Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

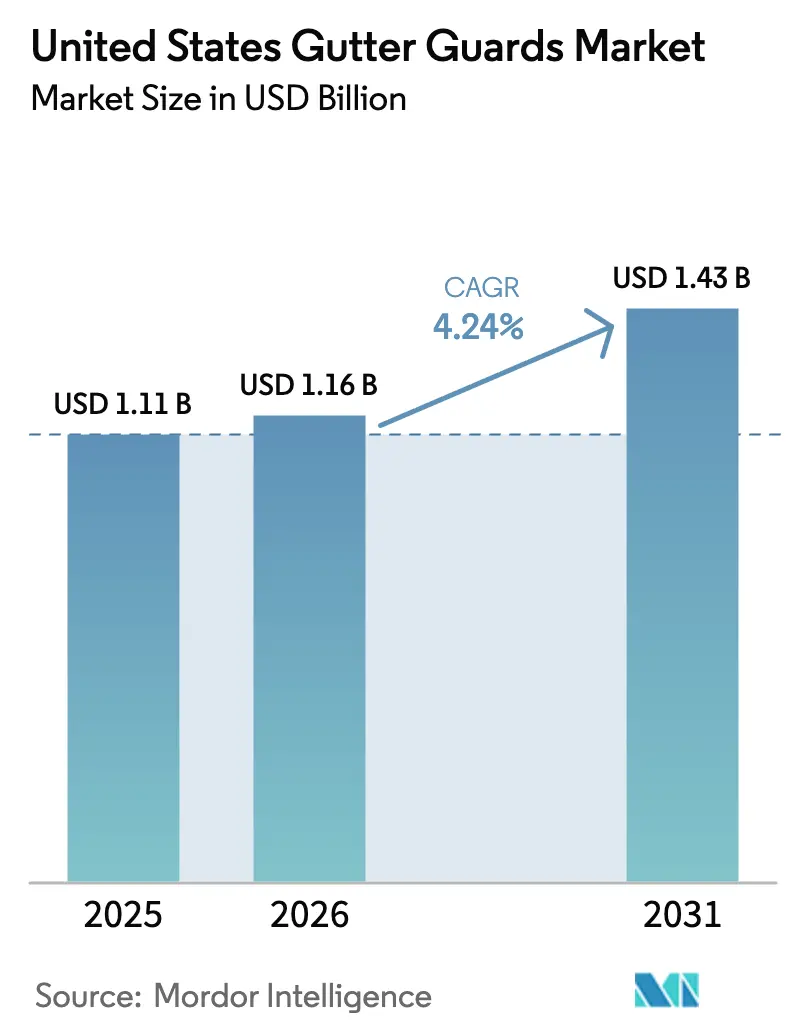

| Base Year Market Size (2025) | USD 1.11 Billion |

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

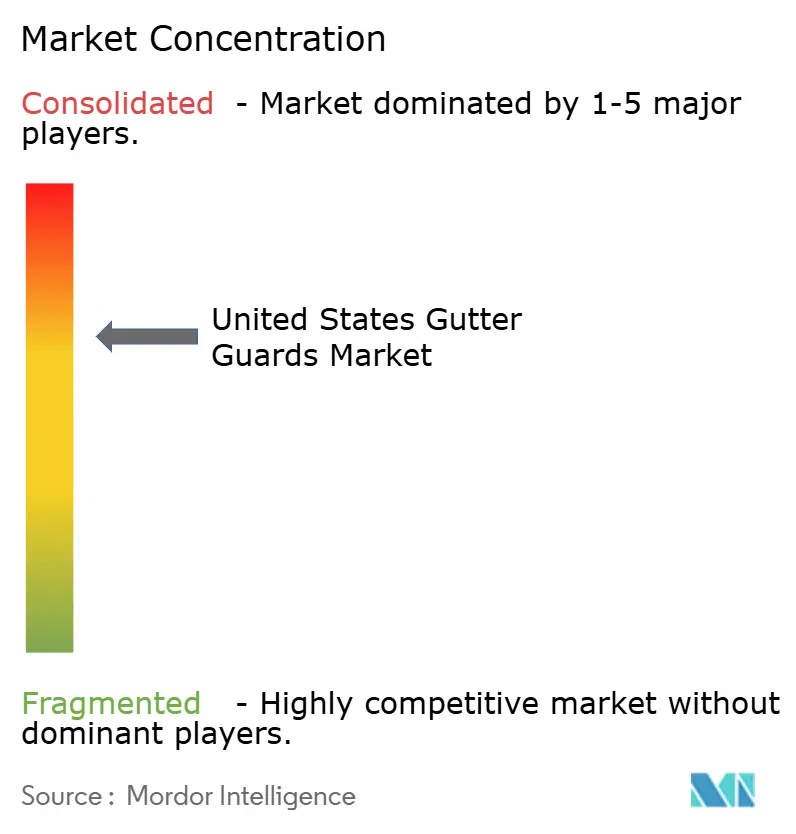

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Gutter Guards Market Analysis by Mordor Intelligence

The United States gutter guards market size was valued at USD 1.11 billion in 2025 and is estimated to grow from USD 1.16 billion in 2026 to reach USD 1.43 billion by 2031, at a CAGR of 4.24% during the forecast period (2026-2031). Aging residential infrastructure, with the median age of owner-occupied homes reaching 41 years and 48% of the stock built before 1980, keeps retrofit demand resilient as roofs and gutters reach replacement cycles alongside broader remodeling needs[1]Source: NAHB, "Almost Half of the Owner-Occupied Homes Built Before 1980", https://eyeonhousing.org/2025/04/almost-half-of-the-owner-occupied-homes-built-before-1980/. Intensifying precipitation patterns elevate the urgency of debris-resistant, high-capacity systems across regions exposed to heavy downpours and tropical systems, which steers homeowners and property managers toward premium solutions that improve flow and reduce overflow risk. Micro-mesh designs benefit from performance-oriented positioning and third-party certifications for water collection readiness, widening their appeal for homeowners seeking long-life products that integrate with sustainability upgrades. The tight labor environment, characterized by persistent shortages across construction trades, supports professional installation models even as it lifts labor costs and extends lead times. Elevated home improvement spending in 2026, supported by owners staying in place and investing in existing properties, sustains demand for bundled roof and gutter protection projects as part of a steady remodeling cycle.

Key Report Takeaways

- By product type, standard mesh and screens led with 41.23% of the United States gutter guards market share in 2025, while micro-mesh screens are the fastest growing at a 4.64% CAGR during 2026 to 2031.

- By material, aluminum held the largest revenue in 2025 at 51.82%, while stainless steel recorded the fastest expansion at a 4.98% CAGR during 2026 to 2031.

- By end user, residential accounted for 71.61% of the United States gutter guards market share in 2025, while commercial is advancing at a 5.12% CAGR from 2026 to 2031.

- By geography, the South held 34.84% of the United States gutter guards market share in 2025, while the West is projected to grow at a 5.34% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Gutter Guards Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing home-improvement and reroofing spending | +1.2% | Global, with early gains in lock-in-effect metros in the Northeast and Midwest, aging stock clusters | Medium term (2-4 years) |

| Rising frequency of extreme rainfall and hurricanes | +0.9% | Gulf Coast and Southeast Atlantic with spill-over to the Northeast | Short term (≤ 2 years) |

| Aging United States housing stock requiring retrofits | +0.8% | National, concentrated in the Rust Belt with older median home ages | Long term (≥ 4 years) |

| Growing popularity of micro-mesh premium systems | +0.7% | National, over-indexed in high-income coastal metros and wildfire-interface zones | Medium term (2-4 years) |

| Smart rain-harvesting integration with gutter guards | +0.5% | West, with spill-over to Texas and Arizona water-scarce metros | Long term (≥ 4 years) |

| Reshoring of aluminum screen manufacturing capacity | +0.3% | National, with production concentrated in the Midwest and the South | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Home-Improvement & Reroofing Spend

Home improvement expenditures are projected to reach USD 524 billion in early 2026, marking a record high despite a deceleration from 2024's 7% growth peak to an estimated 5% in 2025 and 3% in 2026, according to the Harvard Joint Center for Housing Studies' Leading Indicator of Remodeling Activity (LIRA)[2]Qualified Remodeler, "Remodeling Expected to Continue Slow but Steady Growth Into Next Year", https://www.qualifiedremodeler.com/remodeling-expected-to-continue-slow-but-steady-growth-into-next-year/. The lock-in effect around low-rate mortgages continues to favor remodeling over moving, which keeps roofing and related exterior projects on the shortlist for near-term investment, given their property value signaling and durability benefits. Within remodels that involve roofing, new roofs delivered the highest reported homeowner satisfaction, reinforcing the upsell path for guards as contractors bundle gutter protection with reroofing jobs to prevent clogs and overflow on new systems. This acceptance aligns with steady remodeling activity following pandemic-era re-benchmarking, which points to a larger and more durable base of spending than previously captured in cyclical indicators. The United States gutter guards market benefits from this pattern through increased attachment rates when installers have scaffolding and crews on site, reducing incremental install time and contributing to higher close rates on guard add-ons. As a result, reroofing remains a critical pathway to expand micro-mesh penetration and sustain an upgrade mix across the United States gutter guards market.

Rising Frequency of Extreme Rainfall & Hurricanes

Weather volatility is amplifying demand, as 2025 featured multiple billion-dollar severe storm disasters and sustained periods of heavy rainfall that tested roof drainage capacity across major metropolitan areas. Projections for rare extreme precipitation design values in the United States indicate higher intensity events under warming, which challenge legacy gutter systems and elevate the value of debris-resistant guards that preserve flow during downpours. Physical science indicates extreme precipitation tends to increase with atmospheric moisture content, with analyses and educational materials highlighting how a warmer climate can load more moisture and intensify short-duration rainfall. The 2025 Atlantic hurricane season, while producing only 13 named storms (below the 14.4 annual average), generated 132.4 units of Accumulated Cyclone Energy (ACE), 9% above the 1991-2020 baseline, and notably spawned three Category 5 hurricanes (Erin, Humberto, Melissa), the second-highest count on record behind 2005's four, per Colorado State University's Tropical Meteorology Project verification[3]CSU, "Seasonal Hurricane Forecasting", https://tropical.colostate.edu/forecasting.html. Insurance industry responses are materializing through wind-mitigation credits in Florida and Gulf Coast states, where homeowners installing debris-blocking gutter systems can qualify for 5-8% premium reductions on windstorm coverage, creating a financial incentive that offsets 15-20% of installation costs over a 10-year policy horizon, per Florida Office of Insurance Regulation disclosures.

Aging United States Housing Stock Requiring Retrofits

The median age of owner-occupied homes reached 41 years in 2023, and nearly half of the stock predates 1980, which directly correlates with the need for gutter replacement and bundled guard installation when roofs are replaced. As the share of newer homes declines and the older cohort expands, maintenance and replacement cycles intensify, pushing households to prioritize weatherproofing and drainage longevity in exterior upgrades. In this context, guard systems that promise long service life and reduce ladder work for cleaning earn higher consideration in neighborhoods where gutter systems have reached end-of-life. The remodeling channel remains the primary venue for these replacements, given the relatively small contribution of recent construction to total housing stock in the current decade. The United States gutter guards market, therefore, leans on retrofit workflows that align with roofing and exterior envelope projects, where guards present as a preventive measure that protects new gutters and preserves drainage performance. This retrofit focus also favors standardized SKUs and national installers that can scale across aging metros with reliable warranty and service support.

Smart Rain-Harvesting Integration with Gutter Guards

Rainwater harvesting is gaining traction as a recognized alternative water technology for public sector facilities, which strengthens the case for guards that double as first-stage filtration and keep debris out of storage systems. Certifications for potable water pre-filtration on micro-mesh products support adoption in drought-prone regions and help projects meet building performance or program compliance goals that reward efficient water management. New products that decouple storage sites from downspout locations through engineered inserts create flexible layouts, enabling near-full roof capture and improving economics for properties that pair guards with harvesting hardware. Public-sector guidance complements these product advances by clarifying metering, control, and monitoring features, which pave a path for specifying sensor-enabled solutions in buildings with compliance reporting needs. These integrations expand the addressable use cases beyond leaf control toward multi-function systems, a trend that is most visible in Western states yet increasingly relevant nationally. The United States gutter guards market benefits from these adjacent use cases as rainwater collection projects turn guards into enabling technology for conservation-driven retrofits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installed cost versus DIY cleaning | -0.5% | National, amplified in price-sensitive Sun Belt metros | Short term (≤ 2 years) |

| Seasonal labor shortages in skilled installers | -0.4% | National, acute in the Northeast and Midwest winter months, and post-hurricane Gulf Coast demand surges | Medium term (2-4 years) |

| Roof-warranty conflict concerns | -0.2% | National, concentrated in new-construction markets with builder warranties | Short term (≤ 2 years) |

| Emerging self-cleaning gutter-less roof alternatives | -0.1% | West, early adoption in architectural design segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installed Cost Versus DIY Cleaning

Premium micro-mesh systems compete with low-cost DIY guards and intermittent professional cleanings, which makes the initial outlay a barrier for price-sensitive households. Big-box retailers offer aluminum and stainless mesh options in contractor-grade packs, and those options reinforce the visible price gap that budget-conscious buyers weigh against longevity and maintenance savings. Households in older homes often face added costs for gutter replacement or fascia repair before guards can be installed, which increases the all-in ticket and forces sequencing decisions with other age-related projects. In commercial properties, longer rooflines and access requirements can add labor hours and safety controls, which further push installed costs into budget approval discussions. Clear performance warranties and independent validation for filtration and water-capture roles help address value questions, yet the payback narrative still depends on maintenance avoidance and risk reduction rather than short-term savings. These considerations can slow conversion in cohorts that prioritize near-term cash flow, which creates a persistent headwind for the United States gutter guards market even as premium adoption grows.

Seasonal Labor Shortages in Skilled Installers

Construction employers report persistent difficulty filling craft roles, a constraint that reduces capacity during peak spring and fall installation periods and extends homeowner wait times. Firms also cite staffing constraints as a leading cause of project delays, with survey work highlighting how immigration enforcement and aging trade demographics compound seasonal bottlenecks in local labor pools. The sector faces an older workforce profile and insufficient young entrants to offset retirements, which keeps wage pressure elevated and fosters backlogs during high-demand windows. Regional surges after severe weather events further tighten capacity in affected states, pulling crews from neighboring regions and raising mobilization costs that squeeze discretionary projects in the queue. Many installers respond by prioritizing larger, higher-margin projects or integrated roof-and-guard replacements, which can defer smaller guard-only jobs. These dynamics temper near-term growth for the United States gutter guards market in months when installation capacity is fully subscribed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Micro-Mesh Ascendancy Reshapes Value Ladder

Standard mesh and screens commanded 41.23% of the United States gutter guards market share in 2025, reflecting contractor familiarity and price accessibility for cost-driven projects that prioritize basic debris control. Integrated one-piece systems are gaining traction in new builds and whole-home exterior upgrades because they reduce retrofit complexity and come with lifetime warranties, which positions them as a premium alternative for owners who want a single-brand solution. In parallel, surface-tension covers, and foam or brush inserts retain a role in budget-conscious and DIY projects, yet their replacement cycles and performance constraints are balanced against lower upfront cost expectations. As roofers and remodelers standardize guard upsells when scaffolding is already in place, adoption spreads across more price points, which further supports the premium mix within the United States gutter guards market.

Performance credentials and brand positioning are differentiating growth within product types, as micro-mesh suppliers market durability and third-party validations to bolster trust in long-term clog prevention. Product pedigrees that include awards and lab-tested resilience help reduce skepticism among homeowners who previously deferred purchase or relied on periodic cleanings. Builders and remodelers also look for options that avoid roof warranty conflicts, favoring designs that mount to gutters or fascia without disturbing shingles or roof decking in markets where builder warranties remain active. The channel is adapting with national installers that cross-sell guards in roofing and exterior envelope projects, reinforced by private providers that expand geographic reach and unify product and install under one service umbrella. These shifts concentrate visibility around proven designs and integrated installation networks, a pattern that continues to influence product mix and margins across the United States gutter guards market.

By Material: Stainless Steel Commands Premium, Aluminum Dominates Volume

Aluminum accounted for 51.82% of the category in 2025, sustained by a favorable cost-to-durability ratio and broad compatibility with standard fabrication methods used in residential and light commercial installations. Stainless steel is outpacing the baseline at a 4.98% CAGR from 2026 to 2031 as buyers favor corrosion resistance and lower maintenance in coastal and high-precipitation regions, which supports willingness to pay for longer service life in premium micro-mesh designs. Surgical-grade (304 marine-grade) and premium (316) stainless steel mesh options, used by HomeCraft, LeafFilter, and MasterShield, offer 50+ year performance warranties that justify installed costs of USD 15.68-USD 16.80 per linear foot, with contractors reporting zero callback rates for mesh failures versus 5-8% callback incidence for vinyl screen cracking in freeze-thaw cycles[4]This Old House, "Best Gutter Guards for Metal Roofs (2026)", https://www.thisoldhouse.com/gutters/best-gutter-guards-for-metal-roofs. Vinyl and plastic options remain present in the DIY channel, where low entry cost attracts price-first buyers, though replacement intervals are typically shorter than aluminum or stainless alternatives, given exposure to UV and freeze-thaw conditions. Copper retains a specialized role in historic restorations and high-end projects that value a uniform aesthetic and extreme longevity despite higher installed cost and limited availability.

Domestic investment in aluminum rolling and recycling adds resilience to the supply base that serves building products, which benefits frame and screen manufacturers that prefer local sourcing over imported coil. Construction of a large integrated rolling mill and recycling center in Alabama reinforces North American capacity with a timeline aligned to current planning horizons for building product makers. Specification trends also link materials to broader project objectives, with customers requesting certifications and recycled content where possible in institutional and commercial bids. For material suppliers, these dynamics favor aluminum and stainless formats that align with durability, water capture compatibility, and fire safety considerations. As a result, the United States gutter guards market continues to bifurcate into volume aluminum solutions and premium stainless mesh systems, each serving distinct value propositions and budgets.

By End User: Residential Dominance Masks Commercial Upside

The residential segment accounted for 71.61% in 2025, reflecting the size of the single-family housing base and the established practice of bundling guards during reroofing or exterior refresh projects that address aging fascia and drainage systems. Renovation planning increasingly weighs the satisfaction and resale impact of roofing projects, which keeps guard upgrades in scope as homeowners prioritize low-maintenance exterior profiles and safety from ladder work. The United States gutter guards market benefits from the lock-in effect as owners remain in place longer and invest in capital improvements that protect the building envelope and reduce recurring service calls. Installers report that guard attachments are more likely to be accepted when combined with roof shingles or gutter replacement, which reduces incremental mobilization time. Warranty-backed products and familiar brands reinforce homeowner confidence, which aids conversion in regions with higher precipitation and leaf loads.

Commercial applications are expanding at a faster pace, with the United States gutter guards market size for commercial installations projected to advance at a 5.12% CAGR from 2026 to 2031 as property managers pursue longer service intervals and liability reduction for paved areas and entrances. Industrial and institutional sites often require heavier gauge guards for wide runs and snow loads, which pushes material choices toward aluminum and stainless systems designed for box profiles and commercial-grade attachment. Procurement norms also matter, as government and education facilities increasingly specify features related to water capture, filtration, and monitoring, which expands the role of guards in integrated sustainability projects. These commercial use cases favor suppliers that can meet bonding, insurance, and safety requirements while delivering nationwide service coverage. Taken together, the residential base sustains volume while commercial demand contributes incremental growth and product differentiation across the United States gutter guards market.

Geography Analysis

The South accounted for 34.84% of the United States gutter guards market share in 2025, powered by exposure to tropical systems and severe thunderstorm complexes that load gutters with wind-driven debris and heavy rain. States along the Gulf and Southeast Atlantic face repeated roof drainage stress during peak storm periods, which accelerates specification of higher-capacity guard formats and professional installation. Even in seasons with fewer landfalls, severe weather drove numerous billion-dollar events in 2025, reinforcing demand for preventative exterior upgrades that stabilize building performance during peak rainfall. Insurers and local building communities emphasize maintenance of roof drainage to reduce water intrusion risk, which keeps guards visible within broader mitigation conversations. These factors support steady adoption in the region and a strong role for national installers that can scale capacity during post-storm recovery windows across the United States gutter guards market.

The West is the fastest-growing region, with the United States gutter guards market size for the West projected to expand at a 5.34% CAGR during 2026 to 2031, propelled by wildfire interface requirements in designated zones, intense Pacific Northwest rainfall patterns, and high-growth metros in Arizona and Nevada, where builders standardize exterior protection early. Project teams increasingly consider ember resistance, non-combustibility, and debris exclusion from downspouts given local conditions, which pushes choices toward steel and aluminum mesh formats that offer fire-safe profiles. Water conservation goals add another layer, where micro-mesh systems with potable water pre-filtration certifications integrate into rainwater harvesting designs for irrigation or non-potable uses. Public sector technical guidance for rain capture clarifies monitoring and control expectations in new projects, which encourages planning that pairs guards with capture hardware in retrofits and new builds. These overlapping needs create a favorable setting for premium guard adoption and for solution providers that can address code-related requirements across the United States gutter guards market.

The Midwest and Northeast reflect older housing stocks and distinct climate pressures that elevate the utility of durable, snow and ice-compatible solutions. Older rooflines in many metros bring gutter replacement into scope alongside guard installation, aligning work with roofing projects to minimize separate mobilization and ladder exposure. The Northeast experiences the steepest increases in heavy precipitation on the heaviest rain days over multi-decade periods, a pattern that contributes to overflow episodes and encourages more effective debris control in built-up tree canopies. In the Midwest, snow and freeze-thaw cycles add weight and icing considerations, which shape demand for robust attachments and materials suited to low temperatures. These regional variations call for material and design choices aligned with climate realities while sustaining steady retrofit volumes across older housing corridors of the United States gutter guards market.

Competitive Landscape

The market features national installers with recognizable brands alongside specialized manufacturers and regional contractors, a structure that balances scale in procurement and marketing with local expertise and service. Integration strategies have accelerated, with large direct-to-consumer groups adding adjacent services and expanding footprints to increase customer lifetime value and cross-selling potential across exterior and interior categories. A notable portfolio combination expanded capabilities in roofing, gutter protection, and other home services, positioning the combined organization to serve homeowners from structural to finish upgrades with unified branding and support. Network expansion and shared back-office functions also heighten reach for legacy one-piece systems that align product and installation in a single offering. This environment supports multi-brand portfolios and reinforces differentiated models within the United States gutter guards market.

Sales infrastructure is an additional competitive lever as firms modernize lead management and contact strategies to handle seasonal spikes and expansion into new metros. One provider reported material improvements in conversion and revenue per call after upgrading to a new dialing and workflow platform, which exemplifies how sales process optimization can generate share gains in regions with tight advertising markets. Product innovation intersects with sustainability, too, where engineered inserts enable more flexible rain capture without downspout constraints and align with public sector water efficiency objectives. In commercial and industrial settings, suppliers with deeper assortments for large box gutters and heavy loading conditions hold an advantage because they can meet specifications for wide runs and access-limited sites. The capability to deliver at scale under binding warranties remains central to differentiation across the United States gutter guards market.

Specification guidance and warranty alignment matter for winning bids with homeowners and builders that seek clarity on roof warranty compatibility. Systems that attach without disturbing shingles or roof decking address a common concern about voiding coverage and improve acceptance in new construction, or recent reroofs where builder warranties remain in effect. Brand stories that emphasize durability, testing, and recognized design can reduce purchase hesitation as households weigh preventive investment in drainage against competing exterior priorities. For fabricators, domestic rolling capacity expansions add resilience to aluminum supply used in frames and screens, which supports service levels and delivery reliability for large projects. With these vectors in play, the United States gutter guards market rewards firms that combine credible product claims, installation consistency, and robust customer support.

United States Gutter Guards Industry Leaders

-

Leaf Guard

-

All American Gutter Protection

-

Gutter Guards America

-

LeafFilter North, Inc.

-

HomeCraft Gutter Protection

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: LeafFilter Gutter Protection, a division of Leaf Home, was named a winner in the 2026 Good Housekeeping Home Reno Awards for its next-generation gutter protection system engineered to fit nearly every gutter style, including oversized commercial gutters and specialty half-round residential systems.

- October 2025: LeafFilter Gutter Protection partnered with professional contractor and HGTV personality Mike Holmes to promote year-round home maintenance and protection through educational content across digital channels.

- September 2025: Leaf Home completed the acquisition of Erie Home, positioning the company as one of the largest direct-to-consumer residential services providers in North America with an expanded portfolio spanning roofing, gutter protection, and other home services.

- October 2025: HomeCraft Gutter Protection reported significant increases in conversion and revenue, along with expanded call capacity after implementing Convoso’s dialing platform, supporting rapid growth across multiple states.

United States Gutter Guards Market Report Scope

By Product Type

| Micro-Mesh Screens |

| Standard Mesh & Screens |

| Reverse-Curve / Surface-Tension Covers |

| Brush / Bristle Inserts |

| Foam Inserts |

| Integrated Seamless Gutter-Guard Systems |

By Material

| Aluminum |

| Stainless Steel |

| Vinyl / Plastic |

| Others (Foam,Copper) |

By End User

| Residential |

| Commercial |

| Industrial & Institutional |

By Region

| Northeast |

| Midwest |

| Southeast |

| Southwest |

| West |

| By Product Type | Micro-Mesh Screens |

| Standard Mesh & Screens | |

| Reverse-Curve / Surface-Tension Covers | |

| Brush / Bristle Inserts | |

| Foam Inserts | |

| Integrated Seamless Gutter-Guard Systems | |

| By Material | Aluminum |

| Stainless Steel | |

| Vinyl / Plastic | |

| Others (Foam,Copper) | |

| By End User | Residential |

| Commercial | |

| Industrial & Institutional | |

| By Region | Northeast |

| Midwest | |

| Southeast | |

| Southwest | |

| West |

Key Questions Answered in the Report

What is the current size and growth outlook for the United States gutter guards market?

The United States gutter guards market size is USD 1.16 billion in 2026, and it is projected to reach USD 1.43 billion by 2031 at a 4.24% CAGR.

Which product types are leading and growing fastest in the United States gutter guards market?

Standard mesh and screens lead with 41.23% share in 2025, while micro-mesh screens are the fastest growing at a 4.64% CAGR during 2026 to 2031.

Which materials and end users drive demand in the United States gutter guards market?

Aluminum leads by revenue with 51.82% share in 2025, stainless steel grows fastest at a 4.98% CAGR, and residential accounts for 71.61% share in 2025, while commercial grows at a 5.12% CAGR through 2031.

What regional trends matter most for the United States gutter guards market?

The South holds a 34.84% share in 2025 driven by severe weather exposure, and the West is the fastest growing region at a 5.34% CAGR through 2031 as wildfire interface needs and water capture projects raise adoption.

How do weather and remodeling trends support the United States gutter guards market?

Heavy rain events and tropical systems elevate overflow risks, while steady remodeling spend and reroofing projects increase guard attachment rates in retrofit workflows.

What factors can restrain adoption in the United States gutter guards market?

High upfront installed cost relative to DIY options and seasonal labor shortages that extend lead times can slow near-term demand even as long-term preventive value remains strong.

Page last updated on: