Market Overview

| Study Period | 2020 - 2031 |

|---|---|

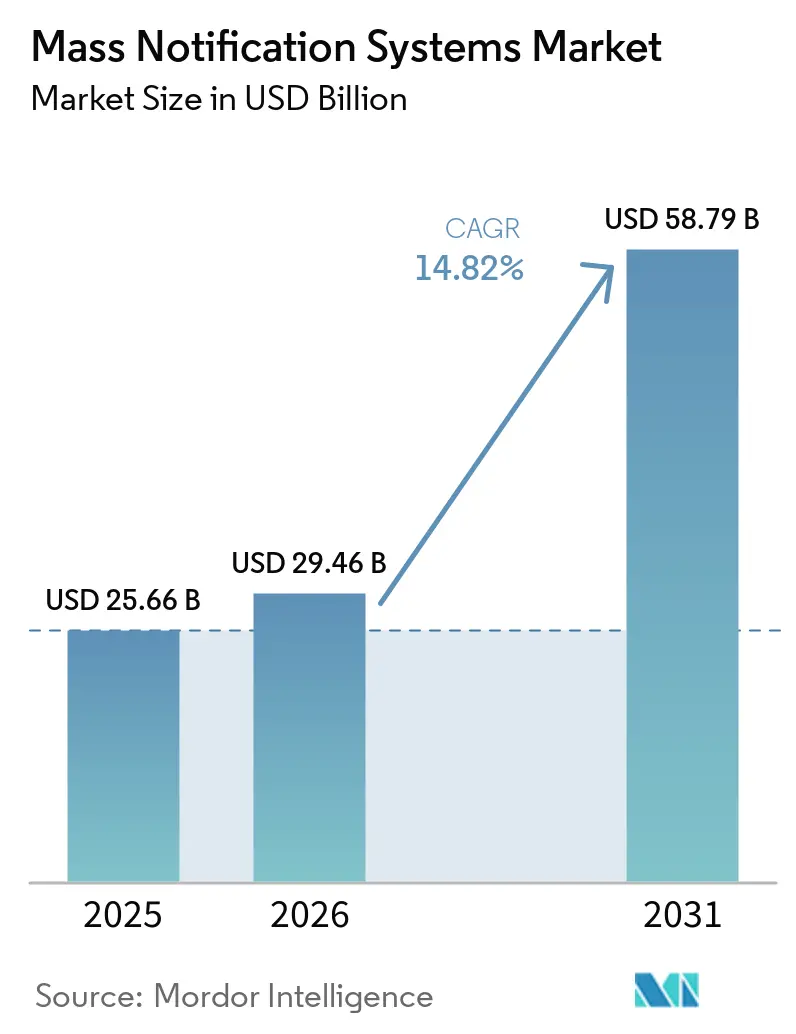

| Market Size (2026) | USD 29.46 Billion |

| Market Size (2031) | USD 58.79 Billion |

| Growth Rate (2026 - 2031) | 14.82% CAGR |

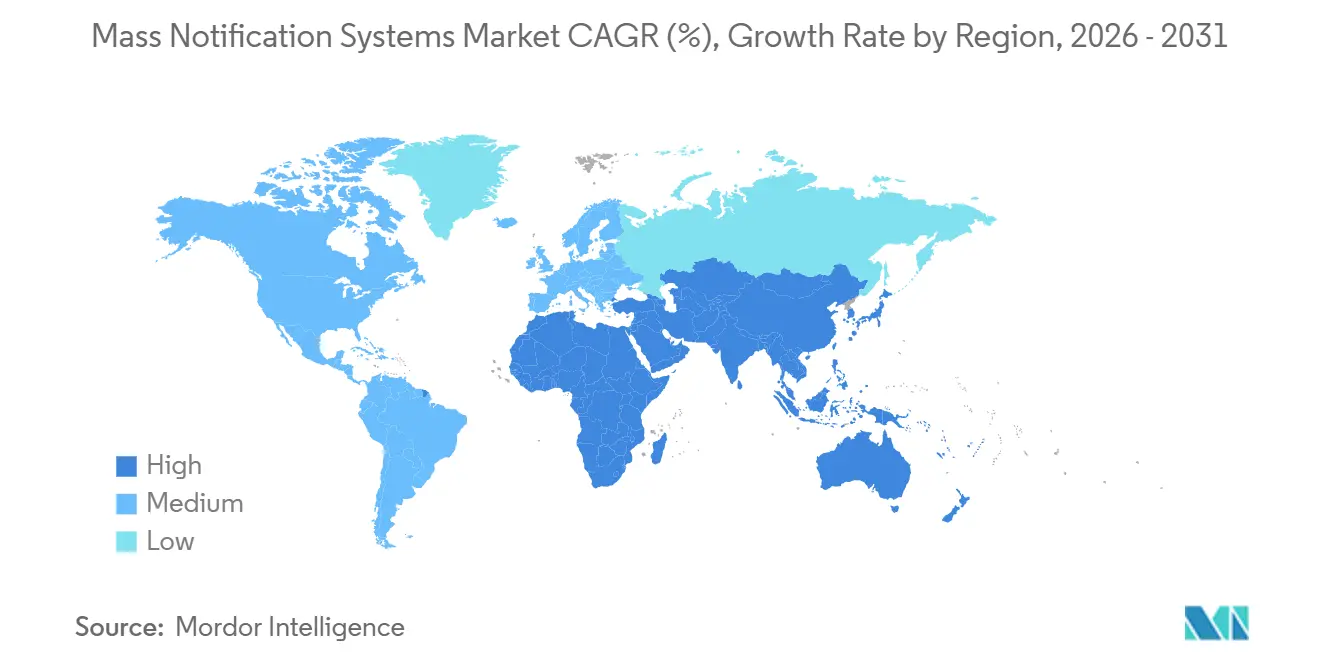

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mass Notification Systems Market Analysis by Mordor Intelligence

The mass notification systems market size is expected to grow from USD 25.66 billion in 2025 to USD 29.46 billion in 2026 and is forecast to reach USD 58.79 billion by 2031 at 14.82% CAGR over 2026-2031. Heightened climate risks, tougher safety regulations, and technology advances are converging to keep adoption momentum high. Organizations now expect a single platform to reach people through text, voice, social, desktop pop-ups, public address, and IoT sensors, all while tailoring messages to location and role. Cloud deployment dominates because enterprises want immediate scale and remote management, yet the hybrid model is catching up as security teams look for tighter on-premise control. Suppliers that master integration with 5G, analytics, and legacy infrastructure are best positioned to win new projects as spending spreads from government to healthcare, education, utilities, and small businesses.

Key Report Takeaways

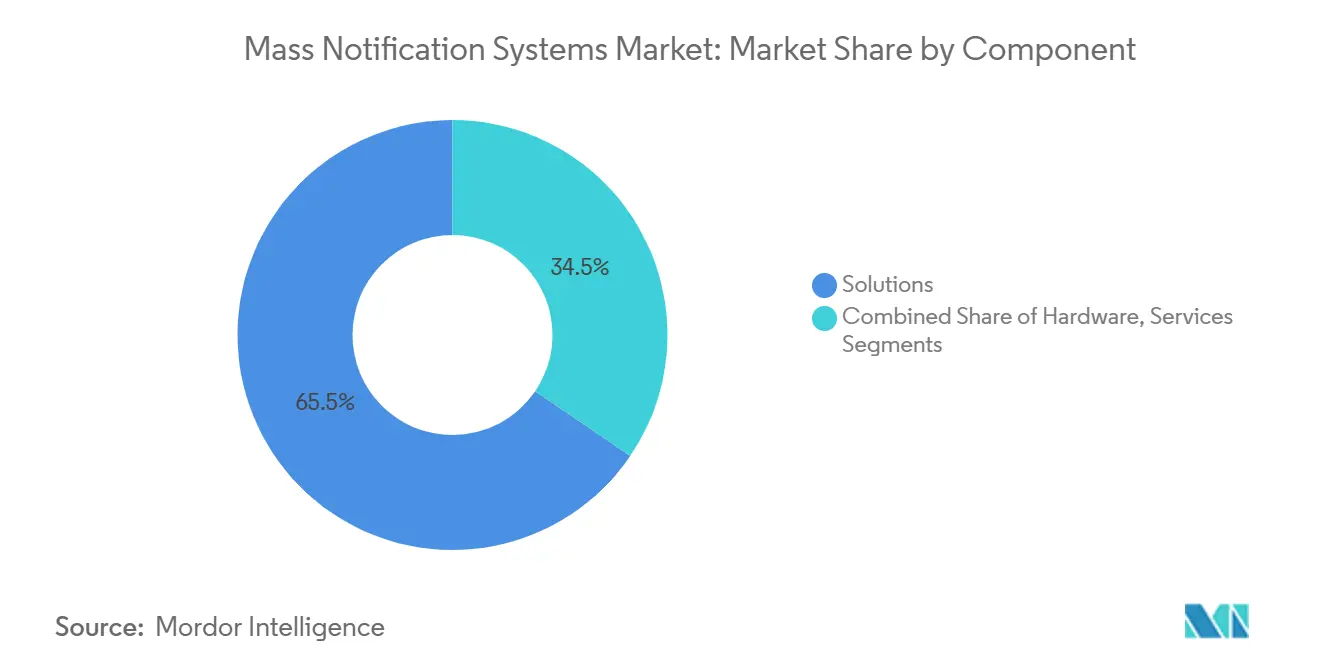

- By component, solutions held 65.50% of mass notification systems market share in 2025, while services are projected to grow at an 17.9% CAGR through 2031.

- By deployment model, cloud captured 70.30% of the mass notification systems market in 2025; hybrid is forecast to expand at a 19.65% CAGR to 2031.

- By solution purpose, integrated public alert and warning platforms led with 38.60% revenue share in 2025, whereas business continuity and disaster recovery is advancing at a 20.85% CAGR.

- By organization size, large enterprises accounted for 61.30% share of the mass notification systems market size in 2025, while SMEs are growing at a 22.1% CAGR.

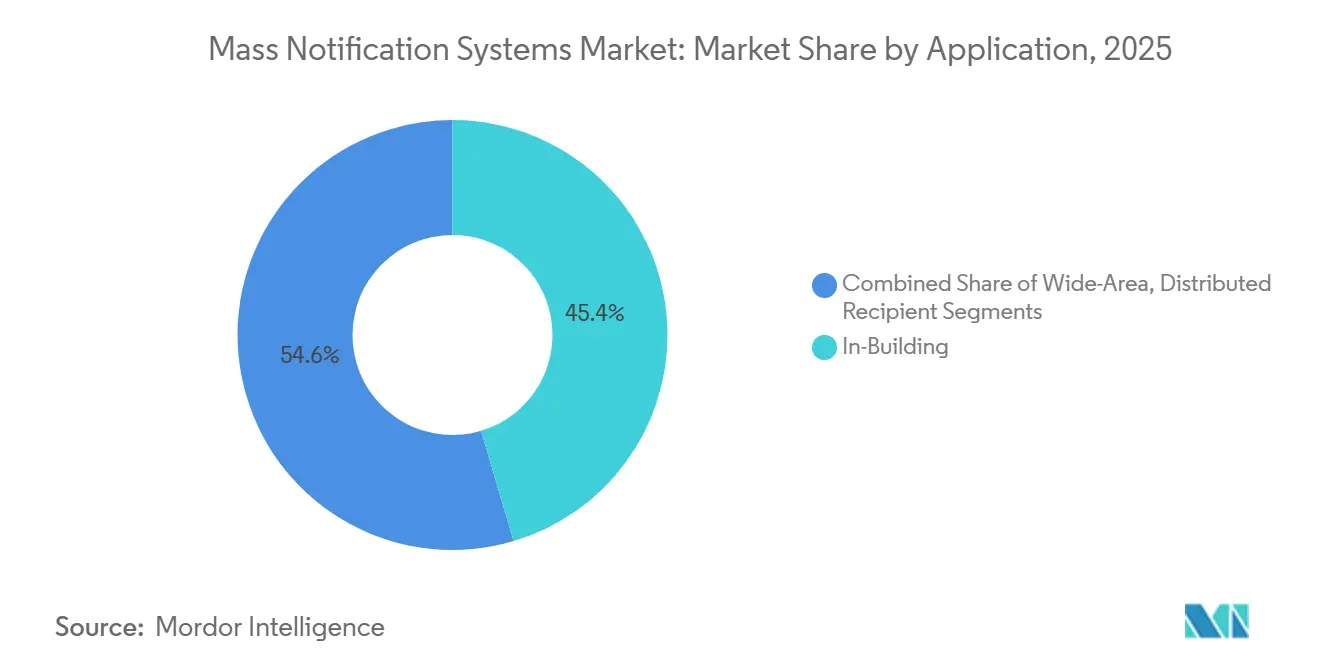

- By application, in-building solutions commanded 45.40% of the mass notification systems market size in 2025; distributed recipient systems are pacing the field at a 18.95% CAGR.

- By end-user vertical, government and defense led with 27.60% share in 2025, and healthcare is projected to climb at a 21.05% CAGR to 2031.

- By geography, North America retained 39.60% share of the mass notification systems market in 2025, but Asia-Pacific is the fastest-growing region with a 16.9% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mass Notification Systems Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated 5G roll-outs enabling multimedia alerting | +3.5% | Asia-Pacific with spillover to North America | Medium term (2-4 years) |

| EU Article 110 multi-channel public-warning mandate | +2.8% | Europe with global compliance ripple effects | Short term (≤ 2 years) |

| Climate-related catastrophes spurring municipal deployments | +2.1% | North America, rising relevance in Asia-Pacific | Long term (≥ 4 years) |

| Campus digitization fostering BYOD safety ecosystems | +1.9% | North America and Europe | Medium term (2-4 years) |

| Utilities’ grid-modernization projects demanding OT/IT-converged alert platforms | +1.4% | North America, Europe, advanced Asia-Pacific | Long term (≥ 4 years) |

| Rapid SME adoption of cloud-based notification platforms | +1.2% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G roll-outs enabling real-time multimedia alerting

5G brings gigabit throughput and millisecond latency, allowing platforms to push high-definition video, floor plans, and interactive evacuation maps rather than plain text. Urban centers in Japan, South Korea, and Singapore already use location-based warnings that adapt as recipients move through a city. Operators report 20% higher connectivity satisfaction during large events compared with 4G, a data point that reassures emergency managers planning for congested networks.[1]Ericsson, “5G Elevates Connectivity at 2024’s Biggest Events,” ericsson.com Vendors able to embed network- slicing and edge-compute features are differentiating on speed, redundancy, and content richness. As spectrum auctions continue and device penetration rises, the mass notification systems market will capture incremental public-safety funding tied to 5G coverage targets.

EU’s EECC Article 110 driving multi-channel compliance

The code obliges all 27 EU states to reach “the maximum possible affected population,” pushing governments to marry cell broadcast, location-based SMS, and app alerts. Funding streams earmarked for compliance have accelerated roll-outs of hybrid platforms that support multilingual content, two-way messaging, and cross-border interoperability.[2]European Commission, “Emergency Communication and Public Warning Systems,” interoperable-europe.ec.europa.eu Commercial users are following the same architecture to streamline business continuity communications, pulling private investment into the mass notification systems market sooner than projected.

Escalating climate catastrophes accelerating municipal deployments

Hurricanes, wildfires, and floods are becoming more frequent and severe, prompting city leaders to integrate sensor networks with automated messaging workflows. Early adopters in California and Florida now trigger neighborhood-level evacuation notices within seconds of a fire perimeter change, improving compliance and reducing casualty rates. These successes are fueling new grants and bond issuances earmarked for modern alerts, lifting long-term demand across the mass notification systems market.[3] Security World Market, “Rising Demand Drives Strong Growth for Mass Notification Systems,” securityworldmarket.com

Campus digitization transforming educational safety

Universities outfitted with campus-wide Wi-Fi, digital signage, and mobile apps are turning personal smartphones into the primary safety channel. BYOD policies enable messages filtered by building, class schedule, or role, while two-way chat features allow students to send live updates to security teams. Integrations with access control and video management systems automate lockdowns when an anomaly is detected, cutting the gap between incident detection and notification

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented spectrum policies delaying cell broadcast adoption | -1.2% | Africa and parts of Middle East | Medium term (2-4 years) |

| Rising cyber-insurance premiums elevating cloud TCO in healthcare | -0.9% | North America and Europe | Short term (≤ 2 years) |

| Alarm fatigue concerns curbing message frequency in large enterprises | -0.7% | Global, especially enterprise environments | Medium term (2-4 years) |

| Limited multilingual content libraries slowing uptake in the Nordics | -0.5% | Nordic countries, ripple effect on multilingual markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented spectrum policies hampering African adoption

Cell broadcast relies on harmonized spectrum guidelines, yet policies vary widely across 54 African nations. Vendors face custom integrations for each carrier, prolonging pilots and inflating costs, which slows public-safety deployments even as 3G and 4G coverage climbs above 90%. Regional harmonization efforts are underway, but until they mature, growth lags other emerging regions.

Cyber-insurance premiums elevating cloud TCO in healthcare

Premium increases of 30-50% have altered cost-benefit analyses for moving patient communications to the cloud. Hospitals now insist on end-to-end encryption, zero-trust architecture, and on-premise data vaults, nudging many toward hybrid deployments. Vendors must absorb extra certification expenses or risk losing bids to incumbents with proven compliance track records

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software platforms consolidate leadership

The mass notification systems market size for solutions reached USD 16.8 billion in 2025, translating to a 65.50% share as agencies and enterprises replaced hardware-centric setups with command-center software. Software unifies SMS, voice, email, sirens, and signage under one console, reducing training needs and license duplication. In the second half of the decade, analytics modules that predict recipient behavior are expected to prompt upgrades among existing customers, keeping solutions revenue on a double-digit climb. Services, while a smaller slice, are advancing at an 17.9% CAGR because integration, customization, and 24/7 monitoring demand specialist skills.

Hardware retains a foothold in plants, airports, and schools where strobe beacons, wall-mounted speakers, and outdoor sirens remain mission critical. Yet manufacturers are embedding IP connectivity in these devices so they can report status back to the central platform. Professional services teams are packaging assessments, regulatory consulting, and lifecycle maintenance into multi-year contracts, creating predictable cash flow for vendors and lowering surprise costs for clients. Such managed models are further widening the solutions edge within the mass notification systems market.

By Deployment Mode: Cloud first, hybrid rising

Cloud captured 70.30% of the mass notification systems market in 2025 as administrators favored instant scale, pay-as-you-go pricing, and hassle-free upgrades. SaaS platforms also simplified multi-tenant management for large enterprises spanning dozens of sites. That model resonates with SMEs that lack IT staff, fueling the highest net-new logo count. Even so, data-sovereignty rules, the need for on-site survivability, and concerns over vendor lock-in are steering financial services, utilities, and hospitals toward hybrid approaches. Hybrid adoption is forecast to grow at 19.65% CAGR, the fastest rate in deployment choices.

On-premise deployments are shrinking but will not disappear. Critical infrastructure owners often keep a local instance running on hardened servers so messages still flow when external links fail. Containerized architectures now let operators shift workloads between public clouds and local clusters, balancing cost and control. As such flexibility becomes mainstream, the mass notification systems market will likely see blurred lines between “cloud” and “on-premise,” with buyers selecting per-workload policies rather than a single blanket model.

By Solution Purpose: Public alert systems anchor spending

Integrated public alert and warning systems held 38.60% of 2025 revenue, driven by state and national mandates. These platforms interface with telecom networks to broadcast evacuation orders, weather alerts, and Amber-style notices. Uptake accelerated after tests proved that cell broadcast reaches nearly every handset, including non-smartphones, making it indispensable in crises. Business continuity and disaster recovery solutions are now the growth engine; their 20.85% CAGR reflects private-sector demand for rapid outage mapping, supply-chain disruption alerts, and cyber incident messaging.

The mass notification systems market size for interoperable emergency communications is also climbing as agencies require cross- jurisdiction collaboration. Standards such as the Common Alerting Protocol are now embedded in RFPs, forcing suppliers to certify interoperability. Added value comes from content-rich features like geocoded maps and push-to-talk voice, which improve clarity and reduce alarm fatigue. Flexibility to pivot between public safety and enterprise workflows is fast becoming a core buying criterion.

By Application: In-building solutions remain vital

In-building platforms represented 45.40% of the market in 2025 because facility managers must reach every occupant during events such as fires or active assailants. These systems interface with fire panels, strobe beacons, and public-address speakers to overcome high ambient noise. Digital signage and desktop takeovers increase visibility even when mobile coverage lags. As organizations reopen hybrid offices, they are repurposing conference room displays and desk phones as additional endpoints, strengthening the segment’s staying power.

Distributed recipient solutions, however, are advancing at a 18.95% CAGR, mirroring workforce mobility and remote learning. They rely on cloud gateways to locate users via GPS or Wi-Fi and then deliver role-based messages, making them indispensable for field technicians, logistics drivers, and telehealth staff. Wide-area systems used by municipalities are also layering geospatial data so warnings stay relevant and minimize fatigue. These trends collectively expand the addressable base of the mass notification systems market while encouraging buyers to adopt a mix of in-building and distributed capabilities.

By End-User Vertical: Government leads, healthcare accelerates

Government and defense held 27.60% of 2025 revenue owing to statutory duty to warn the public and protect personnel. Investments cover everything from outdoor sirens and radio interrupts to secure mobile apps for first responders. Program budgets are shifting toward cloud-based analytics that model population movement and predict shelter capacity, which lifts long-term services revenue. Healthcare facilities are the fastest riser, with a 21.05% CAGR, because patient-safety rules now require rapid code alerts, staff recalls, and visitor notifications.

Hospitals integrate paging, nurse-call, and clinical messaging into one environment to prevent alarm overload and reduce response time to critical events such as cardiac arrest. Education, utilities, and transportation follow closely, each driven by sector-specific regulations and IoT instrumentation. As vertical use cases proliferate, suppliers with configurable templates and open APIs are winning share in the mass notification systems market due to faster deployment and lower customization costs.

Geography Analysis

North America retained 39.60% of 2025 revenue, reflecting mature telecommunications infrastructure, grant funding, and a track record of extreme weather events. Municipalities now embed mass alerting into broader smart-city platforms that tie traffic sensors, flood gauges, and wildfire cameras to automatic outbound messaging. Cloud-native upgrades also coincide with the region’s high cyber-insurance requirements, ensuring data protection features are woven into every deployment.

Asia-Pacific is expanding at a 16.9% CAGR, the highest among all regions. Accelerated 5G roll-outs in South Korea, Japan, and Australia let agencies attach video clips and multilingual subtitles to alerts, boosting comprehension in dense cities. Government stimulus for disaster resilience in typhoon-prone nations such as the Philippines is funneling fresh capital into the mass notification systems market. Meanwhile China’s mega-city projects integrate alerts with surveillance cameras and e-wallet super-apps, blending public safety with everyday digital behavior.

Europe sits between these extremes, but its growth is dominated by regulatory compliance. The EECC Article 110 deadline drove every member state to budget for multi-channel warnings, while GDPR pushed vendors to invest in consent management and data minimization. The Nordic region’s focus on multilingual content slows some projects but ultimately broadens product capability for export. The United Kingdom, operating outside EU directives, is drafting its own standards that still align with cell broadcast best practice, ensuring continued cross-border interoperability.

Competitive Landscape

The mass notification systems market is moderately concentrated. A mix of security giants and niche specialists compete on breadth, ease of integration, and vertical expertise. Motorola Solutions deepened its stack with the acquisition of Rave Mobile Safety, pairing land-mobile radio, video, and command-center software under one umbrella. Honeywell, Siemens, and Eaton still leverage global fire-alarm channels but now emphasize software orchestration to fend off cloud-native disruptors.

Pure-play vendors such as Everbridge, OnSolve, and AlertMedia set pace in incident orchestration by embedding AI for message optimization, predictive analytics, and automated compliance checks. Genasys and Blackberry AtHoc capitalize on secure government networks, offering high-decibel acoustic devices and hardened messaging for defense clients. Regional players in Europe and Asia win deals by tailoring language packs and designing templates that align with local regulations.

Strategic partnerships are multiplying. Telecom operators bundle notification APIs with enterprise mobility-as-a-service, while hyperscale clouds court suppliers to host SaaS platforms with credits and co-marketing. System integrators add value through rapid deployment kits and managed resilience centers. As acquisitions continue, the top five vendors are expected to command close to 50% of global revenue by 2030, yet localized innovation keeps barriers to entry moderate, sustaining healthy competition within the mass notification systems market.

Mass Notification Systems Industry Leaders

Everbridge Inc.

Motorola Solutions Inc.

Honeywell International Inc.

Siemens AG

Blackberry AtHoc Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Genasys Inc. reported record bookings of USD 111 million in FY 2024 and a backlog above USD 40 million, underscoring demand for protective communications across government and public safety sectors.

- April 2025: Genasys secured multi-year contracts with the Utah Department of Corrections and Los Angeles County, expanding its U.S. government footprint

- March 2025: AlertMedia was named a Customers’ Choice in the Gartner Peer Insights report, scoring 4.7/5 from 153 reviews and reinforcing its enterprise traction

- November 2024: Ericsson research showed 5G users achieved 20% higher connectivity satisfaction during large events than 4G users, validating 5G’s role in reliable emergency communications

Global Mass Notification Systems Market Report Scope

Mass Notification Systems are software solutions deployed to send out mass alerts as part of an emergency communication plan via text message, email, phone, or broadcast via speakers/sirens or television. These solutions are used by different end-user verticals, including Healthcare, Government, Educational sector (K-12), Enterprises, Energy and Utilities, etc., for business continuity, disaster management, emergency response, and communications, etc. Sometimes, the solutions enable notifications automatically triggered by warning events, such as extreme weather. Vendors also offer solutions that allow users to send information with one click, with a pre-configured message to a network of citizens, members, or subscribers.

The Mass Notification Systems Market is segmented by Component (Solution, Service), Deployment (On-premise, Cloud), Application (In-building, Wide Area, Distributed Recipient), Purpose of Deployment (Business Continuity and Disaster Recovery, Integrated Public Alert and Warning, Interoperable Emergency Communication), End-User Vertical (Energy and Utilities, Healthcare, Commercial, Government, Education), and Geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Component

| Hardware | Fire Alarm Control Panels |

| Public Address and Voice Evacuation Systems | |

| Notification Beacons and Digital Signage | |

| Solutions | Emergency/Mass Notification Software |

| Incident Management and Situation Awareness | |

| Services | Professional (Consulting, Integration) |

| Managed Services |

By Deployment Mode

| On-premise |

| Cloud |

| Hybrid |

By Solution Purpose

| Business Continuity and Disaster Recovery |

| Integrated Public Alert and Warning |

| Interoperable Emergency Communication |

By Organization Size

| Large Enterprises |

| Small and Mid-size Enterprises (SMEs) |

By Application

| In-Building |

| Wide-Area |

| Distributed Recipient |

By End-User Vertical

| Government and Defense |

| Energy and Utilities |

| Healthcare |

| Education |

| Commercial and Industrial |

| Transportation and Logistics |

| IT and Telecommunications |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Middle East | GCC |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia |

| By Component | Hardware | Fire Alarm Control Panels |

| Public Address and Voice Evacuation Systems | ||

| Notification Beacons and Digital Signage | ||

| Solutions | Emergency/Mass Notification Software | |

| Incident Management and Situation Awareness | ||

| Services | Professional (Consulting, Integration) | |

| Managed Services | ||

| By Deployment Mode | On-premise | |

| Cloud | ||

| Hybrid | ||

| By Solution Purpose | Business Continuity and Disaster Recovery | |

| Integrated Public Alert and Warning | ||

| Interoperable Emergency Communication | ||

| By Organization Size | Large Enterprises | |

| Small and Mid-size Enterprises (SMEs) | ||

| By Application | In-Building | |

| Wide-Area | ||

| Distributed Recipient | ||

| By End-User Vertical | Government and Defense | |

| Energy and Utilities | ||

| Healthcare | ||

| Education | ||

| Commercial and Industrial | ||

| Transportation and Logistics | ||

| IT and Telecommunications | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Middle East | GCC | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

Key Questions Answered in the Report

What is the current value of the mass notification systems market?

The market is valued at USD 29.46 billion in 2026 and is forecast to reach USD 58.79 billion by 2031.

Which component segment leads the mass notification systems market?

Software-based solutions dominate with 65.50% share in 2025, reflecting the shift toward unified, cloud-ready platforms.

Why is Asia-Pacific the fastest-growing region?

Rapid 5G infrastructure expansion, frequent natural disasters, and smart-city investments are driving a 16.9% CAGR in Asia-Pacific.

How are healthcare providers using mass notification platforms?

Hospitals integrate code alerts, staff recall, and patient messaging to meet safety regulations, propelling a 21.05% CAGR in the vertical.

What deployment model is gaining traction alongside cloud?

Hybrid architectures are growing at 19.65% CAGR because they blend on-premise control with cloud scalability, suiting regulated industries.

Which regulation is shaping European adoption?

The EU’s EECC Article 110 requires multi-channel public warnings, prompting every member state to modernize its notification infrastructure.

Page last updated on: