Agricultural Testing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 8.5 Billion |

| Market Size (2031) | USD 11.20 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

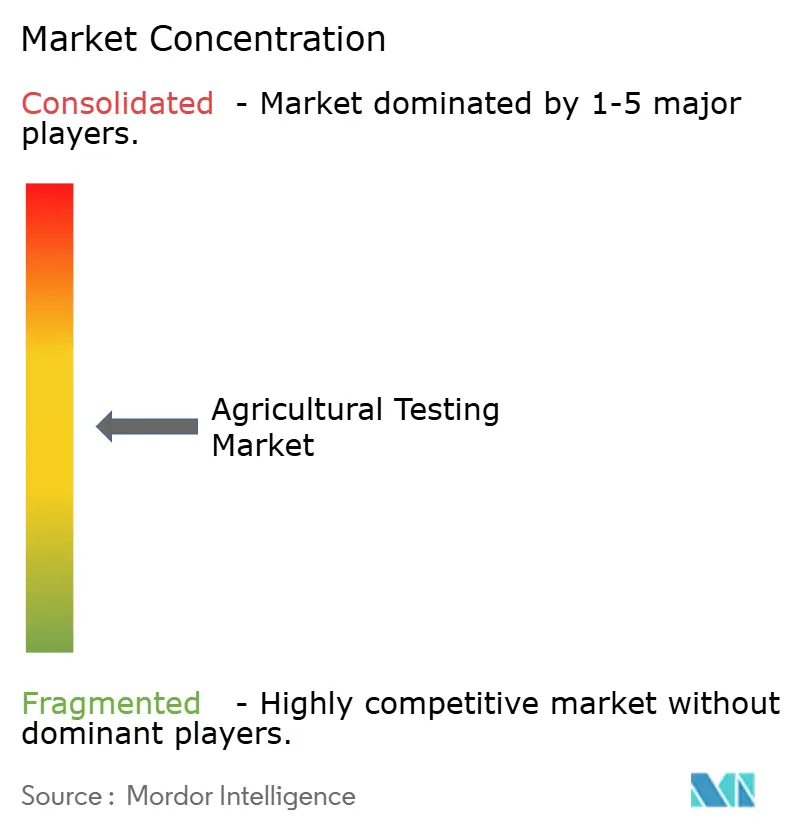

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Testing Market Analysis by Mordor Intelligence

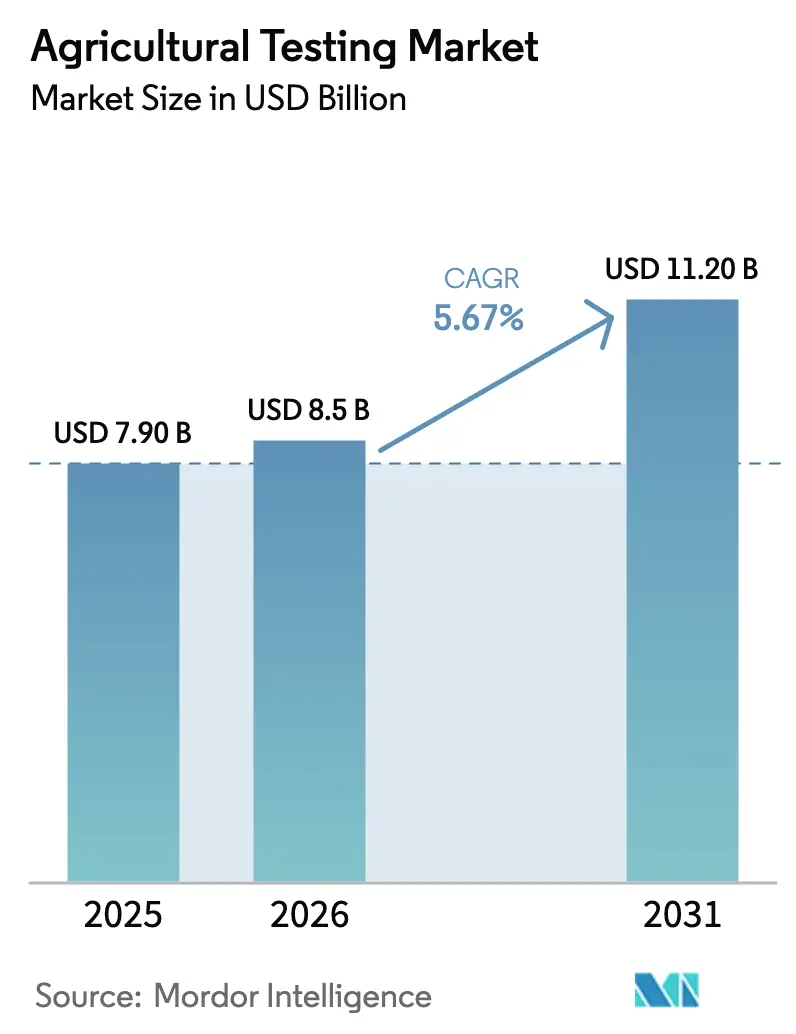

The agricultural testing market size is anticipated to grow from USD 7.9 billion in 2025 to USD 8.5 billion in 2026 and is forecast to reach USD 11.2 billion by 2031 at a 5.67% CAGR over 2026-2031. Heightened regulatory scrutiny, the surge in organic trade certification, and rapid-test innovations are the key forces lifting demand. Laboratories with International Organization for Standardization (ISO)/International Electrotechnical Commission (IEC)17025 credentials now treat blockchain connectivity as a baseline requirement, as retailers seek immutable certificates to shorten border clearance times. Seed companies are accelerating health checks to stop pathogen carryover, while carbon-credit programs are turning soil assays into multi-year annuity contracts. High capital requirements for mass spectrometry upgrades, shortages of skilled professionals, and tariff-influenced reagent costs are influencing the competitive landscape, leading to consolidation as smaller laboratories delegate complex tasks to the five major networks.

Key Report Takeaways

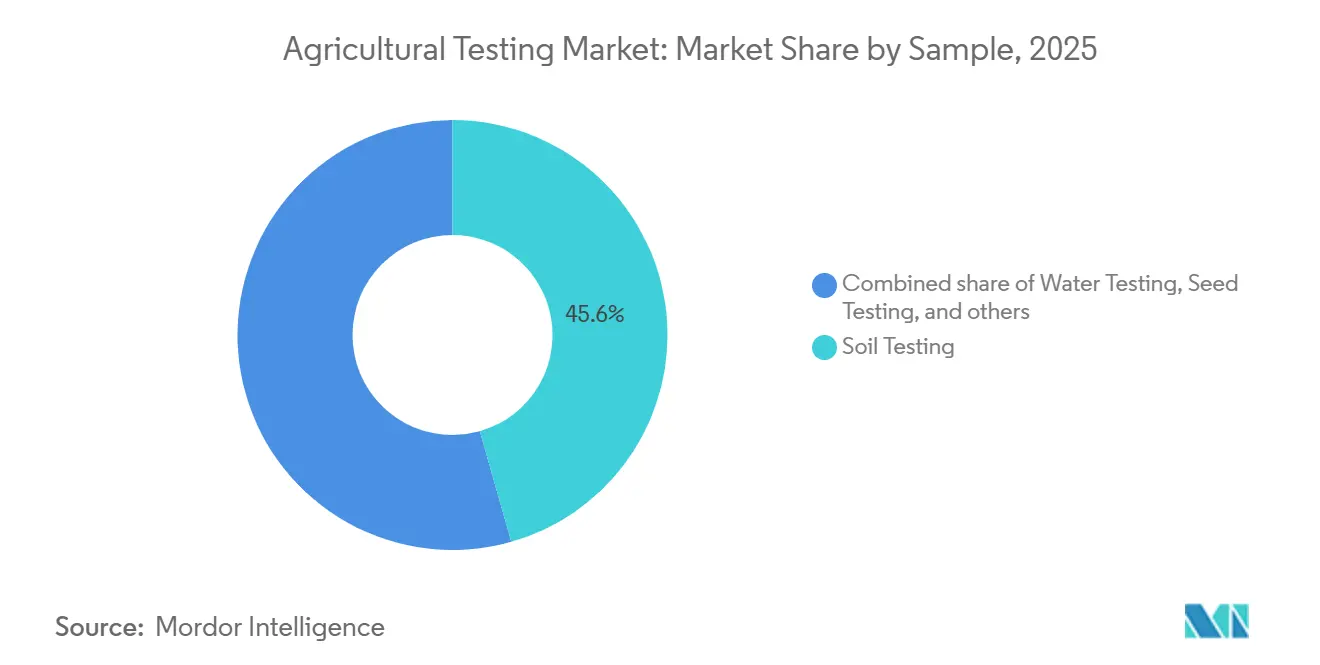

- By sample type, soil testing led with 45.6% of the agricultural testing market share in 2025, while seed testing is projected to expand at an 8.8% CAGR through 2031.

- By application, quality assurance accounted for 54.2% of the agricultural testing market size in 2025, while safety testing is advancing at a 7.6% CAGR through 2031.

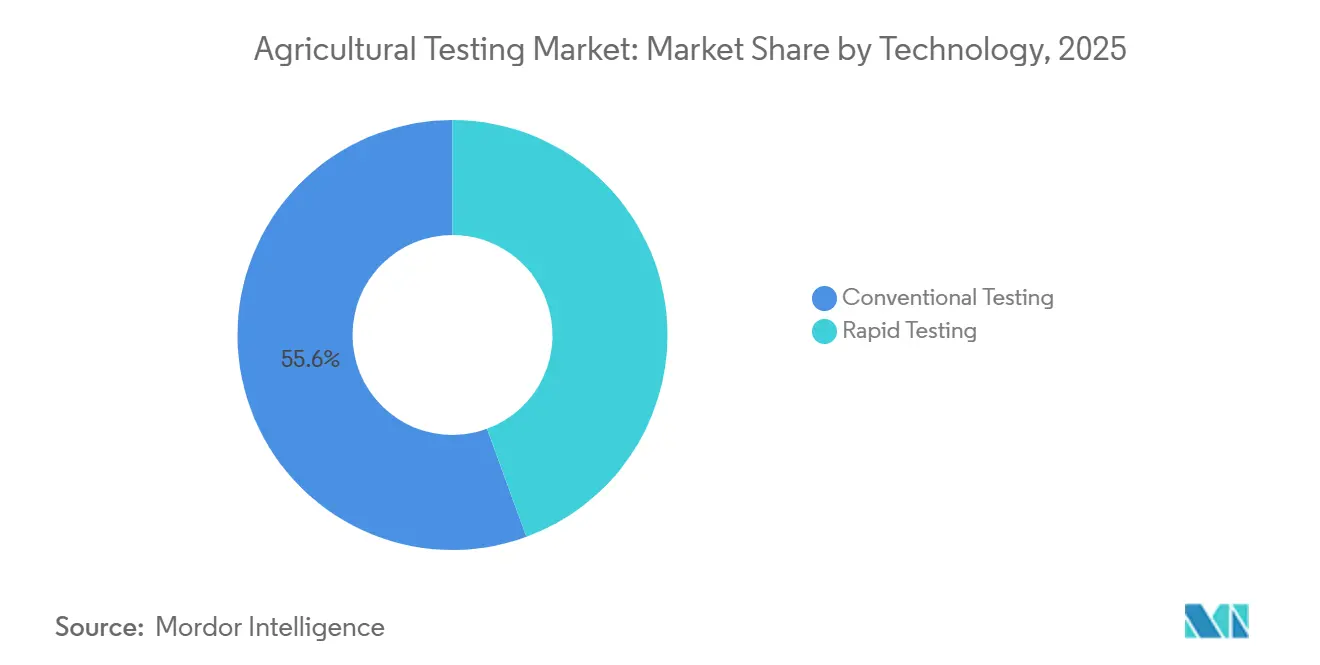

- By technology, rapid methods accounted for 55.6% of revenue in 2025 and are anticipated to post the highest CAGR of 9.2% over 2026-2031.

- Regionally, North America captured 39% of 2025 revenue, whereas Asia-Pacific is forecast to rise at an 8.8% CAGR through 2031.

- The agricultural testing market is moderately concentrated, with key players holding a significant share. SGS Société Générale de Surveillance SA (SGS SA), Eurofins Scientific SE, Intertek Group plc, PerkinElmer, Inc., and Institut Mérieux (Mérieux NutriSciences Corporation) collectively dominate the market, accounting for a significant share of 2025 revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agricultural Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food-safety regulations tightening worldwide | +1.2% | North America and the European Union | Medium term (2–4 years) |

| Escalating food-borne illness outbreaks driving rapid test adoption | +0.9% | North America and the European Union | Short term (≤2 years) |

| Surge in organic food trade requiring certification testing | +0.8% | European Union import hubs and United States retailers | Medium term (2–4 years) |

| On-site DNA/Nanopore sequencing unlocking field pathogen diagnostics | +0.7% | Asia-Pacific innovation clusters and United States specialty crops | Long term (≥4 years) |

| Carbon-credit soil programs spurring high-frequency soil health testing | +0.6% | North America and European Union carbon markets, and South American pilots | Long term (≥4 years) |

| Blockchain traceability clauses in export contracts boosting verified test data | +0.5% | Asia-Pacific to the European Union and North America export routes | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stringent Food-Safety Regulations Tightening Worldwide

United States Food and Drug Administration revisions that took effect in 2024 require two agricultural-water tests per growing cycle, adding significant recurring volume to the agricultural testing market [1]Source: U.S. Food and Drug Administration, “FSMA Final Rule on Produce Safety,” FDA.gov. The European Commission has announced reductions in the maximum residue levels for 47 pesticides, effective in 2025. This change requires exporters from countries such as Brazil, India, and Kenya to provide multi-matrix certificates to avoid rejection at entry checkpoints. Additionally, China now mandates dual testing, at the origin and the port of entry, for all fresh produce shipments, effectively doubling the number of analyses required per consignment. Laboratories with validations from the Association of Official Analytical Chemists are prioritized on retailer vendor lists, as compliance audits increasingly focus on verifying method equivalency. Consequently, the agricultural testing market benefits from regulation-driven demand stability, even during periods of commodity downturns.

Escalating Food-Borne Illness Outbreaks Driving Rapid Test Adoption

Between 2024 and 2025, the Centers for Disease Control and Prevention linked 12 multistate Salmonella outbreaks to cantaloupes, cucumbers, and leafy greens, leading retailers to stipulate same-day pathogen clearances before accepting shipments[2]Source: Centers for Disease Control and Prevention, “Foodborne Outbreaks,” cdc.gov. Portable polymerase chain reaction (PCR) kits can now detect Salmonella, Escherichia coli O157:H7, and Listeria within 90 minutes on-site, positioning them as a valuable tool in the agricultural testing market. A USD 15 field strip helps prevent recalls that can cost over USD 500,000, making growers more inclined to accept the higher per-test cost. In the United Kingdom, regulators have mandated weekly environmental swabbing in packhouses starting in January 2026, increasing demand for rapid testing solutions. However, adoption remains inconsistent in regions where interruptions in cold-chain logistics or power supply affect reagent stability.

Surge in Organic Food Trade Requiring Certification Testing

Retail organic sales hit USD 150 billion in 2025, and both European Union Regulation 2018/848 and the United States National Organic Program call for residue testing at parts-per-billion sensitivity, elevating laboratories with Liquid chromatography-tandem mass spectrometry (LC-MS/MS) fleets into strategic partners[3]Source: Agricultural and Processed Food Products Export Development Authority, “Organic Export Statistics FY 2024-25,” apeda.gov.in. India, for example, shipped USD 1.2 billion in organic spices, teas, and basmati rice but experienced a 22% rejection rate at European ports due to trace levels of pesticides, underscoring the quality gatekeeping role of the agricultural testing market. Certification bodies such as Ecocert now require quarterly soil and tissue panels for farms exceeding 50 hectares, doubling historical submission frequency. For multi-ingredient organic products, each component must carry its own certificate, multiplying demand for discrete analyses per stock-keeping unit. Laboratories that bundle sampling, logistics, and analytics capture repeat business while embedding higher switching costs into client contracts.

On-Site Deoxyribonucleic Acid (DNA) and Nanopore Sequencing Unlocking Field Pathogen Diagnostics

Oxford Nanopore Technologies has introduced a pocket-sized sequencer weighing 120 grams and priced under USD 1,000, reducing the turnaround time for diagnosing diseases such as Xylella fastidiosa from one week to four hours. Early vineyard trials in California reported a 30% reduction in fungicide usage due to real-time viral detection enabling targeted spraying. In November 2025, the United States Department of Agriculture (Animal and Plant Health Inspection Service) validated nanopore protocols for citrus greening, paving the way for subsidies for growers adopting these kits. However, data analytics remains a challenge, with fewer than 15% of agronomists able to run open-source pipelines. This has led cloud vendors to offer subscription services priced between USD 5,000 and USD 15,000 annually. These advancements are transitioning field-deployable genomics from pilot projects to mainstream applications, creating new opportunities within the agricultural testing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Laboratory Instrumentation | -0.8% | Middle East, Africa, South America, and emerging Asian labs | Medium term (2–4 years) |

| Acute Shortage of Skilled Laboratory Technicians | -0.6% | United States, United Kingdom, and Asia-Pacific | Short term (≤2 years) |

| Non-Standard Data Formats Limiting Artificial Intelligence (AI) Interoperability Across Labs | -0.4% | Global, with fragmented Laboratory Information Management System (LIMS) ecosystems in the Asia-Pacific and South America | Long term (≥4 years) |

| Rising Reagent Import Tariffs Straining Small Laboratory Margins | -0.5% | North America and the European Union, and supply-chain dependent Africa and the Middle East | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Laboratory Instrumentation

In 2025, the cost of a single liquid chromatography-tandem mass spectrometer, required to achieve 0.01 ppm pesticide thresholds, ranged from USD 400,000 to USD 600,000. Similarly, an inductively coupled plasma mass spectrometer for heavy metal analysis was priced between USD 300,000 and USD 500,000. While leasing options allowed these costs to be spread over three to five years, they often required bank guarantees that many regional operators found difficult to secure. The expansion of the Bureau of Industry and Security (BIS) Entity List in March 2025, along with the rescission of the Artificial Intelligence (AI) Diffusion Rule in May, created a significant regulatory backlog for technology buyers in the Middle East. Shipments of sensitive components frequently faced delays of up to 9 months in license processing. In countries such as Nigeria and Indonesia, limited infrastructure and skill shortages have led to the outsourcing of analytical testing to hubs in South Africa and Singapore, where companies like Eurofins and SGS hold dominant positions. This dependency increases costs, reduces local profit margins, and slows the growth of the agricultural testing market.

Acute Shortage of Skilled Laboratory Technicians

The American Society for Clinical Laboratory Science reported a 35% vacancy rate in United States agricultural laboratories as of January 2025, a significant increase from 18% five years earlier. Similarly, Brexit has exacerbated workforce shortages in the United Kingdom, where 2,400 qualified analysts are absent from payrolls. While automation can reduce manual pipetting steps by 60%, the cost of robots, ranging from USD 150,000 to 300,000, presents financial challenges for smaller laboratories, requiring a balance between staffing and capital investment. In India, less than 40% of accredited laboratories employ staff with postgraduate degrees in analytical chemistry, posing quality-control risks when conducting high-sensitivity methods. Persistent talent shortages may limit throughput, even as the agricultural testing market faces increasing sample volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sample: Soil Dominance Meets Seed Surge

Soil assays accounted for 45.6% of the agricultural testing market size in 2025, underscoring their central role in nutrient budgeting, heavy-metal surveillance, and carbon trading enrollment. The category anchors the agricultural testing market size at the farm level. Seed tests are expanding at an 8.8% CAGR to 2031, the swiftest pace among samples, because phytosanitary rules require pathogen-free lots before cross-border shipment. Soil biology panels now include microbial biomass metrics, a feature currently offered by fewer than 20% of laboratories and typically priced at a premium. Specialized but smaller segments of demand include testing for water, biosolids, manure, and plant tissue.

Carbon-credit protocols mandate baseline and annual soil sampling, providing consistent revenues that help mitigate seasonal fluctuations. In February 2025, the United States Natural Resources Conservation Service updated its guidelines to require 60-centimeter cores, effectively doubling the sample volume per farm and driving increased throughput in the agricultural testing market. Additionally, the International Plant Protection Convention's mandates on seed pests have transformed germination, purity, and disease checks into essential trade requirements. Water testing demand may rise if the Environmental Protection Agency implements mandatory pre-season screenings for operations with ten or more workers, potentially creating a USD 200-300 million market segment for laboratories in the United States.

By Application: Quality Assurance Leads, Safety Accelerates

Quality assurance accounted for 54.2% of the agricultural testing market in 2025, as growers rely on nutrient and moisture profiles to maximize yields and meet grade specifications. Safety testing, while smaller today, is climbing at a 7.6% CAGR through 2031 on the back of retailer clauses that demand 250-plus pesticide panels per produce lot. The expansion of private-label products by global grocers is prompting suppliers to implement verification processes beyond regulatory requirements, thereby expanding the scope of mandatory testing. Organic handlers are now subject to unannounced residue screenings on 5% of inbound cargoes, adding to the existing safety measures within the agricultural testing market.

Retailers view testing costs as a safeguard against brand-damaging recalls, leading laboratories that provide integrated services such as bundled logistics, analytics, and digital certificate uploads to secure multi-year contracts. Precision agriculture software that incorporates nutrient maps derived from quality reports helps quantify yield improvements, supporting the case for repeat testing. Laboratories categorize organic residue panels under quality assurance to align with program documentation, despite their overlap with safety objectives. This dual-purpose testing approach ensures high utilization rates, even during non-peak harvest periods.

By Technology: Rapid Methods Capture Speed Premium

Rapid assays accounted for 55.6% of the agricultural testing market in 2025 and are anticipated to achieve a 9.2% CAGR through 2031, driven by lateral-flow immunoassays, portable Polymerase Chain Reaction (PCR), and near-infrared readers that compress decision cycles to minutes or hours. Time savings often outweigh the 30-50% price premium, especially when each day's delay can reduce lettuce shelf life by two days. Conventional culture and wet-chemistry methods remain the standard for mycotoxin quantification, with high-performance liquid chromatography offering superior performance to rapid kits at sub-2 ppb detection limits. Regulators now support tiered protocols that enable rapid screening followed by conventional confirmation, fostering a balanced coexistence of methods.

The Association of Official Agricultural Chemists (AOAC) validated 14 new rapid methods for fresh produce during 2024-2025, broadening the range of compliant tools available. Companies like Bruker and Foss have introduced hand-held near-infrared meters capable of sorting grains in real time, effectively transforming grain elevators into micro-laboratories. However, in low-income regions, challenges such as unreliable electricity and limited refrigeration continue to hinder conventional testing. Consequently, investment in agricultural testing technologies aligns with both market demand and infrastructure readiness, driving regional differences in technology adoption.

Geography Analysis

North America is projected to lead the agricultural testing market, accounting for 39% of global revenue in 2025. This dominance is attributed to the mandates of the Food Safety Modernization Act and a well-established laboratory network that employs robotics to expedite pesticide testing. Laboratories in key states such as California, Florida, and Texas concentrate testing capacity, enabling exporters to secure certificates within 36 hours. In contrast, Asia-Pacific is the fastest-growing region, with a compound annual growth rate of 8.8% through 2031. This growth is driven by China's tightening of residue limits and India's expansion of organic farming acreage. Both regions benefit from robust government programs that subsidize testing, though their growth is influenced by distinct factors, such as North America's focus on compliance enforcement and Asia-Pacific's emphasis on export-led certification.

Europe, South America, the Middle East, and Africa collectively represent a mix of surplus capacity and emerging demand. European laboratories experience underutilization during off-peak months, though increased mycotoxin surveillance helps alleviate this challenge. In South America, commodity exports remain a primary driver, with robotic testing lines in Brazil and Argentina significantly reducing turnaround times for soybean and beef certification. The Middle East's food security programs and Africa's aflatoxin initiatives are spurring investments in regional laboratories. However, logistical constraints and shortages of skilled labor continue to hinder progress in these regions.

North America is focusing on integrating rapid screening with blockchain technology to further reduce clearance times and attract premium contracts. In Asia-Pacific, laboratories are expanding their capabilities by installing additional Liquid Chromatography with Tandem Mass Spectrometry instruments to meet export requirements, while mobile units are extending services to rural farming areas. European providers are diversifying into carbon-credit soil projects to reduce reliance on residue testing. Meanwhile, laboratories in South America and Africa are bundling sampling and analytics services to appeal to multinational clients. These initiatives collectively contribute to incremental volume growth across all regions, with regulatory stringency and digital readiness playing a critical role in determining regional growth rates.

Regulatory Landscape

Regulation is tightening around both what must be tested and which laboratories can generate defensible results for trade and enforcement. In the United States, FDA changes that took effect in 2024 increased recurring agricultural-water testing per growing cycle, and in March 2026 the FDA transitioned into the Laboratory Accreditation for Analyses of Foods (LAAF) program, recognizing accreditation bodies to oversee laboratories conducting specified food testing. In the European Union, the multiannual control program for 2026-2028 under Implementing Regulation (EU) 2025/854 formalizes pesticide residue monitoring priorities and supports method harmonization across member states, which lifts demand for multi-residue capability and consistent reporting across matrices.

Across major markets, regulators and official control systems are also pushing more standardized data and process requirements that favor accredited networks. ISO/IEC 17025 continues to operate as a baseline credential for laboratories supporting official controls and cross-border certificates, while digital submissions into official systems (including EU official-control information platforms and USDA digital programs for regulated categories) raise expectations for traceable, auditable reporting. In parallel, risk-based control frequencies and commodity-specific programs, such as USDA FGIS procedures for grain pesticide residue reporting, concentrate testing volume in specific supply-chain nodes, reinforcing the need for validated methods and quality systems for laboratories serving exporters, grain handlers, and food-chain buyers.

Competitive Landscape

The agricultural testing market is moderately concentrated, with key players holding a significant share. SGS Société Générale de Surveillance SA (SGS SA), Eurofins Scientific SE, Intertek Group plc, PerkinElmer, Inc., and Institut Mérieux (Mérieux NutriSciences Corporation) collectively dominate the market, accounting for a significant share of 2025 revenue. These five companies play a central role globally, offering extensive multi-matrix portfolios and worldwide sampling capabilities that help reduce clients' procurement challenges. They maintain accreditations such as ISO/IEC 17025 and United States Department of Agriculture foreign laboratory certifications, ensuring compliance with the standards multinational clients require. Additionally, these firms integrate laboratory information systems with retailer blockchains, enabling same-day certificate uploads.

The financial strength of these top players allows them to maintain advanced technologies, such as Liquid Chromatography with tandem Mass Spectrometry (LC-MS/MS) and Inductively Coupled Plasma Mass Spectrometry (ICP-MS), with refresh cycles every three years an operational pace that few competitors can match. In January 2026, Intertek Group plc strengthened its market position by adopting digital traceability solutions through platforms like IBM Food Trust. PerkinElmer, Inc. has diversified its operations by offering carbon-credit soil services in Australia, reducing its reliance on mining analytics. These diversified networks distribute fixed costs across environmental, pharmaceutical, and consumer-packaged goods segments, mitigating the impact of agricultural market fluctuations.

Smaller, niche laboratories compete by focusing on faster turnaround times and specialized local expertise, often targeting areas such as biosolids or seed pathology to avoid direct competition with global leaders. However, the high cost of instruments, ranging from USD 300,000 to 800,000, and reagent tariff surcharges create significant barriers to scaling operations. Blockchain clauses in export contracts are driving a two-tier market structure, where digitally advanced laboratories secure premium accounts, while analog operators face stagnation. Patent data highlights increasing investments in sequencing technologies, immunoassay reagents, and Artificial Intelligence (AI) for anomaly detection, indicating a trend toward greater technology-driven differentiation in the market.

Agricultural Testing Industry Leaders

Eurofins Scientific SE

SGS Société Générale de Surveillance SA (SGS SA)

Intertek Group plc

PerkinElmer, Inc.

Institut Mérieux (Mérieux NutriSciences Corporation)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hybrid testing models are taking shape, combining rapid on-farm screening with accredited laboratory confirmation. Mobile and handheld diagnostics are moving closer to the point of production, while centralized laboratories continue to run LC-MS/MS and other confirmatory methods for certification and enforcement. In 2026, ICL launched Nutroscan, a handheld leaf-scanning device deployed by agronomists in Brazil for real-time crop nutrition diagnostics, and SBOF Agrosmart launched the SBOF AGROLAB platform in India with rapid soil testing offering a 30-minute turnaround and a 16-parameter panel. These examples point to growing demand for services that translate results into agronomy actions, such as nutrient recommendations and input optimization, rather than providing standalone lab reports.

Opportunities also track tighter measurement requirements and higher-frequency monitoring programs, which increase the value of method robustness, uncertainty management, and longitudinal datasets. The EU introduced specific measurement uncertainty rules for pesticide-residue analysis in feed via Regulation 2026/765, supporting demand for laboratories that can document uncertainty and method performance consistently across instruments and sites. Separately, public programs and research are pushing continuous soil monitoring forward, including the SOILMONITOR lab-on-chip concept and 2026 research on in-situ nitrate sensors, which frames service openings for laboratories and technology providers that can connect devices, data transmission, and QA workflows into auditable soil health and compliance records.

Recent Industry Developments

- March 2026: Eurofins expanded its European seed testing service across ISO/IEC 17025 accredited laboratories in Italy, France, and the Netherlands, offering more than 800 disease and pest detection tests. The expanded cluster strengthens phytosanitary and cross-border seed trade support while standardizing capabilities across multiple sites to handle seasonal peaks and faster turnaround requirements.

- September 2025: Eurofins Scientific completed its planned acquisition of all related-party-owned sites, consolidating them into a single purchased entity aligned to its prior disclosure. Bringing these sites under a unified structure reduces related-party lease exposure and supports tighter governance and operational control, which is relevant for multi-site laboratory networks that depend on consistent quality systems and scalable capacity.

- November 2024: BASF subsidiary trinamiX advanced its handheld near-infrared spectroscopy platform with new application development for on-site nutritional analysis use cases, extending the addressable scope of mobile testing workflows. Wider availability of calibrated handheld spectroscopy supports the shift of certain quality and feed or forage screening steps from centralized labs to farm and elevator settings, while leaving confirmatory testing with accredited laboratories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the agricultural testing market is defined as the revenue generated from testing services used to measure quality and safety attributes of agriculture-related samples, which are then reported as standardized results for farm and supply-chain decisions.

Scope exclusions: This scope does not include on-farm advisory services that do not include a test result, nor does it include general lab equipment sales that are not tied to an agricultural testing service contract.

Segmentation Overview

- By Sample

- Water Testing

- Soil Testing

- Seed Testing

- Bio-solids Testing

- Manure Testing

- Other Samples

- By Application

- Safety Testing

- Quality Assurance

- By Technology

- Conventional Testing

- Rapid Testing

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Rest of Europe

- Asia-Pacific

- India

- China

- Australia

- Japan

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand map and to set boundaries around what is counted as agricultural testing revenue. We mainly pulled public references on crop area and output, fertilizer and input usage, and soil and water quality reporting requirements, since these are practical signals for how much testing demand exists.

Typical sources reviewed included USDA and other national agriculture departments, FAO databases, USGS and similar national geological surveys for soil and water indicators, EPA and comparable environmental agencies for sampling and reporting rules, and peer-reviewed agronomy journals for standard test panels and sampling frequencies. We also checked company annual reports, investor presentations, association websites, and reputable press to understand service mix and pricing direction. Paid subscriptions were used where needed for company financials and news. For method trends, patent databases were reviewed, and for selected reagent and kit flows, we used an import-export shipment-level database. This list is not exhaustive, and many other public and paid sources were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on cross-checking the service scope and the real-world cadence of testing across soil, water, seed, and related sample types, since lab demand changes by crop cycle and regulatory requirements. We spoke with a mix of lab operators, channel partners, agronomists, and large-farm procurement roles across major producing regions. Respondent input helped us close gaps on average test pricing, retest rates, and how often rapid methods replace conventional lab panels in routine programs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 48% |

| Mid tier: 57% | Functional/Unit leaders: 41% | EMEA: 32% |

| Smaller Players: 14% | Managers: 46% | Americas: 20% |

Market-Sizing & Forecasting

Sizing started from a top-down demand pool reconstruction, where crop acreage, intensity of input use, and sample submission frequency were translated into expected test volumes by major sample categories and regions. Those volumes were then converted to value using an average price logic that reflects common test bundles, for example nutrient panels versus residue screening, and the mix shift between conventional lab methods and faster formats.

To keep totals grounded, the outputs were corroborated with selective bottom-up approximations, such as roll-ups of reported testing revenue for a sample of labs, channel checks on typical price ranges, and sanity checks using capacity and throughput signals where they were credibly available. Key inputs we tracked included planted area and cropping cycles, soil health and nutrient management programs, water quality monitoring requirements, adoption of precision agriculture practices that increase sampling, and the degree of export-oriented production that triggers stricter residue and quality testing. Where bottom-up data was incomplete, gaps were handled through conservative coverage ratios that were discussed with interviewees, and then adjusted only when multiple signals pointed in the same direction.

Forecasting used scenario analysis supported by a light multivariate regression on the most stable drivers, mainly planted area, input intensity, and regulation-linked testing triggers. Assumptions were reviewed with industry respondents so the growth path did not rely on a single variable.

Data Validation & Update Cycle

Multiple checks were applied before finalizing the numbers, including triangulating model outputs against independent indicators such as lab expansion announcements, published testing guidelines, and observable shifts in crop and export patterns. When a region or sample type showed an unexpected jump, the assumptions behind sampling frequency, price per test, or method mix were revisited, and targeted follow-ups were triggered to confirm whether a real change occurred.

Each deliverable goes through multi-step analyst review, followed by consistency checks across the historical series and forecast drivers. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or sharp moves in farming input economics. Right before delivery, a final pass is done so clients receive the most current view available at that time.

Mordor Intelligence's Agricultural Testing Market Size Measured Against Other Published Estimates

Published market values for agricultural testing do not always match because the scope can shift between service revenue and broader testing-related products, and because some models apply different timing for currency conversion and price escalation. Differences also show up when one estimate weights certain sample types, such as soil versus seed, more heavily. Other gaps appear when an estimate assumes a faster substitution toward rapid tests without strong checks on actual lab throughput.

The table shows a visible spread around the 2026 value, and in Mordor Intelligence's model the market is treated as agricultural testing service revenue linked to sample-based testing. This avoids counting general lab instrument sales and keeps pricing anchored to typical test bundles rather than list prices.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.50 B (2026) | |

| Industry Publisher A | USD 7.34 B (2026) | Often built from a narrower sample-based scope with more conservative test frequency assumptions, which can undercount retesting driven by regulation and crop-cycle variability. |

| Industry Publisher B | USD 7.23 B (2025) | Uses an earlier base year and a different price progression approach, and the conversion to USD timing can shift the value when local-currency pricing is changing. |

Overall, the spread is mainly explained by what gets counted as market revenue, how test volumes are linked to planted area and compliance triggers, and how prices are carried forward year to year. By keeping inputs traceable to sampling cadence, test bundle pricing, and region-level demand signals, the sizing steps stay repeatable and easier to audit when new information appears.

Key Questions Answered in the Report

What is the current value of the agricultural testing market and its projected growth by 2031?

The agricultural testing market size is USD 8.5 billion in 2026, forecast to reach USD 11.2 billion by 2031 at a 5.67% CAGR.

Which sample type generates the most revenue for laboratories?

Soil assays lead with 45.6% of 2025 revenue due to their role in nutrient management, heavy metal monitoring, and carbon credit programs.

Why are rapid tests gaining share in agricultural analytics?

Retailers and regulators require same-day clearance, and rapid PCR or lateral flow tests reduce turnaround time from days to hours, supporting premium pricing.

Which region is expanding fastest in agricultural testing demand?

Asia Pacific, with an 8.8% CAGR through 2031, driven by stricter Chinese import standards and push towards organic certification by India..

Page last updated on: