Agricultural Biologicals Testing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

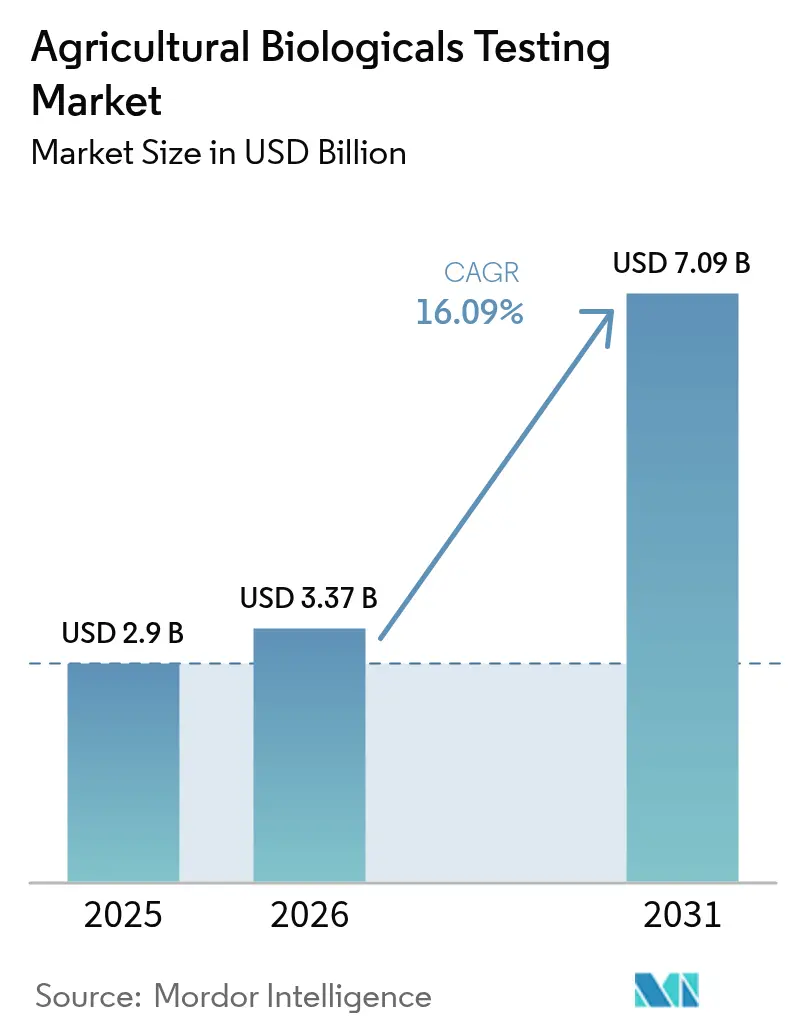

| Market Size (2026) | USD 3.37 Billion |

| Market Size (2031) | USD 7.09 Billion |

| Growth Rate (2026 - 2031) | 16.09% CAGR |

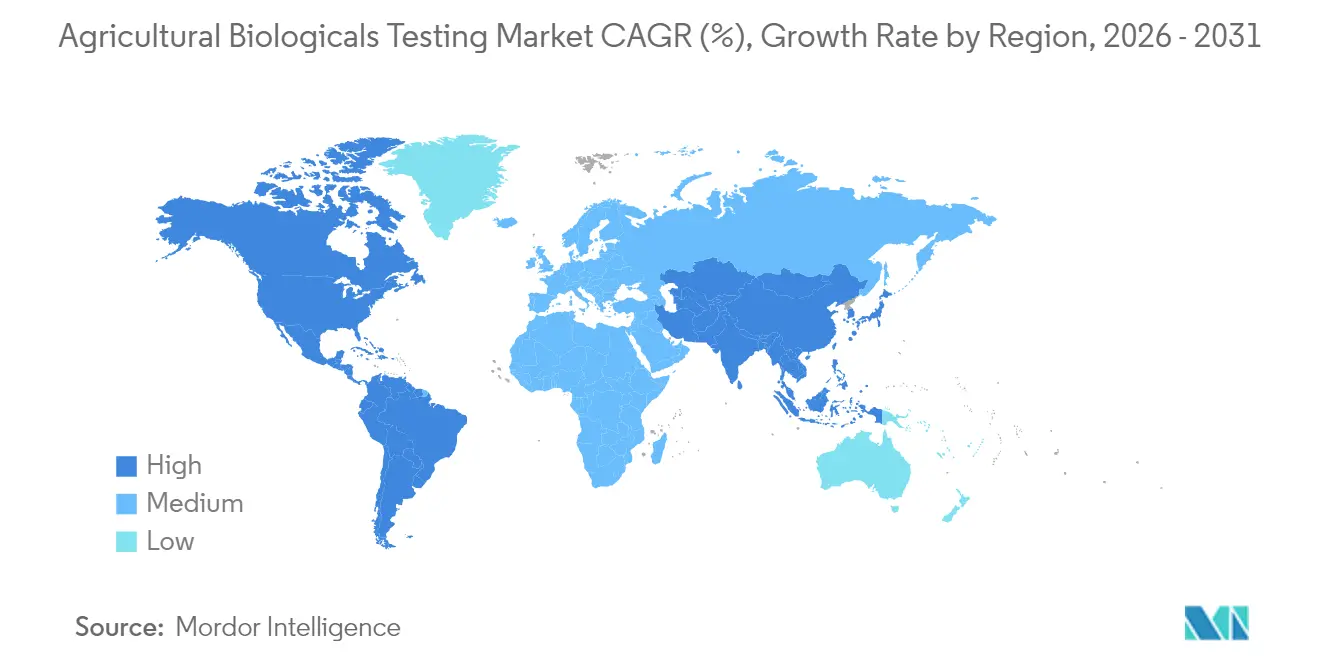

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Biologicals Testing Market Analysis by Mordor Intelligence

The agricultural biologicals testing market size was valued at USD 2.9 billion in 2025 and estimated to grow from USD 3.37 billion in 2026 to reach USD 7.09 billion by 2031, at a CAGR of 16.09% during the forecast period (2026-2031). This rapid growth is rooted in tighter global regulations that demand exhaustive efficacy and safety evidence for biological inputs, rising adoption of sustainable crop protection, and the spread of next-generation sequencing in laboratory workflows[1]Source: “Biochemical Pesticides,” Environmental Protection Agency, epa.gov. Independent laboratories are expanding automated high-throughput platforms that shorten study timelines, while harmonized templates between major regulators are beginning to cut duplicative submissions[2]Source: “Pest Management Regulatory Agency,” Health Canada, canada.ca. Flexible outsourcing models let biological start-ups gain premium testing capacity without the fixed cost of Good Laboratory Practice (GLP) facilities, and digital traceability mandates are transforming reports into real-time blockchain-ready data streams[3]Source: “Digital Product Passports,” European Commission, ec.europa.eu.

Key Report Takeaways

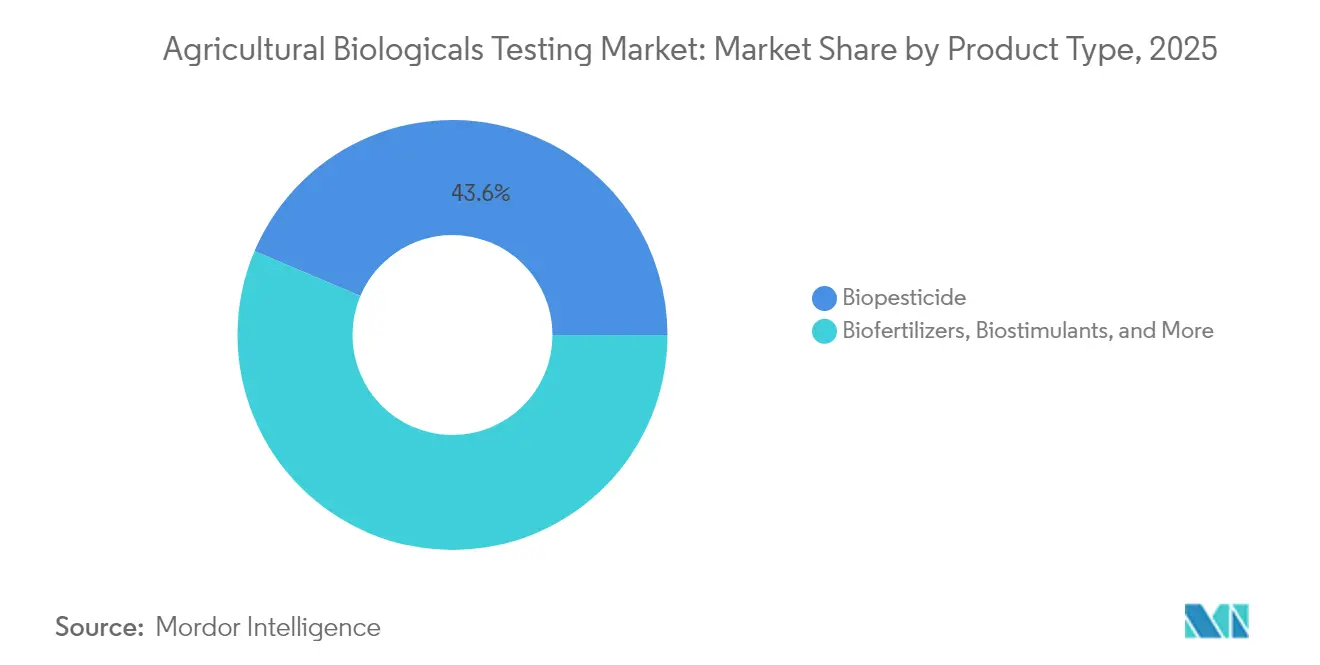

- By product type, biopesticides held 43.62% of the agricultural biologicals testing market share in 2025, and biostimulants testing is projected to advance at a 17.15% CAGR through 2031.

- By application, field support dominated with a 40.12% revenue share in 2025, while analytical services are anticipated to expand at a 17.44% CAGR through 2031.

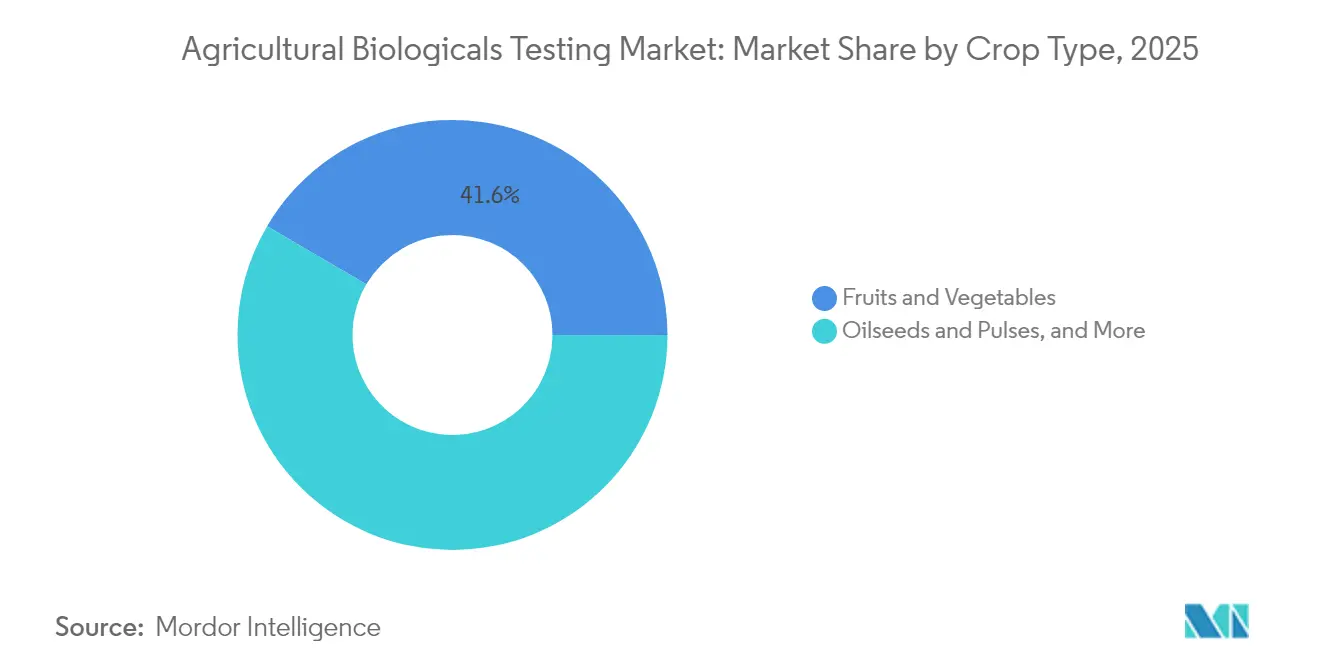

- By crop type, fruits and vegetables accounted for a 41.55% slice of the agricultural biologicals testing market size in 2025, and oilseeds and pulses are forecast to climb at a 16.22% CAGR between 2026 and 2031.

- By geography, North America led the 2025 landscape with a 34.68% share in revenue, while Asia-Pacific is poised to advance at a 16.12% CAGR through 2031.

- The top five players, including Eurofins Scientific SE, SGS SA, Intertek Group plc, Bureau Veritas SA, and ALS Limited, collectively controlled a majority share of the agricultural biological testing market revenues in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Biologicals Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Organic Farming Acreage | +2.8% | Europe and North America lead, global effect | Medium term (2-4 years) |

| Stringent Global Regulations Favoring Biologicals | +3.2% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Rising Consumer Demand for Residue-Free Food | +2.5% | Developed markets worldwide | Medium term (2-4 years) |

| Accelerated Research and Development Investments by Agro-Chemical Majors | +2.1% | North America and Europe | Long term (≥ 4 years) |

| Outsourcing Surge from Mid-Tier Biological Start-Ups | +1.9% | North America and Europe, expanding in the Asia-Pacific | Short term (≤ 2 years) |

| Digital Traceability and Crop Passport Mandates | +1.7% | Europe drives the global roll-out | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Organic Farming Acreage

Organic acreage continues to grow at a faster rate than conventional land, and certification bodies now require multi-season field trials, residue analytics, and soil microbiome studies before approving biological inputs. The United States National Organic Program has intensified residue surveillance, which requires laboratories to integrate advanced chromatographic and molecular workflows [4]Source: “National Organic Program,” United States Department of Agriculture, usda.gov . Europe’s organic scheme mirrors these testing demands and adds blockchain traceability, compelling labs to upgrade digital infrastructure. Field trials are conducted across diverse climatic zones to capture variability, thereby increasing testing volume over two to three harvests. Premium pricing for organic-certified products offsets the elevated testing spend, creating a durable funding loop for laboratory services. As regulators tighten organic input lists, manufacturers rely on independent Good Laboratory Practice (GLP) data to protect product positioning in lucrative organic channels.

Stringent Global Regulations Favoring Biologicals

The Environmental Protection Agency now requires molecular characterization and comprehensive toxicology for biochemical pesticides, while China’s Institute for the Control of Agrochemicals, Ministry of Agriculture (ICAMA), has adopted parallel microbial registration protocols [5]Source: “Institute for the Control of Agrochemicals, Ministry of Agriculture and Rural Affairs,” icama.org.cn. This convergence harmonizes fundamental data packages but raises documentation thresholds, favoring large GLP-certified providers. Post-market surveillance clauses extend testing well beyond launch, creating recurring laboratory revenue. Mutual recognition of data within selected trade blocs prevents full duplication, yet still necessitates region-specific residue and environment studies. Accelerated review lanes reward dossiers that include exhaustive analytics, pushing sponsors to invest in premium lab partners from the outset. The net effect is a larger, more predictable testing pipeline anchored to long-term regulatory compliance.

Rising Consumer Demand for Residue-Free Food

Retail and processor scorecards are increasingly requiring third-party verification that biological inputs leave no detectable chemical residues. High-sensitivity liquid chromatography-mass spectrometry (LC-MS) platforms now quantify active metabolites at part-per-billion levels, and the results are fed directly into supplier dashboards [6]Source: “Pesticide Residue Monitoring Program,” Food and Drug Administration, fda.gov. QR codes on produce packages let shoppers view the testing certificate, linking transparency to brand loyalty. Social media awareness campaigns amplify residue concerns and stimulate premium market segments, especially for fresh fruits and vegetables. Emerging economies emulate Western residue limits as export goals widen, expanding the addressable testing base. Continuous residue monitoring also informs risk communication strategies that maintain public trust in biological crop protection.

Accelerated Research and Development Investments by Agro-Chemical Majors

Global agrochemical leaders now channel up to 40% of discovery budgets into biological programs, a shift that generates demand for microbial bioassays, formulation stability screens, and multi-location efficacy trials. Outsourced testing bridges expertise gaps in molecular biology and metagenomics, where internal capabilities lag. Patent filings for biological agents have climbed 45% each year since 2024, swelling the backlog of studies needed for regulatory packages. Strategic alliances between multinationals and contract labs lock in multi-year volume commitments, letting labs secure financing for facility expansion. Artificial-intelligence discovery suites speed candidate selection but simultaneously multiply confirmatory assays, keeping the laboratory pipeline loaded across the decade.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of harmonized biological testing guidelines | -1.8% | Emerging markets feel the greatest impact | Long term (≥ 4 years) |

| High cost and duration of multi-location field trials | -2.1% | Asia-Pacific most affected | Medium term (2-4 years) |

| Limited reference material libraries for new microbes | -1.5% | Global, acute in novel categories | Medium term (2-4 years) |

| Scarcity of bioassay statisticians and QA auditors | -1.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of Harmonized Biological Testing Guidelines

Regulatory fragmentation forces companies to repeat studies for each jurisdiction, multiplying cost and time. Disagreements over statistical endpoints and environmental safety benchmarks slow Organisation for Economic Co-operation and Development (OECD) harmonization efforts, particularly for RNA-based pesticides. Emerging markets often publish draft guidelines without enforcement clarity, deterring early testing investments. Smaller firms face disproportionate burdens, as parallel programs exhaust limited capital and personnel. Until standard terms and endpoints converge, laboratories must tailor protocols for every submission, reducing economies of scale and extending development cycles.

High Cost and Duration of Multi-Location Field Trials

Biological efficacy trials can exceed USD 500,000 per active ingredient and typically run across several growing seasons to capture environmental variability[7]Source: United States Department of Agriculture, “National Organic Program Handbook,” usda.gov. Weather volatility driven by climate change forces additional replicates to reach statistical significance, swelling budgets further. Insurance premiums for open-field deployment of novel microbes rise annually, and limited qualified sites create bottlenecks that delay project starts. Supply-chain hurdles, from shipping live inoculants to maintaining cold chains, compound logistical risk and expense. Collectively, these factors discourage smaller innovators and constrain market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biopesticides Anchor Demand

The biopesticide segment held 43.62% agricultural biologicals testing market share in 2025, supported by mature regulatory frameworks and standardized GLP protocols. The agricultural biologicals testing market size associated with biopesticide registration is projected to keep rising through 2031 as microbial, botanical, and RNA-based products move through pipelines. Laboratories capitalize on established demand patterns, enabling predictable scheduling and utilization rates. Biofertilizers captured a 27.68% share as soil health gained global attention under EU Regulation 2019/1009. Growing clarity around biostimulant definitions propels that category to the fastest 17.15% CAGR, with test menus expanding into plant metabolomics and gene expression profiling. Labs are diversifying into these niches ahead of impending regulatory milestones that should unlock incremental volume.

Coupled with regulatory harmonization, product-type diversification buffers laboratories against cyclicality. Equipment amortization is spread across assay types, and cross-training scientists allows flexible staffing. As RNA-interference products approach launch, demand grows for molecular assays that verify mode of action and off-target effects, deepening service complexity and revenue per study.

By Application: Field Support Remains Core

Field support activities, multi-location trials, environmental fate studies, and application optimization accounted for 40.12% sales in 2025. This slice of the agricultural biologicals testing market is deeply integrated into growers’ commercialization timelines. Large-scale trials validate efficacy under real farm conditions, and their findings drive label claims and marketing messages. Regulatory dossiers, the second-largest application at a significant share, maintain steady demand due to ongoing registration renewals. The agricultural biologicals testing market size for analytical services, which include molecular diagnostics and sequencing, is expanding at an 17.44% CAGR as sponsors seek deeper insight into strain genetics and product purity.

Routine formulation stability and shelf-life work fills laboratory calendars during off-season months, helping even out capacity utilization. High-throughput analytics slash per-sample costs, encouraging smaller companies to request broader study panels that were once cost-prohibitive. Laboratories differentiate by bundling field and analytical programs into end-to-end packages, offering clients single-contract convenience and unified data reporting.

By Crop Type: Specialty Produce Dominates

High-value fruits and vegetables held a 41.55% share of the agricultural biologicals testing market size in 2025 because fresh-produce buyers enforce the toughest residue limits. Cereals and grains represented a significant share on the back of broad acreage and seed-treatment demand. Oilseeds and pulses posted the fastest 16.22% CAGR outlook, propelled by plant-protein market growth and expanding biological options. The remaining share is derived from ornamentals, turf, and forestry, segments that open additional seasonal laboratory windows and mitigate peak-capacity constraints. Crop diversification ensures balanced revenue throughout the agricultural calendar, allowing laboratories to manage workforce levels efficiently.

Regional production patterns deepen these dynamics and push laboratories to diversify crop expertise. California berry growers seek rapid turnaround residue tests to protect export channels, while Midwest corn producers commission large-plot field trials that validate seed treatment performance across variable soil types. In Europe, greenhouse tomato operations order continuous microbial monitoring to meet digital passport requirements, adding recurrent revenue streams. The agricultural biologicals testing market size tied to cereals and grains is also climbing because exporters must align with tightening import standards in high-value Asian markets. Collectively, crop-specific regulations and buyer protocols ensure sustained demand growth that is resilient across commodity cycles.

Geography Analysis

The Asia-Pacific region is the fastest-growing, with a 16.12% CAGR through 2031, as China enforces molecular data requirements for every microbial pesticide under its Association of Southeast Asian Nations (ICAMA) rules and Japan rolls out RNA-interference test protocols that necessitate advanced molecular diagnostics. China’s vast acreage generates steady demand because both domestic and multinational firms must run local trials to register new strains, while India’s organic acreage is expanding more than 12% each year and drives additional efficacy studies for certification bodies. South Korea is pairing biological inputs with smart-farm sensors, so laboratories there are upgrading data platforms that plug directly into Internet of Things dashboards. Lower labor costs also enable Asian testing companies to run large, multi-location trials at prices that undercut many Western providers. A nascent Association of Southeast Asian Nations (ASEAN) harmonization effort is underway to align study templates, which is expected to reduce regulatory friction across Southeast Asia over the next few years.

North America still holds the largest revenue share, at nearly 34.68% in 2025, as more than 200 GLP-certified facilities already cover the full spectrum of biological assays. A common template adopted by the United States Environmental Protection Agency and Canada’s est Management Regulatory Agency (PMRA) now saves sponsors up to 20% in duplicative study spend while keeping scientific rigor intact. Mexico’s export growers are sending testing volumes up 18% annually as they pursue residue-free certificates for shipments to the United States and Europe. Artificial-intelligence tools embedded in many United States labs cut data-review time by roughly one-quarter, freeing capacity for novel microbial containment studies. The region also benefits from strong university partnerships that pilot next-generation protocols before they spread worldwide.

Europe advances as Regulation 2019/1009 delivers the world’s most detailed roadmap for biostimulant testing. Germany and France account for more than 40% of regional revenue thanks to large farming sectors and strict compliance cultures. The United Kingdom’s post-Brexit rules set forces dual submissions, adding roughly 10% in extra study work for products sold on both sides of the Channel. Digital product passport rules that take effect later in the decade will require blockchain-ready test files, a shift that favors labs with sophisticated data infrastructure. Green Deal incentives and specialty hubs such as the Netherlands for greenhouse crops keep the regional pipeline full even as climatic zones vary widely across the continent.

Competitive Landscape

The agricultural biologicals testing market shows moderate concentration, because the five largest players together hold majority of global revenue, while many regional specialists fill local niches. Scale matters for regulatory expertise and capital investments, yet country-specific agronomy often rewards small firms that can turn reports around quickly and in local languages. Pricing power resides mainly with laboratories that combine GLP credentials with a global footprint, but clients still split work to keep competition alive. As a result, both multinational networks and agile independents capture profitable pockets of demand.

Eurofins Scientific leads with a major share and continues to grow through acquisitions such as Verdelab Bioscience, which added deep phytopathology skills in 2024. SGS SA is another prominent player in the industry and is further expanding its North American capacity and signing multi-year contracts with several crop-protection majors. Intertek put USD 18 million into European automation that pairs robotic handlers with artificial-intelligence analytics, while Bureau Veritas and ALS Limited have targeted soil microbiome and Asia-Pacific field services, respectively. These moves illustrate how capital spending and niche expertise both serve as effective growth levers.

Technology adoption remains the main battleground. Next-generation sequencing shortens microbial identification work, and automated high-throughput platforms shave weeks off efficacy trials. Cloud portals now give clients real-time study dashboards, which have quickly become a baseline expectation. White-space opportunities lie in RNA-based pesticides and complex microbial consortia that still lack standardized methods, so the first laboratories to master these assays will enjoy outsized pricing and early mover loyalty.

Agricultural Biologicals Testing Industry Leaders

Eurofins Scientific SE

SGS SA

Intertek Group plc

Bureau Veritas SA

ALS Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Intertek earmarked USD 18 million for laboratory automation across its European network, rolling out robotic handlers and artificial-intelligence analytics that raise daily sample throughput by nearly one-third.

- January 2025: i2LResearch Ltd., now part of Cawood, launched a secure digital portal that lets clients track study milestones and download regulatory documents in real time, matching new EU digital-passport data requirements.

- December 2024: Fera Science Ltd. opened an advanced containment unit for microbial pesticide trials, featuring climate-stress chambers that simulate extreme weather and support biosafety assessments for next-generation biopesticides.

- November 2024: BiocSol closed a EUR 5.2 million (approximately USD 5.6 million) seed round to accelerate microbial pesticide development, expand laboratory infrastructure, and scale up pilot production. The fresh capital provides the start-up with the room to hire additional microbiologists, validate lead strains under GLP conditions, and prepare its first regulatory submissions.

Global Agricultural Biologicals Testing Market Report Scope

Agricultural biologicals testing refers to various types of tests such as efficacy, toxicity, stability, and microbiological analyses that are conducted on agricultural biologicals like biofertilizers, biopesticides, and biostimulants. Agricultural biologicals comprise natural products developed particularly for crop production. The Agricultural Biologicals Testing Market is segmented by Product Type (Biopesticides, Biofertilizers, Biostimulants, and Other Product Types), Application (Field Support, Regulatory, Analytical, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Africa). The report offers the market size and forecast in value (USD) of the above-mentioned segments.

| Biopesticides |

| Biofertilizers |

| Biostimulants |

| Other Product Types |

| Field Support |

| Regulatory |

| Analytical |

| Other Applications |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Product Type | Biopesticides | |

| Biofertilizers | ||

| Biostimulants | ||

| Other Product Types | ||

| By Application | Field Support | |

| Regulatory | ||

| Analytical | ||

| Other Applications | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast revenue for agricultural biologicals testing in 2031?

The market is projected to reach USD 7.09 billion by 2031.

Which product segment drives the largest share of biologicals testing today?

Biopesticides lead with 43.62% of 2025 revenue.

Which application area is expanding most rapidly?

Analytical services are set to grow at an 17.44% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Stricter Chinese and Japanese protocols and India's organic surge lift regional testing demand at a 16.12% CAGR.

How are digital crop passports influencing laboratory demand?

They mandate blockchain-ready data and real-time access, increasing analytical workload and favoring automated labs.

Page last updated on: