Karl Fischer Titrators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

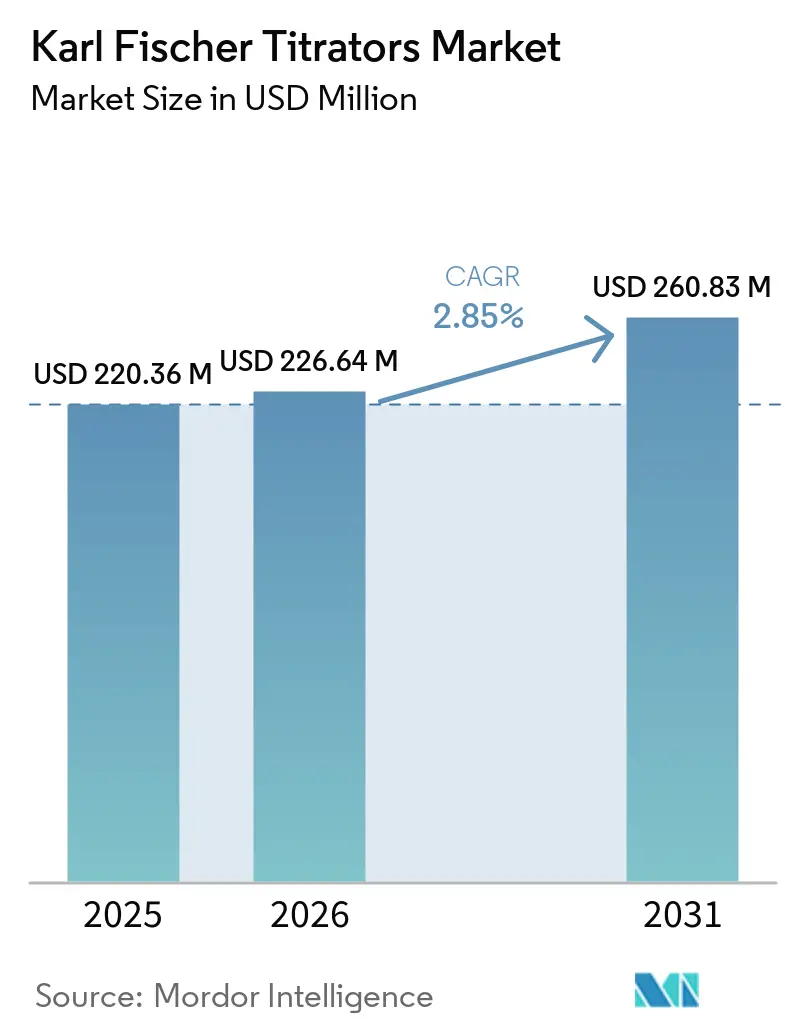

| Market Size (2026) | USD 226.64 Million |

| Market Size (2031) | USD 260.83 Million |

| Growth Rate (2026 - 2031) | 2.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Karl Fischer Titrators Market Analysis by Mordor Intelligence

The Karl Fischer Titrators Market size was valued at USD 220.36 million in 2025 and is estimated to grow from USD 226.64 million in 2026 to reach USD 260.83 million by 2031, at a CAGR of 2.85% during the forecast period (2026-2031).

Growth remains measured because this is a precision instrumentation category with a narrow testing core, but demand quality is improving as many laboratories replace aging semi-automated systems with connected platforms that support audit trails, user controls, and software-led workflows. Regulatory pressure in pharmaceuticals and other moisture-sensitive applications continues to favor direct compendial water determination, which keeps Karl Fischer titration central in release testing and method validation even as labs add faster screening tools around it. Battery cell production and biologics manufacturing are also widening the need for trace-moisture control, especially where very small water deviations can damage stability, safety, or process yield. Vendors are therefore protecting revenue less through broad installed-base growth and more through automation, software compliance, higher-throughput sampling, and reagent systems tailored to difficult matrices. This combination keeps the Karl Fischer titrators market on a steady path, with replacement demand and specialized applications doing more of the work than simple unit expansion.

Key Report Takeaways

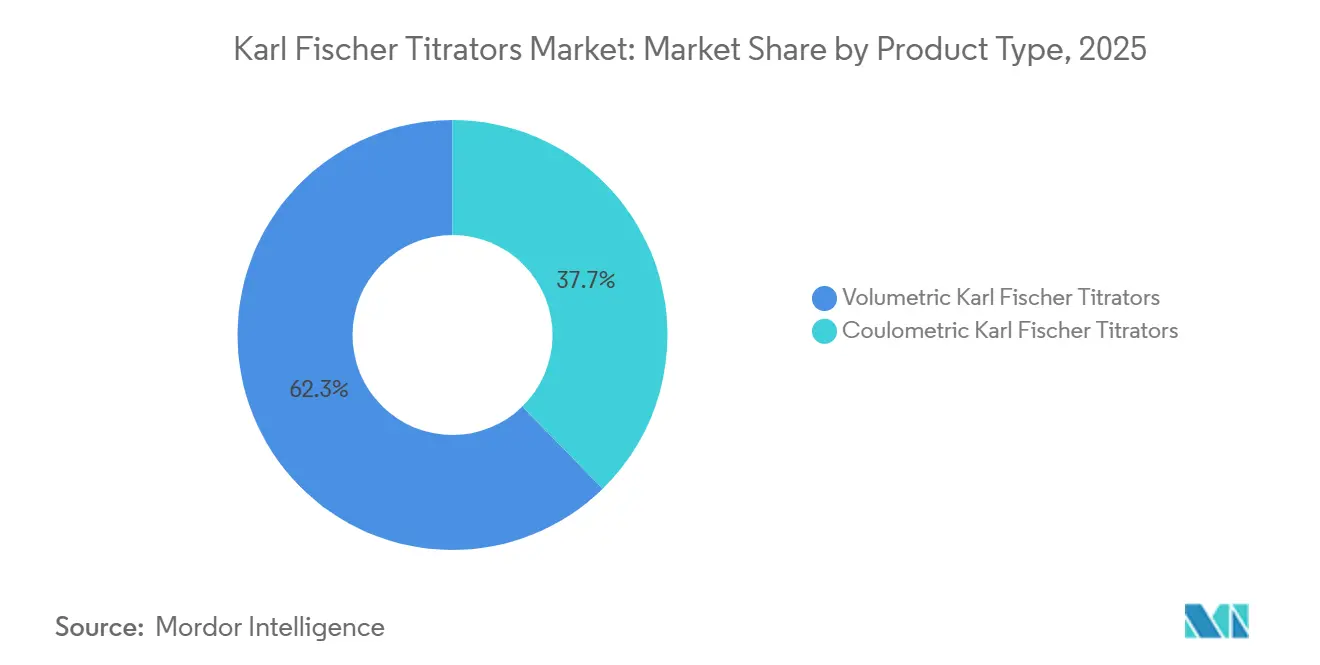

- By product type, volumetric Karl Fischer titrators led with 62.3% revenue share in 2025, while coulometric Karl Fischer moisture analyzers are projected to expand at 4.4% CAGR through 2031.

- By technology, automated platforms held 62.2% of revenue in 2025, while automated systems also recorded the highest projected CAGR at 4.5% through 2031.

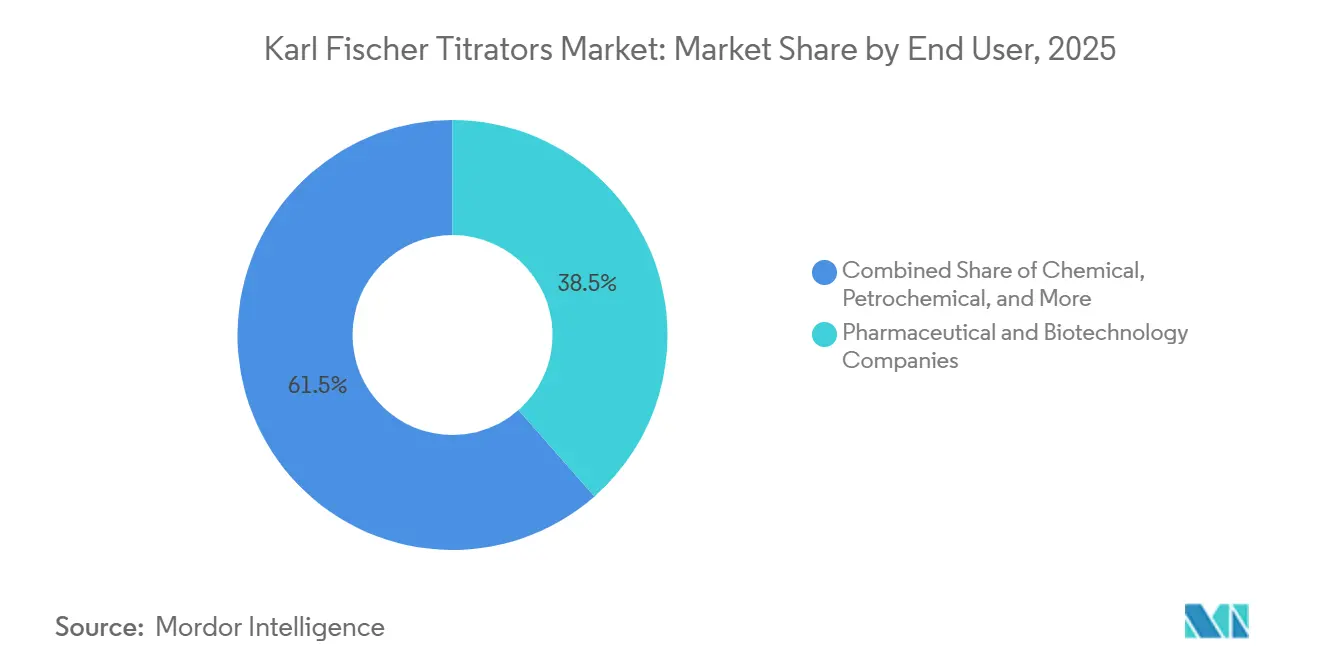

- By end user, pharmaceutical and biotechnology companies accounted for 38.5% of revenue in 2025, while chemical, petrochemical, and energy materials users are forecast to grow at 5.3% CAGR through 2031.

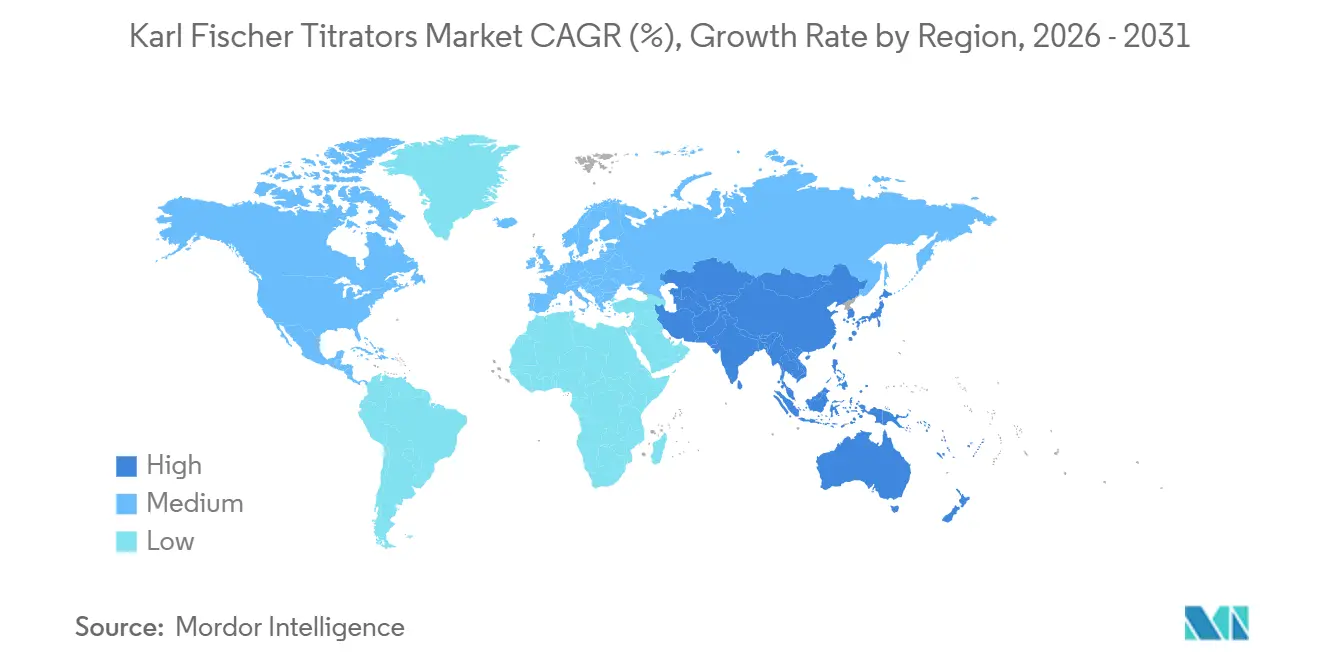

- By geography, Asia-Pacific represented 35.2% of revenue in 2025 and is also the fastest-growing regional cluster with a projected 4.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Karl Fischer Titrators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Pharma And Biotech Moisture-Control Compliance | +0.7% | Global, with concentrated impact in North America, Europe, and Japan | Medium term (2-4 years) |

| Broader Moisture-Critical QA Across Chemicals, Fuels, And Food | +0.3% | Global, with industrial intensity in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Automation, Audit Trails, And LIMS Integration | +0.5% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| CRO And Contract Testing Expansion | +0.3% | Asia-Pacific centered, especially India and China, with spillover to the Middle East and Africa | Long term (≥ 4 years) |

| Battery-Electrolyte And Electrode Moisture Control | +0.4% | Asia-Pacific centered, especially China, South Korea, and Japan, with expansion into Europe and North America | Medium term (2-4 years) |

| Lyophilized Biologics Residual-Moisture Testing | +0.3% | North America and Europe, with emerging adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Pharma And Biotech Moisture-Control Compliance

The market continues to draw its strongest structural support from pharmaceutical and biotechnology quality systems, where moisture limits are not optional and compendial acceptance remains central to routine testing. Mettler-Toledo’s pharmaceutical guidance ties volumetric and coulometric Karl Fischer workflows directly to USP <921> and Ph. Eur. requirements, which keeps the method embedded in testing for active ingredients, excipients, and finished products. The compliance burden now extends beyond the chemistry itself because many regulated facilities must also show secure electronic records, audit trails, user permissions, and traceable review workflows during inspection readiness. That shift changes purchase behavior inside the Karl Fischer titrators market, since older analog units can still measure water but cannot support the digital evidence chain that regulated plants increasingly need. As a result, replacement demand is staying active even where sample volumes are stable, and the decision is often framed around data integrity risk rather than pure analytical performance. This is one reason the Karl Fischer titrators market is seeing firm demand for integrated systems instead of a broad return to lower-cost manual setups.

Battery-Electrolyte And Electrode Moisture Control

The market is also being supported by battery manufacturing, where trace moisture control has become a process gate rather than a laboratory preference. Mettler-Toledo’s battery application material highlights that water in lithium-ion battery materials can contribute to hydrofluoric acid formation and other reactions that reduce performance and raise safety concerns. Chemistry World makes the same point from an application perspective, noting that moisture testing is now tied closely to batteries, fuels, and other industrial settings where water content has direct quality and safety consequences. This matters for the Karl Fischer titrators market because battery producers cannot rely on broad screening alone when electrolytes and electrodes require trace-level measurement with tight repeatability. The application also favors coulometric systems and specialized reagent choices, which pushes demand toward higher-value configurations instead of basic entry platforms. With global electric vehicle capacity still expanding, each new line creates repeated testing points that support durable instrument demand rather than one-time lab purchases[1]International Energy Agency, “Global EV Outlook 2024,” IEA, iea.org.

Lyophilized Biologics Residual-Moisture Testing

The market is gaining another layer of support from lyophilized biologics, where residual moisture must stay within narrow boundaries to protect product stability and shelf life. Merck’s technical documentation on lyophilisates and Mettler-Toledo’s vaccine application material both frame Karl Fischer titration as a practical reference approach for moisture determination in freeze-dried products. Scientific literature also shows why the Karl Fischer titrators market remains relevant even when other tools enter the workflow, since near-infrared approaches used in freeze-drying still require reference methods for calibration and validation. Because lyophilized biologics often operate in low residual moisture ranges, the commercial pull is strongest for coulometric systems that offer stable trace-level measurement without ongoing titer drift concerns. That tilts the Karl Fischer titrators market toward premium instruments in a niche that may be smaller in volume but stronger in revenue quality. It also means alternative methods do not eliminate demand here because they still depend on Karl Fischer data as the accepted benchmark in many workflows.

Automation, Audit Trails, And LIMS Integration

Automation is reshaping the market because laboratories increasingly judge instruments by workflow control and data handling, not only by analytical endpoint accuracy. Metrohm’s OMNIS platform and automation material show how unattended sample handling, parallel workstations, and software-linked titration can turn Karl Fischer testing into part of a broader digital lab environment. Metrohm also linked digitalization to reduced manual steps and better record control in its 2025 communication on titration workflows, while Mettler-Toledo continues to position EVA systems around fast, compliant water-content analysis. This changes the economics of the market because one automated platform can replace several scattered manual routines and reduce operator variability across sites. Large pharmaceutical manufacturers and contract labs respond well to that model because they need repeatable procedures, centralized reviews, and fewer transcription errors across distributed quality teams. The result is that automation is acting less like a one-off equipment upgrade and more like a permanent design preference in the Karl Fischer titrators market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Instrument And Reagent Lifecycle Cost | -0.3% | Global, with greatest pressure in price-sensitive Asia-Pacific and South American laboratories | Medium term (2-4 years) |

| Alternative Moisture-Analysis Method Substitution | -0.4% | Global, with strongest substitution pressure in food, polymers, and fertilizers | Long term (≥ 4 years) |

| Matrix Interference And Difficult Sample Preparation | -0.2% | Global, with concentration in petrochemical, food, and specialty polymer applications | Medium term (2-4 years) |

| Methanol And Reagent-Handling EHS Pressure | -0.2% | Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Alternative Moisture-Analysis Method Substitution

The market faces its clearest substitution risk from near-infrared spectroscopy in repetitive testing environments where samples are stable and speed matters more than direct water reaction chemistry. Metrohm’s application material and recent analytical literature show why NIR is attractive, since it can deliver fast, non-destructive results and fits well with inline process control. Even so, the Karl Fischer titrators market remains protected in regulated and trace-level uses because Karl Fischer titration is still treated as a direct and stoichiometric method for water, while NIR depends on model quality and calibration discipline. In practical terms, substitution pressure is therefore strongest at the lower end of the market, especially in high-throughput food and polymer settings where labs test similar matrices repeatedly. It is far less disruptive in pharmaceuticals, biologics, and battery materials, where reference testing and trace sensitivity still matter more than screening speed. This creates a split pattern in the market, with entry and mid-range units more exposed than premium trace-moisture platforms.

High Instrument And Reagent Lifecycle Cost

Cost remains a real ceiling for the market because ownership involves more than the purchase price of the instrument itself. Reagents, electrode upkeep, solvent waste handling, calibration standards, periodic service, and operator training all add recurring cost that weighs more heavily on smaller laboratories and academic users. KEM has tried to ease that burden with newer systems that lower power use and improve operating efficiency, but even those product improvements do not remove the full lifecycle expense attached to routine Karl Fischer testing. This keeps the Karl Fischer titrators market sensitive to procurement budgets in Southeast Asia, Latin America, and independent contract labs that compare every instrument purchase against simpler moisture methods. It also explains why semi-automated and basic configurations continue to hold space even as premium systems gain attention in regulated facilities. Unless vendors can make automation easier to finance and easier to maintain, the market will continue to see a gap between high-end demand and broad-based penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Volumetric Anchors Revenue While Coulometric Titrators Gain Trajectory

Volumetric systems held 62.3% of Karl Fischer titrators market share in 2025, which kept them firmly in the lead across the product mix. Their position reflects a wide operating range for samples that contain moderate to high moisture, which suits routine work across pharmaceuticals, chemicals, and food ingredients. The Karl Fischer titrators market still depends heavily on these systems because many quality control labs handle varied sample types and need one method that can move across solvents, powders, and finished materials with less configuration change. Compendial familiarity also matters, since laboratories in regulated sectors tend to prefer methods that are already embedded in routine procedures and internal validation packages. Volumetric instruments therefore remain the practical default for many multi-product facilities, especially where trace-level sensitivity is not the central requirement.

Coulometric Karl Fischer titrators are forecast to grow at 4.4% CAGR through 2031, which places them well above the overall category pace. Their strength comes from trace-moisture work, where electrochemical iodine generation avoids routine titer standardization and supports stronger control at low water levels. The market is pulling these systems into battery electrolytes, lyophilized biologics, and moisture-sensitive intermediates, all of which punish small measurement errors more severely than conventional samples. Vendors are responding with premium launches and application-specific design choices, which shows where current product investment is concentrating[2]Metrohm, “OMNIS KF Titrators,” Metrohm, metrohm.com. As a result, the Karl Fischer titrators market is becoming more polarized by use case, with volumetric systems protecting the broad base and coulometric systems capturing the sharper growth edge.

By Technology: Automated Platforms Consolidate Leadership Across Tiers

Automated platforms accounted for 62.2% of Karl Fischer titrators market size in 2025, and they are projected to grow at 4.5% CAGR through 2031. That combination shows that automation is already mainstream inside the market and is still gaining share from manual and semi-automated workflows. Automated systems reduce operator-to-operator variation, support unattended sequences, and strengthen audit readiness through controlled user access and digital records. This is especially valuable in regulated laboratories, where the cost of poor documentation can exceed the cost of the instrument itself. The market is therefore seeing automation move from a productivity feature to a compliance and standardization requirement.

Competitive pressure reinforces this transition because vendors now defend technology positions through software, compliance architecture, and service support more than through hardware alone. Premium suppliers continue to lead in integrated automation, while lower-cost manufacturers push basic automation features into price points that once belonged to semi-automated products. This squeezes the middle of the market, where legacy products risk looking too expensive for basic labs and too limited for digitalized ones. The likely result is continued migration toward either high-compliance automated platforms or simpler budget systems with only essential workflow support. That leaves fully manual technology as a residual niche rather than a future growth engine in the Karl Fischer titrators market.

By End User: Pharma Anchors Demand While Energy Materials Drive Acceleration

Pharmaceutical and biotechnology companies represented 38.5% of revenue in 2025, making them the largest end-user block in the Karl Fischer titrators market. Their position is tied to routine moisture control in active ingredients, excipients, formulations, and stability programs, where validated water determination is tied directly to product quality and release confidence. The Karl Fischer titrators market remains deeply linked to this user group because regulated pharma workflows favor direct reference methods over proxy techniques whenever moisture can affect potency, shelf life, or formulation behavior. Biologics development strengthens that link further, especially for lyophilized products where residual moisture sits in a narrow operating band and analytical errors carry higher consequences. This makes pharmaceutical demand resilient even when broader capital spending slows, since many purchases are tied to compliance, validation, and product risk management.

Chemical, petrochemical, and energy materials users are forecast to grow at 5.3% CAGR through 2031, making them the fastest-growing end-user segment in the market. The strongest lift comes from lithium-ion battery materials, where water content can damage electrolyte stability and downstream performance, which gives coulometric Karl Fischer testing a clear role in quality control. Petrochemical, lubricant, and solvent applications add another layer of demand because moisture often affects storage, processing, or product conformance. Food testing, independent QA and QC laboratories, and research institutions round out the user mix and help stabilize the market outside the largest regulated sectors. Together, these users make the category less dependent on a single end market, even though pharmaceuticals still set the tone for compliance and system design.

Geography Analysis

Asia-Pacific held 35.2% of Karl Fischer titrators market share in 2025, and the region is projected to expand at 4.8% CAGR through 2031. That combination makes Asia-Pacific both the largest and fastest-growing regional block in the Karl Fischer titrators market. Japan remains an important technology anchor because local instrument makers and long-established laboratory practices support a deep installed base across pharmaceutical and chemical testing. China and India are widening the regional demand base as pharmaceutical manufacturing, outsourced analytical work, and battery-related testing continue to grow in scale. The Karl Fischer titrators market also benefits here from a wide spectrum of buyers, ranging from premium regulated labs to cost-sensitive industrial users who still require routine moisture measurement.

The region’s growth profile is stronger than its headline share alone suggests because it combines mature instrumentation demand with new application build-out. Battery materials and cell production give the Karl Fischer titrators market a clear opening in China, South Korea, and Japan, where moisture control is tied closely to product safety and yield. Pharmaceutical outsourcing also supports purchases of automated systems, since CROs and CDMOs need reliable documentation and repeatable testing across international client programs. That favors platforms with audit trails, software control, and stronger workflow standardization rather than only low upfront cost. At the same time, mid-tier price competition remains important in Asia-Pacific, which is why both premium automation and lower-cost alternatives can expand side by side in the Karl Fischer titrators market.

North America and Europe form a mature demand cluster where the Karl Fischer titrators market is driven more by replacement and workflow modernization than by first-time adoption. Regulated pharmaceutical production and advanced laboratory infrastructure support steady demand for connected systems with strong data integrity features. Europe also has an added chemistry dimension because reagent-handling and environmental pressure encourage interest in methanol-free or imidazole-free formulations alongside instrument upgrades. The Middle East and Africa, along with South America, remain smaller but relevant parts of the Karl Fischer titrators market, supported by petrochemical refining, food processing, pharmaceutical quality control, and distributor-led equipment access. These regions are more budget sensitive, which gives cost-competitive systems room to grow even while premium suppliers retain an advantage in highly regulated applications.

Competitive Landscape

The Karl Fischer titrators market is moderately concentrated, with a limited group of established European and Japanese vendors holding strong positions through installed base depth, application expertise, and service reach. Metrohm, Mettler-Toledo, and Xylem Analytics through SI Analytics remain prominent because they compete on workflow breadth, compliance capability, and laboratory integration rather than on hardware alone. This gives the Karl Fischer titrators market a competitive structure where buyers often evaluate software environment, service assurance, and method support at the same time as measurement performance. It also keeps barriers relatively high in regulated accounts because vendors with proven validation support and global service networks enjoy a clear credibility advantage. As a result, competition is active but not fully open, especially in pharmaceutical and other tightly controlled environments.

Recent product activity shows where leading suppliers are placing their bets inside the Karl Fischer titrators market. Metrohm launched the OMNIS Coulometer and Sample Robot Oven in April 2024, reinforcing its focus on automated, higher-throughput workflows for advanced moisture testing. Mettler-Toledo introduced new EVA Karl Fischer platforms, which signals continued investment in modernized user interfaces, faster operation, and software-linked compliance support. Metrohm also highlighted digital titration workflows in 2025, including connectivity and reduced manual data handling, which shows how vendors are building defensibility through lab-wide process fit rather than isolated instrument features. These moves indicate that the Karl Fischer titrators market is rewarding suppliers that can turn moisture testing into a controlled, scalable, and auditable process.

Japanese specialists continue to matter because they retain strong positions in Asia-Pacific laboratories that value reliability, familiarity, and long-term application support. KEM’s current volumetric and coulometric offerings show that the company remains active across both mainstream and trace-moisture needs, which helps preserve its role in pharmaceutical, chemical, and industrial testing environments[3]KEM, “MKC-710M Karl Fischer Moisture Titrator, Coulometric Titration,” Zematra UK, zematra.co.uk. The Karl Fischer titrators market also includes niche strength in application-specific areas where vendors can tailor extraction, sampling, or difficult-matrix handling to sectors such as oils, lubricants, and energy materials. That said, the most meaningful pricing pressure is coming from Chinese domestic suppliers in the mid-tier range, where acceptable performance at lower cost is improving buyer confidence even without matching premium service depth. This is pushing the Karl Fischer titrators market toward a sharper split between premium software-led ecosystems and more price-driven hardware competition.

Karl Fischer Titrators Industry Leaders

Mettler-Toledo

Metrohm

Xylem Analytics / SI Analytics

Hanna Instruments

Kyoto Electronics Manufacturing (KEM)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Brenntag announced the opening of its new Innovation & Application Center in Andheri East, Mumbai, marking a major expansion of its technical and development capabilities for the food and beverage industry across the region. Analytical instruments, including texture analyzers, viscometers, titrators, density meters, refractometers, moisture analyzers, and water activity meters, provide detailed insight into product quality and performance.

- September 2025: Biosolve developed a new set of reagents (HYDROQUANT) free of Carcinogenic, Mutagenic & Reprotoxic (CMR) substances designed for the Karl Fischer titrations.

Global Karl Fischer Titrators Market Report Scope

As per the scope of the report, Karl Fischer titrators are analytical instruments used to determine the water content in a sample through the Karl Fischer titration method. This method involves a chemical reaction where iodine reacts with water in the presence of a suitable reagent, allowing precise measurement of moisture levels in various substances.

The segmentation of the Karl Fischer titrators market is categorized by product type, technology, end user, and geography. By product type, the market includes volumetric Karl Fischer titrators and coulometric Karl Fischer titrators. By technology, it is segmented into automated, semi-automated, and manual. By end user, the market serves pharmaceutical and biotechnology firms, chemical, petrochemical, and energy material producers, food testing and processing labs, CROs, CDMOs, and contract testing entities, academic and research institutions, and independent and industrial QA/QC labs. Geographically, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Volumetric Karl Fischer Titrators |

| Coulometric Karl Fischer Titrators |

| Automated |

| Semi-Automated |

| Manual |

| Pharmaceutical and Biotechnology Companies |

| Chemical, Petrochemical, and Energy Material Manufacturers |

| Food Testing and Processing Laboratories |

| CROs, CDMOs, and Contract Testing Organizations |

| Academic and Research Institutes |

| Independent and Industrial QA/QC Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Volumetric Karl Fischer Titrators | |

| Coulometric Karl Fischer Titrators | ||

| By Technology | Automated | |

| Semi-Automated | ||

| Manual | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Chemical, Petrochemical, and Energy Material Manufacturers | ||

| Food Testing and Processing Laboratories | ||

| CROs, CDMOs, and Contract Testing Organizations | ||

| Academic and Research Institutes | ||

| Independent and Industrial QA/QC Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected growth outlook for Karl Fischer titrators through 2031?

The Karl Fischer titrators market is expected to move from USD 226.64 million in 2026 to USD 260.83 million by 2031 at a CAGR of 2.85%, reflecting steady replacement demand and specialized growth in battery and biologics testing.

Why do pharmaceutical companies still rely on Karl Fischer titration?

Pharmaceutical users continue to rely on Karl Fischer titration because compendial workflows still favor direct water determination, and regulated labs need methods that align with documentation, validation, and audit-trail requirements.

Which product segment is leading revenue and which one is growing fastest?

Volumetric systems led revenue with 62.3% share in 2025, while coulometric systems are growing faster at 4.4% CAGR because they are better suited to trace-moisture work in batteries and lyophilized products.

Why is Asia-Pacific the most important regional cluster?

Asia-Pacific held 35.2% share in 2025 and is growing at 4.8% CAGR because it combines mature demand in Japan with expanding pharmaceutical, outsourcing, and battery-related testing activity across the wider region.

What is the main substitution risk for Karl Fischer titrators?

Near-infrared spectroscopy is the main long-term substitute in repetitive testing environments, but it is less disruptive where direct reference testing and trace sensitivity remain essential.

What features are shaping vendor competition most strongly in 2026?

Automation, audit trails, unattended throughput, and software integration are shaping competition most strongly because buyers increasingly want moisture testing to fit a wider digital laboratory workflow.

Page last updated on: