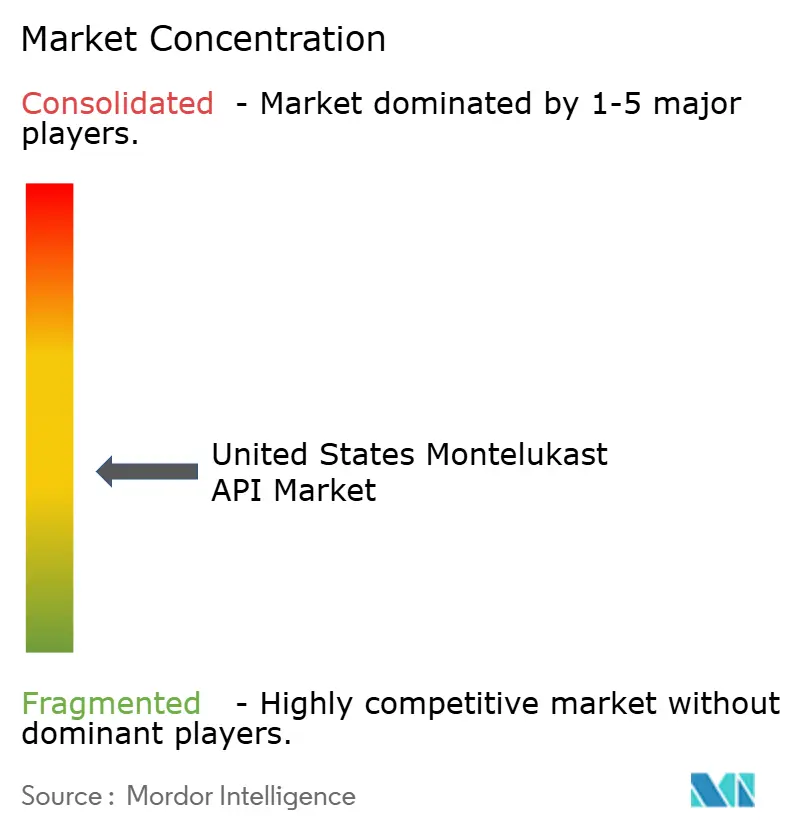

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Montelukast API Market Analysis by Mordor Intelligence

The United States Montelukast API Market size is projected to expand from USD 1.62 billion in 2025 and USD 1.78 billion in 2026 to USD 2.98 billion by 2031, registering a CAGR of 10.85% between 2026 to 2031.

The United States montelukast API market continues to draw support from a large chronic respiratory patient base, as 8.6% of U.S. adults and 6.5% of children had current asthma in 2024, which kept controller therapy demand structurally broad across age groups. The United States montelukast API market also benefits from allergic rhinitis demand, with up to 60 million people affected annually, and longer pollen exposure increasing treatment need beyond the traditional spring season. Growth remains intact even as treatment guidance continues to favor inhaled corticosteroid-based pathways, because current protocols still retain montelukast as an alternative or add-on option and continue to reference neuropsychiatric risk in routine treatment decisions. The pediatric oral formulation base remains a durable demand pool, since younger patients who cannot reliably use inhalers still require chewables, granules, and liquid-compatible therapies that support steady API procurement. The supplier base remains centered on Indian manufacturers with regulated-market filings and large production systems, which keeps U.S. buyers focused on backup qualification, procurement continuity, and tighter quality screening in the United States montelukast API market.

Key Report Takeaways

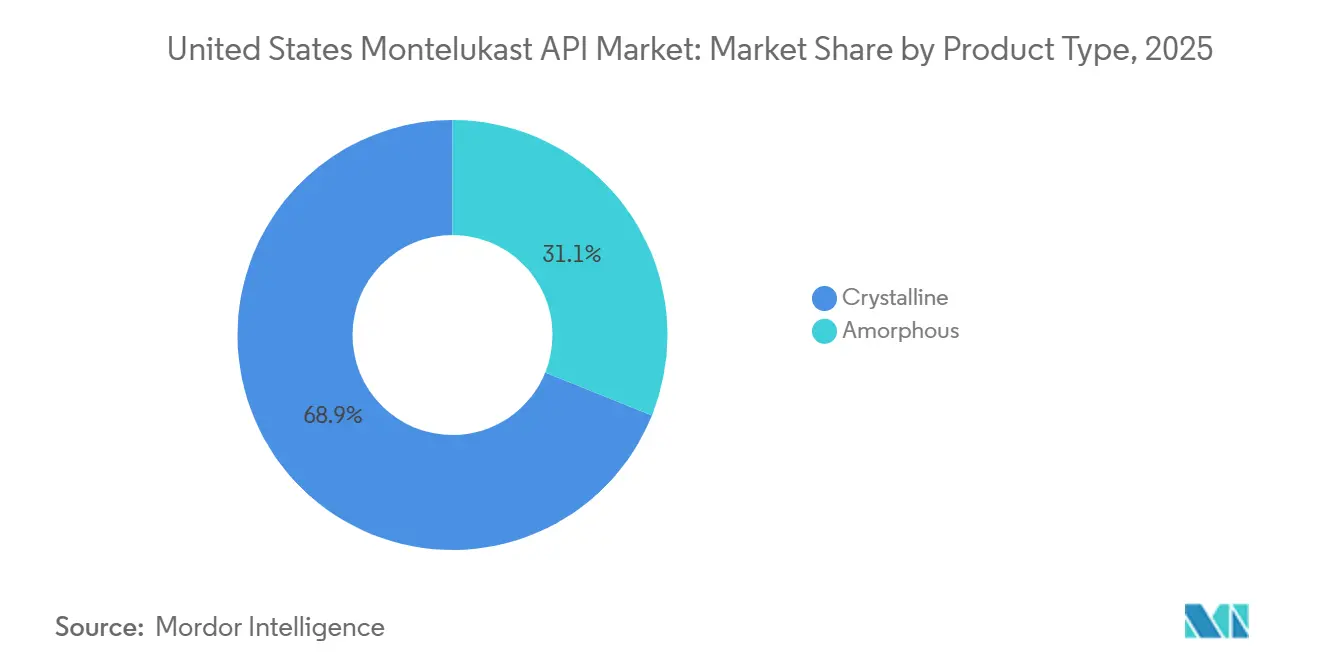

- By product type, crystalline held 68.87% of the United States montelukast API market share in 2025, while amorphous is forecast to expand at 11.36% CAGR through 2031.

- By dosage form compatibility, chewable tablets accounted for 61.83% of procurement volumes in 2026, while oral solutions, suspensions, and syrups are projected to grow at 12.87% CAGR through 2031.

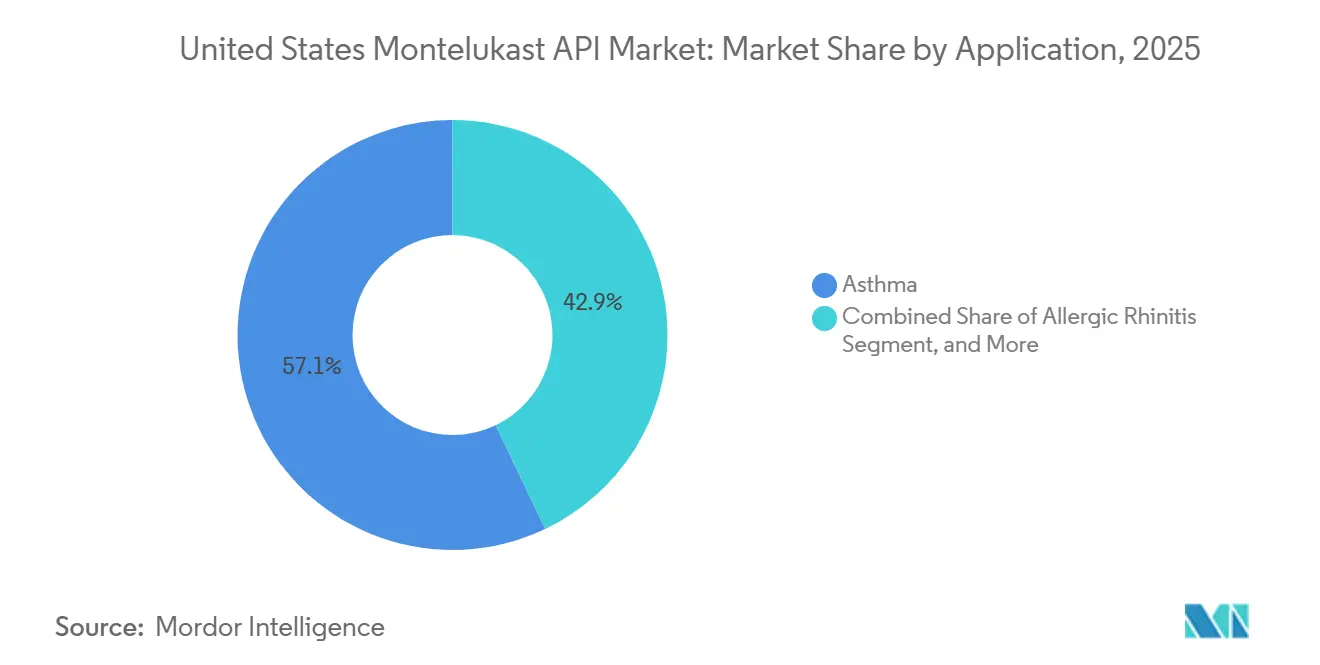

- By application, asthma accounted for 57.12% of the United States montelukast API market size in 2025, while allergic rhinitis is expected to expand at 11.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Montelukast API Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. Asthma Controller Demand Base | +2.5% | National, highest intensity in Southern states and Northeast urban corridors | Long term (≥ 4 years) |

| Generic-First Payer Economics | +1.8% | National, concentrated in states with large Medicaid and PBM-managed commercial populations | Medium term (2-4 years) |

| Pediatric Chewable and Granule Demand | +1.5% | National, strongest in high-prevalence pediatric states in the Southeast and Northeast | Long term (≥ 4 years) |

| Allergy Season Extension and Perennial Rhinitis Burden | +2.0% | National, with early pressure in the Pacific Northwest and Southeast | Long term (≥ 4 years) |

| DMF-Backed Supplier Consolidation After Impurity Scrutiny | +0.7% | Global India-to-U.S. supply channel | Medium term (2-4 years) |

| U.S. Import Dependence Favors Qualified Backup Suppliers | +1.0% | National, centered on major East Coast entry and distribution corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

U.S. Asthma Controller Demand Base

Asthma remains the central demand anchor for the United States montelukast API market because the treated population is large and persistent across both adult and child cohorts. The CDC reported in 2024 that 8.6% of U.S. adults and 6.5% of children had current asthma, which means controller therapy demand remains broad even before allergy-related use is added on top.[1]U.S. Centers for Disease Control and Prevention, “FastStats: Asthma,” Centers for Disease Control and Prevention, cdc.gov This patient pool matters because montelukast stays relevant where physicians want an oral controller option or where inhaler use is inconsistent, especially in younger patients. Once a child is stabilized on an oral regimen, caregivers and prescribers often prefer continuity over disruption, which supports repeat ordering behavior in the United States montelukast API market. That continuity is reinforced by regulatory and chemistry review burdens tied to supplier changes, so established formulator and API relationships tend to last longer than spot-price movements alone would suggest.

Generic-First Payer Economics

Generic-first reimbursement structures continue to support the United States montelukast API market because montelukast remains positioned as a low-cost controller option before escalation to higher-cost therapies. In practical terms, step-therapy design can preserve procurement volumes because it inserts montelukast into many treatment pathways before biologics or other premium therapies are authorized. This keeps demand steady even when clinical guidance becomes more selective, since payer logic and physician workflow do not change at the same speed. Aurobindo Pharma’s March 2025 investor presentation showed 297 U.S. DMFs on file as of December 2024 and API revenue of USD 512 million in FY24, which reflects the scale at which regulated-market suppliers are built around sustained generic demand.[2]Aurobindo Pharma Limited, “Investor Presentation,” Aurobindo Pharma, aurobindo.com The result is a market where price pressure is real, but volume persistence remains strong enough to keep the United States montelukast API market on a double-digit growth path.

Pediatric Chewable And Granule Demand

Pediatric demand continues to protect the United States montelukast API market because oral delivery still fits younger patients better than inhaler-based routines in many real-world settings. The CDC’s 2024 asthma statistics confirm that childhood asthma remains a meaningful treated population, which gives oral pediatric formats a durable clinical base. Chewables and granule-compatible API grades stay important because they match caregiver preference for simpler administration, especially where adherence and technique are hard to maintain. Research published in Pharmaceutics in July 2024 showed successful development of a stable montelukast and levocetirizine fixed-dose combination tablet with pharmaceutical equivalence, which points to additional formulation pathways beyond standard standalone products.[3]P. Akbarzadeh et al., “Enhanced Stability and Compatibility of Montelukast and Levocetirizine in a Fixed-Dose Combination Monolayer Tablet,” Pharmaceutics, mdpi.com That development pressure favors suppliers that can support tighter particle control, stronger purity consistency, and solid-state properties suited to oral pediatric formats.

Allergy Season Extension And Perennial Rhinitis Burden

The United States montelukast API market is also benefiting from a broader allergic rhinitis treatment base, which extends demand beyond asthma alone. CDC material states that up to 60 million people in the United States are affected by allergies each year, and longer pollen seasons are increasing exposure in many regions. The AAAAI reported in 2025 that pollen seasons are lengthening because of earlier spring onset, later autumn frost, and longer growing periods, which expands the duration of symptomatic burden in multiple regions. This matters for montelukast because perennial rhinitis patients often move beyond simple antihistamine use and still need accessible add-on options when symptoms remain uncontrolled. That broadening allergy burden adds another stable layer of demand to the United States montelukast API market, especially in regions where environmental exposure is becoming less seasonal and more persistent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA Boxed Warning on Neuropsychiatric Risk | -1.8% | National | Short term (≤ 2 years) |

| ICS-First Treatment Pathway Shift | -1.4% | National, more pronounced in states with high managed-care penetration | Medium term (2-4 years) |

| Price Erosion in Mature Generic Supply | -2.2% | National | Short term (≤ 2 years) |

| Nitrosamine and Impurity Control Costs | -0.8% | Global supplier base serving the FDA-regulated U.S. import channel | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

FDA Boxed Warning On Neuropsychiatric Risk

The existing boxed warning on neuropsychiatric risk continues to limit new prescribing intensity in the United States montelukast API market, especially for allergic rhinitis starts. The GINA 2024 and 2025 strategy reports both retained repeated reminders around neuropsychiatric risk wherever montelukast appeared in treatment pathways, which shows that caution remains embedded in current clinical practice. The main effect is not a collapse in ongoing use, but a tighter filter on who starts therapy and when it is used in rhinitis care. That means the warning changes the mix of demand more than the existence of demand, since established patients with known benefit are often maintained rather than switched. The United States montelukast API market, therefore, absorbs a continuing restraint through slower new-patient conversion rather than through broad discontinuation of existing therapy.

ICS-First Treatment Pathway Shift

The shift toward inhaled corticosteroid-based pathways is another clear restraint on the United States montelukast API market, particularly for adult and adolescent asthma starts. The GINA 2025 strategy report reinforced ICS-formoterol-based treatment across multiple severity steps, which placed leukotriene receptor antagonists in a more selective role than before. The November 2024 BTS, NICE, and SIGN update also positioned ICS-formoterol as first-line therapy for newly diagnosed patients aged 12 and above, with montelukast used later when control remains inadequate. Even so, the effect is moderated by younger patients, exercise-related use, and patients who do not use inhalers well, because those groups still preserve a meaningful need for oral therapy. The restraint is strongest at treatment initiation, while the established patient base remains more stable because switching a controlled chronic patient is usually slower and more selective.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Amorphous Adoption Following Pediatric Formulation Needs

Crystalline montelukast sodium held 68.87% of product-type demand in 2025, which made it the dominant form in the United States montelukast API market. That lead reflects the continued weight of film-coated tablet manufacturing, where buyers prefer a stable input with well-understood handling, storage, and validation behavior. Crystalline material fits mature generic production lines because those lines are already aligned around repeatable dissolution behavior and long-established chemistry controls. It also benefits from the fact that many approved formulations were built around this form, which makes continuity easier for both API suppliers and finished-dose manufacturers. For that reason, crystalline grades remain the default purchasing choice wherever adult oral solids drive procurement volumes.

The amorphous form is projected to grow at 11.36% CAGR through 2031, which places it ahead of the broader United States montelukast API industry. That faster pace reflects the needs of oral granules, liquids, and other pediatric-friendly formats that require stronger solubility performance and quicker dispersion behavior. The United States montelukast API industry is therefore seeing a gradual shift from a stability-first buying logic toward a format-fit buying logic in selected high-growth contracts. This does not mean crystalline loses relevance, because adult tablets still represent a deep installed base, but it does mean premium demand is moving toward suppliers that can support more specialized solid-state requirements. As combination products and newer pediatric dosage concepts move forward, early capability in amorphous supply is likely to bring better contract durability than commodity crystalline volumes alone.

Crystalline grades also gain support from the practical reality that formulation changes are slow once a product is established. Buyers generally avoid switching the solid-state form in approved products unless the clinical and commercial payoff is clear, because any change can trigger extra chemistry and validation work. That inertia protects existing crystalline relationships in the United States montelukast API market even while amorphous demand rises faster. At the same time, amorphous suppliers can still gain share where new pediatric or liquid-compatible programs are being designed from the start, since they are not held back by legacy formulation choices.

By Dosage Form Compatibility: Chewables Lead While Liquids Gain Speed

Chewable tablets accounted for 61.83% of dosage-form compatibility demand in 2026, which kept them as the largest compatibility segment in the United States montelukast API market. Their position reflects a treatment setting where children need a simple oral format that caregivers can administer without inhaler technique problems. The CDC reported that 6.5% of children had current asthma in 2024, which helps explain why pediatric oral therapies continue to support large and recurring procurement volumes. Chewables are also tied to long treatment windows, since many pediatric patients remain on controller support over multiple years. That combination of clinical fit, caregiver familiarity, and repeat use keeps chewables central to the demand profile.

Oral solutions, suspensions, and syrups are projected to grow at 12.87% CAGR through 2031, which makes them the fastest-rising compatibility segment within the United States montelukast API market. That expansion reflects growing interest in infant and very young child administration, where dosing flexibility and swallowing ease matter more than tablet convenience. Liquid-compatible supply also creates a higher bar for purity and manufacturing consistency, because pediatric formats tend to face tighter scrutiny around residues, degradation, and batch-to-batch performance. This gives specialized suppliers more room to differentiate than they would have in standard adult tablet procurement. As a result, the United States montelukast API market is likely to see a wider value gap between mature tablet-grade supply and pediatric liquid-compatible supply over the forecast period.

Oral granules sit between these two ends of the market and remain important because they support younger patients while retaining straightforward administration. They do not match the installed base of chewables, but they still benefit from the same pediatric logic that protects oral therapy in early childhood. Film-coated tablets remain a large but mature compatibility segment, where demand is steady and pricing is more exposed to generic competition. The balance across these formats shows that the United States montelukast API market is not expanding through one route alone, but through a mix of mature pediatric formats and newer liquid-compatible growth corridors.

By Application: Asthma Dominates While Rhinitis Expands Faster

Asthma accounted for 57.12% of application-led demand in 2025, which made it the largest use case in the United States montelukast API market. That position reflects its long clinical history, broad labeling depth, and continued role as an oral option when controller support is needed beyond simple reliever use. The underlying patient base remains substantial, with the CDC reporting current asthma in both adult and child populations at levels that keep controller treatment demand structurally meaningful. In addition, current asthma guidance still retains montelukast in treatment pathways even as inhaled corticosteroid-based regimens are prioritized more strongly. This keeps asthma as the core volume pool even if its share growth is more measured than before.

Allergic rhinitis is projected to expand at 11.97% CAGR through 2031, which makes it the fastest-growing application in the United States montelukast API market. That pace reflects both the size of the allergy population and the fact that perennial and difficult-to-control patients still need accessible add-on therapy when simpler options do not provide enough relief. CDC material notes that up to 60 million people in the United States are affected by allergies annually, while the AAAAI documented longer pollen seasons and broader environmental exposure in 2025. The application mix is therefore broadening even as asthma remains dominant, which gives the United States montelukast API market a more diversified demand base than a single-indication product would have. Rhinitis growth does not remove the constraints from current warning language, but it does show that clinically persistent allergy populations still support faster expansion than the asthma segment.

Exercise-induced bronchoconstriction remains a smaller but relevant application because it serves patients who value the convenience of an oral preventive option. Urticaria and other off-label use cases remain limited in scale, yet they still add a modest layer of demand diversity to the United States montelukast API market. These smaller applications matter less for share leadership, but they help reduce dependence on one single use case. That makes the overall application mix more balanced even while asthma and rhinitis continue to account for most procurement volumes.

Geography Analysis

Southern states and dense Northeast corridors continue to shape the demand profile of the United States montelukast API market because asthma and allergy burden remain concentrated in those parts of the country. CDC 2024 BRFSS asthma call-back survey tables show meaningful state variation in active disease burden among previously diagnosed adults, which supports uneven treatment intensity across regions. States such as Mississippi and Alabama have historically shown adult asthma prevalence above 10%, which keeps controller demand elevated in the South. Northeast urban corridors also support strong use because pollution, indoor allergen exposure, and dense health-care access keep diagnosis and treatment rates comparatively active.

The supply side of the United States montelukast API market remains tied closely to Indian manufacturing geography, even though the end market is domestic. Morepen’s official API information and April 2025 filing underline the importance of its U.S. FDA approved production base and its leadership position in montelukast API exports, which shows how heavily U.S. buyers rely on India-based producers. Dr. Reddy’s current product page also highlights a multi-country DMF footprint for montelukast sodium, reinforcing the same India-led supply structure. This creates clear scale benefits for U.S. buyers because experienced suppliers already understand regulated-market documentation and quality expectations. At the same time, it raises concentration risk around a limited manufacturing geography, which is why U.S. procurement teams are increasingly focused on dual qualification and continuity planning. Distribution and import processing remain most practical in East Coast pharmaceutical corridors, where formulation, warehousing, and institutional purchasing networks are already dense.

Climate and exposure patterns are widening the regional demand footprint of the United States montelukast API market beyond the most established asthma centers. The AAAAI stated in 2025 that major U.S. regions are seeing longer pollen seasons, although the pace and expression vary by location. This is especially relevant in the Pacific Northwest and Upper Midwest, where longer exposure periods are expanding the number of patients who need treatment across more of the year. The Southeast remains important for another reason, because high asthma burden and stronger pollen exposure are occurring together, which supports the fastest growth corridor inside rhinitis-linked procurement. These shifts do not overturn the existing demand map, but they do make the United States montelukast API market less dependent on a narrow set of traditional high-burden states over time.

Competitive Landscape

The United States montelukast API market remains moderately fragmented, with leadership concentrated among a group of Indian manufacturers that have regulated-market scale rather than among one or two dominant players. Morepen, Dr. Reddy’s, Aurobindo, Lupin, Cipla, and other established suppliers anchor the competitive set because they combine manufacturing depth with filings relevant to major export destinations. Morepen’s official API information identifies montelukast among its key products, while its April 2025 filing stated that the company was India’s number 1 montelukast API exporter and had 144 MT annual API manufacturing capacity. That kind of scale matters because U.S. buyers usually prefer suppliers that can meet both continuity and compliance expectations over long contract periods.

Aurobindo remains a strong competitive reference point in the United States montelukast API market because its March 2025 presentation disclosed 297 U.S. DMFs, 13 manufacturing facilities, and 19,000 MT total installed API capacity across its broader operations. Dr. Reddy’s also holds a meaningful position through its multi-country DMF footprint for montelukast sodium, which supports buyers who want one supplier aligned with several regulated regions at once. Strategic differentiation is therefore shifting away from simple price competition and toward supply assurance, filling depth, and the ability to support formulation-specific needs. Morepen’s April 2025 filing also outlined a sales-force expansion program and deeper regulated-market customer focus, which signals an effort to move beyond transactional selling and strengthen long-duration customer programs. In parallel, Dr. Reddy’s continuing multi-region documentation strategy and Aurobindo’s scale position both companies well for buyers seeking backup qualification without sacrificing regulatory familiarity.

Compliance pressure is becoming a larger competitive filter in the United States montelukast API market than it was a few years ago. APIC published updated nitrosamine risk-management guidance in May 2025, which raised the analytical and process burden for API manufacturers supplying regulated markets. That change favors larger suppliers that can fund impurity studies, route reviews, and ongoing monitoring without weakening commercial execution. It also creates room for suppliers that can support pediatric-focused amorphous or liquid-compatible grades, because those products depend on tighter technical control than mature tablet-grade volumes. The result is a market where fragmentation still exists, but competitive advantage is moving steadily toward scale, documentation strength, and formulation-specific capability.

United States Montelukast API Industry Leaders

Aurobindo Pharma Limited

Hikma Pharmaceuticals PLC

Lupin Limited

Morepen Laboratories Limited

Unichem Laboratories Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: APIC (Active Pharmaceutical Ingredients Committee, CEFIC) published updated guidance for API manufacturers on nitrosamine risk management, requiring systematic risk assessments covering synthesis route vulnerability, impurity fate and purge studies, and cross-contamination evaluation. The guidance directly governs montelukast API suppliers supplying the US and EU channels and is expected to accelerate supplier qualification costs across the supply base.

- May 2025: GINA published its 2025 Strategy Report, further reinforcing ICS-formoterol as preferred first-line therapy across all asthma severity steps and retaining neuropsychiatric risk reminders for montelukast throughout treatment protocols. This update has direct downstream implications for United States prescribing volumes and API demand trajectory in the adult asthma segment.

- April 2025: Morepen Laboratories filed BSE disclosures confirming its position as India’s #1 montelukast API exporter, with exports to 82 countries and 144 MT annual API manufacturing capacity. The company announced a salesforce expansion programme of over 1,000 professionals over 3 years, with more than 200 new hires planned in FY26, as part of a strategy to deepen regulated-market customer programmes.

United States Montelukast API Market Report Scope

The United States Montelukast API market encompasses the domestic production, trade, and commercial supply of Montelukast Sodium, the active pharmaceutical ingredient (API) used to manufacture finished drugs (like Singulair) for asthma, allergic rhinitis, and exercise-induced bronchoconstriction.

The United States Montelukast API Market is segmented by product type, dosage‑form compatibility, and therapeutic application. By product type, the market includes both amorphous and crystalline forms of montelukast API, each selected based on stability and formulation needs. In terms of dosage‑form compatibility, montelukast API is used in film‑coated tablets, chewable tablets, oral granules, and oral solutions/suspensions/syrups, reflecting its broad use across pediatric and adult formulations. By application, demand is driven by its role in treating asthma, allergic rhinitis, exercise‑induced bronchoconstriction, and urticaria.

| Amorphous |

| Crystalline |

| Film-coated tablets |

| Chewable tablets |

| Oral granules |

| Oral solutions / suspensions / syrups |

| Asthma |

| Allergic rhinitis |

| Exercise-induced bronchoconstriction |

| Urticaria and other off-label use |

| By Product Type | Amorphous |

| Crystalline | |

| By Dosage Form Compatibility | Film-coated tablets |

| Chewable tablets | |

| Oral granules | |

| Oral solutions / suspensions / syrups | |

| By Application | Asthma |

| Allergic rhinitis | |

| Exercise-induced bronchoconstriction | |

| Urticaria and other off-label use |

Key Questions Answered in the Report

What is driving growth in United States montelukast API demand through 2031?

Growth is being supported by a large asthma treatment base, a broad allergy population, and steady pediatric oral formulation demand. The market is projected to rise from USD 1.78 billion in 2026 to USD 2.98 billion by 2031 at a 10.85% CAGR.

Why do chewable tablets remain important for montelukast procurement in the United States?

Chewable-compatible API held 61.83% of procurement volumes in 2026 because oral pediatric administration remains practical for children who cannot use inhalers consistently.

Which application is growing faster, asthma or allergic rhinitis?

Asthma remained the largest application with 57.12% of demand in 2025, but allergic rhinitis is growing faster at 11.97% CAGR through 2031.

How are current asthma treatment guidelines affecting montelukast demand?

Current guidelines favor ICS-formoterol more strongly for many adult and adolescent patients, which limits new-start intensity. Even so, montelukast remains relevant as an alternative or add-on therapy and retains strength in pediatric oral use.

Why is the supplier landscape centered on Indian manufacturers?

Large Indian API producers such as Morepen, Aurobindo, and Dr. Reddy’s already operate with regulated-market filings, export experience, and manufacturing scale, which makes them central to U.S. sourcing strategies.

Page last updated on: